theme back to business - credit suisse

TRANSCRIPT

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

13 July 2017 Asia Pacific/India Equity Research

Multi Industry

Tata Group The Credit Suisse Connections Series leverages our

exceptional breadth of macro and micro research to deliver

incisive cross-sector and cross-border thematic insights for

our clients.

Research Analysts

Anantha Narayan

91 22 6777 3730

Nitin Jain

91 22 6777 3851

Arnab Mitra

91 22 6777 3806

Ashish Gupta

91 22 6777 3895

Badrinath S.

91 22 6777 3698

Jatin Chawla

91 22 6777 3719

Lokesh Garg

91 22 6777 3743

Ravi Shankar

91 22 6777 3869

Sunil Tirumalai

91 22 6777 3714

THEME

Back to business

Figure 1: The five likely key focus areas for the new team

Source: Credit Suisse research, Credit Suisse HOLT Lens for Titan, Tata Chemicals and Tata Global Beverages

■ Largest Indian conglomerate but areas to improve. The Tata Group

with over 100 companies is India's largest conglomerate with US$100 bn+

of revenue and 660k employees in FY16 and current market capitalisation

of US$125 bn+. The companies present a mixed bag—only four of the top

ten have a 15%+ ROE, and about 60% of companies for which we have

data have an ROE less than 10%. We estimate TCS to contribute 85-90%

of the parent's dividend receipts. There is a long tail with 94% of revenue

from the top-ten companies and domestic being only one-third of revenue,

with domestic consumption (ex-financial services) being less than 10%.

■ New energy at the top. With the new CEO, N Chandrasekaran (ex-CEO of

TCS), and his team we expect renewed energy at the top with five key

elements of strategy—improvement of return ratios (especially for Tata

Motors, Tata Power, Tata Steel & Tata Teleservices), focus on domestic

consumption and leveraging brands better, simplicity in structure and

holding, ensuring relevance in all sectors it is present in and digital initiatives.

■ Shift in focus will raise return. Execution is where the new team can

differentiate itself. Tata Motors can benefit from better India execution; Tata

Steel from improving returns in Europe and growth in India; Voltas from a

greater focus on its consumer business; and Titan from the domestic

consumption theme. Among others, media reports (Business Today, Live

Mint) have talked of how domestic focus and brand leverage could impact

Tata Global while new consumer offerings and non-core divestiture may

impact Tata Chemicals. We estimate that if some of the changes succeed,

there could be incremental value creation of US$10 bn-plus in the above

covered names and 20-40% gain for such stocks. Additionally, any debt

reduction in other companies could help the enterprise value of the Group.

Themes Companies that could be impacted Incremental value (% of current

market cap)

Return ratios Tata Motors: Domestic focus

Tata Steel: domestic focus, international

restructuring

Voltas: Expansion of consumer business

Titan: Focus on domestic consumption

Tata Chemicals: Consumption, cross-

holdings

Tata Global Beverages: Domestic, cross-

holdings

US$5 bn (22%)

US$2 bn (18%)

US$0.5 bn (21%)

US$3 bn (37%)

US$0.5 bn (19%)

US$0.6 bn (34%)

Domestic consumption

Simplicity, in structure

and holdings

Relevance, in segments

where the Group has

presence

Digital initiatives across

segments

13 July 2017

Tata Group 2

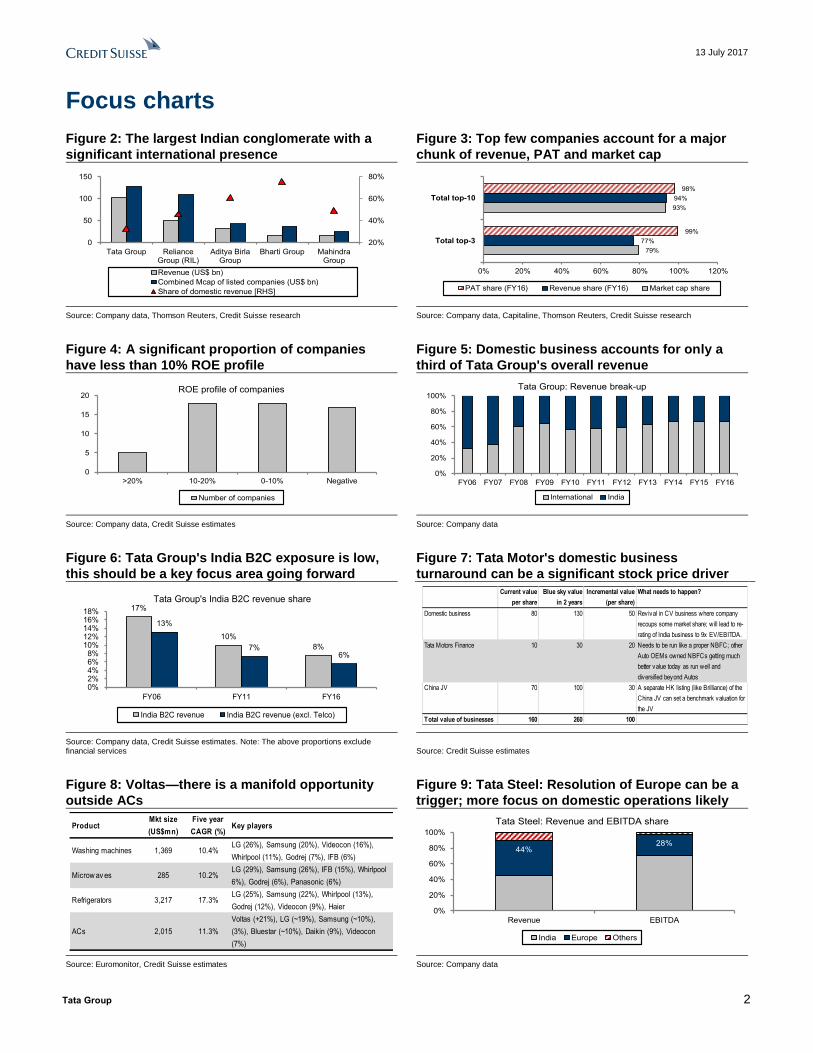

Focus charts

Figure 2: The largest Indian conglomerate with a

significant international presence

Figure 3: Top few companies account for a major

chunk of revenue, PAT and market cap

Source: Company data, Thomson Reuters, Credit Suisse research Source: Company data, Capitaline, Thomson Reuters, Credit Suisse research

Figure 4: A significant proportion of companies

have less than 10% ROE profile

Figure 5: Domestic business accounts for only a

third of Tata Group's overall revenue

Source: Company data, Credit Suisse estimates Source: Company data

Figure 6: Tata Group's India B2C exposure is low,

this should be a key focus area going forward

Figure 7: Tata Motor's domestic business

turnaround can be a significant stock price driver

Source: Company data, Credit Suisse estimates. Note: The above proportions exclude financial services

Source: Credit Suisse estimates

Figure 8: Voltas—there is a manifold opportunity

outside ACs

Figure 9: Tata Steel: Resolution of Europe can be a

trigger; more focus on domestic operations likely

Source: Euromonitor, Credit Suisse estimates Source: Company data

20%

40%

60%

80%

0

50

100

150

Tata Group RelianceGroup (RIL)

Aditya BirlaGroup

Bharti Group MahindraGroup

Revenue (US$ bn)

Combined Mcap of listed companies (US$ bn)

Share of domestic revenue [RHS]

79%

93%

77%

94%

99%

98%

0% 20% 40% 60% 80% 100% 120%

Total top-3

Total top-10

PAT share (FY16) Revenue share (FY16) Market cap share

0

5

10

15

20

>20% 10-20% 0-10% Negative

ROE profile of companies

Number of companies

0%

20%

40%

60%

80%

100%

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Tata Group: Revenue break-up

International India

17%

10%

8%

13%

7%6%

0%2%4%6%8%

10%12%14%16%18%

FY06 FY11 FY16

Tata Group's India B2C revenue share

India B2C revenue India B2C revenue (excl. Telco)

Current value

per share

Blue sky value

in 2 years

Incremental value

(per share)

What needs to happen?

Domestic business 80 130 50 Revival in CV business where company

recoups some market share; will lead to re-

rating of India business to 9x EV/EBITDA.

Tata Motors Finance 10 30 20 Needs to be run like a proper NBFC; other

Auto OEMs owned NBFCs getting much

better value today as run well and

diversified beyond Autos

China JV 70 100 30 A separate HK listing (like Brilliance) of the

China JV can set a benchmark valuation for

the JV

Total value of businesses 160 260 100

ProductMkt size

(US$mn)

Five year

CAGR (%)Key players

Washing machines 1,369 10.4%LG (26%), Samsung (20%), Videocon (16%),

Whirlpool (11%), Godrej (7%), IFB (6%)

Microw av es 285 10.2%LG (29%), Samsung (26%), IFB (15%), Whirlpool

6%), Godrej (6%), Panasonic (6%)

Refrigerators 3,217 17.3%LG (25%), Samsung (22%), Whirlpool (13%),

Godrej (12%), Videocon (9%), Haier

ACs 2,015 11.3%

Voltas (+21%), LG (~19%), Samsung (~10%),

(3%), Bluestar (~10%), Daikin (9%), Videocon

(7%)

44%28%

0%

20%

40%

60%

80%

100%

Revenue EBITDA

Tata Steel: Revenue and EBITDA share

India Europe Others

13 July 2017

Tata Group 3

Back to business

Largest Indian conglomerate but areas to improve Started in 1868, the Tata Group is India's largest conglomerate—FY16 revenue was over

US$100 bn, headcount over 660k and current market capitalisation is over US$125 bn. It

has about 100 operating companies.

As is to be expected in such a large conglomerate, there are many areas for improvement.

Only four companies in the top ten—TCS, Tata Motors, Voltas and Titan—have an ROE in

excess of 15%. ROE is less than 10% for about 60%+ of the companies for which we have

data. TCS is the single largest source of cash for the Group—it contributed 65% of Group

PAT and we estimate that its dividends accounted for 85-90% of the total inflow to the

parent. There is a long tail of companies as well—the top-ten companies (including

subsidiaries) account for 92% of the Group's revenue and 98% of PAT. Domestic B2C, a

strong growth area, contributes less than 10% of revenue (ex-financials).

The Group market capitalisation has been nearly flat over the last year, up 11% over three

years, underperforming the Indian market. Large companies—TCS, Tata Motors and Tata

Steel—have underperformed for over three years as have some smaller ones.

New energy at the top N Chandrasekaran (Chandra) took over as Chairman in January 2017 after a few months

of turmoil following his predecessor's dismissal. He is the first Chairman from outside the

shareholding families and has a stellar track record of leading TCS for seven years. He,

with his new team, can provide renewed energy at the top, in our view.

Based on our understanding of the Group, individual companies, and comments made in the

press (Business Standard, etc), we believe new management's strategy will hinge on five

key objectives: (1) Improvement of return ratios, especially for larger companies; (2) Focus

on domestic consumption. This would likely be for consumer businesses (Global, Chemicals,

Voltas) and financial services (Capital, insurance); (3) Simplification of the structure and

holding, including consolidating similar businesses in different entities and simplification of

intra-group holdings; (4) Relevance—the Group has sub-optimal presence in some large

segments such as financial services, retail/consumer and aviation. It would either want to

scale up or exit some of these. It also has presence in small segments through companies

whose sizes are not significant; and (5) Given the Group's presence in technology and

Chandra's background, it may step up its digital initiatives across its various businesses.

Shift in focus will raise returns Given the above broad themes, we believe companies such as Tata Motors, Tata Steel,

Voltas and Titan could benefit. Tata Chemicals and Tata Global Beverages could also be

impacted by the above strategy. Tata Motors could gain from better execution in the

domestic business, Tata Steel from better returns in the European operations. Voltas can

leverage its consumer brand for new consumer products (outside AC and air coolers), and

demerger of its projects business can also make it a pure consumer play. Titan may

benefit from the Group's focus on domestic consumption. Among others, media reports

(Business Today, Live Mint) have talked of how domestic focus and brand leverage may

impact Tata Global while new consumer offerings and non-core divestiture may impact

Tata Chemicals. Tata Power and Tata Teleservices had combined debt of US$14 bn.

We estimate that if some of the changes succeed, there could be incremental value

creation of US$10 bn-plus in the above covered names and between 20% and 40% for

individual covered stocks. Additionally, any debt reduction in other companies could help

the enterprise value of the Group.

We rate Tata Motors, Tata Steel, Titan, Voltas OUTPERFORM; we are NEUTRAL on TCS.

US$100 bn revenue in FY16, 660k employees, about 100 companies, US$125 bn market cap

Only four of the top ten have a 15%+ ROE,

~60% of companies for which we have data

have ROE <10%

New management at the top can bring renewed energy

We believe management will have

five key objectives

Tata Motors, Tata Steel, Voltas and Titan are likely gainers in our

coverage universe

13 July 2017

Tata Group 4

Table of contents

Focus charts 2

Back to business 3

Largest Indian conglomerate but areas to improve .................................................. 3

New energy at the top .............................................................................................. 3

Shift in focus will raise returns .................................................................................. 3

Largest Indian conglomerate but areas to improve 6

The largest Indian conglomerate with a high global exposure ................................. 6

Delving deeper into the Group's financials ............................................................. 10

Tata Group underperformed the market in the last one and three years, led by TCS

and Tata Motors ..................................................................................................... 17

Renewed energy at the top 19

Five key mantras .................................................................................................... 19

#1 Focus on the big guns ....................................................................................... 20

TCS: Little to be done ............................................................................................. 20

Tata Steel: Focus on India, addressing the pension issue .................................... 23

Tata Motors: India needs to be fixed ...................................................................... 26

Tata Power: Mundra power plant has weighed on profitability .............................. 30

Tata Teleservices: Challenges in the telecom industry .......................................... 32

#2 Domestic business and B2C may garner higher investment share .................. 34

#3 Some strong consumer brands can be leveraged better .................................. 35

#4 Some important segments need to scale up ..................................................... 37

#5 Restructuring of Group companies and their divisions can add value .............. 42

#6 Simplification of the cross-holding structure ...................................................... 44

#7 Sub-scale operations: Are they really needed? ................................................ 45

#8 Divestments may be value accretive for few companies .................................. 46

#9 Selective M&A approach in some businesses .................................................. 47

#10 Culture ............................................................................................................. 48

Shift in focus will raise returns 49

Tata Motors: Domestic business turnaround can offer upside ............................... 49

Tata Steel: The European business turnaround can improve returns significantly 50

Voltas: Consumer business expansion, demerger of projects can make Voltas a

good consumer play ............................................................................................... 51

Scenario analysis based on HOLT ......................................................................... 52

Overall Group financials likely to improve over the next two years ........................ 53

Tata Motors Ltd. (TAMO.BO) 54

13 July 2017

Tata Group 5

Tata Steel Ltd (TISC.BO / TATA IN) 56

Titan Company Ltd (TITN.BO) 58

Voltas (VOLT.BO / VOLT IN) 60

Tata Consultancy Services (TCS.BO / TCS IN) 62

Tata Power (NOT COVERED) 64

Tata Communications (NOT COVERED) 65

Tata Chemicals (NOT COVERED) 66

Indian Hotels (NOT COVERED) 67

Tata Global Beverages (NOT COVERED) 68

Trent Ltd (NOT COVERED) 69

Tata AIA Life Insurance (Not Listed) 70

Appendix: HOLT Analysis 71

13 July 2017

Tata Group 6

Largest Indian conglomerate but areas to improve Started in 1868, the Tata Group had a total revenue of over US$100 bn in FY16 and an

employee base of over 660,000, with presence in several sectors of the Indian economy.

While the Group has close to 100 operating companies (including subsidiaries), the top-

ten and top-20 companies (by revenue, including subsidiaries) of the Group account for

94% and 99% of Group revenue, 98% and 99% of Group PAT and 94% and 99% of the

Group's gross fixed assets (excluding goodwill and intangibles), respectively.

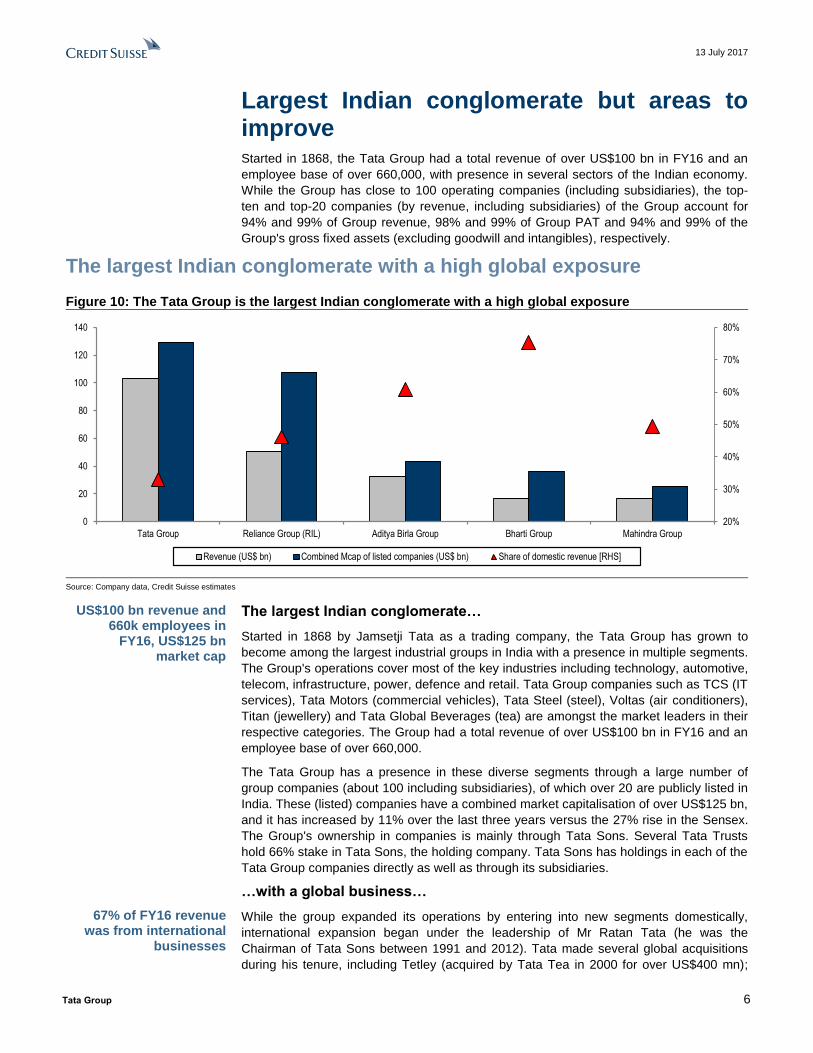

The largest Indian conglomerate with a high global exposure

Figure 10: The Tata Group is the largest Indian conglomerate with a high global exposure

Source: Company data, Credit Suisse estimates

The largest Indian conglomerate…

Started in 1868 by Jamsetji Tata as a trading company, the Tata Group has grown to

become among the largest industrial groups in India with a presence in multiple segments.

The Group's operations cover most of the key industries including technology, automotive,

telecom, infrastructure, power, defence and retail. Tata Group companies such as TCS (IT

services), Tata Motors (commercial vehicles), Tata Steel (steel), Voltas (air conditioners),

Titan (jewellery) and Tata Global Beverages (tea) are amongst the market leaders in their

respective categories. The Group had a total revenue of over US$100 bn in FY16 and an

employee base of over 660,000.

The Tata Group has a presence in these diverse segments through a large number of

group companies (about 100 including subsidiaries), of which over 20 are publicly listed in

India. These (listed) companies have a combined market capitalisation of over US$125 bn,

and it has increased by 11% over the last three years versus the 27% rise in the Sensex.

The Group's ownership in companies is mainly through Tata Sons. Several Tata Trusts

hold 66% stake in Tata Sons, the holding company. Tata Sons has holdings in each of the

Tata Group companies directly as well as through its subsidiaries.

…with a global business…

While the group expanded its operations by entering into new segments domestically,

international expansion began under the leadership of Mr Ratan Tata (he was the

Chairman of Tata Sons between 1991 and 2012). Tata made several global acquisitions

during his tenure, including Tetley (acquired by Tata Tea in 2000 for over US$400 mn);

20%

30%

40%

50%

60%

70%

80%

0

20

40

60

80

100

120

140

Tata Group Reliance Group (RIL) Aditya Birla Group Bharti Group Mahindra Group

Revenue (US$ bn) Combined Mcap of listed companies (US$ bn) Share of domestic revenue [RHS]

US$100 bn revenue and 660k employees in

FY16, US$125 bn market cap

67% of FY16 revenue was from international

businesses

13 July 2017

Tata Group 7

Glaceau (30% stake acquired by Tata Tea in 2006 for over US$670 mn, though sold later);

Corus (acquired by Tata Steel in 2006 for over US$8 bn); and Jaguar Land Rover

(acquired in 2008 for about US$2.3 bn). Besides these, the IT services business, TCS,

was growing at a brisk pace, further expanding the Tata Group's global revenue base.

About 67% of the Group's revenue came from international businesses in FY16.

…and significant focus on corporate social responsibility

The Group has had a significant focus on ethics and corporate social responsibility (CSR)

since the very beginning. For example, Tata Steel introduced eight-hour working days well

before it became a statutory requirement in most of the Western world, and it also started

the provident fund scheme in 1920, much before the government regulations came (in

1952). Many of the companies in the group continue to be perceived as better places to

work by employees.

A professional leader for the first time at the helm

Historically, the Tata Group has been led by family members of the owners of Tata Sons

(66% owned by Tata Trusts and 18% owned by Shapoorji Pallonji). The first five Chairmen

were from the Tata family (Mr. Jamsetji Tata, followed by Mr. Dorab Tata, Mr. Saklatwala,

Mr. JRD Tata and Mr. Ratan Tata), and the last Chairman (Mr. Cyrus Mistry) was from the

Shapoorji Pallonji family. Mr. N Chandrasekaran (appointed as the Chairman effective

January 2017) is the first professional Chairman of the Group and has a distinguished

track record of leading the most valuable (by market capitalisation) company of the group

(TCS) for seven years.

Figure 11: Tata Group—overview of companies in the manufacturing domain

Source: Company data, MCA, Capitaline,Thomson Reuters, Credit Suisse

Auto

Others

Steel

Auto

Didn't include

Others

Others

Steel

Steel

Didn't include

Didn't include

Steel

Didn't include

Steel

Steel

Steel

Manufacturing

Auto and auto components Steel and Steel products Others

Tata Pigments(100% subsidiary of Tata Steel)

Pigments, paintsRev (FY16): Rs 1.1 bnPAT (FY16): Rs 0.1 bn

Net debt (FY16): Rs -0.1 bnROE (FY16): 15%

Tata MotorsPassenger & commercial vehicles

Mcap : US$ 20,183 mnRev (FY17): Rs 2,745 bnPAT (FY17): Rs 102 bn

Net debt (FY17): Rs 425 bnROE (FY17): 15%

Jaguar Land Rover(100% subsidiary of Tata Motors)

Passanger vehiclesRev (FY17): Rs 2.1 tn

PAT (FY17): Rs 105 bn

Net debt (FY17): Rs -170 bnROE (FY17): NA

Tata Daewoo Comm Vehicle(100% subsidiary of Tata Motors)

M&HCV, S KoreaRev: Rs 48 bnPAT: Rs 3 bn

Net debt: NAROE: 15%

Tata Autocomps Limited(26%, Tata Motors)Auto components

Rev (FY16): Rs 8.3 bnPAT (FY16): Rs 0.1 bn

Net debt (FY16): Rs -2.9 bnROE (FY16): 2%

Tata Cummins(50% JV, Tata Motors)

Auto componentsRev (FY15): Rs 25 bnPAT (FY15): Rs 0.5 bn

Net debt (FY15): Rs 3.5 bnROE (FY15): 7%

Tata Metaliks (50% subs of Tata

Steel)Pig and ductile iron pipes

Mcap: US$ 285 mnRev (FY17): Rs 14 bn

PAT (FY17): Rs 1.2 bnNet debt (FY17): Rs 3.1 bn

ROE (FY17): 58% *

Tata SteelDiversified steel producer

Mcap: US$ 7,680 mnRev (FY17): Rs 1,174 bn

PAT (FY17): Rs 38 bn

Net debt (FY17): Rs 724 bnROE (FY17): 9%

Indian Steel and Wire Products

(95% subsidiary of Tata Steel)Wire and steel roll

Rev: Rs 2.3 bn

PAT: Rs 0.1 bnNet debt: Rs 0.2 bn

ROE: 10%

Tata Sponge Iron (55% subsidiary of Tata Steel)

Sponge ironMcap: US$ 197 mn

Rev (FY17): Rs 6.2 bn

PAT (FY17): Rs 0.6 bnNet debt (FY17): Rs -5.7 bn

ROE (FY17): 7%

TRL Krosaki Refractories(27%, Tata Steel)

RefractoriesRev (FY16): Rs 9.9 bnPAT (FY16): Rs 0.0 bn

Net debt (FY16): Rs 1.8 bnROE (FY16): 1%

Tinplate Company of India(75% subsidiary of Tata Steel)

TinplateRev (FY16): Rs 8.3 bnPAT (FY16): Rs 0.7 bn

Net debt (FY16): Rs -0.1 bnROE (FY16): 13%

JAMIPOL(40%, Tata Steel)

De-sulphurising compounds for steel

Rev (FY16): Rs 2.6 bn

PAT (FY16): Rs 0.2 bnNet debt (FY16): Rs -0.5 bn

ROE (FY16): 19%

Tata BlueScope Steel(50% JV, Tata Steel)

Coated steelRev (FY16): Rs 15.1 bnPAT (FY16): Rs 0.3 bn

Net debt (FY16): Rs 8.2 bnROE (FY16): 12%

Jamshedpur Continuous Annealing and Processing

(JV, Tata Steel)Annealed products

Rev (FY16): Rs 1.9 bn

PAT (FY16): Rs -2.2 bnNet debt (FY16): Rs 15.6 bn

ROE (FY16): NA

Rallis IndiaAgro chemical

Mcap (FY17): US$ 748 mnRev (FY17): Rs 17.8 bn

PAT (FY17): Rs 3 bn

Net debt (FY17): Rs -1.9 bnROE (FY17): 30%

Tata ChemicalsChemicals, pulses, saltMcap: US$ 2,442 mn

Rev (FY17): Rs 133 bnPAT (FY17): Rs 9.9 bn

Net debt (FY17): Rs 32.2 bnROE (FY17): 14%

Tata Hitachi Construction(40%, Tata Motors)Heavy equipments

Rev (FY16): Rs 22.5 bnPAT (FY16): Rs -3.4 bn

Net debt (FY16): Rs 8 bnROE (FY16): NA

Tata Petrodyne(100%, Tata Sons)

Upstream oil and gasRev (FY15): Rs 1.1 bnPAT (FY15): Rs 0.5 bn

Net debt (FY15): Rs -2.9 bnROE (FY15): 14%

Advinus Therapeutic(Tata Group)

Contract research - pharmaRev (FY16): Rs 1.6 bnPAT (FY15): Rs 0.1 bn

Net debt (FY15): Rs 3.2 bnROE: NA

Tata Ceramics(57%, Tata Power)

TablewareRev (FY15): Rs 0.5 bnPAT (FY15): Rs 0 bn

Net debt (FY15): Rs 0.1 bnROE: NA

Tayo Rolls (55% subs of Tata

Steel)Cast anf forged steel rolls

Mcap: US$ 10 mnRev (FY16): Rs 1.3 bn

PAT (FY16): Rs -1.6 bnNet debt (FY16): Rs 1.2 bn

ROE : NA

N Chandrasekaran is the first "professional" Chairman of the Group

13 July 2017

Tata Group 8

Figure 12: Tata Group—overview of companies in IT, telecom and services domains

Note: ^ Taken from FY17 BSE filing * Business Standard. Source: Company data, MCA, Capitaline,Thomson Reuters, Credit Suisse research

Figure 13: Tata Group—overview of companies in power, engineering and defence domains

Source: Company data, MCA, Capitaline,Thomson Reuters, Credit Suisse research

Not included

Revenue

PBT

IT, telecom and services

Other servicesIT/Engg services/BPO/consulting Telecom and allied

Tata International(Tata Sons and Industries)

TradingRev (FY16): Rs 130.5 bnPAT (FY16): Rs -0.5 bn

Net debt (FY16): Rs 18.4 bnROE (FY16): NA

Tata Elxsi Engineering services, VFX

Mcap: US$ 744 mnRev (FY17): Rs 12.3 bnPAT (FY17): Rs 1.7 bn

Net debt (FY17): Rs -2.5 bnROE (FY17): 37%

Tata Consultancy ServicesDiversified IT servicesMcap: US$ 73,018 mn

Rev (FY17): Rs 1,180 bnPAT (FY17): Rs 263 bn

Net debt (FY17): Rs -495 bnROE (FY17): 33%

Tata Business SupportServices

(100% subsidiary of Tata Sons)BPO

Rev (FY15): Rs 6 bn

PAT (FY15): Rs 0.2 bnNet debt (FY15): Rs 0.6 bn

ROE (FY15): 15%

Tata Strategic Management(Tata Industries)

Management consultingRev: NAPAT: NA

Net debt: NAROE: NA

Tata Technologies(72% subsidiary of Tata Motors)

Engineering servicesRev (FY16): Rs 10.8 bnPAT (FY16): Rs 2.2 bn

Net debt (FY16): Rs -0.5 bnROE (FY16): 37%

Indian HotelsHotels

Mcap (FY17): US$ 1,959 mnRev (FY17): Rs 40 bn

PAT (FY17): Rs -0.6 bn

Net debt (FY17): Rs 24.7 bnROE (FY17): NA

Taj Air(Associate, Tata Sons)

Aircraft charterRev (FY15): Rs 0.7 bnPAT (FY15): Rs -0.2 bn

Net debt (FY15): Rs -0.7 bnROE (FY15): NA

TKM Global Logistics(100% subsidiary, Tata Steel)

Logistics and supply chainRev (FY15): Rs 0.6 bnPAT (FY15): Rs 0.0 bn

Net debt (FY15): Rs 0.0 bnROE (FY15): 4%

Tata Interactive Learning(Division of Tata Industries)

Interactive learningRev: NAPAT: NA

Net debt: NAROE: NA

Tata Class Edge(Division of Tata Industries)

Smart classRev: NAPAT: NA

Net debt: NAROE: NA

Tata Teleservices Maharashtra(63%, collectively held by several

Tata Group companies)Mcap: US$ 195 mn

Rev (FY17): Rs 27 bn

PAT (FY17): Rs -24 bnNet debt (FY17): Rs 136 bn ^

ROE (FY17): NA

Tata Teleservices(59%, collectively held by several

Tata Group companies)Telecom

Rev (FY16): Rs 143 bn

PAT (FY16): Rs -30 bnNet debt (FY16): Rs 336 bn

ROE (FY16): NA

Tata CommunicationsTelecom solutions and network

servicesMcap: US$ 3,330 mn

Rev (FY17): Rs 176 bn

PAT (FY17): Rs -7.7 bnNet debt (FY17): Rs 66 bn

ROE (FY17): NA

NelcoVSAT, security, managed services

Mcap: US$ 29 mnRev (FY17): Rs 1.4 bnPAT (FY17): Rs 0.1 bn

Net debt (FY17): Rs 0.6 bnROE (FY17): 33%

Tata SIA Airlines (Vistara)(51% JV, Tata Industries)

AirlineRev (FY16): Rs.7.1 bn*PAT (FY16): Rs.-4 bn*

Net debt: NAROE: NA

mjunction services50% subsidiary of Tata Steel

B2B ecommerce for steelRev : Rs.1.3 bnPAT : Rs.0.3 bn

Net debt : Rs.-1.6 bnROE: 19%

Air Asia(40% JV, Tata Industries)

AirlineRev (CY16): Rs.8.3 bn

PBT (CY16): Rs.-1.4 bn

Net debt: NAROE: NA

Tata SkyJV, Tata Sons

D2H television servicesRev (FY16): Rs 44.7 bnPAT (FY16): Rs 0.8 bn

Net debt (FY16): Rs 20.8 bnROE (FY16): NA

Housing/others

Power, engineering, defense, others

Power Engineering/infra Defence

Tata Advanced Materials(100% subsidiary of Tata Sons)

Advanced composites and armoured products

Rev (FY16): Rs 1.3 bn

PAT (FY16): Rs -0.3 bnNet debt (FY16): Rs 1.3 bn

ROE (FY16): NA

Tata PowerIntegrated power company

Mcap: US$ 3,261 mnRev (FY17): Rs 279 bnPAT (FY17): Rs 14 bn

Net debt (FY17): Rs 468 bnROE (FY17): 11%

Tata Advanced Systems(100% subsidiary of Tata Sons)

National security and defenceRev (FY16): Rs 5.7 bnPAT (FY16): Rs 0.2 bn

Net debt (FY16): Rs 0.3 bnROE (FY16): 5%

Tata Power Trading100% subsidiary of Tata Power

Power tradingRev (FY16): Rs 59.4 bnPAT (FY16): Rs 0.2 bn

Net debt (FY16): NAROE (FY16): NA

TAL Manufacturing Solutions100% subsidiary of Tata Motors

DefenceRev (FY16): Rs 2.1 bnPAT (FY16): Rs -0.1 bn

Net debt (FY16): Rs 0.8 bnROE (FY16): NA

Powerlinks TransmissionJV, Tata Power

Power transmissionRev: Rs 2.3

PAT: 1.1

Net debt: 1.6ROE (FY16): 20%

Tata Realty and Infrastructure100% subsidiary of Tata SonsReal estate and infrastructure

Rev (FY16): Rs 0.6 bnPAT (FY16): Rs -0.1 bn

Net debt (FY16): Rs 7.8 bnROE (FY16): NA

Tata Industrial Services100% subsidiary of Tata Industries

Programme management for defence and aerospace

Rev: NA

PAT: NANet debt: NA

ROE: NA

Tata Power Solar100% subsidiary of Tata Power

Solar energyRev (FY16): Rs 14.9 bnPAT (FY16): Rs -0.3 bn

Net debt (FY16): NAROE (FY16): NA

Tata ProjectsTata Sons

InfrastructureRev (FY16): Rs 42.3 bnPAT (FY16): Rs 0.7 bn

Net debt (FY16): Rs 4.0 bnROE (FY16): 7%

Tata Consulting Engineers100% subsidiary of Tata Sons

Project engineeringRev (FY16): Rs 5.0 bnPAT (FY16): Rs 0.1 bn

Net debt (FY16): Rs 0.6 bnROE (FY16): 3%

TRFMaterial handling equipments

Mcap: US$ 40 mnRev (FY17): Rs 10.1 bnPAT (FY17): Rs -0.2 bn

Net debt (FY17): Rs 4.3 bnROE (FY17): NA

JUSCO(100% Subsidiary of Tata Sons)

Urban infrastructureRev: Rs NA

PAT: NA

Net debt: NAROE: NA

Tata Housing Development100% subsidiary of Tata Sons

HousingRev (FY15): Rs 5.8 bnPAT (FY15): Rs 0.2 bn

Net debt (FY16): Rs 17.3 bnROE (FY16): 1%

VoltasAC, engineering solutions

Mcap: US$ 2,532 mnRev (FY17): Rs 60.4 bnPAT (FY17): Rs 5.0 bn

Net debt (FY17): Rs -3.6 bnROE (FY17): 17%

13 July 2017

Tata Group 9

Figure 14: Tata Group—overview of companies in retail and financial services domains

Source: Company data, MCA, Capitaline,Thomson Reuters, Credit Suisse research

Figure 15: Tata Group—holding structure of the key companies

* Investing vehicle for the four Tata Group Companies as its principals viz. Tata Sons, Tata Power, Tata Iron & Steel Company and Tata Industries. Tata Power has 30% stake in Panatone Finvest. Source: BSE, Company data, Credit Suisse research

Retail, consumer, financial services

Financial servicesRetail/consumer

Tata Capital(Subsidiary of Tata Sons)

Diversified financial servicesRev (FY16): Rs 21.8 bnPAT (FY16): Rs 4.1 bn

Net debt (FY16): Rs 333 bnROE (FY16): 8%

Trent Fashion retail chainMcap: US$ 744 mn

Rev (FY17): Rs 18.3 bnPAT (FY17): Rs 0.8 bn

Net debt (FY17): Rs 1.6 bnROE (FY17): 6%

Titan CompanyWatches, jewellery

Mcap: US$ 7,185 mnRev (FY17): Rs 131 bnPAT (FY17): Rs 7 bn

Net debt (FY17): Rs -12 bnROE (FY17): 18%

Tata Coffee (57% sub of Tata

Global Beverages)Coffee producer and exporter

Mcap: US$ 376 mnRev (FY17): Rs 16 bn

PAT (FY17): Rs 1.5 bnNet debt (FY17): Rs 6.2 bn

ROE (FY17): 15%

Tata Investment Corporation (TICL)

Investment companyMcap (FY17): US$ 605 mn

Rev (FY17): Rs 2.5 bn

PAT (FY17): Rs 1.9 bnNet debt (FY17): Rs 24.7 bn

ROE (FY17): 8%

Tata AIG General Insurance(JV, Tata Sons)

General insurance ventureRev (FY16): Rs 2.7 bnPAT (FY16): Rs 0.2 bn

Net debt (FY16): Rs -39 bnROE (FY16): 2%

Infiniti retail100% subsidiary of Tata Sons

Electronics retailRev (FY16): Rs 29.2 bnPAT (FY16): Rs -2 bn

Net debt (FY16): Rs 4.4 bnROE (FY16): NA

Tata Asset Management(68% Tata Sons, 32% TICL)

Asset managementRev (FY16) : Rs 1.4 bnPAT (FY16): Rs 0.1 bn

Net debt (FY16): Rs 0.0 bnROE (FY16): 0%

Tata AIA Life Insurance(JV, Tata Sons)

Life insuarance ventureRev (FY16): Rs 2.7 bnPAT (FY16): Rs 0.6 bn

Net debt (FY16): Rs -20 bnROE (FY16): 3%

Tata Global BeveragesNon alchoholic beverages

Mcap: US$ 1,532 mnRev (FY17): Rs 68 bnPAT (FY17): Rs 3.9 bn

Net debt (FY17): Rs 0.3 bnROE (FY17): 6%

Tata Unistore (Tata CliQ)Unit of Tata IndustriesE-commerce platform

Rev: Rs NAPAT: NA

Net debt: NAROE: NA

Casa DécorJV, Tata Group

Luxury furnishingRev (FY16): Rs 0.1 bnPAT (FY16): Rs -0.1 bn

Net debt (FY16): Rs 0.1 bnROE (FY16): NA

Tata Motor Finance(100% Subsidiary of Tata Motors)

Vehicle financingRev (FY16): Rs 12.9 bnPAT (FY16): Rs 1.0 bn

Net debt (FY16): Rs 130 bnROE (FY16): 3%

31.6

Tata Sons Tata Industries

Promoter entities

Tata Trusts66%

Shapoorji Pallonji: ~18%

Tata Steel

Tata Motors

Tata

Communication

Tata Elxsi

Tata Tele

Tata Tele

(Maharashtra)

Tata Global

Beverages

Tata Coffee

Titan

Trent

Rallis

Tata Chemical

Tata Power

Voltas

Indian Hotel

TCS

Nelco

Tata Investment

Corp

73.3% 68.1%

26.6%

3% 2.4%42.2%

19.4%

4.4%

6%

50%

23.5%

4.4%7.1%

57.5%

30%

31.6%

0.4%

0.4%2.5%

0.5%

31%

1.5%

48.6%

27.7%

4.6%

20.8%

1.6%

2%

28%

1.4%

Tata Trusts: 8%

14%

4.7%Panatone

Finv est: 30% *

19.6%

7%

36.5%

36.2%5.5%

9.3%

7%

NTT Docomo: 26.5%

13 July 2017

Tata Group 10

Delving deeper into the Group's financials

The Tata Group companies are a mixed bag. While the Tata Group has close to 100

operating companies (including subsidiaries), a few of them account for a major part of the

Group's revenue, PAT and market cap. For example, the top-ten and top-20 companies

(by revenue and including subsidiaries) account for 94% and 99% of Group revenue, 98%

and 99% of Group PAT and 94% and 99% of the Group's gross fixed assets (excluding

goodwill and intangibles), respectively. Tata Steel, Tata Motors, Tata Power and Tata

Teleservices are the most significant contributors to the Group's net debt, and together,

accounted for over 90% of the Group's net debt (as per our estimates) in FY16. TCS

accounts for 85-90% of the total dividend received by the parent. About 60% of the

companies for which we have data have a ROE of less than 10%. There is a long tail of

companies within the Group which are quite small.

Financial health check of key companies

TCS has been a consistent performer for the Group—profits have been growing

consistently, cash generation has been decent and it is the most significant source of cash

for the Group (we estimate that dividends from TCS would have accounted for 85-90% of

the total dividend inflow for the Tata Group in FY16). TCS' ROE contracted over FY15-17,

but it was partly because of the cash accumulation in the balance sheet.

Tata Steel's revenue declined by Rs113 bn over FY15-17, but despite that, its profits have

increased by Rs37 bn. Net debt/EBITDA has come down from 8.8x in FY16 to 4.3x in

FY17. While it has generated positive free cash for two consecutive years, the cash

generation has been insufficient to meet the finance cost. ROE has improved, but it still

remains at single-digit levels (9% in FY17).

Tata Motors' revenue has grown over FY15-17 (incremental revenue of Rs92 bn), but

profits have declined in both FY16 and FY17 (Rs59 bn decline over FY15-17). Net

debt/EBITDA is comfortable at 1.4x. While Tata Motors' free cash generation has been

slightly volatile over the last three years (FY14-16), its free cash generation over the last

three years (on a cumulative basis) has been higher than the cumulative finance cost.

ROE has been declining—it has come down from 23% in FY15 to about 15% in FY17.

Tata Power had a Rs21 bn revenue increase over FY15-17 and its profits increased by

Rs12 bn. However, net debt/EBITDA remains high at 8x in FY17 (increased from 5x in

FY16). It has shown a consistent improvement in free cash generation, and in FY16, its

free cash flow was higher than the finance cost. ROE has been improving, but it is still at

the mid-single digit level.

Highly leveraged companies and the cash guzzlers

Companies such as Tata Tele, Tata Tele Maharashtra, Tata Housing and Tata

International have high leverage, with a very high net debt/EBITDA—11x (FY16), 21x

(FY17, 13x in FY16), 63x (FY16), and 43x (FY16), respectively. Tata Tele Maharashtra's

leverage increased significantly in FY17. Companies such as Tata Housing, Infiniti Retail

(Croma) and Trent have been consistently generating negative free cash flows based on

historical data. Tata International and Tata Projects' cash flows showed an improving trend

over FY14-16; however, they were still generating negative free cash in FY16.

A long tail

There are several companies in the Group that are very small in the context of Tata

Group's overall size. Tata Petrodyne and Tata Realty Infrastructure have high asset

intensity and low profitability based on FY16 financials. Similarly, Tata Pigments, Tata

Ceramics, Tata Décor and Tata UniStore (e-commerce) are small players in the industry

they operate in based on reported revenue in FY16.

About 60% of the companies for which we have data have an ROE of less than 10%

13 July 2017

Tata Group 11

Concentration with a few companies

While the Tata Group has close to 100 operating companies, including subsidiaries, a

handful account for a large proportion of the aggregate revenue, PAT and market

capitalisation. For example, the three largest companies of the Group—TCS, Tata Motors

and Tata Steel account for 56%, 16% and 7% of the Group market cap, 17%/43%/17% of

the Group revenue and 63%/34%/2% of the Group PAT, respectively. Together, these

three companies account for 79% of the Group market capitalisation, 77% of the Group

revenue and 100% of the Group PAT (some of the other companies are loss making). If

we go down a level further, the top-ten companies (by revenue and inclusive of

subsidiaries) account for 93% of the Group’s market capitalisation, 94% of its revenue and

98% of PAT.

Figure 16: High level of concentration

Source: Company data, MCA, Capitaline, Credit Suisse research

Improvement in profitability for Tata Steel, consistent performance for TCS, deterioration for Tata Motors

Among the top companies of the Tata Group, there has been divergence in revenue and

PAT performance over the last two years. For example, while Tata Motors has grown its

revenue over FY15-17 (incremental revenue of over Rs92 bn), the profits have declined

for both FY16 and FY17 (Rs59 bn decline over FY15-17). On the other hand, Tata Steel

1%

6%

2%

3%

3%

6%

57%

16%

1%

2%

2%

2%

2%

3%

5%

17%

17%

43%

0%

2%

0%

-8%

2%

1%

2%

2%

63%

34%

-20% -10% 0% 10% 20% 30% 40% 50% 60% 70%

Tata Global Beverages

Titan Company

Tata International

Tata Teleservices

Tata Chemicals

Tata communications

Tata Power

Tata Steel

TCS

Tata Motors

PAT share (FY16) Revenue share (FY16) Market cap share

79%

93%

77%

94%

99%

98%

0% 20% 40% 60% 80% 100% 120%

Total top-3

Total top-10

PAT share (FY16) Revenue share (FY16) Market cap share

TCS, Tata Motors, Tata Steel contribute 77% of

the Group's revenue and 79% of market cap

13 July 2017

Tata Group 12

had a net revenue decline of Rs113 bn over FY15-17, but despite that, its profits have

increased by Rs37 bn. For Tata Power, revenue increased by Rs21 bn and the profits

improved by Rs13 bn over FY15-17.

TCS has been a consistent performer for the Group—its revenue has increased by over

Rs230 bn over FY15-17 and PAT has increased by Rs66 bn. Tata Communications made

losses in FY17 (Rs8 bn) from close to break-even in FY15. Tata Tele's revenue declined

by Rs9 bn and losses increased by Rs11 bn over FY15-17.

Figure 17: Change in the revenue and profits of the key companies over the last two years

Note: For FY16 change, we have considered the IGAAP numbers, while for FY17 changes, we have used Ind AS numbers. Used IFRS numbers for TCS. Source: Company data, Credit Suisse research

Net debt/EBITDA stable-to-improving for Tata Steel and Tata Motors

Tata Steel, Tata Motors, Tata Power and Tata Teleservices are the most significant

companies in terms of net debt, and the first three have accounted for over 90% of the

Group's net debt (as per reported numbers) in the past. For Tata Steel and Tata Motors,

the leverage (net debt/EBITDA) was at a comfortable level (4.3x and 1.4x, respectively, in

FY17), and indeed, it has come down from 8.8x in FY16 to 4.3x in FY17 for Tata Steel.

Tata Power, on the other hand, has witnessed an increase in leverage (it increased from

5x in FY16 to 8x in FY17). Tata Power accounts for 16-20% of the Group's net debt.

Companies such as Tata Tele, Tata Tele Maharashtra, Tata Housing and Tata

International have high leverage, with significantly higher net debt/EBITDA—11x (FY16),

21x (FY17, 13x in FY16), 63x (FY16), and 43x (FY16), respectively.

-300 -200 -100 0 100 200 300

TCS

Tata Motors

Tata Power

Titan Company

Voltas

Indian Hotels

Tata Communications

Tata Tele

Tata Chemicals

Tata Steel

Change in revenue (Rs bn)

FY15-17 FY17 FY16

-60 -40 -20 0 20 40 60 80

TCS

Tata Steel

Tata Power

Indian Hotels

Tata Chemicals

Voltas

Titan Company

Tata Tele

Tata Communications

Tata Motors

Change in PAT (Rs bn)

FY15-17 FY17 FY16

13 July 2017

Tata Group 13

Figure 18: Net debt to EBITDA stable-to-improving for Tata Steel and Tata Motors

Source: Company data, Credit Suisse research

Only four companies of the top-ten have a 15%+ ROE

Only four companies out of the top-ten companies have ROE in excess of 15%—these are

TCS (33% in FY17), Tata Motors (15%), Voltas (17%) and Titan (18%). While Tata Power

(>10%, adjusting for one-off charges) and Tata Steel (9%) have shown some improvement

in FY17, their ROE remains low. Indian Hotels and Tata Global Beverages' ROE stands at

-2% and 6%, respectively.

Among the companies that have witnessed the most significant improvement are Rallis

India and Nelco, as per reported numbers. Rallis' ROE improved from 21% in FY15 to

30% in FY17 and Nelco's from low single-digit levels to over 30% in FY17—besides

operational improvement, this was also helped by higher other income to some extent and

absence of losses from the discontinued operations, as per the reported financials.

Companies such as TCS, Tata Motors, Trent, Titan, Tata Elxsi and the insurance units

(Tata AIA and Tata AIG) witnessed a contraction in ROE. Tata Motors' ROE came down

from 23% in FY15 to 15% in FY17, and Titan's ROE contracted from 29% in FY15 to 18%

in FY17. For TCS, cash accumulation may have been one key reason.

0

10

20

30

40

50

60

70

0

100

200

300

400

500

600

700

800

Tata Steel Tata Motors Tata Power Tata Tele Tatacommunications

Tata Tele(Maharashtra)

Tata Chemicals Indian Hotels Tata Housing TataInternational

Net debt (FY16, Rs bn) Net debt (FY17, Rs bn) Net debt/EBITDA (FY16), RHS Net debt/EBITDA (FY17), RHS

13 July 2017

Tata Group 14

Figure 19: Several companies with sub-optimal ROEs

Source: Company data, Credit Suisse research

TCS remains the cash cow, cash generation improved in Tata Steel

In terms of free cash generation, TCS, being an extremely profitable company and an

asset light business, continues to be the cash cow for the Tata Group—its free cash flow

has been increasing over the last three years. Tata Power has shown a consistent

improvement in free cash generation, and in FY16, its free cash flow was higher than its

finance cost.

Tata Steel too has generated positive free cash for two consecutive years, but it has been

insufficient to meet the finance cost. Similarly, Tata Teleservices generates positive free

cash flow; however, it has not been sufficient to pay its finance costs in the past.

While Tata Motors' free cash generation has been slightly volatile over the last three years

(FY14-16), its free cash generation over the last three years (on a cumulative basis) has

been higher than the cumulative finance cost.

Companies such as Tata Housing, Infiniti Retail (Croma) and Trent have been consistently

generating negative free cash. Tata International and Tata Projects' cash flow showed an

improving trend over FY14-16; however, they were still generating negative free cash in

FY16 and also had a relatively higher leverage (and a correspondingly higher finance

cost).

18%

18%

-20% -10% 0% 10% 20% 30% 40% 50%

Tata Elxsi

TCS

Nelco

Rallis India

Titan Company

Voltas

Tata Motors

Tata Coffee

Tata Chemicals

Tata Steel

Tata Projects

Tata Capital

Tata Sponge Iron

Tata AutoComps

Tata Power

Trent

Tata AIA Life Insurance

Tata AIG General Insurance

Tata Global Beverages

Tata Housing

Tata International

Indian Hotels

Listed companies

Total group

FY17 FY16 FY15

13 July 2017

Tata Group 15

Figure 20: Top-five free cash generating companies in the Tata Group

Rs bn Free cash flow Finance cost

FY14 FY15 FY16 FY17 FY14 FY15 FY16 FY17

TCS 124 181 189 250 0 0 0 0

Tata Motors 92 36 65 47 49 49 42

Tata Power 21 25 58 34 37 32 31

Tata Teleservices 15 29 35 35 30 33

Tata Chemicals 16 7 10 6 5 5 4

Tata Steel -33 -16 5 25 43 48 41 52

Source: Company data, Credit Suisse research

Figure 21: Companies with weak cash generation profile

Rs bn Free cash flow Finance cost

FY14 FY15 FY16 FY17 FY14 FY15 FY16 FY17

Tata International -11.4 -2.6 -0.1 NA 1.6 1.8 2.1 NA

Tata Projects -1.7 -1.4 -0.4 NA 0.4 0.8 1.0 NA

Trent -1.8 -1.7 -0.5 0.3 0.1 0.1 0.4 0.3

Tata Global Beverages 2.2 2.4 -0.5 NA 0.9 0.8 1.2 NA

Infiniti Retail -0.3 -0.2 -0.7 NA 0.5 0.5 0.5 NA

Tata Housing -5.1 -10.7 NA 0.4 0.4 0.6 NA

Source: Company data, Credit Suisse research

■ TCS remains the single largest source of cash for the Group. TCS remains the

single largest source of dividend for the Tata Group—TCS had over 65% share in the

Group's aggregate PAT in FY16, Tata Group has the largest ownership in TCS (73%)

and the average payout historically has been above 40%. Our estimates suggest that

dividends from TCS would have accounted for 85-90% of the total dividend inflow for

Tata Group (from the Group companies, including the cross holdings of the Group

companies) in FY16.

All the other larger companies (Tata Steel, Tata Motors, Tata Power) are capital

intensive and are generating free cash that is either lower than the finance costs or not

significantly higher than it, there is little scope of any significant increase in dividend for

these companies in the near term, although this will be one focus area for new

management. Other companies are much smaller in size, and any increase in dividend

payout there would not change things meaningfully for the Group.

■ Further scope to increase the payout. The last five years' average dividend payout

for TCS has been 42% (excluding dividend tax), and including the recent buy-back of

Rs160 bn, the average payout ratio has been 58%. IT services companies have

accumulated significant cash in their balance sheet and there is an increasing

shareholder demand for a higher dividend payout. With a decent cash generation (PAT

to FCF conversion of over 80%) and over US$4.5 bn of cash in its books as on March

2017 (adjusting for the buyback), there is enough scope to increase the payout, and

this is being actively considered by the Board.

We estimate TCS accounts for 85-90% of

the total dividend inflow for the Group

13 July 2017

Tata Group 16

Figure 22: TCS' payout (dividend and buy back) history

Note: There was a special dividend paid in FY15. Source: Company data, Credit Suisse research.

A long list of tail companies lacking scale and strategic synergies

There are several companies in the Group that are very small in the context of Tata

Group's overall size and also lack scale to be a significant player in the industry they

operate in. For example, companies such as Tata Petrodyne and Tata Realty

Infrastructure have high asset intensity and low profitability based on FY16 financials (Tata

Realty made a net loss of Rs60 mn in FY16, with gross assets of close to Rs19 bn).

Similarly, Tata Pigments, Tata Ceramics (tableware), Tata Décor (luxury furnishing) and

Tata UniStore (e-commerce) are smaller players in the industry they operate based on

FY16 revenue.

31% 33%

79%

35% 35%

96%

42%

58%

0%

20%

40%

60%

80%

100%

120%

FY13 FY14 FY15 FY16 FY17 (exclbuyback)

FY17 (inclbuyback)

5 year average(excl the recent

buyback)

5 year average(incl the recent

buyback)

Payout (excluding dividend tax)

13 July 2017

Tata Group 17

Figure 23: Non top-ten companies (in terms of revenue, FY16 financials)*

Companies Segment/sector Revenue PAT Net debt Gross fixed assets ^

Voltas Air conditioners, engineering solutions 57.5 3.87 -5.8 5.2

Tata Sky D2H television 44.7 0.77 20.8 75.5

Tata Projects Infrastructure 42.4 0.67 4.3 5.7

Indian Hotels Hotels 40.2 -2.31 40.0 99.4

Tata Teleservices (Maharashtra) Telecom 29.7 -3.58 100.0 53.2

Infiniti Retail (Croma) Electronics retail 29.2 -1.97 4.4 1.3

Tata Capital Diversified financial services 21.8 4.05 331.5 1.5

Tata AutoComps Auto components 21.2 0.52 -2.2 5.3

Rallis India Agro chemicals 16.3 1.43 0.6 4.3

Trent Fashion retail chain 15.9 0.55 0.5 10.1

Tata Coffee Coffee producer and exporter 15.5 0.83 7.9 8.1

Tata Metaliks Pig and ductile iron pipes 13.0 1.23 2.1 5.7

TRF Material handling equipment 11.2 -0.36 5.1 2.2

Tata Housing Housing 10.9 -0.04 39.3 0.5

Tata Technologies Engineering services 10.8 2.23 -0.5 4.6

Tata Elxsi Engineering services 10.8 1.55 -1.8 2.1

Tata Sponge Iron Sponge iron 6.3 0.32 -5.4 4.0

Tata Business Support Services BPO 6.0^^ 0.19^^ 0.6^^ 2.1^^

Tata AIA Life Insurance Life insurance venture 2.7 0.64 -20.0 NA

Nelco VSAT, security and allied services 2.0 0.01 0.3 1.1

Tata Advanced Systems National security and defence 1.7 0.07 0.3 3.5

Advinus Therapeutics Contract research – pharma 1.6 0.07^^ 3.2^^ 1.7^^

Tata Asset Management Asset management 1.4 0.06 0.0 0.3

Roots Corporation Budget hotel (Ginger) 1.4 -0.11 0.9 4.0

mjunction services B2B E-commerce for steel 1.3 0.28 -1.6 1.2

Tata Advanced Materials Advanced composites and armoured products 1.3 -0.32 1.3 2.2

Tata Petrodyne Upstream oil and gas 1.1^^ 0.47^^ -2.9^^ 6.8^^

Tata Pigments Pigments, paints 1.1 0.06 -0.1 0.3

TKM Global Logistics Logistics and supply chain 0.6 0.03 0.0 0.1

Tata Realty and Infrastructure Real estate and infrastructure 0.6 -0.06 10.8 18.8

Tata Ceramics Tableware 0.5^^ 0.00^^ 0.1^^ 0.1^^

Tata AIG General Insurance General insurance 0.4 0.20 -39.3 2.4

Casa Décor Luxury furnishing 0.1 -0.06 0.1 0.0

Tata UniStore E-commerce platform (Tata CliQ) 0.0^^ -0.04^^ -0.5^^ NA

Top-10 as % of total 94% 98% 77% 94%

Top-20 as % of total 99% 99% 100% 99%

* Considered independent companies and subsidiaries/JVs/associates with a different business model than the parent. ^ excluding goodwill and intangibles. ^^ FY15 financials as FY16 financials were not available. Source: Company data, Capitaline, MCA, Credit Suisse research

Tata Group underperformed the market in the last

one and three years, led by TCS and Tata Motors

Overall, the aggregate market cap of the listed Tata Group companies has been flattish in

the last one year and up 11% over the last three vs 17% and 27% increase in the broader

market index, the Sensex. The top two companies of the Group—TCS (56% of the Group

market cap) and Tata Motors (16%)—have had a subdued performance over the last one

and three years. TCS' market cap is down 4% over the last one year and up just 1% over

the last three years. Tata Motors, on the other hand, is down 5% and up 9% over the last

one and three years, respectively. Tata Steel's (7% of the market cap) has done well in the

last one year (up 63%).

13 July 2017

Tata Group 18

Tata Metaliks (0.2% of the Group market cap), Tata Elxsi (0.6%), Voltas (2%), Trent (1%),

and Tata Communication (2.3%) have been the top performers over the last three years,

with their market cap up 994%, 192%, 155%, 103%, and 91%, respectively. Tata Tele

(Maharashtra) and Tata Power have seen the most market cap erosion over the last three

years (down 24% and 18%, respectively).

Figure 24: Tata Group companies—market cap movements

Market cap composition Change in market cap

Current 1 yr back 3 yrs back 1 year 3 years

TCS 56.3% 61.0% 61.7% -4% 1%

Tata Motors 16.1% 17.6% 16.3% -5% 9%

Tata Steel 6.5% 4.2% 6.5% 63% 12%

Titan Company 5.7% 4.5% 3.9% 31% 61%

Tata Power 2.7% 2.5% 3.7% 14% -18%

Tata Communications 2.3% 1.7% 1.3% 37% 91%

Voltas 1.9% 1.3% 0.8% 49% 155%

Tata Chemicals 2.0% 1.4% 1.1% 43% 100%

Indian Hotels 1.5% 1.6% 1.0% -4% 61%

Tata Global Beverages 1.3% 1.1% 1.2% 31% 18%

Trent 1.0% 0.7% 0.5% 37% 103%

Rallis India 0.6% 0.5% 0.5% 20% 20%

Tata Elxsi 0.6% 0.7% 0.2% 1% 192%

Tata Investment Corporation 0.5% 0.4% 0.4% 49% 45%

Tata Coffee 0.3% 0.3% 0.2% 27% 59%

Tata Metaliks 0.2% 0.1% 0.0% 111% 994%

Tata Tele (Maharashtra) 0.2% 0.2% 0.3% 6% -34%

Tata Sponge Iron 0.2% 0.1% 0.1% 35% 36%

Nelco 0.0% 0.0% 0.02% 6% 83%

TRF 0.0% 0.0% 0.0% -31% -12%

Tata Group aggregate 4% 11%

Sensex 17% 27%

Source: Thomson Reuters

13 July 2017

Tata Group 19

Renewed energy at the top The Tata Group constitutes one of the oldest, largest and most respected business groups

in India. While many of its group companies have done well over the years, there is

potential for some to improve. The track record of individual companies relative to peers

has also been mixed.

More recently, there was turmoil at the top level of the Group when the previous

Chairman, Cyrus Mistry, was ousted. After a search for a new Chairperson, N

Chandrasekaran (Chandra) was zeroed in on. He is an insider, having spent about 30

years at TCS and leading TCS since 2009. He took over as Chairman of Tata Sons in

January 2017 and has appointed some key personnel in various corporate functions.

Chandra has had a stellar track record at TCS and has led the company to a pole position

among its peers. We are optimistic that some of the relatively problematic areas for the

Tata Group can be solved in the next few years. Some of the recent developments (some

of these are likely to have been initiated by previous management) include:

■ Tata Steel signed a definitive agreement in February to sell its UK specialty steels

business to Liberty House Group for £100 mn.

■ TCS announced a Rs160 bn buy back (about US$2.5 bn), of which Tata Sons obtained

over Rs100 bn (about US$1.5 bn).

■ Tata Steel sold its stake in Tata Motors to Tata Sons for US$586 mn in June.

■ There have been cost cuts and organisational restructuring at Tata Motors.

■ Tata Sons has agreed to support the arbitration award to DoCoMo in relation to Tata

Teleservices.

■ There have been some management changes, such as Rakesh Sarna (CEO of Indian

Hotels), and the head of CV operations at Tata Motors, both have resigned due to

personal reasons, as indicated by the Group.

Five key mantras

Based on our understanding of the Group and the individual companies, and comments

made in the press, we believe new management's strategy will hinge on the following five

key objectives:

■ Improvement of return ratios, with focus on the "big guns". As mentioned earlier,

only four companies out of the top-ten companies have ROE in excess of 15%. The

main focus will be on the larger companies such as Tata Motors, Tata Power, Tata

Steel, and Tata Teleservices.

■ Domestic consumption. While international expansion was a big focus area until

2008, we believe that domestic consumption will be an important focus area for the

Group, going forward. Some of the important areas would include the consumer

business (Tata Global, parts of Tata Chemicals, Voltas) and financial services (Tata

Capital, insurance).

■ Simplicity in structure and holding. The Group consists of multiple companies that

operate, either fully or partially, in the same segments. There is a possibility of

consolidating some of these operations. Also, there are various intra-group holdings

and these can be simplified and consolidated at the Tata Sons level. This process may

also allow individual companies access to some funding, as long as the parent can

fund it, e.g., Tata Steel's recent sale of its stake in Tata Motors to the parent.

13 July 2017

Tata Group 20

■ Relevance. While the Group's presence in some segments is dominant, its presence in

others is not relevant. It also has sub-optimal presence in some large segments of the

economy such as financial services and retail/consumer (including e-commerce). It is

possible that the Group may either exit businesses where it is too small or consolidate,

wherever possible, to increase scale.

■ Digital initiatives across segments. Given the Group's presence in the technology

industry through TCS and others, Chandra's background and the increasing

implementation of digital initiatives by corporations, the Group may step up its digital

initiatives across its various businesses.

While quite a few of these objectives would have been in place even before the new team

took over, execution of this strategy will be key.

The following sections discuss various potential strategic imperatives within the above five

broader segments.

#1 Focus on the big guns

As discussed in the previous section, a handful of companies account for a significant

portion of the value (in terms of market capitalisation), revenue and debt. Some of the key

companies are—TCS, Tata Motors, Tata Steel, Tata Power and Tata Teleservices. Fixing

some of the key issues of these companies can essentially enhance the Group's value

significantly.

TCS: Little to be done

TCS has been the star performer for the Tata Group over the last several years. Its

absolute performance, both fundamental as well as in terms of market capitalisation has

been stellar, as has its performance relative to its peer group (despite being the largest

player among the peers by a margin). However, this performance has stagnated over the

last one year or so—the revenue growth has moderated from 15% levels, a couple of

years back to high single-digit in FY17. Margins are relatively resilient though (in the target

band of 26-28%) and remain at the industry leading levels.

Figure 25: TCS has outperformed the Sensex over

the last five years; stagnation in performance over

the last one year or so

Figure 26: Historically, TCS has grown ahead of the

industry, growth has suffered in the last few

quarters for TCS as well as the industry

Source: Thomson Reuters Source: Company data, Credit Suisse estimates

0

50

100

150

200

250

Jun-12 Dec-12 Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Jun-16 Dec-16

Prices indexed tto Jun-12

TCS Sensex

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Sep-12 Mar-13 Sep-13 Mar-14 Sep-14 Mar-15 Sep-15 Mar-16 Sep-16 Mar-17

Revenue growth (LTM, YoY, cc, organic)

TCS Top-5 Indian IT firms

Not all of these will be new strategies—

however, execution will be key

13 July 2017

Tata Group 21

Structural and cyclical factors behind recent slowdown in growth

The relatively slower growth over the last two years has been on account of some

structural and cyclical factors. On the structural front, commoditisation of traditional

services and cannibalisation of revenue on account of the cloud and automation have hurt.

Expectations of newer digital services making up for the shortfall have not played out fully

yet. Also, TCS' current scale will make it difficult to mirror the high growth rates of the past.

On the cyclical front, cautious spending by customers on new initiatives and the deferment

of discretionary projects have not helped. The sluggish performance of market

capitalisation over the last two years has been on account of a significant P/E derating.

Figure 27: The industry is going through several structural challenges

Source: Company data, Credit Suisse research

Things can potentially improve going forward

While the scale will inhibit high growth numbers, we expect some gradual improvement in

some of the structural issues, mainly in the ability of newer digital services in filling up the

shortfall caused by the deflation in legacy work.

Cyclical factors too can improve, and we expect some improvement in the next few

quarters, driven especially by financial services clients. With this, we believe growth can

pick up over the next two years from the level in FY17 but is unlikely to get back to the

15%+ levels. P/E could expand if growth rates pick up although it is unlikely, in our view, to

reach the high levels of the last five years.

1980 1990 2000 2010 2020

Y2K

Dotcom enabling

Consulting, testing, engg svcs

Package implementation

Infra management

Domain Knowledge

Consulting

Fixed price

Platforms

Automation

Mainframes

Client Server

Internet (Web)

ERP

Application development and maintenance

Digital, end-to-end engg services, platforms based offerings

Coding, T&M project management skills

Design, business consulting, AI, DevOps/Agile, outcome based

Cloud (as-a-service), IoT, mobilecomputing, Open Source

Capability additions

Technology additions

Services additions

13 July 2017

Tata Group 22

Figure 28: After a derating over the last couple of years (and rerating of the broader market), TCS now

trades at a discount to Sensex

Source: Company data, Credit Suisse estimates

What can the Group do for TCS?

In our view, there is little the Group can do for TCS at this point. TCS has been making

investments in newer digital areas over the last many years, and we believe that it will be

well positioned to capitalise on any pick-up in digital spending by clients. Given its track

record over the last many years, we have no reason to believe that TCS will not be

positioned at the forefront of digital services as well.

TCS has largely relied on organic investments and partnerships with start-ups for

emerging technologies so far. Its larger peers, like Accenture, have been aggressively

investing in developing digital capabilities through acquisitions, and have been successful

in building a leadership in digital. While the broad philosophy of TCS’ management is likely

to continue, we believe this is one area which may require a relook by management.

On the cyclical side, like its peers, it will just have to wait for an improvement. On the P/E

front, the only thing the Group can do, in our view, is to have high and consistent dividend

payouts/buy back. While TCS' payout has been reasonably high, it has been lumpy. There

is scope to enhance the average payout and to make it more consistent, given the cash

pile and free cash flow.

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

10

12

14

16

18

20

22

24

Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16 Mar-17

12 month forward P/E

TCS' premium/discount to Sensex [RHS] TCS Sensex

13 July 2017

Tata Group 23

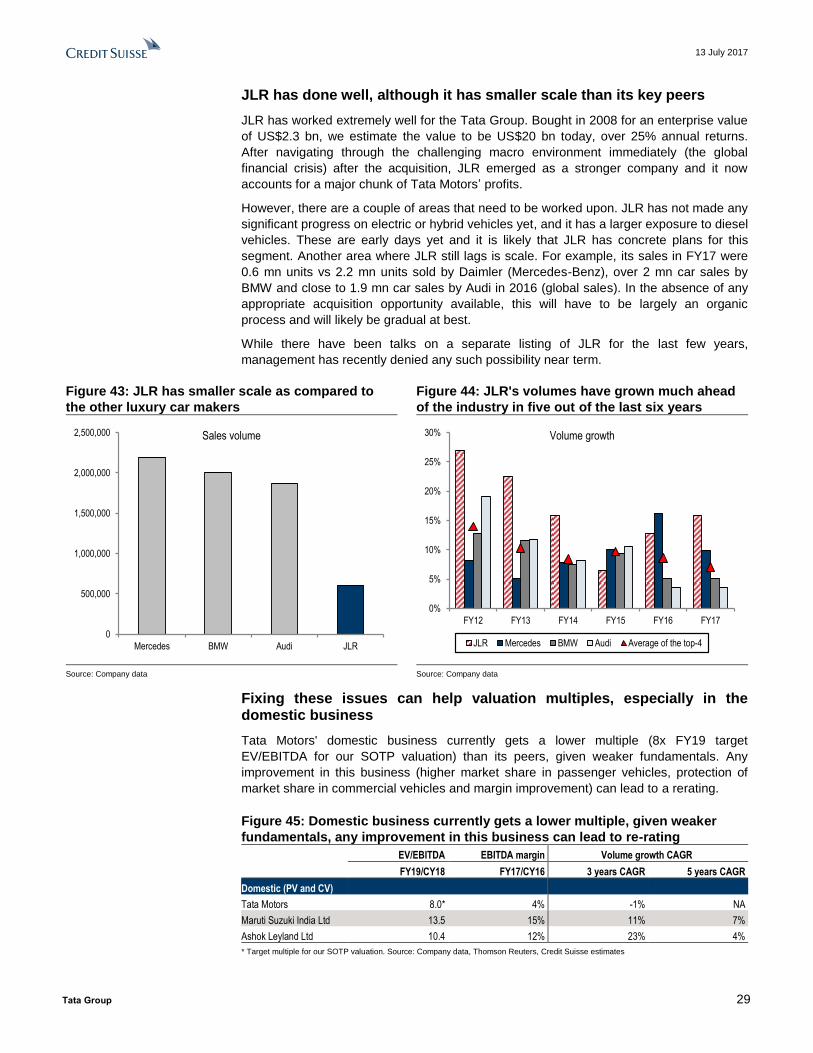

Figure 29: Unlike Accenture and IBM, Indian IT firms

have accumulated significant cash in the balance

sheet over the years

Figure 30: TCS' average payout has been 40%+ over

the last five years (58%, including the recent buy

back); scope to increase this further

* Including buyback. Source: Company data, Credit Suisse estimates. * Including buyback. Source: Company data, Credit Suisse estimates.

Tata Steel: Focus on India, addressing the pension

issue

Tata Steel is one of the leading steel companies globally and the second largest steel

company in India in terms of volumes. The company had consolidated revenue of Rs1.2 tn

in FY17—about 45% of this was contributed by the India business, while the international

operations account for the rest (Europe operations, including Corus, have a predominant

share in the international business, Southeast Asia accounts for the rest). In terms of

EBITDA, India's share is about 70%.

Figure 31: Europe accounts for close to 45% of revenue but has a below 30% EBITDA share (FY17)

Note: Under IndAS. Source: Company data, Credit Suisse estimates.

-20%

0%

20%

40%

60%

80%

100%

120% Application of cash flow generated over FY08-17

Net capex Dividend/Buy-back Acquisitions Cash accumulation

31% 33%

79%

35% 35%

96%

42%

58%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY13 FY14 FY15 FY16 FY17 FY17* 5 yearaverage

5 yearaverage*

Payout (excluding dividend tax)

India46%

Europe44%

Others10%

Tata Steel: Revenue breakup

India70%

Europe28%

Others2%

Tata Steel: EBITDA breakup

International business is 55% of revenue and

30% of EBITDA

13 July 2017

Tata Group 24

Decent progress on the India business, Europe business is still under restructuring

FY17 was a decent year for Tata Steel. Its India business picked up sharply in FY17—

volume growth at 15% was the best in the last six years, and EBITDA/t also improved from

depressed levels of US$105/t to US$150/t. In the European business, volumes were down

30% in FY17 but EBITDA/t improved from -US$17/t to +US$67/t.

Several drivers behind the domestic business' recovery

Tata Steel's domestic business was helped by a higher volume growth, better pricing (the

ASP increased by over 6% during the year) and resulting improvement in profitability

(EBITDA/t was up 45% during the year). The performance of Indian subsidiaries—Tata

Metaliks, Tinplate and Tata Sponge Iron—also improved.

The commencement of production at the Kalinganagar plant (in May 2016) brought close

to US$4 bn of investment to fruition, with about 3 MT of capacity. Tata Steel's profitability

in the last 6-7 quarters had also been impacted by the high cost of purchased iron ore

(captive production was disrupted due to mine closures at Joda, Noamundi and

Khondbond). With the mines back in production and most of the expensive iron ore

already consumed, iron ore cost fell sharply.

The MIP (Minimum Import Price) also helped the domestic business. Tata Steel benefitted

due to its relatively better positioning.

Europe business is still under restructuring

Tata Steel's European business has two parts—Netherlands and the UK. While the former

has historically done well, the latter has been a drag on the company's operations. Tata

Steel sold a part of the UK business (specialty steel) for £100 mn and has also

implemented a transformation programme to improve the performance of the remainder of

the European business.

The imposition of anti-dumping duty by EU on hot-rolled and heavy plates imported from

China could have helped margins to some extent in 2H17. Falling GBP (against USD) was

also a tailwind for the UK business.

Figure 32: Tata Steel's India volume growth was the

best in FY17 in the last six years, and EBITDA/t also

improved from depressed levels

Figure 33: Although volumes were down at Tata

Steel Europe, EBITDA/t improved from the

depressed levels

Source: Company data, Credit Suisse research Source: Company data, Credit Suisse research

-50

50

150

250

350

450

550

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

Tata Steel (India)

Volume growth EBITDA/ton (US$) [RHS]

-110

-60

-10

40

90

-35%

-25%

-15%

-5%

5%

15%

25%

35%

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

Tata Steel Europe

Volume growth EBITDA/ton (US$) [RHS]

+15% volume growth in domestic, 30% decline

in international in FY17

Kalinganagar capacity, resumption of iron ore mines and MIP helped

The UK business has been a drag

13 July 2017

Tata Group 25

Figure 34: EU turnaround—progress in the last two years

Date Development

Jul-2015 SPH (NL pension scheme) re-classified as defined contribution

Jul-2015 Specialty and bar business to refocus on high-value markets (aerospace)

Aug-2015 Mothballed hot strip mill at Llanwern, Newport

Oct-2015 Mothballed plate mills at Scunthorpe, Dalzell and Clydebridge

Oct-2015 Closed two coke ovens at Scunthorpe

Dec-2015 Entered into discussions with Greybull Capital LLP for Longs business

Jan-2016 Further restructuring announcements incl. redundancies in UK

Apr-2016 Sale agreement signed with Greybull

Apr-2016 UK government announced support package for potential buyers of TSUK

Apr-2016 Sold Clydebridge and Dalzell plate mills in Scotland to Scottish government

May-2016 The UK government issued a public consultation paper outlining possible regulatory support to facilitate changes in BSPS

May-2016 Longs business sale completed (to Greybull)

Feb-2017 Definitive agreement with Liberty House Group for the sale of its UK Specialty Steel business.

Source: Company data, Credit Suisse estimates

Positive cash generation and improving debt coverage

After several years of consistent negative free cash flow generation, Tata Steel has

generated positive free cash flow for the last two years—FY16 free cash generation was

marginally positive and was Rs25 bn in FY17. Net debt coverage has improved too. Net

debt has been stable for the last four years, and with improved profitability, the net

debt/EBITDA has come down to the levels of ~4x. The recent sale of stake in Tata Motors

for close to US$590 mn has further reduced this ratio.

Figure 35: After several years of consistent negative

free cash flow generation, Tata Steel has generated

positive free cash flow in FY17 (marginally positive

in FY16)

Figure 36: Net debt is stable for the last four years,

and with improved profitability, net debt/EBITDA is

back to the historical levels ++++ ++++++ +++++

+++++ +++

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

What can be improved?

The domestic business has done well in the last one year and that may remain a key focus

area for the Group, in our view. The European business (the UK in particular) on the other

hand is still operating at sub-optimal levels—a speedy resolution of the UK pension issue

will be important. Also, there have been talks of a strategic JV with ThyssenKrupp.

Elimination of cross holdings can help in debt reduction.

-200

-150

-100

-50

0

50

100

150

200

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

Tata Steel - Consolidated (Rs bn)

CFO Capex FCF

0.0

2.0

4.0

6.0

8.0

10.0

12.0

0

100

200

300

400

500

600

700

800

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

Net debt (Rs bn) Net debt to equity [RHS]

Net debt to EBITDA [RHS]

FY17 FCF was the best in seven years, net

debt/EBITDA back to 4x

13 July 2017

Tata Group 26

Nothing much to be done in the India business but it will be the key segment

Tata Steel's India business is already operating at a reasonably high utilisation. Also much

of the input requirements are met in-house through captive operations. Hence, there is

little scope for further efficiency gains in the India business. Any improvement in EBITDA/t

will largely depend on an increase in realisation (steel prices).

The European business has scope for improvement

Tata Steel's strategy on turning around the European portfolio hinges upon: (1) resolution

of the UK pension issue, (2) the sale of peripheral businesses (several of them have been

already sold), and (3) a broader strategic JV with ThyssenKrupp. The UK assets have

already been largely written down, and hence, there is little risk of a big impairment in the

future.

The company has already moved its active employees in the UK from a defined benefit

pension plan to a defined contribution plan. Additionally, steps to de-link the pension fund

from the scheme sponsor are separately under way. Tata Steel has obtained "in-principle

approval" from the UK pension regulator for a Regulated Apportionment Arrangement. It

will pay £550 mn alongside a 33% stake in Tata Steel UK to close the existing pension

scheme. It will, however, sponsor a closed de-risked new pension scheme to be offered as

a voluntary option to the existing members. That may pave the way for an eventual JV with

ThyssenKrupp, and possibly help the business become self-sufficient.

Tata Motors: India needs to be fixed

Tata Motors originally started operations as a commercial vehicle company (it started as a

locomotive manufacturer in 1945 and ventured into commercial manufacturing in 1954),

and built the passenger vehicle business much later (in the 1990s). Tata Motors has been

the market leader in the commercial vehicles segment in India, and is still trying to build a

prominent positioning in the passenger vehicles segment.

It made a few large acquisitions to expand international operations. In 2004, it acquired

Daewoo's South Korea-based truck manufacturing unit (named as Tata Daewoo) for over

US$100 mn. In 2008, it made a much bigger acquisition of Jaguar Land Rover for a

consideration of US$2.3 bn. These businesses have done well for the company.

India needs to be fixed

Given the long history of the India business and the strong Tata brand in India, the

contribution of this business to the overall value of Tata Motors is very low. For example,

the India business contributes just Rs80 of the CS target price of Rs630 for Tata Motors,