the state of halal food industry in the oic member …

TRANSCRIPT

THE HALAL FOOD INDUSTRY IN OIC MEMBER COUNTRIES

Challenges and Opportunities

Mazhar Hussain S e n i o r R e s e a r c h e r

OIC Stakeholders Forum on Halal Food Standards and Procedures 9-10 December 2015

Outline Growing Interest in Halal Key Markets, Key Facts Enhancing Cooperation in Halal Food among OIC Countries

Halal Food Standards and Certification

Halal Food Authentication The Potential of Islamic Finance for Halal Industry

Challenges and Opportunities

Recommendations and Outlook

0102030405060708090

100

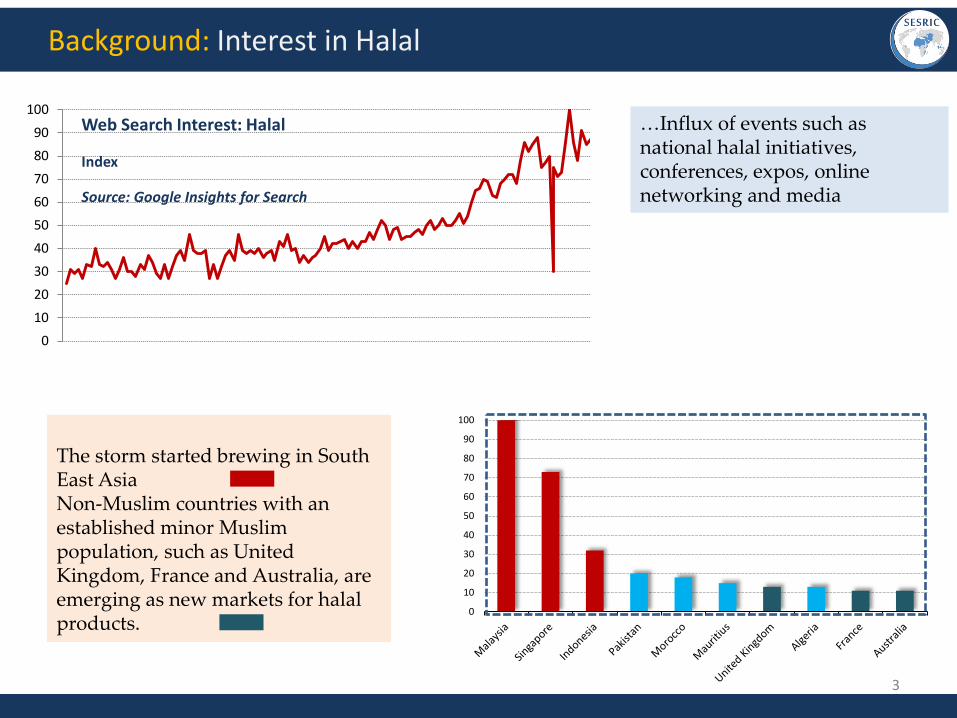

Background: Interest in Halal

…Influx of events such as national halal initiatives, conferences, expos, online networking and media

Web Search Interest: Halal

Index

Source: Google Insights for Search

0

10

20

30

40

50

60

70

80

90

100 The storm started brewing in South East Asia Non-Muslim countries with an established minor Muslim population, such as United Kingdom, France and Australia, are emerging as new markets for halal products.

3

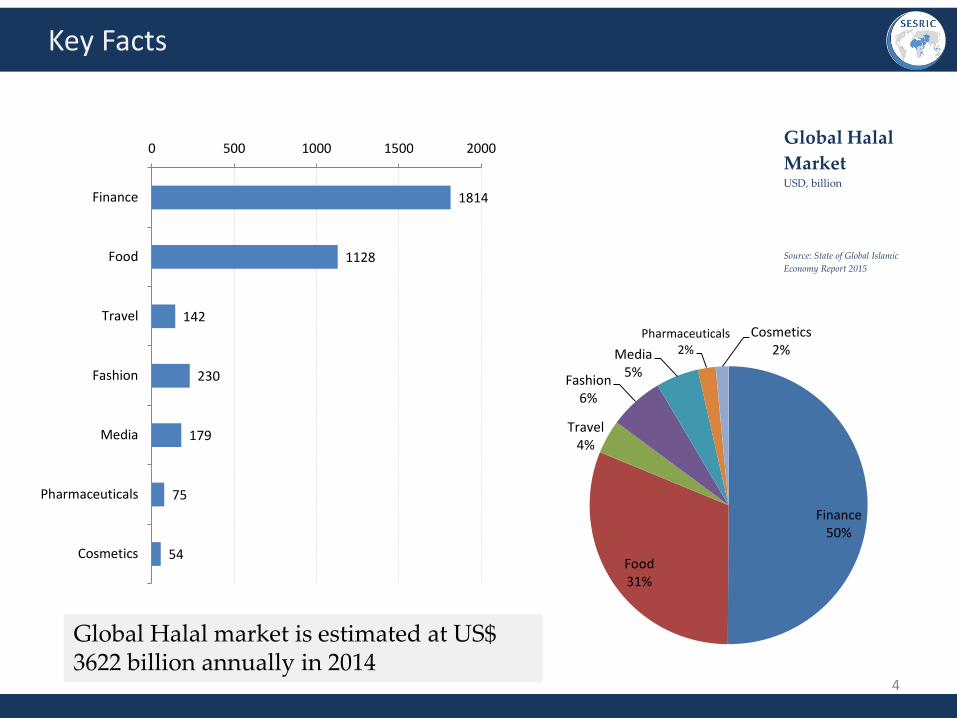

Global Halal Market USD, billion Source: State of Global Islamic Economy Report 2015

Key Facts

4

1814

1128

142

230

179

75

54

0 500 1000 1500 2000

Finance

Food

Travel

Fashion

Media

Pharmaceuticals

Cosmetics

Finance 50%

Food 31%

Travel 4%

Fashion 6%

Media 5%

Pharmaceuticals 2%

Cosmetics 2%

Global Halal market is estimated at US$ 3622 billion annually in 2014

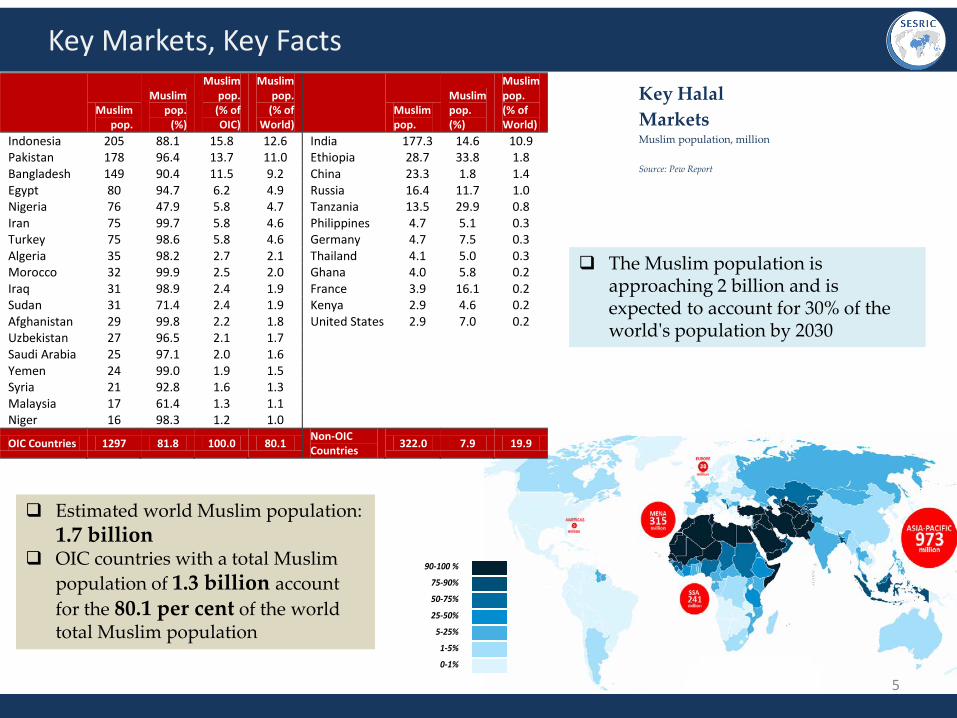

Key Halal Markets Muslim population, million

Source: Pew Report

Muslim pop.

Muslim pop.

(%)

Muslim pop.

(% of OIC)

Muslim pop.

(% of World)

Muslim pop.

Muslim pop. (%)

Muslim pop. (% of World)

Indonesia 205 88.1 15.8 12.6 India 177.3 14.6 10.9 Pakistan 178 96.4 13.7 11.0 Ethiopia 28.7 33.8 1.8 Bangladesh 149 90.4 11.5 9.2 China 23.3 1.8 1.4 Egypt 80 94.7 6.2 4.9 Russia 16.4 11.7 1.0 Nigeria 76 47.9 5.8 4.7 Tanzania 13.5 29.9 0.8 Iran 75 99.7 5.8 4.6 Philippines 4.7 5.1 0.3 Turkey 75 98.6 5.8 4.6 Germany 4.7 7.5 0.3 Algeria 35 98.2 2.7 2.1 Thailand 4.1 5.0 0.3 Morocco 32 99.9 2.5 2.0 Ghana 4.0 5.8 0.2 Iraq 31 98.9 2.4 1.9 France 3.9 16.1 0.2 Sudan 31 71.4 2.4 1.9 Kenya 2.9 4.6 0.2 Afghanistan 29 99.8 2.2 1.8 United States 2.9 7.0 0.2 Uzbekistan 27 96.5 2.1 1.7 Saudi Arabia 25 97.1 2.0 1.6 Yemen 24 99.0 1.9 1.5

Syria 21 92.8 1.6 1.3 Malaysia 17 61.4 1.3 1.1 Niger 16 98.3 1.2 1.0 OIC Countries 1297 81.8 100.0 80.1 Non-OIC Countries 322.0 7.9 19.9

Key Markets, Key Facts

90-100 % 75-90% 50-75% 25-50%

5-25% 1-5% 0-1%

Estimated world Muslim population: 1.7 billion

OIC countries with a total Muslim population of 1.3 billion account for the 80.1 per cent of the world total Muslim population

The Muslim population is approaching 2 billion and is expected to account for 30% of the world's population by 2030

5

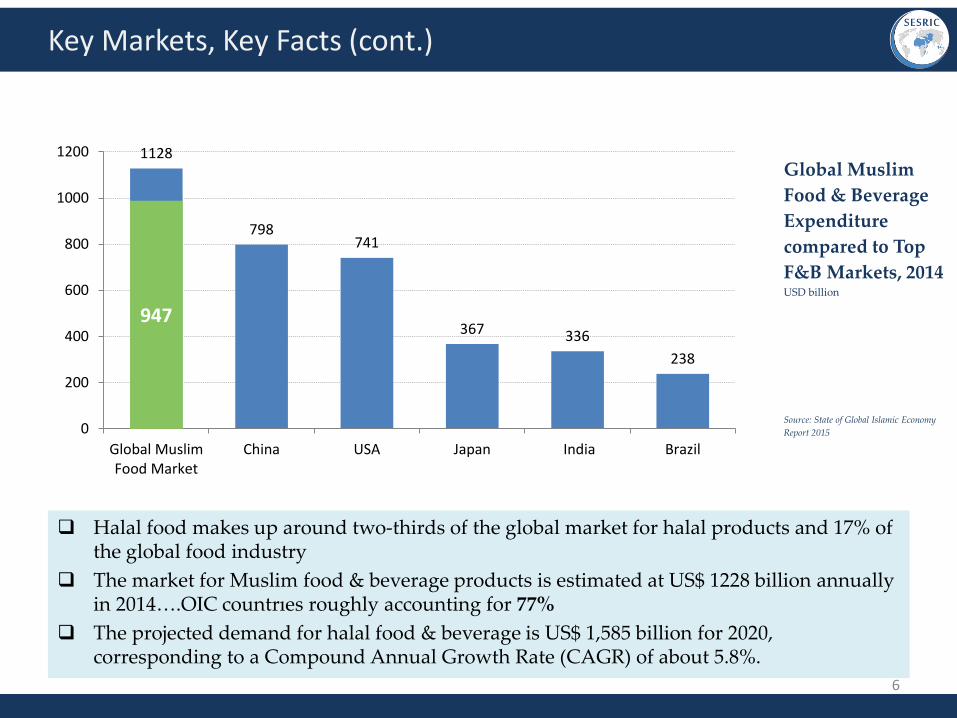

Global Muslim Food & Beverage Expenditure compared to Top F&B Markets, 2014 USD billion

Source: State of Global Islamic Economy Report 2015

Key Markets, Key Facts (cont.)

Halal food makes up around two-thirds of the global market for halal products and 17% of the global food industry

The market for Muslim food & beverage products is estimated at US$ 1228 billion annually in 2014….OIC countrıes roughly accounting for 77%

The projected demand for halal food & beverage is US$ 1,585 billion for 2020, corresponding to a Compound Annual Growth Rate (CAGR) of about 5.8%.

6

1128

798 741

367 336 238

0

200

400

600

800

1000

1200

Global MuslimFood Market

China USA Japan India Brazil

947

Share (%) of Total Muslim Food Expenditure by Region Percent

Source: State of Global Islamic Economy Report 2014

Key Markets, Key Facts (cont.)

The growth in Asia has been driven by changing lifestyles that allow for higher incomes. The GCC countries have higher incomes and consequently higher per capita rates on consumption. The growth in the halal food industry is unlikely to be curbed in the near future.

Countries in North Africa region are not only import-dependent for food, but consumers are predominantly Muslim with rising per capita incomes. With Muslims making up almost one-third of the population, the halal food industry in Sub-Saharan Africa is expected to see continuous growth in the upcoming years

With a total share of 9.5% in halal food Europe, Americas and Australia are presenting huge demand for high quality, healthy and safe products. 7

Asia 49,9%

MENA-Other 21,8%

Sub-Saharan Africa 11,0%

MENA-GCC 7,8%

Europe 7,8%

Americas and Australia

1,7%

Top Countries by Volume of Muslim Food Consumption Market, 2014 USD billion

Source: State of Global Islamic Economy Report 2015

Key Markets, Key Facts (cont.)

8

157,6

109,7 100,5

75,5 62 58,9

44,1 39,4 35,4 34,2

0

20

40

60

80

100

120

140

160

180

Top-10 markets account for 58% of total halal food consumption in 2014

8 OIC countries are ranked among the top-10 markets…among these.. three countries; Indonesia, Turkey and Pakistan account for 30% of total halal food consumption

Top Countries by Halal Food Indicator, 2014

Source: State of Global Islamic Economy Report 2015

Key Markets, Key Facts (cont.)

9

Halal Food Indıcator (HFI) evaluate countries’ health and development of their Halal Food ecosystem. The indicator does not focus on the overall size and growth trajectory of a country in the Halal Food sector; instead it evaluates them on relative strengths of the ecosystem they have for the development of the sector.

1. Trade (OIC Food Trade Relative to its size) 2. Governance (Regulation/Certification requirements) 3. Awareness (Media/Events) 4. Social (Food Price Index)

78

56

53

51

49

45

44

43

41

41

0 10 20 30 40 50 60 70 80 90

Malaysia

Pakistan

UAE

Australia

Oman

Brazil

Jordan

Azerbaijan

Egypt

Qatar

Key Markets, Key Facts (cont.)

10

Population growth Awareness

Major Drivers

Technological development

Food security

Legal framework

Economics

• Formulation and adoption of legislative framework in many countries over the past decade

• lead to use of tech to convert arid land into agricultural land….overseas investment in agrıculture production and manufacturing companies

• ..role in advancing agriculture and the food industry…ıncrease in processed food…mechanical slaughter …stunting…lab testing

• Recognition as engine of growth…many initiatives at govt and corporate level to tape into the market

• …Influx of events such as national halal initiatives, conferences, expos, online networking and media

• .. strong consumer base of over 1.7 billion Muslims…expected to reach 2 billion by 2030 …the fastest growing consumer segment in the world

Source: From niche to mainstream – Halal Goes Global

Halal Food in OIC Countries: Key Issues

Unification of Standards and Certification

Halal Food Authentication

Unveiling the Potential of Islamic Finance

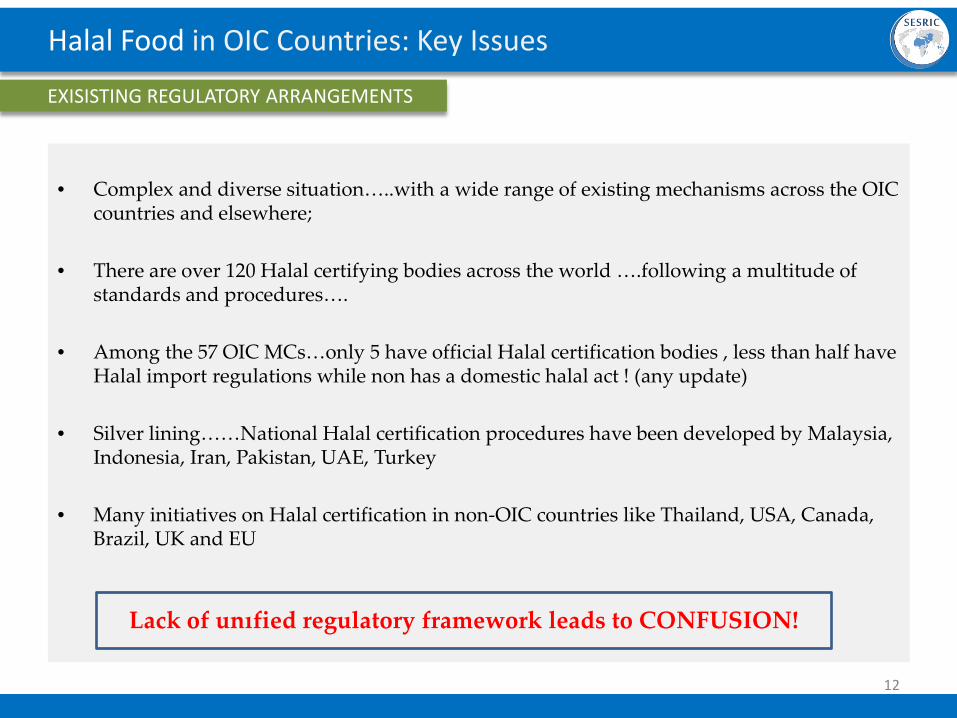

Halal Food in OIC Countries: Key Issues

EXISISTING REGULATORY ARRANGEMENTS

12

• Complex and diverse situation…..with a wide range of existing mechanisms across the OIC

countries and elsewhere;

• There are over 120 Halal certifying bodies across the world ….following a multitude of standards and procedures….

• Among the 57 OIC MCs…only 5 have official Halal certification bodies , less than half have Halal import regulations while non has a domestic halal act ! (any update)

• Silver lining……National Halal certification procedures have been developed by Malaysia, Indonesia, Iran, Pakistan, UAE, Turkey

• Many initiatives on Halal certification in non-OIC countries like Thailand, USA, Canada, Brazil, UK and EU

Lack of unıfied regulatory framework leads to CONFUSION!

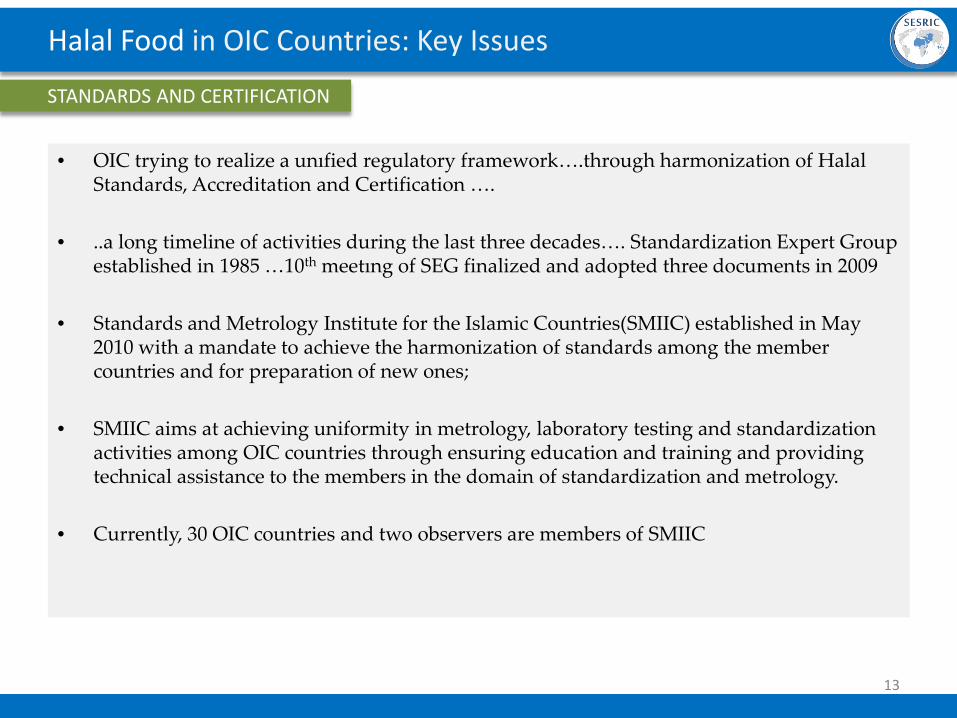

Halal Food in OIC Countries: Key Issues

STANDARDS AND CERTIFICATION

13

• OIC trying to realize a unıfied regulatory framework….through harmonization of Halal Standards, Accreditation and Certification ….

• ..a long timeline of activities during the last three decades…. Standardization Expert Group established in 1985 …10th meetıng of SEG finalized and adopted three documents in 2009

• Standards and Metrology Institute for the Islamic Countries(SMIIC) established in May 2010 with a mandate to achieve the harmonization of standards among the member countries and for preparation of new ones;

• SMIIC aims at achieving uniformity in metrology, laboratory testing and standardization

activities among OIC countries through ensuring education and training and providing technical assistance to the members in the domain of standardization and metrology.

• Currently, 30 OIC countries and two observers are members of SMIIC

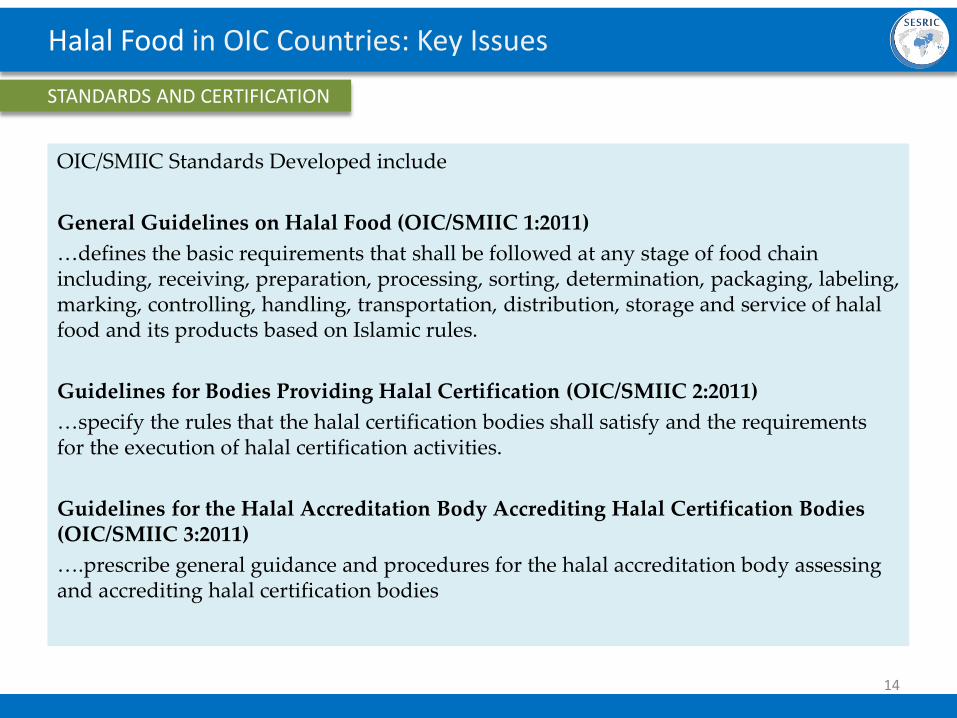

Halal Food in OIC Countries: Key Issues

STANDARDS AND CERTIFICATION

14

OIC/SMIIC Standards Developed include General Guidelines on Halal Food (OIC/SMIIC 1:2011) …defines the basic requirements that shall be followed at any stage of food chain including, receiving, preparation, processing, sorting, determination, packaging, labeling, marking, controlling, handling, transportation, distribution, storage and service of halal food and its products based on Islamic rules. Guidelines for Bodies Providing Halal Certification (OIC/SMIIC 2:2011) …specify the rules that the halal certification bodies shall satisfy and the requirements for the execution of halal certification activities. Guidelines for the Halal Accreditation Body Accrediting Halal Certification Bodies (OIC/SMIIC 3:2011) ….prescribe general guidance and procedures for the halal accreditation body assessing and accrediting halal certification bodies

Thus, It is imperative to develop robust scientific methods for traceability in halal compliance of

ingredients and products. Proper authentication will help to guarantee and sustain authenticity, combat fraudulent practices and control adulteration and substitution

Consolidation of analytical techniques will assist integrity and result in a more rapid growth of halal food industry

However, OIC countries are lagging in the number of laboratories that are able to develop

state-of-the-art analytical and measurement techniques to determine the provenance of halal foods

Halalan Toyyiban requirement Throughout the industry, halal requirements must be complied with at all stages of the

production and supply chain, including procurement of raw materials and ingredients, logistics and transportation, packaging and labelling

Halal Food in OIC Countries: Key Issues

AUTHENTICATION

15

Equity or profit sharing partnerships with halal food

companies

Financial certificates issued by halal companies (leases.,

debt, asset, etc.)

Financing facility to halal food SMEs for start-up

and/or growth

Financing facility to halal food consumers

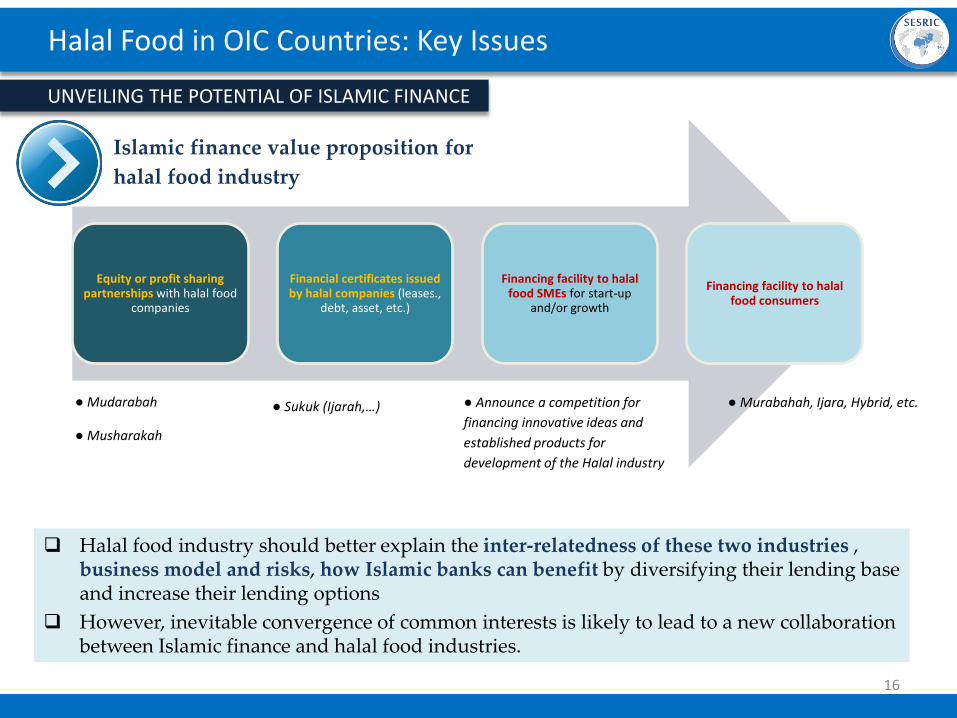

● Mudarabah

● Musharakah

● Sukuk (Ijarah,…) ● Announce a competition for financing innovative ideas and established products for development of the Halal industry

● Murabahah, Ijara, Hybrid, etc.

Islamic finance value proposition for halal food industry

Halal Food in OIC Countries: Key Issues

UNVEILING THE POTENTIAL OF ISLAMIC FINANCE

Halal food industry should better explain the inter-relatedness of these two industries , business model and risks, how Islamic banks can benefit by diversifying their lending base and increase their lending options

However, inevitable convergence of common interests is likely to lead to a new collaboration between Islamic finance and halal food industries. 16

On-going Challenges

Rising demand and trade in the halal food products, in the face of lack of global integrity

in the certification process, has already led to the abuse and misuse of halal food certification. In many instances, halal certificates can be granted very easily;

In the case of high tradable products, such as in the GCC countries, being halal is necessary, but not a sufficient condition as the halal products are already becoming mainstream and competitive products;

Halal markets in OIC and non-OIC countries are fragmented market by ethnicity, location, income, awareness and a few other determinants. Therefore, a one-size-fits-all strategy simply cannot work.

Halal finance is one of the essential ingredients of halal food. Interaction between Islamic finance and halal food industries have been very limited so far.

Most halal products in the export markets fail due to poor product adaptability and lack of branding exercise. Brand awareness and loyalty are not at the desired level;

In many OIC countries, underdeveloped transport and logistics negatively impact the intra-OIC halal food trade. Exporting halal food products to some of member countries can only be achieved through multi-modal transport due to the unavailability of seaports, which inevitably adds costs; and

Scientific techniques as independent means of verifying the halal status of food products are not in place. Traceability for halal certification relies almost solely on paper trail.

17

The halal food market presents vast business opportunities to food manufacturers in the OIC countries: Product variety is currently low and the market is relatively unsaturated, Demand is huge for new and innovative products, as well as mainstream halal foods, The halal-seeking consumer market can grow very rapidly and will potentially include a

variety of consumer types other than Muslims, Halal products can be positioned as higher quality, safer products, targeting consumers

who wish to spend more on food products than average consumers, Many Muslims, who would otherwise prefer halal food, are currently substituting kosher

products for halal foods, spending billions annually.

Opportunities

18

OIC, the member countries and the global halal food stakeholders should agree on the development of the global halal standards and a mutually recognized halal certification structure to prevent further abuse and misuse of halal certification;

Monitoring of the implementation of OIC standards on halal food and guidelines for both certification and accreditation bodies is core to the success of the industry. In this regard, the scientific and technological infrastructure for halal authentication should be established;

The future growth of halal food industry lies in the assurance and sustenance of food quality, rather than pure religious matters. Europe, Americas and Australia with a total share of 57 per cent in total food consumption vis-à-vis only 10 per cent in halal food, are presenting huge demand for higher quality, healthier and safer products;

The inevitable convergence of the halal food and Islamic finance sectors is one of the key developments that is likely to shape the Halal food sector over the coming years. The areas of collaboration for unraveling the potential of Islamic finance for supporting halal food industry should be sought;

OIC member countries with relatively underdeveloped multi-modal transport infrastructure should develop their transportation networks to facilitate the intra-OIC trade of halal food; Integration of production and logistics into an efficient supply chain network has to be considered;

Capacity building programmes for halal food activities: Training of halal inspectors, halal food auditors and laboratory analysts;

The role of conventional, digital and social media in shaping consumer perceptions as well as providing access to 1.7 billion potential customers should be examined.

Recommendations and Outlook

19

T H A N K YO U For enquiries:

Mazhar Hussain Senior Researcher