the worldwide reference in liner shipping - joc.com · pdf filethe worldwide reference in...

TRANSCRIPT

Supply & Demand :

Does it still matter?

ALPHALINER The worldwide reference in liner shipping

Web: www.alphaliner.com E-mail: [email protected]

Transpacific Maritime – March 2013 1

ALPHALINER Containership Market Outlook 2013 www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2013 – Contents not to be reproduced without permission

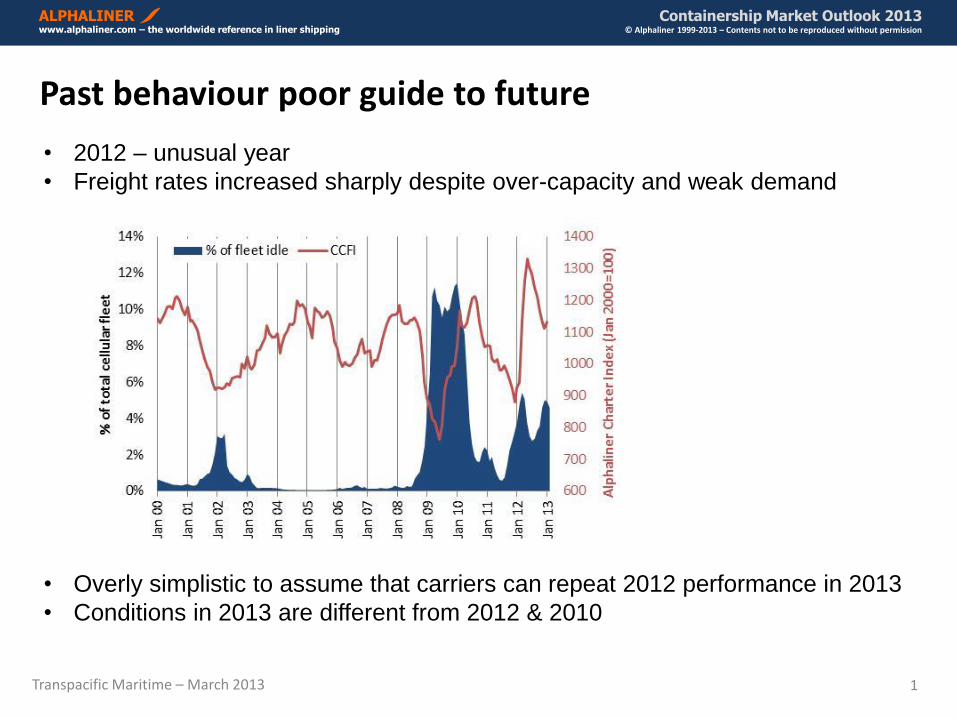

Past behaviour poor guide to future

• 2012 – unusual year

• Freight rates increased sharply despite over-capacity and weak demand

• Overly simplistic to assume that carriers can repeat 2012 performance in 2013

• Conditions in 2013 are different from 2012 & 2010

Transpacific Maritime – March 2013 2

ALPHALINER Containership Market Outlook 2013 www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2013 – Contents not to be reproduced without permission

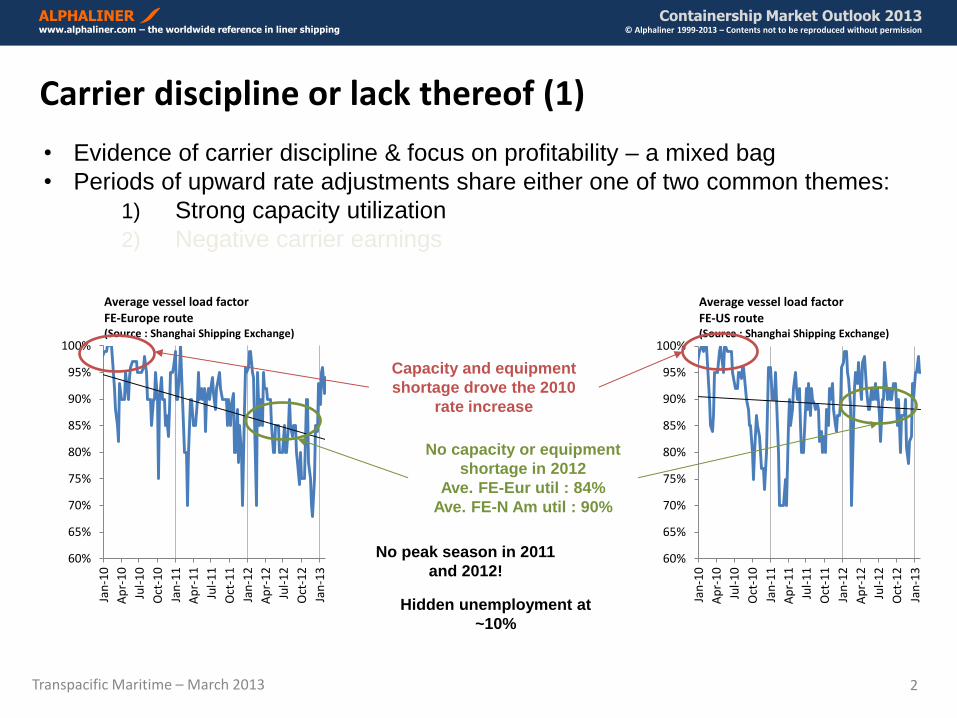

Carrier discipline or lack thereof (1)

• Evidence of carrier discipline & focus on profitability – a mixed bag

• Periods of upward rate adjustments share either one of two common themes:

1) Strong capacity utilization

2) Negative carrier earnings

60%

65%

70%

75%

80%

85%

90%

95%

100%

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Average vessel load factor FE-Europe route (Source : Shanghai Shipping Exchange)

60%

65%

70%

75%

80%

85%

90%

95%

100%

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Average vessel load factor FE-US route (Source : Shanghai Shipping Exchange)

Capacity and equipment

shortage drove the 2010

rate increase

No capacity or equipment

shortage in 2012

Ave. FE-Eur util : 84%

Ave. FE-N Am util : 90%

No peak season in 2011

and 2012!

Hidden unemployment at

~10%

Transpacific Maritime – March 2013 3

ALPHALINER Containership Market Outlook 2013 www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2013 – Contents not to be reproduced without permission

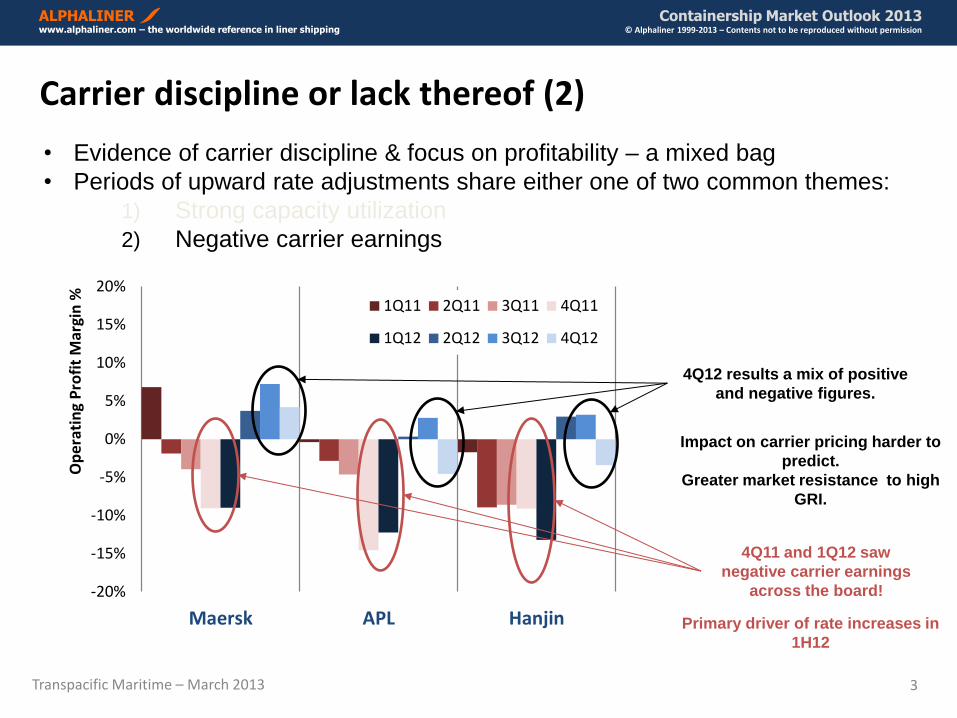

Carrier discipline or lack thereof (2)

• Evidence of carrier discipline & focus on profitability – a mixed bag

• Periods of upward rate adjustments share either one of two common themes:

1) Strong capacity utilization

2) Negative carrier earnings

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Maersk APL Hanjin

Op

era

tin

g P

rofi

t M

argi

n %

1Q11 2Q11 3Q11 4Q11

1Q12 2Q12 3Q12 4Q12

4Q11 and 1Q12 saw

negative carrier earnings

across the board!

Impact on carrier pricing harder to

predict.

Greater market resistance to high

GRI.

4Q12 results a mix of positive

and negative figures.

Primary driver of rate increases in

1H12

Transpacific Maritime – March 2013 4

ALPHALINER Containership Market Outlook 2013 www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2013 – Contents not to be reproduced without permission

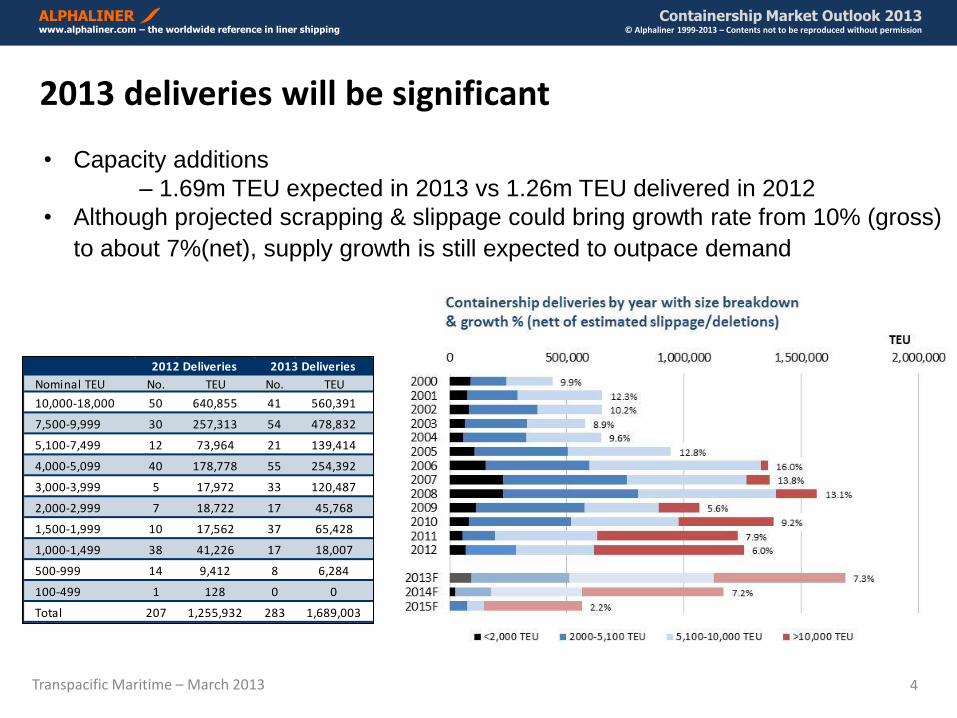

2013 deliveries will be significant

• Capacity additions

– 1.69m TEU expected in 2013 vs 1.26m TEU delivered in 2012

• Although projected scrapping & slippage could bring growth rate from 10% (gross)

to about 7%(net), supply growth is still expected to outpace demand

Nominal TEU No. TEU No. TEU

10,000-18,000 50 640,855 41 560,391

7,500-9,999 30 257,313 54 478,832

5,100-7,499 12 73,964 21 139,414

4,000-5,099 40 178,778 55 254,392

3,000-3,999 5 17,972 33 120,487

2,000-2,999 7 18,722 17 45,768

1,500-1,999 10 17,562 37 65,428

1,000-1,499 38 41,226 17 18,007

500-999 14 9,412 8 6,284

100-499 1 128 0 0

Total 207 1,255,932 283 1,689,003

2013 Deliveries2012 Deliveries

Transpacific Maritime – March 2013 5

ALPHALINER Containership Market Outlook 2013 www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2013 – Contents not to be reproduced without permission

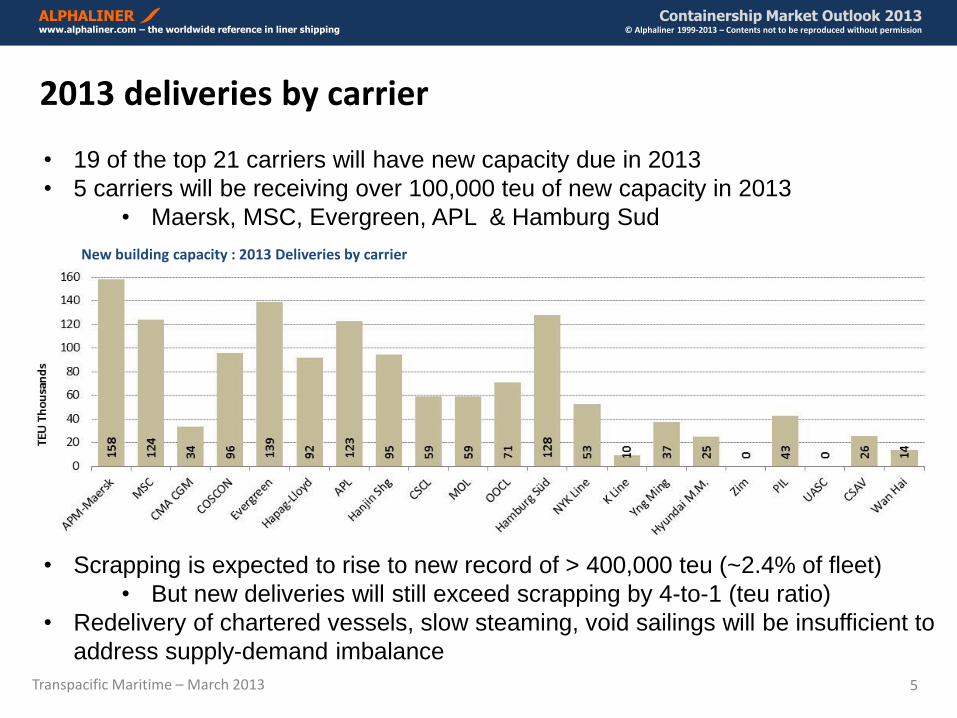

2013 deliveries by carrier

• 19 of the top 21 carriers will have new capacity due in 2013

• 5 carriers will be receiving over 100,000 teu of new capacity in 2013

• Maersk, MSC, Evergreen, APL & Hamburg Sud

• Scrapping is expected to rise to new record of > 400,000 teu (~2.4% of fleet)

• But new deliveries will still exceed scrapping by 4-to-1 (teu ratio)

• Redelivery of chartered vessels, slow steaming, void sailings will be insufficient to

address supply-demand imbalance

New building capacity : 2013 Deliveries by carrier

Transpacific Maritime – March 2013 6

ALPHALINER Containership Market Outlook 2013 www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2013 – Contents not to be reproduced without permission

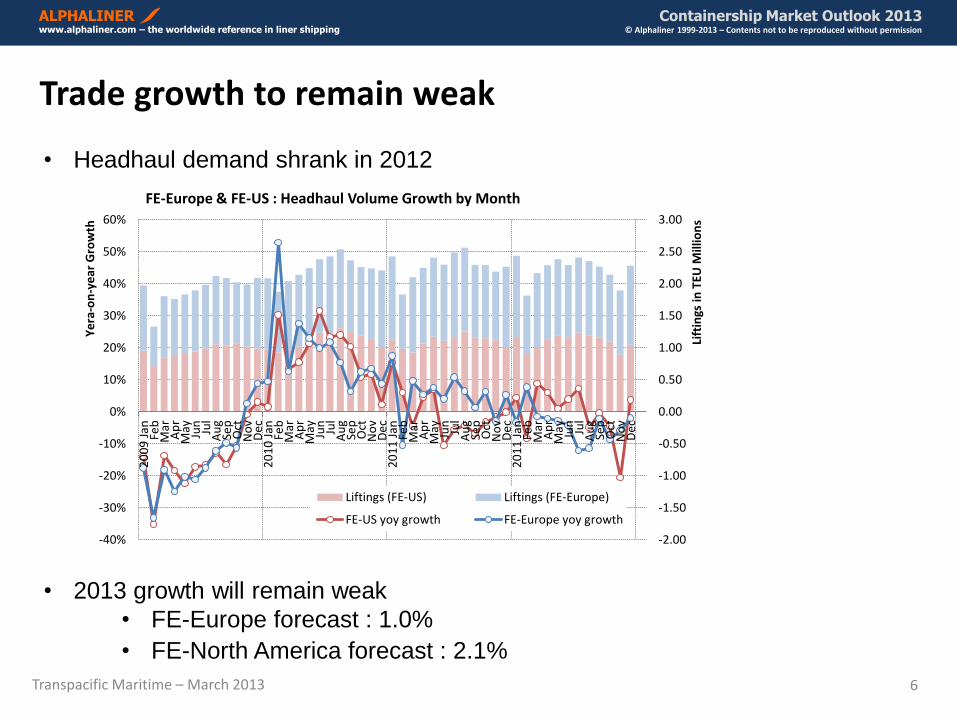

Trade growth to remain weak

• Headhaul demand shrank in 2012

• 2013 growth will remain weak

• FE-Europe forecast : 1.0%

• FE-North America forecast : 2.1%

-2.00

-1.50

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

3.00

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

20

09

Jan Fe

bM

arA

pr

May Jun

Jul

Au

gSe

pO

ctN

ov

De

c2

01

0 J

an Feb

Mar

Ap

rM

ay Jun

Jul

Au

gSe

pO

ctN

ov

De

c2

01

1 J

an Feb

Mar

Ap

rM

ay Jun

Jul

Au

gSe

pO

ctN

ov

De

c2

01

1 J

an Feb

Mar

Ap

rM

ay Jun

Jul

Au

gSe

pO

ctN

ov

De

c

Lift

ings

in T

EU M

illio

ns

Ye

ra-o

n-y

ear

Gro

wth

FE-Europe & FE-US : Headhaul Volume Growth by Month

Liftings (FE-US) Liftings (FE-Europe)

FE-US yoy growth FE-Europe yoy growth

Transpacific Maritime – March 2013 7

ALPHALINER Containership Market Outlook 2013 www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2013 – Contents not to be reproduced without permission

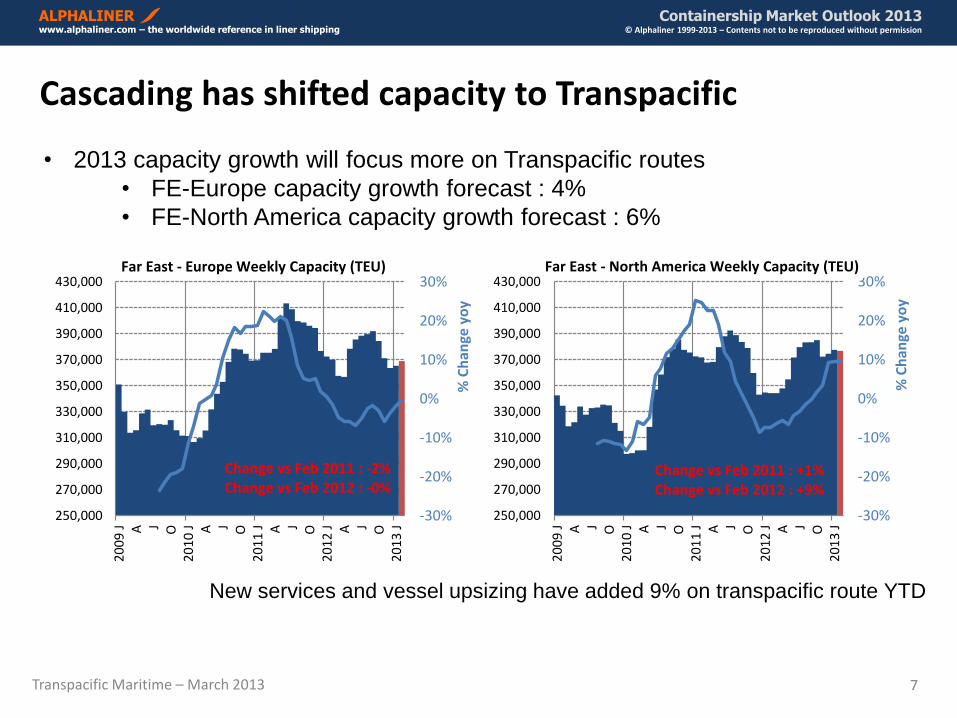

Cascading has shifted capacity to Transpacific

• 2013 capacity growth will focus more on Transpacific routes

• FE-Europe capacity growth forecast : 4%

• FE-North America capacity growth forecast : 6%

-30%

-20%

-10%

0%

10%

20%

30%

250,000

270,000

290,000

310,000

330,000

350,000

370,000

390,000

410,000

430,000

20

09

J A J O2

01

0 J A J O

20

11

J A J O2

01

2 J A J O

20

13

J

% C

han

ge y

oy

Far East - Europe Weekly Capacity (TEU)

Change vs Feb 2011 : -2% Change vs Feb 2012 : -0%

-30%

-20%

-10%

0%

10%

20%

30%

250,000

270,000

290,000

310,000

330,000

350,000

370,000

390,000

410,000

430,000

20

09

J A J O2

01

0 J A J O

20

11

J A J O2

01

2 J A J O

20

13

J

% C

han

ge y

oy

Far East - North America Weekly Capacity (TEU)

Change vs Feb 2011 : +1% Change vs Feb 2012 : +9%

New services and vessel upsizing have added 9% on transpacific route YTD

Transpacific Maritime – March 2013 8

ALPHALINER Containership Market Outlook 2013 www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2013 – Contents not to be reproduced without permission

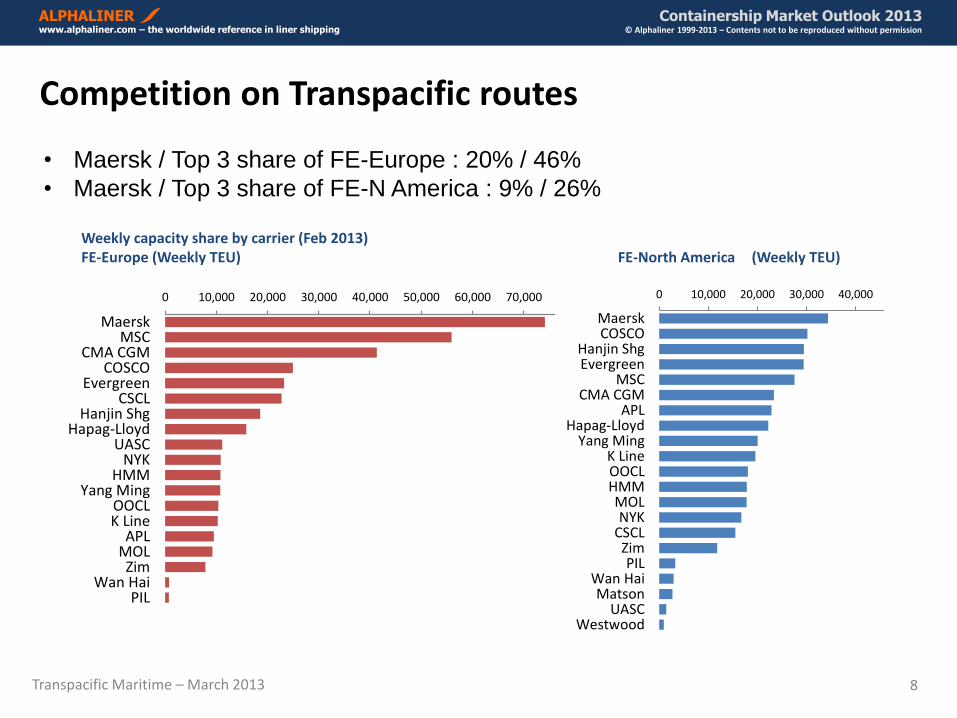

Competition on Transpacific routes

• Maersk / Top 3 share of FE-Europe : 20% / 46%

• Maersk / Top 3 share of FE-N America : 9% / 26%

Weekly capacity share by carrier (Feb 2013) FE-Europe (Weekly TEU) FE-North America (Weekly TEU)

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000

MaerskCOSCO

Hanjin ShgEvergreen

MSCCMA CGM

APLHapag-Lloyd

Yang MingK LineOOCLHMMMOLNYK

CSCLZimPIL

Wan HaiMatson

UASCWestwood

FE - North America Weekly Capacity in nominal TEU

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000

MaerskMSC

CMA CGMCOSCO

EvergreenCSCL

Hanjin ShgHapag-Lloyd

UASCNYK

HMMYang Ming

OOCLK Line

APLMOLZim

Wan HaiPIL

FE - Europe Weekly Capacity in nominal TEU

Transpacific Maritime – March 2013 9

ALPHALINER Containership Market Outlook 2013 www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2013 – Contents not to be reproduced without permission

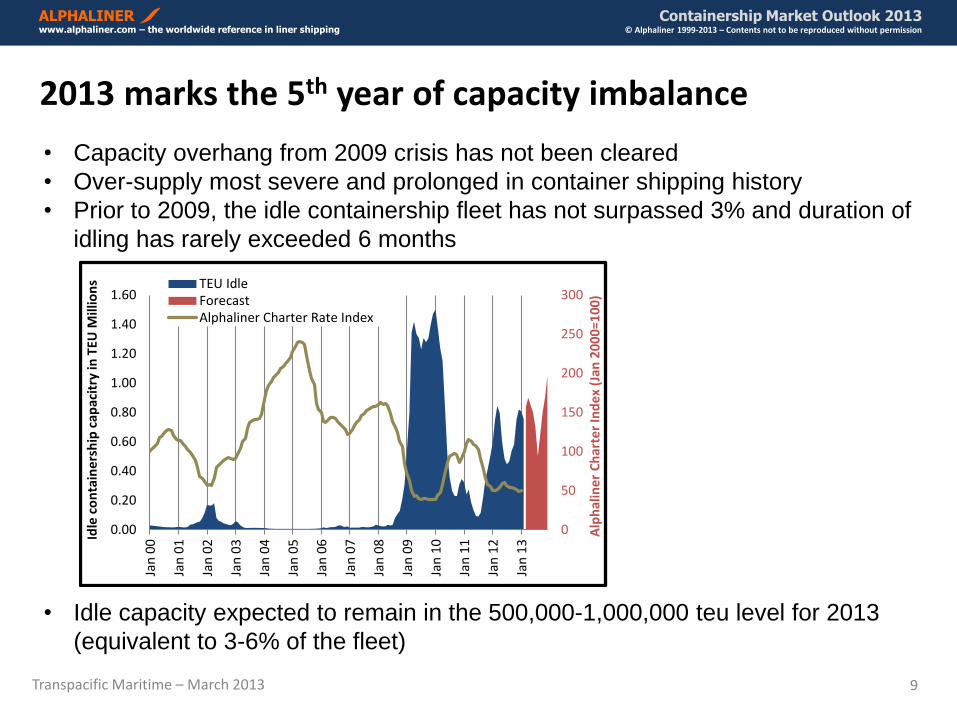

2013 marks the 5th year of capacity imbalance

• Capacity overhang from 2009 crisis has not been cleared

• Over-supply most severe and prolonged in container shipping history

• Prior to 2009, the idle containership fleet has not surpassed 3% and duration of

idling has rarely exceeded 6 months

• Idle capacity expected to remain in the 500,000-1,000,000 teu level for 2013

(equivalent to 3-6% of the fleet)

0

50

100

150

200

250

300

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

Jan

00

Jan

01

Jan

02

Jan

03

Jan

04

Jan

05

Jan

06

Jan

07

Jan

08

Jan

09

Jan

10

Jan

11

Jan

12

Jan

13

Alp

hal

ine

r C

har

ter

Ind

ex

(Jan

20

00

=10

0)

Idle

co

nta

ine

rsh

ip c

apac

itry

in T

EU M

illio

ns TEU Idle

ForecastAlphaliner Charter Rate Index

Transpacific Maritime – March 2013 10

ALPHALINER Containership Market Outlook 2013 www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2013 – Contents not to be reproduced without permission

Carriers unable to break surplus capacity trap in 2013

New deliveries

Return of chartered tonnage

Scrapping increases

Charter rates drop

Surplus Capacity

Rates fall below

breakeven

Idling of surplus capacity

Rates return to breakeven

Idle capacity re-activated

The surplus

capacity trap

may last to

2015

Transpacific Maritime – March 2013 11

ALPHALINER Containership Market Outlook 2013 www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2013 – Contents not to be reproduced without permission

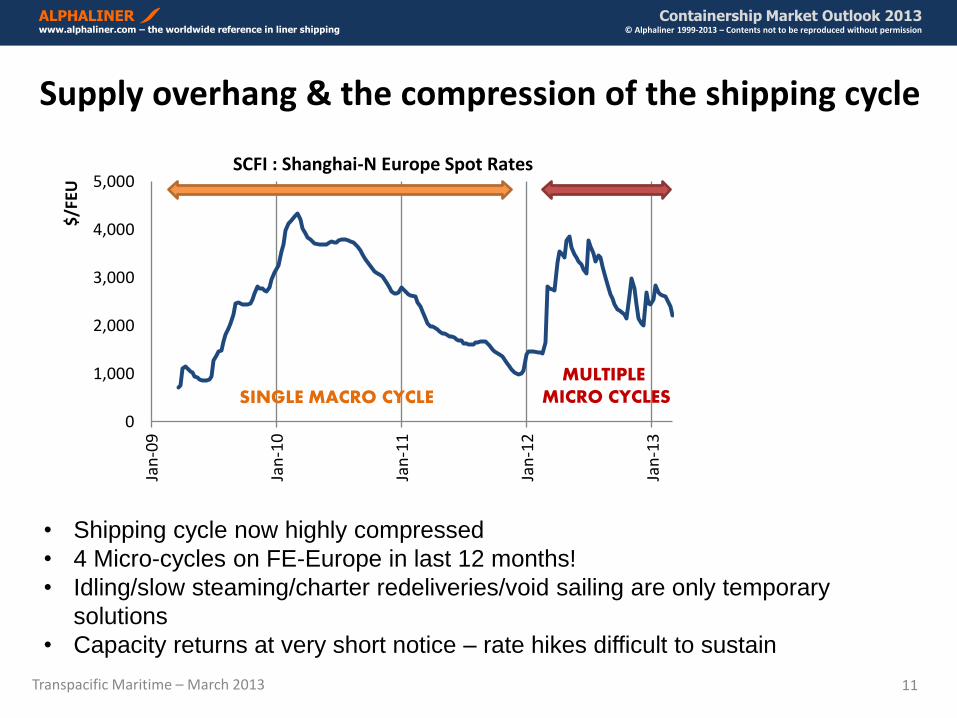

Supply overhang & the compression of the shipping cycle

0

1,000

2,000

3,000

4,000

5,000

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

$/F

EU

SCFI : Shanghai-N Europe Spot Rates

SINGLE MACRO CYCLE MULTIPLE

MICRO CYCLES

• Shipping cycle now highly compressed

• 4 Micro-cycles on FE-Europe in last 12 months!

• Idling/slow steaming/charter redeliveries/void sailing are only temporary

solutions

• Capacity returns at very short notice – rate hikes difficult to sustain

Transpacific Maritime – March 2013 12

ALPHALINER Containership Market Outlook 2013 www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2013 – Contents not to be reproduced without permission

Supply-Demand still relevant

• Rate volatility will continue

• Expect more GRI announcements throughout the year

• But GRI success rate will be lower than 2012

• Supply overhang will continue to dictate rates cycle in 2013

• Oversupply is in the 5-15% range

• Observed unemployment of ~5%

• Hidden unemployment of ~5-10%

• Intense competitive will continue

• None of the main carriers will exit the market

• Predictions of industry consolidation are premature

• Key indicators to watch

• Capacity utilisation

• Carrier profitability (or lack thereof)

Transpacific Maritime – March 2013 13

ALPHALINER Containership Market Outlook 2013 www.alphaliner.com – the worldwide reference in liner shipping © Alphaliner 1999-2013 – Contents not to be reproduced without permission

END

Please send any queries to [email protected]

Alphaliner clients include the following top shipping lines :