the wharf (holdings) limited 2015 final results 9 march 2016 2015 final results... · the wharf...

TRANSCRIPT

The Wharf (Holdings) Limited

2015 Final Results

9 March 2016

2015

1

Resilient IP Core

The Wharf (Holdings) Limited

2015 Final Results

9 March 2016

2015

2

Backdrop

• Core Profit Steady Growth was Sustained in 2015

• IP Resilience Continued and is Expected to Spill Over into 2016

• Headwinds – Global Economic Slowdown, Currency Instability & Uncertainty, HK Retail, China Office

2015

3

Resilient Foundation to Move Ahead

• Navigating Through Tough Times; Stability in Challenging Times

• Resilient Core Operations

• China IP Starting to Bear Fruit; New Malls Outperform

2015

4

Steady Growth in IP Assets

• Total Assets were Stable at $444B

• IP Portfolio Increased by 3% to $310B

• DP Decreased to $38B (excl. JVs & Associates)

2015

70%

15%

15%

Total Assets

$444 billion Others

IP

DP (Incl. JVs & Associates)

5

IP – Strong Execution Amid Tough Market

2.3 2.9 3.7 4.6 4.9 5.7 5.9 6.5 7.6 8.3

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

IP Core Profit (HKD Billion) $8.3B (+9%)

• IP / Core Profit: 76% (2014: 73%)

• Core Expertise of a Unique Portfolio

• Proven Retail Management Drove Rental Growth

• Office Added Impetus

2015

69%

7% 11%

13%

Core Profit

$11 billion Others

HKIP

China IP DP

6

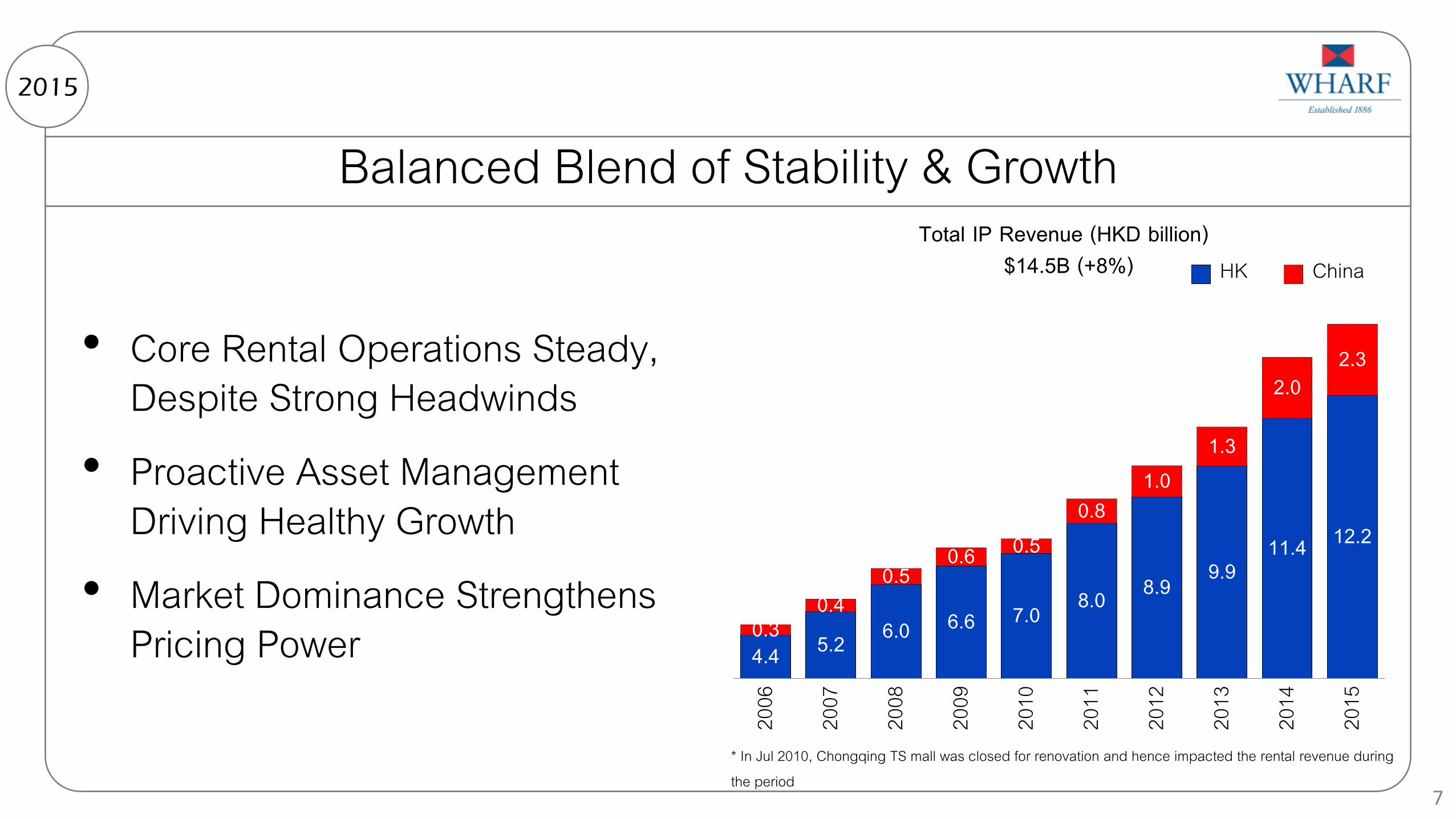

Balanced Blend of Stability & Growth

• Core Rental Operations Steady, Despite Strong Headwinds

• Proactive Asset Management Driving Healthy Growth

• Market Dominance Strengthens Pricing Power

2015

* In Jul 2010, Chongqing TS mall was closed for renovation and hence impacted the rental revenue during the period

4.4 5.2 6.0 6.6 7.0 8.0 8.9 9.9 11.4 12.2

0.3 0.4

0.5 0.6 0.5

0.8 1.0

1.3

2.0 2.3

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Total IP Revenue (HKD billion) HK China$14.5B (+8%)

7

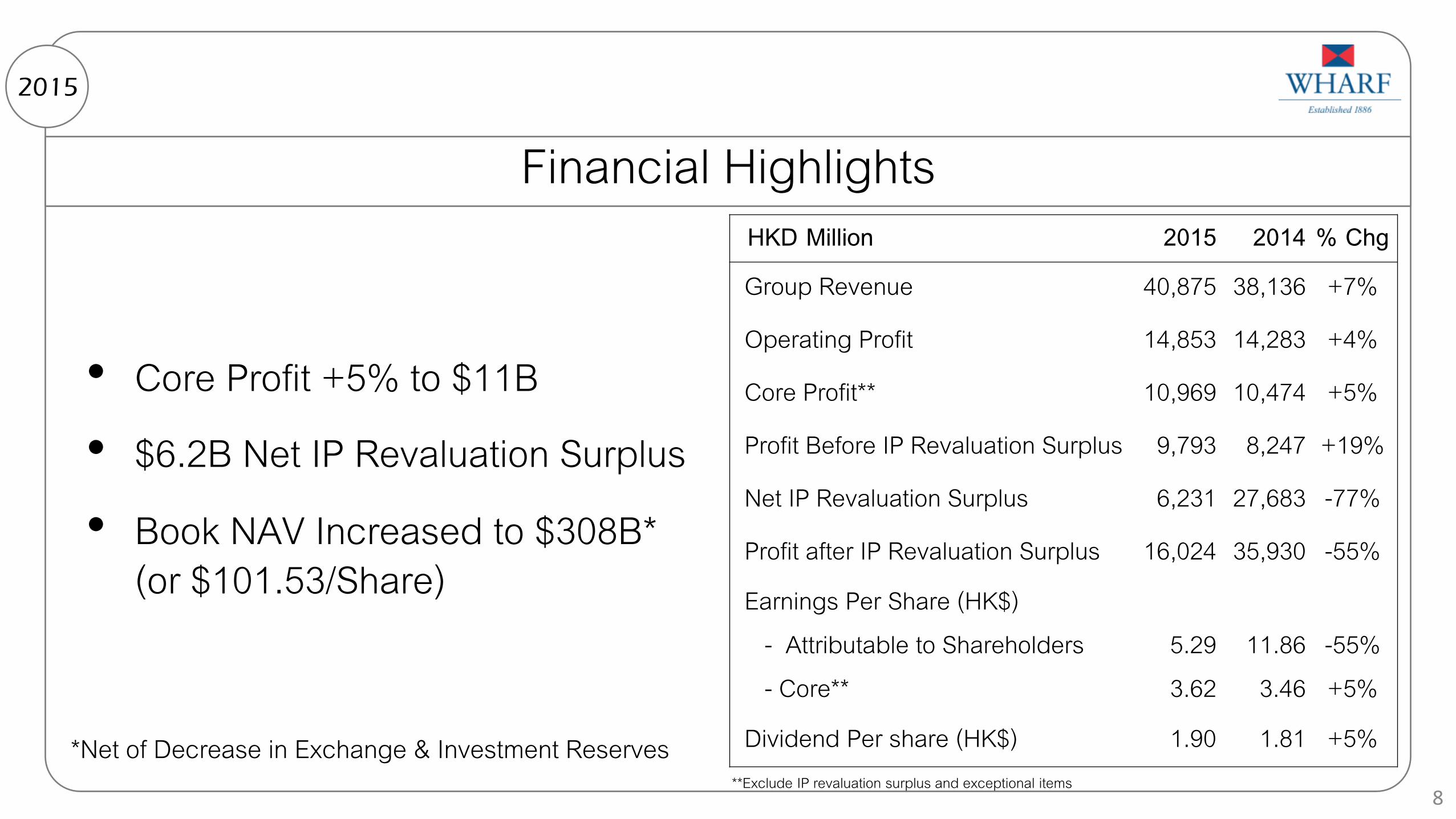

Financial Highlights 2015

**Exclude IP revaluation surplus and exceptional items

• Core Profit +5% to $11B

• $6.2B Net IP Revaluation Surplus

• Book NAV Increased to $308B* (or $101.53/Share)

HKD Million 2015 2014 % Chg Group Revenue 40,875 38,136 +7%

Operating Profit 14,853 14,283 +4%

Core Profit** 10,969 10,474 +5%

Profit Before IP Revaluation Surplus 9,793 8,247 +19%

Net IP Revaluation Surplus 6,231 27,683 -77%

Profit after IP Revaluation Surplus 16,024 35,930 -55% Earnings Per Share (HK$) - Attributable to Shareholders - Core**

5.29 3.62

11.86

3.46

-55% +5%

Dividend Per share (HK$) 1.90 1.81 +5%

8

*Net of Decrease in Exchange & Investment Reserves

Agenda

Hong Kong IP A

China IP & DP B

Others C

Next D

9

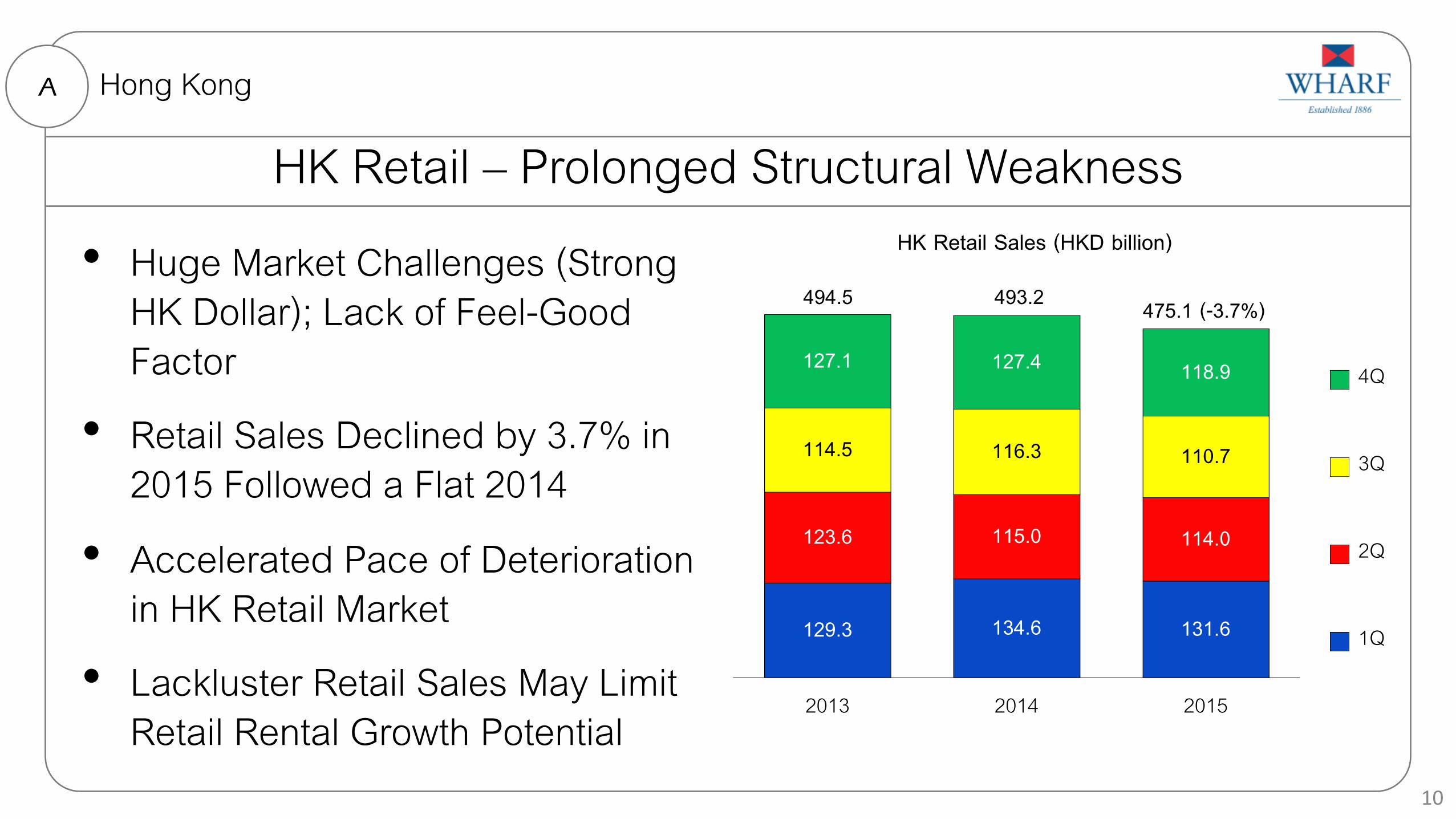

HK Retail – Prolonged Structural Weakness • Huge Market Challenges (Strong

HK Dollar); Lack of Feel-Good Factor

• Retail Sales Declined by 3.7% in 2015 Followed a Flat 2014

• Accelerated Pace of Deterioration in HK Retail Market

• Lackluster Retail Sales May Limit Retail Rental Growth Potential

A Hong Kong

10

129.3 134.6 131.6

123.6 115.0 114.0

114.5 116.3 110.7

127.1 127.4 118.9

2013 2014 2015

HK Retail Sales (HKD billion) Title

4Q

3Q

2Q

1Q

494.5 493.2 475.1 (-3.7%)

Retail Sales in a Tough Market A Hong Kong

11

33.8 35.0 30.7

2013 2014 2015

HC Retail Sales (HKD billion) Title

-12.1%

9.4 10.5

9.1

2013 2014 2015

TS Retail Sales (HKD billion) Title

-12.8%

Proactive Initiatives to Weather Downturn

• Ongoing AEIs & Tenant Mix Refinement Underway to Provide Upside

• Improving Retail Offer with the Most Differentiating & Aspirational Brands to Enhance One-Stop Lifestyle Experience

• Powerful Promotions Underway; Proactively Expanding Customers Base from SE Asia

A Hong Kong

12

2016 Retail Outlook

• Retail Weakness Likely a Multi-Year Story; Heading to a Tough 2016

• HK is a Dynamic Place for International Young Brands & Start-Ups

• Continue to Provide Productive Environment for Our Tenants to Trade, to Have Effective Market Presence & to Meet Shoppers

A Hong Kong

13

Proven Retail Management Driving Performance

• Stable Performance in a Tough Market

• Prime & Quality Malls Driving Strong Retailers’ Demand

• Best-Positioned Destination Retail; Steady Occupancy Cost

• Outstanding Tenant Mix; Creation of New Dining Experiences

A

6%

23%

69%

2%

Retail Revenue By Segment $8.7B (+6%)

PH

Others

TS

HC

Hong Kong

Retail Revenue Growth HC $5,949M +5% TS $2,017M +7% PH $529M +3%

14

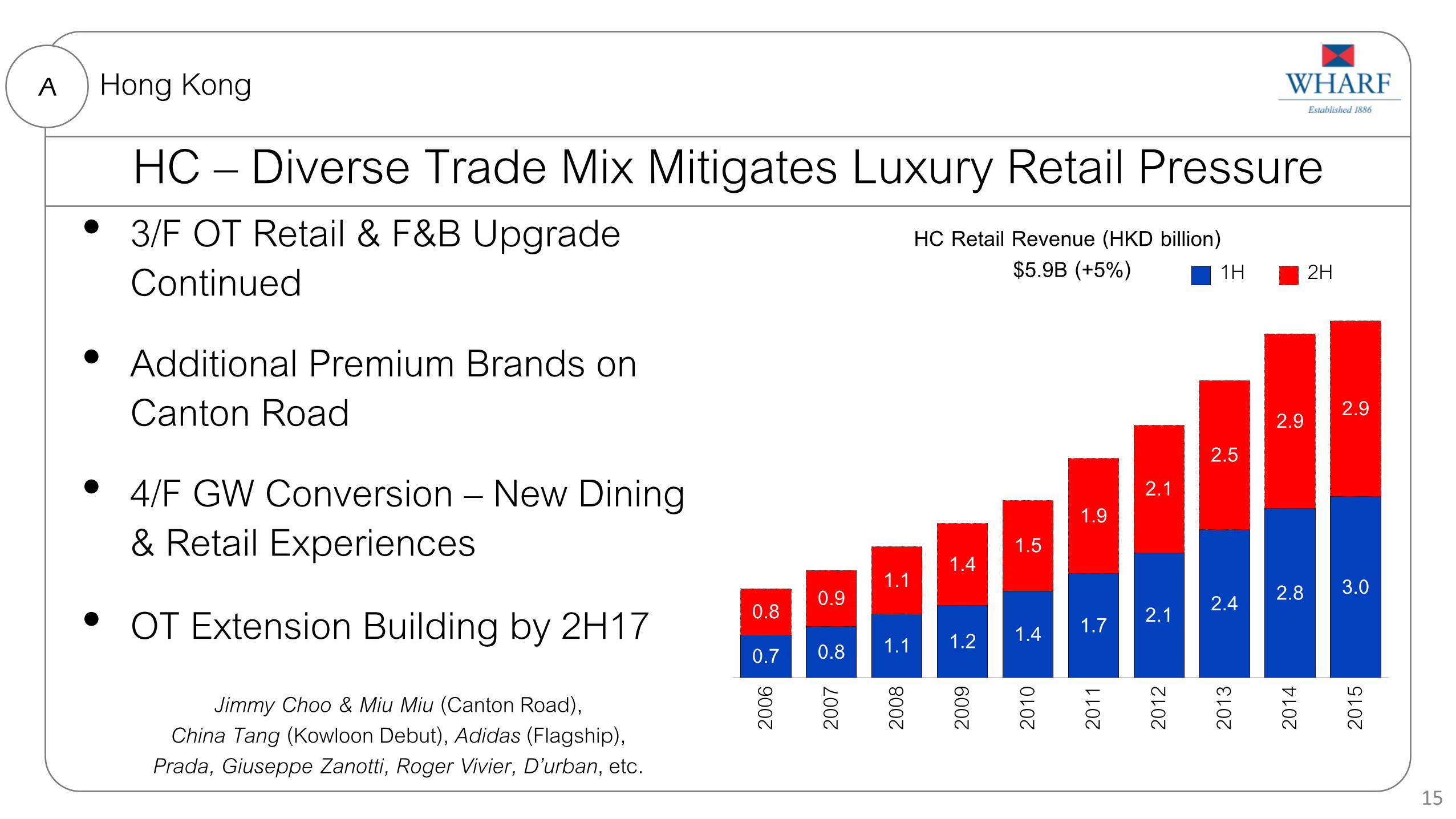

HC – Diverse Trade Mix Mitigates Luxury Retail Pressure • 3/F OT Retail & F&B Upgrade

Continued

• Additional Premium Brands on Canton Road

• 4/F GW Conversion – New Dining & Retail Experiences

• OT Extension Building by 2H17

Jimmy Choo & Miu Miu (Canton Road), China Tang (Kowloon Debut), Adidas (Flagship),

Prada, Giuseppe Zanotti, Roger Vivier, D’urban, etc.

A

0.7 0.8 1.1 1.2 1.4 1.7 2.1 2.4 2.8 3.0 0.8 0.9

1.1 1.4 1.5

1.9 2.1

2.5 2.9 2.9

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

HC Retail Revenue (HKD billion) 1H 2H$5.9B (+5%)

Hong Kong

15

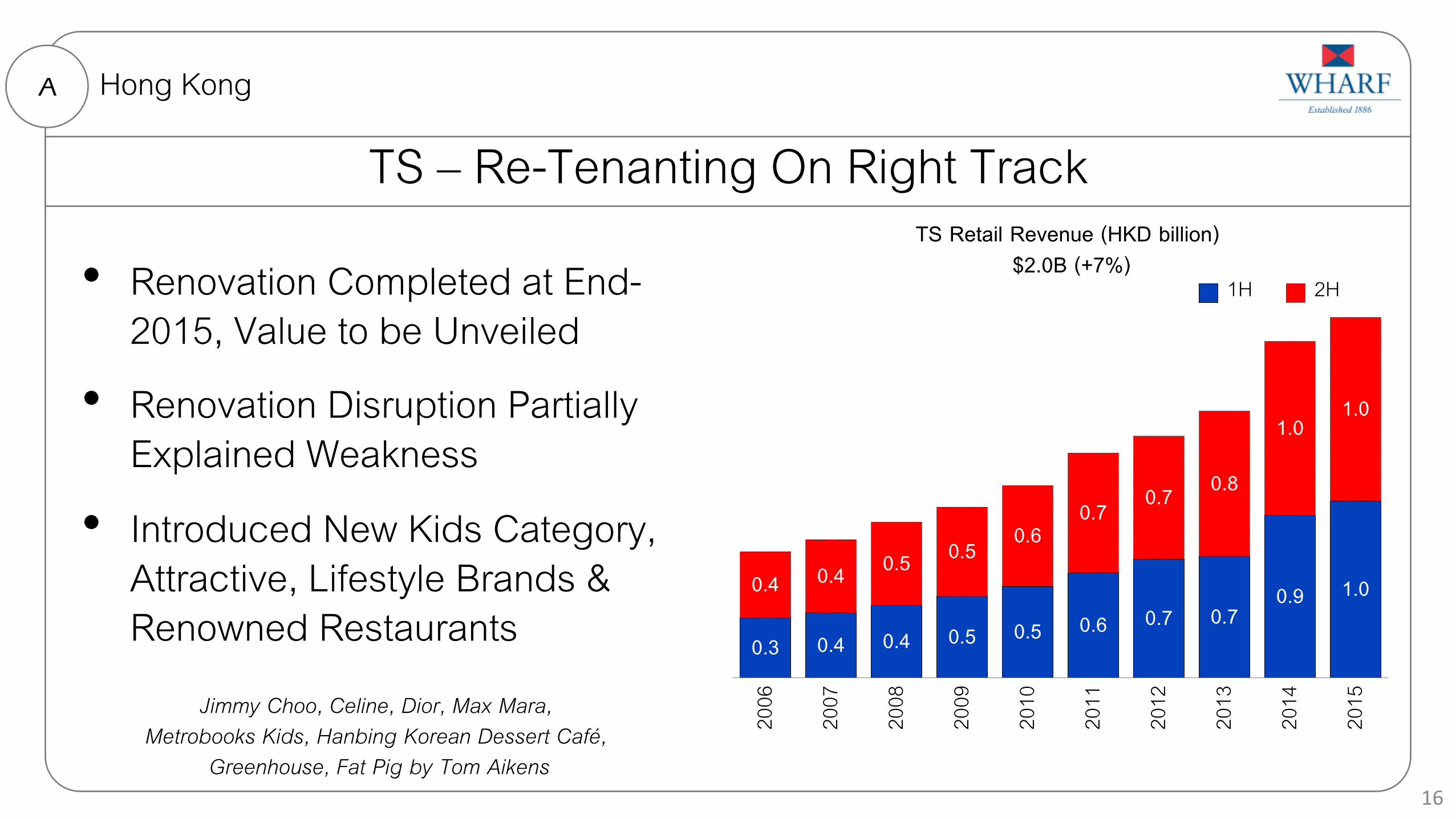

TS – Re-Tenanting On Right Track

• Renovation Completed at End-2015, Value to be Unveiled

• Renovation Disruption Partially Explained Weakness

• Introduced New Kids Category, Attractive, Lifestyle Brands & Renowned Restaurants

A

0.3 0.4 0.4 0.5 0.5 0.6 0.7 0.7 0.9 1.0 0.4 0.4 0.5 0.5 0.6

0.7 0.7 0.8

1.0 1.0

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

TS Retail Revenue (HKD billion)

1H 2H$2.0B (+7%)

Hong Kong

16

Jimmy Choo, Celine, Dior, Max Mara, Metrobooks Kids, Hanbing Korean Dessert Café,

Greenhouse, Fat Pig by Tom Aikens

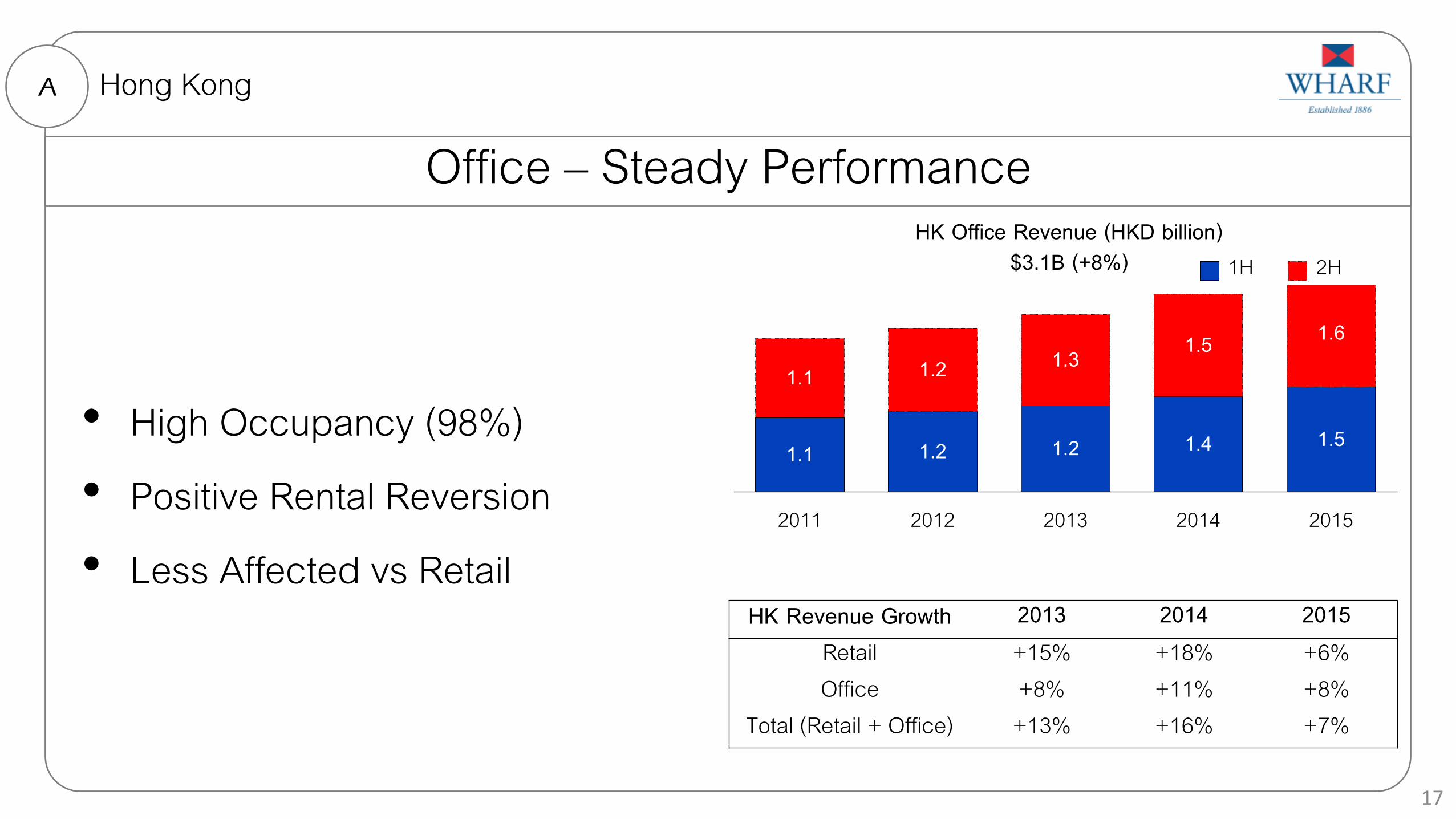

Office – Steady Performance

• High Occupancy (98%)

• Positive Rental Reversion

• Less Affected vs Retail

A

1.1 1.2 1.2 1.4 1.5

1.1 1.2 1.3 1.5 1.6

2011 2012 2013 2014 2015

HK Office Revenue (HKD billion) 1H 2H$3.1B (+8%)

Hong Kong

17

HK Revenue Growth 2013 2014 2015 Retail +15% +18% +6% Office +8% +11% +8%

Total (Retail + Office) +13% +16% +7%

Agenda

Hong Kong IP A

China IP & DP B

Others C

Next D

18

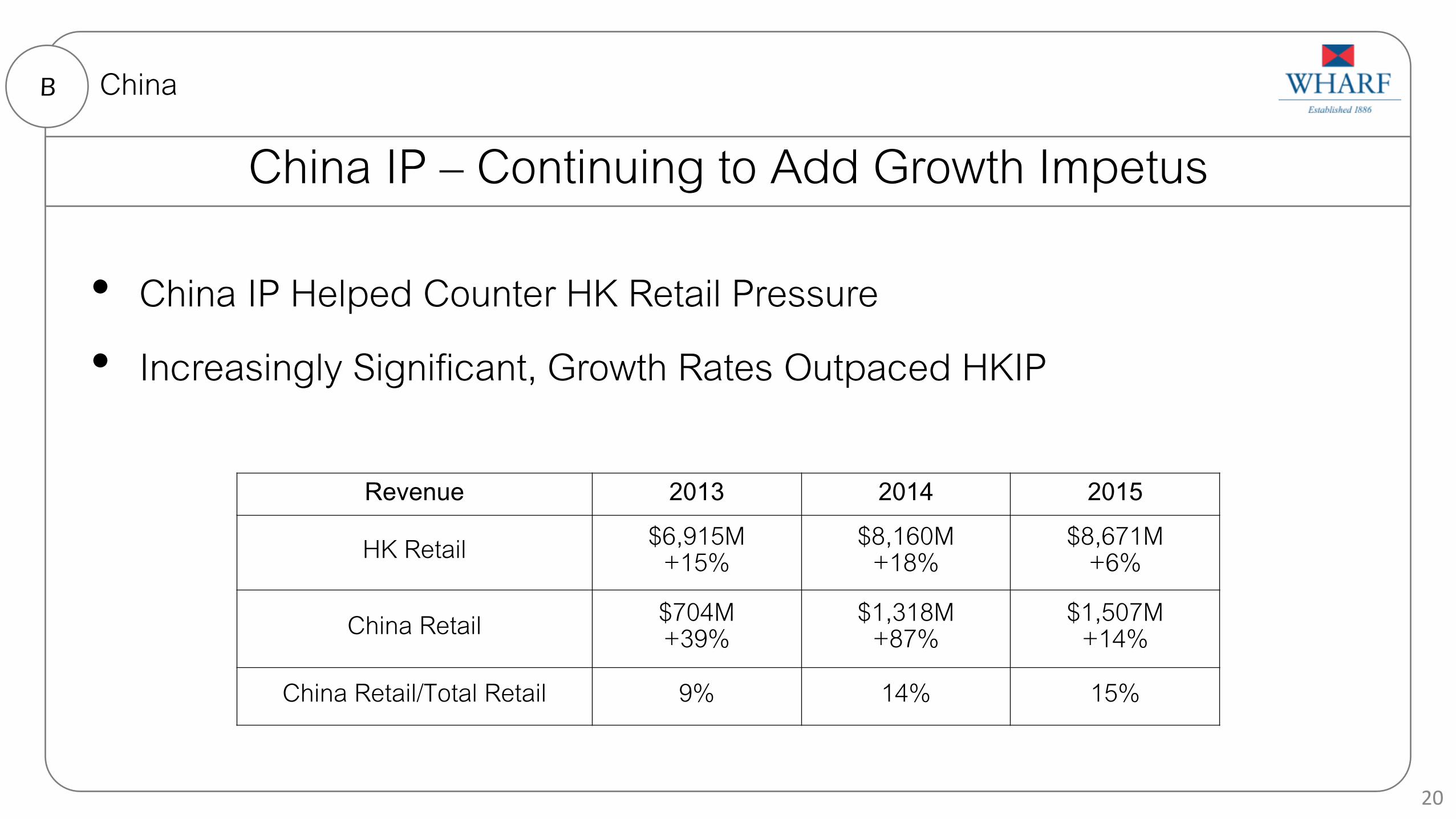

China IP – Continuing to Add Growth Impetus

• Starting to Bear Fruit

• China Retail – Another Pillar and a New Growth Engine

• China Retail Performance Offsets Sector Headwinds in HK

B China

0.2 0.2 0.3 0.3 0.2 0.3 0.5 0.5 0.8

1.1

0.1 0.2 0.2 0.3 0.3

0.5 0.5

0.8

1.2

1.2

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

China IP Revenue (HKD billion) 1H 2H$2.3B (+16%)

19

* In Jul 2010, Chongqing TS mall was closed for renovation and hence impacted the rental revenue during the period

China IP – Continuing to Add Growth Impetus

B China

20

Revenue 2013 2014 2015

HK Retail $6,915M +15%

$8,160M +18%

$8,671M +6%

China Retail $704M +39%

$1,318M +87%

$1,507M +14%

China Retail/Total Retail 9% 14% 15%

• China IP Helped Counter HK Retail Pressure

• Increasingly Significant, Growth Rates Outpaced HKIP

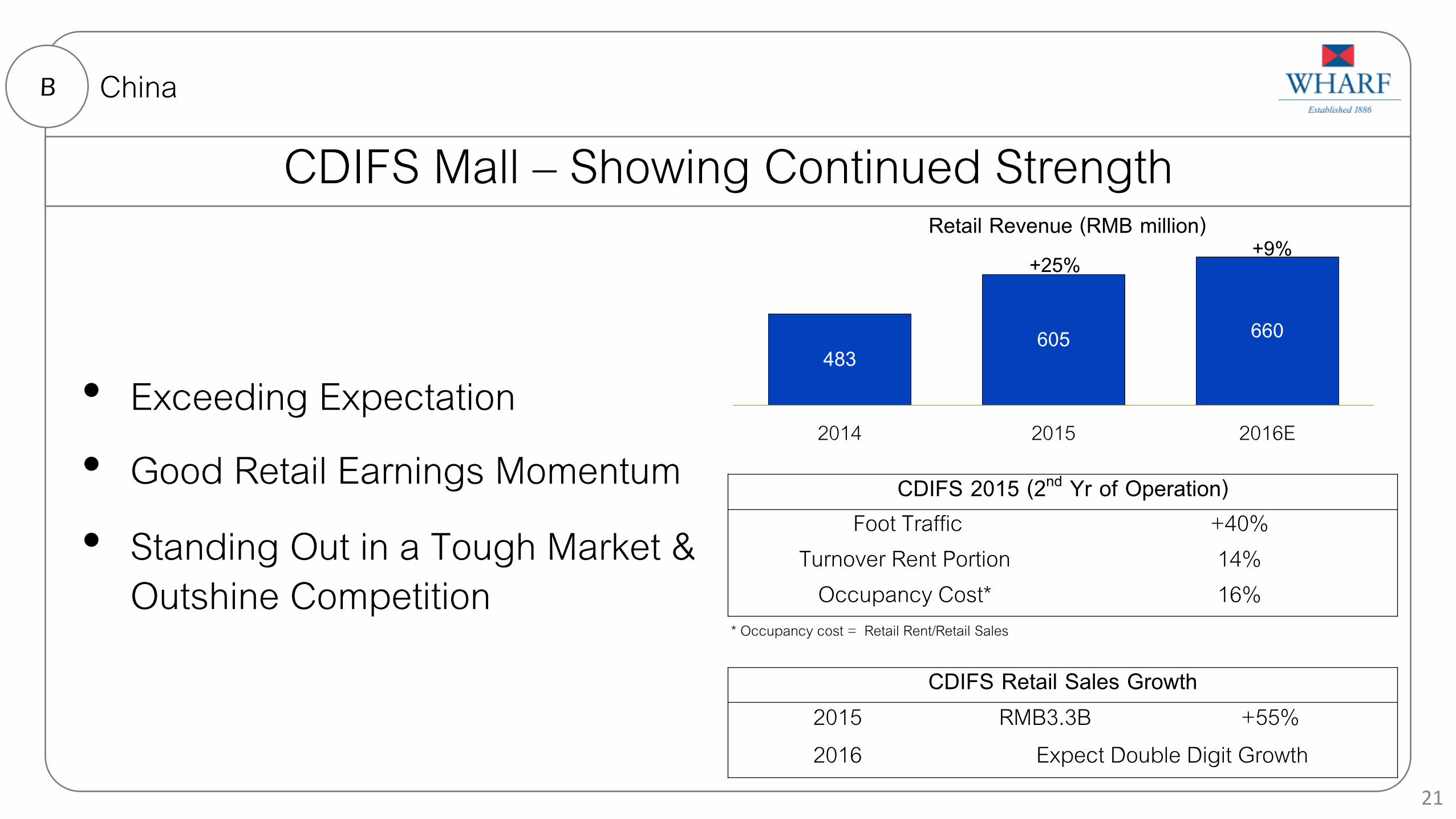

CDIFS Mall – Showing Continued Strength

• Exceeding Expectation

• Good Retail Earnings Momentum

• Standing Out in a Tough Market & Outshine Competition

B China

483 605 660

2014 2015 2016E

Retail Revenue (RMB million)

21

CDIFS 2015 (2nd Yr of Operation) Foot Traffic +40%

Turnover Rent Portion 14% Occupancy Cost* 16%

CDIFS Retail Sales Growth 2015 RMB3.3B +55% 2016 Expect Double Digit Growth

* Occupancy cost = Retail Rent/Retail Sales

+25% +9%

CDIFS Office – Leasing On Track

• Leasing Status In Line with Expectation

• Over 90,000 s.m Leased, Including ~50,000 s.m in 2015

• Rental Rates Achieved among the Highest in the City

• Expected Commitment to Reach Over 50% by End-2016

B China

22

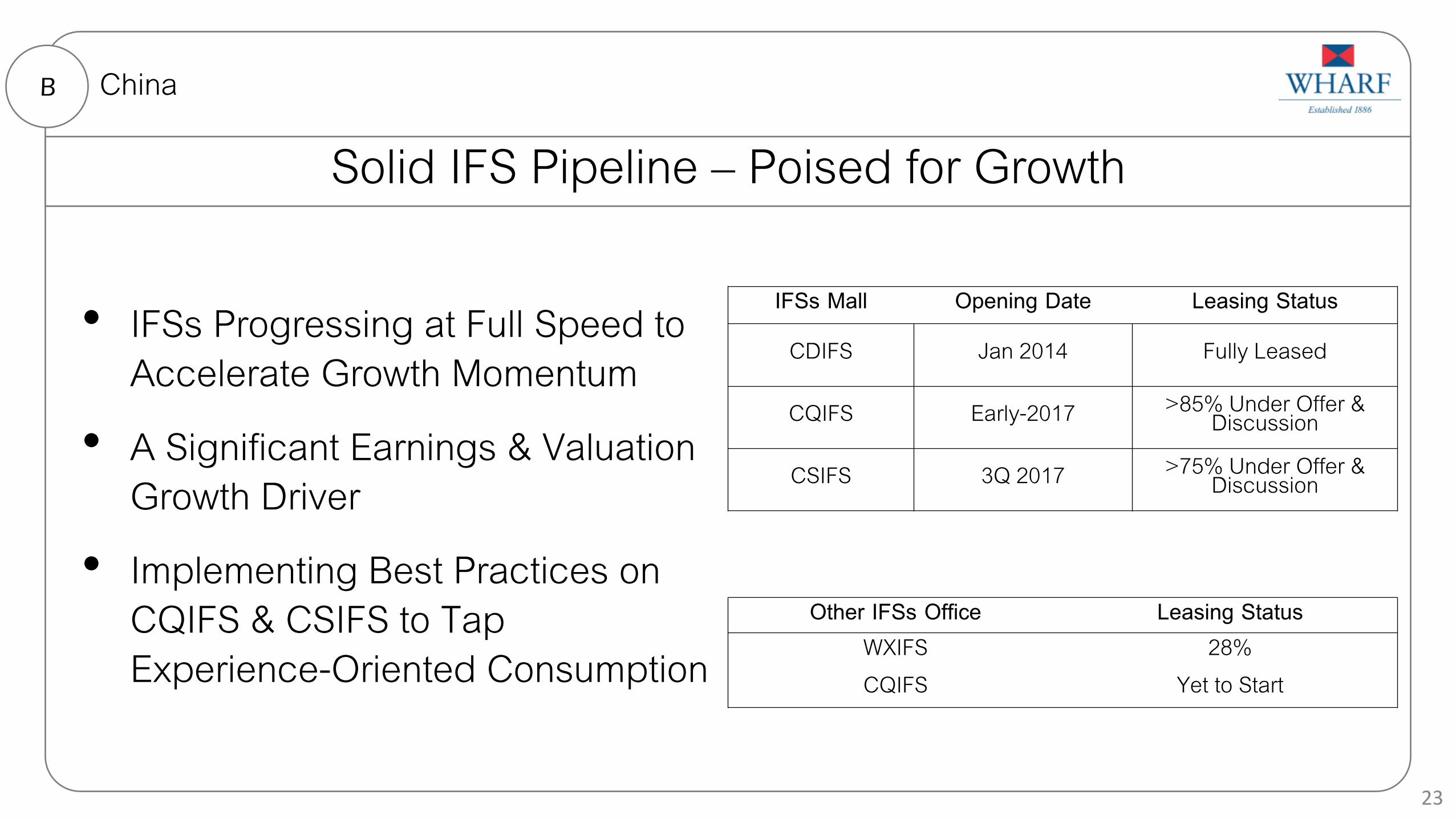

Solid IFS Pipeline – Poised for Growth

• IFSs Progressing at Full Speed to Accelerate Growth Momentum

• A Significant Earnings & Valuation Growth Driver

• Implementing Best Practices on CQIFS & CSIFS to Tap Experience-Oriented Consumption

B China

Other IFSs Office Leasing Status WXIFS 28% CQIFS Yet to Start

23

IFSs Mall Opening Date Leasing Status

CDIFS Jan 2014 Fully Leased

CQIFS Early-2017 >85% Under Offer & Discussion

CSIFS 3Q 2017 >75% Under Offer & Discussion

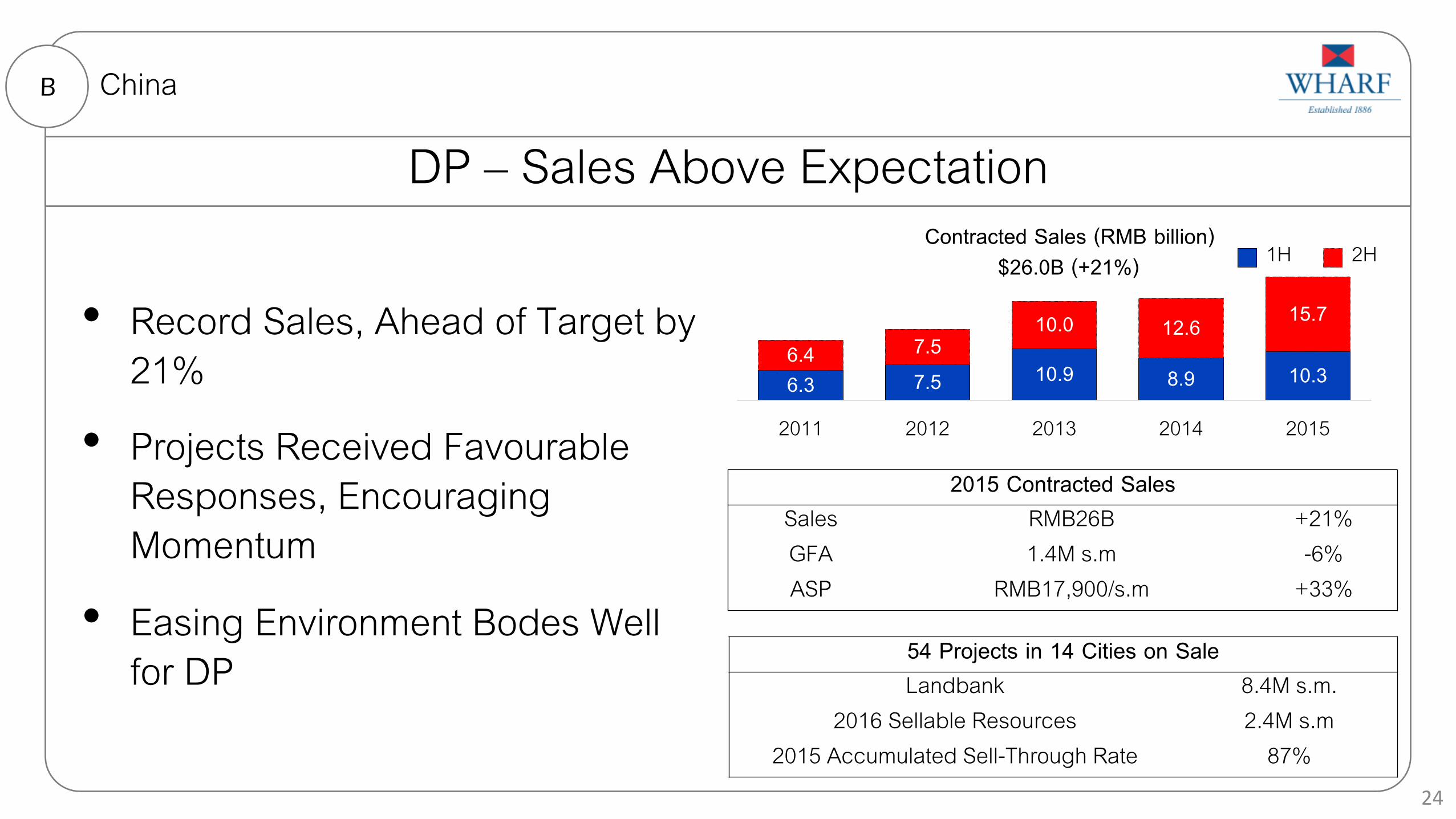

DP – Sales Above Expectation

• Record Sales, Ahead of Target by 21%

• Projects Received Favourable Responses, Encouraging Momentum

• Easing Environment Bodes Well for DP

B China

6.3 7.5 10.9 8.9 10.3 6.4 7.5

10.0 12.6 15.7

2011 2012 2013 2014 2015

Contracted Sales (RMB billion) 1H 2H

2015 Contracted Sales Sales RMB26B +21% GFA 1.4M s.m -6% ASP RMB17,900/s.m +33%

$26.0B (+21%)

24

54 Projects in 14 Cities on Sale Landbank 8.4M s.m.

2016 Sellable Resources 2.4M s.m 2015 Accumulated Sell-Through Rate 87%

DP – Improving Revenue Booking

• Contribution to Core Profit Increased to 11%^, excl. Greentown China

• Solid Execution

• Development Margins Remain Steady

B China

2015 Operating Matrix* Revenue $27,404M +18%

Operating Profit $4,200M +51% Operating Margin 15.3% +3.4ppts Completed GFA 1.7M s.m -8% Recognized GFA 1.6M s.m -5%

* Incl. JVs & Associates

25

2016 Target Completion 2.0M s.m 2016 Sales Target RMB24B

Net Order Book at End-2015 RMB25B GFA 1.4M s.m

^2014: 8%

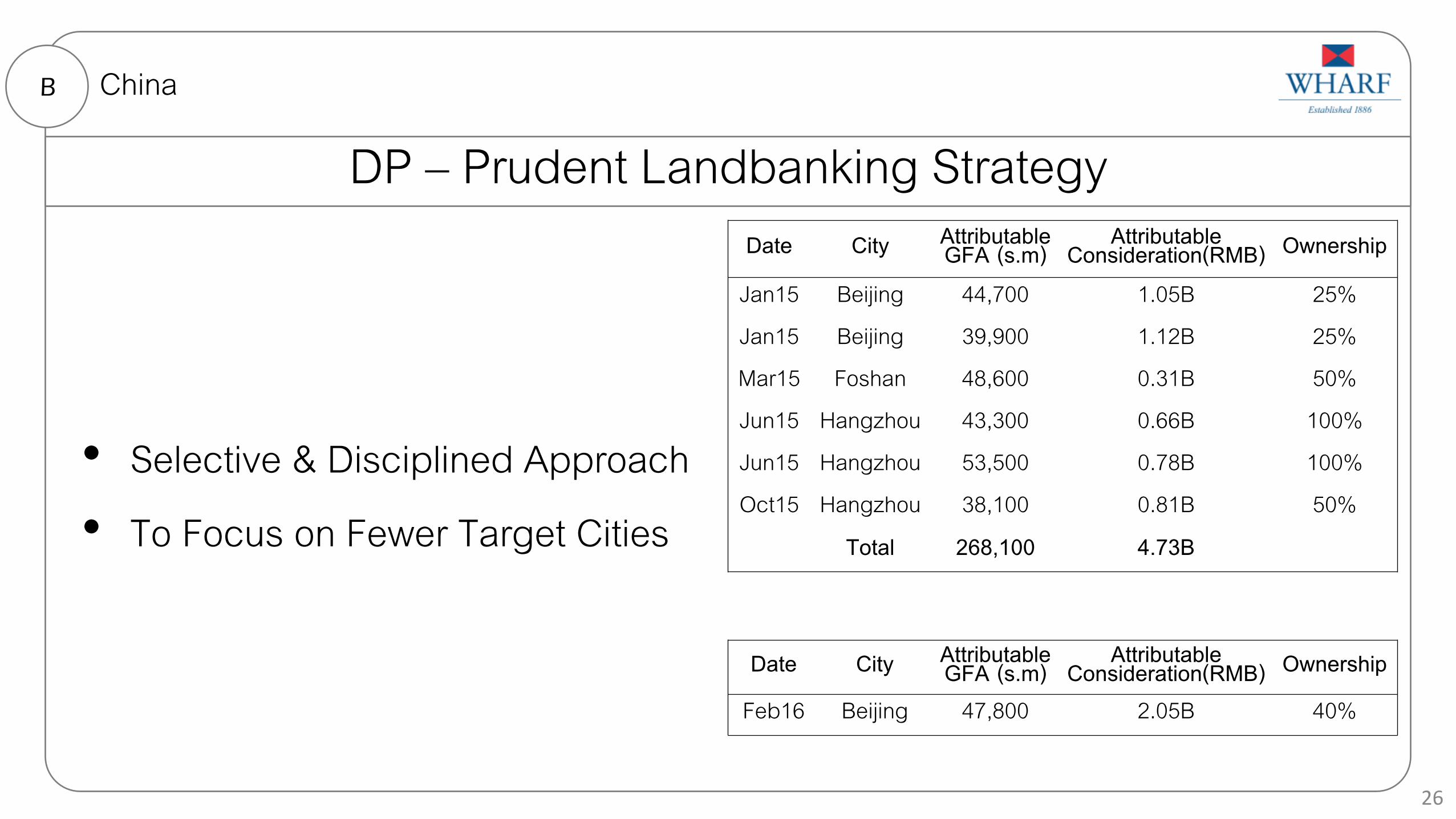

DP – Prudent Landbanking Strategy

• Selective & Disciplined Approach

• To Focus on Fewer Target Cities

B China

Date City Attributable GFA (s.m)

Attributable Consideration(RMB) Ownership

Jan15 Beijing 44,700 1.05B 25% Jan15 Beijing 39,900 1.12B 25% Mar15 Foshan 48,600 0.31B 50% Jun15 Hangzhou 43,300 0.66B 100% Jun15 Hangzhou 53,500 0.78B 100% Oct15 Hangzhou 38,100 0.81B 50%

Total 268,100 4.73B

Date City Attributable GFA (s.m)

Attributable Consideration(RMB) Ownership

Feb16 Beijing 47,800 2.05B 40%

26

Agenda

Hong Kong IP A

China IP & DP B

Others C

Next D

27

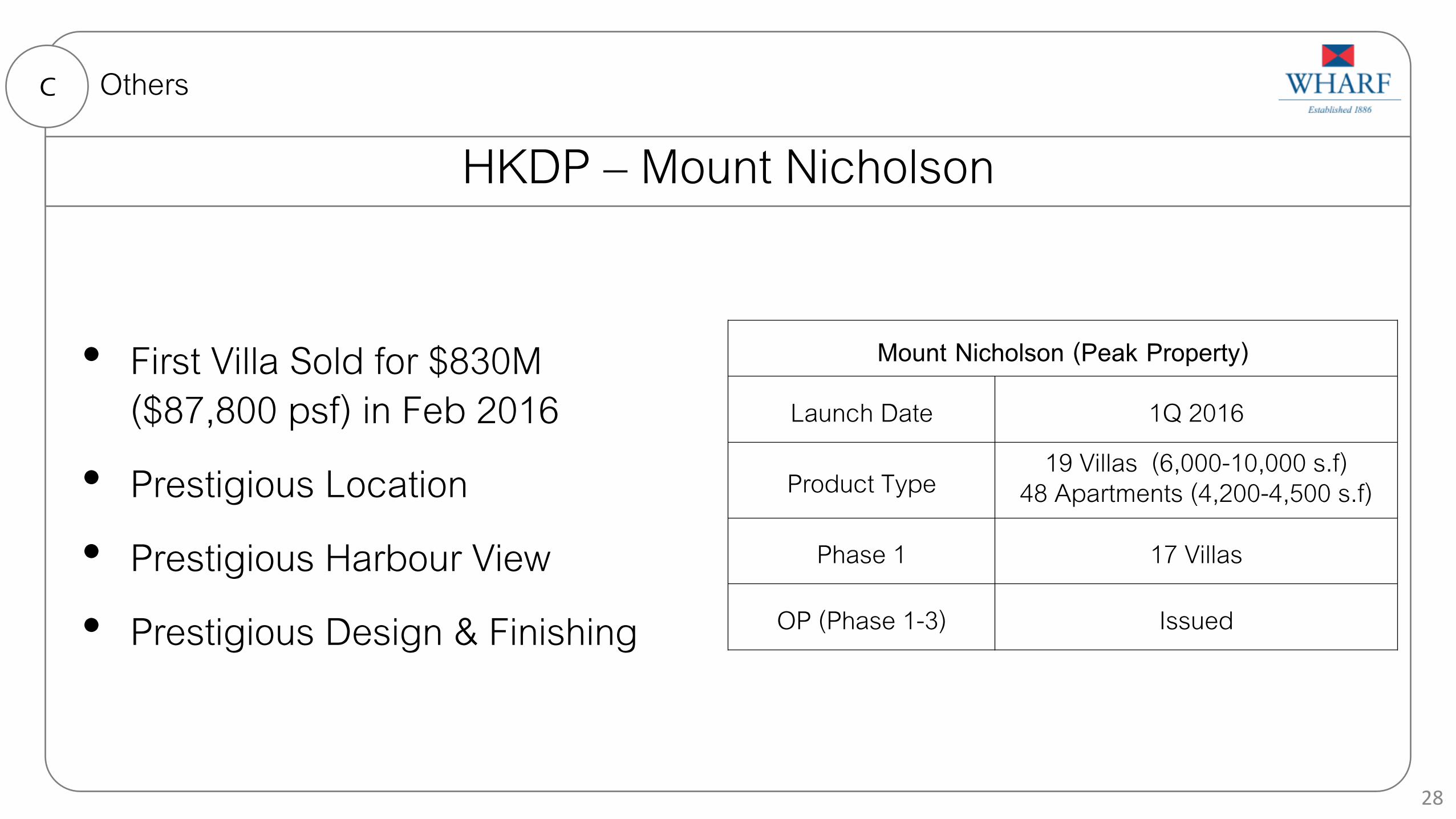

HKDP – Mount Nicholson

• First Villa Sold for $830M ($87,800 psf) in Feb 2016

• Prestigious Location

• Prestigious Harbour View

• Prestigious Design & Finishing

C Others

Mount Nicholson (Peak Property)

Launch Date 1Q 2016

Product Type 19 Villas (6,000-10,000 s.f) 48 Apartments (4,200-4,500 s.f)

Phase 1 17 Villas

OP (Phase 1-3) Issued

28

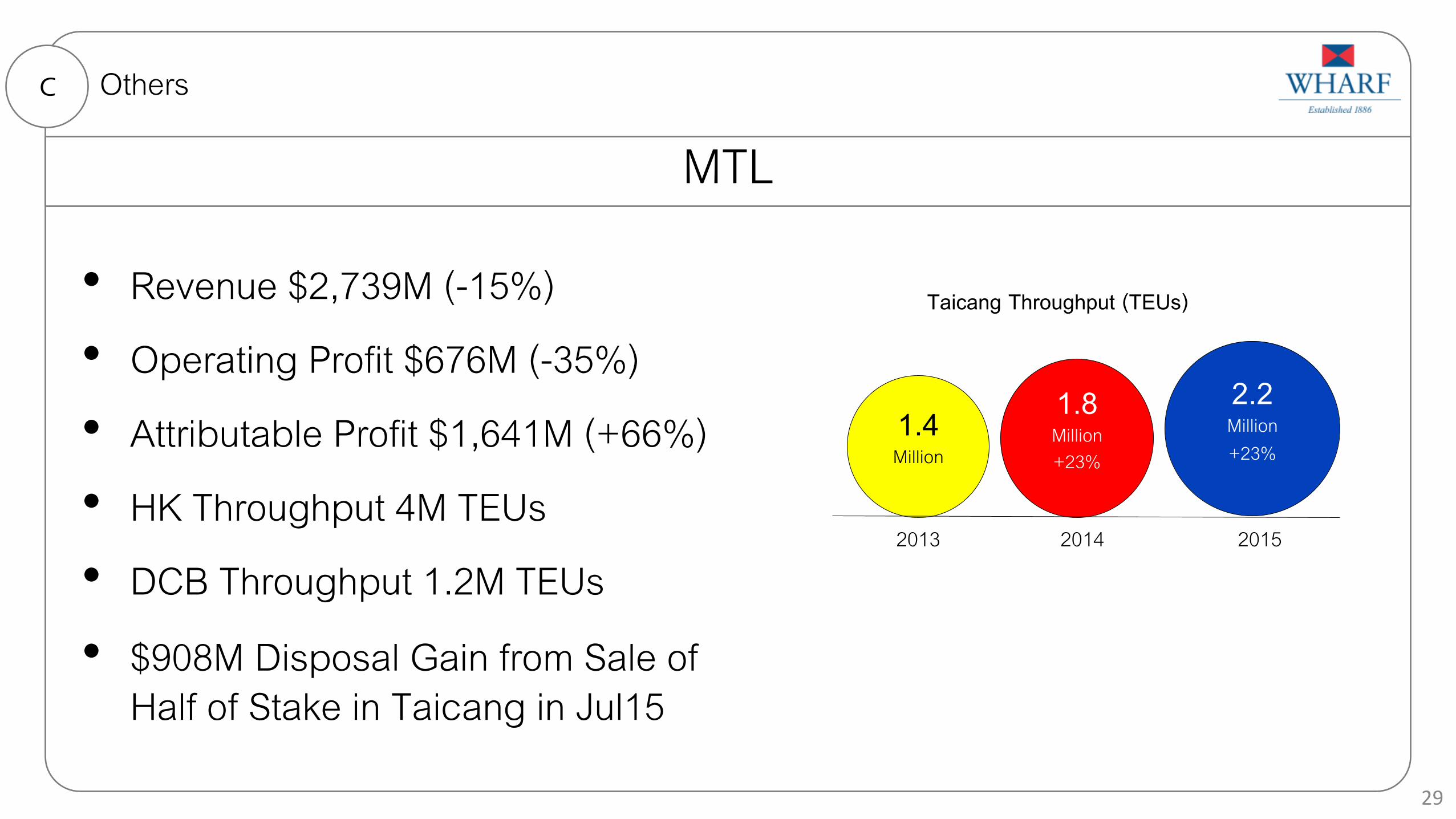

MTL

• Revenue $2,739M (-15%)

• Operating Profit $676M (-35%)

• Attributable Profit $1,641M (+66%)

• HK Throughput 4M TEUs

• DCB Throughput 1.2M TEUs

• $908M Disposal Gain from Sale of Half of Stake in Taicang in Jul15

C Others

2015 2014

Taicang Throughput (TEUs)

2.2 Million +23%

1.4 Million

29

1.8 Million +23%

2013

Marco Polo Hotel

• Revenue $1,549M (-$51M)

• Operating Profit $278M (-$109M)

• Hospitality Industry Under Pressure

• Niccolo in CDIFS Commands One of the Highest Room Yields in Chengdu in Less than One Year from Opening

C Others

30

CME*

Wharf T&T • Achieved Record Results

• Revenue $1,991M (+$41M)

• Operating Profit $362M (+$10M)

• Free Cash Flow Improved to $450M

C Others

31

i-Cable • Revenue $1,510M (-$156M)

• Operating Loss $246M

• Early Signs of Subscription Revenue Stabilization

* Strategic Review to Evaluate Different Options to Enhance These Businesses

Prudent Financial Management C

21.1%

25.6%

18.8% 15.8%

19.2% 20.6% 21.7% 20.4%

18.9%

14.9%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Net Debt to Total Equity

Net Debt / (Cash)

(HKD B) Wharf

(excl. subs) MTL HCDL i-CABLE Group Total

Net Debt to Total Equity

31 Dec 2015 39.9 8.8 (1.7) 0.2 47.2 14.9% 31 Dec 2014 49.0 11.0 (0.7) 0.0 59.3 18.9%

• Disciplined Capital Allocation

• Net Debt to Total Equity Fell Below 15% (2014: 19%)

• Group Net Debt $47B, Decreased by $12B

Others

32

Prudent Financial Management C

• Floating Rate Debt: 83% of Total Debt

RMB Devaluation Impact: • Net Loss $158M

• Shareholders’ Equity: Net Exchange Deficit $6.5B

2.3% 2.8%

3.2% 3.2% 2.8%

2011 2012 2013 2014 2015

Average Interest Cost

8.5

13.1 11.9 15.3 14.1

7.8

Jan16-Dec16 Jan17-Dec17 Jan18-Dec18 Jan19-Dec19 Jan20-Dec20 Jan21 & After

Debt Maturity (HKD billion)

Others

33

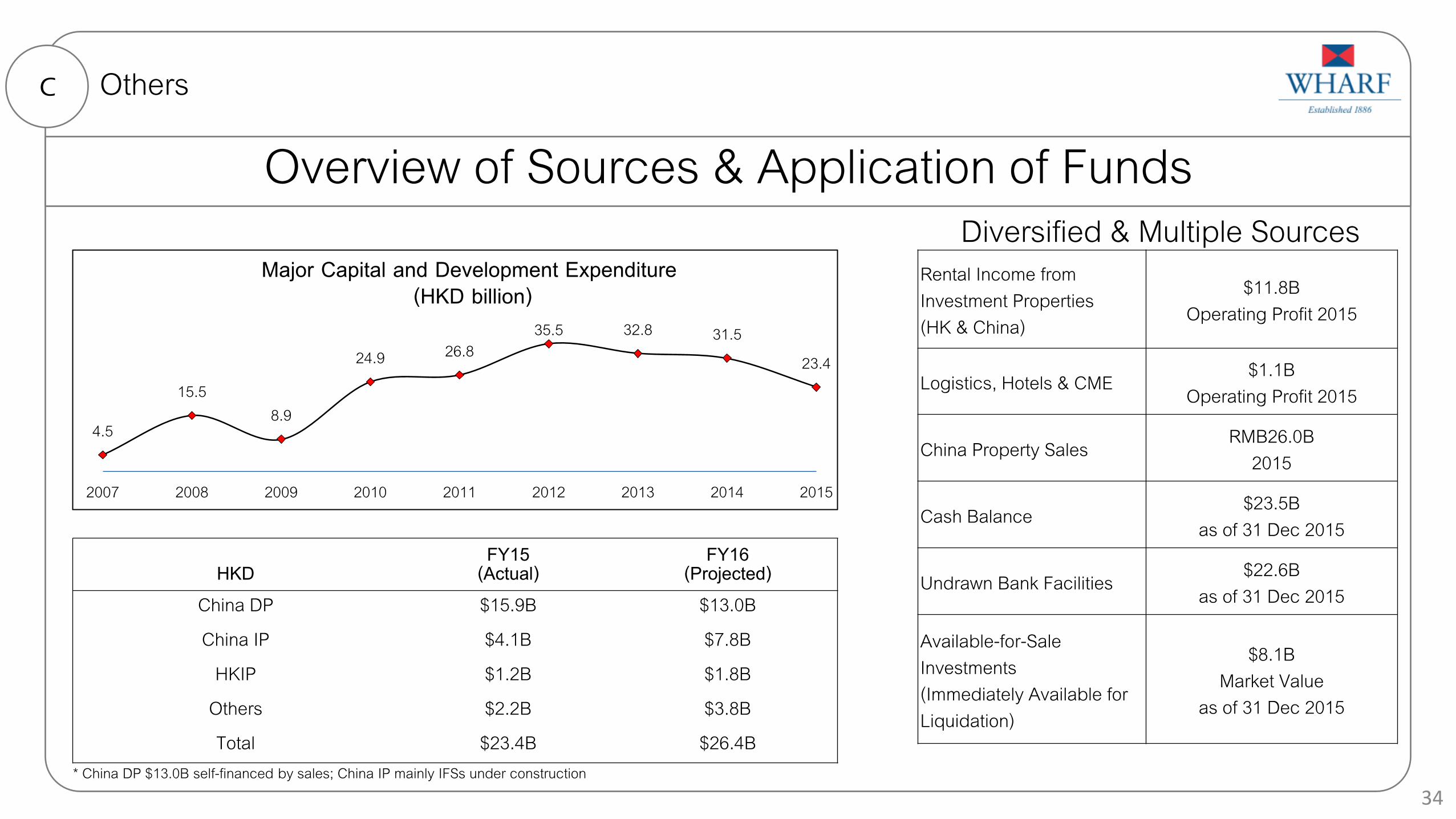

Overview of Sources & Application of Funds C

Diversified & Multiple Sources

* China DP $13.0B self-financed by sales; China IP mainly IFSs under construction

HKD FY15

(Actual) FY16

(Projected) China DP $15.9B $13.0B China IP $4.1B $7.8B

HKIP $1.2B $1.8B Others $2.2B $3.8B Total $23.4B $26.4B

4.5

15.5 8.9

24.9 26.8 35.5 32.8 31.5

23.4

2007 2008 2009 2010 2011 2012 2013 2014 2015

Major Capital and Development Expenditure (HKD billion)

Rental Income from Investment Properties (HK & China)

$11.8B Operating Profit 2015

Logistics, Hotels & CME $1.1B Operating Profit 2015

China Property Sales RMB26.0B 2015

Cash Balance $23.5B as of 31 Dec 2015

Undrawn Bank Facilities $22.6B as of 31 Dec 2015

Available-for-Sale Investments (Immediately Available for Liquidation)

$8.1B Market Value

as of 31 Dec 2015

Others

34

Agenda

Hong Kong IP A

China IP & DP B

Others C

Next D

35

Next Highlights D Next

OT 4-Storey Extension CSIFS CQIFS

36

CSR

37

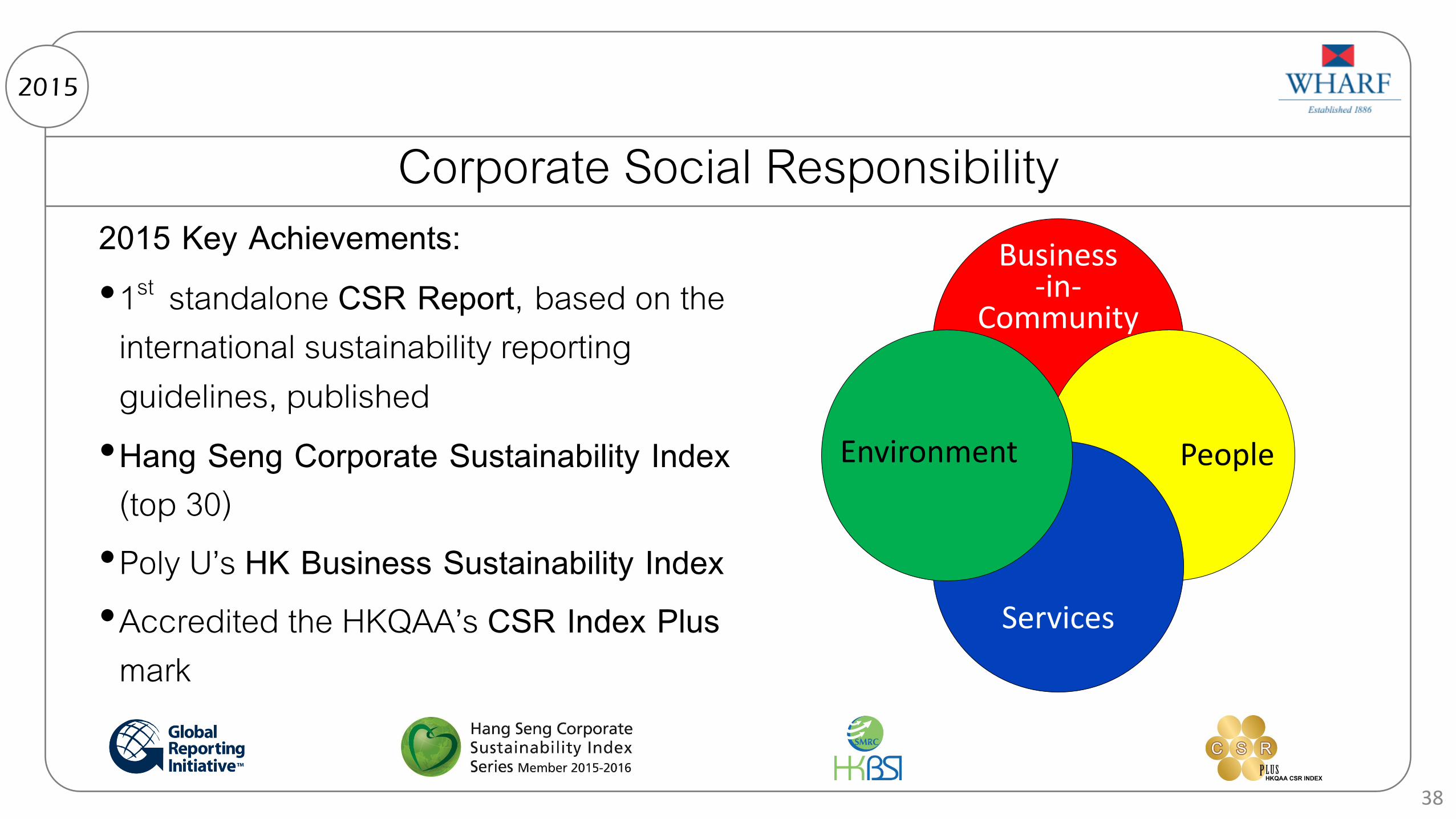

2015

Corporate Social Responsibility

38

2015 Key Achievements: •1st standalone CSR Report, based on the

international sustainability reporting guidelines, published

•Hang Seng Corporate Sustainability Index (top 30)

•Poly U’s HK Business Sustainability Index •Accredited the HKQAA’s CSR Index Plus

mark

Business -in-

Community

People

Services

Environment

2015

Business-in-Community

39

Flagship Business-in-Community initiative Project WeCan

Key Youth Development initiative Architectural Design Internship

Project Partners

27 Companies 3 Universities

3 Consulates 2 Organizations

Supporting

50 schools 42,000 students*

*representing a substantial 30% of students in all lower banding schools

Project Partners

2 Universities

Awardees

16 postgraduates (architecture)

Countries for Internships so far France, Germany, Japan, The Netherlands, Switzerland and USA

Appendix

40

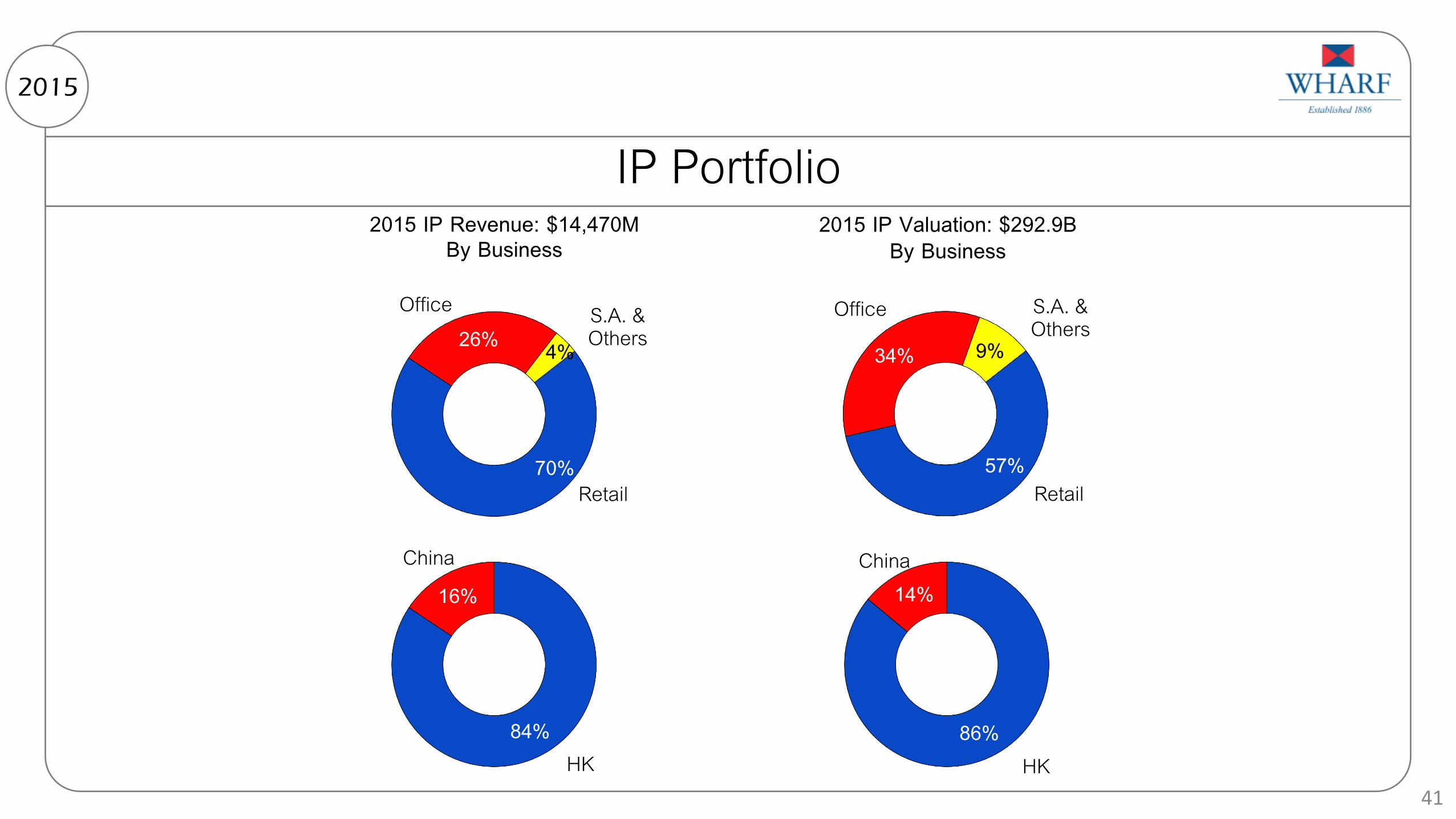

IP Portfolio 2015

70%

26% 4%

Office S.A. & Others

Retail 57%

34% 9%

Office S.A. & Others

Retail

84%

16% China

HK 86%

14% China

HK

2015 IP Revenue: $14,470M By Business

2015 IP Valuation: $292.9B By Business

41

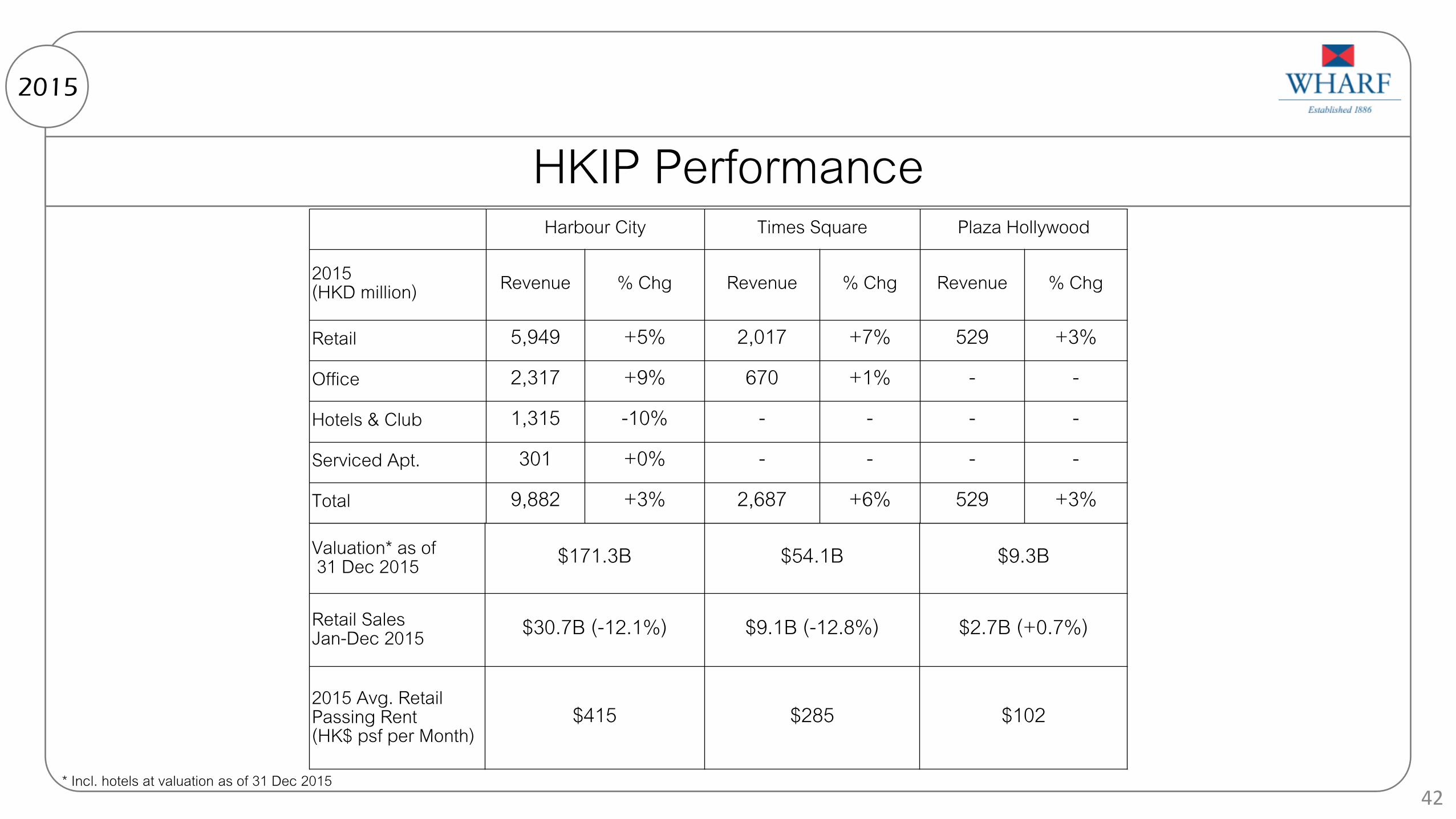

HKIP Performance 2015

Harbour City Times Square Plaza Hollywood

2015 (HKD million) Revenue % Chg Revenue % Chg Revenue % Chg

Retail 5,949 +5% 2,017 +7% 529 +3% Office 2,317 +9% 670 +1% - - Hotels & Club 1,315 -10% - - - - Serviced Apt. 301 +0% - - - - Total 9,882 +3% 2,687 +6% 529 +3%

Valuation* as of 31 Dec 2015 $171.3B $54.1B $9.3B

Retail Sales Jan-Dec 2015 $30.7B (-12.1%) $9.1B (-12.8%) $2.7B (+0.7%)

2015 Avg. Retail Passing Rent (HK$ psf per Month)

$415 $285 $102

* Incl. hotels at valuation as of 31 Dec 2015 42

Retail Performance 2015

80.0 114.0

138.0 163.5 167.6

2011 2012 2013 2014 2015

Retail Valuation (HKD billion)

4.8 5.5

6.4

7.8 8.4

2011 2012 2013 2014 2015

Retail Operating Profit (HKD billion)

43

Commercial Properties Pipeline 2015

14.0 14.2 14.2 14.2 14.5

5.7 5.7 5.7 5.7 5.7

3.9 6.6 7.4 8.2 8.2 2.0 2.0

6.9 6.9 2.2 2.2

2.7 2.7 0.8 0.8 4.0

8.7

11.0

2013 2014 2015 2016 2017

Commercial Properties Completion Schedule (Million s.f)

Changsha IFS

Suzhou IFS

Changsha Outlets

Wuxi IFS

Chongqing IFS*

Chengdu IFS

Other China Commercial Prop.

HK Commercial Prop.

53.8M s.f

Total development area, incl. basement area & carpark *Gross Basis

44

China Commercial Properties Pipeline 2015

645,000 s.m.*

Retail, Grade A offices & hotel

Retail 102,000 s.m.

300m tower

Jiangbei new CBD

50:50 JV with COLI

2016

368,000 s.m.

Grade A offices, apartments & hotel

No Retail

450m tower

Suzhou new CBD

80:20 JV with Genway

2017

250,000 s.m.

Grade A offices & hotel

No Retail

339m tower

Taihu Plaza CBD

wholly-owned

2016

1,026,000 s.m.

Retail, Grade A offices & hotel

Retail 230,000 s.m.

452m tower

Prime city center

wholly-owned

2017

Wuxi IFS Chongqing IFS Suzhou IFS

* Gross area

Changsha IFS

45

Chengdu City Profile

• Financial Center & Trading Hub in SW China

• Thriving City for Business Start-Ups

2015

46

4%

44%

53%

Tertiary Primary

Secondary

2015 Tertiary Industry +9.0% 53% of CD GDP (National: 50.5%)

Chengdu

Population 14 million

2015 GDP +7.9% (National Avg.: +6.9%)

2015 Retail Sales +10.7%

2015 Disposable Income per Capita

RMB33,476 +8.0%

No. of Fortune 500 Companies in 2015 299

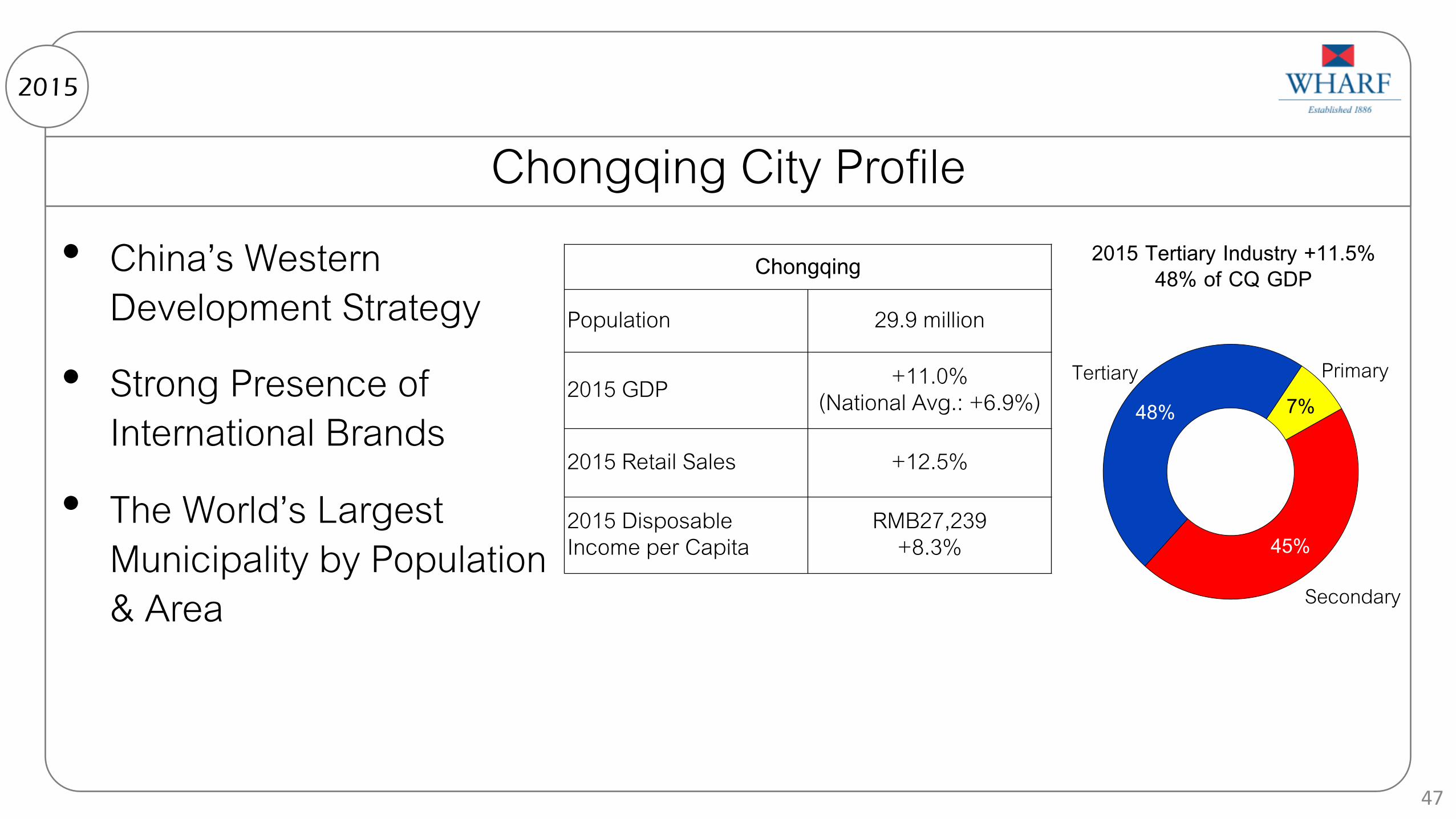

Chongqing City Profile • China’s Western

Development Strategy

• Strong Presence of International Brands

• The World’s Largest Municipality by Population & Area

2015

47

7%

45%

48% Tertiary Primary

Secondary

2015 Tertiary Industry +11.5% 48% of CQ GDP Chongqing

Population 29.9 million

2015 GDP +11.0% (National Avg.: +6.9%)

2015 Retail Sales +12.5%

2015 Disposable Income per Capita

RMB27,239 +8.3%

Changsha City Profile • Hub City in Central China

• Beneficiary of China’s “Rise of Central China” Campaign

• Important Entertainment Center in China – Presence of Hunan Satellite TV

2015

48

4%

53%

43% Tertiary Primary

Secondary

2015 Tertiary Industry +12.1% 43% of CS GDP Changsha

Population 7.3 million

2015 GDP +9.9% (National Avg.: +6.9%)

2015 Retail Sales +12.1%

2015 Disposable Income per Capita

RMB39,961 +8.5%

China Contracted Sales Breakdown by City 2015

49

Region City No. of projects on sale in 2015

Contracted Sales (%)

GFA Sold (%)

Eastern China Shanghai 6 27% 12% Suzhou 5 21% 20% Wuxi 4 7% 14% Changzhou 3 3% 8% Ningbo 3 3% 3% Hangzhou 8 17% 10%

Eastern China Sub-Total: 29 78% 67% Western China Chengdu 7 4% 8%

Chongqing 3 5% 8% Western China Sub-Total: 10 9% 16%

Southern China Foshan & Guangzhou 8 4% 8% Others Beijing 1 3% 1%

Tianjin, Dalian & Wuhan 6 6% 8% Southern & Others Sub-Total: 15 13% 17%

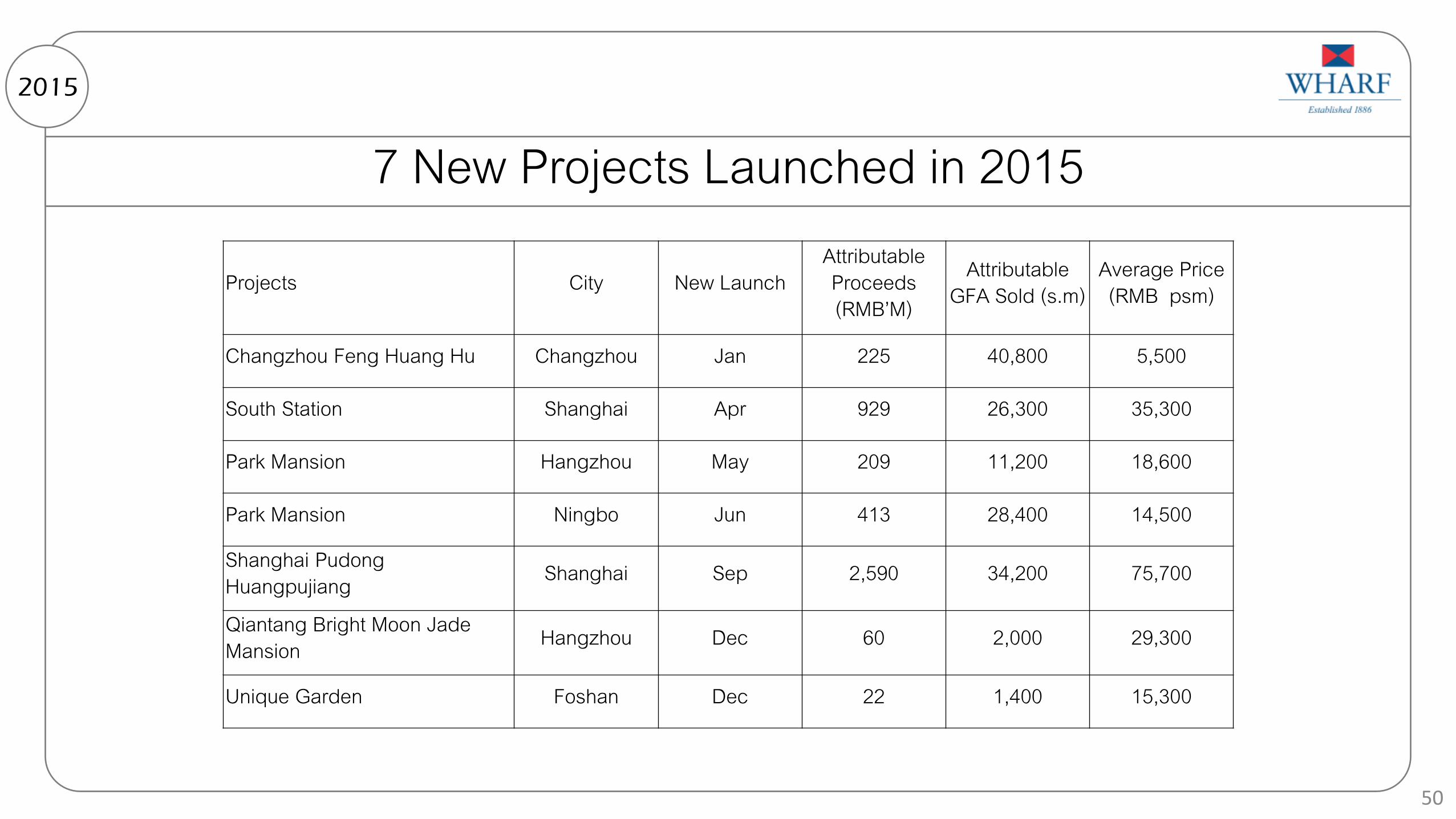

7 New Projects Launched in 2015 2015

50

Projects City New Launch Attributable Proceeds (RMB’M)

Attributable GFA Sold (s.m)

Average Price (RMB psm)

Changzhou Feng Huang Hu Changzhou Jan 225 40,800 5,500

South Station Shanghai Apr 929 26,300 35,300

Park Mansion Hangzhou May 209 11,200 18,600

Park Mansion Ningbo Jun 413 28,400 14,500

Shanghai Pudong Huangpujiang Shanghai Sep 2,590 34,200 75,700

Qiantang Bright Moon Jade Mansion Hangzhou Dec 60 2,000 29,300

Unique Garden Foshan Dec 22 1,400 15,300

China Key Projects on Sales in 2015 2015

51

Projects City Attributable Proceeds (RMB’M)

Attributable GFA sold

(s.m) Average Price

(RMB psm) Ownership

Suzhou Times City Suzhou 3,203 180,900 17,400 80% Shanghai Pudong Huangpujiang Shanghai 2,590 34,200 75,700 100%

Zhoupu Shanghai 2,451 72,400 33,900 100% Palazzo Pitti (Lot C) Hangzhou 1,372 48,500 26,300 100% Ambassador Villa Suzhou 1,222 30,400 37,800 100% Royal Seal Hangzhou 1,082 23,800 43,600 100% South Station Shanghai 929 26,300 35,300 27% Bellagio Suzhou 864 65,000 13,300 100% Unique Garden Beijing 754 13,700 53,700 33% Bi Xi Wuxi 753 79,600 9,400 100% Qiantang Ming Yue Hangzhou 740 26,200 26,200 50% Songjiang Xianhe Rd. Shanghai 734 25,200 29,100 100%

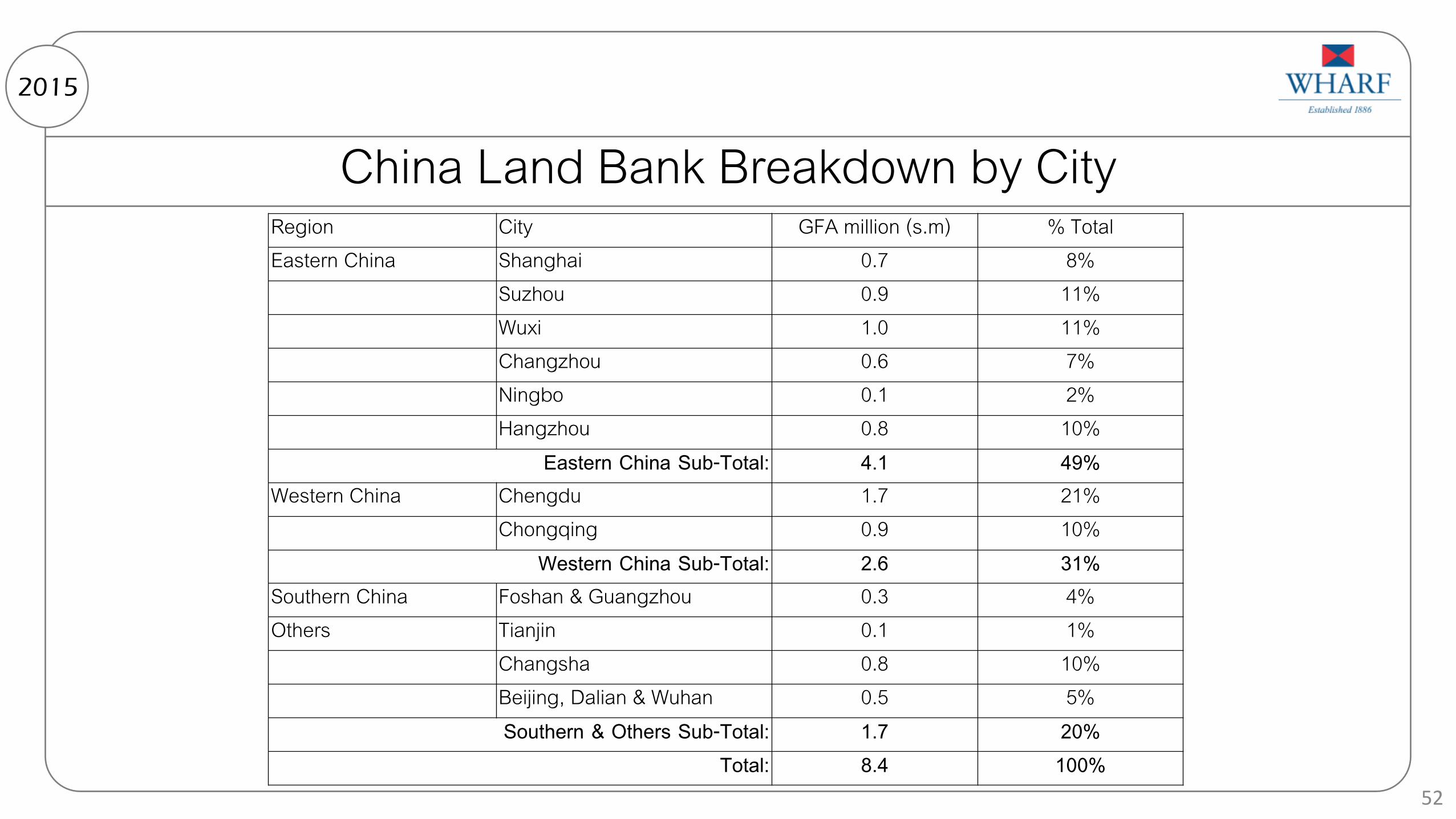

China Land Bank Breakdown by City 2015

52

Region City GFA million (s.m) % Total Eastern China Shanghai 0.7 8%

Suzhou 0.9 11% Wuxi 1.0 11% Changzhou 0.6 7% Ningbo 0.1 2% Hangzhou 0.8 10%

Eastern China Sub-Total: 4.1 49% Western China Chengdu 1.7 21%

Chongqing 0.9 10% Western China Sub-Total: 2.6 31%

Southern China Foshan & Guangzhou 0.3 4% Others Tianjin 0.1 1%

Changsha 0.8 10% Beijing, Dalian & Wuhan 0.5 5% Southern & Others Sub-Total: 1.7 20%

Total: 8.4 100%

China Key Properties Completion 2015

53

Projects Attributable GFA (s.m) Key completion in 2015 Suzhou Times City 243,200 Wuxi Times City 166,900 Hangzhou Palazzo Pitti (Lot C/D) 152,400 Hangzhou Shi Ji Hua Fu 128,100 Hangzhou Junting 127,300 Chengdu Le Palais 113,800 Projected key completion in 2016 Changzhou Feng Huang Hu 234,100 Suzhou Times City 193,900 Chongqing IFS 141,700 Changzhou Ambassador Villa 129,700 Hangzhou Greentown Zhijiang No.1 104,500 Ningbo Park Mansion 103,900

China New Projects for Sale in 2016 2015

54

Projects City Ownership

Site No. 12 Hangzhou 100%

Site No. 13 Hangzhou 100%

Jingan Garden Shanghai 55%

The Pearl on the Crown Beijing 25%

Crown Land Beijing 25%

Thank You

2015

55

Resilient IP Core

2015

56

End of Presentation

The Wharf (Holdings) Limited [HKEx Stock Code: 0004.HK]

Disclaimer

1) All information and data are provided for information purposes only. All opinions included

herein constitute Wharf’s judgment as of the date hereof and are subject to change without

notice. The Group, its subsidiaries and affiliates hereby disclaim (i) all express, implied,

and statutory warranties of any kind to user and/or any third party including warranties as

to accuracy, timeliness, completeness, or fitness for any particular purpose; and (ii) any

liability whatsoever for any loss howsoever arising from or in reliance upon the whole or

any part of the information and data contained herein.

2) The full-year statutory financial information of preceding financial years quoted in this

presentation are derived from statutory annual financial statements for that relevant

financial years, each of which had been delivered to Registrar of Companies in accordance

with the prevailing Companies Ordinance and were reported on by the auditors with

relevant auditors’ reports without qualification or modification.