the uk balance of payments rgs newcastle economics department

TRANSCRIPT

The UK Balance of Payments

RGS Newcastle Economics Department

The Balance of Payments

• BOP records all financial transactions between the UK & the Rest of the World

• The UK is an open economy which – trades both goods and services – is open to inflows and outflows of financial

capital and fixed capital investment

• BOP measures the extent to which the UK is “paying its way” with other countries

Trade in goods (visible trade)

• Consumer durables

• Capital goods / techology /software

• Commodities (including mineral fuels)

• Components & basic raw materials

• Foodstuffs and Beverages

• Semi-finished manufactured products

International Trade in Services

• Tourism• Travel / Civil Aviation• Insurance• Consultancy• Banking services• Accountancy services

• Data processing• Information services• Music &

Entertainment• Shipping• Educational services

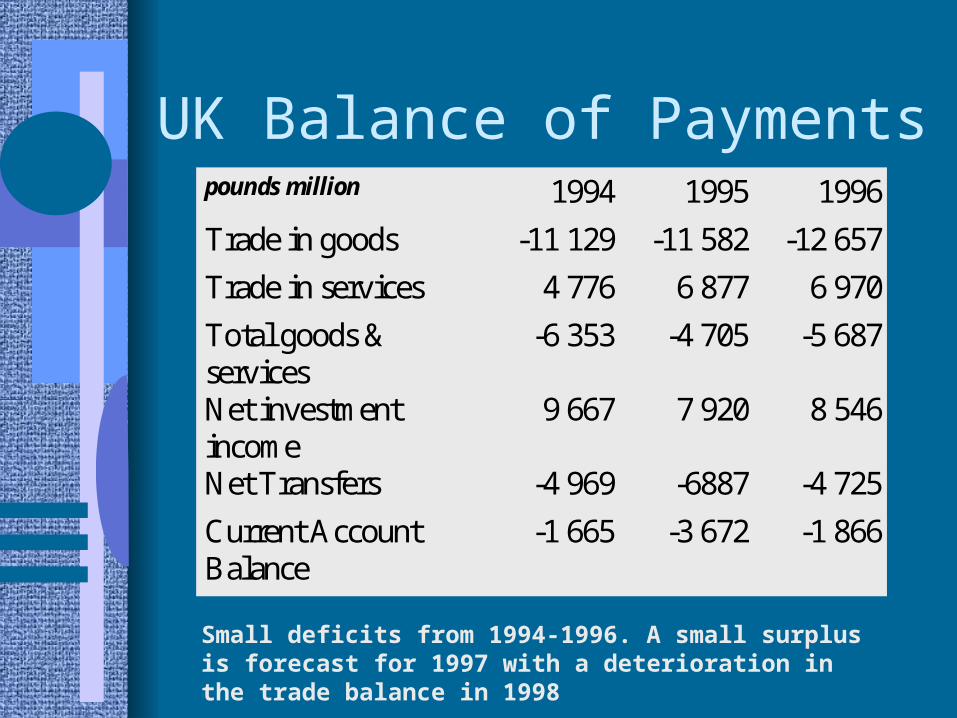

UK Balance of Paymentspounds million 1994 1995 1996

Trade in goods -11 129 -11 582 -12 657

Trade in services 4 776 6 877 6 970

Total goods &services

-6 353 -4 705 -5 687

Net investmentincome

9 667 7 920 8 546

Net Transfers -4 969 -6887 -4 725

Current AccountBalance

-1 665 -3 672 -1 866

Small deficits from 1994-1996. A small surplus is forecast for 1997 with a deterioration in the trade balance in 1998

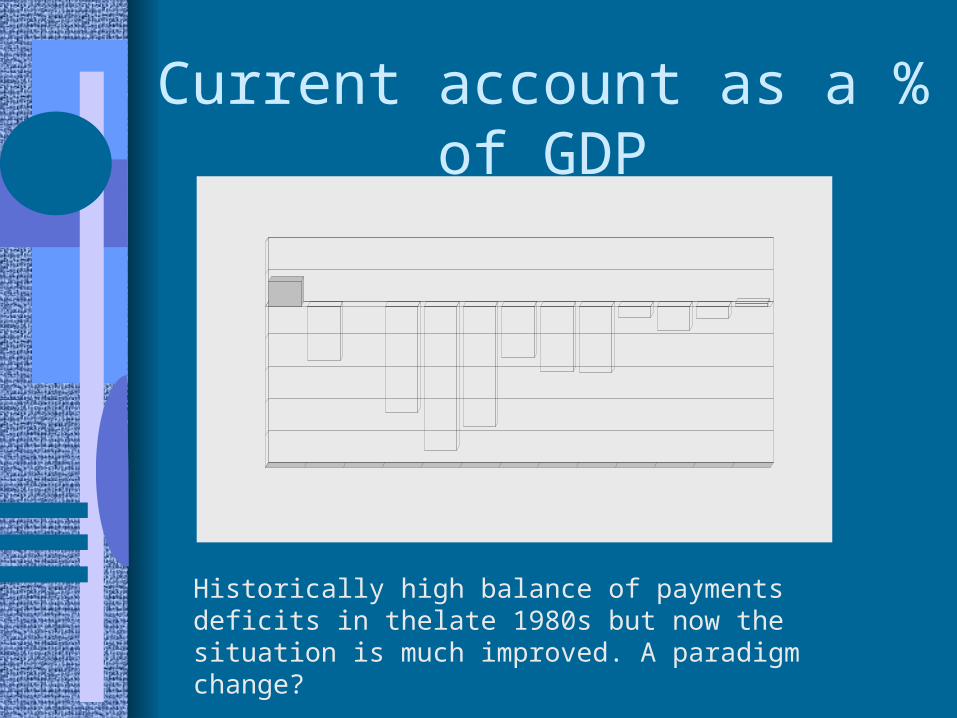

Current account as a % of GDP

80-84 av85-89 av 88

8990

9192

9394

9596

97

1997 figure is a third quarter forecast

-25

-20

-15

-10

-5

0

5

10

billi

on p

ound

sUK CURRENT ACCOUNT BALANCE

Historically high balance of payments deficits in thelate 1980s but now the situation is much improved. A paradigm change?

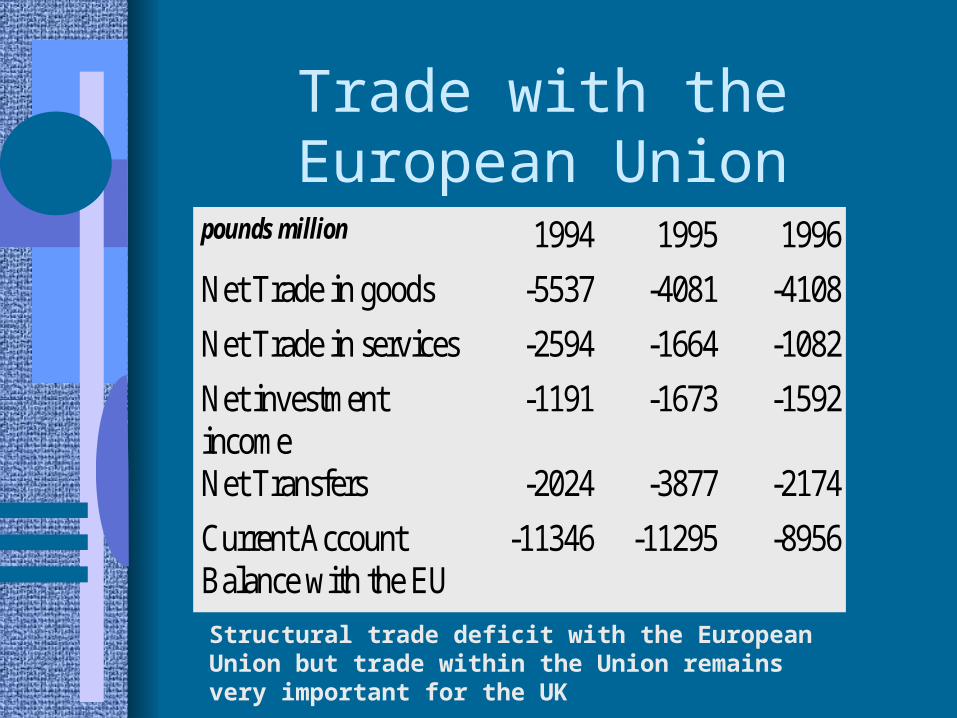

Trade with the European Union

pounds million 1994 1995 1996

Net Trade in goods -5537 -4081 -4108

Net Trade in services -2594 -1664 -1082

Net investmentincome

-1191 -1673 -1592

Net Transfers -2024 -3877 -2174

Current AccountBalance with the EU

-11346 -11295 -8956

Structural trade deficit with the European Union but trade within the Union remains very important for the UK

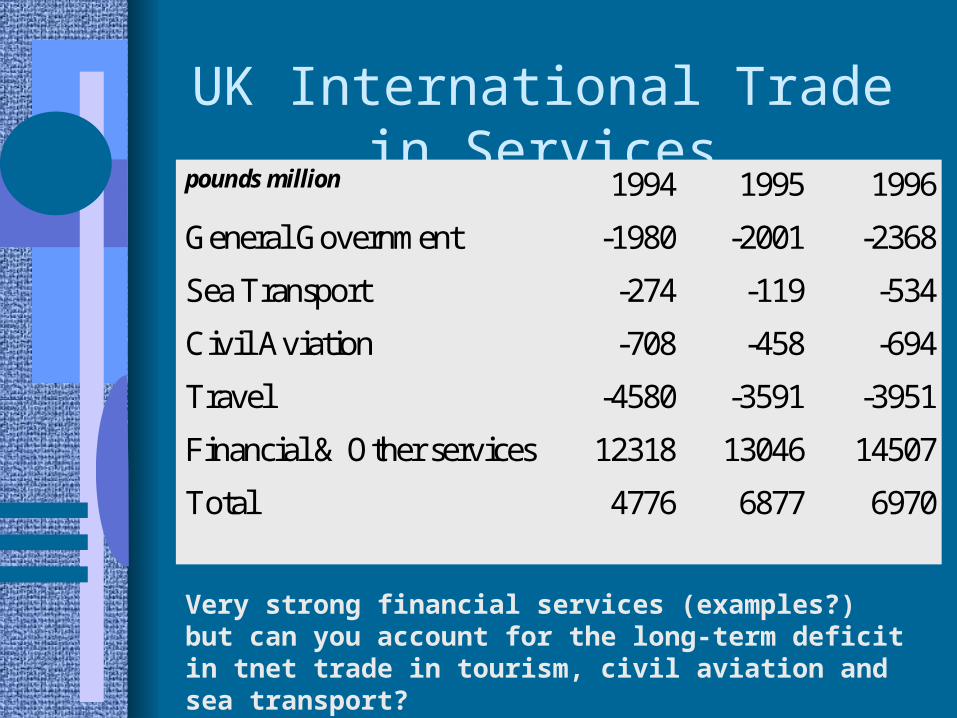

UK International Trade in Servicespounds million 1994 1995 1996

General Government -1980 -2001 -2368

Sea Transport -274 -119 -534

Civil Aviation -708 -458 -694

Travel -4580 -3591 -3951

Financial & Other services 12318 13046 14507

Total 4776 6877 6970

Very strong financial services (examples?) but can you account for the long-term deficit in tnet trade in tourism, civil aviation and sea transport?

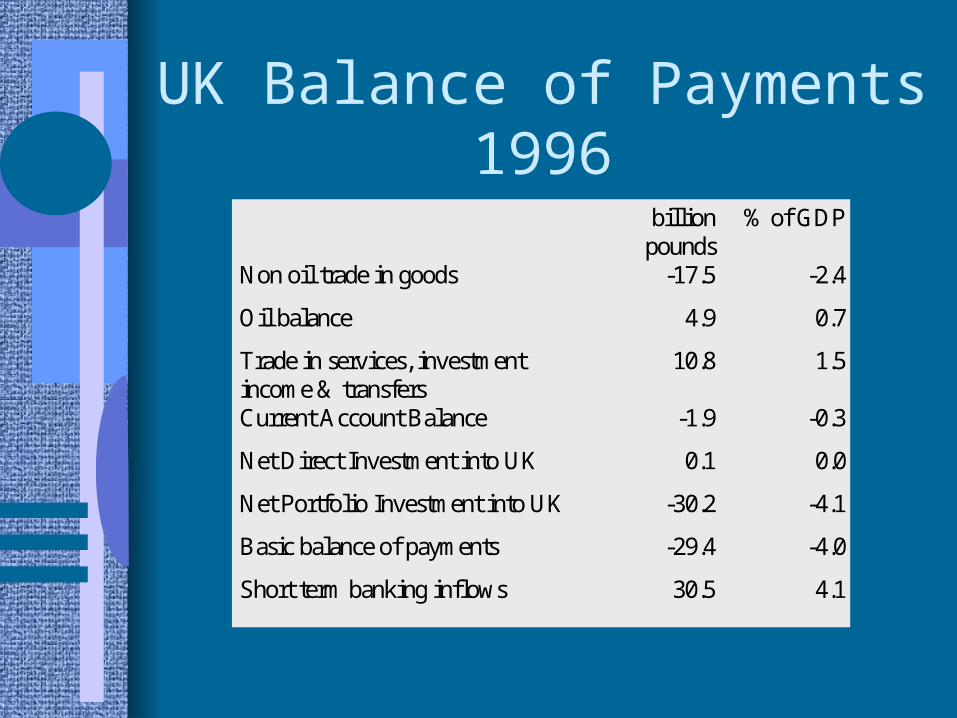

UK Balance of Payments 1996

billionpounds

% of GDP

Non oil trade in goods -17.5 -2.4

Oil balance 4.9 0.7

Trade in services, investmentincome & transfers

10.8 1.5

Current Account Balance -1.9 -0.3

Net Direct Investment into UK 0.1 0.0

Net Portfolio Investment into UK -30.2 -4.1

Basic balance of payments -29.4 -4.0

Short term banking inflows 30.5 4.1

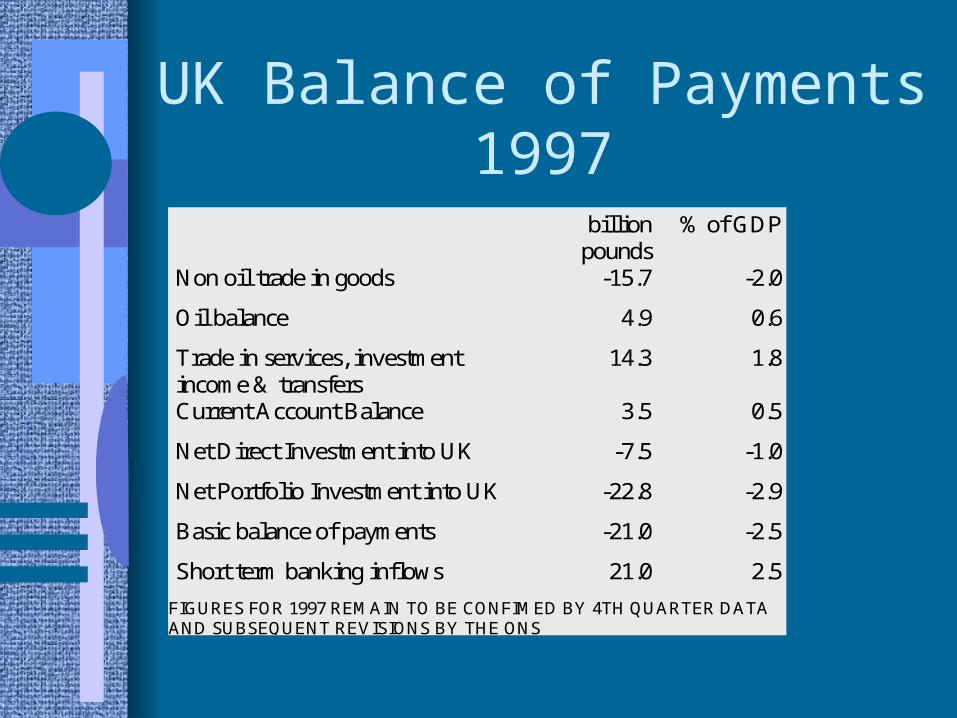

UK Balance of Payments 1997

billionpounds

% of GDP

Non oil trade in goods -15.7 -2.0

Oil balance 4.9 0.6

Trade in services, investmentincome & transfers

14.3 1.8

Current Account Balance 3.5 0.5

Net Direct Investment into UK -7.5 -1.0

Net Portfolio Investment into UK -22.8 -2.9

Basic balance of payments -21.0 -2.5

Short term banking inflows 21.0 2.5

FIGURES FOR 1997 REMAIN TO BE CONFIMED BY 4TH QUARTER DATAAND SUBSEQUENT REVISIONS BY THE ONS

Composition of UK exports of goods% of total exports 1960 1969 1979 1995

Food, beverages &tobacco

5 6 7 7

Basic materials 4 4 3 2

Mineral fuels 4 2 11 6

Manufactured goods 84 85 76 84

(Semi manufacturedgoods)

(36) (35) (31) (28)

(Finishedmanufactured goods)

(48) (50) (45) (55)

Note the importance of exporting finished manufacturing goods and the impact of north sea oil from the mid 1970s

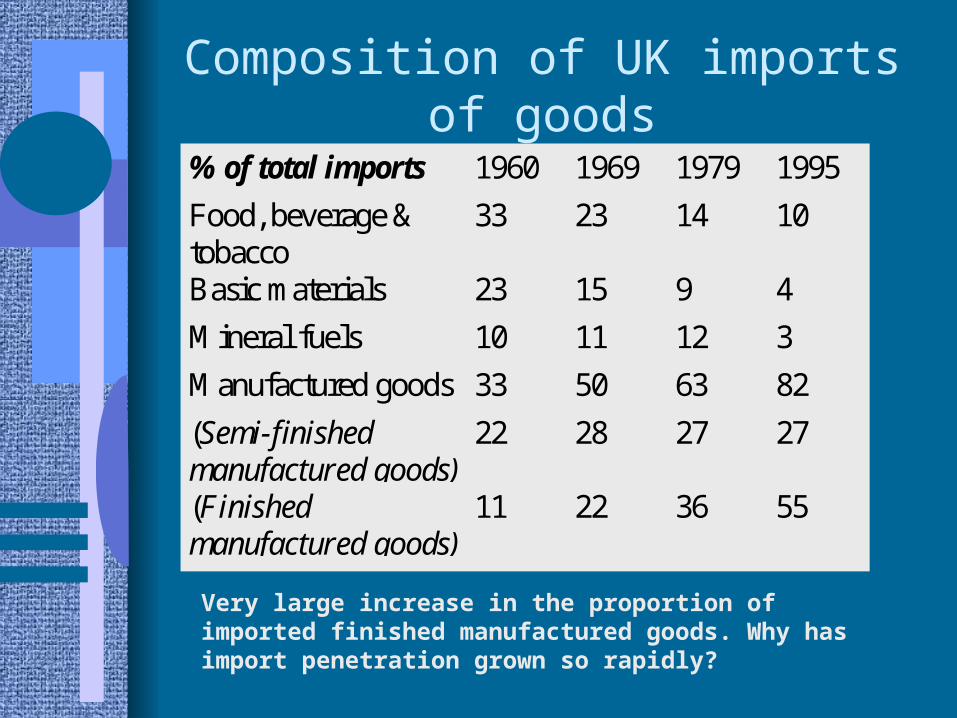

Composition of UK imports of goods

% of total imports 1960 1969 1979 1995

Food, beverage &tobacco

33 23 14 10

Basic materials 23 15 9 4

Mineral fuels 10 11 12 3

Manufactured goods 33 50 63 82

(Semi-finishedmanufactured goods)

22 28 27 27

(Finishedmanufactured goods)

11 22 36 55

Very large increase in the proportion of imported finished manufactured goods. Why has import penetration grown so rapidly?

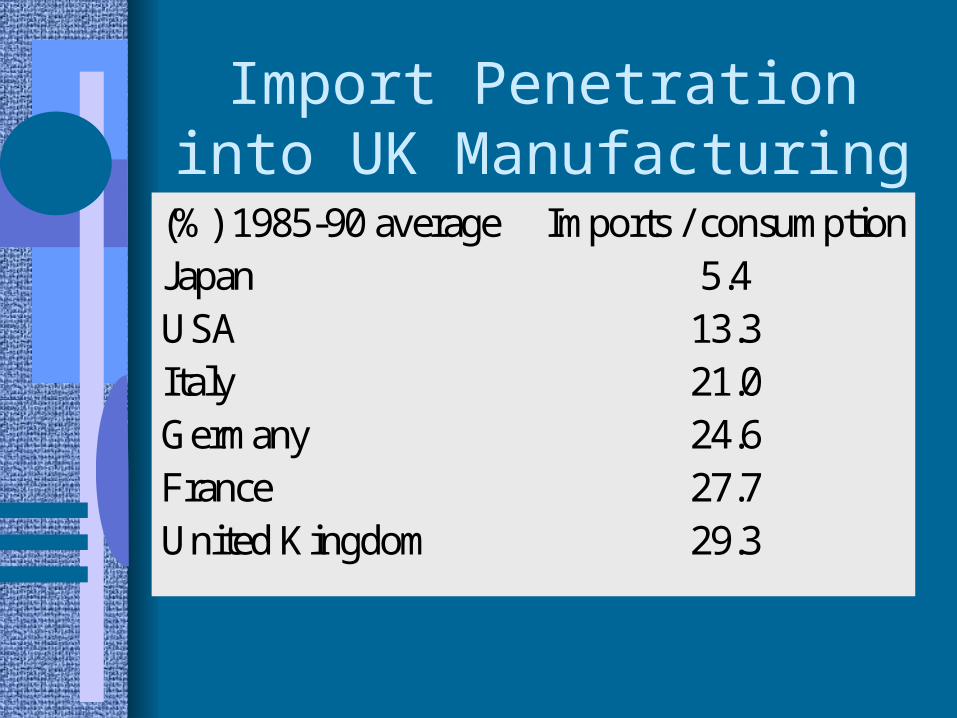

Import Penetration into UK Manufacturing

(%) 1985-90 average Imports / consumptionJapan 5.4USA 13.3Italy 21.0Germany 24.6France 27.7United Kingdom 29.3

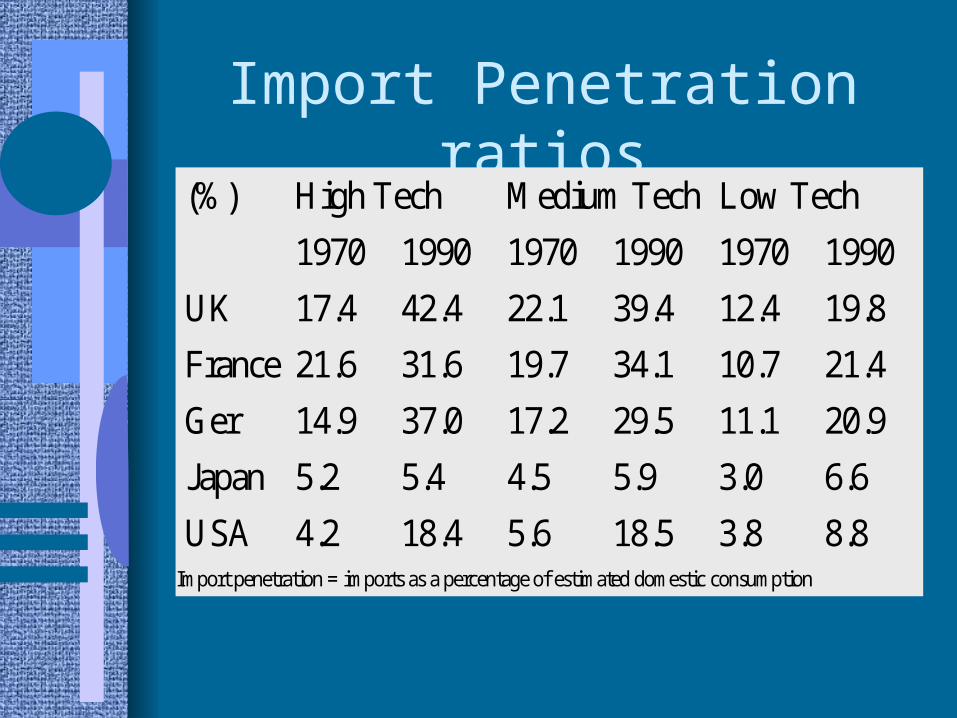

Import Penetration ratios(%) High Tech Medium Tech Low Tech

1970 1990 1970 1990 1970 1990

UK 17.4 42.4 22.1 39.4 12.4 19.8

France 21.6 31.6 19.7 34.1 10.7 21.4

Ger 14.9 37.0 17.2 29.5 11.1 20.9

Japan 5.2 5.4 4.5 5.9 3.0 6.6

USA 4.2 18.4 5.6 18.5 3.8 8.8Import penetration = imports as a percentage of estimated domestic consumption

Export market shares(%) High Tech Medium Tech Low Tech

1970 1990 1970 1990 1970 1990

UK 10.5 10.2 11.9 8.5 8.9 8.5

France 7.7 8.7 8.5 10.0 10.7 12.1

Ger 17.7 16.2 23.1 24.7 15.0 17.9

Japan 13.2 21.1 8.5 16.9 13.2 7.1

USA 31.1 26.3 21.7 15.4 13.4 13.3Export market share for each country as a % of total exports

Causes of a BOP deficit

• Important to distinguish between – cyclical factors affecting import & export demand– structural factors (see later)– impact of “external shocks” (e.g. Asian Flu or the

OPEC oil crises)

• Could also take a– short/medium term– long term approach

Short-medium term factors behind a payments deficit

• Deficit normally emerges because of– fast growth of domestic demand– high MPM / Yed for imports– capacity constraints in domestic economy– decisions by the private sector to move into

financial deficit– changes in the exchange rate– impact of external shocks for open economies

Long-run explanations

• Structural weaknesses in the traded goods sector of the economy– insufficient productive capacity– lack of cost and & price competitiveness– inadequate non-price competitiveness

• Changing comparative advantage in the global economy (increasing competition)

• Overvalued exchange rates not reflecting price differentials?

• Long run decline in certain key sectors

Policies to correct a BOP deficit

• Cyclical deficit tends to be self-correcting

• Lower exchange rate will also help to improve the trade balance

• Policies focus either on– expenditure-reduction

– expenditure-switching

• Structural trade deficits may take many years to eliminate

• Focus in long run needed on improving the supply-side performance of the economy

Summary of policies

Expenditure reduction

• deflationary fiscal policies

• tightening of domestic monetary policy

Structural change• supply-side reforms• export promotion

Expenditure switching

• devaluation / depreciation of exchange rate

• tariffs and other import controls

• achieving period of low relative inflation

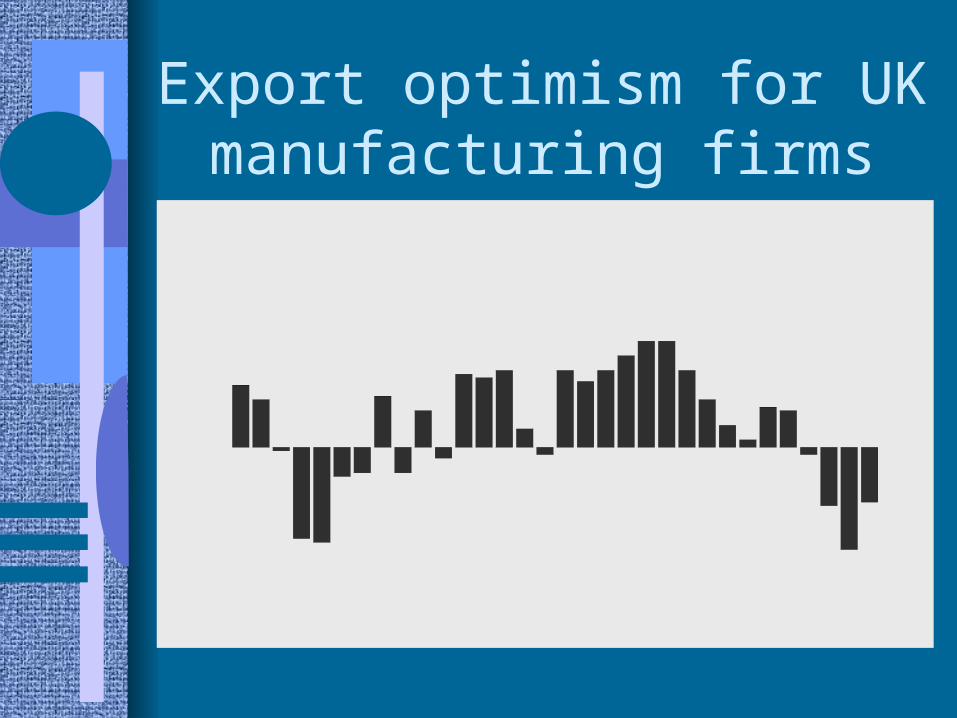

Export optimism for UK manufacturing firms

90Q13

91Q13

92Q13

93Q13

94Q13

95Q13

96Q13

97Q13

-40

-30

-20

-10

0

10

20

30

40

Net

Bal

ance

of

resp

on

den

ts

MANUFACTURING EXPORT OPTIMISMAre you more or less optimistic about export order books in the next six

months?

94Q

1 2 3 495

Q1 2 3 4

96Q

1 2 3 497

Q1 2 3 4

-4

-3

-2

-1

0

1T

hous

ands

TR

AD

E B

ALA

NC

E (

mill

ion

poun

ds)

80

85

90

95

100

105

EX

CH

AN

GE

RA

TE

IND

EX

(19

90=

100)

Trade Balance (LHS)

Sterling Index (RHS)

UK TRADE & THE STERLING EXCHANGE RATE

Exchange rate and trade balances