the value of barbados’ fisheries: a preliminary assessment

TRANSCRIPT

Barbados Fisheries Management Plan, Public Information Document No. 2 FMP-PID-2

THE VALUE

OF BARBADOS’ FISHERIES:

A preliminary assessment

Environmental Special Projects Unit

Ministry of Energy and theEnvironment

Fisheries Division

Ministry of Agriculture and RuralDevelopment

Centre for Resource Managementand Environmental Studies

University of the West Indies

August 2007

THE VALUE

OF BARBADOS’ FISHERIES:

A preliminary assessment

By

Robin Mahon1

Christopher Parker2

Travis Sinckler3

Stephen Willoughby2

Julieann Johnson2

1 Centre for Resource Management and Environmental Studies, University of the WestIndies, Cave Hill Campus, Barbados2 Fisheries Division, Ministry of Agriculture and Rural Development, Hincks Street,Bridgetown, Barbados3 Environmental Special Projects Unit, Ministry of Energy and the Environment, #1 Sturges,St. Thomas, Barbados (recently established as the Natural Heritage Department at the sameaddress)

This booklet was prepared by the Centre for Resource Management and EnvironmentalStudies (CERMES), University of the West Indies, Cave Hill Campus, Barbados in

collaboration with the Fisheries Division, Ministry of Agriculture and Rural Developmentand the Environmental Special Projects Unit, Ministry of Energy and the Environment.

The funds were provided by the Environmental Special Projects Unit

It should be cited as:

Mahon R., C. Parker, T. Sinckler and S. Willoughby and J. Johnson. 2007. The value ofBarbados’ fisheries: a preliminary assessment. Fisheries Division, Ministry of Agricultureand Rural Development, Barbados, Fisheries Management Plan Public InformationDocument No. 2: 24 pp.

Photographs: Cover clockwise from top left - Cast netting on the west coast (© Corrie Scott), Flyingfishbagged for sale (Tanya Staskiewicz), Grilled fish at Maria’s in Oistins (Robin Mahon), Longliner (TanyaStaskiewicz), Pulling a seine on the west coast © Corrie Scott), Bajan fish filleted and vacuum packed in thesupermarket (Robin Mahon); cover centre - cleaning fish in Oistins Market (Tanya Staskiewicz); page 4 – theBridgetown Fisheries Complex (BFC) harbour (Robin Mahon); page 5 – Skeete’s Bay fishing site (RobinMahon); page 7 – retrieving a gill net and deboning flyingfish (Fisheries Division); page 8 – Bajan fish productsin a St. Vincent supermarket (Robin Mahon) and seafood processing business (Tanya Staskiewicz); page 9 –iceboats and longliners in the BFC harbour (Robin Mahon); page 11 – offloading tuna at the BFC (ChristopherParker); page 13 – blue marlin (Greg Franklin) and seafood restaurant (Robin Mahon); page 15 – steaking fishat Weston (Lara Schuhmann); page 17 – wahoo, back when fish were big (Dudley Wiles); page 21 – pot fishingon the west coast (© Corrie Scott) and potfishes (Fisheries Division).

ii

SUMMARYThe value assigned to fisheries in the national economy is often based on the ex-vessel valueof the fish landed. As the fish moves through various market pathways to the consumer, itincreases in value with each transaction, and contributes to livelihoods. This additional valueshould be accounted for in assigning an economic value to fisheries and in determining theappropriate investment in management. A preliminary assessment of this additional valuewas carried out for the major fisheries of Barbados by: determining the pathways along whichfish move from fisher to consumer, amounts moving on each path, and price increase at eachstep. Overall, additional value was about US$19 M, and was about 2.6 times the landed valueof the fishery. This ranged from about 7.4 times the landed value for flyingfish to zero for seaurchins. The distribution of this additional value among reseller groups varied from being68% for restaurants, 20% for processors/exporters, 8% for fish frys, 3% for vendors and <1%for supermarkets. These results underscore the need to value fishery products broadly,especially in a tourism economy where seafood is important mainstay of restaurants and fishfry operations.

CONTENTS

INTRODUCTION .....................................................................................................................1

HOW THE VALUATION WAS DONE...................................................................................2

THE TOTAL VALUE OF BARBADOS’ FISHERIES ............................................................3

VALUATIONS FOR SPECIES AND SPECIES GROUP........................................................5

Flyingfish ...............................................................................................................................6

Dolphinfish ............................................................................................................................8

Tuna .....................................................................................................................................10

Billfishes (including blue marlin) ........................................................................................12

Swordfish .............................................................................................................................14

Kingfish................................................................................................................................16

Snapper ................................................................................................................................18

Shark and barracuda.............................................................................................................19

Lobster .................................................................................................................................20

Reef fishes (potfish).............................................................................................................21

Jacks (seine fish) ..................................................................................................................22

Bonito...................................................................................................................................23

All others..............................................................................................................................23

NEXT STEPS ..........................................................................................................................24

FURTHER READING ............................................................................................................24

INTRODUCTIONFishing and fish have been an importantpart of Barbadian commerce and culturefrom the earliest recorded times (Welch2005). The fishing industry has gonethrough many changes, particularly theoffshore fleet. In the late 1950s, the fleetconverted from sail to motor. The ‘ice-boat’ emerged in the 1980s and increasedthe fishing range of the fleet. The 1990ssaw the appearance of longliners, whichnow number 30 or more. This offshorefleet, targeting flyingfish and largepelagics such as dolphinfish, tuna,billfishes, and kingfish (mainly wahoo),has been the mainstay of the industry. Fishcomplexes at Oistins, Bridgetown, ConsetBay and Skeetes Bay have been builtprimarily to serve its needs. A processingindustry has emerged to clean, cut andpackage these products for local andexport markets.

Though small, the inshore fisheries are noless a part of Barbados’ fishing culture.Sea eggs, reef fishes (pot fish), snappersand brims, jacks and sprats are keyexamples of the resources harvested fromthe island shelf and the deeper waters of itsslope. Less important, but nonethelesscontributing to the overall fishery picturefor Barbados are lobster, conch andseamoss. These inshore resources aretaken by a variety of fishing methods --diving, spearfishing, handlines, traps, castnets and seines nets among them. Theinshore fleet comprises a large number ofsmall open vessels (moses). For a fullerdescription of the Barbados fishingindustry see Willoughby and Leslie(2000).

Fishing adds much to Barbadian life. Itprovides an important and readilyavailable source of food of the highestquality. It also provides a means oflivelihood for many people. Those whocatch fish, sell fish, and process anddistribute fish are estimated to numbermore than 6,000. Those who cook and

serve fish, whether in exclusiverestaurants, at fish frys or the numerousrum shops across the island have not beencounted. They all owe their living, eitherin whole or in part to these resources.Numerous others make a living bysupporting the industry. Some build, selland maintain the boats, their engines andall the fishing and electronic equipmentthat they carry. Others sell and service thevehicles and equipment involved intransporting, processing and exportingfish.

The fishing industry is important in otherways as well. It provides an importantinput to the tourism industry. Flyingfish,dolphinfish, kingfish and tuna areperennial favourites with visitors.Recently, fish frys have emerged as amajor feature and attract large numbers oflocals and visitors. Fish exports are on theincrease, providing foreign revenue. Lastbut not least, when we consider the valueof the Barbadian fishing industry we musttake account of the colour and interest thatthe fishing industry adds to Barbadian lifeand culture. It fascinates locals and visitorsalike and inspires our artists. And there isthe Oistins Fish Festival.

Unfortunately, the true value of theBarbados fishing industry to the economyof Barbados has never been properlyassessed. Only the ex-vessel value of thefish landings is reflected under fisheries inthe GDP estimates of Barbados. Clearly,as fish passes from hand to hand alongvarious pathways and finally to consumerthere is considerable value added along theway. To obtain a true picture of themarket value of the fishing industry, thisadded value must be included.

In this report we make a preliminaryattempt to assess the added value by:

Identifying the pathways along whichfish and fish products flow.

2

Estimating the value and value addedof fish and fish products at each stagein each path.

Our findings are illuminating. The ex-vessel value turns out to be only 20% ofthe total value, when value added iscounted.

We re-emphasise that fisheries may alsohave considerable value in several otherways that this study has not explored.These include:

The value of the support services to thefishing industry;

The value of fishing and fish productsin attracting visitors to the island;

The value of fish as food inmaintaining the health of Barbadians,and thus educing health costs; or

The value of fisheries in the cultureand identity of Barbadians.

Each of these can be assessed usingappropriate methods. The value of theseshould be estimated as soon as possible.

HOW THE VALUATION WAS DONEThe steps were: (1) to construct for eachfishery type a diagram showing thepathways that fish follow from the fisherto the consumer; then (2) starting with thetotal estimated landings in each fisherytype, estimate the percentage that movesalong each pathway. This was doneseparately for each type of fishery becausein different types of fisheries, productsmay follow different pathways, or thesame pathways in different proportions.The average annual landings for the five-year period 1999 to 2003 were used in thisstudy.

Finally, the price that the fishery productwas sold for at each step along the pathwas estimated. The sale of fish from thefisherman to the first buyer provides thelanded or ex-vessel value of the fish. Ateach step after that, the difference betweenthe purchase price of the fish and itsselling price gives the price increase orvalue added. By multiplying the totalamount of fish by the value-added perkilogram, the total value added wasestimated. When fish was actuallyprocessed or changed form by cleaning,deboning or preparation for cooking a 20%loss figure was applied to account forunused parts.

The accuracy of the estimates of value is amatter of concern. Much of the

information required was available fromrecords at the Fisheries Division, or wasobtained from interviews with FisheriesDivision staff. The Fisheries Divisionroutinely collects information on totalamounts of fish landed and on sellingprices at major landing sites. Theirestimates of total landings by category arethe starting point for this valuation. Thisinformation was supplemented byconducting surveys of a variety of sourcesincluding: fish boners, scalers, vendors andhawkers, processors, restaurants andhotels, supermarkets and fish-fry vendors.Surveys were carried out on the south andwest coasts of the island, with three hotelsand five restaurants surveyed on eachcoast. The sample population was derivedfrom the hotels and restaurants catering toa broad base of clientele, i.e. local andforeign. Prices used are annual averages.These are known to vary seasonally, but itwas beyond the scope of this project toattempt a seasonal breakdown.

The estimate for sea urchins was derivedfrom data provided by McConney et al.(2003). It was based on estimated numbersof full-time and part-time fishers and theiraverage respective earnings per season asreported in a survey. Owing to problemswith willingness of fishers to provideinformation on earnings and uncertainty

3

regarding numbers, and designation ofpart-time and full-time status, this estimateis considered to be one of the least reliable.

Two types of fishery are missing from thisvaluation study, because the products areseldom sold in the regular market places.These are conch and small inshorepelagics called ‘sprats’. There are nosubstantial conch resources in Barbados,although conch can be found scattered

throughout the island shelf whereverappropriate habitats occur. When diversencounter these they are taken and soldlocally to known buyers or to restaurants.Sprats, likewise are sold locally toconsumers on the beach or as bait. Thereare no data for these fisheries from whichto develop estimates. Since most is solddirectly from fisher to consumer, thevalue-added is likely to be minimal.

THE TOTAL VALUE OF BARBADOS’ FISHERIESThis study shows that the total value of thefish landed in Barbados is considerablygreater than its ex-vessel value (Table 1).The value added component ranges from0% in the case of the ‘all others’ categoryto 88% of the total value in the case of

flyingfish. It is higher for offshorefisheries, the catch of which is processed,exported and is the main attraction at fishfrys and restaurants, than it is for inshorefisheries, the catch of which is most oftensold directly to consumers.

Table 1. The value added for different fisheries (BDS$)

Fish Type Ex-vessel value Value added

(% of total)

Overall value

Flyingfish 3,588,498 26,648,676 (88) 30,237,174

Dolphinfish 5,005,384 6,002,346 (55) 11,007,731

Tuna 1,402,850 2,435,389 (63) 3,838,239

Billfishes 615,609 654,605 (52) 1,270,214

Swordfish 193,043 123,037 (390 316,080

Kingfish 266,918 184,283 (410 451,201

Subtotal - offshore 11,072,302 36,048,336 (77) 47,120,638

Snappers 164,301 245,929 (60) 410,229

Shark and barracuda 89,441 84,633 (49) 174,074

Lobster 7,867 7,775 (50) 15,642

Jacks 59,252 33,796 (36) 93,048

Bonito 9,771 9,369 (49) 19,139

Reef fishes 89,314 56,056 (39) 145,370

Sea eggs 2,775,000 0 (0) 2,775,000

All others 402,095 57,780 (13) 459,875

Subtotal - coastal 3,597,041 495,338 (12) 4,092,379

Total 14,669,343 36,543,674 (71) 51,213,017

When the value-added is broken outaccording to who sells the fish and towhom, it shows that the majority of theadditional value is derived from sale ofcooked fish to consumers in restaurants

and at fish frys (Table 2). Vendors andprocessors (however) generate appreciableamounts of additional values as theytransport, clean and market fish.

3

Table 2. The value added by different sellers according tocategory of buyer (BDS$).

Seller Buyer Value added($BDS)

(%)

Vendor Consumer 464,399 1.3

Fish fry 189,494 0.5

Restaurant 525,350 1.4

Subtotal 1,179,243 3.2

Processor Consumer 383,866 1.1

Export 1,583,735 4.3

Fish fry 182,915 0.5

Restaurant 4,638,553 12.7

Supermarket 490,337 1.3

Subtotal 7,279,406 19.9

Restaurant Consumer 24,819,781 67.9

Fish fry Consumer 3,118,813 8.5

Subtotal 27,938,595 76.5

Supermarket Consumer 146,430 0.4

5

VALUATIONS FOR SPECIES AND SPECIES GROUPThe results of the survey are displayed inthe form of path diagrams and value addedtables for each species or fishery group.

In the path diagrams, the percentages offish moving from each seller to the variousbuyers are shown. A dashed line is used toindicate path transactions in which the20% loss factor due to cleaning orprocessing was applied. The pathway fromexport to consumer is included forcompleteness, but no value added isestimated for this path.

The value added table for each species orgroup shows the actual quantities andprices of fish as it passes from one form toanother and one path component toanother.

Flyingfish and large pelagics had the mostcomplex pathways, often involving export.Coastal resources that were most oftensold directly to consumers had the simplestpathways.

6

Flyingfish

Flyingfish is the mainstay of the fishingindustry, comprising about 63% of thelandings. Note the large proportion of fishgoing to processors that then goes on to

high valued-added markets, i.e. hotels,restaurants and export.

FISHER

VENDORS/HAWKERS

PROCESSORS

CONSUMERS

RESTAURANTS

FISH FRY

1%

9%

25%

21%

45%

54%1%

4%

100%

100%

100%

SUPERMARKETSEXPORT MARKET

86% 8%

100%

46%

7

Table 3. Estimation of the value added and overall value for flyingfish (BDS$)

Fis

hfo

rm

Seller BuyerProportion

(%)

Amount

(kg)Price

(BDS $)

Pricedifference(BDS $)

Value/

valueadded

(BDS $)

Vendors/hawkers 25 378,669 2.53 958,032

Processors 45 670,870 2.02 1,355,157

Fish fry 9 134,174 2.89 387,763Fisher

Consumer 21 307,109 2.89 887,546Wh

ole

Total Landings (kg) 1,490,822 Landedvalue

3,588,498

Restaurants 46 174,188 6.30 3.77 656,687Vendors/Hawkers Consumer 54 204,481 3.54 1.01 206,526

Consumer 1 6,709 10.59 8.57 57,494

Restaurants 86 576,948 9.70 7.68 4,430,962

Supermarkets 8 53,670 9.10 7.08 379,981

Fish fry 1 6,709 9.30 7.28 48,839

Processors

Export Market 4 25,158 9.56 7.54 189,688

Deb

on

ed

Supermarket Consumer 100 29,518 10.59 1.49 43,982

Restaurants Consumer 100 751,136 $43.85 $34.15 25,651,286

Fish fry Consumer 100 159,332 $22.36 $12.80 2,039,444

Co

ok

ed

Supermarket Consumer 100 24,151 $18.97 $9.87 238,373

Value added by deboned and cooked flyingfish 33,943,263

Overall value of flyingfish fishery outputs 37,531,761

8

Dolphinfish

Dolphinfish is next most important singlespecies after flyingfish at about 21% of thetotal landings. It is an important food fishspecies throughout the Caribbean region aswell as an important component of

recreational fisheries. This resource isshared with our neighbors and itssustainability may be at risk as there is noarrangement for collaboration inmanagement of the fishery.

9

Table 4. Estimation of the value added and overall value for dolphinfish (BDS$)

Fis

hfo

rm Seller BuyerProportion

(%)

Amount

(kg)Price

(BDS $)

Pricedifference(BDS $)

Value/

valueadded

(BDS $)

Vendors/hawkers 29 146,967 10.17 1,494,652

Processors 56 283,798 9.15 2,596,751

Fish fry 8 40,543 11.65 472,321

Fisher

Consumer 7 35,475 12.45 441,661Wh

ole

fish

Total Landings(kg) 506,782 Landed Value 5,005,384

Fish frys 43 63,196 11.67 1.50 94,794Vendors/Hawkers Consumer 57 83,771 12.45 2.28 190,998

Consumer 16 45,408 16.47 7.32 332,384

Restaurants 48 136,223 15.46 6.31 859,567

Supermarkets 10 28,380 14.96 5.81 164,887

Fish fry 6 17,028 14.56 5.41 92,121

Processors

Export market 20 56,760 25.35 16.20 919,505

Deb

on

ed

Supermarkets Consumer 65 18,447 16.65 5.00 92,234

Restaurants Consumer 100 136,223 49.50 34.04 4,637,031

Fish fry Consumer 100 79,689 22.87 11.20 892,516

Co

ok

ed

Supermarket Consumer 100 9,933 14.17 1.72 17,085

Value added by deboned and cooked dolphin fish 8,293,122

Overall value of dolphinfish fishery outputs 13,298,506

10

Tuna

This is primarily yellowfin tuna which isdistributed throughout the Atlantic Oceanand fished by vessels from many countries.This species is targeted mainly by the

longline fleet. It is a valuable exportcommodity especially when carefulhandling at sea and ashore is practiced toensure a high grade fresh product.

FISHER

VENDORS/HAWKERS

PROCESSORS&

EXPORTERS

CONSUMERS

RESTAURANTS

FISH FRY

4%

6%

17%

7%

70%

48%52%5%

28%

100%

100%

SUPERMARKETSEXPORT MARKET

49%9%

100%

11

Table 5. Estimation of the value added and overall value for tuna (BDS$)

Fis

hfo

rm

Seller BuyerProportion

(%)

Amount(kg)

Price(BDS $)

Pricedifference(BDS $)

Value/

valueadded

(BDS $)

Vendors/hawkers 17 26,125 9.10 237,740

Processors 70 107,575 8.90 957,414

Fish fry 6 9,221 10.31 95,065

Fisher

Consumer 7 10,757 10.47 112,631

Total Landings (kg) 153,678 Landed Value 1,402,850Wh

ole

fish

Processors Export market 28 30,121 30.76 21.86 658,443

Fish fry 48 12,540 10.65 1.55 19,437Vendors/hawkers Consumer 52 13,585 11.47 2.37 32,197

Consumer 5 5,379 10.59 1.69 9,090

Restaurants 49 52,712 14.87 5.97 314,688

Supermarkets 9 9,144 12.10 3.20 29,260

Processors

Fish fry 9 9,682 12.30 3.40 32,918

Deb

on

ed

Supermarkets Consumer 100 5,486 17.15 5.05 27,706

Restaurants Consumer 100 52,712 3.35 38.48 2,028,341

Fish fry Consumer 100 9,682 $23.50 11.20 108,435

Co

ok

ed

Supermarkets Consumer 100 3,658 19.65 7.55 27,614

Value added by deboned and cooked tuna 3,288,129

Overall value of tuna fishery outputs 4,690,978

12

Billfishes (including blue marlin)

Billfishes are among the most depletedlarge pelagic species in the Atlantic Ocean.Consequently, they cannot be exported tothe USA and are consumed locally. They

are also targeted by sportfishers especiallythe charter boats that serve the tourismindustry.

FISHER

VENDORS/HAWKERS

PROCESSORS

CONSUMERS

RESTAURANTS

FISH FRY

16%

21%

21%

20%

38%

74%26%26%

48%

100%

100%

100%

SUPERMARKETS

10%

13

Table 6. Estimation of the value added and overall value for billfishes (including bluemarlin) (BDS$)

Fis

hfo

rm

Seller BuyerProportion

(%)

Amount(kg)

Price(BDS $)

Pricedifference(BDS $)

Value/valueadded

(BDS $)

Vendors/hawkers 21 13,944 8.92 124,377

Processors 38 25,231 8.35 210,681

Fish fry 21 13,944 9.93 138,460

Fishermen

Consumer 20 13,280 10.70 142,092Wh

ole

Total Landings (kg) 66,398 Landed Value 615,609

Fish fry 74 10,318 13.67 4.75 49,012Vendors/Hawkers Consumer 26 3,625 14.45 5.53 20,048

Consumer 26 6,560 16.96 8.61 56,483

Restaurants 48 12,111 16.53 8.18 99,068

Supermarkets 10 2,523 16.57 8.22 20,740

Processors

Fish fry 16 4,037 16.54 8.19 33,063

Deb

on

ed

Supermarkets Consumer 100 2,271 23.85 7.28 16,532

Restaurants Consumer 100 12,111 60.20 43.67 528,887

Fish fry Consumer 100 13,944 22.87 6.33 88,263

Co

ok

ed

Supermarket Consumer 100 1,328 25.56 8.99 11,938

Value added by deboned and cooked billfish 924,033

Overall value of billfsh fishery outputs 1,539,642

14

Swordfish

Swordfish are a highly prized food fish butthe Atlantic stocks have been severelydepleted. Consequently, there is stringent

management by the InternationalCommission for Conservation of AtlanticTunas aimed at rebuilding stocks.

FISHER

VENDORS/HAWKERS

PROCESSORS

CONSUMERS

RESTAURANTS

FISH FRY

16%

11%

16%

15%

58%

74%26%26%

48%

100%

100%

100%

SUPERMARKETS

10%

15

Table 7. Estimation of the value added and overall value for swordfish (BDS$)

Fis

hfo

rm

Seller BuyerProportion

(%)

Amount(kg)

Price(BDS $)

Pricedifference(BDS $)

Value/

valueadded

(BDS $)

Vendors/hawkers 16 1,831 17.65 32,315

Processors 58 6,637 16.10 106,855

Fish frys 11 1,259 17.90 22,531

Fishermen

Consumer 15 1,716 18.26 31,342

Wh

ole

fish

Total Landings (kg) 11,443 Landed Value 193,043

Fish frys 74 1,355 18.67 1.02 1,382Vendors/

Hawkers Consumer 26 476 19.25 1.60 762

Consumer 26 1,726 21.00 4.90 8,455

Restaurants 48 3,186 21.67 5.57 17,745

Supermarkets 10 664 21.96 5.86 3,889

Deb

on

ed

Processors

Fish fry 16 1,062 21.00 4.90 5,203

Restaurants Consumer 100 3,186 58.92 37.25 118,668

Fish fry Consumer 100 3,675 27.50 6.50 23,891

Co

ok

ed

Supermarket Consumer 100 601 24.87 2.91 1,748

Value added by deboned and cooked swordfish 181,744

Overall value of swordfish fishery outputs 556,531

16

Kingfish

This group comprises mainly wahoo, butalso includes some true kingfish and ceromackerel. These species are an important

component of the small-scale fisheries inthe eastern Caribbean

FISHER

VENDORS/HAWKERS

PROCESSORS

CONSUMERS

RESTAURANTSSUPERMARKETS

FISH FRY

16%

22%

21%

9%

48%

64%36%26%

48%

10%

100%

100%

100%

17

Table 8. Estimation of the value added and overall value for kingfish (BDS$)

Fis

hfo

rm

Seller BuyerProportion

(%)

Amount(kg)

Price(BDS $)

Pricedifference(BDS $)

Value/valueadded

(BDS $)

Vendors/hawkers 21 5,874 9.49 55,741

Processors 48 13,426 9.15 122,844

Fish fry 22 6,153 9.90 60,919

Fishermen

Consumer 9 2,517 10.89 27,413Wh

ole

Total Landings (kg) 27,970 Landed Value 266,918

Fish frys 64 3,759 11.90 $2.41 9,060Vendors/Hawkers Consumer 36 2,115 12.89 $3.40 7,189

Consumer 26 3,491 13.67 $4.52 15,778

Restaurants 48 6,444 15.67 $6.52 42,017

Supermarkets 10 1,343 13.96 $4.81 6,458

Deb

on

ed

Processors

Fish fry 16 2,148 13.00 $3.85 8,270

Supermarket Consumer 100 940 18.38 $4.42 4,154

Restaurants Consumer 100 6,444 38.20 $22.53 145,190

Fish fry Consumer 100 6,153 15.66 $2.66 16,368

Co

ok

ed

Supermarket Consumer 100 403 19.56 $5.60 2,256

Value added by deboned and cooked kingfish 256,739

Overall value of kingfish fishery outputs 523,656

18

Snapper

Table 9. Estimation of the value added and overall value for snapper (BDS$)

Fis

hfo

rm

Seller BuyerProportion

(%)

Amount

(kg)Price

(BDS $)

Pricedifference(BDS $)

Value/valueadded

(BDS $)

Vendors/hawkers 35 5,426 9.62 52,199

Processors 45 6,976 10.65 74,298

Consumer 19 2,946 12.10 35,641

Fisher

Restaurants 1 155 13.95 2,163

Total Landings (kg) 15,503 Landed Value 164,301Wh

ole

fish

Processors Restaurants 1 70 14.96 4.31 64

Vendors/Hawkers

Consumer 100 5,426 12.10 2.48 13,457

Consumer 3 209 11.36 0.71 149

Restaurants 88 6,139 15.76 5.11 31,371Processors

Supermarkets 9 628 18.96 8.31 5,218Deb

on

ed

Supermarket Consumer 100 628 20 1.04 653

Co

ok

-ed Restaurants Consumer 100 6139 67.60 51.84 318,256

Value added by deboned and cooked snapper 368,514

Overall value of snapper fishery outputs 901,329

19

Shark and barracuda

Table 10. Estimation of the value added and overall value for shark and barracuda(BDS$)

Fis

hF

orm

Seller BuyerProportion

(%)Amount

(kg)Price

(BDS $)

Pricedifference(BDS $)

Value/valueadded

(BDS $)

Vendors/hawkers 50 4,888 6.75 32,991

Fish fry 15 1,466 10.65 15,616

Restaurants 10 978 10.65 10,410

Fisher

Public consumer 25 2,444 12.45 30,425Wh

ole

fish

Total Landings (kg) 9,775 Landed Value 89,441

Fish frys 17 249 11.67 4.92 1,226

Deb

on

ed

Vendors/Hawkers Public consumer 83 1,217 12.45 5.70 6,937

Fish fry Consumer 100 249 31.50 20.85 5,197

Co

ok

-ed

Restaurants 100 978 56.70 46.05 45,014

Value added by deboned and cooked shark and barracuda 58,374

Overall value of shark and barracuda fishery outputs 147,815

20

Lobster

Table 11. Estimation of the value added and overall value for lobster (BDS$)

Fis

hF

orm

Seller BuyerProportion

(%)Amount

(kg)Price

(BDS $)

Pricedifference(BDS $)

Value/valueadded

(BDS $)

Vendors/Hawkers 45 182 19.00 3,463

Consumer 20 81 22.00 1,782

Fisher

Processors 35 142 18.50 2,622

Total Landings (kg) 405 Landed Value 7,867

Restaurants 76 108 43.50 25.00 2,693Processors

Supermarkets 24 34 44.20 25.70 874

Vendors/

Hawkers

Consumer 100 182 24.00 5.00 911

Wh

ole

Supermarkets Consumer 100 34 56.00 11.80 401

Co

ok

-ed Restaurants Consumer 100 108 97.00 53.50 5,764

Value added by re-sale of whole and cooked lobster 10,644

Overall value of lobster fishery outputs 29,276

21

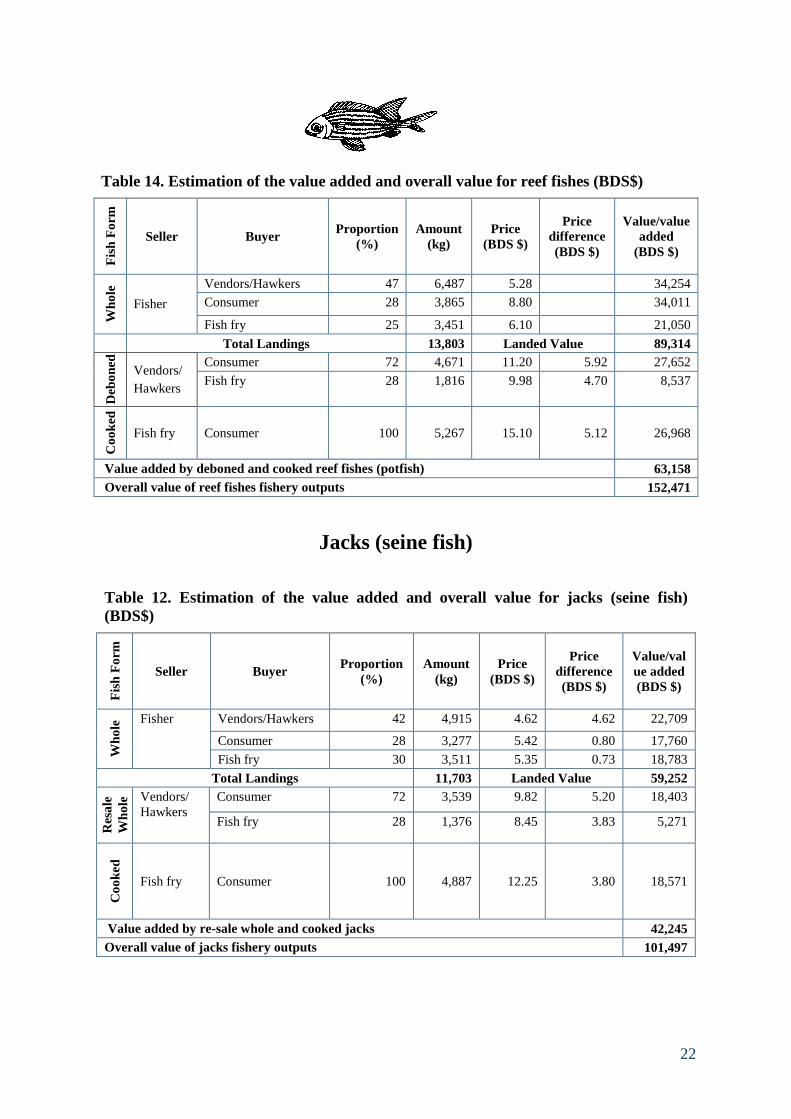

Reef fishes (potfish)

It is generally accepted that the reef fishstocks on the south and west coast of theisland are depleted. Estimates from othersimilar areas indicate that we should beable to get somewhere in the range of 390-530 metric tons of reef fishes a years forthe entire island. Even towards the lowerend of this range (about 400 mt/yr),current catches are far short of that. If the

state of depletion is due to overfishing,then fishers and consumers stand to gainconsiderably if the stocks are rebuilt.

As an added benefit there would be agreater abundance and variety of fishes onthe reefs, in particular the species whichare attractive for snorkelers and divers.Therefore, the tourism industry would alsobenefit from rebuilding.

22

Table 14. Estimation of the value added and overall value for reef fishes (BDS$)

Fis

hF

orm

Seller BuyerProportion

(%)Amount

(kg)Price

(BDS $)

Pricedifference(BDS $)

Value/valueadded

(BDS $)

Vendors/Hawkers 47 6,487 5.28 34,254

Consumer 28 3,865 8.80 34,011

Wh

ole

Fisher

Fish fry 25 3,451 6.10 21,050

Total Landings 13,803 Landed Value 89,314

Consumer 72 4,671 11.20 5.92 27,652

Deb

on

ed

Vendors/

HawkersFish fry 28 1,816 9.98 4.70 8,537

Co

ok

ed

Fish fry Consumer 100 5,267 15.10 5.12 26,968

Value added by deboned and cooked reef fishes (potfish) 63,158

Overall value of reef fishes fishery outputs 152,471

Jacks (seine fish)

Table 12. Estimation of the value added and overall value for jacks (seine fish)(BDS$)

Fis

hF

orm

Seller BuyerProportion

(%)Amount

(kg)Price

(BDS $)

Pricedifference(BDS $)

Value/value added(BDS $)

Vendors/Hawkers 42 4,915 4.62 4.62 22,709

Consumer 28 3,277 5.42 0.80 17,760

Wh

ole

Fisher

Fish fry 30 3,511 5.35 0.73 18,783

Total Landings 11,703 Landed Value 59,252

Consumer 72 3,539 9.82 5.20 18,403

Res

ale

Wh

ole Vendors/

HawkersFish fry 28 1,376 8.45 3.83 5,271

Co

ok

ed

Fish fry Consumer 100 4,887 12.25 3.80 18,571

Value added by re-sale whole and cooked jacks 42,245

Overall value of jacks fishery outputs 101,497

23

Bonito

Table 13. Estimation of the value added and overall value for bonito (BDS$)

Fis

hF

orm

Seller BuyerProportion

(%)Amount

(kg)Price

(BDS $)

Pricedifference(BDS $)

Value/valueadded

(BDS $)

Vendors/Hawkers 37 630 5.08 5.08 3,199

Public Consumer 30 511 6.16 1.08 3,145

Fisher

Fish fry 33 562 6.10 1.02 3,426Wh

ole

Total Landings 1,702 Landed Value 9,771

Public consumer 65 409 11.58 6.50 2,661

Deb

on

ed

Vendors/Hawkers Fish fry 35 220 11.58 6.50 1,433

Co

ok

ed

Fish fry Consumer 100 782 15.84 9.74 7,617

Value added by deboned and cooked bonito 11,711

Overall value of bonito fishery outputs 21,481

All others

Table 15. Estimation of the value added and overall value for all others (BDS$)

Fis

hF

orm

Seller BuyerProportion

(%)Amount

(kg)Price

(BDS $)

Pricedifference(BDS $)

Value/valueadded

(BDS $)

Vendors/Hawkers 40 23,959 6.08 145,672

Public Consumer 35 20,964 7.16 150,104Fisher

Fish fry 25 14,975 7.10 106,319Wh

ole

Total Landings 59,898 Landed Value 402,095

Public consumer 80 19,167 8.46 2.38 45,618

Deb

on

ed Vendors/Hawkers

Fish fry 20 4,792 8.58 2.50 11,980

Co

ok

ed

Fish fry Consumer 100 19,766 7.84 0.74 14,627

Value added by deboned and cooked fish 72,225

Overall value of all other fishery outputs 474,320

24

NEXT STEPSThis was a preliminary study with limitedtime and funds. Hence, several data gapswere identified. These will need furtherresearch.

Fish-fry vendors did not provide accessto records of their purchasing and re-sale practices therefore the estimatesare based on verbal information.

There are no records of landings forlobster, sea urchins and conch. Theseresources are considered high valuedby various players in the “value-addedchain”.

There is no information on otherestablishments such as rum shops andsmall restaurants that are known tofrequently sell fish. These warrantfurther investigation, as due to theirlarge numbers, they probably addsignificant overall value.

No information was obtained on thecontribution from food processorsmaking fish products.

Prices were averaged since there werea range of prices available for eachcategory of seller.

The locations of the survey should beextended, to receive a more

representative contribution from thefishery resources.

Consumers are varied and there is theneed for a better understanding of theircharacteristics.

This preliminary study has providedinsight into the apparent value of fisheriesto the national economy. It indicates thatthere is the need to fully investigate thisvalue in all its ramifications in order thatthe industry can receive support that isconsistent with its value.

In addition to refinement of thepreliminary estimates provided here andfilling of the gaps identified above, there isthe need to examine the value ofassociated supporting activities such as:

Fishing industry gear and equipmentsupply;

Vessel construction, repair andmaintenance;

Support for distribution and processingsystems.

We recommend that these be pursuedsystematically until the value of this vitalindustry is fully understood.

FURTHER READINGFisheries Division. 2001. BarbadosFisheries Management Plan. Ministry ofAgriculture and Rural Development,Barbados, 67 pp.

Mahon, R. and P. McConney. 2004 [ed].Management of large pelagic fisheries inCARICOM. FAO Fisheries TechnicalPaper No 464, 149 p.

McConney, P., R. Mahon and C. Parker.2003. Barbados case study: the sea eggfishery. Caribbean Coastal Co-management Guidelines Project.

Caribbean Conservation Association,Barbados. 75 pp.

Welch, P. L.V. 2005. Exploring the marineplantation: An historical investigation ofthe Barbados fishing industry. The Journalof Caribbean History 39: 19-37

Willoughby, S. and D. Leslie. 2000.Fishing gear of Barbados. Ministry ofAgriculture and Rural Development,Barbados, Fisheries Division Report FDR-002-2000, 41 p.