the zimbabwe 2019 mid-term fiscal policy review · the zimbabwe 2019 mid-term fiscal policy review...

TRANSCRIPT

The Zimbabwe2019 Mid-Term Fiscal Policy Review

Tax Summary

05 September 2019

Document Classification: KPMG Confidential

2© 2019 KPMG Zimbabwe is a partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The Honourable Mthuli Ncube, Minister of Finance and Economic Development,presented the 2019 Mid-Term Fiscal Policy Review Statement on Thursday (MTFP), 1August 2019 with the theme “Building a Strong Foundation for Future Prosperity”.

This summary includes the key changes from the 2019 Mid-Term Fiscal Policy ReviewStatement as confirmed in the Finance Act No 2 of 2019 which was gazetted into lawon Wednesday 21 August 2019. We have also included a summary of other keyexisting tax provisions.

This document expresses the views of KPMG and should not be interpreted as taxadvice. You are encouraged to seek specific tax advise based on your requirements.

Key highlights include:

Repealing of the Indigenisation Act allowing foreign investors to own greater than51% of businesses in diamond and platinum sectors. A new Act, the EconomicEmpowerment Act, will replace the Indigenisation Act.

No changes were made to rebase capital allowances in respect of capitalinvestment made in US$ prior to the introduction of the ZW$.

Revision of Pay As You Earn (PAYE) tax table effective 1 August 2019, includingseparate US$ and ZW$ tax tables. We also highlight the current inconsistencybetween the tax tables as gazetted (max rate of 45%) and those available on theZIMRA website as at 30 August 2019 (max rate 40%).

The ZW$60,000 VAT registration threshold and the annual tax free bonusthreshold for employees of ZW$1,000 remain unchanged.

The introduction of 2% royalties for small scale gold miners and a floating ratebetween 3% and 5% for large scale miners.

Mining royalties will be tax deductible, however, only effective from 1 January2020.

Excise Duty on fuel, tobacco and alcohol products have been increased.

Capital Gains Tax for immovable property acquired before 22 February 2019 to becomputed at 5% on the gross selling price or assessed value.

IMTT capped at ZW$15 000 for transactions above ZW$750 000.

The key policy proposals announced in the 2019 National Budget are also included inthis document.

Overview

The information contained herein is of a general nature and is not intended to address thecircumstances of any particular individual or entity. Although we endeavour to provide accurateand timely information, there can be no guarantee that such information is accurate as of the dateit is received or that it will continue to be accurate in the future. No-one should act on suchinformation without appropriate professional advice after a thorough examination of the particularsituation.

Document Classification: KPMG Confidential

3© 2019 KPMG Zimbabwe is a partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Revenue measures Effective 01/08/19 every

reference in the Act to the“dollar” shall be construedto be a reference to theZimbabwean Dollar asdefined in StatutoryInstrument (SI) 142 of 2019.

Amendments to the 2%IMTT exemptions list.

Amendment toemployment tax rates.

Deductibility of miningroyalties effective 01/01/20.

Amendments of specifiedamounts in various taxprovisions.

Changes to rate of CapitalGains Tax and Capital GainsWithholding Tax.

A supplementary budgetwas presented, whichproposed to increasegovernment spending by140%, from ZW$7.7 billionto ZW$18.6 billion

Source: Mid Term Policy Statement

Currency reforms With effect from 24 June

2019, the Finance Act No. 2of 2019 abolished the multi-currency system fordomestic transactions. TheZimbabwe Dollar asintroduced by SI 142 of2019, becomes the solelegal tender for domestictransactions with a fewexceptions.

The Finance Act No. 2 of2019 authorises the RBZ toprint and issue bank notes,coins and electroniccurrency, subject toapproval by the Ministerthrough a StatutoryInstrument.

The RBZ Act was alsoamended to effect thechanges brought about bySI 33 and SI 142 of 2019.This was done byformalising the introductionof the ZW$, and theexchange rate of foreigncurrency on a willing buyerwilling seller basis.

Every enactment in US$, asat 22 February 2019 , is tobe construed to be ZW$ arate of 1:1.

Within 6 months from thegazetting of the Finance ActNo. 2 of 2019, the Ministerof Finance or Justice has toamend other Acts to effectchanges on fees, penaltiesor charges levied by thoseActs. The changes will takeeffect from the date thateach Act is amended, andthese changes should bereflected in ZimbabweDollars. However, fees,penalties or chargesindicated by specificprovisions of the relevantActs and payable by non-residents will be payable inforeign currency.

Consequently, the upwardrevision of government feesis expected.

7.7

18.6

ORIGINAL EXP.

REVISED EXP.

ZW$ Billion

Key Changes

Document Classification: KPMG Confidential

4© 2019 KPMG Zimbabwe is a partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

“Introduction of a flat rate of 5% Capital

Gain Tax on the gross selling price for specified assets

bought before 22 February 2019”

Capital Gains Tax For immovable property

acquired before 22 February2019 and disposed after thatdate, CGT will effectively becomputed on the grossproceeds at 5%.

Rate of CGT on the capitalgain remains at 20% forassets acquired after 22February 2019.

Effective 01 January 2019,sale of shares or othermarketable securities to theSovereign Wealth Fundshall be exempt from CGT.

Capital Gains Withholding Tax (CGWHT) CGWHT is charged at 5% of

the sales price forimmovable propertyacquired before 22 February2019, and 15% for propertyacquired after 22 February2019.

CGWHT for marketablesecurities is charged at 1%and 5% of the sales price,for listed and unlistedshares, respectively.

CGT payable in the currencyof the transaction.

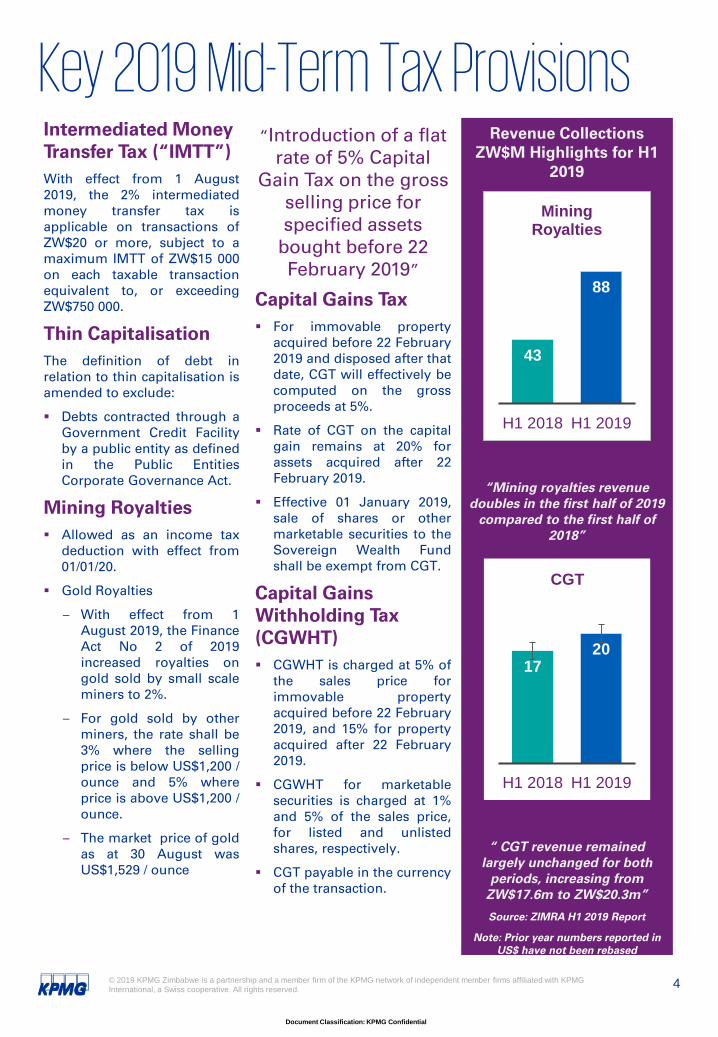

Revenue Collections ZW$M Highlights for H1

2019

“Mining royalties revenue doubles in the first half of 2019

compared to the first half of 2018”

“ CGT revenue remained largely unchanged for both

periods, increasing from ZW$17.6m to ZW$20.3m”

Source: ZIMRA H1 2019 Report

Note: Prior year numbers reported in US$ have not been rebased

43

88

H1 2018 H1 2019

Mining Royalties

1720

H1 2018 H1 2019

CGT

Intermediated Money Transfer Tax (“IMTT”)With effect from 1 August2019, the 2% intermediatedmoney transfer tax isapplicable on transactions ofZW$20 or more, subject to amaximum IMTT of ZW$15 000on each taxable transactionequivalent to, or exceedingZW$750 000.

Thin CapitalisationThe definition of debt inrelation to thin capitalisation isamended to exclude:

Debts contracted through aGovernment Credit Facilityby a public entity as definedin the Public EntitiesCorporate Governance Act.

Mining Royalties Allowed as an income tax

deduction with effect from01/01/20.

Gold Royalties

– With effect from 1August 2019, the FinanceAct No 2 of 2019increased royalties ongold sold by small scaleminers to 2%.

– For gold sold by otherminers, the rate shall be3% where the sellingprice is below US$1,200 /ounce and 5% whereprice is above US$1,200 /ounce.

– The market price of goldas at 30 August wasUS$1,529 / ounce

Key 2019 Mid-Term Tax Provisions

Document Classification: KPMG Confidential

5© 2019 KPMG Zimbabwe is a partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

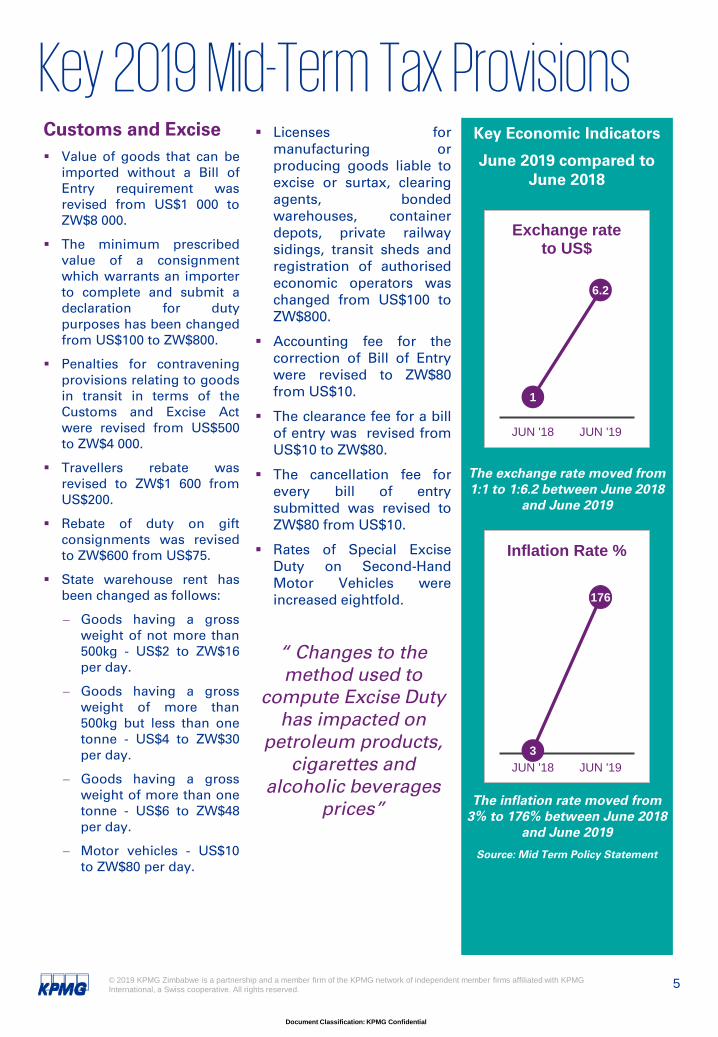

Licenses formanufacturing orproducing goods liable toexcise or surtax, clearingagents, bondedwarehouses, containerdepots, private railwaysidings, transit sheds andregistration of authorisedeconomic operators waschanged from US$100 toZW$800.

Accounting fee for thecorrection of Bill of Entrywere revised to ZW$80from US$10.

The clearance fee for a billof entry was revised fromUS$10 to ZW$80.

The cancellation fee forevery bill of entrysubmitted was revised toZW$80 from US$10.

Rates of Special ExciseDuty on Second-HandMotor Vehicles wereincreased eightfold.

“ Changes to the method used to

compute Excise Duty has impacted on

petroleum products, cigarettes and

alcoholic beverages prices”

Key Economic Indicators

June 2019 compared to June 2018

The exchange rate moved from 1:1 to 1:6.2 between June 2018

and June 2019

The inflation rate moved from 3% to 176% between June 2018

and June 2019

Source: Mid Term Policy Statement

Customs and Excise Value of goods that can be

imported without a Bill ofEntry requirement wasrevised from US$1 000 toZW$8 000.

The minimum prescribedvalue of a consignmentwhich warrants an importerto complete and submit adeclaration for dutypurposes has been changedfrom US$100 to ZW$800.

Penalties for contraveningprovisions relating to goodsin transit in terms of theCustoms and Excise Actwere revised from US$500to ZW$4 000.

Travellers rebate wasrevised to ZW$1 600 fromUS$200.

Rebate of duty on giftconsignments was revisedto ZW$600 from US$75.

State warehouse rent hasbeen changed as follows:

− Goods having a grossweight of not more than500kg - US$2 to ZW$16per day.

− Goods having a grossweight of more than500kg but less than onetonne - US$4 to ZW$30per day.

− Goods having a grossweight of more than onetonne - US$6 to ZW$48per day.

− Motor vehicles - US$10to ZW$80 per day.

Key 2019 Mid-Term Tax Provisions

3

176

JUN '18 JUN '19

Inflation Rate %

1

6.2

JUN '18 JUN '19

Exchange rate to US$

Document Classification: KPMG Confidential

6© 2019 KPMG Zimbabwe is a partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Pay As You Earn(“PAYE”)

Amendments ofemployment tax ratesseparating UnitedStates dollars andZimbabwe dollarearnings With effect from 1 August

2019, a new FDS year ofassessment starts, and endson 31 December 2019.Taxpayers will be requiredto submit two ITF16s for2019.

The adjacent tables presentthe amendment of taxableemployment income levelsfor the period beginning on1 August 2019, and endingon 31 December 2019.

Employees earningremuneration in foreigncurrency have to remitPAYE in that underlyingcurrency based on the taxtables denominated inUnited States currency. TheFinance Act No 2 of 2019did not prescribe the ratesapplicable for the USDPAYE tables. The tablespresented are based on theprovisions of the 2019Finance Act (No.2).

Employee Tax

Zimbabwean Dollar 2019 (1 August to 31 December) tax tables

RTGS$ RTGS$ RTGS$ % RTGS$

0 - 3 500 0% - -

3 501 - 15 000 20% of excess over 3 500

15 001 - 50 000 2 300 + 25% of excess over 15 000

50 001 - 100 000 11 050 + 30% of excess over 50 000

100 001 - 150 000 26 050 + 35% of excess over 100 000

150 001 - and over 43 550 + 45% of excess over 150 000

Zimbabwean dollar 2019 (1 January to 31 July) tax tables

RTGS$ RTGS$ RTGS$ % RTGS$

0 - 4 200 0% - -

4 201 - 18 000 20% of excess over 4 200

18 001 - 60 000 2 760 + 25% of excess over 18 000

60 001 - 120 000 13 260 + 30% of excess over 60 000

120 001 - 180 000 31 260 + 35% of excess over 120 000

180 001 - 240 000 52 260 + 40% of excess over 180 000

240 001 - and over 76 260 + 45% of excess over 240 000

United States Dollar 2019 (1 August to 31 December) tax tables

US$ US$ US$ % US$

0 - 350 0% - -

351 - 1 500 20% of excess over 350

1 501 - 5 000 230 + 25% of excess over 1 500

5 001 - 10 000 1 105 + 30% of excess over 5 000

10 001 - 15 000 2 605 + 35% of excess over 10 000

15 001 - and over 4 355 + 45% of excess over 15 000

Document Classification: KPMG Confidential

7© 2019 KPMG Zimbabwe is a partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

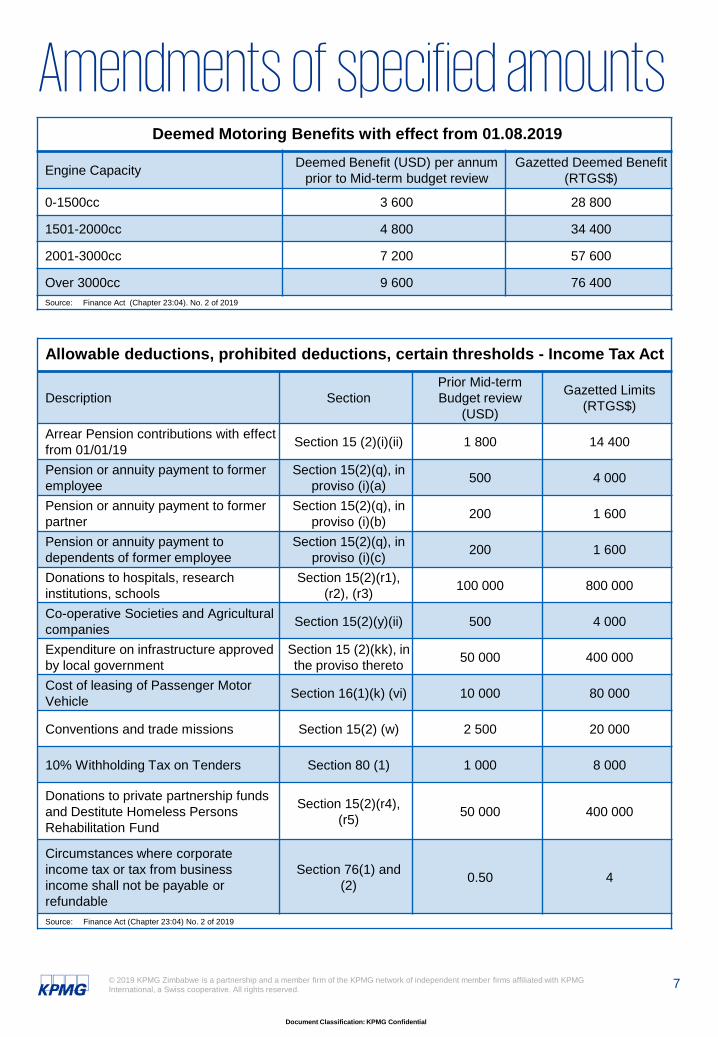

Amendments of specified amountsDeemed Motoring Benefits with effect from 01.08.2019

Engine Capacity Deemed Benefit (USD) per annum prior to Mid-term budget review

Gazetted Deemed Benefit (RTGS$)

0-1500cc 3 600 28 800

1501-2000cc 4 800 34 400

2001-3000cc 7 200 57 600

Over 3000cc 9 600 76 400Source: Finance Act (Chapter 23:04). No. 2 of 2019

Allowable deductions, prohibited deductions, certain thresholds - Income Tax Act

Description SectionPrior Mid-term Budget review

(USD)

Gazetted Limits (RTGS$)

Arrear Pension contributions with effect from 01/01/19 Section 15 (2)(i)(ii) 1 800 14 400

Pension or annuity payment to former employee

Section 15(2)(q), in proviso (i)(a) 500 4 000

Pension or annuity payment to former partner

Section 15(2)(q), in proviso (i)(b) 200 1 600

Pension or annuity payment to dependents of former employee

Section 15(2)(q), in proviso (i)(c) 200 1 600

Donations to hospitals, research institutions, schools

Section 15(2)(r1), (r2), (r3) 100 000 800 000

Co-operative Societies and Agricultural companies Section 15(2)(y)(ii) 500 4 000

Expenditure on infrastructure approved by local government

Section 15 (2)(kk), in the proviso thereto 50 000 400 000

Cost of leasing of Passenger Motor Vehicle Section 16(1)(k) (vi) 10 000 80 000

Conventions and trade missions Section 15(2) (w) 2 500 20 000

10% Withholding Tax on Tenders Section 80 (1) 1 000 8 000

Donations to private partnership funds and Destitute Homeless Persons Rehabilitation Fund

Section 15(2)(r4), (r5) 50 000 400 000

Circumstances where corporate income tax or tax from business income shall not be payable or refundable

Section 76(1) and (2) 0.50 4

Source: Finance Act (Chapter 23:04) No. 2 of 2019

Document Classification: KPMG Confidential

8© 2019 KPMG Zimbabwe is a partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Allowable deductions, prohibited deductions, certain thresholds - Income Tax Act

Description SectionPrior Mid-term Budget review

(USD)

Gazetted Limits (RTGS$)

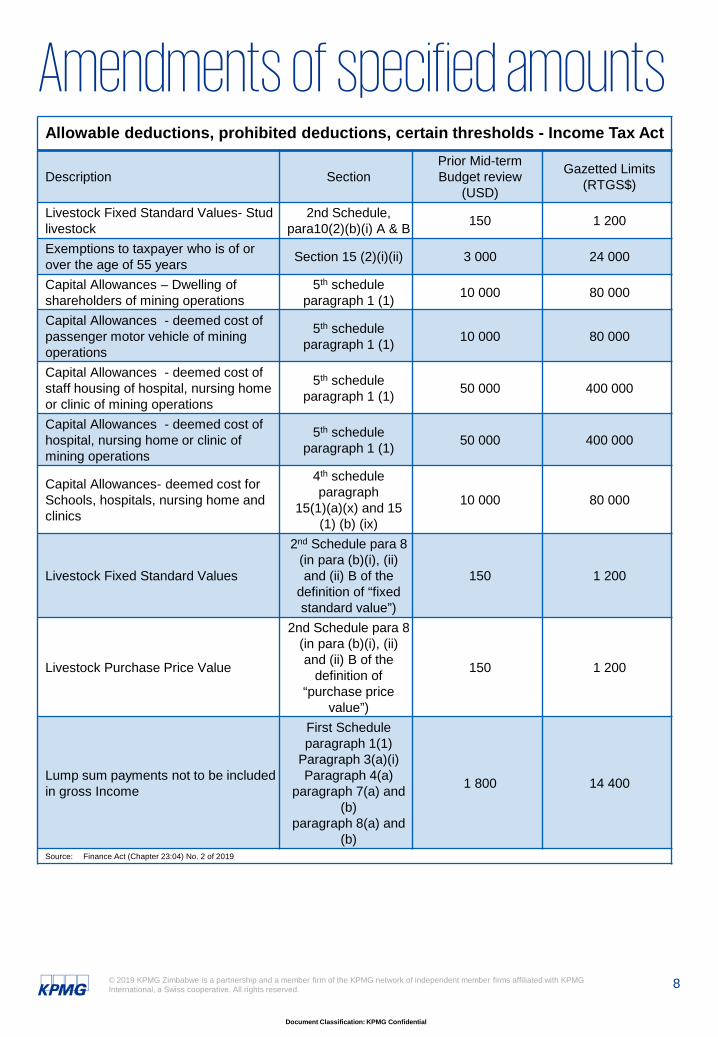

Livestock Fixed Standard Values- Stud livestock

2nd Schedule, para10(2)(b)(i) A & B 150 1 200

Exemptions to taxpayer who is of or over the age of 55 years Section 15 (2)(i)(ii) 3 000 24 000

Capital Allowances – Dwelling of shareholders of mining operations

5th schedule paragraph 1 (1) 10 000 80 000

Capital Allowances - deemed cost of passenger motor vehicle of mining operations

5th schedule paragraph 1 (1) 10 000 80 000

Capital Allowances - deemed cost of staff housing of hospital, nursing home or clinic of mining operations

5th schedule paragraph 1 (1) 50 000 400 000

Capital Allowances - deemed cost of hospital, nursing home or clinic of mining operations

5th schedule paragraph 1 (1) 50 000 400 000

Capital Allowances- deemed cost for Schools, hospitals, nursing home and clinics

4th schedule paragraph

15(1)(a)(x) and 15 (1) (b) (ix)

10 000 80 000

Livestock Fixed Standard Values

2nd Schedule para 8 (in para (b)(i), (ii) and (ii) B of the

definition of “fixed standard value”)

150 1 200

Livestock Purchase Price Value

2nd Schedule para 8 (in para (b)(i), (ii) and (ii) B of the

definition of “purchase price

value”)

150 1 200

Lump sum payments not to be included in gross Income

First Schedule paragraph 1(1)

Paragraph 3(a)(i) Paragraph 4(a)

paragraph 7(a) and (b)

paragraph 8(a) and (b)

1 800 14 400

Source: Finance Act (Chapter 23:04) No. 2 of 2019

Amendments of specified amounts

Document Classification: KPMG Confidential

9© 2019 KPMG Zimbabwe is a partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Allowable deductions, prohibited deductions, certain thresholds - Income Tax Act

Description SectionPrior Mid-term Budget review

(USD)

Gazetted Limits (RTGS$)

Deductions in respect of contributions to benefit and pension funds

6th Schedule, para 4 (b) 1 500 12 000

Deductions in respect of contributions to retirement annuity funds

6th Schedule, para 18 2 700 21 600

Capital Allowances - deemed cost of passenger motor vehicle of mining operations

5th schedule paragraph 1 (1) 10 000 80 000

Capital Allowances- deemed cost for renewal or replacement of buildings, works or equipment of mining operations

5th schedule paragraph 6 10 000 80 000

Capital Allowances- deemed cost for renewal or replacement of buildings, works or equipment of mining operations

5th schedule paragraph 6 proviso 1 500 12 000

Deductions in respect of contributions by employers to pension funds

6th Schedule, para 10 (b), para14 (a),

para 14 (b), para 15 (b), para 16 (b), para

17(2) (a)

5 400 43 200

Deductions in respect of contributions to employees to pension funds

6th Schedule, para 10 (b), para14 (a),

para 14 (b), para 15 (b), para 16 (b), para

17(2) (a)

5 400 43 200

Source: Finance Act (Chapter 23:04) No. 2 of 2019

Amendments of specified amounts

Document Classification: KPMG Confidential

10© 2019 KPMG Zimbabwe is a partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Allowable deductions, prohibited deductions, certain thresholds - Income Tax Act

Description SectionPrior Mid-term Budget review

(USD)

Gazetted Limits (RTGS$)

Exemption for shareholders above 55 years old for aggregated amount of any dividends and interests.

15th Schedule, paragraph 7(2)(a) Below 600 4 800

Exemption for shareholders above 55 years old for aggregated amount of any dividends and interests.

15th Schedule, paragraph 7(2) (b) 600 - 720 4800 - 5 760

Exemption for shareholders above 55 years old for aggregated amount of any dividends and interests.

15th Schedule, paragraph 7(2) (c) 720 - 840 5 760 - 6 720

Exemption for shareholders above 55 years old for aggregated amount of any dividends and interests.

15th Schedule, paragraph 7(2) (d) 840 - 960 6 720 - 7 680

Exemption for shareholders above 55 years old for aggregated amount of any dividends and interests.

15th Schedule, paragraph 7(3)(a); 480 3 840 - 6 720

Exemption for shareholders above 55 years old for aggregated amount of any dividends and interests.

15th Schedule, paragraph 7(3)(a);

(b); (c); (d)480 - 600 3 840 – 4 800

Exemption for shareholders above 55 years old for aggregated amount of any dividends and interests.

15th Schedule, paragraph 7(3)(a);

(b); (c); (d)600 – 720 4 800 – 5 860

Limitation of expenditure on employee’s housing incurred by petroleum operators

12th Schedule, paragraph 5(1)(vi) 720 - 800 5 860 - 6 720

Limitation of expenditure on a passenger motor vehicle incurred by petroleum operators

12th Schedule, paragraph 5(1) (f)

and (e)10 000 80 000

Limitation of deductions for any resident units incurred by a special mining lease

22nd paragraph 6 (2) (f) 25 000 400 000

Circumstances where employee tax shall not be payable or refundable

13th Schedule, paragraph

18(1)(a)(ii) and 18(1)(b

0.05 0.40

Source: Finance Act (Chapter 23:04) No. 2 of 2019

Amendments of specified amounts

Document Classification: KPMG Confidential

11© 2019 KPMG Zimbabwe is a partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Allowable deductions, prohibited deductions, certain thresholds - Income Tax Act

Description SectionPrior Mid-term Budget review

(USD)

Gazetted Limits (RTGS$)

Credit for taxpayers over 55 years Finance Act section 10 900 7 200

Credit for blind persons’ credit Finance Act section 11 900 7 200

Credit for mentally or physically disabled person

Finance Act section 13 900 7 200

Assessed losses full deduction threshold

CGT Act Section 2(1) 100 800

Sale of marketable security by a person above 55 years

CGT Act Section 10 (m) 1 800 14 400

Assessed loss not to be carried and taxable income not to be taxable

CGT Act Section (2) (h) 50 400

Limitation of expenditure on a passenger motor vehicle incurred by a special mining lease

22nd Schedule, paragraph 6(2)(g) 25 000 400 000

Limitation of deductions for any resident units incurred by a special mining lease

Section 15(2)(q), in proviso (i)(b) 10 000 80 000

Limitation of expenditure on a school, hospital employees resident units incurred by a special mining lease

Twenty-Second Schedule, paragraph

6(h)(ii)A IV10 000 80 000

Limitation of expenditure on a school, hospital , nursing home or nursing home or clinic incurred by a special mining lease

22nd Schedule, paragraph 6(b)(vii) 150 000 1 200 000

Trade threshold for definition of an informal trader.

26th Schedule, paragraph 1 (in

paragraph (a) of the definition of “informal

trader”)

6 000 48 000

Source: Finance Act (Chapter 23:04) No. of 2019

Amendments of specified amounts

2019 key tax provisions

Document Classification: KPMG Confidential

13© 2019 KPMG Zimbabwe is a partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Intermediated Money Transfer Tax (IMTT) Finance Act Number 1 of

2019 amended thecalculation of IMTT towhat is effectively referredto as the “2% tax”. IMTT isa tax levied on alltransactions mediated byfinancial institutions andmobile money operators.Tax is charged at 2% ofthe transaction value.

IMTT is a prohibiteddeduction for income taxpurposes based on theprovision introducedthrough the Finance ActNo. 1 of 2019.

Charitable institutions The receipts and accruals

of income from trade andinvestment not beingapplied in promoting theobjects of an ecclesiastical,charitable or educationalinstitution are taxable witheffect from 01/01/16,unless they meet therequirements and registerunder section 26 of theCompanies Act.

This is possible where anyprofits are applied to theobjects of the organisationwhich are considered to bein the interests of thepublic or any section ofthe public.

Introduction of local currency through SI 33 of 2019 Statutory Instrument 33 of

2019 introduced a localcurrency on 22 February2019, that is, the RTGSdollar. The instrumentdirected that all taxenactments previouslystated in US$ be translatedto RTGS$ at a rate of 1:1.

“All legal enactments quoted in USD are

now construed to be in RTGS$ at 1:1”

The rate used to translatedbalances previouslyreported in US$, includingcapital allowances willadversely impact the actualeffective tax rates ofbusinesses which will nowbe significantly greater thanthe general corporateincome tax rate of 25%

The accounting for legacydebts (blocked funds)expected to be addressedthrough the issuance ofinstruments from RBZ iscurrently being debated,and is likely to result inforeign exchange and fairvalue gains or losses whichwill be realised on actualsettlement / maturity of thelegacy debt and relatedinstruments from the RBZ.We expect the taxation ofsuch gains and losses to bedeferred to the time atwhich such gains or lossesare actually realised.

The RBZ is yet to announcethe specific terms in respectof settling legacy debts.

Corporate TaxDigital Tax The Finance Act No.1 of

2019 introduced thetaxation of non-residentsatellite broadcasters ande-commerce platformswhose Zimbabwean annualsales exceed US$500,000.

Gross sales are taxed at5%.

Payment of tax in underlying currency Section 4A(1) of the Finance

Act prescribes the paymentof tax in the currency inwhich transaction wasdone.

This implies payment of taxin foreign currency for alltax heads, includingcorporate income tax,where applicable.

Transfer Pricing S.I. 109 of 2019 was

gazetted on 10 May 2019.The instrument sets out thedocumentationrequirements for transferpricing as well as therequirement to make suchdocumentation availablewithin 7 days should ZIMRArequest it.

All eligible entities arerequired to submit transferpricing returns togetherwith annual Income taxreturns for the year ended31 December 2019.

Failure by taxpayers tocomply with theseRegulations will result inpenalties being levied.

It is pertinent for taxpayersto seek advice to facilitatetax compliance.

Document Classification: KPMG Confidential

14© 2019 KPMG Zimbabwe is a partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Customs and Excise

“Payment of duty in foreign currency for

specified goods including motor

vehicles”Excise duties are as follows effective 01/01/2019:

Cigarettes: increased fromUS$20 to US$25 per 1000sticks

Fuel: increased by 7 centsper litre for diesel andparaffin, and 6.5 cents perlitre for petrol

Vehicles Tourism Industry: Rebate of

duty on 75 new buses witha carrying capacity of 8 to55 passengers including thedriver.

Motor Industry: Rebate ofduty on the outstandingquota of buses extended byone year. A further onehundred 60-seater buses tobe imported at 5% customsduty.

Customs duty, import VATand surtax on importedmotor vehicles is payable inforeign currency with effectfrom 23/11/18, but thisexcludes commercialvehicles and vehicles forphysically disabled persons.

The payment of duties inforeign currency remains inplace for vehicles and otherluxury goods even after theenactment of S.I.142

Value Added Tax

Time of Supply The definition of the time of

supply of goods or serviceshas been extended to be theearlier of any one of thefollowing;

− Invoicing for the goodsor services; or

− Receipt of theconsideration (payment)for the goods orservices; or

− Removal of a moveablegood from the place ofsale; or

− At the point in time thatthe recipient takespossession of animmoveable property;or

− At he point in time thatthe service is performed

Imported Services The supply of imported

services has been extendedto include services suppliedto locally registered entitiesby foreign serviceproviders.

All businesses importingany type of service forconsumption in Zimbabweare now liable to pay 15%VAT.

VAT on imported services isnot claimable as input tax.

Value Added Tax, Customs & ExciseMajor Contributors of

H1 2019 Fiscal Performance

Source: ZIMRA H1 2019 Report

Note: Prior year numbers reported in US$ have not been

rebased

9

671

2018 2019

IMTT ($M)

451

1273

2018 2019

EXCISE ($M)

430

651

2018 2019

VAT ($M)

416

664

2018 2019

PAYE ($M)

Document Classification: KPMG Confidential

© 2019 KPMG Zimbabwe is a partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

kpmg.com/socialmedia kpmg.com/app

Contact Details

Vinay [email protected]+263 242 302 600+263 782 403 877

Steve [email protected]+263 242 303 700+263 772 240 537