the source for maritime information and...

TRANSCRIPT

Copyright © 2009 IHS Global Insight. All Rights Reserved.

The Source for Maritime Information and Insight

Copyright © 2008 IHS Inc. All Rights Reserved. 1

A Greener Shade of Blue

Christopher Pålsson

Director

IHS Fairplay

Copyright © 2009 IHS Global Insight. All Rights Reserved.

20 minutes of What’s

•What’s

• Going On?

• Possible?

• Going to Happen?

Copyright © 2009 IHS Global Insight. All Rights Reserved.

WHAT’S GOING ON?

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Intense Activity

37.5

38

38.5

39

39.5

40

40.5

41

41.5

42

42.5

-80 -75 -70 -65 -60 -55

New York

Baltimore

Philadelphia

Richmond

Boston

20

25

30

35

40

45

50

-85 -80 -75 -70 -65 -60 -55 -50 -45 -40

Miami

Richmond

New York

Palm Beach

Charleston

Savannah

Baltimore

Portland

Wilmington

Bar Harbor

Copyright © 2009 IHS Global Insight. All Rights Reserved.

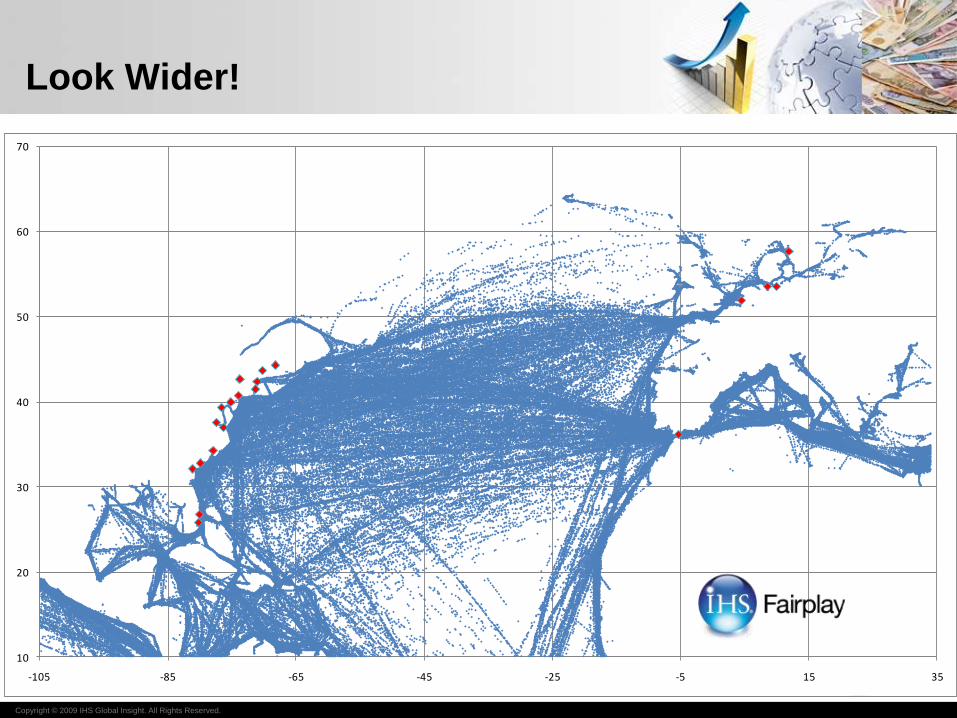

Look Wider!

10

20

30

40

50

60

70

-105 -85 -65 -45 -25 -5 15 35

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Follow the Supply Chain

-70

-50

-30

-10

10

30

50

70

-180 -130 -80 -30 20 70 120 170

Copyright © 2009 IHS Global Insight. All Rights Reserved.

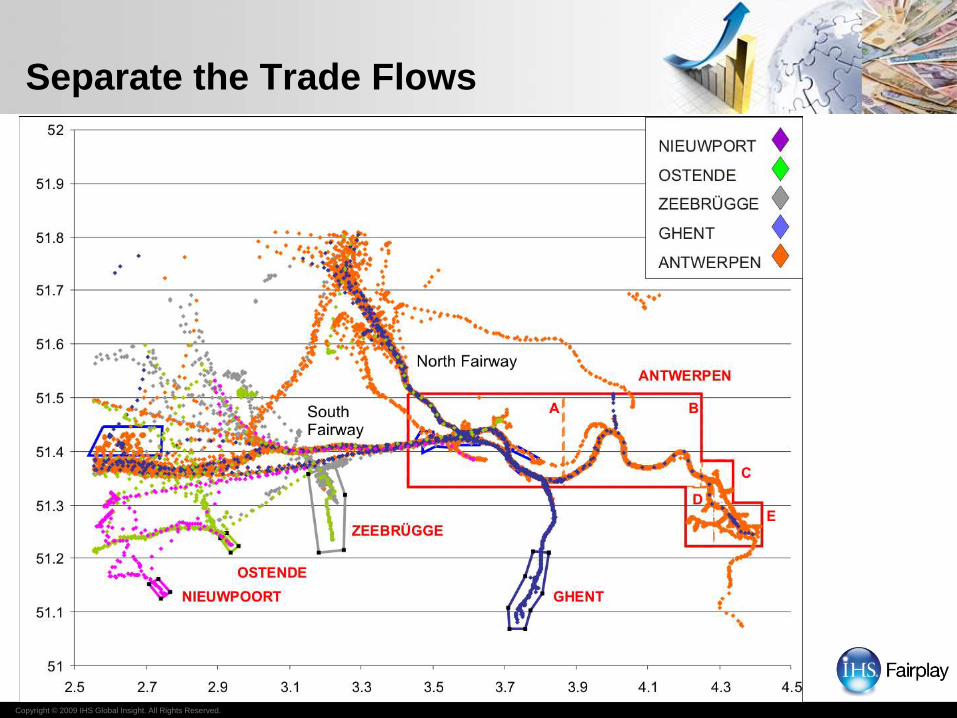

Separate the Trade Flows

Copyright © 2009 IHS Global Insight. All Rights Reserved.

..or just a single vessel

Brovig Wind, IMO 9327281, 2009-07-29 00:59 - 2009-08-15 02:07

25

27

29

31

33

35

37

39

41

43

45

-15 -13 -11 -9 -7 -5 -3 -1 1 3 5

BROVIG WIND

Ports

Laayoune, 2009-08-05 12:58 - 2009-08-07 10:55

Lisbon

Agadir

Algeciras

Cartagena

Algiers

Barcelona

Santander Bilbao

Ceuta

Tan tan

Copyright © 2009 IHS Global Insight. All Rights Reserved.

WHAT’S POSSIBLE?

Copyright © 2009 IHS Global Insight. All Rights Reserved.

For Each Vessel;

IMO no

Long

Lat

Time

IMO no

Long

Lat

Time +X minutes

Calculate:

• Distance

• Average speed

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Traffic data AIS-Live

Vessel data Reg of Ships

Engine emission

characteristics

database

IMO No

Engine

designation

Emissions

calculations

Output of

results

Emissions Model

Copyright © 2009 IHS Global Insight. All Rights Reserved.

The speed determines the power outtake

0

Knots

Pro

puls

ion fuel consum

ption tonsfu

el/day Cruise speed level

Port approach level

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Actual effect could

differ substantially.

GT vis-à-vis ME power (kW)Example: Bulk carriers

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Add Sulphur

ME1.5%

AE0.1%

Copyright © 2009 IHS Global Insight. All Rights Reserved.

A Touch of Abatementwhere appropriate

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Slow Steam

Present the results

Copyright © 2009 IHS Global Insight. All Rights Reserved.

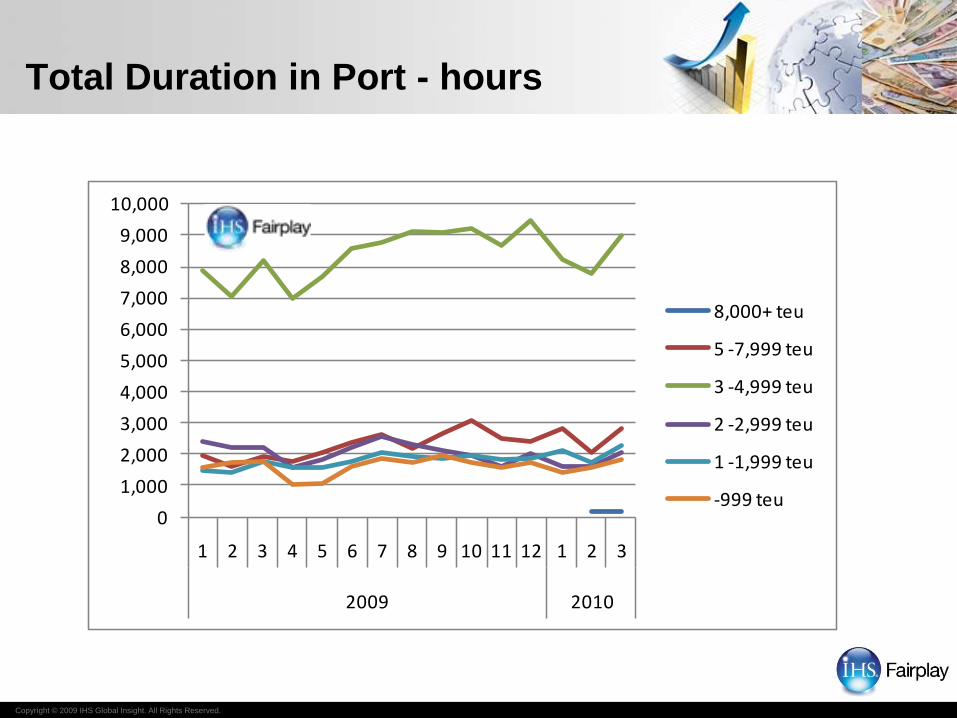

Total Duration in Port - hours

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3

2009 2010

8,000+ teu

5 -7,999 teu

3 -4,999 teu

2 -2,999 teu

1 -1,999 teu

-999 teu

Copyright © 2009 IHS Global Insight. All Rights Reserved.

TEU Capacity of ”Calling” Vessels

0

500

1,000

1,500

2,000

2,500

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3

2009 2010

8,000+ teu

5 -7,999 teu

3 -4,999 teu

2 -2,999 teu

1 -1,999 teu

-999 teu

Copyright © 2009 IHS Global Insight. All Rights Reserved.

CO2 while @ Berth

0

1

2

3

4

5

6

7

8

9

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3

2009 2010

-999 teu

1 -1,999 teu

2 -2,999 teu

3 -4,999 teu

5 -7,999 teu

8,000+ teu

Copyright © 2009 IHS Global Insight. All Rights Reserved.

WHAT’S

GOING TO

HAPPEN?

Que?

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Global Scenarios to 2030

•Global Redesign (Planning case)

• Rebalanced production & consumption between

regions.

• Global growth propelled by Emerging Markets.

• Growing tension over nuclear weapons proliferation.

• Non-fossil fuels increase market share.

• Energy demand shift away from OECD.

• OECD oil demand has peaked.

• Continued resource nationalism.

• Oil loses monopoly in transportation sector.

• Successful GHG emissions agreement in latter part.

www.ihsglobalscenarios.com

Vortex

• Boom

• Bust

• Lost Decade

Vortex

• Boom

• Bust

• Lost Decade

Metamorphosis

• Non-fossil fuel focus

• Battery innovation

© 2009, Cambridge Energy Research Associates, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

4

IHS_CERA_Template_MMDD09

Source: IHS Cambridge Energy Research Associates.

####

Copyright © 2009 IHS Global Insight. All Rights Reserved.

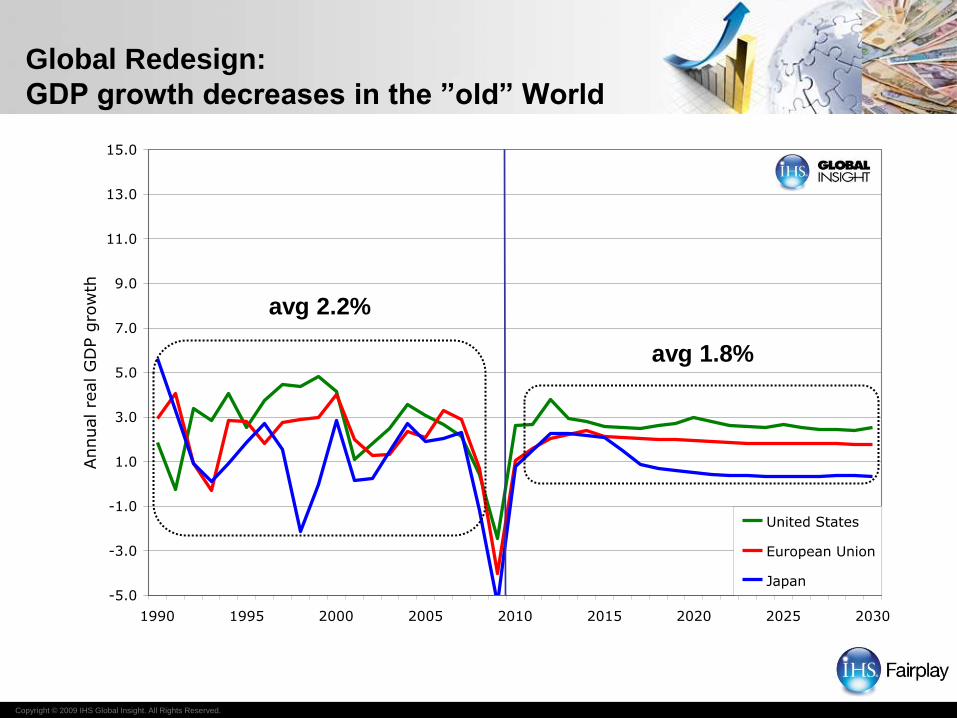

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

11.0

13.0

15.0

1990 1995 2000 2005 2010 2015 2020 2025 2030

Annual re

al G

DP g

row

th

United States

European Union

Japan

Global Redesign:

GDP growth decreases in the ”old” World

avg 1.8%

avg 2.2%

Copyright © 2009 IHS Global Insight. All Rights Reserved.

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

11.0

13.0

15.0

1990 1995 2000 2005 2010 2015 2020 2025 2030

Annual re

al G

DP g

row

th

China

India

Brazil

Global Redesign:

GDP growth decreases in the ”new” World

avg 5.9%

avg 6.3%

Copyright © 2009 IHS Global Insight. All Rights Reserved.

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

11.0

13.0

15.0

1990 1995 2000 2005 2010 2015 2020 2025 2030

Annual re

al G

DP g

row

th

World

Global Redesign:

but GDP growth increases in the total World

avg 3.5%avg 2.9%

Copyright © 2009 IHS Global Insight. All Rights Reserved.

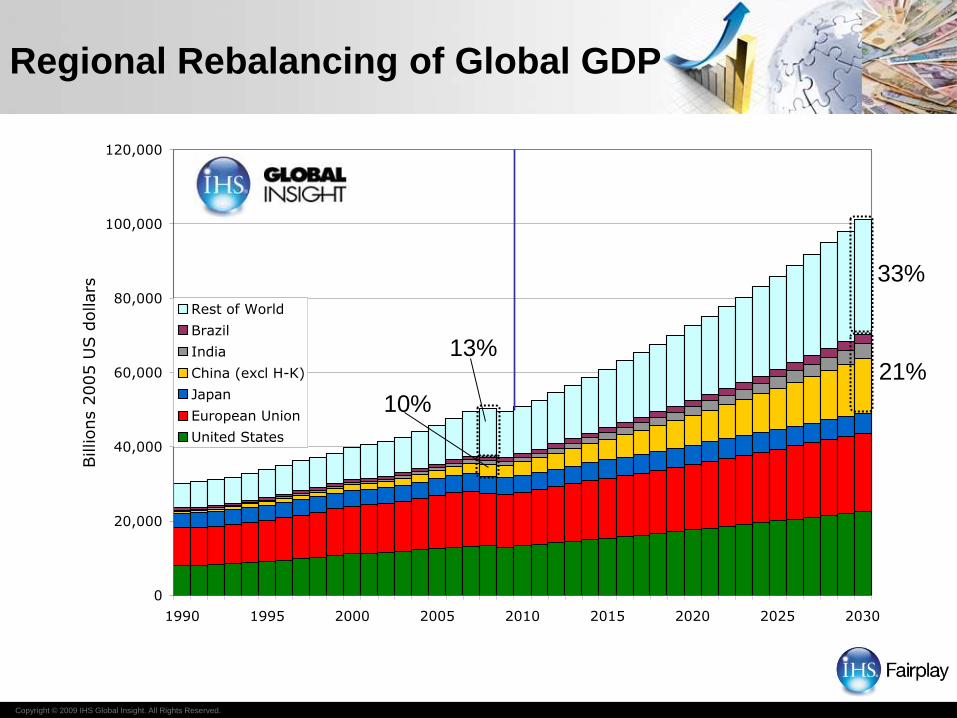

Regional Rebalancing of Global GDP

0

20,000

40,000

60,000

80,000

100,000

120,000

1990 1995 2000 2005 2010 2015 2020 2025 2030

Billions 2

005 U

S d

ollars

Rest of World

Brazil

India

China (excl H-K)

Japan

European Union

United States

21%

10%

13%

33%

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Global Redesign:

rebalance of World Exports, tonnes.

5

10

15

20

25

2000 2005 2010 2015 2020 2025 2030

Export

s.

Billion t

onnes.

Rest of World

Brazil

India

China (excl H-K)

Japan

European Union

United States

19%

10%

56%

54%

Trade decreased 7% in 2009.

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Global Redesign:

N America Containerized Imports

5

10

15

20

25

30

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

S America

N America

Middle East

Europe

C America

Africa & RoW

AustralAsia

Asia other

Asia FE

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Capacity Delivery; More of Everything

0

2

4

6

8

10

12

14

16

18

20

1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012

Co

nta

ine

r fl

ee

t, m

illio

n te

u, 1

97

6-

-999 teu 1 -1,999 teu 2 -2,999 teu 3 -4,999 teu 5 -7,999 teu 8,000+ teu2010-05

Forecast

Copyright © 2009 IHS Global Insight. All Rights Reserved.

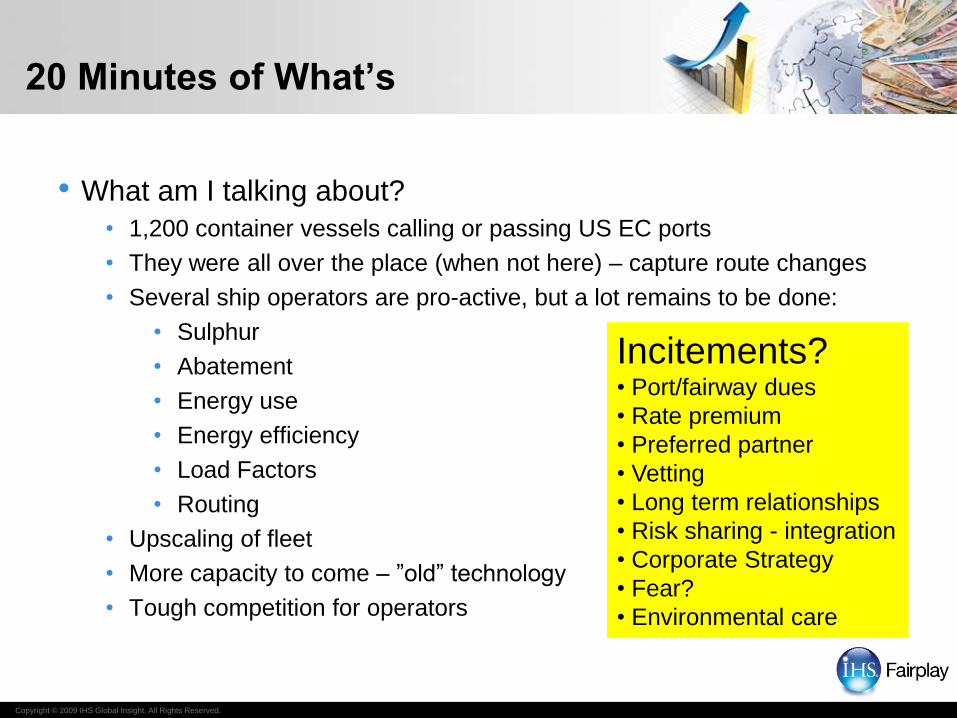

20 Minutes of What’s

• What am I talking about?

• 1,200 container vessels calling or passing US EC ports

• They were all over the place (when not here) – capture route changes

• Several ship operators are pro-active, but a lot remains to be done:

• Sulphur

• Abatement

• Energy use

• Energy efficiency

• Load Factors

• Routing

• Upscaling of fleet

• More capacity to come – ”old” technology

• Tough competition for operators

Incitements?• Port/fairway dues

• Rate premium

• Preferred partner

• Vetting

• Long term relationships

• Risk sharing - integration

• Corporate Strategy

• Fear?

• Environmental care

A Greener Shade of Blue“…and the truth is plain to see”

Thank you

Thanks to Procul

Harum, ”A whiter shade

of pale” for inspiration.

“…I was feeling kinda seasick”

Copyright © 2009 IHS Global Insight. All Rights Reserved.

The Source for Maritime Information and Insight

Copyright © 2008 IHS Inc. All Rights Reserved. 32