the taxation of trusts - bsp seminars · 2016-02-27 · terms and conditions 5—the taxation of...

TRANSCRIPT

March 2015 2014 edition

nb1504 Volume 1

By Costa Divaris

The Taxation of Trusts —the law & the return

The Taxation of Trusts —the law & the return by Costa Divaris

2014 Edition

Terms and conditions

5—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Terms and conditions

User rights This work is made available subject to the author’s and publisher’s copyright and nonexclusive user rights granted to you to use it solely for your personal or professional purposes and not to distribute it in any form. For these limited purposes only, the copying and adaption of the specimen letters included here is specifically permitted.

Electronic version The electronic version of this work is available by way of e-mail or hyperlink in the form of a PDF file. By supplying the publisher with your e-mail address, you agree to receive e-mail notifications of forthcoming seminars, publications and related offers from BSP Seminars®. To unsubscribe at any time, send an e-mail with the subject ‘No more e-mail’ to [email protected]. Should you be a subscriber, such an e-mail will also terminate your free subscription to the Tax Shock, Horror newsletter.

Further copies Apart for the purposes of the eponymous seminar for which these notes were developed and printed, this work is otherwise available in electronic format only. Should you require a further or printed and bound copy of this work, please contact the publisher.

Provenance, edition and product number Product number in the BSP Seminars® Store of this 2014 edition ver 2: nb1504. This work is based upon ‘Trusts & Tax—Case & Statute Law’ vol I (2012).

Disclaimer This work is not intended to constitute advice on the topics covered. The views expressed are those of the author and publisher. While reasonable care has been taken to ensure the accuracy of this publication, the author and publisher expressly disclaim all and any liability to any person relating to anything done or omitted to be done or to the consequences thereof in reliance upon this work, and do not accept responsibility for any loss or damage that may be sustained as a result of reliance by any person on the information contained herein. In particular, anyone who may be affected by statutory provisions dealt with in this work is strongly advised to refer to the relevant Government Gazette as originally published.

Terms and conditions

6—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Copyright ©2015 Costa Divaris/The Electronic Publishing Corp CC (referred to here as ‘the author’ and ‘the publisher’ respectively) Gauteng South Africa. This work is copyright under the Berne Convention. In terms of the Copyright Act 98 of 1978 and subject to the user rights detailed above, no part of this work may be reproduced or transmitted in any form or by any means, presently known or that may be devised, electronic or mechanical, including photocopying, recording or by any information storage and retrieval system, without permission in writing from the publisher.

BSP Seminars®, Knowledge in Business® and Law Lookup® are registered trademarks.

Publisher The Electronic Publishing Corp CC (C Divaris). Bsp Seminars® is a division of The Electronic Publishing Corp cc. 12 Eshowe Street Paulshof Extension 10. Telephone 011 234 2434. Fax-to-e-mail 086 515 0955. Postnet Suite 72 Private Bag X87 Bryanston 2021. Business and Seminar Manager: Lesley Byrne. Contact Lesley Byrne: 082 854 2238; [email protected]. Contact Costa Divaris: Mobile 083 677 3333; [email protected].

Latest legislation upon which this work is based The Income Tax Act 58 of 1962, as last amended by all amending tax acts up to and including the Tax Administration Laws Amendment Act 44 of 2014 (20 January 2015).

ISBN 978–0–928221–62–6

Stylistic conventions—text

7—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Stylistic conventions—text

This work follows all of the conventions set out in the latest edition of the Bsp Stylebook (C Divaris, DS McAllister), a free publication.

Legislative or contractual elements that are expressly and formally defined are referred to as terms, and are embraced, when necessary, by quotation marks. Other words (single words) and expressions (a collection of words) that are effectively defined or are used by me as personal terms of art are shown, when necessary, in italics, without quotation marks. Thus ‘gross income’ but hidden definition.

Otherwise, quotation marks are used purely to indicate a formal, verbatim quotation arising within the text. When a quotation appears separately from the text and indented, no quotation marks are used, while paragraph-indentations are dispensed with in the first line of the quotation and in every first line following an interruption of the quotation by indented or hanging material. Tables might not necessarily follow these rules.

Inside a quotation, quotations within the text of the quotation are embraced by single quotation marks and quotations within those quotations with double quotation marks, subject to recycling should the nesting continue. Quotations shown separately from the text of a quotation are presented without quotation marks but subject to a further indentation.

Legislative material included here is reproduced from publicly or commercially available consolidations, rendered in my own ‘value-added’ style and updated by me where necessary to render the text fully up to date with all amending acts dated 2014. Each extract is followed in small print by a note indicating the amending act under which it was first enacted or last amended.

Where lists of defined terms are provided, no recognition is given to terms defined in the Tax Administration Act but applying also to the Income Tax Act.

Any extracts from the Tax Shock, Horror newsletter reproduced here are reproduced in their form as originally published and thus may not be fully up to date.

8—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Stylistic conventions—legislation

9—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Stylistic conventions—legislation

Identifier Act, provision number (usually section, subsection; paragraph, subparagraph)

Dates, periods, percentages, fractions Rendered in bold

Outside parties Rendered in italics

Cross-references Restated in short form within square parentheses

Acts, self-references, Schedules, Parts Underlined

Defined words within quotation marks Rendered in bold

Defined words without quotation marks (‘as defined in’) Rendered in bold italics

Quasi-defined words (‘as contemplated in’, ‘referred to’, ‘as defined in’ ‘as determined by’) Rendered in bold italics

Apparent errors Either rectified within square parentheses or correction suggested within square parentheses and indicated by question mark

Extracts from explanatory memoranda Rendered in small print

Commentary, headed ‘Legislative history’, boxed, italicized Details and effective date of amendment

Commentary, headed ‘Past wording’, boxed, italicized Immediately preceding text of amended legislation

10—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Contents—chapters

11—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Contents—chapters

Click on an item to go to that page. Terms and conditions .......................................................................................... 5 Stylistic conventions—text ................................................................................. 7 Stylistic conventions—legislation ...................................................................... 9 Contents—chapters........................................................................................... 11 Contents—extracts from the act (ITA) ............................................................... 15 Contents—extracts from the act (TAA) ............................................................. 17 Contents—commentary .................................................................................... 19 Contents—sections & subsections .................................................................... 21

Chapter 1 ........................................................................................................ 29 The tax base ...................................................................................................... 29

Normal tax: the charging provision ................................................................ 29 Section 1(1) sv ‘normal tax’, s 5(1) ............................................................. 29 Section 1(1) sv ‘year of assessment’ ............................................................ 32

Normal tax: the tax base ................................................................................. 33 Section 1(1) sv ‘taxable income’ ................................................................. 33 Section 1(1) sv ‘gross income’ .................................................................... 35 Section 1(1) sv ‘gross income’, para (n) ...................................................... 37 Section 8(1)(a)(i) ......................................................................................... 39 Section 26A ................................................................................................. 40 Paragraph 2, 8th Sch ..................................................................................... 41 Section 22(1), (2) ......................................................................................... 43 Section 1(1) sv ‘Republic’ ........................................................................... 45

Normal tax: imposition .................................................................................. 47 Section 1(1) sv ‘person’ ............................................................................... 47

Chapter 2 ........................................................................................................ 55 Residence.......................................................................................................... 55

The decider between worldwide and source-based taxation .......................... 55 Section 1(1),‘foreign investment entity’ ...................................................... 72

Chapter 3 ........................................................................................................ 75 Source ............................................................................................................... 75

A concept of as much interest to residents as to nonresidents ........................ 75 Section 1(1),‘gross income’, para (n)(ii) ...................................................... 78 Section 9(2) .................................................................................................. 85 Section 9(3) .................................................................................................. 88 Section 9(4) .................................................................................................. 88

Chapter 4 ........................................................................................................ 99 Tax rates for trusts ............................................................................................ 99

Special trusts v ordinary trusts ....................................................................... 99 Section 1(1) sv ‘year of assessment’ ............................................................ 99 Section 1(1) sv ‘normal tax’, s 5(1) ........................................................... 100 Section 1(1) sv ‘taxable income’ ............................................................... 104 Section 26A ............................................................................................... 104 Section 1(1) sv ‘taxable capital gain’, para 10, 8th Sch .............................. 105

Contents—chapters

12—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Paragraph 8 8th Sch .................................................................................... 106 Chapter 5 ...................................................................................................... 109

What is a trust? ............................................................................................... 109 Common-law and fiscal trusts, trustees and beneficiaries ............................ 109

Section 1(1) sv ‘trust’ ................................................................................ 113 Section 1(1) sv ‘trustee’ ............................................................................. 117 Section 1(1) sv ‘beneficiary’ ...................................................................... 118

Chapter 6 ...................................................................................................... 123 The trust as taxpayer ....................................................................................... 123

The trustees, acting jointly, are the true fiscal actor ..................................... 123 Representative taxpayer—under the Income Tax Act .................................. 129

Section 1(1) sv ‘representative taxpayer’ ................................................... 129 Paragraph 13(7), 4th Sch ............................................................................. 133

Representative taxpayer—under the Tax Administration Act ...................... 135 Chapter 7 ...................................................................................................... 151

Special types of fiscal trusts ........................................................................... 151 The special trust ........................................................................................... 151

Section 1(1) sv ‘special trust’ .................................................................... 151 The trust as personal service provider .......................................................... 166 The closure rehabilitation trust ..................................................................... 177 Chapter 8 ...................................................................................................... 179

When the donor pays the tax .......................................................................... 179 Introduction .................................................................................................. 179 Income tax .................................................................................................... 185

Section 7(1) ................................................................................................ 185 Section 7(2), (2A), (2B), (2C) .................................................................... 187 Section 7(3), (4) ......................................................................................... 193 Section 7(5) ................................................................................................ 195 Section 7(6) ................................................................................................ 196 Section 7(7) ................................................................................................ 197 Section 7(8) ................................................................................................ 199 Section 7(9), (10), (11) .............................................................................. 200

Capital gains tax ........................................................................................... 203 Paragraph 68, 8th Sch ................................................................................. 203 Paragraph 69, 8th Sch ................................................................................. 205 Paragraph 70, 8th Sch ................................................................................. 207 Paragraph 71, 8th Sch ................................................................................. 208 Paragraph 72, 8th Sch ................................................................................. 209

Income tax and capital gains tax .................................................................. 211 Paragraph 73, 8th Sch ................................................................................. 212

Chapter 9 ...................................................................................................... 215 When the beneficiaries pay tax ....................................................................... 215

Income tax .................................................................................................... 215 Section 25B(1), (2) .................................................................................... 221 Section 25B(3), (4), (5), (6), (7) ................................................................. 223

Capital gains tax ........................................................................................... 226 Paragraph 80, 8th Sch ................................................................................. 229

Chapter 10 .................................................................................................... 233 General tax issues ........................................................................................... 233

Contents—chapters

13—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Applying the law .......................................................................................... 233 Chapter 11 .................................................................................................... 245

Offshore trusts ................................................................................................ 245 Introduction .................................................................................................. 245 Income tax rules ........................................................................................... 248

Section 25B(2A) ........................................................................................ 248 Capital gains tax rules .................................................................................. 251

Paragraph 80(3), 8th Sch ............................................................................ 252 Responding to the rules ................................................................................ 254 Chapter 12 .................................................................................................... 261

Loans to and by trusts ..................................................................................... 261 Introduction .................................................................................................. 261 Loans as an act of liberality ......................................................................... 267 Chapter 13 .................................................................................................... 275

Trusts and other taxes and issues .................................................................... 275 Other taxes levied by the Income Tax Act ................................................... 275 Chapter 14 .................................................................................................... 283

The new trust return ........................................................................................ 283 Information to create the income tax return for a trust ................................. 283 Appendix ...................................................................................................... 287

Form ITR 12T .................................................................................................. 287

14—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Contents—extracts from the act (ITA)

15—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Contents—extracts from the act (ITA)

Click on an item to go to that page. From the Act 1—‘normal tax’ (ss 1(1), 5(1)) ................................................... 29 From the Act 2—‘year of assessment’ (s 1(1)) ................................................. 32 From the Act 3—‘taxable income’ (s 1(1)) ...................................................... 33 From the Act 4—‘gross income’, preamble (s 1(1)) ........................................ 35 From the Act 5—‘gross income’, para (n) (s 1(1)) ........................................... 37 From the Act 6—the taxable allowances plug-in (s 8(1)(a)(i)) ........................ 39 From the Act 7—the taxable capital gain plug-in (s 26A) ................................ 40 From the Act 8—application of the CGT (para 2, 8th Sch) ................................ 41 From the Act 9—the trading stock plug-in (s 22(1), (2)) ................................. 43 From the Act 10—‘Republic’ (s 1(1)) .............................................................. 45 From the Act 11—‘person’ (s 1(1)) .................................................................. 47 From the Act 12—‘company’ (s 1(1)) .............................................................. 49 From the Act 13—‘foreign investment entity’ (s 1(1)) .................................... 72 From the Act 14—source of recoupments (s 1(1), ‘gross income’) ................. 78 From the Act 15—domestically sourced income-flows (s 9(2)) ....................... 85 From the Act 16—pensions & annuities deemed services (s 9(3)) ................... 88 From the Act 17—foreign sourced income-flows (s 9(4)) ............................... 88 From the Act 18—‘year of assessment’ (s 1(1)) ............................................... 99 From the Act 19—‘normal tax’ (ss 1(1), 5(1)) ............................................... 100 From the Act 20—‘taxable income’ (s 1(1)) .................................................. 104 From the Act 21—the taxable capital gain plug-in (s 26A) ............................ 104 From the Act 22—taxable capital gain (s 1(1), para 10, 8th Sch) ................... 105 From the Act 23—net capital gain (para 8, 8th Sch) ....................................... 106 From the Act 24—‘trust’ (s 1(1)) ................................................................... 113 From the Act 25—‘trustee’ (s 1(1)) ................................................................ 117 From the Act 26—‘beneficiary’ (s 1(1)) ........................................................ 118 From the Act 27—‘representative taxpayer’ (s 1(1)) ..................................... 129 From the Act 28—donations tax and representative taxpayers (s 61) ............ 132 From the Act 29—delivery of tax certificate (para 13(7), 4th Sch) ................. 133 From the Act 30—‘special trust’ (s 1(1)) ....................................................... 151 From the Act 31—‘personal service provider’ (para 1, 4th Sch) ..................... 167 From the Act 32—obsolete attribution rule (s 7(1)) ....................................... 185 From the Act 33—spousal attribution rules (s 7(2), (2A), (2B), (2C)) ........... 187 From the Act 34—diversion to minor child (s 7(3), (4)) ................................ 193 From the Act 35—undistributed income (s 7(5)) ........................................... 195 From the Act 36—revocable distributed income (s 7(6)) ............................... 196 From the Act 37—cession of income-streams (s 7(7)) ................................... 197 From the Act 38—diversion to nonresident (s 7(8)) ....................................... 199 From the Act 39—special rules (s 7(9), (10), (11)) ........................................ 200 From the Act 40—spousal attribution rules (para 68, 8th Sch) ....................... 203 From the Act 41—diversion to minor child (para 69, 8th Sch) ....................... 205

Contents—extracts from the act

16—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

From the Act 42—undistributed capital gain (para 70, 8th Sch) ..................... 207 From the Act 43—revocable distributed gain (para 71, 8th Sch) .................... 208 From the Act 44—diversion to nonresident (para 72, 8th Sch) ....................... 209 From the Act 45—attribution of income and gain (para 73, 8th Sch) ............. 212 From the Act 46—income of trusts v beneficiaries (s 25B(1), (2)) ................ 221 From the Act 47—deductions (s 25B(3), (4), (5), (6), (7)) ............................. 223 From the Act 48—gains of trusts v beneficiaries (para 80, 8th Sch) ............... 229 From the Act 49—distribution from nonresident trust (s 25B(2A)) ............... 248 From the Act 50—distribution from nonresident trust (para 80(3), 8th Sch) .. 252

Contents—extracts from the act (TAA)

17—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Contents—extracts from the act (TAA)

Click on an item to go to that page From the Tax Administration Act 1—ss 1, 151: ‘taxpayer’ ........................... 135 From the Tax Administration Act 2—ss 1, 153(1): ‘representative taxpayer’ 136 From the Tax Administration Act 3—s 23: registered persons ...................... 140 From the Tax Administration Act 4—s 153(2): notification of status ............ 141 From the Tax Administration Act 5—s 153(3): taxpayer unrelieved ............. 142 From the Tax Administration Act 6—s 154: representative liability ............. 142 From the Tax Administration Act 7—s 155: personal liability ...................... 145 From the Tax Administration Act 8—s 169(2): recovery .............................. 145

18—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Contents—commentary

19—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Contents—commentary

Click on an item to go to that page. Commentary 1—ss 1(1), 5(1): significance of ‘normal tax’ ............................. 30 Commentary 2—ss 1(1), 5(1): significance of ‘year of assessment’ ................ 32 Commentary 3—s 1(1): significance of ‘taxable income’ ................................ 33 Commentary 4—s 5(1): the tax base ................................................................ 34 Commentary 5—s 1(1): ‘gross income’, structure of ....................................... 35 Commentary 6—s 1(1): para (n) of ‘gross income’ ......................................... 38 Commentary 7—s 8(1)(a)(i): the taxable allowances plug-in .......................... 40 Commentary 8—s 26A: the taxable capital gain plug-in .................................. 41 Commentary 9—para 2(1), 8th Sch: territoriality of the CGT ............................ 42 Commentary 10—s 22(1), (2): the trading stock plug-in ................................. 43 Commentary 11—s 1(1): significance of ‘Republic’........................................ 45 Commentary 12—s 1(1): significance of ‘person’ ........................................... 47 Commentary 13—s 1(1): significance of ‘company’ ....................................... 50 Commentary 14—associations, universitas, body of persons .......................... 51 Commentary 15—unincorporated associations & bodies of persons ............... 53 Commentary 16—universitas ........................................................................... 53 Commentary 17—s 1(1): structure of ‘resident’ ............................................... 55 Commentary 18—residence: the Kuttel case .................................................... 58 Commentary 19—Interpretation Note 3 on ordinarily resident ....................... 64 Commentary 20—Interpretation Note 6 on effective management .................. 66 Commentary 21—residency article in tax treaty with China ............................ 68 Commentary 22—s 1(1): ‘gross income’, para (n)(ii): source of recoupments 79 Commentary 23—s 9: identifying s 9(2) and (4) originating causes ................ 81 Commentary 24—Trust Property Control Act: ‘trust’.................................... 109 Commentary 25—Trust Property Control Act: ‘trust instrument’ .................. 111 Commentary 26—all the fiscal trusts, as ‘persons’ ........................................ 113 Commentary 27—s 1(1): significance of ‘trustee’ ......................................... 117 Commentary 28—s 1(1): significance of ‘beneficiary’ .................................. 118 Commentary 29—s 1(1): significance of ‘representative taxpayer’ ............... 130 Commentary 30—s 61: donations tax ............................................................ 133 Commentary 31—representative taxpayer as taxpayer .................................. 135 Commentary 32—what is a representative taxpayer? .................................... 137 Commentary 33—change of representative taxpayer ..................................... 140 Commentary 34—notification by representative taxpayer ............................. 141 Commentary 35—taxpayer remains on the line ............................................. 142 Commentary 36—representative liability ....................................................... 143 Commentary 37—personal liability ............................................................... 145 Commentary 38—recovery ............................................................................ 146 Commentary 39—s 1(1): significance of ‘special trust’ ................................. 152 Commentary 40—disability special trusts ...................................................... 153 Commentary 41—youth special trusts ............................................................ 154

Contents—commentary

20—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Commentary 42—special income tax treatment for special trusts .................. 155 Commentary 43—special CGT treatment for special trusts ............................. 157 Commentary 44—special trusts for the disabled ............................................ 163 Commentary 45—para 1, 4th Sch: ‘personal service provider’ ....................... 167 Commentary 46—PSPs in the main body of the Income Tax Act ................... 169 Commentary 47—PSPs in the Fourth Schedule (PAYE) .................................. 173 Commentary 48—PSPs in the Sixth Schedule (micro-business) ..................... 174 Commentary 49—s 7(1): academics love this meaningless provision ........... 185 Commentary 50—spousal attribution rules .................................................... 190 Commentary 51—diversion to minor children ............................................... 194 Commentary 52—s 7(5): undistributed income ............................................. 195 Commentary 53—s 7(6): revocable distributed income ................................. 196 Commentary 54—s 7(7): cession of income-streams ..................................... 198 Commentary 55—s 7(8): diversion to nonresident ......................................... 200 Commentary 56—s s 7(9), (10), (11): special rules ........................................ 201 Commentary 57—para 68, 8th Sch: spousal attribution rules ......................... 204 Commentary 58—para 69, 8th Sch: diversion to minor child ......................... 206 Commentary 59—para 70, 8th Sch: undistributed capital gain ....................... 207 Commentary 60—para 71, 8th Sch: revocable distributed gain ...................... 209 Commentary 61—para 72, 8th Sch: diversion to nonresident ......................... 210 Commentary 62—para 73, 8th Sch: attribution of income & gain .................. 213 Commentary 63—s 25B(1), (2): income of trusts v beneficiaries .................. 221 Commentary 64—s 25B(3), (4), (5), (6), (7): deductions ............................... 224 Commentary 65—para 80, 8th Sch: gains of trusts v beneficiaries ................. 230 Commentary 66—s 25B(2A): distribution from nonresident trust ................. 249 Commentary 67—para 80(3), 8th Sch: distribution from nonresident trust .... 252

Contents—sections & subsections

21—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Contents—sections & subsections

Click on an item to go to that page. Section 1(1) sv ‘normal tax’, s 5(1) .................................................................. 29

ITA s 1(1) sv ‘normal tax’ ............................................................................... 29 ITA s 5(1) ........................................................................................................ 29 ITA s 6(1) ........................................................................................................ 30 ITA s 6A(1) ..................................................................................................... 31 ITA s 6B(2) ..................................................................................................... 31 ITA s 6quat(1), extract .................................................................................... 31 ITA s 6quin(1), extract .................................................................................... 31 ita s 64N(1) .................................................................................................... 31

Section 1(1) sv ‘year of assessment’ ................................................................ 32 ITA s 1(1) sv ‘year of assessment’ .................................................................. 32

Section 1(1) sv ‘taxable income’ ...................................................................... 33 ITA s 1(1) sv ‘taxable income’ ........................................................................ 33 ITA s 1(1) sv ‘taxable income’ ........................................................................ 34 ITA s 1(1) sv ‘income’ .................................................................................... 34

Section 1(1) sv ‘gross income’ ......................................................................... 35 ITA s 1(1) sv ‘gross income’, preamble .......................................................... 35 ITA s 1(1) sv ‘gross income’, para (i) ............................................................. 36 ITA s 1(1) sv ‘gross income’, para (ii) ............................................................ 36

Section 1(1) sv ‘gross income’, para (n) ........................................................... 37 ITA s 1(1) sv ‘gross income’, para (n) ............................................................ 37 ITA s 1(1) sv ‘taxable income’ ........................................................................ 38

Section 8(1)(a)(i) .............................................................................................. 39 ITA s 8(1)(a)(i) ................................................................................................ 39 ITA s 1(1) sv ‘taxable income’, para (b) ......................................................... 40

Section 26A ...................................................................................................... 40 ITA s 26A ........................................................................................................ 40 ITA s 1(1) sv ‘taxable income’, para (b) ......................................................... 41

Paragraph 2, 8th Sch .......................................................................................... 41 ITA 8th Sch para 2(1) ....................................................................................... 41 ITA 8th Sch para 2(2) ....................................................................................... 41

Section 22(1), (2) .............................................................................................. 43 ITA s 22(1) ...................................................................................................... 43 ITA s 22(2) ...................................................................................................... 43

Section 1(1) sv ‘Republic’ ................................................................................ 45 ITA s 1(1) sv ‘Republic’ .................................................................................. 45 MZA S 4 ........................................................................................................... 45 MZA S 5 ........................................................................................................... 45 MZA S 6 ........................................................................................................... 46 MZA S 7 ........................................................................................................... 46 MZA S 8 ........................................................................................................... 46

Section 1(1) sv ‘person’ .................................................................................... 47 ITA s 1(1) sv ‘person’ ..................................................................................... 47

Contents—sections & subsections

22—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

IA s 2 sv ‘person’ ............................................................................................ 47 ITA s 1(1) sv ‘company’ ................................................................................. 49 ITA s 1(1) sv ‘company’, para (d) ................................................................... 50 ITA s 1(1) sv ‘resident’, with headings ........................................................... 55 ITA s 1(1) sv ‘resident’, structural representation, para (a)(i) ......................... 57 ITA s 1(1) sv ‘resident’, structural representation, para (a)(ii) ........................ 57 ITA s 1(1) sv ‘resident’, para (b) ..................................................................... 65 ITA s 1(1) sv ‘resident’, structural representation, treaty persons ................... 67 Republic of China, art 4 ................................................................................. 68 ITA s 1(1) sv ‘resident’, first proviso .............................................................. 70 ITA s 1(1) sv ‘resident’, structural representation, para (a)(ii) ........................ 70 ITA s 1(1) sv ‘resident’, structural representation, proviso (A) to para (a)(ii) 71

Section 1(1),‘foreign investment entity’ ........................................................... 72 ITA s 1(1) sv ‘foreign investment entity’ ........................................................ 72 ITA s 1(1) sv ‘resident’, structural representation, second proviso ................. 73 ITA s 1(1) sv ‘gross income’, extract, structural representation ...................... 77

Section 1(1),‘gross income’, para (n)(ii) .......................................................... 78 ITA s 1(1) sv ‘gross income’, para (n)............................................................. 78 ITA s 1(1) sv ‘dividend’ .................................................................................. 81 ITA s 24I(1), preamble .................................................................................... 81 ITA s 24I(1) sv ‘exchange difference’ ............................................................. 81 ITA s 24I(1) sv ‘exchange item’ ...................................................................... 82 ITA s 1(1) sv ‘foreign dividend’ ...................................................................... 82 ITA 8th Sch para 2(2) ....................................................................................... 83 ITA s 24J(1), preamble .................................................................................... 83 ITA s 24J(1) sv ‘interest; ................................................................................. 83 ITA s 8E(2) ...................................................................................................... 84 ITA s 9(1) ........................................................................................................ 84 ITA S 23I(1) sv ‘intellectual property’ ............................................................. 84

Section 9(2) ...................................................................................................... 85 ITA s 9(2), preamble ....................................................................................... 85 ITA s 9(2)(a).................................................................................................... 85 ITA s 9(2)(b).................................................................................................... 85 ITA s 9(2)(c) .................................................................................................... 85 ITA s 9(2)(d).................................................................................................... 85 ITA s 9(2)(e) .................................................................................................... 86 ITA s 9(2)(f) .................................................................................................... 86 ITA s 9(2)(g).................................................................................................... 86 ITA s 9(2)(h).................................................................................................... 86 ITA s 9(2)(i) .................................................................................................... 86 ITA s 9(2)(j) .................................................................................................... 87 ITA s 9(2)(k) .................................................................................................... 87 ITA s 9(2)(l) .................................................................................................... 87

Section 9(3) ...................................................................................................... 88 ITA s 9(3) ........................................................................................................ 88

Section 9(4) ...................................................................................................... 88 ITA s 9(4) ........................................................................................................ 88 ITA s 9(2)(a).................................................................................................... 89 ITA s 9(4)(a).................................................................................................... 89

Contents—sections & subsections

23—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

ITA s 9(2)(f) .................................................................................................... 89 ITA s 9(2)(g) ................................................................................................... 89 ITA s 9(2)(h) ................................................................................................... 90 ITA s 9(2)(b) ................................................................................................... 91 ITA s 9(2)(b) ................................................................................................... 91 ITA s 9(4)(b) ................................................................................................... 91 ITA s 9(2)(c) .................................................................................................... 92 ITA s 9(2)(c) .................................................................................................... 92 ITA s 9(2)(d) ................................................................................................... 92 ITA s 9(4)(c) .................................................................................................... 92 ITA s 9(2)(e) .................................................................................................... 92 ITA s 9(2)(e) .................................................................................................... 92 ITA s 9(2)(i) .................................................................................................... 93 ITA s 9(2)(i) .................................................................................................... 93 ITA s 9(2)(j) .................................................................................................... 94 ITA s 9(2)(k) .................................................................................................... 94 ITA s 9(2)(k) .................................................................................................... 94 ITA s 9(4)(d) ................................................................................................... 95 ITA s 9(2)(l) .................................................................................................... 96 ITA s 9(2)(l) .................................................................................................... 96 ITA s 9(4)(e) .................................................................................................... 96

Section 1(1) sv ‘year of assessment’ ................................................................ 99 ITA s 1(1) sv ‘year of assessment’ .................................................................. 99

Section 1(1) sv ‘normal tax’, s 5(1) ................................................................ 100 ITA s 5(1) ...................................................................................................... 100 R&MA&ARLA 42 of 2014 s 2, extract ........................................................... 100 R&MA&ARLA 42 of 2014 Appendix I, extract ............................................. 101 R&MA&ARL Bill, 2015 s 3(1) ....................................................................... 102 R&MA&ARL Bill, 2015 Appendix I, extract ................................................. 102

Section 1(1) sv ‘taxable income’ .................................................................... 104 ITA s 1(1) sv ‘taxable income’ ...................................................................... 104

Section 26A .................................................................................................... 104 ITA s 26A ...................................................................................................... 104

Section 1(1) sv ‘taxable capital gain’, para 10, 8th Sch ................................... 105 ITA s 1(1) sv ‘taxable capital gain’ ............................................................... 105 ITA 8th Sch para 10 ....................................................................................... 105

Paragraph 8 8th Sch ......................................................................................... 106 ITA 8th Sch para 1 sv ‘net capital gain’ ......................................................... 106 ITA 8th Sch para 8 ......................................................................................... 106 TPCA s 1 sv ‘trust’ ......................................................................................... 109 TPCA s 1 sv ‘trust instrument’ ....................................................................... 111

Section 1(1) sv ‘trust’ ..................................................................................... 113 ITA s 1(1) sv ‘trust’ ....................................................................................... 113 ITA s 1(1) sv ‘person’ ................................................................................... 113 ITA s 1(1) sv ‘trust’ ....................................................................................... 113 TDA s 1(1) sv ‘person’ .................................................................................. 113 TDA S 1(1) sv ‘trust’ ...................................................................................... 113 VATA s 1(1) sv ‘person’ ................................................................................ 114 VATA s 1(1) sv ‘trust fund’ ........................................................................... 114

Contents—sections & subsections

24—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Section 1(1) sv ‘trustee’ .................................................................................. 117 ITA s 1(1) sv ‘trustee’ ................................................................................... 117

Section 1(1) sv ‘beneficiary’ .......................................................................... 118 ITA s 1(1) sv ‘beneficiary’ ............................................................................ 118 ITA s 1(1), preamble .................................................................................... 119 DELA s 1(1) sv ‘person’ ................................................................................. 123 ITA s 1(1) sv ‘person’ ................................................................................... 123 M&PRRA s 1(1) sv ‘person’ .......................................................................... 123 STTA s 1 sv ‘person’ ...................................................................................... 123 TDA s 1(1) sv ‘person’ .................................................................................. 123 VATA s 1(1) sv ‘person’ ................................................................................ 123 ITA s 1(1) sv ‘taxpayer’ ................................................................................ 124 VATA s 1(1) sv ‘vendor’ ............................................................................... 124 VATA s 7(1) ................................................................................................... 124 TDA s 2(1), extract ........................................................................................ 125 ITA s 61(a) .................................................................................................... 125 ITA 4th Sch para 1 sv ‘employer’ ................................................................ 126 VATA s 46(i).................................................................................................. 126 TDA s 3(1B) .................................................................................................. 127 ITA s 25D(3) ................................................................................................. 128

Section 1(1) sv ‘representative taxpayer’ ....................................................... 129 ITA s 1(1) sv ‘representative taxpayer’ ......................................................... 129 ITA s 1(1) sv ‘representative taxpayer’, para (c) ........................................... 130 ITA s 1(1) sv ‘representative taxpayer’, para (b) ........................................... 130 ITA s 1(1) sv ‘trustee’ ................................................................................... 130 ITA s 1(1) sv ‘income’ .................................................................................. 131 ITA s 1(1) sv ‘representative taxpayer’, proviso ........................................... 131 ITA s 1(1) sv ‘representative taxpayer’, partially rewritten ........................... 132 ITA s 61 ......................................................................................................... 132 ITA s 56(1)(l) ................................................................................................. 133

Paragraph 13(7), 4th Sch ................................................................................. 133 ITA 4th Sch para 13(7) ................................................................................... 133 TAA s 1 sv ‘taxpayer’ .................................................................................... 135 TAA s 151 ...................................................................................................... 135 TAA s 152 ...................................................................................................... 135 TAA s 1 sv ‘representative taxpayer’ ............................................................. 136 TAA s 153(1) ................................................................................................. 136 ITA s 1(1) sv ‘representative taxpayer’ ......................................................... 137 ITA 4th Sch para 1 sv ‘representative employer’ ........................................... 138 VATA s 46 ..................................................................................................... 138 TAA s 23 ........................................................................................................ 140 TAA s 234(a) ................................................................................................. 141 TAA s 234(b) ................................................................................................. 141 TAA s 153(2) ................................................................................................. 141 TAA s 153(3) ................................................................................................. 142 TAA s 154(1) ................................................................................................. 142 TAA s 154(2) ................................................................................................. 143 TAA s 1 sv ‘tax debt’ ..................................................................................... 144 TAA s 169(1) ................................................................................................. 144 ITA s 1(1) sv ‘representative taxpayer’, proviso ........................................... 144

Contents—sections & subsections

25—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

TAA s 155 ...................................................................................................... 145 TAA s 169(2) ................................................................................................. 145 TAA s 1 sv ‘tax debt’ ..................................................................................... 146 TAA s 169(1) ................................................................................................. 146

Section 1(1) sv ‘special trust’ ......................................................................... 151 ITA s 1(1) sv ‘special trust’ ........................................................................... 151 ITA s 6B(1) sv ‘disability’ ............................................................................. 152 ITA s 1(1) sv ‘relative’ .................................................................................. 152 ITA s 9D(2A)(f) ............................................................................................. 155 ITA s 18A(1) ................................................................................................. 156 ITA s 18A(3A) .............................................................................................. 156 ITA s 37D(1), preamble ................................................................................. 156 ITA s 37D(2) ................................................................................................. 156 ITA 8th Sch para 1 sv ‘special trust’ .............................................................. 157 ITA 8th Sch para 5 ......................................................................................... 157 ITA 8th Sch para 6 ......................................................................................... 158 ITA 8th Sch para 7 ......................................................................................... 158 ITA 8th Sch para 10 ....................................................................................... 158 ITA 8th Sch para 44, preamble ....................................................................... 159 ITA 8th Sch para 44 sv ‘primary residence .................................................... 159 ITA 8th Sch para 45 ....................................................................................... 159 ITA 8th Sch para 47 ....................................................................................... 160 ITA 8th Sch para 48 ....................................................................................... 160 ITA 8th Sch para 49 ....................................................................................... 160 ITA 8th Sch para 50 ....................................................................................... 161 ITA 8th Sch para 53 ....................................................................................... 161 ITA 8th Sch para 59 ....................................................................................... 162 ITA 8th Sch para 82 ....................................................................................... 162 ITA 4th Sch para 1 sv ‘personal service provider’ ......................................... 167 ITA s 1(1) sv ‘gross income’, preamble ........................................................ 169 ITA s 1(1) sv ‘gross income’, para (cA) ........................................................ 170 ITA s 11(cA) ................................................................................................. 170 ITA s 12E(4) .................................................................................................. 171 ITA s 23, preamble ........................................................................................ 172 ITA s 23(k) .................................................................................................... 172 ITA 4th Sch para 1, preamble ......................................................................... 173 ITA 4th Sch para 1 sv ‘employee’ .................................................................. 173 ITA 4th Sch para 2(1A) .................................................................................. 173 ITA 4th Sch para 11(a) ................................................................................... 174 ITA 6th Sch para 3 ......................................................................................... 174 ITA s 1(1) sv ‘income’ .................................................................................. 180 ITA s 1(1), preamble ..................................................................................... 182 ITA s 66(13B) ................................................................................................ 182 ITA s 20(2) .................................................................................................... 182 ITA s 103(2) ................................................................................................. 183 ITA S 1(1) sv ‘representative taxpayer’, proviso ........................................... 184 ITA s 1(1) sv ‘representative taxpayer’, para (c) ........................................... 184 ITA s 1(1) sv ‘capital gain’ .......................................................................... 184

Section 7(1) .................................................................................................... 185 ITA s 7(1) ...................................................................................................... 185

Contents—sections & subsections

26—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

ITA s 1(1) sv ‘income’ .................................................................................. 186 Section 7(2), (2A), (2B), (2C) ........................................................................ 187

ITA s 7(2) ...................................................................................................... 187 ITA s 7(2A) ................................................................................................... 188 ITA s 7(2B) ................................................................................................... 189 ITA s 7(2C) ................................................................................................... 189 ITA s 1(1) sv ‘taxable income’ ...................................................................... 192 CA s 17 .......................................................................................................... 193

Section 7(3), (4) .............................................................................................. 193 ITA s 7(3) ...................................................................................................... 193 ITA s 7(4) ...................................................................................................... 193

Section 7(5) .................................................................................................... 195 ITA s 7(5) ...................................................................................................... 195

Section 7(6) .................................................................................................... 196 ITA s 7(6) ...................................................................................................... 196

Section 7(7) .................................................................................................... 197 ITA s 7(7) ...................................................................................................... 197

Section 7(8) .................................................................................................... 199 ITA s 7(8)(a) .................................................................................................. 199 ITA s 7(8)(b) .................................................................................................. 199

Section 7(9), (10), (11) ................................................................................... 200 ITA s 7(9) ...................................................................................................... 200 ITA s 7(10) .................................................................................................... 200 ITA s 7(11) .................................................................................................... 201 PFA s 37D(1)(d), (e) .................................................................................... 202

Paragraph 68, 8th Sch ...................................................................................... 203 ITA 8th Sch para 68(1) ................................................................................... 203 ITA 8th Sch para 68(2 .................................................................................... 203

Paragraph 69, 8th Sch ...................................................................................... 205 ITA 8th Sch para 69 ........................................................................................ 205 CA s 17 .......................................................................................................... 206

Paragraph 70, 8th Sch ...................................................................................... 207 ITA 8th Sch para 70 ........................................................................................ 207

Paragraph 71, 8th Sch ...................................................................................... 208 ITA 8th Sch para 71 ........................................................................................ 208

Paragraph 72, 8th Sch ...................................................................................... 209 ITA 8th Sch para 72 ........................................................................................ 209 ITA 8th Sch para 73(2) ................................................................................... 211

Paragraph 73, 8th Sch ...................................................................................... 212 ITA 8th Sch para 73(1) ................................................................................... 212 ITA 8th Sch para 73(2) ................................................................................... 213 ITA s 1(1) sv ‘gross income’, preamble ........................................................ 218

Section 25B(1), (2) ......................................................................................... 221 ITA s 25B(1).................................................................................................. 221 ITA s 25B(2).................................................................................................. 221 ITA s 1(1) sv ‘representative taxpayer’, proviso ........................................... 223

Section 25B(3), (4), (5), (6), (7) ..................................................................... 223 ITA s 25B(3).................................................................................................. 223 ITA s 25B(4).................................................................................................. 223

Contents—sections & subsections

27—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

ITA s 25B(5) ................................................................................................. 223 ITA s 25B(6) ................................................................................................. 224 ITA s 25B(7) ................................................................................................. 224 ITA 8th Sch para 2(1) ..................................................................................... 226 ITA s 26A ...................................................................................................... 226 ITA 8th Sch para 11(1)(d) .............................................................................. 227

Paragraph 80, 8th Sch ...................................................................................... 229 ITA 8th Sch para 80(1) ................................................................................... 229 ITA 8th Sch para 80(2) ................................................................................... 229 ITA s 1(1) sv ‘gross income’, para (a) .......................................................... 236 ITA s 10(2) .................................................................................................... 236 ITA s 20(2A) ................................................................................................. 237 ITA 8th Sch para 11(1)(d) .............................................................................. 238 ITA s 1(1) sv ‘trading stock’ ........................................................................ 239 ITA 8th Sch para 1 sv ‘value shifting arrangement’ ..................................... 242 ITA 8th Sch para 11(1)(g) .............................................................................. 242 ITA 8th Sch para 37 ....................................................................................... 242 ITA s 1(1) sv ‘resident’, extract ..................................................................... 245

Section 25B(2A) ............................................................................................. 248 ITA s 25B(2A)............................................................................................... 248

Paragraph 80(3), 8th Sch ................................................................................. 252 ITA 8th Sch para 80(3) ................................................................................... 252 TPCA s 9(1) ................................................................................................... 254 TPCA s 9(2) ................................................................................................... 254 ITA s 55(1) sv ‘donation’ ............................................................................. 269 ITA s 58(1) ................................................................................................... 269 ITA s 55(1), preamble .................................................................................. 275 ITA s 55(1) sv ‘donation’ ............................................................................. 276 ITA s 56(1)(l) ................................................................................................ 276 ITA s 64D sv ‘beneficial owner’ ................................................................... 276 GN 506 GG 37767 of 25 June 2014 para 1 .................................................... 277 ITA 4th Sch para 15(1) ................................................................................... 279 ITA 4th Sch para 1 sv ‘employee’, extract ..................................................... 279 ITA 7th Sch para 1 sv ‘associated institution’ ................................................ 281 ITA 7th Sch para 16 ....................................................................................... 281

28—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

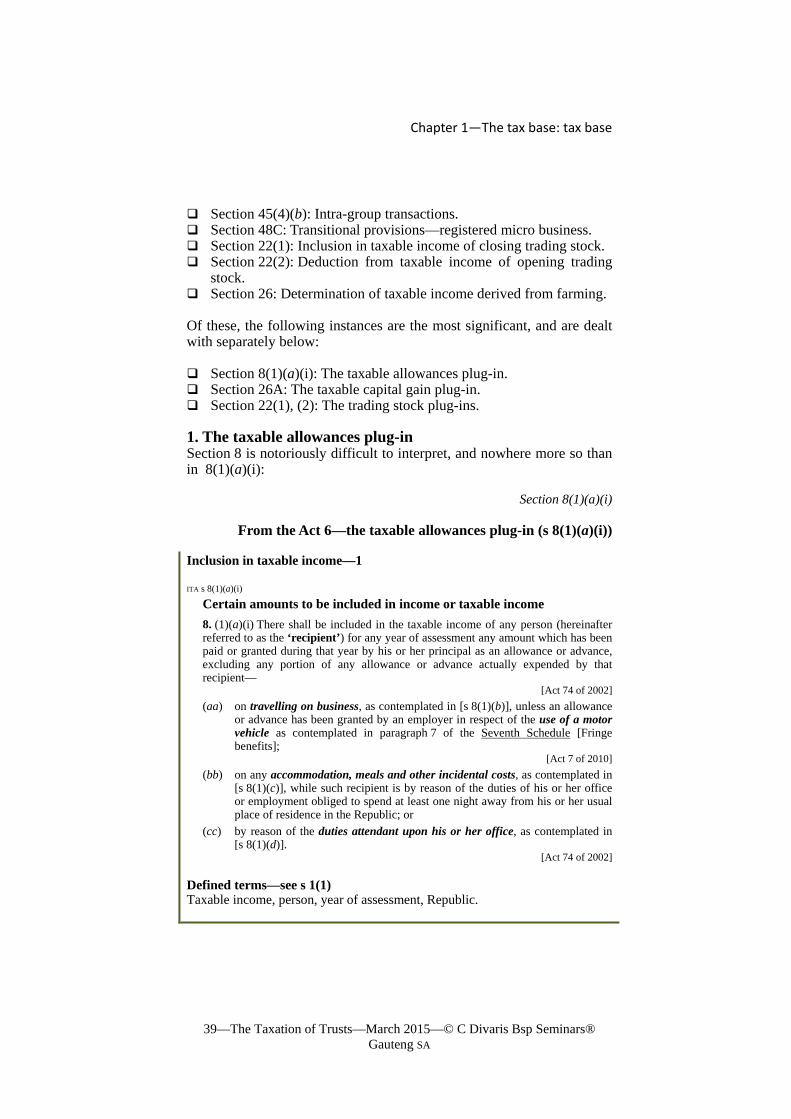

Chapter 1—The tax base: charging provision

29—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

CHAPTER 1

The tax base

Normal tax: the charging provision

What is ‘normal tax’? After generations of being the subject-matter of a hidden definition in s 5(1) of the Income Tax Act, ‘normal tax’ is now the subject-matter of a truly silly place-keeping definition in s 1(1):

Section 1(1) sv ‘normal tax’, s 5(1)

From the Act 1—‘normal tax’ (ss 1(1), 5(1))

Definition

ITA s 1(1) sv ‘normal tax’

‘[N]ormal tax’ means income tax referred to in section 5(1); [Act 28 of 2011]

Normal tax: the charging provision

ITA s 5(1)

Levy of normal tax and rates thereof 5. (1) Subject to the provisions of the Fourth Schedule [PAYE and provisional tax]

there shall be paid annually for the benefit of the National Revenue Fund, an income tax (in this Act referred to as the normal tax) in respect of the taxable income received by or accrued to or in favour of—

(a) …[Deleted.]; [Act 30 of 2002]

(b) …[Deleted.]; [Act45 of 2003]

(c) any person (other than a company) during the year of assessment ended the last day of February each year; and

[Act 45 of 2003] (d) any company during every financial year of such company.

[Act 103 of 1976]

Defined terms—see s 1(1) Tax, this Act, normal tax, taxable income, person, company, year of assessment, financial year.

Chapter 1—The tax base: charging provision

30—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Commentary 1—ss 1(1), 5(1): significance of ‘normal tax’

Normal tax as income tax The first absurdity is that s 1(1) defines ‘normal tax’ as the income tax referred to in s 5(1), which provides for an income tax to be known as the normal tax! Why is it necessary to refer to income tax?

Then the characterization by these provisions of the normal tax as an income tax is needlessly confusing, especially since, with the advent of the so-called capital gains tax (CGT), income must be taken in an economist’s sense, of any increment to wealth, whether of a revenue or a capital nature. Most taxpayers refer rather to income tax in contradistinction to the capital gains tax, but, in fact, there are no such taxes; there is only the normal tax. Nevertheless, there is a real difference between effective rates of normal tax under the so-called income tax system and effective rates under the so-called capital gains tax system.

And, popular usage notwithstanding, the proper term for the tax imposed by s 5(1), the formal charging provision, is the ‘normal tax’, no matter what its components.

The subject to clause In the typical arse-about-face drafting style of fiscal statutes, s 5(1) commences with the reservation Subject to the provisions of the Fourth Schedule. In their classical application, such subject-to clauses render the provision in which they appear subservient or subordinate to the cross-referenced provision (97 TSH 2011). In this application, what the subject-to clause signifies is that the subordinate rule is that normal tax is to be paid annually. For the dominant rule, see the Fourth Schedule to the Income Tax Act and its PAYE and provisional tax payment rules. In fact, though, PAYE and provisional tax are separate taxes in their own right (43 TAW 2014).

Normal tax and the rebates A huge deficiency of the definition of ‘normal tax’ is that it fails to make any reference to the rebates. Because these, in their terms, are deductible from the normal tax payable, it is submitted that the true meaning of ‘normal tax’ is the amount remaining after the deduction of all deductible rebates. Thus, on the several occasions on which the act refers to the normal tax chargeable—for example, in the First Schedule to the act, on the computation of taxable income derived from pastoral, agricultural or other farming operations—what is indicated is the net normal tax payable after deduction of all rebates. The point is made explicit in para 20 of the Fourth Schedule, relating to the provisional tax (which refers to the normal tax payable rather than the normal tax chargeable).

What follow are all those parts of the normal tax rebates providing for their deduction from normal tax:

ITA s 6(1)

Normal tax rebates 6. (1) There shall be deducted from the normal tax payable by any natural person,

other than normal tax in respect of any retirement fund lump sum benefit, retirement

Chapter 1—The tax base: charging provision

31—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

fund lump sum withdrawal benefit or severance benefit, an amount equal to the sum of the amounts allowed to the taxpayer by way of rebates under [s 6(2)].

[Act 24 of 2011]

ITA s 6A(1)

Medical scheme fees tax credit 6A. (1) A rebate, to be known as the medical scheme fees tax credit, must be

deducted from the normal tax payable by a person who is a natural person. [Act 31 of 2013]

ITA s 6B(2)

(2) A rebate, to be known as the additional medical expenses tax credit, must be deducted from the normal tax payable by a person who is a natural person.

[Act 22 of 2012]

ITA s 6quat(1), extract

Rebate or deduction in respect of foreign taxes on income 6quat. (1) Subject to [s6 quat(2)], where the taxable income of any resident during a

year of assessment includes— …, there must be deducted from the normal tax payable in respect of that taxable income

a rebate determined in accordance with this section. [Act 24 of 2011]

ITA s 6quin(1), extract

Rebate in respect of foreign taxes on income from source within Republic

6quin. (1) Subject to subsections (3) and (3A), where any portion of the taxable income of a resident is attributable to an amount that is from a source within the Republic and is received by or accrued to that resident in respect of services rendered within the Republic, and an amount of tax in respect of that amount is—

…, a rebate determined in accordance with [s 6quin(2)] must be deducted from the

normal tax payable by that resident. [Act 22 of 2012]

There is one further rebate to be found in the act but it is deductible not from normal tax but the dividends tax payable:

ita s 64N(1)

Rebate in respect of foreign taxes on dividends 64N. (1) A rebate determined in accordance with this section must be deducted from

the dividends tax payable in respect of a dividend contemplated in paragraph (b) of the definition of ‘dividend’ in section 64D.

[Act 17 of 2009]

Annually means during the year of assessment Although s 5(1) ostensibly imposes the normal tax annually, that term is made precise by the references in s 5(1)(c) to the year of assessment of persons other than companies—referred to here as unincorporated persons—and in s 5(1)(d)

Chapter 1—The tax base: charging provision

32—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

to the year of assessment of companies.

Drafting error Sadly, the draftsperson of the formal (albeit place-keeping) definition of ‘normal tax’ missed the opportunity of separating definitional from substantive provisions, leaving it to the user to do the work for which the draftsperson alone was paid. To add to the confusion, s 5 as a whole is hopelessly confused in its terminology, referring to tax paid, charged and assessed, all of which signify the imposition of a tax. Since s 5 is technically known as a charging provision, perhaps the imposition of a tax is best referred to as the charging of that tax.

On this basis, what s 5(1) achieves, in its substantive role, is to charge all persons (comprising persons other than companies and companies) with a liability for the normal tax upon an annual basis, the tax base being the taxable income derived by (a very common elegant variation for received by or accrued to or in favour of, to be found throughout the act) such persons annually.

And, at the definitional level, the normal tax is the tax charged by s 5(1).

Section 1(1) sv ‘year of assessment’

From the Act 2—‘year of assessment’ (s 1(1))

Definition

ITA s 1(1) sv ‘year of assessment’

‘[Y]ear of assessment’ means any year or other period in respect of which any tax or duty leviable under this Act is chargeable, and any reference in this Act to any year of assessment ending the last or the twenty-eighth or the twenty-ninth day of February shall, unless the context otherwise indicates, in the case of a company or a portfolio of a collective investment scheme in securities be construed as a reference to any financial year of that company or portfolio ending during the calendar year in question.

[Act 17 of 2009

Defined terms—see s 1(1) Tax, this Act, year of assessment, company, financial year.

Commentary 2—ss 1(1), 5(1): significance of ‘year of assessment’

Years of assessment The definition of ‘year of assessment’ caters for broken periods of less than a year and maps February year-ends on to calendar years for the benefit of a company and a portfolio of a collective investment scheme in securities.

While companies thus generally have years of assessment coincident with their financial years, unincorporated persons are compelled by s 5(1) generally to have years of assessment ending on the last day of February each year.

Chapter 1—The tax base: tax base

33—The Taxation of Trusts—March 2015—© C Divaris Bsp Seminars® Gauteng SA

Normal tax: the tax base