the way to customer loyalty - qvartz · the psd2 way to customer loyalty 5 brief on psd21 the...

TRANSCRIPT

Kernefunktioner 1

The PSD2 way to customer loyalty 1

PSD2

The way to customer loyalty

2 The PSD2 way to customer loyalty

The PSD2 way to customer loyalty 3

Introduction

The changes facing the banking industry is an oppor-

tunity for some and a threat to many. Combined with

new technologies, the PSD2 (Revised Payment Ser-

vice Directive) directive opens doors for disrupters,

which were not open only months years ago. Mean-

while, customers are searching for a combination of

personalised services and core banking that mini-

mises their overhead costs, while fulfilling their needs

for other non-banking services. And all this is taking

place on a global scale where distance is rapidly dis-

rupted by digital solutions.

The authors of this perspective are fully aware that

most banks, particularly the major banks, have al-

ready embarked on their individual open banking

journey, so by stating the following hypothesis, we

aim to initiate a discussion on how to leverage future

retail banking differently:

Early movers will gain significant customer loyalty

advantages – if they dare to work with competitors

(banks), third-party services and tech giants in one

collaborative open banking environment.

This perspective underpins the validity of the above

hypothesis and outlines what is required to success-

fully achieve the announced first mover advantages,

while describing the future roles of each of the key

players within the retail banking ecosystem and how

they mutually benefit the most from being collabora-

tive:

The future role of the bank

The future role of the tech giant

The future role of the merchant

The future role of the fintech

4 The PSD2 way to customer loyalty

Changing dynamics

The global governing dynamics for banking are

changing due to a number of well-known factors;

globalisation, technological progress and regulatory

tightening and changes.

We claim that local knowledge in combination with

borrower liability is becoming less of a key loyalty

factor since the underlying drivers for these exact

measures are being commoditised so that outside

agents acting within financial services (or with the

will to enter financial services) can potentially access

these. And with frictionless global movability of capi-

tal (and amount of excess cash available), lending

availability is not limited by local capital scarcity.

Hence, the dynamics for retail banking are changing

from borrower liability, local knowledge and lending

availability to customer behaviour, technology and

regulation as drivers for global digital personal bank-

ing.

The consequences are that traditional customer loy-

alty factors no longer apply and customers search

for better and different services.

The change in retail banking behaviour is caused by

changes in the underlying dynamics in society, driven

by changing technology such as blockchain, IoT, big

data and AI. These technologies are all undergoing a

tremendous leap, motivated by customer behaviour.

While technology is of a more general character and

affects all of society, the regulatory changes im-

posed, specifically towards banking and with retail

supportive purposes, are conscious political choices

enforced for certain outcomes, on the back of in-

creased technology possibilities. Hence, it is a contin-

uous loop - as suggested on the right side of

EXHIBIT 1 below.

A vast number of capital and liquidity measures have

been imposed since the 2007-2008 financial crisis,

and lately, they have been followed up by a number

of transparency measures affecting both wholesale

banking and retail banking (Mifid2 and PSD2).

PSD2 is a significant game changer for retail banking,

and throughout the world, it will change the land-

scape of customer experience and loyalty com-

pletely (this point is explained in the next para-

graph). However, it is not all bad. If banks adapt and

accept the new era fast enough, it can become an

advantage to the banks and place them as global

leaders within collaborative open banking.

EXHIBIT 1:

The PSD2 way to customer loyalty 5

Brief on PSD21

The regulatory game changer for retail banking is

PSD2 ratified as of January 13, 2018. The directive

has two main purposes:

1. Enhancing competition and level the playing

field in a rapidly changing market environment

2. Ensuring consumer protection

While the latter is all about protection of payment

transactions and account access, the first has to do

with opening up for new market participants who

want to engage with banking customers.

Two types of market participants are introduced:

1. Payment initiation services providers (PISPs).

These initiate payments on behalf of customers.

They give assurance to retailers that the money

is on its way.

2. Aggregators and account information service

providers (AISPs). These give an overview of

available accounts and balances to their custom-

ers.

These (market participants) services that have his-

torically been privileged to the data-owners (which

de-facto means banks) are now open to third parties

if accepted by customers (given that the third par-

ties meet the security standards applicable). More-

over, banks have to comply with an open API mini-

mum compliance standard, securing infrastructural

conditions.

The immediate consequence is that the interface be-

tween banks and customers is disrupted. Hence, the

monopolised loyalty is gone overnight. Full stop.

The remaining part of this text will outline the future

roles within the open collaborative banking ecosys-

tem, through a zooming-in on first the Nordic bank-

ing sector, and then the Danish sector isolated. How-

ever, we do believe that the open collaborative bank-

ing philosophy can be extrapolated anywhere.

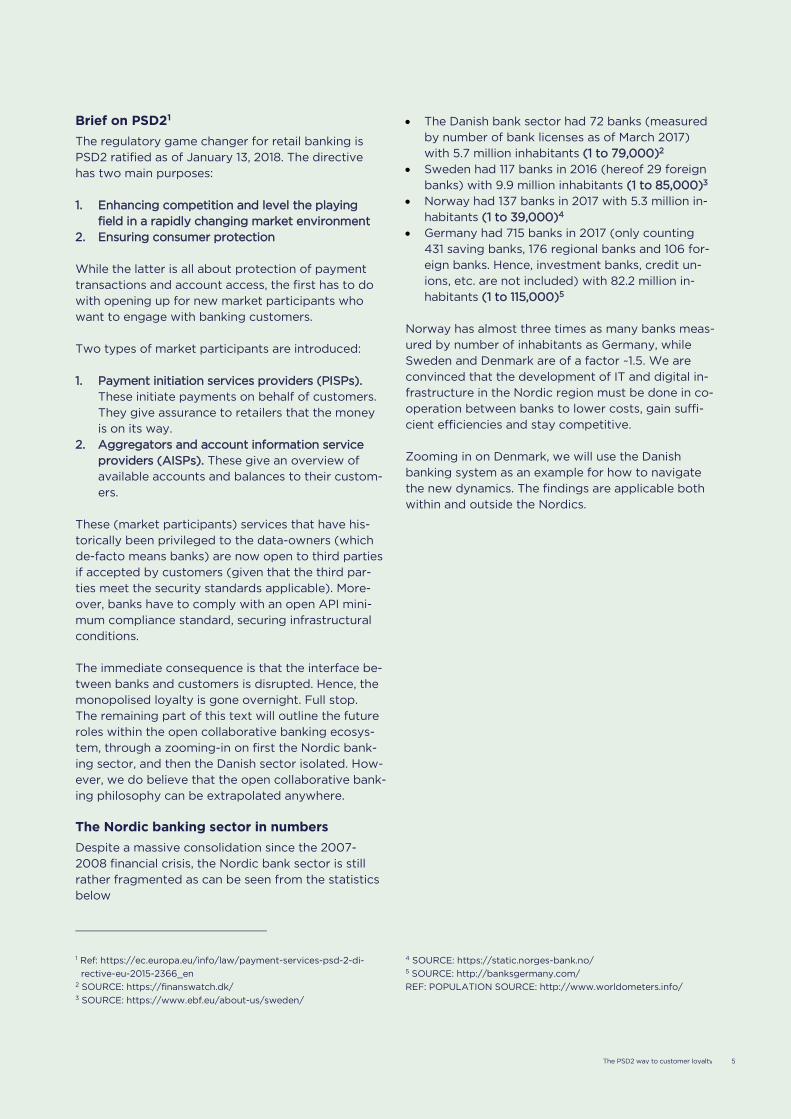

The Nordic banking sector in numbers

Despite a massive consolidation since the 2007-

2008 financial crisis, the Nordic bank sector is still

rather fragmented as can be seen from the statistics

below

1 Ref: https://ec.europa.eu/info/law/payment-services-psd-2-di-

rective-eu-2015-2366_en 2 SOURCE: https://finanswatch.dk/ 3 SOURCE: https://www.ebf.eu/about-us/sweden/

The Danish bank sector had 72 banks (measured

by number of bank licenses as of March 2017)

with 5.7 million inhabitants (1 to 79,000)2

Sweden had 117 banks in 2016 (hereof 29 foreign

banks) with 9.9 million inhabitants (1 to 85,000)3

Norway had 137 banks in 2017 with 5.3 million in-

habitants (1 to 39,000)4

Germany had 715 banks in 2017 (only counting

431 saving banks, 176 regional banks and 106 for-

eign banks. Hence, investment banks, credit un-

ions, etc. are not included) with 82.2 million in-

habitants (1 to 115,000)5

Norway has almost three times as many banks meas-

ured by number of inhabitants as Germany, while

Sweden and Denmark are of a factor ~1.5. We are

convinced that the development of IT and digital in-

frastructure in the Nordic region must be done in co-

operation between banks to lower costs, gain suffi-

cient efficiencies and stay competitive.

Zooming in on Denmark, we will use the Danish

banking system as an example for how to navigate

the new dynamics. The findings are applicable both

within and outside the Nordics.

4 SOURCE: https://static.norges-bank.no/ 5 SOURCE: http://banksgermany.com/

REF: POPULATION SOURCE: http://www.worldometers.info/

6 The PSD2 way to customer loyalty

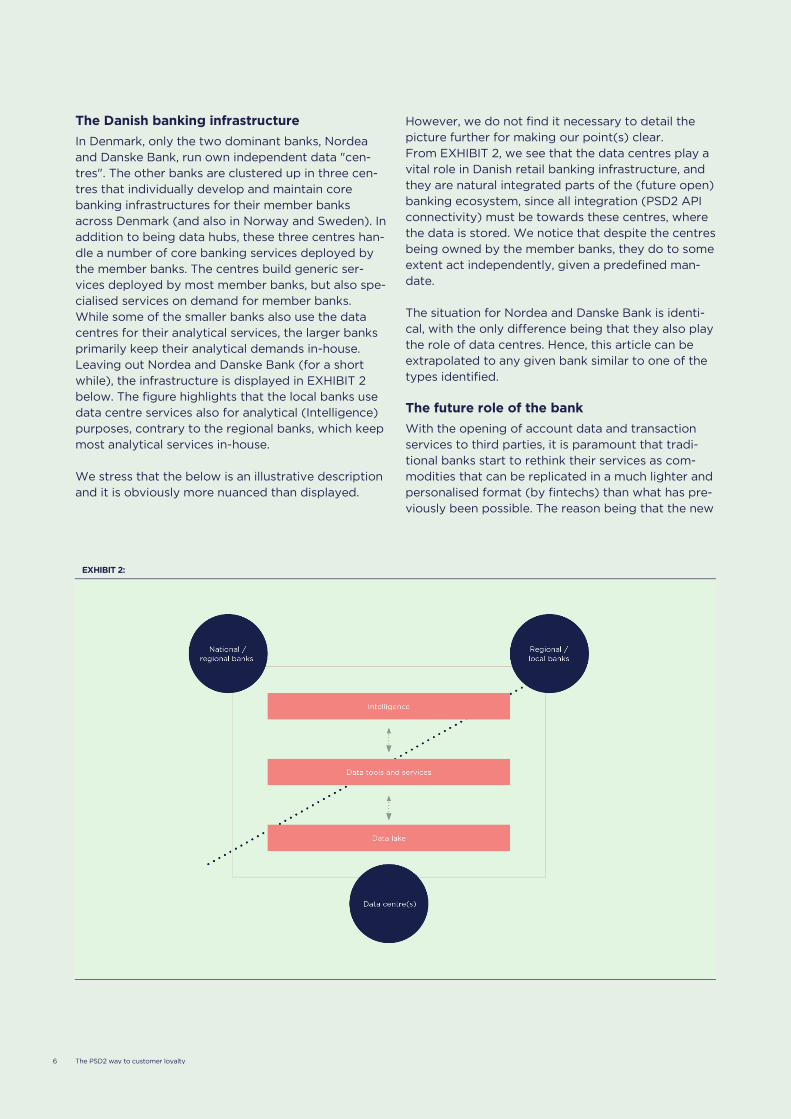

The Danish banking infrastructure

In Denmark, only the two dominant banks, Nordea

and Danske Bank, run own independent data "cen-

tres". The other banks are clustered up in three cen-

tres that individually develop and maintain core

banking infrastructures for their member banks

across Denmark (and also in Norway and Sweden). In

addition to being data hubs, these three centres han-

dle a number of core banking services deployed by

the member banks. The centres build generic ser-

vices deployed by most member banks, but also spe-

cialised services on demand for member banks.

While some of the smaller banks also use the data

centres for their analytical services, the larger banks

primarily keep their analytical demands in-house.

Leaving out Nordea and Danske Bank (for a short

while), the infrastructure is displayed in EXHIBIT 2

below. The figure highlights that the local banks use

data centre services also for analytical (Intelligence)

purposes, contrary to the regional banks, which keep

most analytical services in-house.

We stress that the below is an illustrative description

and it is obviously more nuanced than displayed.

However, we do not find it necessary to detail the

picture further for making our point(s) clear.

From EXHIBIT 2, we see that the data centres play a

vital role in Danish retail banking infrastructure, and

they are natural integrated parts of the (future open)

banking ecosystem, since all integration (PSD2 API

connectivity) must be towards these centres, where

the data is stored. We notice that despite the centres

being owned by the member banks, they do to some

extent act independently, given a predefined man-

date.

The situation for Nordea and Danske Bank is identi-

cal, with the only difference being that they also play

the role of data centres. Hence, this article can be

extrapolated to any given bank similar to one of the

types identified.

The future role of the bank

With the opening of account data and transaction

services to third parties, it is paramount that tradi-

tional banks start to rethink their services as com-

modities that can be replicated in a much lighter and

personalised format (by fintechs) than what has pre-

viously been possible. The reason being that the new

EXHIBIT 2:

The PSD2 way to customer loyalty 7

market players (fintechs and the like) do not carry

any kind of heavy technology legacy portfolio.

Hence, they can build their infrastructure much

lighter and much more agile than ever before. We

will elaborate on their role later on.

The implications are that traditional loyalty factors

are no longer unique and reserved to banks.

Fintechs, competitor banks, merchants and tech gi-

ants can (with proper cyber security in place) be

granted access to provide highly valuable services

and data as a consequence of PSD2. Banks will

simply lose the customer interface if their response

to the changing dynamics is too passive.

So instead of working against the inevitable disrup-

tion, we suggest that all the relevant stakeholders

partner up in one open collaborative digital banking

ecosystem.

Hence, banks have to open up their infrastructure to

fintechs and collaborate on multiple financial ser-

vices and not only be PSD2 minimal compliant. Also,

banks have to aggregate core banking services with

merchant services such as online streaming services,

grocery shopping, magazines, fitness memberships,

newspaper subscriptions, airline loyalty programmes

(and many others) to create customer value through

new services that are both convenient and financially

viable for their customers.

In addition, banks have to accept that they should

not individually build their own API infrastructure.

This will simply just create a new heavy "spaghetti"

legacy that will eventually be replaced by something

lighter and more agile on a Nordic scale.

To secure a true Nordic ecosystem, banks must sup-

port a joint infrastructural base across the entire Nor-

dic banking community.

The future role of the tech giant

The strengths of tech giants are superior hardware

and software, big data handling and digital architec-

tural design. No one, not even the largest Nordic

banks, can compete with the tech giants on these

measures. The reason for this is obvious: tech giants

are born digital and think digital first in all they do.

Tech giants will play an extremely important role in

the future landscape/ecosystem of Nordic banking.

They will play the role of data hub for all banks on

the one side, and all third party agents on the other

side. Hence, they are both linked to individual banks'

data centres (BEC, BD, SDC, Nordea and Danske

Bank) through individual APIs, and they also transfer

data to all third parties (PISPs and AISPs) that have

been granted access to customer accounts or to ac-

count transactions, through one standardised API.

Building the Data/API Hub requires technology and

data experience to such a level that it does not exist

within any of the Nordic banks – and neither should it

be their focus.

Playing this role of technology provider is crucial for

the digital open collaborative ecosystem to be com-

plete and optimised.

The future role of the merchant

Using already stored bank data in the bundling of

services and products across different business areas

is a potential driver for future customer loyalty.

Banks holds enormous amounts of data supporting

analytical joint ventures with merchants. Hence, by

proper analysis of bank data combined with dis-

counts and offers from merchants, is it possible to

improve the financial situation of retail customers,

while bank loyalty is preserved.

In this win-win-win situation, merchants get access

to banks customer portfolio, customers obtain hard

economic value and ease of access to a wide range

of services, while banks retain customer loyalty.

There is an endless number of possible combinations

and both local and international partners can be

brought into play.

Two alternative routes are

1. Exclusive merchant discounts

2. Financial improvements through analytics

We provide examples of both below.

8 The PSD2 way to customer loyalty

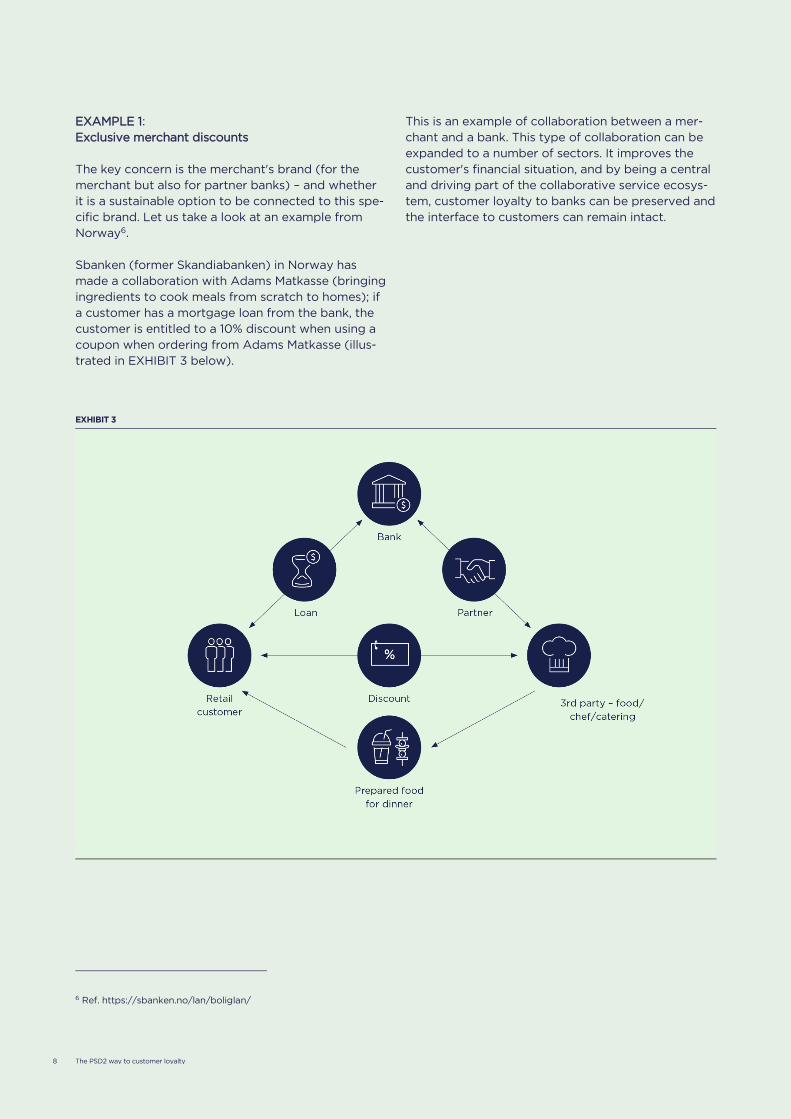

EXAMPLE 1:

Exclusive merchant discounts

The key concern is the merchant's brand (for the

merchant but also for partner banks) – and whether

it is a sustainable option to be connected to this spe-

cific brand. Let us take a look at an example from

Norway6.

Sbanken (former Skandiabanken) in Norway has

made a collaboration with Adams Matkasse (bringing

ingredients to cook meals from scratch to homes); if

a customer has a mortgage loan from the bank, the

customer is entitled to a 10% discount when using a

coupon when ordering from Adams Matkasse (illus-

trated in EXHIBIT 3 below).

6 Ref. https://sbanken.no/lan/boliglan/

This is an example of collaboration between a mer-

chant and a bank. This type of collaboration can be

expanded to a number of sectors. It improves the

customer's financial situation, and by being a central

and driving part of the collaborative service ecosys-

tem, customer loyalty to banks can be preserved and

the interface to customers can remain intact.

EXHIBIT 3

The PSD2 way to customer loyalty 9

EXAMPLE 2:

Financial improvement through analytics

Below, we look at examples of individualised mer-

chant offers linked to purchase patterns and financial

options:

Everyday digital financial advisor

Everyday need prediction and personalised

recommendations

Everyday help to fulfil goals and wishes

Everyday investment advice

Illustrated in EXHIBIT 4 below.

This is now possible through easy and sufficient ac-

cess to customer data, combined with a complete

overview of current offers from collaborating mer-

chants.

Hence, by pattern recognition and general behaviour

of similar segments, is it possible to create a very

comprehensive and personal customer experience,

based on data analytics.

EXHIBIT 4:

10 The PSD2 way to customer loyalty

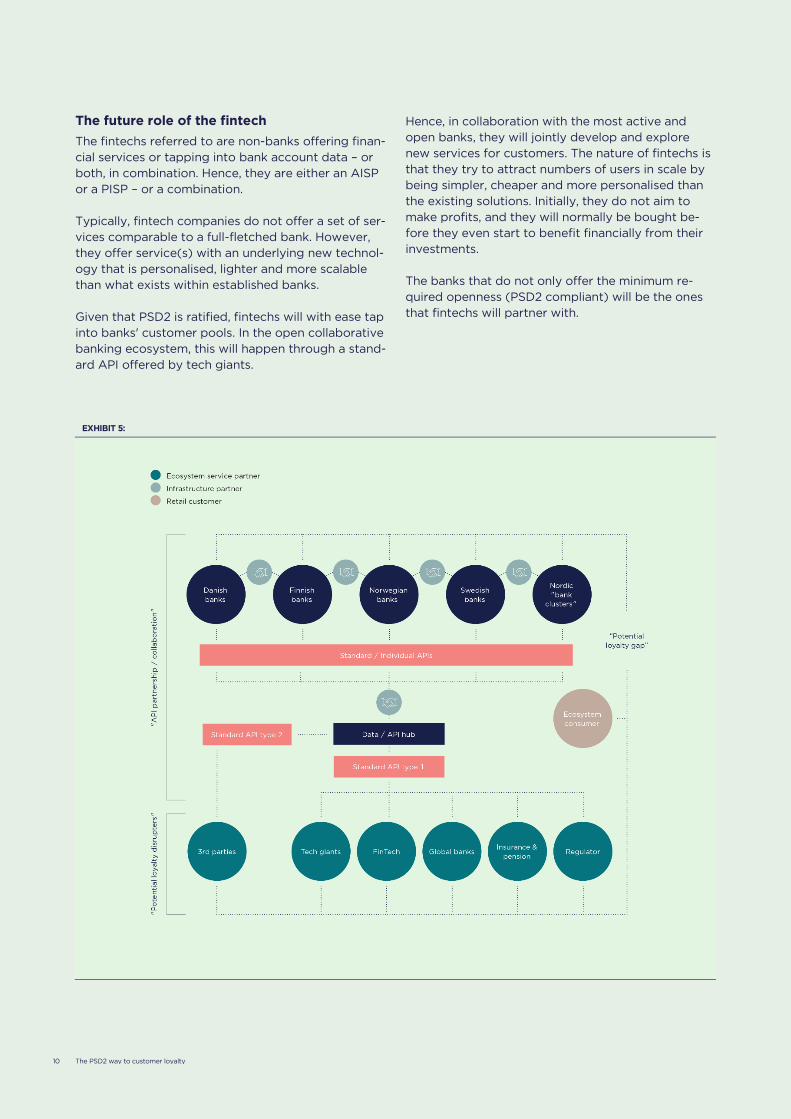

The future role of the fintech

The fintechs referred to are non-banks offering finan-

cial services or tapping into bank account data – or

both, in combination. Hence, they are either an AISP

or a PISP – or a combination.

Typically, fintech companies do not offer a set of ser-

vices comparable to a full-fletched bank. However,

they offer service(s) with an underlying new technol-

ogy that is personalised, lighter and more scalable

than what exists within established banks.

Given that PSD2 is ratified, fintechs will with ease tap

into banks' customer pools. In the open collaborative

banking ecosystem, this will happen through a stand-

ard API offered by tech giants.

Hence, in collaboration with the most active and

open banks, they will jointly develop and explore

new services for customers. The nature of fintechs is

that they try to attract numbers of users in scale by

being simpler, cheaper and more personalised than

the existing solutions. Initially, they do not aim to

make profits, and they will normally be bought be-

fore they even start to benefit financially from their

investments.

The banks that do not only offer the minimum re-

quired openness (PSD2 compliant) will be the ones

that fintechs will partner with.

EXHIBIT 5:

The PSD2 way to customer loyalty 11

The digital banking ecosystem

In regards to open collaborative banking, we belive

that the Nordic region is in a sweet spot when it

comes to digital banking. The Nordic countries are

small and well-organised, and the existing digital in-

frastructure is at an overall high level. In addition, we

find the populations to be sufficiently digitally ma-

ture to participate in a collaborative open banking

ecosystem.

We believe that by creating the ecosystem (see

EXHIBIT 5 above) is key to sustainable banking cus-

tomer loyalty. Also; merchants will leverage on

broader customer access while tech giants will con-

trol the infrastructure and data centres, banks and

customers will benefit financially from this

collaboration.

Conclusion

Through the initiatives described above, is it possible

for banks to lead the collaborative open banking

ecosystem. The most crucial part is collaboration be-

tween the banks. Hence, Nordic banks should refrain

from inventing their own individual standards as this

simply does not make sense for the region. Instead,

this standard should be developed jointly, but with a

tech giant driving it.

By creating this Nordic ecosystem, the region will

become attractive for fintechs, financial service pro-

viders and other collaborators – and jointly, these will

add to the most collaborative retail banking environ-

ment yet to be found.

Finally, the banks that supply these opportunities to

customers and proactively support an open banking

environment will stand out in comparison to the rest.

Hence, customer proximity will be superior and this

will be key to enhanced loyalty.

12 The PSD2 way to customer loyalty

Tim Bruun Madsen

+45 61 22 42 69

Jesper Adeltoft

+45 29 69 69 36

The PSD2 way to customer loyalty 13

www.qvartz.com