the value of food aid monetization: benefits, risks and best practices

DESCRIPTION

Informa Economics has released its study “The Value of Food Aid Monetization: Benefits, Risks and Best Practices (November 2012), showing multiple benefits to recipients.TRANSCRIPT

The Value of Food Aid Monetization: Benefits, Risks and Best Practices

Prepared for the:

Alliance for Global Food Security

Informa Economics 775 Ridge Lake Blvd. Suite 400 Memphis, TN 38120 Phone: 901.766.4669 www.informaecon.com

November 2012

i

TABLE OF CONTENTS

I. EXECUTIVE SUMMARY ................................................................................................. 1

II. INTRODUCTION........................................................................................................... 18

III. PROJECT SCOPE & METHODOLOGY ..................................................................... 19

A. SCOPE ........................................................................................................................ 19

B. METHODOLOGY ............................................................................................................ 19

1. Overview ................................................................................................................. 19

2. Key “Risks and Benefits” Study Questions & Methodology .................................... 20

3. Determination of Fair Market Value ........................................................................ 22

IV. FOOD AID & MONETIZATION OVERVIEW ............................................................... 28

A. OVERVIEW OF FOOD AID PROGRAMS AND MONETIZATION ................................................ 28

B. U.S. INTERNATIONAL FOOD AID PROGRAMS ................................................................... 29

C. POTENTIAL BENEFITS AND RISKS OF FOOD AID MONETIZATION ........................................ 35

V. THE GAMBIA – SOYBEAN OIL – INTERNATIONAL RELIEF AND DEVELOPMENT 37

A. FOOD AID OVERVIEW .................................................................................................... 37

1. The Gambia Food Aid Overview ............................................................................. 37

2. Program Overview: IRD – The Gambia – Soybean Oil Monetization ...................... 38

B. THE GAMBIA SOYBEAN OIL MONETIZATION RATIONALE ................................................... 39

1. Vegetable Oil Supply and Demand – Significant Demand & Insufficient Domestic Production .................................................................................................................. 39

2. Commercial Import Limitations and/or Additional Monetization Rationale .............. 40

C. IMPACT ON DOMESTIC MARKET ...................................................................................... 41

1. Price Impact ............................................................................................................ 41

2. Production .............................................................................................................. 43

3. Internal Market Development .................................................................................. 45

4. Consumers/Food Availability .................................................................................. 46

D. IMPACT ON COMMERCIAL TRADE ................................................................................... 47

E. DIRECT MONETIZATION COSTS AND REVENUES .............................................................. 49

F. THE GAMBIA CONCLUSIONS ........................................................................................... 50

VI. GUATEMALA – SOYBEAN MEAL – PROJECT CONERN INTERNATIONAL .......... 53

A. FOOD AID OVERVIEW .................................................................................................... 53

1. Guatemala Food Aid Overview ............................................................................... 53

2. Program Overview: PCI – Guatemala - Soybean Meal Monetization ..................... 54

B. GUATEMALA SOYBEAN MEAL MONETIZATION RATIONALE ................................................. 55

1. Soybean Meal Supply and Demand – Significant Demand & Insufficient Domestic Production .................................................................................................................. 55

2. Commercial Import Limitations and/or Additional Monetization Rationale .............. 56

C. IMPACT ON THE DOMESTIC MARKET ............................................................................... 57

1. Price Impact ............................................................................................................ 57

2. Production .............................................................................................................. 59

ii

3. Internal Market Development .................................................................................. 61

4. Consumers/Food Availability .................................................................................. 62

D. IMPACT ON COMMERCIAL TRADE ................................................................................... 64

E. DIRECT MONETIZATION COSTS AND REVENUES .............................................................. 66

F. GUATEMALA CONCLUSIONS ........................................................................................... 67

VII. LIBERIA – RICE – LAND O’ LAKES ......................................................................... 70

A. FOOD AID OVERVIEW .................................................................................................... 70

1. Liberia Food Aid Overview ...................................................................................... 70

2. Program Overview: Land O’ Lakes – Liberia – Rice ............................................... 71

B. LIBERIA RICE MONETIZATION RATIONALE ....................................................................... 72

1. Rice Supply and Demand – Sufficient Domestic Demand, Yet Insufficient Domestic Production .................................................................................................................. 72

2. Commercial Import Limitations and/or Additional Monetization Rationale .............. 74

C. IMPACT ON THE DOMESTIC MARKET ............................................................................... 75

1. Price Impact ............................................................................................................ 75

2. Production .............................................................................................................. 77

3. Internal Market Development .................................................................................. 80

4. Consumers/Food Availability .................................................................................. 80

D. IMPACT ON COMMERCIAL TRADE ................................................................................... 81

E. DIRECT MONETIZATION COSTS AND REVENUES – COST RECOVERY ................................. 84

F. LIBERIA CONCLUSIONS .................................................................................................. 85

VIII. MOZAMBIQUE – WHEAT – WORLD VISION .......................................................... 88

A. FOOD AID OVERVIEW .................................................................................................... 88

1. Mozambique Food Aid Overview ............................................................................ 88

2. Program Overview: World Vision – Mozambique - Wheat Monetization ................. 89

B. MOZAMBIQUE WHEAT MONETIZATION RATIONALE ........................................................... 90

1. Wheat Supply and Demand – Insufficient Domestic Production, Yet Sufficient Domestic Demand ...................................................................................................... 90

2. Commercial Import Limitations and/or Additional Monetization Rationale .............. 93

C. IMPACT ON DOMESTIC MARKET ...................................................................................... 94

1. Price Impact ............................................................................................................ 94

2. Production .............................................................................................................. 97

3. Internal Market Development .................................................................................. 99

4. Consumers/Food Availability ................................................................................ 100

D. IMPACT ON COMMERCIAL TRADE ................................................................................. 102

E. DIRECT MONETIZATION COSTS AND REVENUES ............................................................ 105

F. MOZAMBIQUE CONCLUSIONS ....................................................................................... 105

IX. UGANDA – WHEAT – ACDI/VOCA .......................................................................... 108

A. FOOD AID OVERVIEW .................................................................................................. 108

1. Uganda Food Aid Overview .................................................................................. 108

2. Program Overview: ACDI/VOCA – Uganda - Wheat Monetization ....................... 109

B. WHEAT MONETIZATION RATIONALE .............................................................................. 111

1. Wheat Supply and Demand – Insufficient Domestic Production ........................... 111

iii

2. Commercial Import Limitations and/or Additional Monetization Rationale ............ 113

C. IMPACT ON THE DOMESTIC MARKET ............................................................................. 113

1. Price Impact .......................................................................................................... 113

2. Production ............................................................................................................ 116

3. Internal Market Development ................................................................................ 118

4. Consumers/Food Availability ................................................................................ 119

D. IMPACT ON COMMERCIAL TRADE ................................................................................. 121

E. DIRECT MONETIZATION COSTS AND REVENUES ............................................................ 125

F. UGANDA CONCLUSIONS .............................................................................................. 125

X. CONCLUSIONS .......................................................................................................... 128

APPENDIX ...................................................................................................................... 130

A. COUNTRY PROFILES – SELECT MONETIZATION CASES .................................................. 130

B. LITERATURE REVIEW REFERENCES .............................................................................. 141

iv

List of Figures Figure 1: World Wheat Prices ............................................................................................ 23 Figure 2: World Rice Prices ............................................................................................... 24 Figure 3: Daily Average Freight Rates by Vessel Size ...................................................... 25

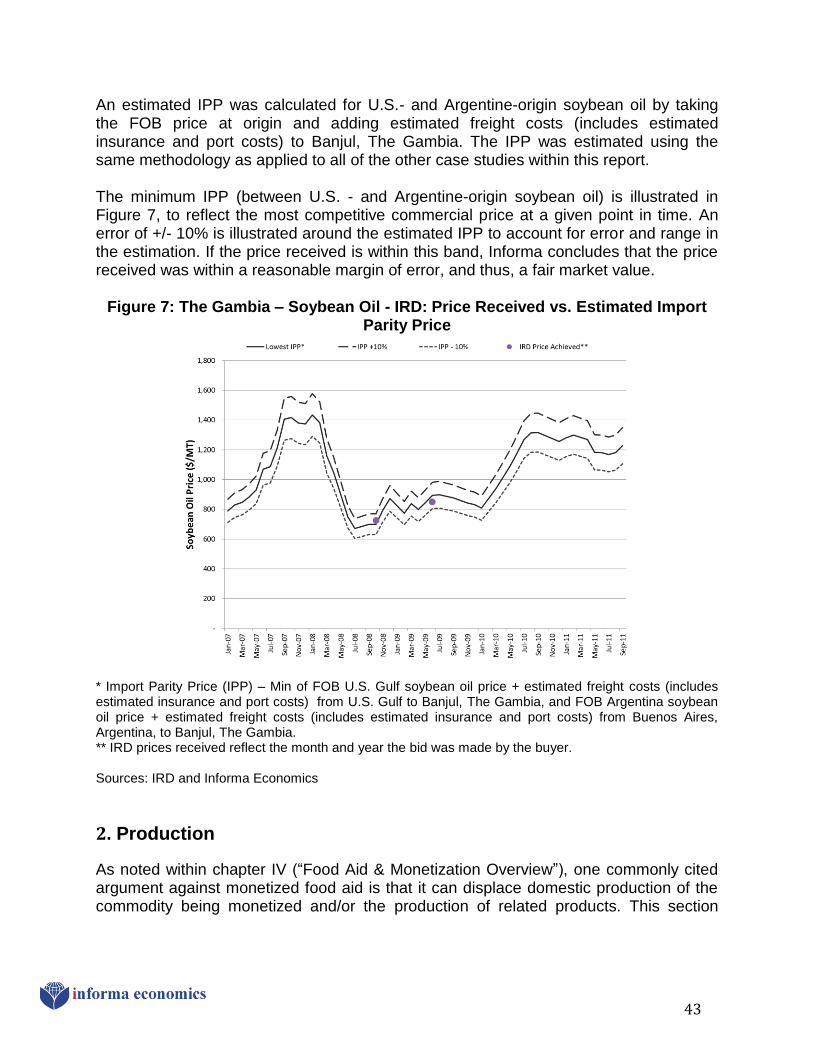

Figure 4: U.S. International Food Assistance Tonnages, FY 2006 - 2010 ........................ 34 Figure 5: U.S. International Food Assistance Funding, FY 2006 - 2010 ........................... 34 Figure 6: Vegetable Oil Production and Consumption in The Gambia .............................. 40 Figure 7: The Gambia – Soybean Oil - IRD: Price Received vs. Estimated Import Parity

Price ....................................................................................................................... 43

Figure 8: The Gambia Oil Crop Production & Monetized Soybean Oil Trends*................. 45 Figure 9: The Gambia Commercial Vegetable Oil & Monetized Soybean Oil Imports, Fiscal

Year ........................................................................................................................ 48 Figure 10: Guatemala – SBM – PCI: Price Received vs. Alternative Market Price Estimates

................................................................................................................................ 59 Figure 11: Guatemala Feed Grains/Meals: Production & Monetized Soybean Meal Trends*

................................................................................................................................ 61

Figure 12: Guatemala Per Capita Soybean Meal and Poultry Meat Consumption, 1961 - 2009 ........................................................................................................................ 63

Figure 13: Guatemala Commercial & Monetized Soybean Meal Imports, Fiscal Year ...... 65 Figure 14: 2007 Liberia Food Supply (kg/capita/yr) ........................................................... 74 Figure 15: Liberia – Rice - LOL: Price Received vs. Estimated Import Parity Price ........... 77

Figure 16: Liberia Rice and Related Product Crop Production & Monetization Trends* .... 79 Figure 17: Liberia – Monetized and Commercial Rice Imports .......................................... 82

Figure 18: Liberia’s Top Twenty Food Imports, in 2009. ................................................... 83 Figure 19: Top Crops Produced in Mozambique, by Volume ........................................... 91 Figure 20: 2007 Mozambique Food Supply (kg/capita/yr) ................................................ 92

Figure 21: Mozambique – Wheat – WV: Price Received vs. Estimated Import Parity Price................................................................................................................................ 97

Figure 22: Mozambique Wheat and Related Product Production & Monetization Trends *99 Figure 23: Mozambique Commercial & Monetized Wheat Imports by Fiscal Year .......... 103

Figure 24: Mozambique Cereal Imports. ......................................................................... 104 Figure 25: 2007 Uganda Food Supply (kg/capita/yr) ....................................................... 112 Figure 26: Uganda – Wheat – ACDI/VOCA: Price Received vs. Estimated Import Parity

Price ..................................................................................................................... 115 Figure 27: Uganda Wheat and Related Product Production & Monetization Trends* ...... 117 Figure 28: Uganda Commercial & Monetized Wheat Imports .......................................... 122 Figure 29: Uganda Cereal Imports, 2001-2010 ............................................................... 124 Figure 30: Uganda Food Imports, 2009 ........................................................................... 124

v

List of Tables Table 1: U.S. International Food Assistance Tonnage, FY 2006 – 2010, Metric Tons ..... 28 Table 2: U.S. International Food Assistance Funding, FY 2006 – 2010, Million U.S. Dollars

................................................................................................................................ 28

Table 3: PL480 Title II Appropriations, FY 2003 – 2013, Million U.S. Dollars ................... 31 Table 4: PL 480 Title II Funds, FY 2006 – 2010, Million U.S. Dollars ............................... 31 Table 5: Volume and Value of U.S. Soybean Oil Programmed for Monetization* for The

Gambia, Fiscal Years 2006-2010 ........................................................................... 38 Table 6: The Gambia Vegetable Oil Imports, Fiscal Years 2001 to 2010 .......................... 48

Table 7: Volume of The Gambia Vegetable Oil Imports .................................................... 49 Table 8: Value of The Gambia Vegetable Oil Imports ....................................................... 49 Table 9: Direct IRD Soybean Oil Monetization Costs & Revenues – The Gambia ............ 50 Table 10: Volume and Value of U.S. Soybean Meal Programmed for Monetization* for

Guatemala, Fiscal Years 2001-2011 ...................................................................... 54 Table 11: Guatemala’s Monetized Soybean Meal, Commercial Imports, and Monetized

Imports as Share of Total Imports, 2001 – 2011 ..................................................... 56

Table 12: Guatemala Soybean Meal Imports, Fiscal Years 2001 to 2011 ......................... 65 Table 13: Volume of Guatemala Soybean Meal Imports by Country of Origin .................. 65

Table 14: Value of Guatemala Soybean Meal Imports by Country of Origin ..................... 66 Table 15: Per Unit Price of Guatemala Soybean Meal Imports ......................................... 66 Table 16: Direct PCI Soybean Meal Monetization Costs & Revenues - Guatemala .......... 67

Table 17: Volume and Value of Rice Programmed for Monetization* in Liberia Fiscal Years 2006-2010 .............................................................................................................. 71

Table 18: Awardees for Rice Programmed for Monetization for Liberia ............................ 71 Table 19: Liberia Rice Supply and Demand (MT) ............................................................. 73 Table 20: Liberia Anticipated Import Requirements for 2011 Marketing Year ................... 83

Table 21: World Rice Exports to Liberia ............................................................................ 84 Table 22: World Rice Exports to Liberia ............................................................................ 84

Table 23: World Rice Exports to Liberia ............................................................................ 84 Table 24: Direct LOL Rice Monetization Costs & Revenues - Liberia ............................... 85

Table 25: Volume and Value of U.S. Wheat Programmed for Monetization* for Mozambique, Fiscal Years 2001-2010 ................................................................... 89

Table 26: Mozambique Wheat Supply and Demand (MT) ................................................ 91

Table 27: World Vision Mozambique Wheat Monetization – Number of Bidders, Buyers, Demand, and Quantity Sold .................................................................................... 95

Table 28: Mozambique Wheat Imports, Fiscal Years 2001 to 2010 ................................ 103 Table 29: Volume of Mozambique Wheat Imports by Country of Origin .......................... 103 Table 30: Value of Mozambique Wheat Imports by Country of Origin ............................. 104

Table 31: Direct WV Wheat Monetization Costs & Revenues - Mozambique.................. 105

Table 32: Volume and Value of US Wheat Programmed for Monetization for Uganda, Fiscal Years 2001-2011 ........................................................................................ 109

Table 33: Awardees for US Wheat Programmed for Monetization in Uganda Fiscal Years 2006-2011 ............................................................................................................ 109

Table 34: Uganda Wheat Supply and Demand (MT) ....................................................... 111 Table 35: Uganda’s Largest Wheat Millers (by Capacity) ............................................... 118

vi

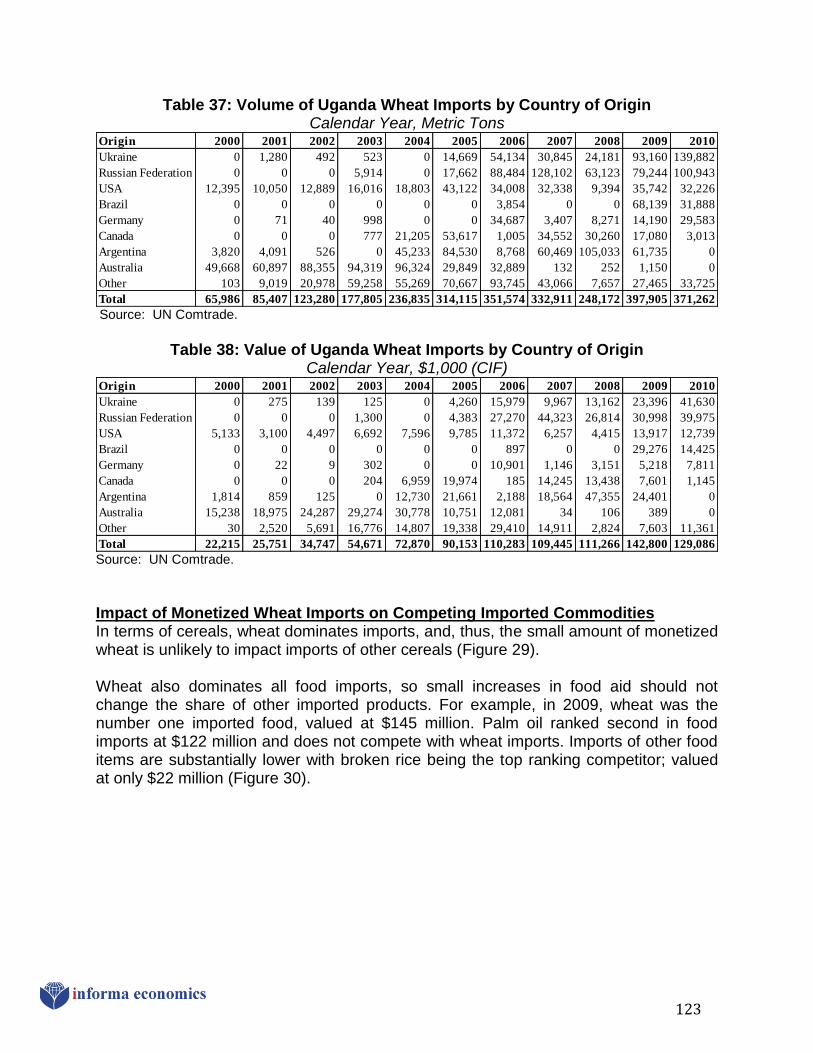

Table 36: Uganda Wheat Imports, 2001 to 2011 ............................................................. 122 Table 37: Volume of Uganda Wheat Imports by Country of Origin .................................. 123

Table 38: Value of Uganda Wheat Imports by Country of Origin ..................................... 123 Table 39: Direct ACDI/VOCA Wheat Monetization Costs & Revenues - Uganda ............ 125

vii

DISCLAIMER This report was produced by Informa Economics, Inc. (“Informa”) for the Alliance for Global Food Security (“AGFS”). Informa has used the best and most accurate information available to complete this study. Informa is not in the business of soliciting or recommending specific investments. The reader of this report should consider the market risks inherent in any financial investment opportunity. While Informa has extended its best professional efforts in completing this analysis, the liability of Informa to the extent permitted by law, is limited to the professional fees received in connection with this project.

viii

Abbreviations and Terms Abbreviations ACDI/VOCA – a private voluntary organization registered with USAID AGFS – Alliance for Global Food Security CCC – Commodity Credit Corporation CBO – Community Based Organization CIF – Cost, insurance and freight CS – Cooperating Sponsor CDSO – Crude degummed soybean oil DAP – Development Assistance Program EMG – Emerging Markets Group ERS – Economic Research Service FAO – Food and Agriculture Organization of the United Nations FAS – Foreign Agricultural Service, U.S. Department of Agriculture FFE – Food for Education FFP – Food for Progress FFW – Food for Work FOB – Free on board GAO – U.S. Government Accountability Office GTIS – Global Trade Information System (same as Global Trade Atlas) IPP – Import parity price IRD – International Relief and Development ITSH – Internal transportation, storage and handling IDP – Internally displaced person LOL – Land O’ Lakes LRA – Lord’s Resistance Army MONCON – Monetization consortium MYAP – Multi-Year Assistance Program NAADS – National Agricultural Advisory Services NGO – Non-Governmental Organization PCI – a private voluntary organization registered with USAID, previously called “Project Concern International” PVO – Private Voluntary Organization SFP – School Feeding Program USDA – United States Department of Agriculture USAID – United States Agency for International Development WFP – United Nations World Food Program WV – World Vision Terms Throughout this report, all “tons” refer to metric tons (MT) and all “dollars ($)” refer to U.S. $, unless otherwise noted. The terms “agricultural commodity” and “commodity” are used interchangeably and they mean any agricultural commodity or the products thereof.

ix

The terms “cooperative,” “developing country,” “food security,” “nongovernmental organization,” and “private voluntary organization” have the same meanings given those terms in section 402 of the Food for Peace Act (7 U.S.C. 1732), as follows:

“COOPERATIVE.—The term ‘cooperative’ means a private sector organization whose members own and control the organization. and share in its services and its profits and that provides business services and outreach in cooperative development for its membership. DEVELOPING COUNTRY.—The term ‘developing country’ means a country that has a shortage of foreign exchange earnings and has difficulty meeting all of its food needs through commercial channels. (6) FOOD SECURITY.—The term ‘food security’ means access by all people at all times to sufficient food and nutrition for a healthy and productive life. (7) NONGOVERNMENTAL ORGANIZATION.—The term ‘nongovernmental organization’ means an organization that works at the local level to solve development problems in a foreign country in which the organization is located, except that the term does not include an organization that is primarily an agency or instrumentality of the government of the foreign country. (8) PRIVATE VOLUNTARY ORGANIZATION.—The term ‘private voluntary organization’ means a not-for-profit, nongovernmental organization (in the case of a United States organization, an organization that is exempt from Federal income taxes under section 501(c)(3) of the Internal Revenue Code of 1986) that receives funds from private sources, voluntary contributions of money, staff time, or in-kind support from the public, and that is engaged in or is planning to engage in voluntary, charitable, or development assistance activities (other than religious activities).”

The term “Bellmon analysis” is used to describe the analysis undertaken to make the determination required under section 403(a) of the Food for Peace Act:

“403(a) PROHIBITION.—No agricultural commodity shall be made available under this Act unless it is determined that—

(1) adequate storage facilities will be available in the recipient country at the time of the arrival of the commodity to prevent the spoilage or waste of the commodity; and (2) the distribution of the commodity in the recipient country will not result in a substantial disincentive to or interference with domestic production or marketing in that country.”

The term “cost recovery” is a measurement of total monetization revenues (cost per metric ton times total tonnage) divided by monetization costs (commodity procurement cost, foreign- flag freight cost, and, where applicable, inland transportation, storage and handling costs).

1

I. EXECUTIVE SUMMARY

The United States provides food aid overseas to promote development and food security and to address emergency needs. Most of the food commodities are distributed to recipients (86% in fiscal year 20101). In some cases, commodities may be ”monetized” – sold on the market or to the government of the recipient country and the proceeds used for development activities to improve agriculture, nutrition, livelihoods, access to education and food security, and to reduce vulnerability in crisis-prone regions. Net food-importing developing countries are the primary recipients. This study summarizes the potential risks and benefits of monetization and evaluates data from specific monetization cases against those potential risks and benefits. Best practices to minimize chances of adverse impacts on local production or markets and to avoid disruption of commercial trade also are identified. Two common criticisms of monetization found in the literature are summarized in the title of a June 2011 U.S. General Accountability Office (GAO) report: International Food Assistance: Funding Development Projects through the Purchase, Shipment, and Sale of U.S. Commodities is Inefficient and Can Cause Adverse Market Impacts. The basis for the GAO finding that food aid is “inefficient” is that the “cost recovery” of food aid monetization is generally less than 100% – e.g., the funds generated for development projects via the proceeds from monetization of the commodities are less than the costs incurred to procure and ship the commodities to recipient countries. However, this basic cost recovery formula only tells part of the story; it is not sufficient for determining the value of monetization to a recipient country. Cost recovery only places a value on the proceeds generated from the sale and does not take into account additional benefits that accrue from the provision of the commodity itself. GAO’s rationale for concluding that monetization “can result in adverse market impacts” is that there is insufficient and inconsistent collection of data by USAID and USDA to prove otherwise; a problem that can be addressed by better coordination between the agencies, a clearer description of what constitutes the “reasonable market price” for a commodity, and improved USAID and USDA data collection.2 In this study five food aid monetization cases were evaluated in detail to determine whether and how monetization adds value and creates benefits besides generating funds for conducting development activities.3 One of the primary research questions

1 GAO, June 2011. “International Food Assistance: Funding Development Projects through the Purchase,

Shipment, and Sale of U.S. Commodities is Inefficient and Can Cause Adverse Market Impact”. 2 Obtaining a “reasonable market price in the economy where the agricultural commodity is to be sold” is

a requirement for PL 480 Title II and Food for Progress programs in order to avoid disrupting world prices or normal patterns of commercial trade. See section 403(e) of the Food for Peace Act. 3 This study reviewed 19 monetization cases conducted by private voluntary organizations and

cooperatives. Five of the cases were chosen for in-depth analysis: two PL 480 Title II development programs, two Food for Progress programs and one McGovern-Dole International Food for Education and Child Nutrition program. Data and background information for the in-depth studies were collected from applications and reports submitted by implementing organizations to administrative agencies (USDA and

2

was: “Does monetization create benefits that would not have occurred with direct program funding?” In short, the answer was found to be “yes.” Monetization can lead to benefits beyond those that would be created via direct program funding by addressing credit, hard currency, small volume, and other constraints to buying on the international market, thereby creating business opportunities and increasing the availability of the commodity in the recipient country. The study also found that, due to the practices used when designing and implementing the five reviewed programs, (1) the sale of the commodities did not compete with or create disincentives to local production, (2) the sale of the commodities did not disrupt commercial trade, and (3) the sale was for a fair market value (e.g., the sales price received for the commodity was comparable to prevailing market prices for similar commodities in the country of sale), which helps mitigate the potential for market disruption. Best practices for determining the fair market value and collecting consistent data on monetization are described in this report. Study Questions The purpose of in-depth analysis of each of the five case studies was to answer the following questions about the potential risks and benefits of monetization: Was there sufficient domestic demand and insufficient domestic production to

warrant the monetization and importation of the chosen commodity?

Methodology Overview: This was evaluated by comparing historical production and consumption levels of the monetized commodity and related commodities in each of the evaluated countries.

Does food aid monetization provide benefits that would not be achieved with

alternative policy options (e.g., direct program funding)?

Does the monetization add to food availability and/or quality? And/or has monetization aided market development?

Is there another reason for monetization over alternative policy options (e.g., direct program funding)?

Methodology Overview: This evaluation was based primarily on interviews with program representatives from each of the reviewed countries, and, to a lesser extent, information from reports submitted by implementing agencies to USAID and USDA, as well as published evaluations and reports. The purpose was to identify potential credit, currency, volume and/or other market barriers that may prevent

USAID); additional sales and market information collected by those organizations during the course of program implementation; interviews with program representatives; data published or provided by USDA and USAID; independent, published evaluations of the programs; market analysis conducted by USAID contractors in the recipient countries (called the “Bellmon Estimation Studies for Title II” or “BEST,” http://www.usaidbest.org); and market and shipping information from widely used commercial sources.

3

buyers from purchasing the commodity or a similar quality product off of the open market. For example, in several of the evaluated cases small- or medium-sized buyers were disadvantaged in sourcing commodities because they could not purchase commercial-scale quantities on the open market. Volume constraints were analyzed by comparing freight costs for commercial-scale shipments with the costs that would have likely been incurred to ship the smaller volumes that would have been transacted by the in-country buyers.

Has the monetization had an adverse impact on domestic production of the monetized commodity and/or related products?

Methodology Overview: This was evaluated by comparing both the volumes and trends of monetization of the commodity against the in-country production of that commodity and/or related products. Two key statistics were evaluated: (1) the transaction volume of the monetized commodity relative to total domestic production of that commodity (both with and without related products included); and (2) whether there was any historical correlation that might indicate that the level of monetization had a negative impact on production.

Has the monetization disrupted commercial trade of the monetized commodity and/or related products?

Methodology Overview: This was evaluated by comparing both the volumes and trends of the monetized commodity against the total imports of that commodity and/or related products. Two key statistics were evaluated: (1) the transaction volume of the monetized commodity relative to total imports of that commodity and related products; and (2) whether there was any historical correlation that might indicate that the level of monetization had a negative impact on imports.4

What is the average direct cost recovery rate?

Methodology Overview: The “cost recovery rate” equals revenues from sales divided by the costs of procuring and shipping the commodity, plus other costs incurred in carrying out the monetization. Revenue and cost data were provided by implementing organizations, which had collected the information during the course of program implementation in each of the reviewed countries. “Revenues” equal the transaction price multiplied by the volume. “Costs” are the sum of the commodity procurement price (price of the commodity at the U.S. loading port), ocean freight cost (prevailing foreign-flag rate at the time of sale for shipping the cargo from the U.S. port to the destination port), and, when applicable, internal transportation, storage, and handling costs (any additional costs incurred by the program after the cargo reaches the destination port to deliver the product to the in-country buyer[s]). A three-year average cost recovery rate (revenues divided by costs) was utilized

4 The Global Trade Atlas, FAO and USDA databases were the primary sources of information to conduct

this review.

4

whenever three years of data were available. If the commodity was monetized for less than three years, then the average cost recovery rate for the entire program was used.

Key Conclusions/Findings In all evaluated cases monetization did not disrupt domestic production or the marketing of locally-produced commodities. Domestic production of the commodity chosen for monetization was insufficient to meet demand, which helps mitigate any potential disincentive to or interference with domestic production.5 In all of the cases analyzed within this study, the commodity chosen for monetization was consumed in significant amounts in the target country and national production was insufficient to meet the demand. As a result, the sales did not compete with local production or the marketing of locally-produced commodities. For example: in Gambia, where soybean oil was monetized, the country produces only 10% to 16% of its total vegetable oil demand. In Mozambique, where wheat was monetized, domestic wheat production accounts for roughly 1% of domestic demand. In some cases, an appropriate way to mitigate any potential disruption to local production and marketing is by timing the monetization to occur when domestic availability is particularly low (e.g., during the growing season) or demand is particularly high (e.g., before certain holidays). In all evaluated cases monetization did not disrupt commercial imports. Achieving a fair market value for the monetized commodity helps ensure that monetization does not interfere with commercial sales. Monetizing at levels that are low relative to total import volumes can also help avoid interfering with commercial sales, but in years when a low-income net food-importing country is unable to maintain typical commercial import levels due to economic stress or high world prices, keeping a low ratio of monetization to total imports is not necessarily beneficial. In the evaluated cases monetization transaction volumes were relatively small compared with total import volumes (10% or less). There was one case where total monetization volumes (from all programs) reached 10% of total import volumes (Mozambique), but it was found upon further evaluation, and supported by other studies, that monetization did not have an adverse impact on commercial imports.

5 Section 403(a)(2) of the Food for Peace Act states that no commodity can be provided under this Act,

unless “the distribution of the commodity in the recipient country will not result in a substantial disincentive to or interference with domestic production or marketing in that country." This provision applies to any commodity provided, whether for distribution or monetization, under PL 480 and Food for Progress, except for an emergency.

5

Informa found that overall, the level of commercial imports increased over time and monetization’s share of imports decreases. Moreover, because the Mozambican milling industry relies on imported wheat, when commercial imports declined by 153,512 MT from 2007 to 2008 due to high world prices, it would have been helpful to the domestic industry and consumers to increase the volume of monetization relative to commercial imports. Total monetization did increase that year, but only by 2,190 MT. Thus, while monetization of 10% or less of average import levels for the preceding three years is a useful guideline for avoiding interference with commercial trade, depending on the specific situation in the recipient country, levels above 10% may be warranted. All cases evaluated in this study achieved a “fair market value,” that is, the price was comparable to prices for similar quality products available on the market in the country where the sales took place, or, if limited volume is traded on the local market, the price that local buyers would have to pay to obtain similar quality products off of the world market. [See subheading that follows, entitled, Best Practices: Determination of the “Fair Market Value”.] Obtaining the fair market value minimizes the potential for any adverse impacts on the market or disruption of normal patterns of commercial trade, as required by section 403(e) of the Food for Peace Act.6 Monetization can address a variety of market constraints and thereby create business opportunities and increase food availability and/or improve access to more nutritious foods within the recipient country. The five cases demonstrated a number of ways that monetization can add value, compared to direct project funding, by addressing market constraints. Market constraints include the following: Credit Constraints – Limited access to financing prevents potential buyers from

purchasing commodities on the world market. Monetization provides those buyers with financing options. For example, monetization programs can offer more flexible payment terms than what is commercially available by not requiring an international letter of credit or allowing payment in installments, rather than full payment upon delivery. This benefit is highlighted in the Uganda, Mozambique and Liberia case studies. In Uganda ACDI/VOCA allowed buyers to buy the wheat in installments, which encouraged a wide variety of millers to participate and was particularly helpful to those with cash-flow limitations. The World Vision wheat monetization in

6 Section 403(e) of the Food for Peace Act, “World Prices,” stipulates:

“(1) IN GENERAL.—In carrying out this Act, reasonable precautions shall be taken to assure that sales or donations of agricultural commodities will not unduly disrupt world prices for agricultural commodities or normal patterns of commercial trade with foreign countries. (2) SALE PRICE.—Sales of agricultural commodities described in paragraph (1) shall be made at a reasonable market price in the economy where the agricultural commodity is to be sold, as determined by the Secretary or the Administrator, as appropriate.”

These provisions apply to any commodity provided, whether for distribution or monetization, under PL 480 and Food for Progress, except for an emergency.

6

Mozambique had credit terms that encouraged participation of smaller millers, giving them experience with commercial trade practices, while making the sales process more competitive to facilitate achievement of a fair market value. Payments for rice under the LOL program in Liberia were spread over a 120-day period from arrival in port, with a 15% advance payment.

Volume Constraints – For medium- and small-scale buyers, higher freight rates and

other costs associated with low-volume sales impede their ability to source commodities on the world market. Freight rates can increase by multiples of 2 or more when less than full-sized commercial volumes are procured. Monetization provides small- and medium-sized buyers access to the commodities at a landed price (e.g., cost, insurance and freight (CIF) price) that is comparable to prices a larger buyer would have paid for full-sized shipments of similar products. This benefit was highlighted in The Gambia (IRD), Uganda (ACDI/VOCA), Liberia (LOL), and Guatemala (PCI) case studies. In Uganda ACDI/VOCA stored imported wheat and buyers took delivery by truck, as needed. This enabled larger volumes per shipment to be brought in, thereby reducing freight rates.

Currency Risk Constraints – The risk of volatile exchange rates can prevent buyers

from purchasing on the global market. Monetization programs that allow buyers to purchase in local currency mitigate this risk. This benefit is highlighted in the evaluated Uganda and Mozambique case studies where monetization is conducted in local currency. A Uganda market analysis conducted by independent USAID contractors reported that “Title II wheat monetizations have played a pivotal role in developing a competitive domestic milling industry, by providing high-quality wheat under favorable sales contracts that are generally not available through regular commercial sales (including payment in Ugandan shillings).”7

Hard Currency Constraints – When sales are made in local currency, a country that

has limited hard currency reserves is able to import more food commodities without making a difficult tradeoff between food, fuel, and other necessary imported goods. Of the cases evaluated, payment was made in local currency for Uganda and Mozambique.

Price Constraints – The worldwide run up in commodity prices during late 2007 and

early 2008 made commercial commodity imports cost prohibitive for many net food-importing, developing countries. Monetization levels slightly increased in some countries to help fill the gap, although the amounts provided through monetization were too small to offset the declining imports. For example, due to the high price environment, total commercial wheat imports in Mozambique fell by 153,512 MT from 2007 to 2008, and total wheat imports for monetization only increased by 2,190 MT. In Uganda, from 2007 to 2008, commercial wheat imports fell 94,639 MT and total monetized wheat increased by 9,900 MT.

7 Fintrac. “USAID Office of Food for Peace Uganda Bellmon Estimation”. USAID. July 2011.

7

As described above, monetization helps overcome market constraints and thereby creates business opportunities and/or adds volume to the food available within the country. In some cases, overcoming these constraints improves the quality and/or nutritional value of the food available. For example, through IRD’s program in The Gambia, consumers had access that they would not otherwise have had to soybean oil, which has better nutritional value than the vegetable oils that are typically imported (which is higher in saturated fat). In Mozambique millers had the opportunity to produce higher quality flour by blending high-protein hard red winter and northern spring wheat varieties with the soft wheat varieties typically available in Mozambique. Well timed monetization deliveries can also even out food availability throughout the year, alleviating local market price volatility. In the Uganda program, shipments are planned to arrive when market supplies are low, helping to stabilize local prices. However, this important advantage can be disrupted if administrative agencies (USDA and USAID) are not able to order commodities to meet the schedules requested by implementing agencies For the McGovern-Dole International Food for Education and Child Nutrition program, cash support is not always made available for ITSH (internal transportation, storage and handling) and related costs. Therefore, monetization serves as a flexible funding tool when direct funding is not an option. For example, in the Guatemala Food for Education program implemented by PCI, soybean meal, a product that is growing in demand due to the expansion of poultry production, was monetized and the sales proceeds were used to support the ITSH costs of the school feeding program. The amount monetized was small compared to total import requirements: from 2009 through 2011, monetized soybean meal under this program averaged less than 3% of total soybean meal imports. Best Practices: Determination of the “Fair Market Value” As previously noted, all cases evaluated in this study achieved a “fair market value,” that is, the sales price was comparable to prices for similar quality products available on the market in the country where the sales took place, or, if limited volume is traded on the local market, the price that local buyers would have to pay to obtain similar quality products off of the world market. This was determined by an evaluation of the fair market value for the monetized commodity at the time the sales contract was signed. Obtaining the fair market value minimizes the potential for any adverse impacts on the market or disruption of commercial trade. Both USAID and USDA already require detailed reports from private voluntary organizations and cooperatives during the course of program implementation, including information about the monetization of commodities. Thus, the fair market value analysis can be included in those regular program reports.

8

There are two appropriate ways to determine the fair market value for a commodity that will be sold in a foreign country: (1) direct in-country market analysis and (2) determination of the “import parity price.” Both methods reflect best practices. Since circumstances vary by country and commodity, it is important that implementing organizations have the opportunity to use either method when determining the fair market value for a monetized commodity. Method 1 - Direct In-Country Market Analysis: Before a sales agreement is signed, implementing agencies conduct a market analysis to determine prevailing prices and market trends for the commodity and similar or substitute commodities in the country where it will be sold. This is completed by collecting information from a variety of sources, such as the port of entry, customs offices, wholesale markets and market participants. If reliable local price information is available, such data can be used to establish the fair market value, after adjusting for quality variations, as necessary. Quality adjustment can be made by looking at average price premiums and discounts on the world market between the evaluated qualities, focusing on prices in key exporting countries. Method 2 - Calculate the Import Parity Price: When, local price data is unavailable or unreliable, evaluating the import parity price (IPP) is a good way to determine the fair market value. The IPP represents the price that local buyers would have to pay to obtain similar quality products off the world market. Since transactions between major buyers and sellers at primary export points are relatively transparent, they can give guidance as to what represents a fair market value for a particular commodity. The following steps are taken to calculate the IPP and used to determine the fair market value in relation to the local market where the commodity will be monetized: Determine the best quality match for the commodity.

Identify appropriate export point(s) with transparent prices.

Determine the “commodity, insurance and freight” or “CIF” price for the commodity by adding by adding: (1) the FOB price (“free on board,” the price of a commodity at the loading port); (2) the prevailing ocean freight rate from that market to the port where the commodity will be off-loaded; and (3) the prevailing insurance costs for shipping the commodity to the port where it will be off-loaded.

Determine off-load and handling charges at receiving points.

Where applicable, quantify internal transportation, storage and handling costs.

9

Key Benefits/Risks by Case Study The following lists key risks and benefits specific to each of the evaluated case studies.

Key Benefits Key Risks

The Gambia – Vegetable Oil – IRD

There is sufficient domestic demand and insufficient domestic production.

Domestic production comprised between 10% and 16% of domestic annual vegetable oil supply from 2000 to 2007.

Gambian consumers gained access that they would not otherwise have had to soybean oil, which has better nutritional value relative to the palm oil that they generally purchase (which is higher in saturated fat).

Small lots of soybean oil were made available for sale and such small quantities would have been difficult and cost-prohibitive for the buyers to obtain on the world market.

There was no adverse impact on local production of vegetable oil.

The quantity of monetized soybean oil is small relative to domestic oil crop production. Between 2008 and 2010, monetized soybean oil accounted for 1% of the total vegetable oil crop production in The Gambia.

There has been no disruption to commercial trade.

The monetized soybean oil share of total vegetable oil imports was small, averaging less than 5%.

IRD received a fair market value for the soybean oil after a competitive and transparent tender process, indicating that the monetization did

The cost recovery rate* was low relative to other monetization cases highlighted in this report for reasons outside of IRD’s control.

The procurement price paid by USDA for the soybean oil was high when compared to FOB Gulf soybean oil prices during the period when the commodity was shipped and monetized.

The length of time between the issuance of the sales tender by IRD in the Gambia and the delivery of the soybean oil created a risk factor that discouraged some buyers from offering bids, making the sales process less competitive.

U.S. soybean oil receives a premium on The Gambian market over the lower-priced refined palm oil that dominates imports, but it faces significantly higher transportation costs. Transit time is also longer (150 days versus 60 days), which imposes a price risk to buyers and can impact the sales price.

10

Key Benefits Key Risks

The Gambia – Vegetable Oil – IRD

not disrupt market prices or interfere with commercial trade.

Monetization proceeds are being used to improve production and processing revenues within the cashew value chain across three countries: Senegal, The Gambia, and Guinea Bissau. There are barriers to monetizing in Senegal and Guinea Bissau, so the proceeds from The Gambia monetization are providing regional benefits.

The Food for Progress monetization program is the major U.S. assistance program in The Gambia and plays an important role in advancing foreign policy. Food for Progress is a good match for expanding private sector agricultural development in The Gambia and providing an entry point for U.S. Embassy to engage the Gambian Government in discussions.

Key Benefits Key Risks

Guatemala – Soybean Meal – Project Concern International

There is high demand for soybean meal in Guatemala and insufficient domestic supply.

Guatemala does not produce any soybean meal and because of growth of the poultry industry, domestic demand is significant and growing.

The monetization did not have a negative impact on domestic production.

While Guatemala is a net food-importing developing country with significant demand for soybean meal, there are no significant market barriers preventing current monetization buyers from purchasing a comparable quality product from the open market.

Thus, monetization should only provide a very small amount compared to total import demand, which it did.

11

Soybean meal is not produced in Guatemala. Comparing the levels monetized to production of similar commodities in the country, soybean meal monetization accounted for 0.7% of overall grain and meal production.

The monetization of soybean meal did not disrupt commercial trade.

Monetization of soybean meal for all programs from 2009 through 2011 averaged less than 3% of total soybean meal imports.

PCI received a fair market value for the soybean meal, indicating the monetization did not disrupt market prices or interfere with commercial patterns of trade.

Engaging a local broker helped PCI achieve the fair market value.

The cost recovery* rate was 83%.

The buyer took possession of the cargo upon loading at the U.S. port. Therefore, the risk of port delays, which can occur when shipping food aid to Guatemala and can add to program costs, were the buyer’s responsibility.

Under the McGovern-Dole International Food for Education and Child Nutrition program, cash support is not always made available for ITSH (internal transportation, storage and handling) and related costs, which is the case with Guatemala. Thus, monetization served as a flexible funding tool that allowed the program to obtain the ITSH funds necessary to implement the school feeding program.

According to the Ministry of Education in Guatemala, primary school students in the Department of Huehuetenango complete only 1.5 years of schooling

It is also important that market demand is growing, since this decreases the chance of disrupting normal patterns of commercial trade.

A fair market value was achieved, even though there was only one official bid.

PCI took steps to attract more bidders by employing a local broker, but this did not change the number of bids received. This is likely attributable to the fact that a minimum sales price was set in the request for bids which was not attractive to all buyers.

12

on average, demonstrating the worst educational achievement in the entire country. Children in the program target area who attend school typically arrive at school hungry after walking an average of three kilometers to get there. Thus, the chief objective of this three-year school feeding program targeting 30,000 children is to use school feeding as a platform to: (a) improve school enrollment and attendance; (b) improve student health status; and (c) enhance the learning environment by improving school infrastructure. Besides providing school meals as an incentive for attendance, a key component of the program is to increase parent, community and local government participation and support for school feeding activities.

Key Benefits Key Risks

Liberia – Rice – Land O’Lakes

Liberia does not produce enough rice to cover its domestic consumption demands.

Since 2005, production has accounted for between 30% and 55% of Liberia’s domestic demand.

Buyers seeking less-than commercial volumes of rice are prevented from buying on the world market because the cost of shipping such small quantities is cost prohibitive. The monetization program helped overcome the barriers by providing an opportunity to buy smaller lots and allowing incremental payments.

The availability of parboiled rice was increased, thereby providing higher

The Liberian government’s import license restrictions and a lack of small buyer access to credit limit the ability of smaller players to import rice. Even though a line of credit was provided as part of the rice monetization, because the monetized rice was sold for U.S. dollars, smaller market players were not likely to participate.

13

Key Benefits Key Risks

quality rice to the population at large.

The monetization does not interfere with local production.

Over the past 3 years, rice consumption has averaged 340,000 MT, while local production only provided an average of 180,000 MT. With the end of Liberian Civil Wars, demand is growing. Thus, the monetization of 11,000 MT in 2012 did not interfere with local production.

Monetization of rice did not disrupt commercial trade.

The total amount of rice monetized in 2012 was small relative to total rice imports – equivalent to 6.8% of the average amount of rice imported over the preceding three marketing years, 2009-2011. (Final import data are not yet available for 2012, but total imports are likely to be higher than the past three-year average.)

Historically, there is no indication that monetization of rice has interfered with trade, since commercial imports have continued to rise.

LOL received a fair market value when it sold the rice, indicating that the monetization did not disrupt market prices or interfere with commercial trade.

The cost recovery* rate was high, 95%.

The program just started in 2012 and the objective is to improve meat value chains that were devastated by the civil war, focusing specifically on improved goat rearing. The program is promoting

14

Key Benefits Key Risks

commercial goat production, meat processing and marketing by re-stocking 21,000 goats and providing training in animal husbandry, fodder production and business management to 10,000 producers. Two slaughter-houses in Monrovia will be being renovated and 12 easy-to-use slaughter slabs will be added to improve meat safety. In addition to increasing incomes and expanding businesses, the program will benefit over 550,000 consumers in the targeted areas by improving the nutritional quality of the diet.

Key Benefits Key Risks

Mozambique – Wheat – World Vision

Mozambique is not a commercial wheat producer and locally available wheat varieties are mainly soft wheat.

Since FY2005, Mozambique’s wheat production-to-consumption ratio has ranged between 0.53% and 1.23%.

Monetizing hard wheat created the opportunity for millers to blend this higher-protein wheat with soft wheat to produce better quality flour.

The sales process was structured to encourage a variety of millers to participate in the tenders, by allowing payment in local currency and in installments (versus full payment upon receipt of the commodities).

This stimulated participation of small- and medium-sized enterprises that may not be able to buy on the world market because of

In some years the total volume of wheat monetized in Mozambique exceeded, 10% of total import volumes.

Even though BEST reports generally suggest that the 10% level should not be exceeded, there is no evidence that this was disruptive to local production or commercial markets in Mozambique.

In some years the country was not able to maintain commercial import levels due to high world market prices or the unexpected cancelation of sales contracts. In such years, it would be reasonable for monetization levels to increase as a percentage of total import volume. In fact, it may be desirable to increase monetization in such cases even if monetized amounts will exceed 10% of imports.

15

Key Benefits Key Risks

credit, hard currency and minimum volume constraints.

The importance of wheat monetization to fill supply gaps was very apparent when worldwide wheat prices spiked in 2008: Mozambique’s total commercial wheat imports plummeted by 153,512 MT from 2007 to 2008.

Monetization in Mozambique is for local currencies, thereby avoiding draw-down on the country’s limited hard currency reserves and eliminating the buyer’s foreign exchange risk.

The local currency proceeds also provide the added benefit of funding agriculture, nutrition and natural resource management programs in poor, crisis-prone areas of the country, in coordination with the Government of Mozambique’s nutrition and agriculture development strategies.

Monetization has not disrupted commercial trade.

As also noted by Donovan et al. (2010), Mozambique’s commercial wheat import volumes have been increasing, monetized volumes have been decreasing, and the monetized import share of total imports has been declining.

The monetization of the wheat was for the fair market value, indicating that monetization did not disrupt market prices or interfere with commercial trade.

Between 2009 and 2011, cost recovery* rates have averaged 80%. The cost recovery rate reached 101% for the first transaction in 2012.

Mozambique is a poor developing country that requires wheat imports to supply its milling industry and to meet consumer demand. A drop in supply can set back development of the industry and increase consumer prices.

16

Key Benefits Key Risks

Uganda - Wheat – ACDI/VOCA

There is sufficient domestic demand and insufficient domestic production.

Uganda only produced 6% of its domestic wheat needs in 2010.

Food availability has increased and quality has improved, relative to what would have been achieved without monetization, by:

Addressing credit constraints; Reducing buyer risk by allowing

purchases in domestic currency; Reducing cost-prohibitive prices

faced by small- and medium-sized buyers who need to buy less-than- commercial-sized volumes; and

Increasing the consumption of better quality flour by blending high-protein Hard Red Winter Wheat with soft wheat varieties.

Monetization has helped expand the capacity of the Uganda wheat milling industry.

The supply gap during the Russia export embargo was partially offset by monetization of wheat and the potential for market volatility was reduced.

There was no adverse impact on local production.

There was no disruption of commercial trade.

Total monetized wheat averaged 7.6% of total wheat imports from 2006-2010, and was 5.4% of imports in FY 2011.

Over the last four years, U.S. monetized wheat shipments to Uganda have been relatively flat,

One of the food aid shipments, or the announcement of that shipment, could have been better aligned with the market needs in Uganda. A case was noted where the price received was lower than desired because the shipment was announced after buyers had already filled their warehouses with wheat and, therefore, market demand was low.

Inland transportation costs to Uganda are high and infrastructure improvements would greatly improve the cost efficiency of supplying wheat and other imported products to the country.

17

Key Benefits Key Risks

while commercial imports reached a record high in 2009 and have remained high since then.

ACDI/VOCA received a fair market value for the wheat, indicating that the monetization did not disrupt market prices or interfere with commercial trade.

During the course of the FY 2007-2011 MYAP, the average cost recovery* rate was 82%. For the first monetization in FY 2012, the cost recovery rate was 91%.

From FY 2007-2012, ACDI/VOCA, along with sub-recipients Africare, the Lutheran World Federation and The AIDS Support Organization, as well as local NGOs and CBOs, implemented a $74.3 million food security program in northern Uganda, targeting poor, vulnerable populations. It improved agricultural productivity, household savings, nutrition, and hygiene, and thereby strengthened the ability of communities to withstand climatic and other shocks. Under the ACDI/VOCA program, 97,006 rural households (580,000 household members) received training and technical assistance and 309,400 people were assisted by rehabilitation of 249 km of rural feeder roads. ACDI/VOCA also provided 12 months of supplementary food rations and complementary services to 127,016 people living with HIV/AIDs and their family members.

* Cost recovery (for all evaluated cases) measures total monetization revenues (cost per metric ton times total tonnage) divided by monetization costs (commodity procurement cost, foreign- flag freight cost, and, where applicable, inland transportation, storage and handling costs).

18

II. INTRODUCTION

The United States provides agricultural commodities overseas to promote development and food security and to meet emergency needs. Most of the commodities are directly distributed to recipients (86% in fiscal year 20108). However, in some cases, commodities may be "monetized” -- sold on the market or to the government of the recipient country and the proceeds used for developmental activities. Two common criticisms of monetization found in the literature are summarized in the title of a June 2011 U.S. General Accountability Office (GAO) report: International Food Assistance: Funding Development Projects through the Purchase, Shipment, and Sale of U.S. Commodities is Inefficient and Can Cause Adverse Market Impacts. The basis for the GAO finding that food aid is “inefficient” is that the “cost recovery” of food aid monetization is generally less than 100% – e.g., the funds generated for development projects via the proceeds from the monetization of the commodities are less than the cost incurred to procure and ship the commodities to recipient countries. However, this basic cost recovery formula only tells part of the story; it is not sufficient for determining the value of monetization to a recipient country. “Cost recovery” only places a value on the sales’ proceeds and does not take into account additional benefits that accrue from the provision of the commodity itself. Additionally, GAO’s rationale for concluding that monetization “can result in adverse market impacts” is that there is insufficient and inconsistent collection of data by USAID and USDA to prove otherwise; a problem that can be addressed by better coordination between the agencies, a clearer description of what constitutes the “reasonable market price” for a commodity, and improved USAID and USDA data collection. This study summarizes the potential risks and benefits of monetization, as reviewed in the literature, and evaluates data from five specific monetization cases against those potential risks and benefits, and describes, in detail, several cases that demonstrate the value and need for food aid monetization beyond the generation of funds to conduct development activities. Best practices to minimize chances of any adverse local market impacts also are identified. The study found that, due to the practices used when designing and implementing the five reviewed programs, in each case (1) the sale of the commodities did not compete with local production, (2) the sale of the commodities did not disrupt commercial trade, and (3) the sale was for a fair market value (e.g., the sales price received for the commodity was comparable to prevailing market prices for similar commodities in the country of sale), which helps to mitigate market disruption. The best practice for determining the fair market value is described in the report.

8 GAO. 2001. “International Food Assistance: Funding Development Projects through the Purchase,

Shipment, and Sale of U.S. Commodities is Inefficient and Can Cause Adverse Market Impact”.

19

III. PROJECT SCOPE & METHODOLOGY

A. Scope

Based on a review of the legislative requirements for monetization and a literature review of studies relevant to food aid monetization, Informa identified various benefits and costs that were often noted, sometimes with and sometimes without evidence or concrete examples. Based on this research, a set of critical questions was developed to use as Informa reviewed particular monetization cases. A set of 19 cases, representing a range of countries, commodities, organizations and program types, was provided by non-governmental organizations that agreed to provide data for use in this review. After reviewing those 19 cases, Informa refined its set of questions and identified a subset of five studies that represented a range of commodities, programs, countries and organizations that would provide sufficient data for an in-depth review. The non-governmental organizations representing these five cases provided applications and reports that had been submitted to the administrative agencies (USAID and USDA) and other information collected during the course of implementing the programs (such as tender and sales documents and ongoing market analysis). Informa also interviewed program representatives and collected relevant third-party reports and evaluations. For those five food aid monetization cases, Informa applied its study questions and evaluated a range of potential risks and benefits of monetization. The purpose was to determine value that may be gained from monetization beyond the generation of funds to conduct food security and developmental programs. In addition, while evaluating the programs and analyzing country-specific data, Informa sought to identify beneficial practices used in developing and implementing monetization programs that reduce the likelihood of interfering with local production or disrupting commercial trade patterns.

B. Methodology

1. Overview

Informa conducted a literature review of studies and policy reports that identified potential risks and benefits of food aid monetization and/or highlighted the successes/failures of specific cases. Some of the literature was based on opinion or assumption of what may happen if certain analyses and precautions were not taken, while others provided data analysis from actual cases. The objective of this literature review was not to critique or analyze existing studies, but rather to compile a list of commonly cited potential risks and benefits. This list was utilized when developing the key questions for evaluating each of the five case studies examined within this study – the “risks and benefits” questions. In addition, Informa reviewed the relevant laws and regulations for food aid programs to identify key requirements for monetization and incorporated analysis of whether those requirements were met into the “risks and benefits” questions.

20

Informa began with a group of 19 monetization cases provided by non-governmental organizations that are members of the Alliance for Global Food Security. A brief summary of each of these cases is presented in Appendix A. This group was narrowed down to five cases for more in-depth analysis. These cases were selected to represent a variety of countries, commodities and implementing organizations. Ongoing or recently-completed programs and programs for which independent analyses and evaluations had been conducted were preferred because of greater data availability. Each of the five cases was evaluated against the set of key “risks and benefits” questions... Within the scope of this study, Informa analyzed public data (including BEST reports and program evaluations, as well as data made available by USAID, USDA, FAO, and the Global Trade Atlas). Informa also evaluated data provided by Private Voluntary Organization (PVOs) about their programs, including reports provided to USAID and USDA, sales records, market assessments, and other information collected and reported in the course of implementing food aid programs. The scope of this study does not include field visits, but representatives of PVOs in the United States and in countries where the monetization took place were interviewed.

2. Key “Risks and Benefits” Study Questions & Methodology

Each case study was analyzed to answer the following questions: Was there sufficient domestic demand and insufficient domestic production to

warrant the monetization and importation of the chosen commodity?

Methodology Overview: This was evaluated by comparing historical production and consumption levels of the monetized commodity and related commodities in each of the evaluated countries.

Does food aid monetization provide benefits that would not be achieved with

alternative policy options (e.g., direct program funding)?

Does the monetization add to the food availability and/or quality? And/or has monetization aided market development?

Is there another reason for monetization over alternative policy options (e.g., direct program funding)?

Methodology Overview: This evaluation was based primarily on reports submitted by implementing agencies to USAID and USDA, other data provided by and interviews with program representatives from each of the reviewed countries, and information from published evaluations and reports. The purpose was to identify potential credit, currency, volume and/or other market barriers that may prevent buyers from purchasing the commodity or a similar quality product off of the open market. For example, in several of the evaluated cases small- or medium-sized

21

buyers were disadvantaged in sourcing commodities because they could not purchase commercial-scale quantities on the open market. Volume constraints were analyzed by comparing freight costs for commercial-scale shipments with the costs that would have likely been incurred to ship the smaller volumes that would have been transacted by the in-country buyers.

Has the monetization had an adverse impact on domestic production of the monetized commodity and/or related products?

Methodology Overview: This was evaluated by comparing both the volumes and trends of monetization of the commodity against the in-country production of that commodity and/or related products. Two key statistics were evaluated: (1) the transaction volume of the monetized commodity relative to total domestic production of that commodity (both with and without related products included); and (2) whether there was any historical correlation that might indicate that the level of monetization had a negative impact on production.

Has the monetization disrupted commercial trade of the monetized commodity and/or related products?

Methodology Overview: This was evaluated by comparing both the volumes and trends of the monetized commodity against the total imports of that commodity and/or related products. Two key statistics were evaluated: (1) the transaction volume of the monetized commodity relative to total imports of that commodity and related products; and (2) whether there was any historical correlation that might indicate that the level of monetization had a negative impact on imports. The Global Trade Atlas, FAO and USDA were the primary sources of information for this analysis.9

What is the average direct cost recovery rate?

Methodology Overview: The “cost recovery rate” equals revenues from sales divided by the costs of procuring and shipping the commodity, plus other costs incurred in carrying out the monetization. Revenue and cost data were provided by implementing organizations, which had collected the information during the course of program implementation in each of the reviewed countries. “Revenues” equal the transaction price multiplied by the volume. “Costs” are the sum of the commodity procurement price (price of the commodity at the U.S. loading port), ocean freight cost (prevailing foreign-flag rate at the time of sale for shipping the cargo from the U.S. port to the destination port), and, when applicable, internal transportation, storage, and handling costs (any additional costs incurred by the program after the

9 Implementing organizations observed that for some target countries, standard sources of

information on import levels, such as customs reports or exporting country records of exports to the recipient country, may under-report actual import levels because they do not capture illegal or informal trade.

22

cargo reaches the destination port to deliver the product to the in-country buyer[s]).10 A three-year average cost recovery rate (revenues divided by costs) was utilized whenever three years of data were available. If the commodity was monetized for less than three years, then the average cost recovery rate for the entire program was used. A three-year average cost recovery rate (revenues divided by costs) was utilized whenever three years of data was available (not all programs had monetized the evaluated commodity for three years).

3. Determination of Fair Market Value

For food monetization to be successful, it must not have an adverse impact on the domestic market or international trade. In fact, as noted under the section on “Potential Benefits and Risks of Food Aid Monetization” in chapter IV, these two areas are often cited as potential negatives of food monetization programs. Another common criticism is that the cost recovery rate is often less than 100%. In considering these issues, understanding what the “fair market value” in the global market is for the commodity to be monetized and how this fair market value relates to the local market is critical. Obtaining a fair market value can help improve the cost recovery rate as well as help to mitigate any potential negative market affects. With this in mind, this section describes the concept of fair market value as it relates to the monetization process and potential measures and procedures for determining the fair market value. The concept of a global fair market value is usually defined by market participants in terms of transparent prices observed at major export and import locations. Typical export movements from major suppliers to major buyers are usually in large, ship-lot sizes of 45 thousand MT to 60 thousand MT. Transactions between major buyers and sellers at primary export points are relatively transparent and can give guidance as to what represents a fair market value in global terms. Using wheat as an example, the chart below shows wheat prices at major wheat exporting points in different parts of the world.

10