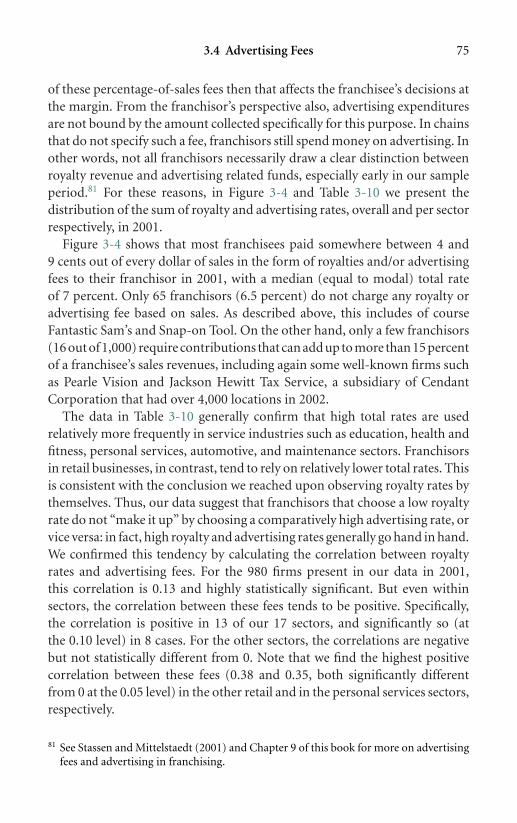

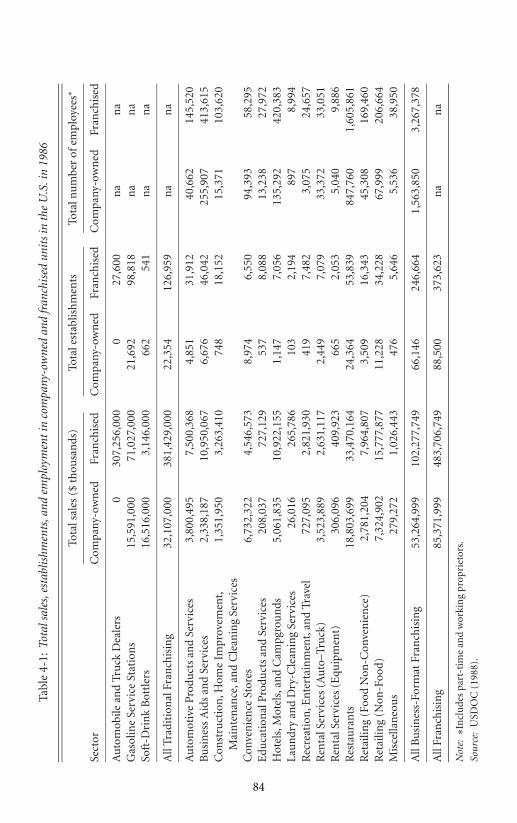

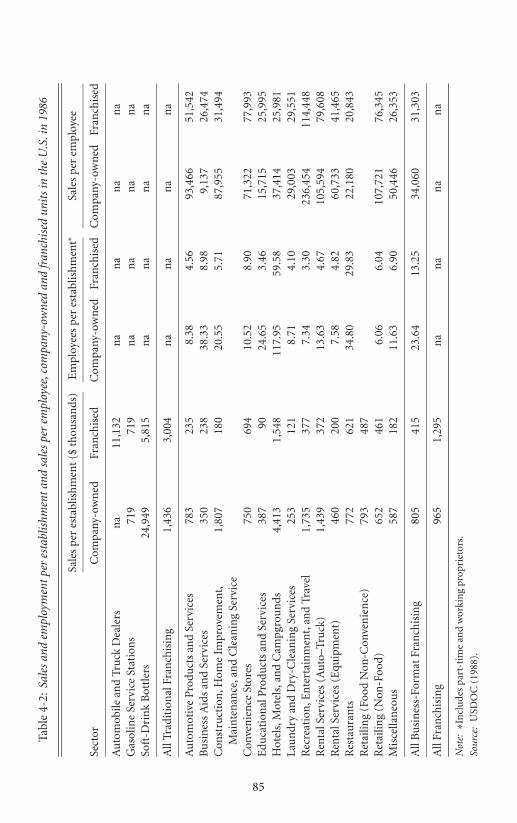

the_economics of franchise

TRANSCRIPT

P1: JZP0521772524agg.xml CB802/Blair 0 521 77252 4 April 29, 2005 22:11

ii

This page intentionally left blank

P1: JZP0521772524agg.xml CB802/Blair 0 521 77252 4 April 29, 2005 22:11

THE ECONOMICS OF FRANCHISING

This book describes in much detail both how and why franchising works. It alsoanalyzes the economic tensions that contribute to conflict in the franchisor–franchisee relationship. The treatment includes a great deal of empirical evidenceon franchising, its importance in various segments of the economy, the termsof franchise contracts, and what we know about how all of these have evolvedover time, especially in the U.S. market. A good many myths are dispelled in theprocess. The economic analysis of the franchisor–franchisee relationship beginswith the observation that for franchisors, franchising is a contractual alternative tovertical integration. Subsequently, the tensions that arise between a franchisor andits franchisees, who in fact are owners of independent businesses, are examined inturn. In particular, the authors discuss issues related to product quality control,tying arrangements, pricing, location and territories, advertising, and terminationand renewals.

Roger D. Blair is Huber Hurst Professor in the Department of Economics at theUniversity of Florida, where he has served on the faculty since 1970. He teachescourses in antitrust economics, law and economics, and the economics of sports.Professor Blair has published 165 articles, primarily in economics journals andlaw reviews, and has contributed numerous chapters to books. He has servedas an antitrust consultant to the U.S. Department of Justice; the Federal TradeCommission; the attorneys general of Arizona, California, Florida, Missouri,Oregon, and Washington; and numerous corporations. The books he has coau-thored include Antitrust Economics, Law and Economics of Vertical Integrationand Control, Monopsony: Antitrust Law and Economics, and forthcoming fromCambridge University Press, Intellectual Property: Economics and Legal Dimen-sions of Rights and Remedies, with Thomas F. Cotter.

Francine Lafontaine is Professor of Business Economics and Public Policy at theStephen M. Ross School of Business at the University of Michigan and Professorof Economics, Department of Economics, University of Michigan. Since joiningthe faculty at Michigan in 1991, Professor Lafontaine has primarily taught appliedmicroeconomics to MBA students, along with elective courses on firm strategyand antitrust and on the economics of franchising. She has published numer-ous scholarly articles on franchising in top journals in her field, including theJournal of Political Economy, the RAND Journal of Economics, the Journal of Lawand Economics, the Journal of Law, Economics and Organization, and the Journalof Industrial Economics, as well as in marketing and entrepreneurship journals.Professor Lafontaine is widely recognized as a world expert on the subject of fran-chising and, as such, has acted as consultant to various companies and FederalTrade Commission.

i

P1: JZP0521772524agg.xml CB802/Blair 0 521 77252 4 April 29, 2005 22:11

ii

P1: JZP0521772524agg.xml CB802/Blair 0 521 77252 4 April 29, 2005 22:11

The Economics of Franchising

ROGER D. BLAIRUniversity of Florida

FRANCINE LAFONTAINEUniversity of Michigan

iii

cambridge university pressCambridge, New York, Melbourne, Madrid, Cape Town, Singapore, São Paulo

Cambridge University PressThe Edinburgh Building, Cambridge cb2 2ru, UK

First published in print format

isbn-13 978-0-521-77252-5

isbn-13 978-0-521-77589-2

isbn-13 978-0-511-16065-3

© Roger D. Blair and Francine Lafontaine 2005

2005

Information on this title: www.cambridge.org/9780521772525

This publication is in copyright. Subject to statutory exception and to the provision ofrelevant collective licensing agreements, no reproduction of any part may take placewithout the written permission of Cambridge University Press.

isbn-10 0-511-16065-8

isbn-10 0-521-77252-4

isbn-10 0-521-77589-2

Cambridge University Press has no responsibility for the persistence or accuracy of urlsfor external or third-party internet websites referred to in this publication, and does notguarantee that any content on such websites is, or will remain, accurate or appropriate.

Published in the United States of America by Cambridge University Press, New York

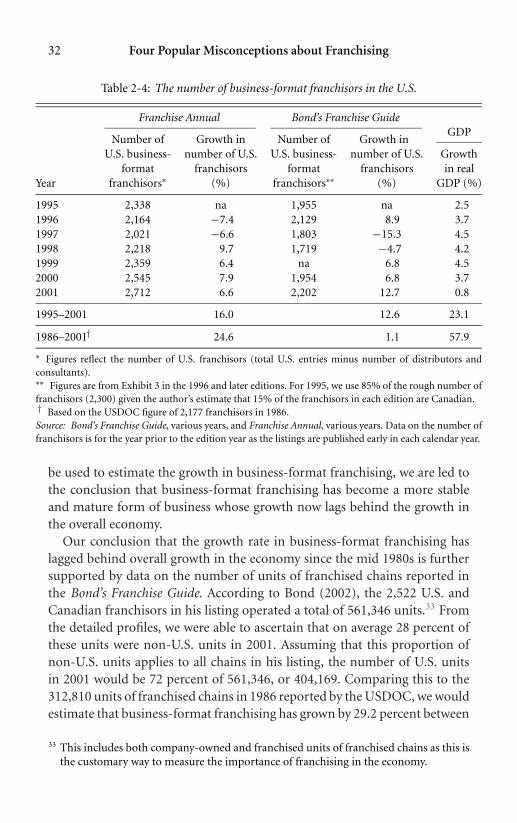

www.cambridge.org

hardback

paperback

paperback

eBook (EBL)

eBook (EBL)

hardback

P1: JZP0521772524agg.xml CB802/Blair 0 521 77252 4 April 29, 2005 22:11

To my parents, Jacques and Therese, who would have been proud,

and my family, Robert and Colette, for always being there for me.

To the memory of my parents, Duncan and Eleanor Blair,

who gave me so much.

v

P1: JZP0521772524agg.xml CB802/Blair 0 521 77252 4 April 29, 2005 22:11

vi

P1: JZP0521772524agg.xml CB802/Blair 0 521 77252 4 April 29, 2005 22:11

Contents

Preface page xi

1 Introduction 1

1.1 What Is a Franchise? 31.2 Traditional and Business-Format Franchising 51.3 In Which Industries Do We Find Franchising? 81.4 Plan of Study 18

2 Four Popular Misconceptions about Franchising 20

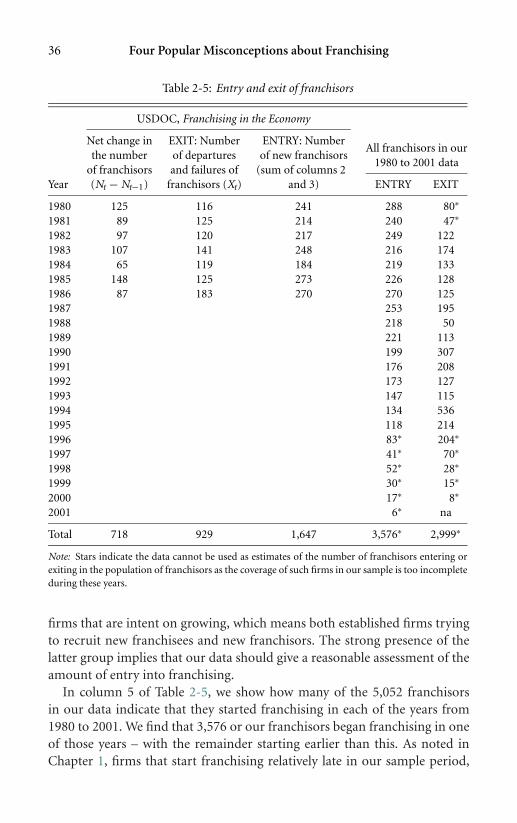

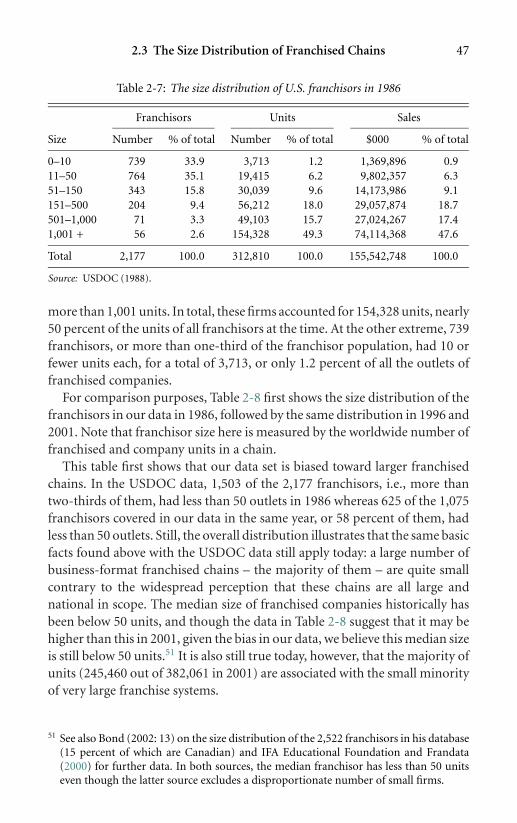

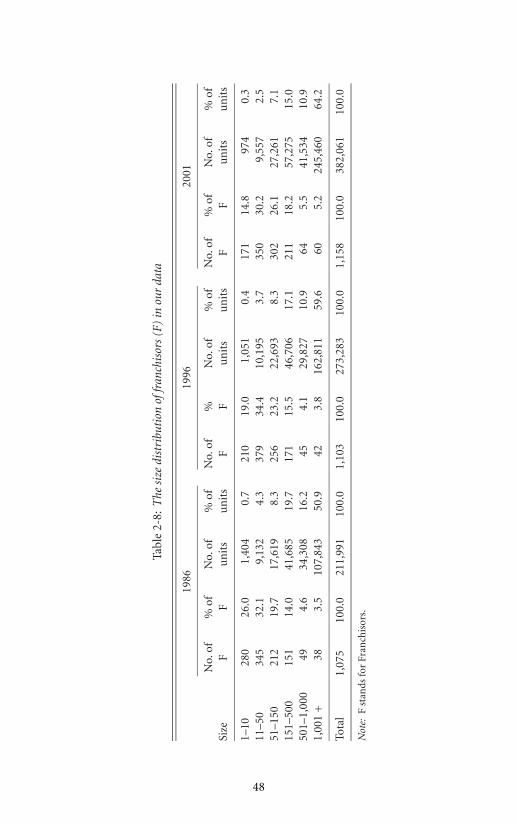

2.1 Growth: Fact and Fancy 212.2 Entry and Exit 342.3 The Size Distribution of Franchised Chains 462.4 Multi-Unit Franchisees 492.5 Conclusion 52

3 Franchise Contracts 54

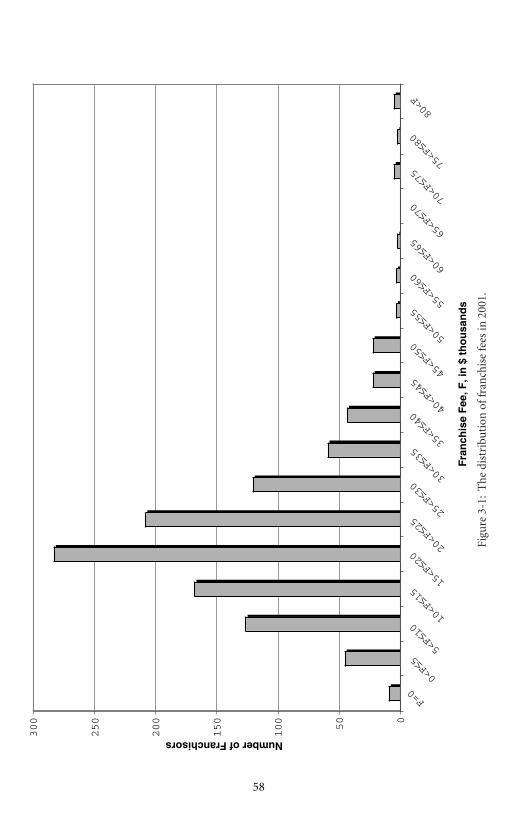

3.1 Introduction 543.2 Franchise Fees 563.3 Royalty Rates 623.4 Advertising Fees 693.5 Non-Monetary Contract Clauses 783.6 Some Final Thoughts and Comments 79

4 Franchising, Vertical Integration, and Vertical Restraints 82

4.1 Introduction 824.2 Dual Distribution or Partial Vertical Integration

in Franchising 834.3 Contractual Equivalents 944.4 Incentive Issues and Agency Theory 1074.5 Conclusion 116

vii

P1: JZP0521772524agg.xml CB802/Blair 0 521 77252 4 April 29, 2005 22:11

viii Contents

5 Quality Control 117

5.1 Introduction 1175.2 A Simple Model of Vertical Externalities 1215.3 Contractual Efforts to Resolve Incentive Problems 1255.4 Costs of Control 1335.5 Observed Quality Differentials between Company and

Franchised Units 1355.6 Conclusion 137

6 Franchise Tying Contracts 139

6.1 Introduction 1396.2 Antitrust Treatment of Tying Contracts in General 1426.3 Application to Franchise Tying Contracts 1446.4 The Kodak Decision and Its Progeny 1506.5 Franchise Tying Cases After Kodak 1526.6 Identifying Market Power After Kodak 1566.7 Post-Contractual Opportunism 1646.8 Evaluating Franchise Opportunities 1666.9 Conclusion 168

6.10 Appendix: Vertical Integration and Tying Contracts 168

7 Vertical Price Controls in Franchising 174

7.1 Introduction 1747.2 The Legal History of Maximum Resale Price Fixing

in the United States 1777.3 An Economic Analysis of Maximum Resale Price Restraints 1827.4 The Public Policy Implications of Khan 1967.5 Conclusion 1977.6 Appendix: Sales-Based Royalties and Demand Externalities 198

8 Encroachment 202

8.1 Introduction 2028.2 Market Coverage and “Traditional” Encroachment 2048.3 Industry Responses 2228.4 Non-Traditional Encroachment 2318.5 Conclusion 2338.6 Appendix: Carvel Corporation’s Contract: Before and After 234

9 Advertising and Promotion 236

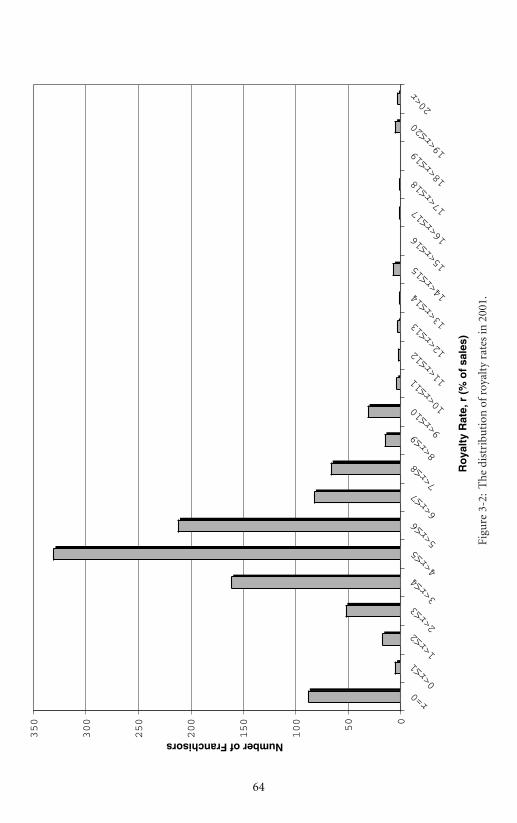

9.1 Introduction 2369.2 A Simple Model of Advertising as Information 2379.3 The Effect of Scale Economies 2449.4 Advertising as a Public Good in Franchised Chains 246

P1: JZP0521772524agg.xml CB802/Blair 0 521 77252 4 April 29, 2005 22:11

Contents ix

9.5 Advertising in Franchised Chains in Practice 2509.6 Franchisor–Franchisee Conflict 2539.7 Conclusion 257

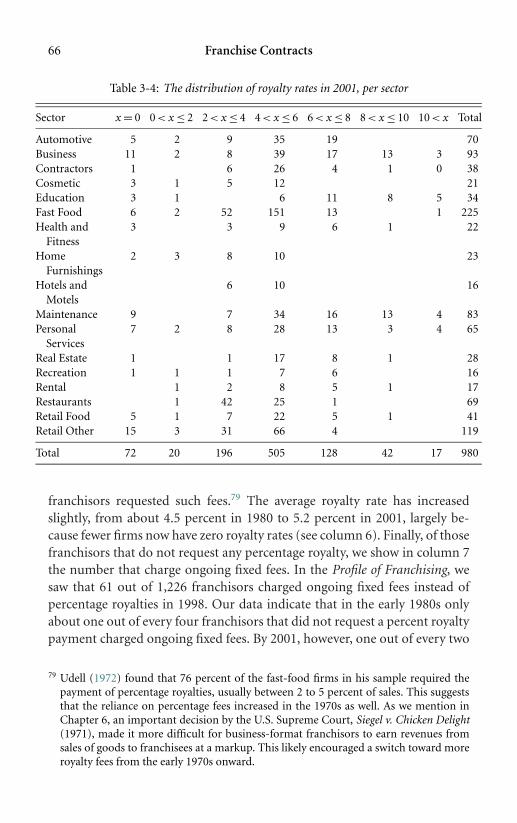

10 Termination and Non-Renewal 258

10.1 Introduction 25810.2 Franchise Contract Duration, Termination, and Renewal:

A Look at the Data 25910.3 The Role of Duration, Termination, and Non-Renewal

in Theory 26410.4 Termination and Non-Renewal: Legal Considerations 27510.5 Assessing Damages for Wrongful Termination 28010.6 Conclusion 290

11 Concluding Remarks 291

11.1 Introduction 29111.2 A Summary 29311.3 International Franchising 29711.4 The Future 29811.5 Conclusion 300

Articles, Books, and Other Publications 303

Cases, Codes, and Statutes 321

Index 325

P1: JZP0521772524agg.xml CB802/Blair 0 521 77252 4 April 29, 2005 22:11

x

P1: JZP0521772524agg.xml CB802/Blair 0 521 77252 4 April 29, 2005 22:11

Preface

Franchising has become a very visible part of the economic landscape in theUnited States. Its role in distributing products to customers in the rest ofthe world has also grown considerably over the last several decades. In thisbook, we describe what franchising is and how it works. In most situations,franchising works very well for franchisors, franchisees, and consumers alike,which is why it has grown to the extent that it has. Because it works well mostof the time, we expect that franchising will continue to flourish in the worldeconomy. At the same time, however, we know from economic principles thatfranchise relationships are by their very nature fraught with many difficultiesarising essentially from differences between the needs and goals of the fran-chisors and those of the franchisees. Economists and management researchershave made significant progress in the last twenty or so years toward increasingour understanding of the sources of these problems. We highlight much oftheir work in this book.

We had many goals in writing this book. First, from a managerial perspec-tive, we hope that an improved understanding of the basic sources of frictionin franchise relationships will allow franchisors and franchisees alike to de-velop better ways of dealing with each other’s concerns, either through thefranchise contract itself or through other means of their choosing. Second,from a public policy perspective, we hope that jurisdictions considering var-ious forms of regulation and control of franchise relationships will be betterable to assess the validity and merit of the claims made by interested parties,and thus the cost and benefit of various forms of intervention. In particular,we explore the not-so-obvious consequences of many types of public policies.Finally, from an academic perspective, we want to provide researchers with aclearer understanding of franchising as an institutional framework. By doingso, we hope to foster more interest in the study of franchising itself and ofcontracts and organizations more generally.

xi

P1: JZP0521772524agg.xml CB802/Blair 0 521 77252 4 April 29, 2005 22:11

xii Preface

For past and continuing collaboration, we thank our colleagues, SugatoBhattacharyya, Amanda K. Esquibel, James Fesmire, Jill Boylston Herndon,Arturs Kalnins, David L. Kaserman, Patrick J. Kaufmann, Scott E. Masten,Emmanuel Raynaud, Richard E. Romano, Kathryn L. Shaw, and MargaretE. Slade. We also thank Robert Picard for his expert data management andassistance throughout this project. We are also grateful to Anne Parmigiani forher careful proofing of the manuscript and to Colette Picard for proofing thetables. Our editor at Cambridge University Press, Scott Parris, also deserves aspecial thanks for his patience and continuing encouragement. Finally, we aregrateful to the National Science Foundation (NSF), under grant SBR-9312083,and our respective institutions for their support.

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

1

Introduction

Franchising has become a part of everyday life for most consumers in theUnited States today – it is everywhere. Numerous firms in a variety of in-dustries have adopted franchising as a method of doing business. As a re-sult, consumers now often purchase meals and hotel services along withcar repairs, clothing, specialty foods, and many other types of goods andservices through franchised companies. Why have so many firms involvedin such different activities all chosen to organize themselves as franchisedcompanies? We know that a combination of factors makes franchising desir-able. On the one hand, the increased reliance of consumers on brand names,due in part to increased consumer mobility and greater time constraints,has played an important role in the development of retail and other chains.1

In addition, chains can benefit from lower costs through bulk purchasingprograms and by realizing economies of scale in production, new productdevelopment, and advertising. These benefits, however, really explain whychains have become more prevalent in the economy, not why franchisinghas become so ubiquitous. After all, the stores in these chains could all becorporately owned, as is the case in many chains. Why then do we see somany other chains organized as franchises? The answer apparently lies inthe capacity of franchising to combine the chain’s comparative advantagesin creating brand recognition and capturing economies of scale with the

1 The increased time constraints, in turn, can be traced to the increased participationof women in the labor force, and the resulting “out-sourcing” by households, as wellas the increasing complexity of products available for consumption. The result is thathouseholds must now make a greater number of more complex consumption decisions.Known brands that reduce uncertainty and thus save time become particularly valuableto customers in this context. Moreover, the cost of creating and maintaining nationalor internationally known brands has gone down dramatically over time.

1

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

2 Introduction

local entrepreneur’s local knowledge and drive.2 In other words, in the idealfranchise relationship, each party is able to specialize in what each does bestand yet benefit from the efforts of the other. In fact, as we will see in moredetail later, most franchise contracts are written such that both parties sharein the sales revenues of the franchised outlet. The contract thus ensures thatboth parties have incentives to put forth effort to increase those revenues.Such joint incentives are more difficult to achieve in a corporate environmentand therein lies the main long-term advantage of franchising over corporateorganization.

The capacity of franchising contracts to harness the effort of a central en-tity, the franchisor, and of a number of local entrepreneurs, the franchisees,explains in our view much of its current prevalence and popularity as a way oforganizing certain economic activities. In particular, franchising is well suitedto retailing and service businesses as firms in these sectors need to establish alarge number of geographically dispersed outlets to reach customers. In thatcontext, both suppliers of franchises, namely the firms who organize them-selves as franchised chains, and the demanders of franchises, that is thoseindividuals eager to develop a small local business, benefit from the intercon-nection that franchising affords them. Franchisors and their franchisees thuscooperate with one another in a kind of partnership. In many regards, theinterests of the franchisor and its franchisees are mutually compatible. Theircooperation increases value for both parties: both earn more profit than theywould absent this cooperation.

In an economic sense, we know that franchising must be efficient as anorganizational form since it continues to thrive in competition with other or-ganizational structures.3 In this book, we summarize much of what is knownabout the economics of franchising. We examine the economic principles thathelp explain its popularity as a method of distribution, but also highlight howeconomic principles can shed light on many ways in which franchisor andfranchisee needs diverge. These divergent interests create conflict between thefranchisor and its franchisees, conflict that undermines the value that coop-eration creates. For continued success, this conflict must be minimized. Webelieve that clearly laying out the sources of conflict is a good first step towardthat goal. We therefore devote a substantial portion of this book to the analysisof conflict in franchising. We also devote significant attention to describing

2 Caves and Murphy (1976) first made this point and developed the argument.3 This follows from the survivor principle. For more on this principle and its origins, see

Stigler (1968).

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

1.1 What Is a Franchise? 3

franchising and analyzing how it works. In the process, we report data onvarious aspects of the franchise relationship wherever available and relevant,complementing existing data with new empirical information we derive froma data set on U.S. franchisors that we have built over time from directories.Because our data and our knowledge of applicable law are particular to U.S.franchising, much of our discussion is focused on the way franchising worksin this country. This, however, is not as much of a shortcoming as one mightsuppose. First, we present non-U.S. information whenever we can. More im-portantly, the general economic principles that we highlight are relevant in allcountries and, as will be clear from available data, franchising practices do notdiffer markedly between countries. Thus, our hope is that the content of thisbook will prove relevant to anyone with an interest in franchising regardlessof where he or she lives and works.

Before launching into an economic analysis of franchising as an orga-nizational form, we explore a few basics to frame our subsequent analy-sis. We begin by defining the franchise relationship, distinguishing betweentraditional and business-format franchising, and identifying the locus andextent of franchising in the U.S. economy. We then describe our data onfranchisors, data that we rely on throughout the book. We conclude thisintroductory chapter by laying out a road map for the remainder of the book.

1.1 What Is a Franchise?

According to the American Heritage Dictionary of the English Language, theword franchise comes from the old French word franche, which means freeor exempt. In medieval times, a franchise was a right or privilege granted bya sovereign power – king, church, or local government. Sovereigns grantedfranchises for various activities, such as building roads, holding fairs, orga-nizing markets, or for the right to maintain civil order and collect taxes. Inessence, the sovereign gave an individual or group of individuals the monopolyrights over a particular activity in a particular location for a certain periodof time. In most cases, the grantee was required to make a payment to thesovereign power for this right or privilege, usually in the form of a share ofthe product or profit. That payment was called a royalty, a term still in use tothis day.

Today, a franchise agreement is most often understood as a contractualarrangement between two legally independent firms in which one firm, thefranchisee, pays the other firm, the franchisor, for the right to sell the fran-chisor’s product and/or the right to use its trademarks and business format

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

4 Introduction

in a given location for a specified period of time. But this use of the termfranchising in the English language only goes back to the late 1950s: accord-ing to Dicke (1992: 2), the word franchise – understood as a method of doingbusiness or distributing goods and services – entered the English businesslexicon in 1959. Moreover, governments still grant franchises in certain in-dustries. This occurs, for example, in the cable TV industry in the UnitedStates where the rights to be the sole provider of cable services in a givenmarket for a certain time period are sold by local governments to firms usu-ally through what is called a “franchise bidding” process.4 In addition, theword franchise is used in the sports industry to refer to the right to operatea team in a particular locale.5 In this book, however, we focus on the type offranchising that represents an ongoing business relationship between legallyindependent commercial firms, and accordingly we use the term to meanonly such arrangements.

According to the Federal Trade Commission (FTC), the body that has ju-risdiction in the United States over federal disclosure rules for franchisors,three elements must be present for a business relationship to be deemed afranchise.6 First, the franchisor must license a trade name and trademark thatthe franchisee operates under, or the franchisee must sell products or servicesidentified by this trademark. Second, the franchisor must exert significantcontrol over the operation of the franchisee or provide significant assistance tothe franchisee. Third, the franchisee must pay at least $500 to the franchisor atany time before or within the first six months of operation.7 Note that thoughthis definition of franchising is specific to the U.S., most definitions used byauthorities outside of the U.S., including Australia, Canada, and the European

4 For more on “franchise bidding” in the U.S. cable industry, see for example Zupan(1989a, 1989b) and Prager (1990) and the references therein. For an analysis of contem-porary highway construction franchise contracts granted by a government, see Engelet al. (2001).

5 For examples of this use of the term franchise, see Noll and Zimbalist (1997) and thehistory of the NFL at http://www.football.com/history/index.shtml.

6 For a detailed account of different definitions of commercial franchises used in theacademic literature across a variety of fields, see Stanworth and Curran (1999). For areview of the legal elements of franchises as per the text of various state franchise laws,see for example Pitegoff (1989).

7 See Federal Trade Commission (1979). See http://www.ftc.gov/bcp/franchise/netrule.htm for a guide to this rule. Note that in its interpretive guide, the FTC specifiesthat payments for inventory at bona fide wholesale prices for resale are not considereda “minimum payment” for the purposes of this last requirement. See Final InterpretiveGuides, 44 Fed. Reg. at 49967.

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

1.2 Traditional and Business-Format Franchising 5

Union (EU), rely on a similar set of criteria.8 In their implementation, how-ever, foreign definitions are often less inclusive. We come back to this brieflybelow.

1.2 Traditional and Business-Format Franchising

In the U.S., the Department of Commerce (USDOC) historically has distin-guished two separate types of franchised relationships: traditional (or productand trade name) franchising and business-format franchising. The formeris characterized by franchised dealers who “concentrate on one company’sproduct line and to some extent identify their business with that company”(USDOC 1988: 1). Thus, the Ford dealer, for example, is identified as a dis-tributor of Ford automobiles. As the name suggests, traditional franchisingis the oldest form of modern franchising. By most accounts, it can be tracedback in the U.S. at least to the mid-1800s when the McCormick Harvest-ing Machine Company and the Singer Sewing Machines Company sold theirproducts through sales agents who were given exclusive sales territories.9 Ini-tially, these firms, like others who used such agents at the time, imposed fewrestrictions or qualifications on their agents and exerted very little control overthem. Over time, however, both companies found they needed more controlover these sales agents if they were to protect their respective reputationsand brands. The McCormick Company responded by establishing company-owned branch houses throughout the U.S. and Canada. These branch houseswere given oversight responsibilities for the sales agents in their territories.As a result, McCormick was able to systematize procedures and communica-tions with its agents, thereby transforming them into what one would nowcall “dealers.” As for the Singer Company, it addressed the need for controlby converting many of the independent agencies into company outlets. Moreimportantly, it devised a series of recommendations for the remaining agentsas to how the offices should be run and, for the first time, required detailed

8 See the Franchising Code of Conduct, Commonwealth of Australia, 1998; the ArthurWishart Act in Ontario, Canada; and the EEC Block Exemption for Vertical Restraints. Notethat a definition of franchising is no longer included directly in the EEC Block Exemptionfor Vertical Restraints, but a description of the contents of franchise agreements is foundin the attached guidelines (text fig. 35, 36, 189ff.) and the know-how definition hasremained the same as in the old EEC Block Exemption for Franchise Agreements.

9 See Dicke (1992) on the history of franchising in the United States, including a de-tailed account of its evolution at these two companies. See also Marx (1985) on thedevelopment of franchising in automobile retailing in the U.S.

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

6 Introduction

financial reporting from these agents. The contracts and methods of controlthat Singer developed at the time are largely recognized as the forerunners ofthe modern franchise agreement.10

Traditional franchising today is comprised largely of automobile dealer-ships, gasoline service stations, and soft-drink bottlers.11 In all of these busi-nesses, the franchisor is a manufacturer who sells finished or semi-finishedproducts to its dealers/franchisees. In turn, the franchisees resell these prod-ucts to consumers or other firms in the distribution chain. Because the fran-chisor’s product is sold to its franchisees, the franchisor’s profits from itsdealer network flow from the markups it earns on these products. In contrastto what occurs in business-format franchising, as described below, traditionalfranchisees do not pay running royalties on their sales.

Traditional franchising accounted for 72.7 percent of all sales by fran-chised chains in 1986, the last year in which the U.S. government collectedand published statistics on franchising.12 The remaining 27.3 percent of allfranchised sales were generated by business-format franchising firms in whichthe franchisor primarily sells a way of doing business (i.e., a business format)to its franchisees. A business-format franchise thus “includes not only theproduct, service, and trademark, but the entire business format itself – amarketing strategy and plan, operating manuals and standards, quality con-trol, and continuing two-way communication” (USDOC 1988: 3).

The first true business-format franchise system was created by MarthaMathilda Harper (Plitt 2000). This entrepreneur developed her network ofHarper Beauty Shops from the early 1890s onward using a business model

10 In England, the development of franchising is usually traced back to the developmentof the “tied house system,” namely the ownership of licensed beer retailers by brewers.See especially Knox (1958) on the reasons behind the growth of this system in London.

11 William E. Metzger is said to have been the first franchisee in automotive retailing; heobtained a franchise to sell steam automobiles from General Motors Corporation in1898 (Justis and Judd 1998: 1–9). Coca-Cola sold its first bottling franchise in 1899.

12 The USDOC cancelled its publication of Franchising in the Economy in 1988 as part ofits privatization program. This publication was the only source of Census-type data onfranchising in the United States. Efforts by the International Franchise Association (IFA)to take over the publication of this annual report on a permanent basis were unsuccessful.However, in cooperation with Frandata Inc., the IFA Educational Foundation recentlyproduced The Profile of Franchising, Volumes I, II, and III. These profiles report summarydata per sector based on information contained in the disclosure documents of allfranchisors that had to file such documents in at least one of the twelve filing U.S. states.Though the resulting set of franchisors covered in the profiles is not the whole populationof franchisors in the U.S., these publications provide some very useful information thatwe rely on when appropriate in the remainder of this book.

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

1.2 Traditional and Business-Format Franchising 7

that included all of the components of a business format as described by theUSDOC, and more. But though she grew her network to more than 500 shopsin the U.S., Canada, and Europe by the mid-1920s, Mathilda Harper unfor-tunately did not leave a lasting mark on franchising. Other firms, such asthe supermarket chain Piggly Wiggly, Hertz Car Rentals, IGA (IndependentGrocers Association), A&W Restaurants, Ben Franklin Retailers, Maid Rite(a hamburger restaurant chain), and Terminix Termite and Pest Control allstarted franchising in the 1920s and are still franchising today. According to theFrench Franchise Federation, Jean Prouvost, owner of the Lainiere de Roubais,launched his network of Pingouin stores also in the 1920s, thereby initiat-ing the concept of franchised distribution in France.13 These early entrantswere followed in the 1930s by companies like Howard Johnson Restaurants,Stewart’s Drive-In, Arthur Murray Schools of Dancing, and Culligan in theU.S., and by the Canadian Tire retail chain and its Associate Store program,Merle Norman Cosmetics, and Le Groupe RONA among others in Canada.14

But it was not until the 1950s, with the advent of chains such as Burger Kingand McDonald’s, and the economic boom of the post–World War II era, thatbusiness-format franchising fully came into its own in the U.S. and Canada,and, even more recently, throughout much of the rest of the world.15

Business-format franchising today encompasses a very large number offirms that provide a wide array of goods and services: automotive productsand services, computer sales, business aids and services, construction andmaintenance, legal, domestic, and childcare services, and non-food retail-ing as well as the more visible hotel, fast-food, and car rental franchises.In exchange for the business format, franchisees typically pay a relativelysmall lump-sum fixed fee at the beginning of the contract period and payrunning royalties that are usually calculated as a fixed percentage of the

13 See Federation Francaise de la Franchise (2003: 12). Though this source indicatesthat the network of stores was developed in the 1930s, the French National Archivesstates that it was started in 1923. See http://www.archivesnationales.culture.gouv.fr/camt/fr/egf/lettrel.html.

14 Some networks, such as IGA, le Groupe RONA, and Best Western International, areorganized as cooperatives whose role it is to provide their franchisees (members) withpurchasing power and name recognition. The development and organization of thesecooperatives is interesting in light of Caves and Murphy’s (1976: 576) view of franchisingas a mechanism by which “franchisees hire out the collective and large-scale productionof goodwill.” See also Lafontaine and Raynaud (2002) for an analysis that draws ananalogy between food production cooperatives and franchises.

15 See Arthur Andersen & Co. (1995) for an overview of the number of franchisors andfranchisees in 36 countries around the world.

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

8 Introduction

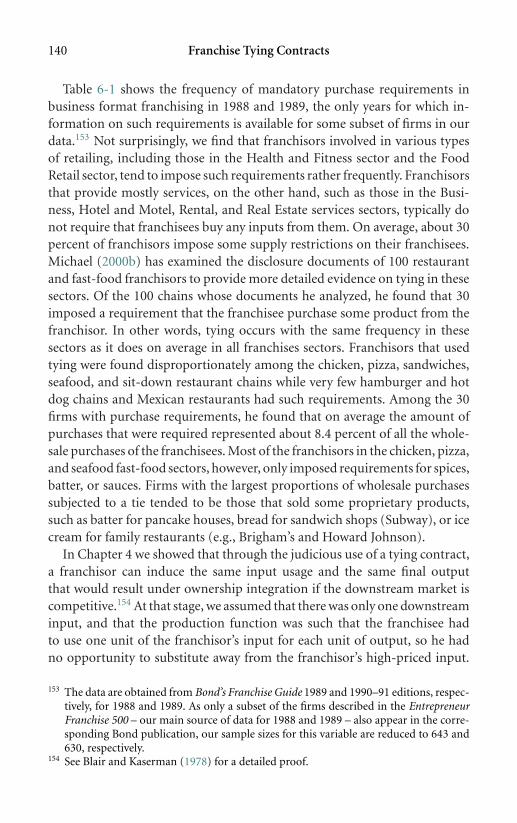

franchisee’s sales revenues.16 Business-format franchisees also often con-tribute an additional fraction of their sales or revenues toward an adver-tising fund for the chain as a whole. Presumably, the advertising carried outwith these funds benefits all franchisees and thereby benefits the franchisoras well.

In the end, the distinction between traditional and business-format fran-chising is somewhat arbitrary and basically a matter of degree. Dnes (1992a)and Klein (1995), for example, both argue that there is little economic differ-ence between the two, in terms of either the type of agreements they rely onor the type of support provided or control exerted by franchisors. And whenit comes to theoretical analyses of franchise relationships, the distinction be-tween these two types of franchising indeed is largely irrelevant: researchershave considered both types simultaneously in many studies. But while intheory the distinction may not be so meaningful, it is important from a de-scriptive standpoint for two main reasons. First, in many countries outsidethe U.S., traditional franchising is not included in franchising statistics. As aresult, the franchising sector appears artificially large in the U.S. relative tothese other countries. Second, in the U.S., authors often refer to all franchis-ing when they emphasize its economic importance: after all, sales of goodsand services through traditional and business-format franchising togetheramounted to almost 13 percent of real gross domestic product (GDP) (seeChapter 2), or 34 percent of retail sales, in 1986 according to the USDOC(1988: 14). When presenting data about the growth in franchising in the U.S.,however, the data more often measure business-format franchising only. Thisis because business-format franchising has grown much faster than traditionalfranchising over the last few decades. Thus, the separation of franchising intotwo different types has allowed the trade press to mostly emphasize those fran-chising figures that show franchising in its most favorable light. We return tothe issue of franchising growth in the next chapter.

1.3 In Which Industries Do We Find Franchising?

As noted by the USDOC (1988: 14), “[r]etailing dominates franchising, ac-counting for 87 percent of all franchising receipts in 1987. The retail salesof all firms associated with franchising reached about $522 billion in 1987,

16 There are exceptions to royalties calculated as a percentage of total revenue. These includeminimum payment provisions, increasing and decreasing scales, and royalties definedas a percentage of profits. These alternatives, however, are observed far less frequentlythan constant rate sales revenue royalties. See Chapter 3 for details.

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

1.3 In Which Industries Do We Find Franchising? 9

or 34 percent of all U.S. retail sales, which are estimated at $1.5 trillion.”17

Table 1-1 shows the sectoral breakdown for sales, the number of establish-ments, and employment for franchised firms in the U.S. in 1986 as per theUSDOC (1988). It also shows average sales per establishment in each sector.

Table 1-1 first confirms that sales through traditional franchising are al-most three times the level of sales of business-format franchisors. In contrast,the bulk of the establishments and employment are in business-format fran-chising. The number of establishments is twice as large and the number ofemployees is almost three times larger in business-format than in traditionalfranchising. This implies that sales per unit and sales per employee are muchlarger in traditional than in business-format franchising. This is shown in thelast column of Table 1-1, in which sales per establishment for car dealershipsand soft-drink bottlers completely overwhelm those of gasoline stations aswell as those of every type of business-format franchise. While the govern-ment data above all pertain to 1986, a recent report on the economic impactof franchising in the U.S. economy suggests that business-format franchisingin 2001 encompassed 4.3 times as many establishments and employed fourtimes as many workers as traditional franchising did.18

Table 1-1 also illustrates that franchising occurs in a wide variety of retailand service industries in the U.S. economy. Within business-format fran-chising, the bulk of sales, units, and employees in 1986 were found in therestaurant sector, which includes such well-known chains as Burger King,KFC, Little Caesar’s, McDonald’s, and Subway, among many others. The nextlargest sector from a sales perspective was the non-food retailing sector, whichincludes chains such as The Athlete’s Foot, The Body Shop, Decorating Den,and General Nutrition Centers. From an establishment and an employmentperspective, however, the second largest business-format franchising sectorwas the business aids and services sectors, with firms such as Money Mailer,SignFast, and Snelling Personnel Services.

The data in Table 1-1, however, reflect the sector distribution of franchisingactivities as it existed in 1986. Unfortunately, since Franchising in the Economyis no longer published by the U.S. government, updated figures correspondingto those in Table 1-1 are unavailable. This lack of data has made it quite difficult

17 Retail sales in the U.S. reached $3.5 trillion in nominal terms in 2001 (U.S. CensusBureau, “Monthly Retail Trade Survey,” Historical Retail Trade Data). Assuming thatthe proportion of retail trade accounted for by franchised companies has remained atabout one-third of all retailing, franchising would now account for more than $1 trillionin retail business in the U.S. (in 2001 dollars). We address the issue of franchising growthin Chapter 2.

18 See IFA Educational Foundation and Price Waterhouse Coopers, 2004.

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

10 Introduction

Table 1-1: Sales, establishments, and employment in franchising in the U.S. in 1986

Sales perSales Number of Number of establishment

Sector ($ thousands) establishments employees∗ ($ thousands)

Automobile and Truck Dealers 307,256,000 27,600 947,400 11,132Gasoline Service Stations 86,618,000 120,510 596,400 719Soft-Drink Bottlers 19,662,000 1,203 126,200 16,344

All Traditional Franchising 413,536,000 149,313 1,670,000 2,770

Automotive Products and Servicesa 11,300,863 36,763 186,182 307Business Aids and Servicesb 13,288,254 52,718 669,522 252Construction, Home 4,615,360 18,900 118,991 244

Improvement, Maintenance,and Cleaning Servicesc

Convenience Stores 11,278,895 15,524 152,688 726Educational Products and Servicesd 935,166 8,625 41,210 108Hotels, Motels, and Campgrounds 15,983,990 8,203 555,674 1,949Laundry and Drycleaning Services 291,802 2,297 9,891 127Recreation, Entertainment, 3,549,025 7,901 27,732 449

and Travele

Rental Services (Auto–Truck) f 6,155,006 9,528 66,423 646Rental Services (Equipment)g 716,019 2,718 14,926 263Restaurants 52,273,863 78,203 2,453,621 668Retailing (Food 10,746,011 19,852 214,768 541

Non-Convenience)h

Retailing (Non-Food)i 23,102,779 45,456 274,663 508Miscellaneous j 1,305,715 6,122 44,486 213

All Business-Format Franchising 155,542,748 312,810 4,830,777 497

Total Franchising 569,078,748 462,123 6,500,777 1,231

Note: ∗ Includes part-time and working proprietors.a Includes Tire, Battery, and Accessory Stores; Auto and Truck Wash Services; Brake and Muffler Repair and

Services; and some establishments with significant sales of non-automotive products such as HouseholdAppliances, Garden Supplies, and others.

b Includes Computer Services, Business Consultants and Brokers, Security, Dentists, Insurance, and Others.c Includes Furniture Repairs, Water Conditioning, Lawn Care, Sewer Cleaning, and Carpet Cleaning.d Includes Day-Care Centers and Health and Diet Services.e Includes Travel Agencies, Miniature Golf Courses, and Dance Studios.f Includes Leasing.g Includes Formal Wear.h Includes Retail Specialty Food Shops, Donut Shops, Ice Cream Stores, Coffee Services, Candy Stores,

Bakeries and Supermarkets.i Includes General Merchandise, Drugs and Cosmetics, Gift Shops, Shoes and Apparel, Hardware, Paints

and Floor Covering, Furniture, Draperies and Bedding, Consumer Electronics, and Vending.j Includes Beauty Salons, Fitness Centers, Wholesale Services, and Others.

Source: USDOC (1988) (with calculations for rows involving “all traditional” and “all business format”).

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

1.3 In Which Industries Do We Find Franchising? 11

to accurately assess how franchising has evolved since the mid-1980s in theUnited States.19

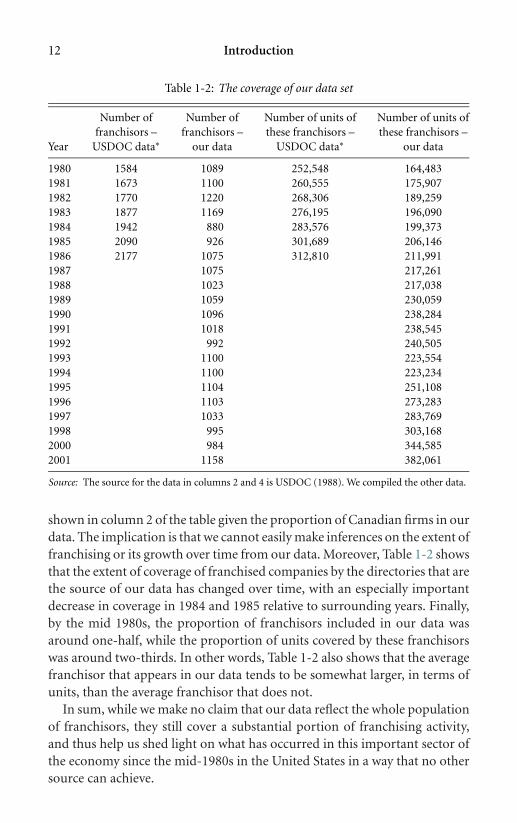

In this book, we rely on a database on franchisors that we have constructedfrom franchisor directories to shed some light on the evolution of franchis-ing and the franchise relationship since the mid-1980s, and to provide amore accurate description of current data patterns. Our database covers allthe franchisors that appear at least once in the 1981 to 1993 Entrepreneur’s“Franchise 500” surveys or in the 1994 to 2002 editions of Bond’s SourceBook of Franchise Opportunities, now called the Bond’s Franchise Guide.20

Each year, these publications give detailed profiles for about 1,000 franchis-ing companies and, hence, cover a very significant portion of the industry. Ineach case, the data for a given year are obtained from the next year’s survey ordirectory as these are all published early in the calendar year. In other words,our 2001 data are from the 2002 Bond’s Franchise Guide. After 1994, we choseto use the Bond’s Franchise Guide because Entrepreneur’s 1994 survey coveredfewer chains than usual and, from 1995 onward, Entrepreneur stopped report-ing advertising fee data. Furthermore, the Bond’s Franchise Guide, which hasthe advantage of providing more details on each of the franchisors it profiles,had become an annual publication by then.21 Together, these sources provideinformation from 1980 through 2001 (except for 1999, as the 2000 Bond’sFranchise Guide was never published) and cover more than 5,000 franchisorsin total, 12 percent of which on average are Canadian.

Table 1-2 displays the specific number of franchisors included in our dataeach year. For the years when this information was available, namely the early1980s, the table also shows the total number of U.S. franchisors according tothe USDOC. It is clear from this information that our data are not of censusquality, meaning that not all U.S. franchisors are included in our sources. Infact, the number of U.S. franchisors in the data is slightly below the numbers

19 The 2001 snapshot provided by the IFA Educational Foundation and Price WaterhouseCoopers (2004) does not use the same sector classification as the USDOC. Moreover,it only provides aggregate information on total establishments, jobs, payroll, and valueadded in each sector and does not allow us to follow franchising activities over time.Of course, we still rely on it whenever it provides additional insights into franchisingactivity.

20 We exclude from our data the few chains that are in these sources but yet report eitherno outlet at all (that is, no company nor franchised outlet) or report absolutely no fees(that is, no royalty rate, franchise fee, advertising rate, or ongoing fixed payments) inthe survey year.

21 The Bond’s Franchise Guides were also published in 1985, 1989, and then in 1990–91and 1991–92, and in 1993. Since then, they have been published yearly, except for the2000 edition (with the 1999 data) that was skipped.

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

12 Introduction

Table 1-2: The coverage of our data set

Number of Number of Number of units of Number of units offranchisors – franchisors – these franchisors – these franchisors –

Year USDOC data∗ our data USDOC data∗ our data

1980 1584 1089 252,548 164,4831981 1673 1100 260,555 175,9071982 1770 1220 268,306 189,2591983 1877 1169 276,195 196,0901984 1942 880 283,576 199,3731985 2090 926 301,689 206,1461986 2177 1075 312,810 211,9911987 1075 217,2611988 1023 217,0381989 1059 230,0591990 1096 238,2841991 1018 238,5451992 992 240,5051993 1100 223,5541994 1100 223,2341995 1104 251,1081996 1103 273,2831997 1033 283,7691998 995 303,1682000 984 344,5852001 1158 382,061

Source: The source for the data in columns 2 and 4 is USDOC (1988). We compiled the other data.

shown in column 2 of the table given the proportion of Canadian firms in ourdata. The implication is that we cannot easily make inferences on the extent offranchising or its growth over time from our data. Moreover, Table 1-2 showsthat the extent of coverage of franchised companies by the directories that arethe source of our data has changed over time, with an especially importantdecrease in coverage in 1984 and 1985 relative to surrounding years. Finally,by the mid 1980s, the proportion of franchisors included in our data wasaround one-half, while the proportion of units covered by these franchisorswas around two-thirds. In other words, Table 1-2 also shows that the averagefranchisor that appears in our data tends to be somewhat larger, in terms ofunits, than the average franchisor that does not.

In sum, while we make no claim that our data reflect the whole populationof franchisors, they still cover a substantial portion of franchising activity,and thus help us shed light on what has occurred in this important sector ofthe economy since the mid-1980s in the United States in a way that no othersource can achieve.

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

1.3 In Which Industries Do We Find Franchising? 13

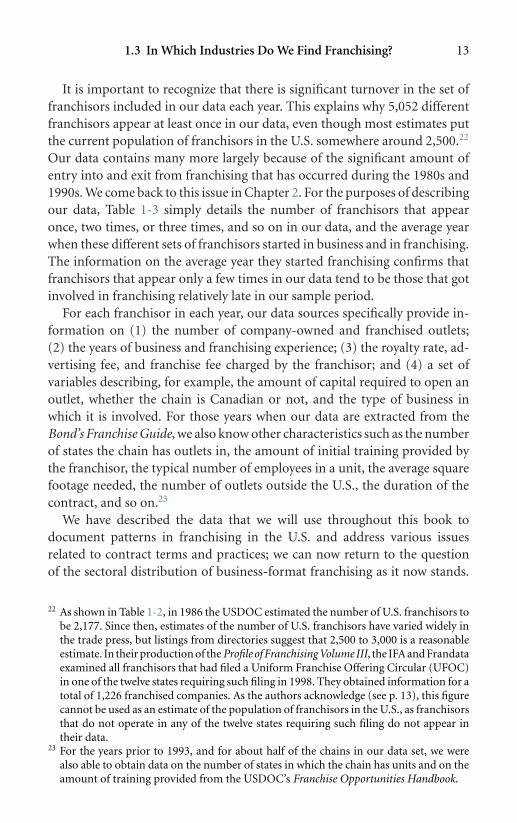

It is important to recognize that there is significant turnover in the set offranchisors included in our data each year. This explains why 5,052 differentfranchisors appear at least once in our data, even though most estimates putthe current population of franchisors in the U.S. somewhere around 2,500.22

Our data contains many more largely because of the significant amount ofentry into and exit from franchising that has occurred during the 1980s and1990s. We come back to this issue in Chapter 2. For the purposes of describingour data, Table 1-3 simply details the number of franchisors that appearonce, two times, or three times, and so on in our data, and the average yearwhen these different sets of franchisors started in business and in franchising.The information on the average year they started franchising confirms thatfranchisors that appear only a few times in our data tend to be those that gotinvolved in franchising relatively late in our sample period.

For each franchisor in each year, our data sources specifically provide in-formation on (1) the number of company-owned and franchised outlets;(2) the years of business and franchising experience; (3) the royalty rate, ad-vertising fee, and franchise fee charged by the franchisor; and (4) a set ofvariables describing, for example, the amount of capital required to open anoutlet, whether the chain is Canadian or not, and the type of business inwhich it is involved. For those years when our data are extracted from theBond’s Franchise Guide, we also know other characteristics such as the numberof states the chain has outlets in, the amount of initial training provided bythe franchisor, the typical number of employees in a unit, the average squarefootage needed, the number of outlets outside the U.S., the duration of thecontract, and so on.23

We have described the data that we will use throughout this book todocument patterns in franchising in the U.S. and address various issuesrelated to contract terms and practices; we can now return to the questionof the sectoral distribution of business-format franchising as it now stands.

22 As shown in Table 1-2, in 1986 the USDOC estimated the number of U.S. franchisors tobe 2,177. Since then, estimates of the number of U.S. franchisors have varied widely inthe trade press, but listings from directories suggest that 2,500 to 3,000 is a reasonableestimate. In their production of the Profile of Franchising Volume III, the IFA and Frandataexamined all franchisors that had filed a Uniform Franchise Offering Circular (UFOC)in one of the twelve states requiring such filing in 1998. They obtained information for atotal of 1,226 franchised companies. As the authors acknowledge (see p. 13), this figurecannot be used as an estimate of the population of franchisors in the U.S., as franchisorsthat do not operate in any of the twelve states requiring such filing do not appear intheir data.

23 For the years prior to 1993, and for about half of the chains in our data set, we werealso able to obtain data on the number of states in which the chain has units and on theamount of training provided from the USDOC’s Franchise Opportunities Handbook.

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

14 Introduction

Table 1-3: Sample characteristics

Number of Number of Started in StartedObserved firms observations business in (mean) franchising in (mean)

Only once 1,429 1,429 1977.8 1984.3Twice 946 1,892 1978.5 1984.73 times 591 1,773 1976.8 1983.44 times 460 1,840 1974.4 1982.45 times 278 1,390 1976.8 1983.06 times 254 1,524 1974.5 1982.27 times 204 1,428 1974.8 1981.98 times 165 1,320 1971.8 1980.69 times 97 873 1971.6 1980.610 times 110 1,100 1971.2 1979.411 times 86 946 1973.2 1978.512 times 72 864 1972.7 1979.913 times 70 910 1969.4 1977.114 times 48 672 1970.6 1976.915 times 36 540 1971.1 1978.116 times 37 592 1966.1 1973.217 times 37 629 1966.2 1972.518 times 37 666 1968.5 1974.419 times 25 475 1965.0 1969.920 times 34 680 1964.3 1969.921 times 36 756 1961.8 1965.5

Total 5,052 22,299

Note: Although our data covers a period of 22 years, from 1980 to 2001, we can observe a given chaina maximum of 21 times since we have no data for the year 1999.

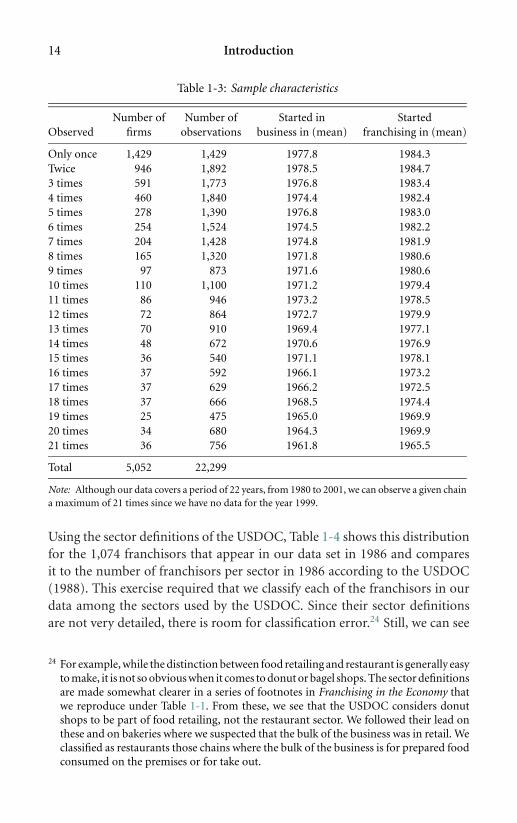

Using the sector definitions of the USDOC, Table 1-4 shows this distributionfor the 1,074 franchisors that appear in our data set in 1986 and comparesit to the number of franchisors per sector in 1986 according to the USDOC(1988). This exercise required that we classify each of the franchisors in ourdata among the sectors used by the USDOC. Since their sector definitionsare not very detailed, there is room for classification error.24 Still, we can see

24 For example, while the distinction between food retailing and restaurant is generally easyto make, it is not so obvious when it comes to donut or bagel shops. The sector definitionsare made somewhat clearer in a series of footnotes in Franchising in the Economy thatwe reproduce under Table 1-1. From these, we see that the USDOC considers donutshops to be part of food retailing, not the restaurant sector. We followed their lead onthese and on bakeries where we suspected that the bulk of the business was in retail. Weclassified as restaurants those chains where the bulk of the business is for prepared foodconsumed on the premises or for take out.

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

Tabl

e1-

4:T

hese

ctor

aldi

stri

buti

onof

busi

ness

-for

mat

fran

chis

ors

Nu

mbe

rof

Nu

mbe

rof

Pro

port

ion

Nu

mbe

rof

Nu

mbe

rof

fran

chis

ors

infr

anch

isor

sin

ofpo

pula

tion

fran

chis

ors

infr

anch

isor

sin

Sect

or19

86pe

rU

SDO

Cda

tase

tin

1986

sam

pled

in19

86da

tain

1996

data

in20

01

Au

tom

otiv

eP

rodu

cts

and

Serv

ices

174

9554

.673

80B

usi

nes

sA

ids

and

Serv

ices

436

189

43.3

173

180

Con

stru

ctio

n,H

ome

Impr

ovem

ent,

184

100

54.3

130

167

Mai

nte

nan

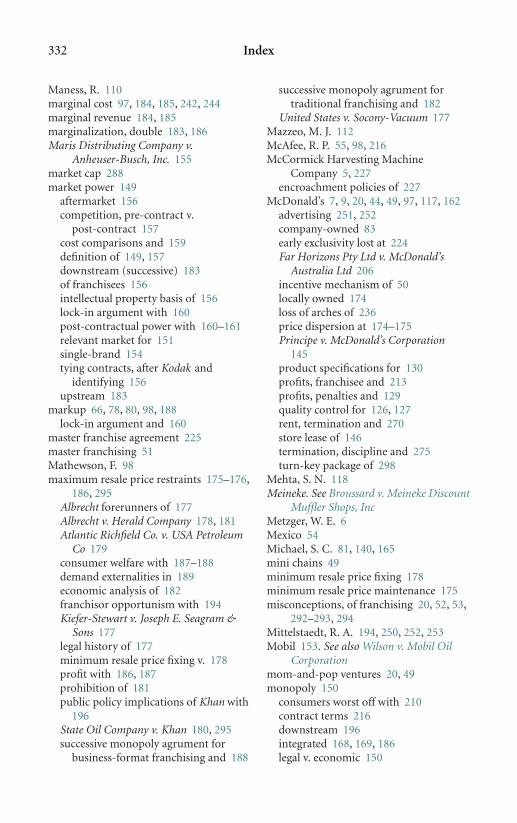

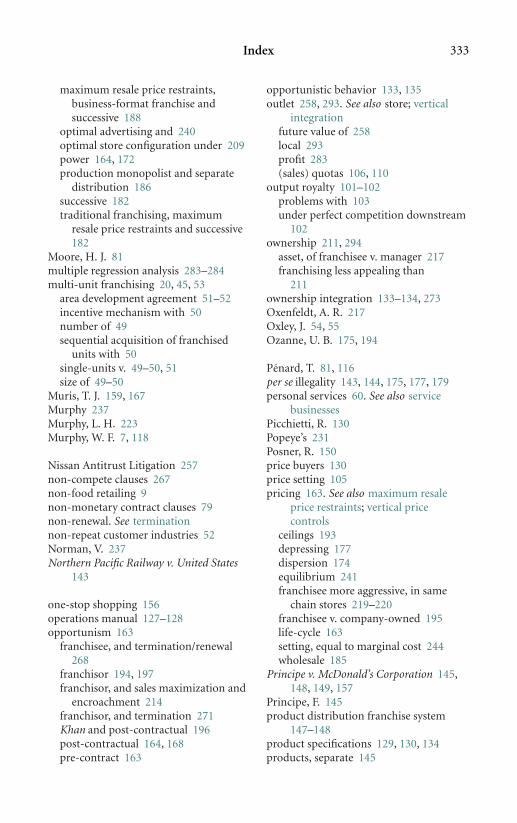

ce,a

nd

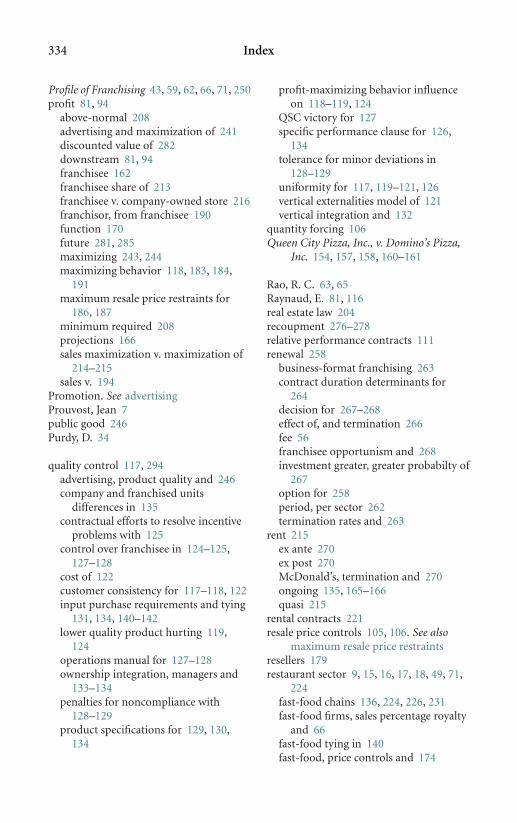

Cle

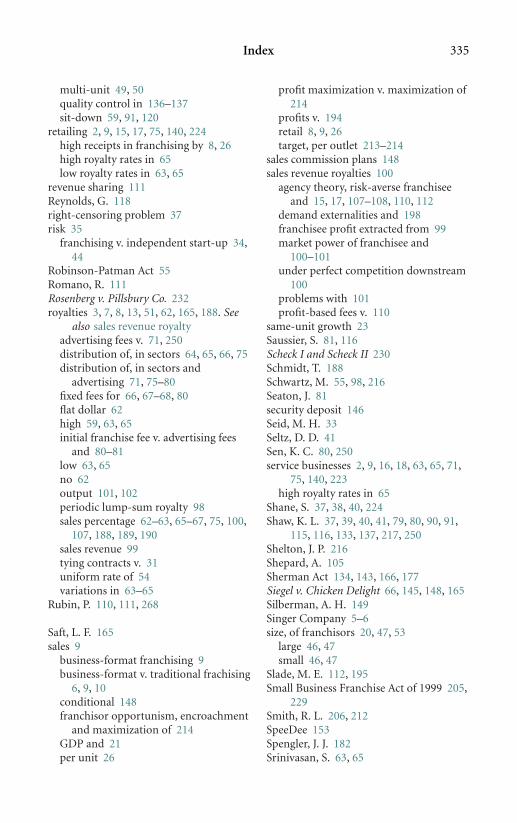

anin

gSe

rvic

esC

onve

nie

nce

Stor

es27

1451

.98

10E

duca

tion

alP

rodu

cts

and

Serv

ices

6834

50.0

5662

Hot

els,

Mot

els,

and

Cam

pgro

un

ds50

2142

.014

21La

un

dry

and

Dry

-Cle

anin

gSe

rvic

es19

947

.410

12R

ecre

atio

n,E

nte

rtai

nm

ent,

and

Trav

el45

2453

.340

29R

enta

lSer

vice

s,A

uto

–Tru

ck27

1763

.013

18R

enta

lSer

vice

s,E

quip

men

t36

2158

.313

8R

esta

ura

nts

488

209

42.8

243

245

Ret

ailin

g(F

ood

Non

-Con

ven

ien

ce)

198

100

50.5

8910

3R

etai

ling

(Non

-Foo

d)33

917

651

.917

415

9M

isce

llan

eou

s86

6676

.767

64

Tota

lNu

mbe

rof

2,17

71,

075

49.4

1,10

31,

158

Bu

sin

ess-

Form

atFr

anch

isor

s

Sour

ce:

Th

eso

urc

efo

rth

eda

tain

the

firs

tco

lum

nis

USD

OC

(198

8).W

eco

mpi

led

the

oth

ers.

15

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

16 Introduction

from Table 1-4 that our best effort at classifying all the franchisors suggeststhat our data covers between 42 and 77 percent of the franchisors in each ofthe USDOC sectors in 1986.

Table 1-4 also shows the number of franchisors in our data set, perUSDOC sector, ten years later in 1996, and then again in 2001. It is diffi-cult to disentangle from these figures how much of the change in numbersof franchisors per sector between 1986 and 1996 or 2001 is due to samplingchanges, and how much is due to real growth in some sectors compared toothers. Assuming that there has not been a major change over time in the sur-vey sampling procedures used by our sources, the data in Table 1-4 suggestthat there has been some decline since the mid-1980s in the number of auto-motive products and services franchisors and equipment rental franchisors.On the other hand, the data indicate that there are now more franchisors inthe construction, maintenance and cleaning services industry, in the educa-tional products and services sector, and in the restaurant sector. We expect thelatter reflects the relative growth in the number of sandwich and bagel shopsas well as the newer quick-casual segment of this industry. These patternsare confirmed generally by corresponding data from the IFA Educational andPrice Waterhouse Coopers (2004) report which show a significant decrease,relative to the 1986 USDOC data, in the number of establishments in theautomotive sector in the U.S. (from the 36,763 shown in Table 1-1 to 28,755in 2001 according to the IFA report) and a substantial increase in the numberof restaurants (from 78,203 in Table 1-1 to 183,318 in the IFA report). Un-fortunately, differences in sector definitions between the sources prevent usfrom making further comparisons.

As we discuss in some detail in Chapter 2, our data set offers a goodapproximation of the overall population of new franchisors except for thelast few years of our data. To provide a better sense of where entry has beenmost prevalent in the 1980s and early 1990s, we rely on the number of newfranchisors in our data per USDOC sector. Specifically, we present in Table 1-5the number of franchisors that started franchising in every three-year period,starting in 1980 and ending in 1997. We end with 1997 because we only have afew years of data to identify the new entrants at the end of our sample periodand, hence, we do not capture them all. But from our earlier data, more than90 percent of the franchisors appear in our data within five to six years ofwhen they start franchising. Thus, the number of new franchisors in 1995and 1996 may still be underestimated in Table 1-5; for all the years prior tothat, however, we have a reasonable estimate of the number of new entrants.

The data in Table 1-5 first show a sizable reduction in the number of newfranchisors in the early 1990s relative to the 1980s, even ignoring the 1995 to

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

Tabl

e1-

5:T

hese

ctor

aldi

stri

buti

onof

new

busi

ness

-for

mat

fran

chis

ors

Nu

mbe

rof

fran

chis

ors

inda

tase

tth

atst

arte

dfr

anch

isin

gin

:

Sect

or19

80–8

219

83–8

519

86–8

819

89–9

119

92–9

419

95–9

7To

tal

Au

tom

otiv

eP

rodu

cts

and

Serv

ices

5055

5030

1912

216

Bu

sin

ess

Aid

san

dSe

rvic

es14

310

213

111

470

3559

5C

onst

ruct

ion

,Hom

eIm

prov

emen

t,73

5868

7148

3935

7M

ain

ten

ance

,an

dC

lean

ing

Serv

ices

Con

ven

ien

ceSt

ores

54

43

53

24E

duca

tion

alP

rodu

cts

and

Serv

ices

3228

3424

329

159

Hot

els,

Mot

els,

and

Cam

pgro

un

ds8

811

74

745

Lau

ndr

yan

dD

ry-C

lean

ing

Serv

ices

28

114

43

32R

ecre

atio

n,E

nte

rtai

nm

ent,

and

Trav

el26

2620

2226

812

8R

enta

lSer

vice

s,A

uto

–Tru

ck13

84

33

233

Ren

talS

ervi

ces,

Equ

ipm

ent

1932

1318

32

87R

esta

ura

nts

139

107

134

120

8427

611

Ret

ailin

g(F

ood

Non

-Con

ven

ien

ce)

6469

6632

3519

285

Ret

ailin

g(N

on-F

ood)

130

105

143

9090

5261

0M

isce

llan

eou

s73

5152

5831

2428

9

Tota

lBu

sin

ess-

Form

atFr

anch

isin

g77

766

174

159

645

424

234

71

Sour

ce:

Com

pile

dby

the

auth

ors.

17

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

18 Introduction

1997 data. On average, for the three 3-year periods in the 1980s, there weremore than 700 new entrants; for the two 3-year periods in the early 1990s,the average declined to 525. Consistent with Table 1-4, Table 1-5 also showsfewer new franchisors in the automotive products and services sector and inthe equipment rental sector in the early 1990s than in earlier periods. Othersectors, such as the educational products and services sector and, to a lesserextent, the construction and maintenance and restaurant sectors, show a fairlyconstant number of new entrants over the 1980 to 1994 period despite thefairly large decline in total entry at the end of this time period. In other words,in proportion to total entry, these sectors are more than holding their own.This further supports the data in Table 1-4 in which we found significantgrowth in these sectors.25

According to the USDOC data and industry sources, the growth inbusiness-format franchising was tied to the fast-food industry in the 1960sand to the business aids and services and the automotive products and ser-vices in the 1970s. Our data suggest that in the 1980s and early 1990s, ithas been tied mostly to the personal service sector (such as maid services,day-care facilities, lawn maintenance, and health and fitness services) and tothe diversification and continued growth of franchising within the restaurantindustry.

1.4 Plan of Study

Our goal in The Economics of Franchising is to both describe how franchisingworks and highlight the economic tensions that contribute to conflict in thefranchisor–franchisee relationship. To this end, we begin in Chapter 2 withan examination of four popular misconceptions regarding franchising. Thesemisconceptions involve the extent of growth, the financial security affordedby franchising, the size of franchised chains, and the extent of single-unitownership by franchisees.

In Chapter 3, we highlight some of the main components of franchisecontracts, paying particular attention to the financial components of thecontract, namely royalty rates, franchise fees, and advertising fees. For each ofthese, we examine in particular their levels and how they vary across chainsand industries. We also investigate how the tendency to use these differentfees and the levels at which they are set have evolved between 1980 and 2001.

25 Of course, growth really depends not only on entry, but also on how many firms exitthe sector. We return to this issue in Chapter 2.

P1: KsF0521772524c01.xml CB802/Blair 0 521 77252 4 April 29, 2005 18:26

1.4 Plan of Study 19

We conclude, among other things, by pointing out the similarity between thefees structures and levels charged by U.S. and non-U.S. franchisors.

In Chapter 4, we explore franchising as a contractual alternative to verticalintegration for franchisors. We show how firms involved in franchising typ-ically use a mix of franchised and vertically integrated, or company-owned,outlets. We then present a more detailed examination of a set of vertical re-straints that can be used to replicate the vertically integrated outcome, at leastin theory, and evaluate their performance under various circumstances. Fi-nally, we discuss agency–theoretic arguments that have been used to explainvariation in the main financial contract terms used in franchise contracts, andshow how these arguments also can shed light on why different franchisorschoose different levels of vertical integration.

From that point on, each of the remaining chapters of this book is dedi-cated to a detailed examination of a specific conflict area between franchisorsand franchisees. We begin each of these chapters with the economic motiva-tion for the problem, followed by an examination of the relevant court casesand legislation, if applicable. We conclude each chapter by examining thelikely effect of this source of conflict on franchisors, franchisees, and fran-chising as a method of distribution. Specifically, we explore quality controland quality decisions in Chapter 5. We review input purchase requirements inChapter 6. Chapter 7 focuses on pricing decisions and price constraints. InChapter 8, we examine outlet location decisions and the encroachment prob-lem. We discuss inherent conflicts of interest related to advertising and pro-motion in Chapter 9 and terminations, renewals and transfers of franchisedunits in Chapter 10. Chapter 11 concludes by returning to the idea that despiteall these sources of conflict, franchising is a robust organizational form thathas withstood the test of time and will continue to play a major role in theU.S. and global economies.

P1: KsF0521772524c02.xml CB802/Blair 0 521 77252 4 April 30, 2005 12:17

2

Four Popular Misconceptions about Franchising

There are many misconceptions surrounding franchising in the United Statesand abroad. In our view, these misconceptions result from relying on casualimpressions rather than a careful evaluation of the empirical evidence. In thischapter, we focus our attention on four such misconceptions. By summarizingthe existing data, we hope to disabuse the reader of these misconceptions andthereby generate a more realistic appreciation of franchising.

We begin with the notion that franchising has been growing at a phenom-enal rate in the U.S. for several decades. As we shall show, this impression ismisleading: for the last two decades at least, our best estimates indicate thatfranchising in the U.S. has grown, at most, at rates commensurate with therest of the economy. Interestingly, research conducted in the United Kingdomsuggests that similar claims of tremendous growth in franchising in thatcountry in the 1990s are also ill-founded. Second, we examine the extentof entry and exit for franchisors, and then also for franchisees. The datashow that many firms indeed become new franchisors each year, a fact thatis well-publicized in the trade press. But many firms also exit franchisingor fail, and this generally receives much less attention. As for franchisees,we find that the notion that franchising poses substantially fewer businessrisks for franchisees than starting an independent business is not supportedby the data. Third, we consider the size of franchised chains. Contrary tothe impression created by the pervasive presence of very large franchisedchains with household names such as Dunkin’ Donuts, H&R Block, andMcDonald’s, we show that the majority of franchised chains are quite smalland, thus, not well-established contrary to what people expect. Fourth, andfinally, there is an impression that franchisees’ businesses are necessarilysmall, “mom-and-pop” ventures, with each of them operating a single unit.This is also not true: multi-unit franchising is pervasive, and a number of

20

P1: KsF0521772524c02.xml CB802/Blair 0 521 77252 4 April 30, 2005 12:17

2.1 Growth: Fact and Fancy 21

multi-unit franchisees are large enough to rival the size of their own or otherfranchisors.

2.1 Growth: Fact and Fancy

In this section, we explore how franchising has grown relative to the economyas a whole since the early 1970s. These facts are then compared to the impres-sion of tremendous growth found in the trade press. Our point here is not todeny the importance of franchising as an organizational form, nor the rolethat it has played in the growth of the economy over the last few decades. Onthe contrary, it should be clear from the preceding chapter that franchisingis a very important method of doing business in the U.S. and elsewhere. Butmany of the reports of its growth in the last two decades have been grosslyexaggerated and must be put in proper perspective.

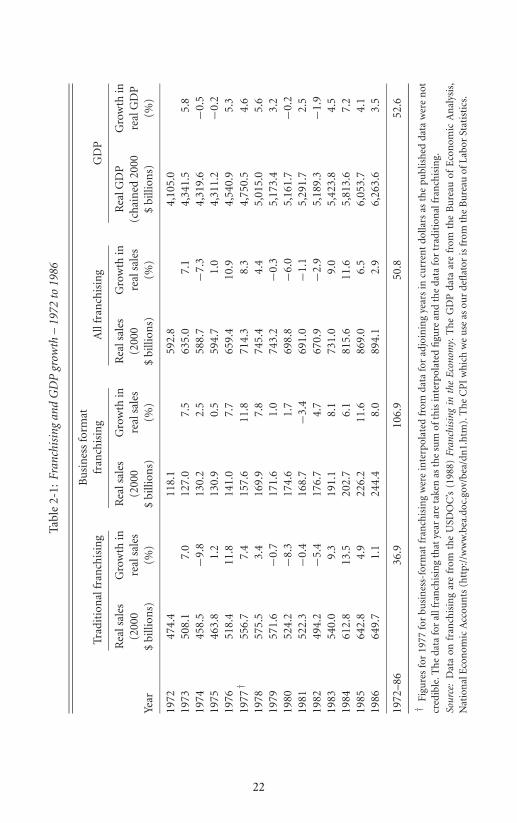

We begin our assessment with the period 1972 to 1986, when census-type data on the number of franchisors, the number of units, and sales byfranchised chains are available from the USDOC.26 Table 2-1 contains thesales data, in real 2000 U.S dollars, and the growth rates in these real saleslevels for traditional and business-format franchising, separately and overall(all franchising), between 1972 and 1986. For comparison purposes, the tablealso includes data on real GDP and its growth over the same period.

The data in this table imply that business-format franchising indeed hasoutperformed the economy as a whole over most of this period. Specifically,in real terms, business-format franchising sales have grown by 106.9 percentbetween 1972 and 1986 while GDP grew by 52.6 percent over the sameperiod. Traditional franchising, however, has grown less than the rest of theeconomy, by 36.9 percent during this time. The result is that the sum of allfranchising has grown at a rate that is basically the same as the rate of growthof the economy as a whole. This growth rate is nowhere near the double-digitgrowth rates suggested by the popular press. For example, the FranchiseTimes, April 1996, reports that “Franchising growth should increase in 1996,with total unit expansion projected between 12% and 14%, up from 1995’s10% to 12%.” Equivalent and even higher growth figures appeared regularlyin the trade press throughout the late 1970s and 1980s. We further examinethe genesis of some of these very optimistic growth figures below. For now, wesimply conclude that even business-format franchising did not grow at these

26 This source, which was first published in 1969, was modified significantly in 1972 suchthat only the data from that year onward are comparable.

P1: KsF0521772524c02.xml CB802/Blair 0 521 77252 4 April 30, 2005 12:17

Tabl

e2-

1:Fr

anch

isin

gan

dG

DP

grow

th–

1972

to19

86

Bu

sin

ess

form

atTr

adit

ion

alfr

anch

isin

gfr

anch

isin

gA

llfr

anch

isin

gG

DP

Rea

lsal

esG

row

thin

Rea

lsal

esG

row

thin

Rea

lsal

esG

row

thin

Rea

lGD

PG

row

thin

(200

0re

alsa

les

(200

0re

alsa

les

(200

0re

alsa

les

(ch

ain

ed20

00re

alG

DP

Year

$bi

llion

s)(%

)$

billi

ons)

(%)

$bi

llion

s)(%

)$

billi

ons)

(%)

1972

474.

411

8.1

592.

84,

105.

019

7350

8.1

7.0

127.

07.

563

5.0

7.1

4,34

1.5

5.8

1974

458.

5−9

.813

0.2

2.5

588.

7−7

.34,

319.

6−0

.519

7546

3.8

1.2

130.

90.

559

4.7

1.0

4,31

1.2

−0.2

1976

518.

411

.814

1.0

7.7

659.

410

.94,

540.

95.

319

77†

556.

77.

415

7.6

11.8

714.

38.

34,

750.

54.

619

7857

5.5

3.4

169.

97.

874

5.4

4.4

5,01

5.0

5.6

1979

571.

6−0

.717

1.6

1.0

743.

2−0

.35,

173.

43.

219

8052

4.2

−8.3

174.

61.

769

8.8

−6.0

5,16

1.7

−0.2

1981

522.

3−0

.416

8.7

−3.4

691.

0−1

.15,

291.

72.

519

8249

4.2

−5.4

176.

74.

767

0.9

−2.9

5,18

9.3

−1.9

1983

540.

09.

319

1.1

8.1

731.

09.

05,

423.

84.

519

8461

2.8

13.5

202.

76.

181

5.6

11.6

5,81

3.6

7.2

1985

642.

84.

922

6.2

11.6

869.

06.

56,

053.

74.

119

8664

9.7

1.1

244.

48.

089

4.1

2.9

6,26

3.6

3.5

1972

–86

36.9

106.

950

.852

.6

†Fi

gure

sfo

r19

77fo

rbu

sin

ess-

form

atfr

anch

isin

gw

ere

inte

rpol

ated

from

data

for

adjo

inin

gye

ars

incu

rren

tdo

llars

asth

epu

blis

hed

data

wer

en

otcr

edib

le.T

he

data

for

allf

ran

chis

ing

that

year

are

take

nas

the

sum

ofth

isin

terp

olat

edfi

gure

and

the

data

for

trad

itio

nal

fran

chis

ing.

Sour

ce:

Dat

aon

fran

chis

ing

are

from

the

USD

OC

’s(1

988)

Fran

chis

ing

inth

eE

cono

my.

Th

eG

DP

data

are

from

the

Bu

reau

ofE

con

omic

An

alys

is,

Nat

ion

alE

con

omic

Acc

oun

ts(h

ttp:

//w

ww

.bea

.doc

.gov

/bea

/dn

1.h

tm).

Th

eC

PI

wh

ich

we

use

asou

rde

flat

oris

from

the

Bu

reau

ofLa

bor

Stat

isti

cs.

22

P1: KsF0521772524c02.xml CB802/Blair 0 521 77252 4 April 30, 2005 12:17

2.1 Growth: Fact and Fancy 23

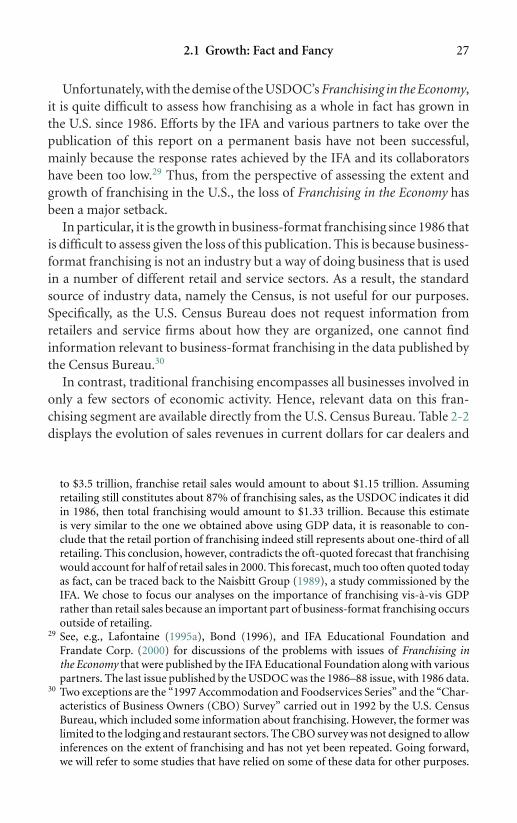

rates during this period: 106.9 percent over a 14-year period amounts to about7.6 percent per year.

Figures 2-1 and 2-2 show the data on franchising growth relative to GDPgrowth in two additional ways. Figure 2-1 presents information on theevolution of the number of units of business-format and traditional fran-chised chains, along with data on the evolution of real GDP, from 1972 to1986. We use the number of units instead of sales as an alternative way tocapture real rather than nominal growth in franchising. Figure 2-2 jointly ad-dresses the issue of same-unit growth along with growth in number of unitsby depicting the value of goods sold through franchising as a proportion ofreal GDP between 1972 and 1986. Such a ratio gives a “unit free” measure ofthe extent of franchising, eliminating the need to distinguish between nomi-nal and real figures.27 In both figures, the franchising data again are from theUSDOC (1988).

Figure 2-1 first shows the dramatic decrease in the number of units intraditional franchising over this period, mostly due to the closing of a largenumber of smaller gasoline stations that were replaced by the new “pumper”stations that could handle much larger sales volumes. It also shows that thenumber of units in business-format franchising has grown steadily over thisperiod. But, of course, GDP also has grown during this time. As the timetrends in the two series are quite similar, it appears that in terms of units,business-format franchising was growing at a rate similar to that of theeconomy as a whole even back in the 1970s and early 1980s. Perhaps mostimportantly, Figure 2-1 addresses directly one type of claim about franchisinggrowth that is currently found in the trade press: “With a new franchisebusiness opening somewhere in the U.S. every 17 minutes, franchising isindeed the success story of the 1980s and 1990s” (IFA, Winter 1992 FranchiseOpportunities Guide, 10). In the Winter 1995 edition, this figure had become“a new franchise business every 8 minutes” (12). But a new franchise businessevery 17 minutes is equivalent to 85 new franchises per day, or more than30,000 new franchises per year. A new franchise every 8 minutes amounts tomore than 65,000 new franchises a year. The data in the graph suggest a muchmore modest growth than either of these startling claims, even if we focuson business-format franchising and even if the period covered by the graphis seen by many as the prime period of growth for this form of franchising.On average, between 1972 and 1986, business-format franchising grew byabout 9,000 units per year. This is noteworthy growth, but nothing close

27 For meaningful comparisons, both franchising sales and GDP need to be measured inthe same units, either both in real dollars or both in nominal dollars.

P1: KsF0521772524c02.xml CB802/Blair 0 521 77252 4 April 30, 2005 12:17

Yea

r

Number of Units

GDP in billions of chained 2000 dollars

Tra

ditio

nal -

uni

ts

Bus

. For

mat

- u

nits

Rea

l GD

P

Figu

re2-

1:N

um

ber

ofu

nit

san

dre

alG

DP

inth

eU

.S.

24

P1: KsF0521772524c02.xml CB802/Blair 0 521 77252 4 April 30, 2005 12:17

Yea

r

% of GDP

Tra

ditio

nal (

ratio

of c

urre

nt $

)

Bus

. for

mat

(ra

tio o

f cur

rent

$)

Tot

al (

ratio

of c

urre

nt $

)

Figu

re2-

2:Fr

anch

isin

gsa

les

asa

per

cen

tof

GD

P19

72–1

986.

25

P1: KsF0521772524c02.xml CB802/Blair 0 521 77252 4 April 30, 2005 12:17

26 Four Popular Misconceptions about Franchising

to the claims above. Further, if we extrapolate from the data in the graph, thereis nothing there to suggest that this growth should be expected to increasedramatically later and thus justify the claims made in the early 1990s. Finally,the number of traditional franchised units actually decreased between 1972and 1986, and again there is nothing in the data and nothing going on inthe industry to suggest this would reverse itself. Indeed, the retail gasolineindustry at the time was replacing its large number of older stations, eachwith just a few pumps, service bays and full service, with a smaller numberof large self-serve multi-pump stations with attending convenience storesinstead of service bays (see, e.g., Marvel 1995). And in fact, according to theU.S. census of retailing, the number of establishments within the traditionalfranchising sectors of gasoline retailing, car retailing and soft-drink bottlingwas down from 149,313 in 1986 to 130,640 in 1992, and by 1997, it haddecreased further to 125,509.