the voracity and scarcity effects of export booms and ... · the voracity and scarcity effects of...

TRANSCRIPT

The Voracity and Scarcity Effects of Export Booms and Busts on Firm Bribery

Joël Cariolle, Research Officer

Foundation for Researches and Studies on International Development (FERDI),

Clermont-Ferrand, France,

The opinions expressed and arguments employed herein are solely those of the authors and do not

necessarily reflect the official views of the OECD or of its member countries.

This document and any map included herein are without prejudice to the status of or sovereignty over

any territory, to the delimitation of international frontiers and boundaries and to the name of any

territory, city or area.

This paper was submitted as part of a competitive call for papers on integrity, anti-corruption and trade

in the context of the 2016 OECD Integrity Forum.

1

Abstract

The evidence of a “voracity effect” of revenue windfalls fostering rent-seeking and corruption is

widely documented by the literature. However, the reverse hypothesis of a “scarcity effect” of

revenue downfalls, stimulating corruption by creating resource shortages, finds theoretical

foundations but less empirical support. This paper tests the concomitance of a voracity and

scarcity effect, by examining the effect of export booms and busts on firm bribery within a multi-

level estimation framework. Based on 19,712 bribe reports of firms located in 36 developing

countries, estimations support a positive effect of both export booms and busts on bribery, when

financial and democratic institutions are failing. Conversely, a robust negative effect of booms

and busts is evidenced when institutions are better off. Therefore, consistent with the literature,

this paper gives additional evidence on the importance of institutional safeguards against

corrupt practices in times of abundance. But more importantly, it provides new insights into

their importance in times of shortage.

Keywords

corruption, rent-seeking, export instability, booms, busts, financial markets, democracy,

institutions

2

1. INTRODUCTION

The resource curse literature provides theoretical predictions and empirical findings that

support a ‘voracity effect’ of resource booms on growth, prevailing in weak institutional contexts

(Tornell and Lane, 1999; Sachs and Warner, 2001; Mehlum et al., 2006). According to these

studies, windfalls are detrimental to integrity in the public and private sectors because they

stimulate the ‘grabbing hand’ rather than the ‘productive hand’ of economic agents, especially

when institutions cannot keep agents away from entering in rent-seeking activities.

Conversely, the hypothesis of a ‘scarcity effect’, according to which corrupt behaviors could be

stimulated by revenue shortfalls, has not yet been considered by empirical studies. However, the

theoretical literature on queuing models (Lui, 1985) and auction models (Saha, 2001) of bribery

provides interesting insights into how corrupt behaviors help jumping the queue or diverting

rationed public goods. In these models, economic agents compete for scarce resources, thereby

giving strong discretionary powers to those who are charged with their allocation, and inciting

them to extract bribes. Therefore, both positive and adverse shocks may foster corrupt practices,

especially when institutions are ‘grabber-friendly’ rather than ‘producer-friendly’ (Mehlum et

al., 2006).

However, the possibility of concomitant voracity and scarcity effects has not yet been explored

by the literature. To test the coexistence of these two effects, I estimate the separate effects of

aggregate export booms and busts on firm-level bribery, and I emphasize the role institutions in

this relationship. Multi-level cross-section estimations are conducted, by exploiting micro-level

data on 19,712 bribe reports from firms located in 36 developing countries. A significant and

robust positive effect of both export booms and busts on firms’ informal payments is found

when pillars of democracy are weak and when financial markets are imperfect. Conversely, a

significant and robust negative effect of booms and busts on bribery is evidenced when

democratic and financial institutions are better off.

The next section presents the literature review and the analytical framework. The third section

details the data and explains the multi-level estimation framework. The fourth section exposes

empirical results. The fifth section concludes.

3

2. LITERATURE REVIEW AND ANALYTICAL FRAMEWORK

Many studies point out that if countries with weak institutions undergo resource windfalls, rent-

seeking behaviors are likely to spread and growth rates are likely to fall (Tornell and Lane, 1999;

Mehlum et al., 2006; Voors et al., 2011). This rise in opportunistic rent-seeking behaviors in a

context of resource abundance underlies the ‘voracity effect’ of shocks, highlighted by Tornell

and Lane (1999).

By contrast, theoretical papers suggest that rent-seeking and corruption may also spread in

contexts of resource scarcity. They argue that when public goods are rationed, corruption can

act as grease in resource allocation or redistribution mechanisms (Lui, 1985; Bardhan, 1997).

Therefore, one can also expect that falls in public and private revenues foster corruption by

making economic agents competing for scarce resources.

2.1. The symmetric effects of shocks on corruption

The influential work of Tornell and Lane (1999) gives interesting theoretical insights into how

‘voracious’ appetites for wealth accumulation are stimulated by temporary resource windfalls.

Their predictions have found strong empirical support from the resource curse literature (Sachs

and Warner, 1995; Mehlum et al., 2006; Van der Ploeg, 2011; Voors et al. 2011), which provides

various empirical evidence of the positive effect of economic booms on rent-seeking and

corruption. Public and private agents are therefore likely to engage in bribery, extortion or

embezzlement, when opportunities for corrupt transactions flourish. Therefore, such

‘opportunistic’ corrupt behaviors should spread during positive shocks and decline during

negative ones.

The question of how corrupt transactions expand during adverse shocks has been less

addressed by the empirical literature. It can however find interesting answers in queuing

models (Lui, 1985) or auction models (Saha, 2001) of bribery. These models focus on the

demand-side of bribery and emphasize how public servants may personally benefit from public

resource scarcity by extracting bribes from people competing for rationed public resources.

Moreover, it has been shown that public resource shortages can be exacerbated by corrupt

public officials who can artificially slow down the speed of the queue or generate additional red

tape, in order to extract more bribes from individuals (Aidt, 2003). In other words, when

resources get scarce, countries may be stuck in a high-corruption equilibrium (Mehlum et al.

2003), and bribery may become an informal pricing signal of public resource scarcity.

From the supply side of bribery, adverse shocks may put firms under economic or financial

stress, and may incite them to bribe in order to relieve the state burden and to get privileged

access to public resources. Therefore, corruption may be a way for both public and private

4

agents to cushion economic hardships. Such ‘survival’ corrupt behaviors underlie the scarcity

effect of shocks on corruption, characterized by a rise (decline) in survival corruption during

adverse (positive) shocks.

As a result, the effect of positive and negative shocks on corruption may be symmetric. The

following sub-section stresses how institutional safeguards against malpractices can make this

symmetric effect either positive or negative.

2.2. The role of institutions.

In their seminal work, Murphy et al. (1991) show that talents in an economy are split between

productive activities, which are conducive to growth through enhanced productivity and

innovations; and rent-seeking activities, which are harmful to growth by their negative effect on

productivity and institutions (Murphy et al. 1993). Building upon this literature, I state that i)

the voracity and scarcity effects of shocks on corruption depends on the attractiveness of rent-

seeking compared to production, and ii) that this relative attractiveness relies on the

institutional framework.

Mehlum et al. (2006) propose a theoretical model stressing how the direction of the effect of

natural resource windfalls on growth depends on whether institutions are more favorable to

producers (‘producer-friendly institutions’) or to rent-seekers (‘grabber friendly institutions’).

Could a same conditional effect hold during adverse shocks? In fact, good institutions – i.e.

effective rule of law, efficient financial markets, well-functioning democracy, and so on. – make

countries more resilient (Rodrik, 1998, 2000), and therefore help keeping productive activities

appealing during economic hardships.

To sum up, one can expect that opportunistic corruption spreads during positive shocks, and

that survival corruption spreads during negative shocks when institutions are ‘grabber friendly’.

On the contrary, opportunistic and survival corrupt behaviors are likely to decrease during

positive and negative shocks, respectively, when institutions are ‘producer friendly’. Table 1

summarizes this symmetric effect of positive and negative shocks, conditional on institutions.

5

Table 1. Institutions, asymmetric corrupt transactions, and the symmetric effect shocks.

Economic shocks

Institutions Positive shocks Negative shocks

Grabber-friendly institutions + opportunistic corruption + survival corruption

Producer-friendly institutions - survival corruption - opportunistic corruption

3. EMPIRICAL FRAMEWORK

This analytical framework is tested by analyzing the effect of rises and falls in export proceeds

on firms’ informal payments, conditional on the quality of institutions, in a sample of developing

countries. Corruption is therefore expressed as a function of positive shocks, negative shocks,

and a set of controls, including institutional variables:

𝐶𝑜𝑟𝑟𝑢𝑝𝑡𝑖𝑜𝑛 = 𝐸{𝑝𝑜𝑠𝑖𝑡𝑖𝑣𝑒 𝑠ℎ𝑜𝑐𝑘𝑠, 𝑛𝑒𝑔𝑎𝑡𝑖𝑣𝑒 𝑠ℎ𝑜𝑐𝑘𝑠|𝐼𝑛𝑠𝑡𝑖𝑡𝑢𝑡𝑖𝑜𝑛𝑠, 𝐶𝑜𝑛𝑡𝑟𝑜𝑙𝑠} (1)

Multi-level estimations of this corruption equation are conducted using micro data on firms’

bribery as dependent variable, macro-level measures of exports booms and export busts as

interest variables, along with a set of micro-level controls, macro-level controls, and sector-

dummy variables. Data sources and summary statistics are provided in Appendix A.

3.1. WBES data on firms’ experience of bribery and firms’ characteristics

The WBES data provides a comprehensive and comparable-internationally firm-level

assessment of business environment conditions around the world, encompassing a wide range

of information on the supply-side of bribery along with other firm-level characteristics.1 From

this dataset, two dependent variables reflecting bribe prevalence among firms are used.

The first dependent variable is the size of informal payments reported by firms, expressed as a

share of their total sales. This dependent variable is bi-dimensional because an increase in this

variable can be both induced by an increase in the incidence and/or an increase in the size of

bribes. However, it has been contended that respondents may under-report or over-report bribe

amounts (Clarke, 2011). One way to circumvent this problem is to derive from the first

1 WBES data has been collected according to a stratified random sampling with replacement, based on firm size, geographic location and sector of activity. Enterprises were interviewed between 2006 and 2014 and asked the following question: “We’ve heard that establishments are sometimes required to make gifts or informal payments to public officials to “get things done” with regard to customs, taxes, licenses, regulations, services etc. On average, what percent of total annual sales, or estimated total annual value, do establishments like this one pay in informal payments or gifts to public officials for this purpose?”

6

dependent variable a second and complementary dependent variable, equal to one if a firm has

reported an informal payment, and zero if it has reported no informal payment. The first

dependent variable will be termed “bribe payment”, while the second one will be termed “bribe

incidence”.

I also draw from the WBES dataset a range of firm-level controls that are expected to affect their

inclination to engage in corruption. Building on studies on the determinants of firm-level

corruption (Svensson, 2003; Hellman et al., 2003; Dabla-Norris et al., 2008; Diaby and Sylwester,

2015), I control for the logarithm of a firm’s total annual sales, for the share of direct and

indirect exports in total sales, for the firm’s size (using dummy variables for medium-size and

large-size firms, based on their number of employees), for the firm’s share of public ownership,

for its share of working capital funded by internal funds, its share of working capital funded by

public and private commercial banks, and its sector of activity (using sector dummies).

3.2. Export instability variables

The emphasis placed by this study on export fluctuations is first justified. The rationale behind

export boom and bust variables is then explained.

3.2.1. Export shocks as a major and primary source of macroeconomic instability in developing

countries.

The emphasis placed on export fluctuations is justified for various reasons. First, in developing

countries, the instability in export earnings has been pinpointed as a major source of output

fluctuations (Guillaumont, 2009; Guillaumont and Chauvet, 2001), with a dramatic impact on

growth, investment, tax receipt, redistribution policy, and development outcomes (Balassa,

1989; Bevan et al. 1993; Easterly et al., 1993; Guillaumont et al. 1999). Export windfalls and

downfalls therefore seriously affect, directly and indirectly, revenue inflows in the whole

economy, thereby disrupting households and firms’ economic decisions, including decisions to

engage in corrupt transactions.

Second, export instability is a primary source and mostly-exogenous of macroeconomic

instability, caused by external shocks such as ups and down in international commodity prices,

in the terms of trade, in international interest rates, but also internal shocks such as natural

resource discoveries or climate-related shocks (Jones and Olken, 2010). By contrast, focusing on

the effect of intermediate instabilities – related to growth, public spending or investment –

would lead to a possible downward bias if governance is good and the country is resilient

(Rodrik, 2000; Guillaumont, 2009), or an upward bias if governance is bad and the country is not

resilient (Acemoglu et al., 2003).

7

3.2.2. Identifying corruption responses to asymmetric shocks

The literature often introduces periodic shock variables to study their impact on institutional

outcomes (Voors et al., 2011). However, such an approach applied to corrupt transactions abuts

on the inertia of corruption levels. In fact, one can expect corrupt transactions to spread in

response to irregular and abrupt patterns of export fluctuations rather than regular or normal

fluctuations. Corruption decisions, by their very illegal or illicit nature, probably come after

successive shocks, especially when sharp fluctuations challenge institutional safeguards against

malpractices and make them unable keeping production more attractive than rent-seeking.

Therefore, the focus is placed on the effect of transitory booms and busts of exports, distributed

around a trend estimated over the last 15 years, exhibiting both deterministic and stochastic

paths.2 Variables of export booms and busts are derived from the four-year (t; t-3) skewness of

the distribution of exports around their trend:

2/32

3

ˆ

ˆ1

ˆ

ˆ1

100

T

it

itit

T

it

itit

it

y

yy

T

y

yy

TSkewness with T=[t;t-3] (2)

Where yit is the observed constant value of export in country i at time t, and �̂�it the mixed trend.

As stressed by Rancière et al. (2008), the skewness provides a de facto measure of the

asymmetry and abruptness of shocks around a reference value. The four-year calculation time

window has been chosen to capture the effect of short-run fluctuations. It therefore does not

reflect the asymmetry property of the entire export distribution, since enlarging the time

windows would come at the cost of having similar values of skewness for remote and recent

abrupt shocks, with a possible shift in their effect on bribe prevalence.3 Therefore, this variable

reflects the abruptness and asymmetry of shocks in light of the recent history of export

fluctuations.

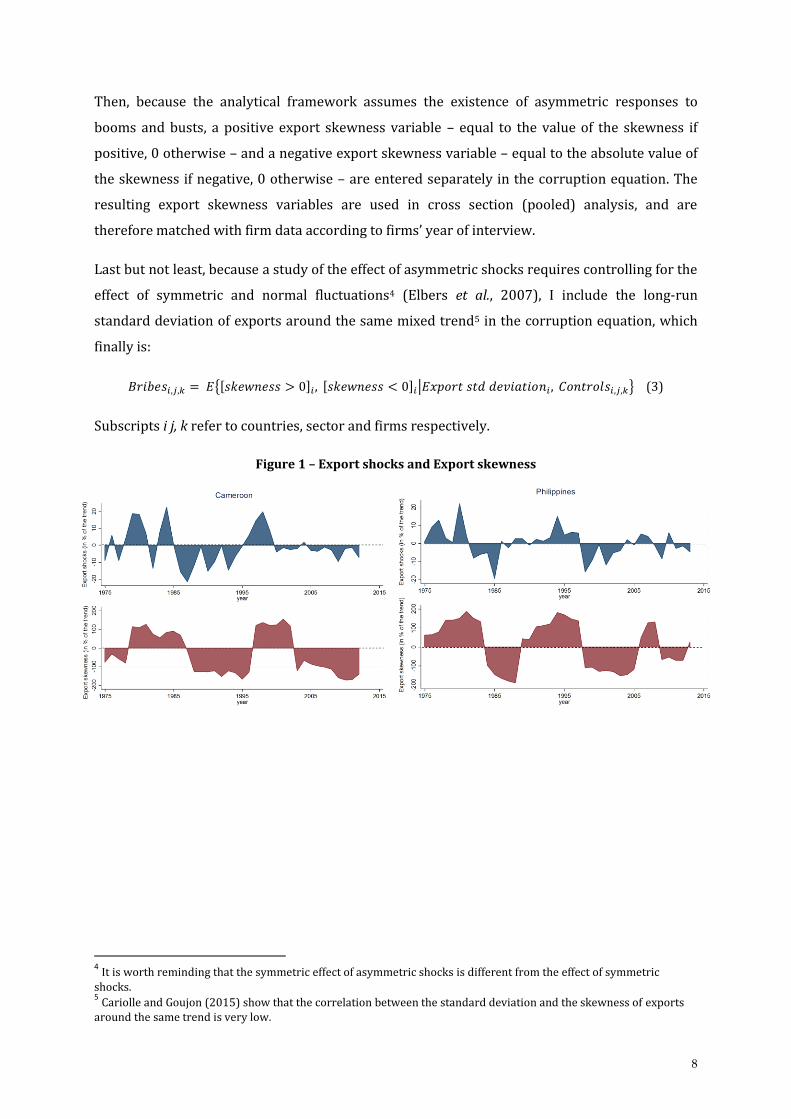

The time correlation between export shocks and export skewness series is illustrated in figure 1

for Pakistan, Philippines, Colombia, and Cameroon. One can see that, contrary to periodic export

shocks variables, the skewness of exports synthetizes well the asymmetry of fluctuations in the

recent history of shocks.

2 That is, a trend with the following shape: yt = α0 + α1. t + α2. yt−1 + ξt with y the constant value of exports, �t a zero-mean i.i.d disturbance term, t a 15 year time trend. See Cariolle and Goujon (2015) for a detailed discussion on

this trend estimation method. 3 Enlarging the time window to six does not change estimated relationships (hereafter presented) but lowers their

significance.

8

Then, because the analytical framework assumes the existence of asymmetric responses to

booms and busts, a positive export skewness variable – equal to the value of the skewness if

positive, 0 otherwise – and a negative export skewness variable – equal to the absolute value of

the skewness if negative, 0 otherwise – are entered separately in the corruption equation. The

resulting export skewness variables are used in cross section (pooled) analysis, and are

therefore matched with firm data according to firms’ year of interview.

Last but not least, because a study of the effect of asymmetric shocks requires controlling for the

effect of symmetric and normal fluctuations4 (Elbers et al., 2007), I include the long-run

standard deviation of exports around the same mixed trend5 in the corruption equation, which

finally is:

𝐵𝑟𝑖𝑏𝑒𝑠𝑖,𝑗,𝑘 = 𝐸{[𝑠𝑘𝑒𝑤𝑛𝑒𝑠𝑠 > 0]𝑖 , [𝑠𝑘𝑒𝑤𝑛𝑒𝑠𝑠 < 0]𝑖|𝐸𝑥𝑝𝑜𝑟𝑡 𝑠𝑡𝑑 𝑑𝑒𝑣𝑖𝑎𝑡𝑖𝑜𝑛𝑖 , 𝐶𝑜𝑛𝑡𝑟𝑜𝑙𝑠𝑖,𝑗,𝑘} (3)

Subscripts i j, k refer to countries, sector and firms respectively.

Figure 1 – Export shocks and Export skewness

4 It is worth reminding that the symmetric effect of asymmetric shocks is different from the effect of symmetric

shocks. 5 Cariolle and Goujon (2015) show that the correlation between the standard deviation and the skewness of exports

around the same trend is very low.

9

3.3. Institutional quality and other macro-level control variables

To test the effect of export booms and busts conditional on the quality of institutions, I

emphasize two separate dimensions of the institutional framework affecting the relative cost of

engaging corrupt transactions: on the one hand, key features of democracy affecting the

probability for corrupt agents of getting caught and sanctioned (Brunetti and Weder, 2003;

Bhattacharyya and Hodler, 2010, 2015), and supporting the protection of property rights and

the freedom of choice (Farhadi et al., 2015); and on the other hand, the performance of financial

markets, which determines the cost of alternative financial resources and the opportunity cost of

diverting resources through corruption (Altunbas and Thornton, 2012).

Democracy variables are drawn from the Freedom House (FH) database, which provides three

sets of variables reflecting three dimensions of modern democracies: the extent of civil liberties

(CL), of political rights (PR), and the freedom of the press (FotP).6 To proxy the imperfection of

financial market, I use three variables drawn from the World Development Indicators: the share

of domestic credit provided by the banking sector in GDP as a proxy for access to credit markets

(used as control variable in the baseline equation), the share of money and quasi-money (M2) in

GDP as an alternative proxy the overall financial development, and the index of credit

information depth which reflects the quality of credit information available through public or

private credit registries. These institutional variables will be separately used as interaction

terms in the corruption equation.

Finally, the baseline corruption equation comprises macro-level controls reflecting determinants

of corruption (Mauro, 1995; La Porta et al., 1999; Treisman, 2000) - that is, the GDP per capita,

the primary completion rate, the share of natural resource rents in GDP, the share of

government expenditures in GDP, the share of trade (exports plus imports) in GDP, the

6 Description of indices is given at https://freedomhouse.org/. The FotP Index ranges from 0 (the most free) to 100 (the least free), the CL and PR indices range from 1 (the most free) to 7 (the least free).

10

logarithm of the population, and the durability of the polity. Since James (2015) pointed out the

importance of sectorial characteristics in channeling the effect of revenue windfalls on

institutional quality, I also use sector dummies to control for it, including unobserved sector-

specific shocks. In the same way as for instability variables, country-level control variables are

matched with micro-level variables according to years of survey rounds.

3.4. Empirical method

The effect of export booms and busts on bribe payments and bribery incidence is estimated

within a three-level (country-sector-firm) estimation framework, based on a maximum

likelihood procedure. In fact, multi-level analysis is particularly fitted for this problematic, as it

takes into account the contextual nature of corrupt transactions (Martin et al., 2007), and allows

controlling for intra-class correlation between observations that could underlie a possible

contagion effects of corrupt transactions (Andvig and Moene, 1990). Therefore, adopting a

multi-level empirical framework should yield significant value to the study of macro-level

determinants of micro-level corrupt transactions.

3.4.1. General econometric framework

Pooled estimations of the following baseline econometric model are conducted:

𝐵𝑟𝑖𝑏𝑒𝑖,𝑗 ,𝑘 = 𝛽0 + 𝛽1. [𝑠𝑘𝑒𝑤 > 0]𝑖 + 𝛽2. [𝑠𝑘𝑒𝑤 < 0]𝑖 + 𝛽3. 𝑋𝑖 + 𝛽5. 𝑌𝑖,𝑗,𝑘 + 𝑑𝑗 + 휀𝑖,𝑗,𝑘 (4)

Where the dependent variable Bribei,j,k is either the amount or the incidence of informal

payments, Xi the macro-level controls, Yi,j,k the micro-level controls, dj the sector dummies and εi,j,k

an i.i.d residual.

In a second step, drawing on a similar specification as Murphy et al. (1991) and Bhattacharyya

and Hodler (2010), I estimate the effect of export booms and busts conditional on institutional

quality, by adding to the baseline model in equation (4) the interaction between export

skewness variables (skew) and institutional variables (instit), which gives:

𝐵𝑟𝑖𝑏𝑒𝑖,𝑗,𝑘 = 𝛿0 + 𝛿1. [𝑠𝑘𝑒𝑤 > 0]𝑖 + 𝛿2. [𝑠𝑘𝑒𝑤 < 0]𝑖 + 𝛿3. [𝑠𝑘𝑒𝑤 > 0 × 𝑖𝑛𝑠𝑡𝑖𝑡]𝑖 + 𝛿4. [𝑠𝑘𝑒𝑤 < 0 ×

𝑖𝑛𝑠𝑡𝑖𝑡]𝑖 + 𝛿5. 𝑖𝑛𝑠𝑡𝑖𝑡𝑖 + 𝛿6. 𝑋𝑖 + 𝛿7. 𝑌𝑖,𝑗,𝑘 + 𝑑𝑗 + 휀𝑖,𝑗,𝑘 (5)

3.4.2. Multi-level analysis

In a single-level estimation framework, it is assumed that observations are independent, i.e. that

residuals are uncorrelated at different layers of the data structure, are zero-mean and have

constant variance (Hox, 2010). However, various arguments regarding the very nature of

corruption decisions can be invoked to relax this assumption. First, previous studies highlighting

11

the holistic origin and the potential structuring role of corrupt systems in economic transactions

(Williamson, 2009; Andvig, 2006, Graef, 2005) strongly suggest that corruption is context-

dependent. In fact, in the same way as exam performances are markedly affected by unobserved

class and school characteristics, corruption decisions are driven by imbricated sector-level

(Diaby and Sylvester, 2015) and country-level (Martin et al. 2007) characteristics. Second, it has

been shown that “corruption may corrupt” (Andvig and Moene, 1990), suggesting that corrupt

transactions may be contagious within a given group of individuals and are therefore correlated

to each other. This problem of intra-class correlation induces loss of efficiencies and biases in

coefficient estimations (Hox, 2010). Third, amounts of reported informal payments as well as

missing data are also likely to be influenced by sector and country unobserved features. For all

these reasons, a multi-level framework is particularly relevant for the analysis of firms’

corruption decisions. The effect of export booms and busts on bribe payments and bribery

incidence is therefore estimated within a three-level (country-sector-firms) estimation

framework.

In three-level estimations, the total residual (εi,j,k) is modelled as a function of a country-level

(λi), a sector-level (μi,j), and a firm-level (νi,j,k) components, so that εi,j,k = λi + μi,j + νi,j,k. It is

assumed that these error components are random, i.e. that 𝐸{λi|𝑋𝑖 , 𝑌𝑖,𝑗,𝑘 , 𝑑𝑗} = 0,

𝐸{μi,j|𝑋𝑖 , 𝑌𝑖,𝑗,𝑘 , 𝑑𝑗, λi } = 0, and 𝐸{νi,j,k|𝑋𝑖 , 𝑌𝑖,𝑗,𝑘 , 𝑑𝑗, λi, μi,j } = 0. In addition to random intercepts,

the model also associates a country-level random component θ to the coefficients before export

skewness-related variables (including interaction terms modelled in equation (5)).7 Applied to

equation (4), the augmented three-level model is therefore the following:

𝐵𝑟𝑖𝑏𝑒𝑖,𝑗 ,𝑘 = 𝛽′0 + (𝛽′1 + 𝜃1,𝑖′ ). [𝑠𝑘𝑒𝑤 > 0]𝑖 + (𝛽′2 + 𝜃2,𝑖

′ ). [𝑠𝑘𝑒𝑤 < 0]𝑖 + 𝛽3. 𝑋𝑖 + 𝛽5. 𝑌𝑖,𝑗,𝑘 + 𝑑𝑗 +

λi + μi,j + ν𝑖,𝑗,𝑘 (4’)

The same decomposition of coefficients before shock-related variables applies to equation (5).

When the binary dependent variable on corruption incidence is used, I perform a probabilistic

linear multi-level modelling of equations (4) and (5), based on a maximum likelihood estimation

procedure, in order to avoid convergence problems (Caudill, 1988).8

3.4.3. Endogeneity issues

There are various reasons to expect that multi-level estimates of equations (4) and (5) reflect

the causal effect of export booms and busts on firms’ bribes. First, the literature on the

7 Random coefficients at the sector-level are not included since in the WBES dataset some firms are grouped within sectors which are not clearly defined. 8 due to the presence of sector dummy variables in our model. The resulting estimates are consistent with estimates obtained from a single-level Probit estimation framework. The latter can be provided upon request.

12

measurement of structural economic vulnerability (Guillaumont, 2009, Guillaumont and

Chauvet, 2001) considers the instability of exports around a random and deterministic trend as

a structural variable independent from policy-related factors, the latter being reflected in the

trend rather than in fluctuations around it. Second, and more importantly, even though export

shocks could be caused by poor policies (as suggested in Acemoglu et al. (2003) and Raddatz

(2007)), it is unlikely that a transaction undertaken by a single firm has macro-level

consequences (Farla, 2014). This argument should also hold when using democracy and

financial market variables as interaction terms in equation (5). However, as mentioned earlier,

corrupt transactions may be contagious within groups of firms (Andvig and Moene (1990)). In

statistical terms, this phenomenon is reflected by intra-class correlation, which could induce a

reverse causality bias if the contagious nature of bribes makes country exports fluctuating and

institutions failing.

Fortunately, the advantage of the three-level estimation framework set earlier is that it controls

for this source of endogeneity (Hox, 2010), in so far as this contagion effect plays at the sector

and/or the country-levels. Last but not least, three-level modeling takes into account sector-level

and country-level unobserved factors influencing firms inclination to report bribe payments or

stay silent, as well as inclination to under or over-report them. For all these reasons, we expect

estimates of the effect of booms and busts on bribery to be unaffected by reverse causality,

measurement error and omitted variable biases.

4. EMPIRICAL RESULTS

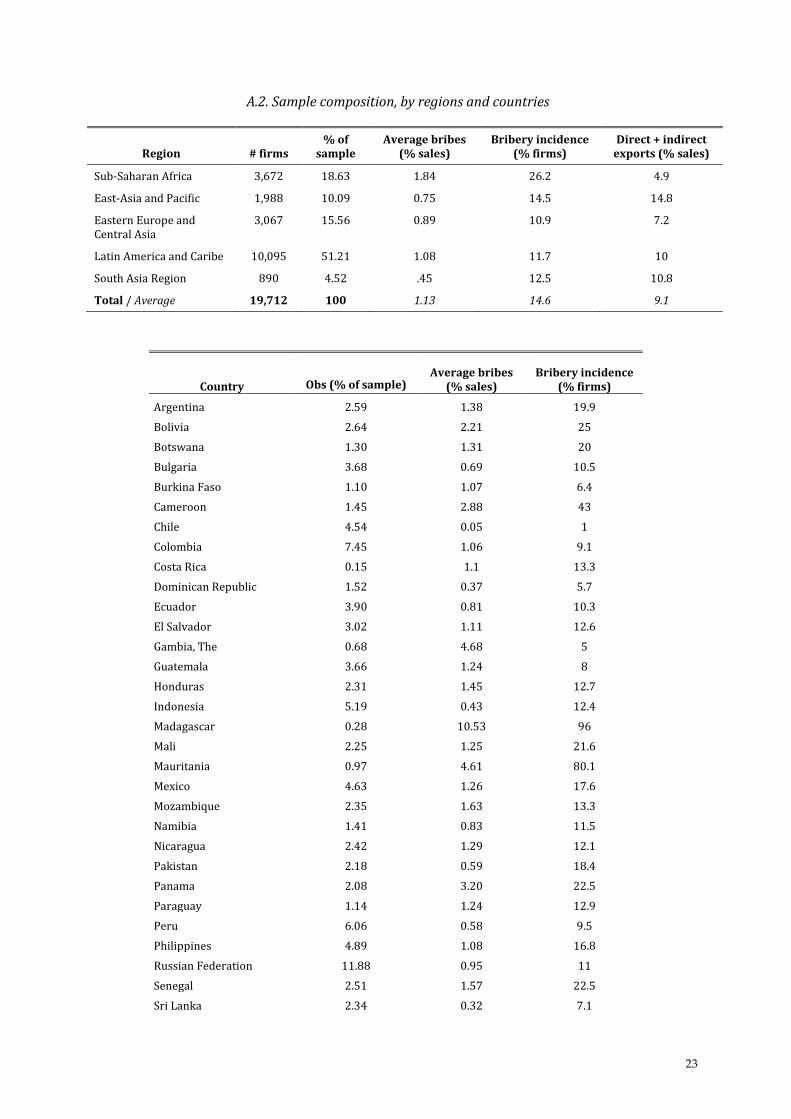

The baseline estimation sample consists of pooled data covering 19,712 firms, surveyed in 2006,

2007, 2009, 2010, 2011, and 2012, and located in 36 developing countries. Countries with less

than 30 observations have been removed from the sample. Summary statistics of variables used

in the empirical analysis, and statistics related to bribery and firms’ exports by country and

region are detailed in Appendix.

4.1. Preliminary evidence

Figure 4 exposes preliminary graphical evidence on the relationship between the skewness of

exports and bribery variables. In graph 4a), variables of bribe payments and bribe incidence

have been averaged by different ranges of skewness values for an extended sample of

developing countries. It shows that the prevalence of bribery is strictly increasing with the

intensity of positive shocks, supporting at first sight the existence of opportunistic corruption

spreading with export booms, consistently with the literature’s findings. A positive correlation

between the intensity of export busts and bribe prevalence is also apparent but nonlinear. Graph

4b) plots country averages of bribe payments and incidence against average values of export

13

skewness for the estimation sample. It provides additional illustration of the symmetric positive

correlation between export booms, export busts and corruption prevalence in developing

countries.

Figure 4. Export booms and busts and bribe prevalence in developing countries

a) Average bribe payment and incidence according to different ranges of export shocks intensity

Sample: 80 developing countries, 41,182 observations.

b) Graphical illustration of the correlation between country averages of export skewness and country averages of bribe prevalence in the estimation sample

Estimation sample: 36 developing countries, 19,712 observations.

4.2. Main results

To further the analysis, estimates of equation (4) are reported in table 2, and support previous

graphical relationships.9 Three-level estimates in columns (1) and (2) show a positive and

significant effect of export booms and export busts on the size of bribe payments, with an effect

9 Estimates of micro and macro-level controls are not reported but are displayed and commented in Cariolle (2016).

14

of booms of slightly larger magnitude than the effect busts. Estimation with the corruption

incidence variable in column (2) also points to a positive symmetric effect of booms and busts on

corruption incidence, but in less reliable confidence level.

Therefore, this first bunch of evidence highlights a consistent positive symmetric effect of export

booms and busts on firms’ bribery, but this symmetric effect seems reflected on the average size

of bribes rather than on their incidence. The stability of export skewness coefficients after

controlling for micro and macro-level determinants of bribery suggests that export movements

are independent from other controls. To sum up, these first estimations support that corruption

expands during both positive and negative shocks, thereby suggesting that most countries in the

baseline sample do not have strong-enough institutions to prevent firms from entering in

corruption during economic upheavals.

Table 2. The baseline equation – three-level estimations.

Dependent variable: Bribe payments Bribe incidence

(1) (2) (3) (4)

Export skewness >0 0.012*** (0.01) 0.010*** (0.01) 0.001** (0.05) 0.001 (0.31)

Export skewness <0 0.005*** (0.01) 0.004** (0.02) 0.001 (0.23) 0.001 (0.42)

Export standard deviation -0.004*** (0.00) 0.006 (0.77) -0.000 (0.47) 0.005*** (0.00)

Macro-controls No Yes No Yes

Micro-controls No Yes No Yes

Dummies firm size No Yes No Yes

Dummies sector No Yes No Yes

Wald Stat 71.51*** 162.39*** 23.37*** ..

LR Stat 567.44*** 257.7*** 1935*** 1223.8***

#Countries/#obs 36(19,712)

Controls are not reported. Standard errors are clustered by country. When possible, estimates are rounded up to three decimal spaces. P-values in parenthesis. *significant at 10%; **significant at 5%; ***significant at 1%.

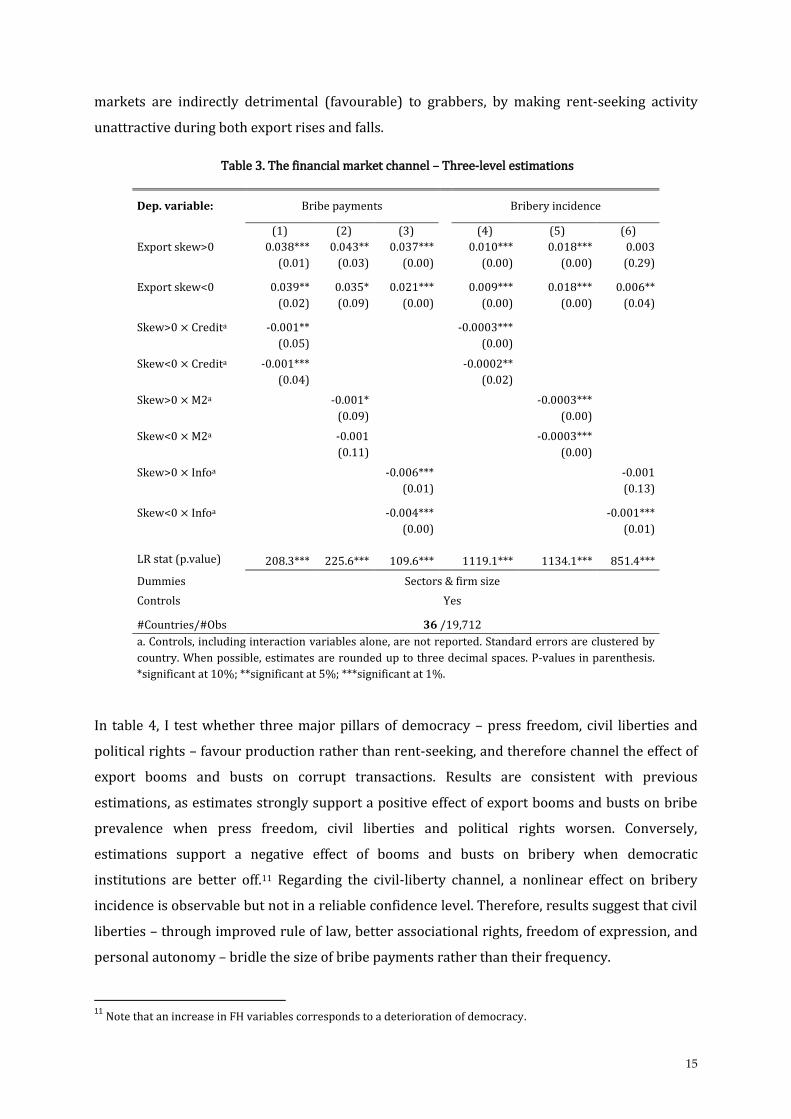

Table 3 reports multi-level estimates of equation (5), using as interaction terms the three

variables of financial market performance, separately. It provides significant and robust

evidence of a symmetric effect of export booms and busts conditional on financial market well-

functioning: export booms and busts are found to increase bribery when access to financial

services is restricted and when financial information is opaque, while they are found to reduce it

when access to financial services is improved and when financial information is more

transparent.10 Thus, empirical evidence strongly support that improved (failing) financial

10 Financial variable thresholds above/below which the direction of the effect reverses , and the number of countries above/below these thresholds, can be provided on request.

15

markets are indirectly detrimental (favourable) to grabbers, by making rent-seeking activity

unattractive during both export rises and falls.

Table 3. The financial market channel – Three-level estimations

Dep. variable: Bribe payments Bribery incidence

(1) (2) (3) (4) (5) (6)

Export skew>0 0.038***

(0.01)

0.043**

(0.03)

0.037***

(0.00)

0.010***

(0.00)

0.018***

(0.00)

0.003

(0.29)

Export skew<0 0.039**

(0.02)

0.035*

(0.09)

0.021***

(0.00)

0.009***

(0.00)

0.018***

(0.00)

0.006**

(0.04)

Skew>0 × Credita -0.001**

(0.05)

-0.0003***

(0.00)

Skew<0 × Credita -0.001***

(0.04)

-0.0002**

(0.02)

Skew>0 × M2a -0.001*

(0.09)

-0.0003***

(0.00)

Skew<0 × M2a -0.001

(0.11)

-0.0003***

(0.00)

Skew>0 × Infoa -0.006***

(0.01)

-0.001

(0.13)

Skew<0 × Infoa -0.004***

(0.00)

-0.001***

(0.01)

LR stat (p.value) 208.3*** 225.6*** 109.6*** 1119.1*** 1134.1*** 851.4***

Dummies Sectors & firm size

Controls Yes

#Countries/#Obs 36 /19,712

a. Controls, including interaction variables alone, are not reported. Standard errors are clustered by

country. When possible, estimates are rounded up to three decimal spaces. P-values in parenthesis.

*significant at 10%; **significant at 5%; ***significant at 1%.

In table 4, I test whether three major pillars of democracy – press freedom, civil liberties and

political rights – favour production rather than rent-seeking, and therefore channel the effect of

export booms and busts on corrupt transactions. Results are consistent with previous

estimations, as estimates strongly support a positive effect of export booms and busts on bribe

prevalence when press freedom, civil liberties and political rights worsen. Conversely,

estimations support a negative effect of booms and busts on bribery when democratic

institutions are better off.11 Regarding the civil-liberty channel, a nonlinear effect on bribery

incidence is observable but not in a reliable confidence level. Therefore, results suggest that civil

liberties – through improved rule of law, better associational rights, freedom of expression, and

personal autonomy – bridle the size of bribe payments rather than their frequency.

11

Note that an increase in FH variables corresponds to a deterioration of democracy.

16

To sum up, there are strong and robust empirical evidence, consistent with literature’s findings,

of a nonlinear symmetric effect of export sharp fluctuations on bribery, conditional on the

quality of financial markets and democratic institutions. On the one hand, the credit provided

domestically by the private sector and the depth of the financial information, and on the other

hand, an independent press and enforced political rights, appear as effective institutional

safeguards against the prevalence of corruption responses to shocks.

Table 4. The democracy channel – Three-level estimations.

Multi-level estimations

Dep. variable: Bribe payments Bribery incidence

(1) (2) (3) (4) (5) (6)

Export skew>0 -0.025***

(0.00)

-0.022***

(0.00)

-0.006

(0.19)

-0.003*

(0.08)

-0.003

(0.44)

-0.002***

(0.00)

Export skew<0 -0.031***

(0.01)

-0.018**

(0.02)

-0.016***

(0.00)

-0.016***

(0.01)

-0.007*

(0.09)

-0.009***

(0.00)

Skew>0 × FotPa 0.001***

(0.00)

0.0001**

(0.02)

Skew<0 × FotPa 0.001***

(0.01)

0.0003***

(0.00)

Skew>0 × CLa 0.012**

(0.00)

0.000

(0.62)

Skew<0 × CLa 0.008***

(0.00)

0.002

(0.19)

Skew>0 × PRa 0.007***

(0.01)

0.001***

(0.01)

Skew<0 × PRa 0.008***

(0.00)

0.003***

(0.00)

#Countries/#obs 36/19,712

Dummies Sector & firm size

Controls Yes

LR Test 160.6*** 159.9*** 197.6*** 1021.3*** 1017.7*** 1170.5***

Controls, including interaction variables alone, are not reported. Standard errors are clustered by country. P-values in parenthesis. *significant at 10%. When possible, estimates are rounded up to three decimal spaces. a. An increase in Freedom House’s indices corresponds to a deterioration of democracy.

4.3. Robustness check: four-level estimations

In robustness analysis, a four-level model is estimated, including years of interview as an

additional intermediary level in the data hierarchy, between the sector level and the firm level. It

is worth making sure that change in the modelling of the data structure does not alter previous

results. In fact, depending on country contexts, the overall confidence level towards surveyors

after repeated surveys may change. Ignoring this additional level in the data structure may

therefore eventually bias estimations.

The total residual (εi,j,k) in equations (4) and (5) is therefore modelled as a function of a country-

level random component (λi), a sector-level random component (μi,j), a year-level random

17

component (ρi,j,t) and a firm-level random component (νi,j,t,k), so that εi,j,t,k = λi + μi,j + ρi,j,t + νi,j,t,k.

The random slope component is kept at the country level. For convergence reason, we run four-

level estimation using the bribe-payment dependent variable only. Results are presented in

Appendix B. Estimated nonlinear relationships remain stable and significant, compared to three-

level estimates. Therefore, results are robust to the inclusion of the year of survey round as an

additional level of analysis in the model.

5. CONCLUDING REMARKS

This paper provides robust empirical evidence, consistent with literature’s findings, of a

“voracity effect” of export booms and a “scarcity effect” of export busts on bribe prevalence.

These effects are estimated within a three-level estimation framework, which allows a

contextualization of corrupt transactions at the sector and country-levels, thereby controlling

for sector and country unobserved features that could induce measurement errors, omitted

variable bias, and reverse causality bias.

Multi-level estimates support a nonlinear symmetric effect of export booms busts on bribe

payments and incidence, consistent with the resource curse literature (Mehlum et al., 2006;

Bhattacharyya and Hodler, 2010, 2015): export booms are found to foster bribe payments and

incidence when financial and democratic institutions are failing, and to reduce them when

institutions are better off. But more importantly, estimates point that export collapses in weak

institutional contexts may also be a curse, by inciting firms to compete for scarce resources and

to divert them through corruption and rent-seeking.

Last but not least, this study identifies policy levers that could dampen the positive symmetric

effect of export booms and busts on bribe prevalence: policies aimed at improving the

functioning of financial markets and supporting civil liberties, political rights and press freedom

should prevent firms from entering in corruption during economic booms and economic

hardships, by keeping productive activities more attractive than rent-seeking. In short, this

paper gives additional evidence on the importance of institutional safeguards against corrupt

practices in times of abundance, and new insights into their importance in times of shortage.

18

ACKNOWLEDGEMENTS

The author is grateful to Patrick Guillaumont, Elise Brezis, Bernard Gauthier, Jan Gunning,

Olivier Cadot, Michaël Goujon, Jean-louis Combes, Laurent Wagner, Gaëlle Balineau, Alexis Le

Nestour, Aurélia Lepine, as well as participants at research seminars at Navarra University

(Spain) and Gretha (Bordeaux), at the 2014 EPCS meeting in Cambridge (April, 4-6, 2014), at the

63th annual congress of the AFSE in Lyon (June, 18-16, 2014), and at the 2015 Ferdi workshop

“Commodity market instability and asymmetries in developing countries: Development impacts

and policies”, for helpful comments and suggestions. This paper benefited from the support of

the FERDI (Fondation pour les etudes et recherches sur le développement international) and the

French Government’s ‘Investissement d’Avenir’ programme (reference ANR-10-LABX-14-01).

Remaining errors are mine.

19

REFERENCES

Acemoglu, D., Johnson, S., Robinson, and Thaicharoen J Y. (2003). Institutional causes,

macroeconomic symptoms: instability, crises and growth. Journal of Monetary Economics, 50(1),

49-123.

Altunbas, Y., and Thornton, J. (2012). Does Financial Development Reduce Corruption?.

Economics Letters, 114(2), 221–223.

Andvig, J.C. (2006). Corruption and Fast Change. World Development, 34(2), 328-340.

Andvig, J. C., and Moene, K. O. (1990). How corruption may corrupt. Journal of Economic Behavior

& Organization, 13(1), 63-76.

Balassa, B. (1989). Temporary windfalls and compensation arrangements. Weltwirtschaftliches

Archiv, 125(1), 97-113.

Bardhan, P. (1997). Corruption and development: A review of issues. Journal of Economic

Literature, 35(3), 1320-1346.

Bevan, D., Collier, P. and J.W. Gunning (1993). Trade shocks in developing countries,

Consequences and policy responses. European Economic Review, 37(2-3), 557-565.

Bhattacharyya, S., and Hodler, R. (2015). Media freedom and democracy in the fight against

corruption. European Journal of Political Economy, 39, 13-24.

Bhattacharyya, S., and Hodler, R. (2010). Natural resources, democracy and

corruption. European Economic Review, 54(4), 608-621.

Cariolle, J., and M. Goujon (2015) Measuring Macroeconomic Instability: A critical Survey

Illustrated with Export Series. Journal of Economic Surveys, 29, 1-26.

Caudill, S. B. (1988). Practitioners corner: An advantage of the linear probability model over

probit or logit. Oxford Bulletin of Economics and Statistics, 50(4), 425-427.

Clarke, G.R.G. (2011). How Petty is Petty Corruption? Evidence from Firm Surveys in Africa.

World Development, 39(7), 1122-1132.

Dabla-Norris E., Gradstein, M. and G. Inchauste (2008). What causes firms to hide output? The

determinants of informality. Journal of Development Economics, 85, 1–27.

Diaby, A., and K. Sylwester (2015). Corruption and Market Competition: Evidence from Post-

Communist Countries. World Development, 66, 487–499.

Easterly, W., Kremer, M., Pritchett, L., and Summers, L. H. (1993). Good policy or good

luck?. Journal of Monetary Economics, 32(3), 459-483.

Elbers, C., Gunning, J.W., and B.H. Kinsey (2007). Growth and Risk: Methodology and Micro

Evidence. World Bank Economic Review, 21(1), 1-20.

20

Farhadi, M., Islam, M. R., & Moslehi, S. (2015). Economic Freedom and Productivity Growth in

Resource-rich Economies. World Development, 72, 109-126.

Farla, K. (2014). Determinants of firms’ investment behaviour: a multilevel approach. Applied

Economics, 46(34), 4231-4241.

Guillaumont, P. (2009). Caught in a trap: Identifying the Least Developed Countries. Economica.

Guillaumont, P., and L. Chauvet, (2001). Aid and Performance : A Reassessment. Journal of

Development Studies, 37(6), 66-92.

Guillaumont, P., Guillaumont-Jeanneney, S., and J-F. Brun (1999). How Instability Lowers African

Growth. Journal of African Economies. 8(1), 87-107.

Hellman, J. S., Jones, G., and D. Kaufmann (2003). Seize the state, seize the day: state capture and

influence in transition economies. Journal of Comparative Economics, 31(4), 751-773.

Hox, J.J. Multi-level Analysis, Techniques and Applications, Quantitative Methodology Series,

Rouledge, 2010.

James, A. (2015). The resource curse: A statistical mirage?. Journal of Development

Economics, 114, 55-63.

Jones, B.F., and B. Olken (2010). Climate Shocks and Exports. American Economic Review: Papers

& Proceedings, 100, 454–459.

La Porta, R., Lopez-de-Silanes, F., Shleifer, A., and Vishny, R. (1999). The quality of

government. Journal of Law, Economics, and Organization, 15(1), 222-279.

Lui, F.T. (1985). An Equilibrium Queuing Model of Bribery. Journal of Political Economy, 93(4),

760-781.

Martin, K. D., Cullen, J. B., Johnson, J. L., and Parboteeah, K. P. (2007). Deciding to bribe: A cross-

level analysis of firm and home country influences on bribery activity. Academy of Management

Journal, 50(6), 1401-1422.

Mauro, P. (1995). Corruption and growth. The Quarterly Journal of Economics, 110(3), 681-712.

Mehlum, H., Moene, K., and R. Torvik (2006). Institutions and the resource curse. Economic

Journal, 116(508), 1-20.

Mehlum, H., Moene, K., and R. Torvik (2003). Predator or prey? Parasitic enterprises in economic

development. European Economic Review, 47(2), 275-294.

Murphy, K.M., Shleifer, A., and R.W. Vishny (1993). Why is Rent-Seeking so Costly to Growth. The

American Economic Review, 83(2), 409-414.

Murphy, K.M., Shleifer, A., and R.W. Vishny (1991). The Allocation of Talent: Implication for

Growth. The Quarterly Journal of Economics, 106(2), 503-530.

21

van der Ploeg, F. (2011). Natural Resources: Curse or Blessing?. Journal of Economic Literature,

49(2), 366-420.

Raddatz, C. (2007). Are external shocks responsible for the instability of output in low-income

countries? Journal of Development Economics, 84, 155–187.

Rancière, R., Tornell, A., and F. Westermann (2008). Systemic crises and growth. The Quarterly

Journal of Economics, 123(1), 359-406.

Rodrik, D. (2000). Participatory Politics, Social Cooperation, and Economic Stability. American

Economic Review, 90(2), 140-144.

Rodrik, D. (1998). Why do more open economies have bigger governments? Journal of Political

Economy, 106(5), 997-1032.

Sachs, J. D., and A.M. Warner (2001). The curse of natural resources. European economic

review, 45(4), 827-838.

Saha, B. (2001). Red tape, incentive bribe and the provision of subsidy. Journal of Development

Economics, 65, 113–33.

Svensson, J. (2003). Who Must Pay Bribes and How Much? Evidence from a Cross Section of

Firms. The Quarterly Journal of Economics, 118(1), 207-230.

Tornell, A., and P.R. Lane (1999). The Voracity Effect. The American Economic Review. 89(1), 22-

46.

Treisman; D. (2000). The causes of corruption: a cross-national study. Journal of Public

Economics, 76(3), 399-457.

Voors, M.J., Bulte, E.H., and R. Damania (2011). Income Shocks and Corruption in Africa: Does a

Virtuous Cycle Exist?. Journal of African Economies, 20(3), 395-418.

Williamson, C.R. (2009). Informal institutions rule: institutional arrangements and economic

performance. Public Choice, 139(3-4), 371-387.

22

APPENDICES

A.SUMMARY STATISTICS

A.1. Sample summary statistics

Source Mean Std. Dev.

Bribe payments (in % of total sales)

WBES

1.133 4.718

Bribery incidence (in % of firms] 14.62 35.34

Log total sales 16.94705 3.199014

State ownership (% firms) 0.3216315 4.704202

Indirect exports (% of firm’s sales) 2.585486 12.82395

Direct exports (% of firm’s sales) 6.538187 20.46367

Internal funds (% of working capital) 65.99668 36.38616

Public and private commercial funding

(% of working capital) 13.36995 24.25725

% of large-size firms 18.71 39.00

% of medium-size firms 33.13 0.4707002

% of small-size firms 48.15 0.4996716

Export std dev (in % of trend)

World

Development

Indicators

(Doing Business)

10.33 22.40

Export skewness > 0 (in % of trend) 38.59 55.51

Export skewness < 0 (in % of trend) 76.21 69.10

Primary completion rate 90.27 16.89

GDP per capita (2005 Constant USD) 3616 2558

Log population 15.40 2.72

Dom. credit to private sector (% GDP) 34.74 20.61

M2 ( % of GDP) 42.45574 15.06237

Depth of credit info index 4.259334 2.117428

Gvt final consumption (% of GDP) 13.30 3.62

Trade openness (% in GDP) 66.88 27.89

Natural resource rents (% of GDP) 10.65 8.11

Political regime durability (in years) Polity IV 17.29 12.62

FotP global index

Freedom House

51.91 15.88

CL global Index 3.271053 1.135549

PR global Index 3.19166 1.665923

23

A.2. Sample composition, by regions and countries

Region # firms % of

sample Average bribes

(% sales) Bribery incidence

(% firms) Direct + indirect

exports (% sales)

Sub-Saharan Africa 3,672 18.63 1.84 26.2 4.9

East-Asia and Pacific 1,988 10.09 0.75 14.5 14.8

Eastern Europe and Central Asia

3,067 15.56 0.89 10.9 7.2

Latin America and Caribe 10,095 51.21 1.08 11.7 10

South Asia Region 890 4.52 .45 12.5 10.8

Total / Average 19,712 100 1.13 14.6 9.1

Country Obs (% of sample) Average bribes

(% sales) Bribery incidence

(% firms)

Argentina 2.59 1.38 19.9

Bolivia 2.64 2.21 25

Botswana 1.30 1.31 20

Bulgaria 3.68 0.69 10.5

Burkina Faso 1.10 1.07 6.4

Cameroon 1.45 2.88 43

Chile 4.54 0.05 1

Colombia 7.45 1.06 9.1

Costa Rica 0.15 1.1 13.3

Dominican Republic 1.52 0.37 5.7

Ecuador 3.90 0.81 10.3

El Salvador 3.02 1.11 12.6

Gambia, The 0.68 4.68 5

Guatemala 3.66 1.24 8

Honduras 2.31 1.45 12.7

Indonesia 5.19 0.43 12.4

Madagascar 0.28 10.53 96

Mali 2.25 1.25 21.6

Mauritania 0.97 4.61 80.1

Mexico 4.63 1.26 17.6

Mozambique 2.35 1.63 13.3

Namibia 1.41 0.83 11.5

Nicaragua 2.42 1.29 12.1

Pakistan 2.18 0.59 18.4

Panama 2.08 3.20 22.5

Paraguay 1.14 1.24 12.9

Peru 6.06 0.58 9.5

Philippines 4.89 1.08 16.8

Russian Federation 11.88 0.95 11

Senegal 2.51 1.57 22.5

Sri Lanka 2.34 0.32 7.1

24

Swaziland 1.42 1.26 40

Togo 0.51 0.91 12.9

Uruguay 2.51 0.17 4

Venezuela, RB 0.59 3.06 36.7

Zambia 2.39 1.12 16.1

Total / average 100.00 1.13 14.6

25

B. FOUR-LEVEL ESTIMATIONS

Dep. variable: Bribe payments

(1) (2) (3) (4) (5) (6) (7)

Export skew>0 0.010*** (0.01) 0.037*** (0.01) 0.041*** (0.00) 0.037*** (0.00) -0.025** (0.02) -0.022*** (0.00) -0.006 (0.20)

Export skew<0 0.003 (0.14) 0.037*** (0.01) 0.033*** (0.00) 0.021*** (0.00) -0.029*** (0.01) -0.018*** (0.00) -0.014** (0.00)

Financial market performancea

Skew>0 × Credit -0.001*** (0.00)

Skew<0 × Credit -0.001*** (0.00)

Skew>0 × M2 -0.001** (0.03)

Skew<0 × M2 -0.001*** (0.00)

Skew>0 × Info -0.006*** (0.00)

Skew<0 × Info -0.004*** (0.00)

Democracya

Skew>0 × FotP 0.001*** (0.01)

Skew<0 × FotP 0.001*** (0.00)

Skew>0 × CL 0.012*** (0.00)

Skew<0 × CL 0.008*** (0.00)

Skew>0 × PR 0.006*** (0.00)

Skew<0 × PR 0.007*** (0.00)

#Countries/#obs 36/19,712

Dummies Sector, firm size

Controls Yes

Wald Stat(pvalue) 136.1*** 141.4*** 134.1*** 589.2*** 145.9*** 181.3*** 178.3***

LR Test 254.3*** 226.8*** 242.7*** 876.6*** 235.9*** 204.5*** 202.7***

a. Controls, including interaction variables alone, are not reported. P-values in parenthesis. *significant at 10%; **significant at 5%; ***significant at 1%. When possible, estimates are rounded to three decimal spaces. CL is Freedom House’s Civil Liberty index, PR, Freedom House’s Political Right index, and FotP is Freedom House’s Freedom of the Press index. An increase in Freedom House’s indices corresponds to a deterioration of democracy.