the swiss professional journal for payment traffic … · the swiss professional journal for...

TRANSCRIPT

CLEARITThe Swiss professional journal for payment trafficEdition 42 | December 2009

> Single Euro Payments Area’s legal framework from the Swiss viewpoint Interview with SEPA law expert Martin Hess

> How secure are SEPA direct debits?

> Cover payments: Best practices of the new message type

Front cover photo: SIX Group VIP-Lunch at Sibos in Hongkong, 16 September.

Interview Page 4SEPA legal framework from the Swiss perspective: Market access through legal comparisonSince 2006, the attorney Martin Hess has been focusing on the Single Euro Payments Area (SEPA). As author of several reports for the financial centers Switzerland and Liechtenstein he is acknowledged as a Swiss SEPA expert.

Products & Services Page 8How secure is payment by SEPA direct debits?SEPA’s vision – to standardize cashless euro payments in Europe – was first realized with the launch of SEPA credit transfers in January 2008. Then, on November 2, another service was successfully started: SEPA direct debit. What role do security concerns play in the future acceptance of this payment instrument?

Facts & Figures Page 10PSD increases competitionThe EU regulations governing payment services for domestic markets – Payment Services Directive (PSD) – forms the legal basis for a modern legal framework for payments in the 30 EU/EEA countries, including Liechtenstein. Its purpose is to make payment traffic as simple, efficient and secure as possible, and to encourage competition. But the latter goal, especially, is questionable, as a new study now shows.

Business & Partners Page 11SWIFT access for corporate clientsThe cooperative of financial institutions was founded in 1973 with the purpose of guaranteeing cross-border, secure transmission of messages between financial institutions. The success particularly drew the attention of globally active corporates interested in standardizing the interfaces and processes of their international correspondent banking networks.

Standardization Page 12Cover payments: Best practices of the new message typeOn 21 November 2009 SWIFT introduced the new MT202COV format for cover payments. The move is designed to increase the transparency of international payment transactions with the aim of additionally bolstering measures designed to combat money laundering and the financing of terrorism. In concrete terms, all banks involved in the payment chain can calibrate the (additionally) provided data in the course of sanctions screening.

Highlights Page 14Good grades for CLEARITThe readers’ survey was conducted the third time during the past nine years. And the upward trend is continuing!

2 CONTENT / CLEARIT | December 2009

3EDITORIAL / CLEARIT 1 | 2009

Dear readersOn November 2, 2009, another European payment traffic milestone was reached: SEPA Direct Debit was introduced successfully in several countries, including Switzerland. This means that Switzerland is again among the first nations to introduce a new SEPA service on time, as it was for SEPA credit transfers in January 2008. On the very first day, SIX Group, in cooperation with SECB, had already suc-cessfully processed the first debits from the SEPA zone. After starting SEPA direct debits next year for the B2B area, as well, Switzerland will have introduced all SEPA payment traffic basic services. But the next challenges in relation to SEPA Additional Optional Services (SEPA AOS) are already in the offing, specifically in the areas of e-payments, e-mandates and e-invoicing. At first glance, e-invoicing doesn’t seem to be part of this picture. What does e-in-voicing have to do with payment traffic?

The internal corporate flows are connected to the payment systems through electronic invoicing. That’s why SEPA and a successful European initiative complement each other for electronic invoicing. Based on increased efficiency and automation of the delivery chain, the EU expects tremen-dous advantages for businesses and financial services providers resulting from these two initiatives. These benefits were quantified in a 2007 analysis conducted on behalf of the EU Commission. The study showed that the EU could save a healthy 238 billion euro by introducing EU comprehensive e-invoicing by 2012.

As a result, in 2007 the EU asked a panel of experts to evaluate by the end of 2009 which measures would foster a rapid expansion of e-invoicing in the EU. In parallel,

various industry-related organizations, such as EBA, Equens and SWIFT, began addressing the topic. All three organizations came to the conclusion that they want to be actively involved. Last year, EBA, in cooperation with Innopay, published a study about e-invoicing in Europe, and since then it has been working with a group of banks on developing pan-European e-invoicing solutions based on the existing e-banking systems. That should be available by the end of 2011. In 2008, Equens started an initiative to construct an international, open e-invoicing network intended to connect existing systems in various countries. To date, Italian and Belgian systems are connected to Equens.

I am convinced that over the next few years, analogous to the introduction of electronic business processes, e-invoic-ing will rapidly spread across all of Europe as well as worldwide, and that soon it won’t be possible to imagine a business world without it. The Swiss banks are well po-sitioned in this respect, also. In cooperation with SIX Paynet, more than 90 banks have been offering e-invoicing services for some time now, allowing their customers to obtain access using the e-invoicing service under e-banking solutions. PostFinance has entered the market with its own product, as well. <

Martin FrickCEO, SIX Paynet and SIX Interbank Clearing

3EdiTORiAL / CLEARIT | December 2009

Since 2006, the attorney Martin Hess has been focusing on the Single Euro Payments Area (SEPA). As author of several reports for the financial centers Switzerland and Liechtenstein he is acknowledged as a Swiss SEPA expert. He was recently speaker at the Swiss Banking Law Day 2009 and author of the essay “Euro payments in accordance with the SEPA Rulebooks, particularly concerning the liability of banks” and co-author of the article “Payments in euro by Swiss banks according to the SEPA Rulebooks,” which appeared in the Swiss Review of Business and Financial Market Law mid-2009.

SEPA legal framework from the Swiss perspec-tive: market access through legal comparison

CLEARIT: Mr. Hess, on the one hand SEPA is based on the self-regulation of the financial industry, represented by the EPC, while on the other hand, on the political will of the European Commission to introduce the standardi-zation of payment transactions throughout Europe. What is the legal framework of the two endeavors, how do they interact and what is the legal nature of the regulations enacted by the EPC?Martin Hess: SEPA is based on private legal agreements. These were concluded between an institution in accord-ance with Belgian law (EPC – European Payments Council) and each of the financial institutions. The framework for these agreements is the EU regulation on payments, generally known as the Payment Services Directive (PSD). The PSD sets out binding rules that must be implement-ed by each of the member states. They primarily regulate the relationship between the banks and their clients and broach the issues of transparency and consumer protec-tion. The SEPA rulebooks cover other regulatory areas. They fundamentally deal with the relationship between financial institutions. Rules are thus defined that must be applied between the banks, and that only concern the re-lationship between banks and their customers in a very indirect way. However, certain standards can only be adhered to if the bank’s customers also follow the SEPA standards, especially in the case of direct debits. Although the SEPA rulebooks definitely have an influence on the re-lationship to the customers, they do not directly regulate it. It must be clearly stated that without the PSD there would be no SEPA rulebooks. Conversely, as self-regu-lation initiatives, these rulebooks are, of course, also an instrument of the European financial industry to hinder any binding EU standards that prescribe in great detail what individual banks are allowed to do and what not. The banking industry was keen to prevent that in any case. Any textual deviation between the SEPA rulebooks and the

PSD is unthinkable. The only room to maneuver is there where the PSD does not prescribe anything. Thus any SEPA participation is either directly or indirectly subject to PSD regulations.

“By demonstrating the parity of Swiss regulations, we dispelled any concerns regarding the idea that Switzerland has a locational advantage and that the SEPA rulebooks could not be legally binding.”

The Swiss financial institutions are part of SEPA, even though Switzerland is neither an EU nor an EEA member country. Who made the decision and which prerequisites did Switzerland have to fulfill in order to be accepted as a SEPA participant? Switzerland was a member of the EPC right from the start. That is actually amazing and is largely due to the excellent personal contacts between the Swiss and the European financial institutions. Nevertheless, there were some reser-vations and the Swiss financial center had to satisfy three requirements in order to participate in SEPA:1. Swiss financial institutions had to assure that they are capable of fulfilling the obligations defined in the SEPA rulebooks.2. Our country must have a level playing field with other European countries.3. The central PSD regulations regarding the relationship between financial institutions and customers must be effectively represented in Swiss law or in equally binding practice.

4 iNTERviEw / CLEARIT | Dezember 20094 iNTERviEw / CLEARIT | December 2009

5

With regard to the level playing field, in Brussels we had to demonstrate that Swiss financial institutions do not simply operate in a vacuum but are required to behave like EU banks in all respects, for instance with regard to money laundering. By demonstrating the parity of Swiss regula-tions, we dispelled any concerns regarding the idea that Switzerland has a locational advantage and that the SEPA rulebooks could not be legally binding.

In contrast to the EU, there is no law governing payment transactions in Switzerland. To which degree can the legal situation even be compared? The PSD prescribes the framework for payments in Europe. It must be implemented under national law. The PSD is a special sectoral law, like so many in the EU. Switzer-land has fewer of these special laws. We have our general codifications, the Swiss Civil Code and the Swiss Code of Obligations. These do not specifically cover payment trans-actions. In addition, we have the Federal Court practice, the cantonal court practice and the traditional tenets. These have always stood us in good stead. In contrast to other European countries, Switzerland is also aware of the general principle of “good faith.” In some cases Switzerland endorses European law and enacts corre-sponding regulations in a spirit of autonomous adaptation. As regulations regarding payments in Switzerland are to be found scattered among various laws, we first need to explain these to other countries in Europe. Although we can testify to the parity of Swiss and EU law with a good conscience, how can we expect Europeans whose market we wish to penetrate to understand the complex Swiss legal situation? In the end we have to admit that although our legal system functions well, it is not always as simple to convince others of this fact.

The EPC rulebook prescribes that participants are required to provide evidence that the PSD regulations relevant for SEPA credit transfers and direct debits are effectively represented in national law or are based on a substantially equivalent binding practice. What does “substantially equivalent binding practice” precisely mean? After exhaustive preparation on the part of the Swiss financial industry, we were able to demonstrate in Brussels how payment transactions are made in our country. We compared the Swiss regulations with those of the PSD, paragraph for paragraph. In doing so we were successful in plausibly convincing the EPC members that the legal system in Switzerland is essen-tially equivalent to that of the EU.

The Swiss financial institutions were admitted the SEPA, even though Switzerland is not part of the EU, which is a great achievement. However, no one can tell whether it will remain that way in the long run. As soon as a law is amended somewhere in an EU state it can have an

Short biography Martin Hess is currently Managing Partner of Wenger & Vieli AG. His practice focuses on financial services law, mergers & acquisitions and information technology law. He advises Swiss and foreign financial institutions on all matters with respect to financial services and capital markets law, both relating to regulatory law as well as private law. He has been involved in structur-ing the legal basis for electronic funds transfer systems and securities clearing systems as well as for central counterparties for stock exchange transactions. He further contributed as an expert to the legislation in Switzerland on securities law and netting.

Martin Hess obtained his doctorate degree in law from the University of Zurich in 1984. In 1987, he was admitted to the Bar Association of Canton Zurich. Before joining private practice in 1994, he was Research Assistant at the Faculty of Law of the Uni-versity of Zurich and, later, served as Legal Counsel to the Swiss National Bank. In 1994 and 1997, he was a member of International Monetary Fund missions to countries in Eastern Europe. Martin Hess has regularly published articles on the subject areas of his practice and contributed as co-author to one of the leading legal commentaries on Swiss banking law.

5iNTERviEw / CLEARIT | December 2009

influence on the “equivalent practice.” A legal comparison cannot be compared with an international treaty: the latter remains valid as long as it is not renegotiated. It can also be clearly stated that the EPC members are extremely reluctant to grapple with Swiss law. It is up to Switzerland to provide evidence that Swiss law is equivalent in the respective areas.

The SEPA Credit Transfer Scheme has been well accepted by banking clients in Switzerland. The pro-portion of international SEPA payments is far aboveaverage in comparison with other countries. To which degree is the PSD also binding for these transactions?Payments within Switzerland are not subject to the PSD, no more than are cross-border payments between Switzer-land and the EU or the EEA. However, when it comes to the following payment chain, caution is recommended: as soon as a payment transferred to Switzerland from the EU leaves Switzerland for the EU, the transaction becomes subject to the PSD. The Swiss bank as link will then have to voluntarily observe the PSD regulations if it does not want to lose its mandate as correspondence bank.

The SEPA Direct Debit Scheme was introduced on November 2nd. Are there essential differences to credit transfers from a legal point of view?The legal fundamentals are the same, but with regard to the authorization to debit, SEPA direct debits are handled

6 iNTERviEw / CLEARIT | December 2009

differently to Swiss direct debit payments. Whereas in the case of an LSV+ or BDD transaction the debtor gives his or her bank the explicit authorization to debit the account, in the case of a SEPA direct debit the creditor gives the debit order to his or her bank, which then passes it on to the debtor’s bank. That is something new in Switzerland.

“Is Switzerland really autonomous if it de-clares EU law as being inapplicable in what are actually technical areas? In this case I refer to the Settlement Finality Directive, the Financial Collateral Arrangements Directive and the PSD. Aren’t we already interpreting EU law autonomously and therefore actually not autonomous at all?”

Switzerland has had a currency union with Liechtenstein since 1921. As an EEA country Liechtenstein has imple-mented the PSD in national law. Does that cause legal problems to arise in bilateral payment transactions or in card processing?

EU Parliament and Council

• EU Payment Services Directive (PSD) 2007• Regulation on cross-border payments in euro 2001• (EU Directive cross-corder credit transfers 1997)

Binding legal acts (also for the relationship between financial institution and customer)

Addressee: States

European Payments Council

• EU law as SEPA Rulebooks basis• SEPA Rulebooks = multi-lateral contracts under Belgian law• Rules governing the relationship between financial institutions and not with regard to bank/customer

Contract governed by private law(in principle only for the relationship between financial institutions)

Addressee: Financial institutions

Source: Wenger & Vieli AG

Regulatory basis of SEPA

77iNTERviEw / CLEARIT | December 2009

Debtor Bank Creditor Bank

Creditor

Debit authorization for LSV

Debit authorization for SEPA

Source: Wenger & Vieli AG

Debtor

Debit authorization in comparison

This subject is highly interesting, but also complex. In this case we have three different areas: the currency area (Swiss francs), the legal area (EU/EEA) and the payment system for Swiss francs (SIC) used in Switzerland under Swiss law.

The question now is, how to achieve compatibility between these three areas. For example – the credit card business is currently a topic of discussion – certain services could then no longer be provided from Switzerland. In any case, a payment in Swiss francs from Liechtenstein to Frankfurt, for example, is subject to the PSD and for that reason the corresponding regulations must be observed, even if a Swiss payment system such as SIC is used. Geograph-ically, Switzerland is situated in the middle of Western Europe. In the case of international payment transactions the interfaces resulting from non-membership of the EU or the EEA are shown transparently. Is Switzerland really autonomous if it declares EU law as being inapplicable in what are actually technical areas? In this case I refer to the Settlement Finality Directive, the Financial Collateral Arrangements Directive and the PSD. Aren’t we already in-terpreting EU law autonomously and therefore actually not autonomous at all? Market access through legal compari-son works as long as our laws prove to be equivalent. This is far easier when the actual conditions such as in the case of payment transactions are basically similar. The future will show whether this method will endure or whether more binding regulations have to be made with the EU. <

Interview: Andreas Galle, SIX Interbank [email protected]é Gsponer, Enterprise Services [email protected]

8 PROdUCTS & SERviCES / CLEARIT | December 2009

The European countries’ mutual approach to the free movement of European citizens and goods has found its continuation within the electronic payment traffic due to SEPA (Single Euro Payments Area). Its vision – to standardize cash-less euro payments in Europe – was first realized with the launch of SEPA credit transfers in January 2008. Then, on November 2, 1 pm, another service was successfully started: SEPA direct debit. What role do security concerns play in the future acceptance of this payment instrument?

How secure is payment by SEPA direct debits?

2,600 European financial institutions from 22 countries are already participating in this new scheme; among them, the Swiss financial institutions Credit Suisse, Neue Aargauer Bank, Clariden Leu, UBS and PostFinance. The first one of the new direct debit schemes to be intro-duced was the SEPA Core Direct Debit Scheme, which is the base direct debit scheme (with general right of revo-cation), particularly for the “Business to Customer” area. According to the schedule, SEPA B2B Direct Debit Scheme (without general right of revocation) should be introduced in the business-to-business area starting in late 2010, as well as various additional services such as the e-mandate.

What is a SEPA direct debit?In a kind of credit transfer turnaround, the debtor author-izes the creditor to collect the amount due at his bank. The basis for each direct debit is a bilateral mandate between a debtor and a creditor to use the SEPA direct debit as a form of payment.

The debtor issues to a creditor – by means of a debit mandate, either nationally or abroad – the rights to execute SEPA collection in euro from the debtor’s account. Neither the creditor’s nor the debtor’s financial institution are aware of this bilateral agreement before the first submission (by electronic mandate) of a direct debit.

Thus, the SEPA Direct Debit Scheme works the same way as the schemes existing in most European countries where the creditor has a physical copy of the mandate.

How secure is the process? Even though direct debits are basically an agreeable solution for invoicing and payment for both debtors and creditors, the Swiss direct debit procedures (LSV+/BDD) plays a relatively small role – with a share of less than 4% of all payment instruments – compared to other European

countries, such as Germany, with a share of more than 40%.

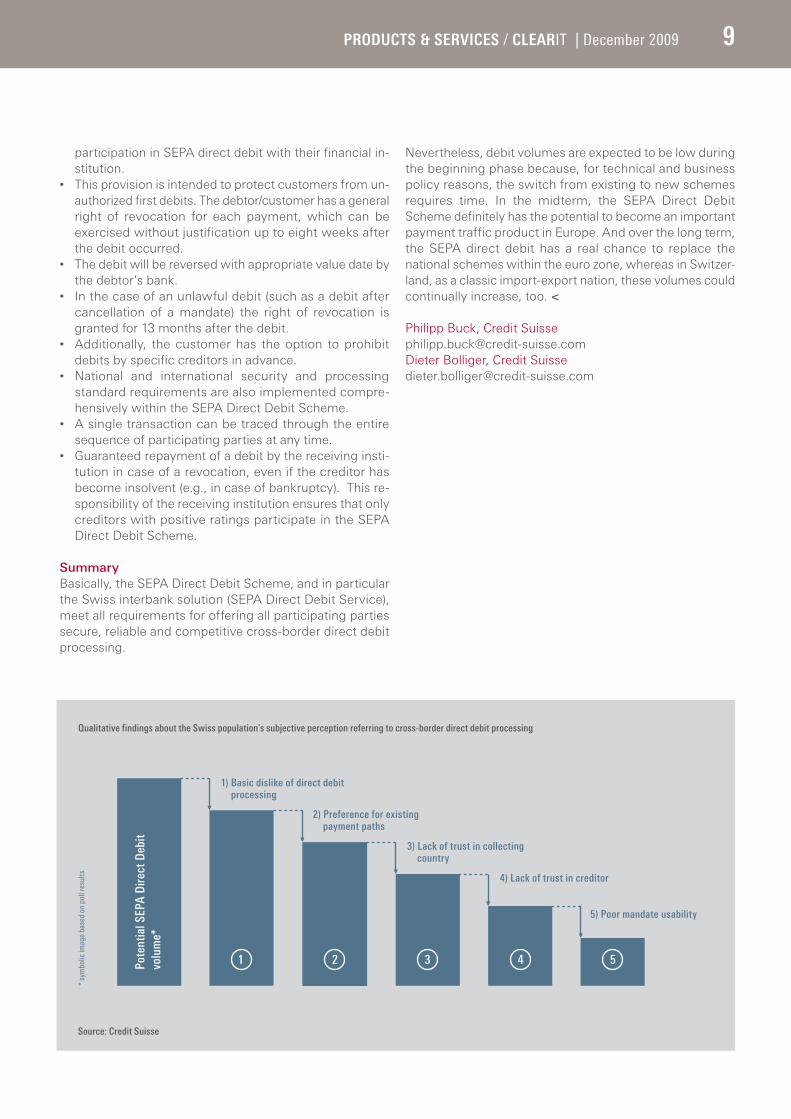

In parts of the Swiss population there are significant res-ervations about direct access by third parties to private bank accounts, reflecting a heightened security awareness. These reservations, and the need for heightened security, magnified by other unspecified insecurities, can affect the SEPA Direct Debit Scheme.

In a poll (see graph on page 9), most people interviewed wanted to maintain total control over their accounts and define the exact time a payment is executed, or they preferred already-existing payment paths via invoice, credit card charge, etc. For those individuals who basically were open to cross-border direct debit processing, the trust in the collecting country plays an important role: While there is a relatively high level of trust in the countries bordering on Switzerland, it decreases proportionally with increasing eastern distance. An additional factor is the size and repu-tation of a collecting party: Here, generally known brands are preferred over small businesses. The mandate’s customer friendliness is also a deciding element: The lower the corresponding efforts for the debtor, the higher the readiness to sign the mandate.

The findings – and, in particular, the high security require-ments – were included in the SEPA Direct Debit Scheme conception and development in an effort to reduce creditor reservations to a minimum, thereby reaching the highest possible level of acceptance in the market.

The SEPA Direct Debit Scheme design contains the following security measures in particular:• Without a specific contract for SEPA direct debits,

creditor accounts are not accessible at most of the Swiss financial institutions. This means that a SEPA direct debit can only be debited once the debtor has confirmed

99PROdUCTS & SERviCES / CLEARIT | December 2009

Qualitative findings about the Swiss population’s subjective perception referring to cross-border direct debit processing

participation in SEPA direct debit with their financial in-stitution.

• This provision is intended to protect customers from un-authorized first debits. The debtor/customer has a general right of revocation for each payment, which can be exercised without justification up to eight weeks after the debit occurred.

• The debit will be reversed with appropriate value date by the debtor’s bank.

• In the case of an unlawful debit (such as a debit after cancellation of a mandate) the right of revocation is granted for 13 months after the debit.

• Additionally, the customer has the option to prohibit debits by specific creditors in advance.

• National and international security and processing standard requirements are also implemented compre-hensively within the SEPA Direct Debit Scheme.

• A single transaction can be traced through the entire sequence of participating parties at any time.

• Guaranteed repayment of a debit by the receiving insti-tution in case of a revocation, even if the creditor has become insolvent (e.g., in case of bankruptcy). This re-sponsibility of the receiving institution ensures that only creditors with positive ratings participate in the SEPA Direct Debit Scheme.

SummaryBasically, the SEPA Direct Debit Scheme, and in particular the Swiss interbank solution (SEPA Direct Debit Service), meet all requirements for offering all participating parties secure, reliable and competitive cross-border direct debit processing.

Nevertheless, debit volumes are expected to be low during the beginning phase because, for technical and business policy reasons, the switch from existing to new schemes requires time. In the midterm, the SEPA Direct Debit Scheme definitely has the potential to become an important payment traffic product in Europe. And over the long term, the SEPA direct debit has a real chance to replace the national schemes within the euro zone, whereas in Switzer-land, as a classic import-export nation, these volumes could continually increase, too. <

Philipp Buck, Credit [email protected] Bolliger, Credit [email protected]

* sy

mbo

lic im

age

base

d on

pol

l res

ults

Pote

ntia

l SEP

A D

irect

Deb

it vo

lum

e*

51

1) Basic dislike of direct debit processing

2

2) Preference for existing payment paths

3

3) Lack of trust in collecting country

4

4) Lack of trust in creditor

5) Poor mandate usability

Source: Credit Suisse

10 FACTS & FiGURES / CLEARIT | December 2009

The EU regulations governing payment services for domestic markets – Payment Services Directive (PSD) – forms the legal basis for a modern legal framework for payments in the 30 EU/EEA countries, including Liechtenstein. Its purpose is to make payment traffic as simple, efficient and secure as possible, and to encourage competition. But the latter goal, especially, is questionable, as a new study now shows.

PSD increases competition

In addition to simplifying payment traffic, the EU is hoping that the Payment Services Directive will increase competition by opening payment traffic markets for new providers. That, in turn, should lead to higher efficiency and lower costs, es-pecially for the consumer. With regards to the introduction of PSA, Accenture launched a survey* among 29 financial institutions, inquiring about the chances of that element of competition becoming reality.

Fight for market shareThe results show that the banks surveyed mostly do see new opportunities, but that they don’t have any particular plans to acquire new customers with the introduction of the PSD. Nor are the current payment traffic providers concerned about new competition. This leads to the supposition that the most important banks offering payment traffic services, and the payment service processing specialists such as Equens or VocaLink, are already firmly established. Thus, competition will only actually increase among the already-active market participants, with the main beneficiaries being the company clients of the financial institutions. If today, for example, a company has to task five different banks to issue pan-European payments, in the future this will be possible using a single service provider – at a far lower price, no less.

Swiss banks at a disadvantageIt is assumed that banks need to offer new SEPA services to secure customer retention and loyalty. Particularly in that regard, Swiss banks could be faced with obvious competi-tive disadvantages. Even if Swiss financial institutions fully integrate the PSD in their payment traffic services, they will be at a disadvantage vis-à-vis the banks in EU/EEA countries, because SEPA credit transfers or direct debits are not subject to EU price regulations and can thus be priced individually – read, more expensively – by the receiving banks in Europe. One example: If a business customer has a SEPA credit transfer to Austria processed through a bank in Germany, fees may only be within the eurocent range, according to EU price regulations. However, if the same SEPA payment is transferred from Switzerland, the receiving Austrian bank can bill the customer, let’s say, a 50 euro fee, because Switzerland is not governed by the EU regulation. Thus, European providers processing payment traffic from the PSD area of application are at a consider-able advantage. <

Thomas Sontheimer, Partner Financial Services, [email protected]

* The results of the Accenture survey “Harmonizing Payments – Insights to Progress on the European Payment Services Directive” are based on replies to an online survey of 29 Euro

Banking Association banks in May of 2009.

24

510

24

What opportunities do you see with the PSD?

Number of respondents for a particular category

Provide pan-European payment and banking services

Launch new products Reduce costs Acquire new corporate customers

Acquire new retailcustomers

1111BUSiNESS & PARTNERS / CLEARIT | December 2009

Since the implementation of its networks, SWIFT has developed into the most important infrastructure in the area of standardized message transmission for the banks. The SWIFT standards have significantly contributed to the automation of internal banking processes, supporting the trend toward a global financial industry.

Since SWIFT was originally founded for the purpose of ex-changing financial messaging between the banks, it took some time until a way of accepting corporate clients as SWIFT participants could be found that didn’t alter the character of SWIFT as a bank-maintained cooperative.

Since mid-2006, corporates have been able to join SWIFT directly and exchange messages and files within the network with all their SWIFT participating banks. In September 2009, 512 corporate clients exchanged messages with 1,230 banks worldwide. In comparison, in 2006 there were 181 business clients and fewer than 100 banks.

In Switzerland, 24 internationally active corporate clients are already using the SWIFT network. These organiza-tions largely use SWIFT for transmission of their payment orders, notification of expected payment receipts and con-firmation of foreign currency exchange transactions. On the other side, they receive their deposit and account statements from their banks via SWIFT in a standardized format, which permits automated account reconciliation.

SWIFT’s strength lies primarily in that it provides a com-munication interface for internationally active institutions striving for standardization in their cooperation with partners worldwide. SWIFT doesn’t yet have the same appeal for more nationally focused business clients or or-ganizations that only generate a low message volume. For these business customers, implementation efforts and the related costs are still too high. Nor does SWIFT, as yet, provide a cost-effective alternative to the banks’ propri-etary communication interfaces.

However, SWIFT’s success story has proven that the cooperative is capable of registering market demands and developing appropriate solutions. Hence, it is only a

SWIFT access for corporate clientsSWIFT was founded in 1973 as a cooperative of financial institutions with the purpose of guaranteeing cross-border, secure transmission of messages between financial institutions. The success particularly drew the attention of globally active corporates interested in standardizing the interfaces and processes of their international correspondent banking networks.

question of time until SWIFT will offer an option for na-tionally focused and smaller company clients. <

Michael Montoya, Head of Global Payments & Cash Management Services, [email protected]

Additional information about SWIFT for corporates: www.swift.com/corporates/

MT101

MT103

MT300

MT210

others

MT940

MT942 MT300

MT910

MT900

others

Sent messages

Number of messages exchanged by the 24 Swiss corporates participating in SWIFT (January 2008 to August 2009)

Received messages

On 21 November 2009 SWIFT introduced the new MT202COV format for cover payments. The move is designed to increase the transparency of international payment transactions with the aim of additionally bolstering measures designed to combat money laundering and the financing of terrorism. In concrete terms, all banks involved in the payment chain can calibrate the (additionally) provided data in the course of sanctions screening.

New message type for cover payments – best practices

The MT202COV format includes a sequence B that es-sentially amounts to a copy of the direct customer order MT103. Thus banks that execute the cover payment now also have access to the payment details of the underlying MT103, including information on the ordering customer, the beneficiary party and the reason for payment.

Following international recommendations (see http://pmpg.webexone.com/) and as supplementary information for the financial center of Switzerland, the Swiss Bankers Associa-tion (SBA) published its own set of best practices in handling the MT202COV format last October (circular No. 7626).

Reactions Although a great many of points have been regulated in the above-mentioned recommendations, there is still a large amount of uncertainty regarding the future behavior of market participants. Already now there are signs that several financial institutions will only be performing serial payments. Due to the increased cost expected, other financial in-stitutions are considering raising their fees for sanctions screening.

However, the crucial question will be how to deal with blocked or refused cover payments, particularly if the account of the beneficiary customer has already been credited. As a result of various reactions from market participants it can be assumed that direct customer orders will be increasingly withheld until the money has been arrived in order to avoid risks.

In view of the various international and national recom-mendations, most countries have not issued any regulatory requirements. It cannot be ruled out that the MT202 will continue to be used instead of the MT202COV. For this reason there is no guarantee that covering banks will receive the necessary data from the respective customer order. Neither are banks able to differentiate between bank-to-bank payments (MT202) and cover payments (MT202COV).

Minor change – major impactThe new standard will significantly increase transparency for the banks concerned and make an important contri-bution to combating money laundering and the financing of terrorism. The new additional information can be trans-mitted at moderate technical cost. Sanctions screening too is relatively straightforward. The changes in the op-erational processes, the use of serial payments instead of cover payments and the introduction of the new fees will have a great impact on the market. Existing liability risks connected with blocked or refused payments are also likely to influence the behavior of market participants. <

Maria-Luisa Tavano, Credit [email protected] Kunz, Credit [email protected]

12 STANdARdiZATiON / CLEARIT | December 2009

• For international payments an MT202COV is to be used. This is the case if at least one of the correspond-ence banks involved is based in a foreign country.

• The additional data fields of the MT202COV must be calibrated with the currently valid sanctions lists.

Main points of the SBA recommendations:

13STANdARdiZATiON / CLEARIT | December 2009

Source: SWIFT

Bank A'sCorrespondent

MT202COVor equivalent

MT910/950or equivalent

Ordering & Beneficiary Parties and Remittance Information are trans-ported the MT202COV

OrderingCustomer

Bank B'sCorrespondent

Bank BMT103

MT202COV

Remittance Information

BeneficiaryCustomer

Bank A

• All data fields of the MT202COV must be forwarded in their complete and unchanged form.

• The first receiving bank within Switzerland is required to perform a sanctions screening procedure. For this reason the MT202COV data do not need to be ad-ditionally transmitted when forwarding to a further Swiss bank. This applies particularly to forward-ing within the SIC and euroSIC systems. Thus the

corresponding SIC formats (B11) have not been enlarged.

• The ordering customer data contained in the MT202COV do not need to be checked for com-pleteness within the context of art.15 para. 4 of GwV-FINMA 1.

14 HiGHLiGHTS / CLEARIT | December 2009

The readers’ survey was conducted the third time during the past nine years. And the upward trend is continuing. Many thanks especially to the devoted readers.

Good grades for CLEARIT

More than ten percent of the respondents had already par-ticipated in the first survey, another fifteen percent took part of the second one.

With an average grade of more than five of six possible points for quality of copy, layout and topic mix (see chart 1) CLEARIT is more popular than ever with its readers. An overwhelming majority is happy with the quarterly schedule (see chart 2) as well as with the balance in topics discussed (see chart 3).

Editorials and interviews increasingly popularWhile in 2003 only half of the participants surveyed found the editorials interesting to very interesting, three years later their rate of approval had increased to almost 70% and this time the rate was up to almost 80%. Interviews, to, are increasing in popularity (see chart 4). Standardiza-tion questions and payment traffic products reached their highest approval rate yet (3.5 each in 2009; 3.5 and 3.6 respectively in 2009). The popularity of compliance and SEPA related articles climbed from the last survey by 2.9 and 3.2 to 3.2 and 3.3 respectively.

One nation in spite of many culturesBasically, the evaluations of the correspond with those of the German speaking readership (see chart 5). The de-viations are minimal, yet noteworthy in that in this latest survey the French speaking readers issued better grades on average for both content and layout. For text quality, this is not necessarily a foregone conclusion, since the vast majority of all articles is translated from German. Clearly, the level of comprehensibility is not compromised, which means that the translators are doing a very fine job, indeed.

The CLEARIT Council and the editorial team will do every-thing in their power to continue to maintain the high quality level achieved, and, during the next meeting, will carefully analyze the suggestions for improvement submitted. <

Gabriel Juri, SIX Interbank [email protected]

The lucky winners of an iPod: • Theo Schmid (Credit Suisse)• Raffaele Esposito (SWIFT)• Ursizin Blumenthal (Rothschild Bank)• Philippe Metrailler (Banque Cantonale du Valais)• Donato Panizzolo (BSI)• Ruedi Becker (Schweizerische Nationalbank)

Chart 1: Overall assessment (6 = highest, 1 = lowest)

Content Format, Layout Topic mix

2003 2006 2009

5.20

5.10

5.00

4.90

4.80

4.70

4.60

15HiGHLiGHTS / CLEARIT | December 2009

Chart 2: Happy with frequency (in %)

95

90

85

80

75

2003 2006 2009

Chart 4: How interesting are the editorial, interview, info concerning payment traffic

committees and products? (4 = very interesting, 1 = not interesting at all)

4.00

3.50

3.00

2.50

2.00

1.50

1.00

Editorial Interview Committees Products

2003 2006 2009

Chart 6: Phase out printed version (in %)

35

30

25

20

15

10

5

–

2003 2006 2009

Chart 5: Language comparison German/French (6 = highest, 1 = lowest)

Chart 7: Read all issues (in %)

89

88

88

87

87

86

86

85

2003 2006 2009

Content Format, Layout Topic mix

German 2006 French 2006 German 2009 French 2009

Chart 3: Balanced topic contents (in %)

95

94

93

92

91

90

89

88

2003 2006 2009

5.20

5.10

5.00

4.90

4.80

4.70

4.60

PublisherSIX Interbank Clearing LtdHardturmstrasse 201CH-8021 Zurich, Switzerland

Ordering/[email protected]

EditionEdition 42 – December 2009Published regularly, also online at www.CLEARIT.ch. Circu-lation German (1300 copies), French (400 copies) and English (available in electronic format only on www.CLEARIT.ch).

CouncilPatrick Bürki, PostFinance, Boris Brunner, UBS Ltd, SusanneEis, SECB, Oliver Buob, SNB, Martin Frick, SIX Interbank Clearing Ltd, Andreas Galle, SIX Interbank Clearing Ltd, André Gsponer (Head), Enterprise Services Ltd, Gabriel Juri,SIX Interbank Clearing Ltd, Roger Mettier, Credit Suisse, Christoph Weder, Liechtensteinischer Bankenverband, Jean-Jacques Maillard, BCV

Editorial TeamAndré Gsponer, Enterprise Services AG, Andreas Galle,Gabriel Juri (Head) und Christian Schwinghammer, SIXInterbank Clearing Ltd

TranslationFrench: Word + Image, English: HTS

LayoutFelber, Kristofori Group, Advertising agency

PrinterBinkert Druck Ltd, Laufenburg

ContactsProduct Management SIX Interbank Clearing LtdT +41 44 279 4747Customer Service Swiss Euro Clearing Bank GmbHT +49 69 97 98 98 35

Additional information about the Swiss payment traffic systems can

be found on the Internet at www.six-interbank-clearing.com

Masthead

This year’s Sibos VIP-Lunch of SIX Group took place at the Peninsula Hotel’s Felix Bar in Hongkong.