these consolidated financial statements are originally ... · 30 june 2011 (unaudited) and 31...

TRANSCRIPT

These consolidated financial statements are originally issued in the Indonesian language.

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS AS OF 30 JUNE 2011 (UNAUDITED) AND

31 DECEMBER 2010 (AUDITED), AND FOR THE SIX-MONTH PERIODS ENDED 30 JUNE 2011 AND 2010 (UNAUDITED)

Table of Contents

Page Consolidated Balance Sheets………………………………………………………………………………… 1-2 Consolidated Statements of Income…………………………………………………………………………. 3 Consolidated Statements of Changes in Shareholders’ Equity…………………………………………… 4

Consolidated Statements of Cash Flows ……………………………………………………………………. 5-6 Notes to the Consolidated Financial Statements…………………………………………………………… 7-58

**************************

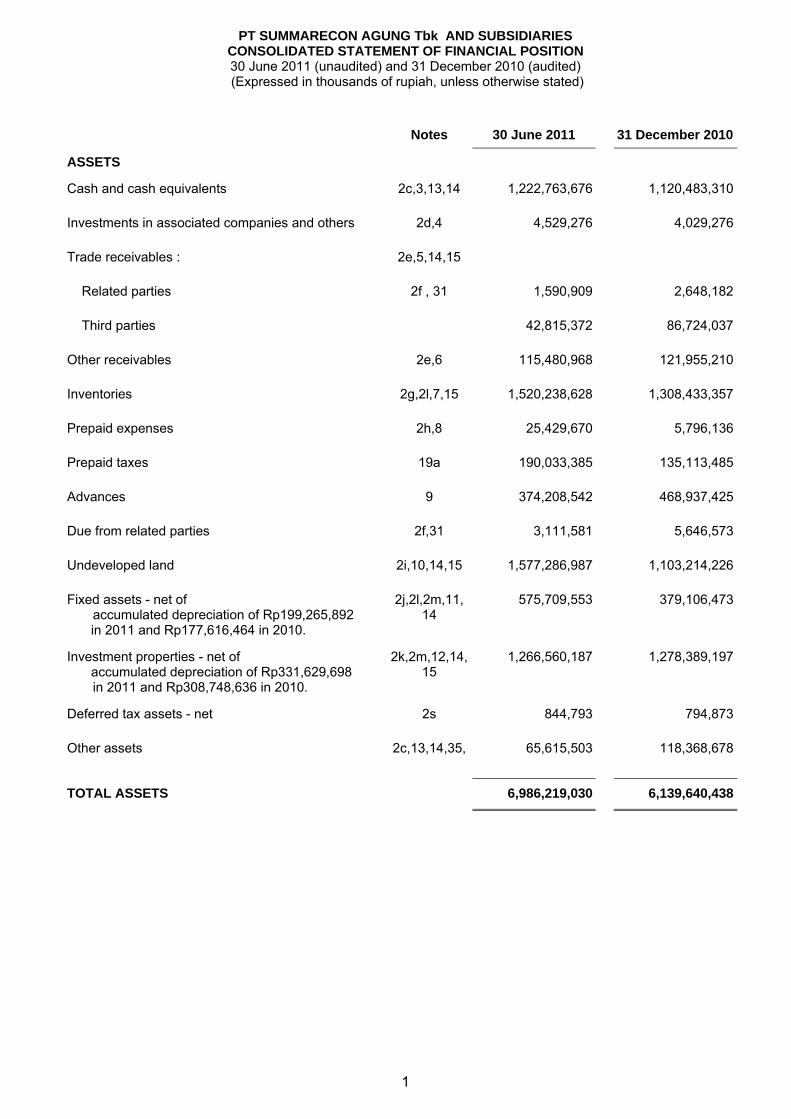

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES CONSOLIDATED STATEMENT OF FINANCIAL POSITION 30 June 2011 (unaudited) and 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

1

Notes 30 June 2011 31 December 2010

ASSETS

Cash and cash equivalents 2c,3,13,14 1,222,763,676 1,120,483,310

Investments in associated companies and others 2d,4 4,529,276 4,029,276

Trade receivables : 2e,5,14,15

Related parties 2f , 31 1,590,909 2,648,182

Third parties 42,815,372 86,724,037

Other receivables 2e,6 115,480,968 121,955,210

Inventories 2g,2l,7,15 1,520,238,628 1,308,433,357

Prepaid expenses 2h,8 25,429,670 5,796,136

Prepaid taxes 19a 190,033,385 135,113,485

Advances 9 374,208,542 468,937,425

Due from related parties 2f,31 3,111,581 5,646,573

Undeveloped land 2i,10,14,15 1,577,286,987 1,103,214,226

Fixed assets - net of accumulated depreciation of Rp199,265,892

in 2011 and Rp177,616,464 in 2010.

2j,2l,2m,11, 14

575,709,553 379,106,473

Investment properties - net of accumulated depreciation of Rp331,629,698 in 2011 and Rp308,748,636 in 2010.

2k,2m,12,14,15

1,266,560,187 1,278,389,197

Deferred tax assets - net 2s 844,793 794,873

Other assets 2c,13,14,35,

65,615,503 118,368,678

TOTAL ASSETS 6,986,219,030 6,139,640,438

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES CONSOLIDATED STATEMENT OF FINANCIAL POSITION 30 June 2011 (unaudited) and 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

2

Notes 30 June 2011 31 December 2010

LIABILITIES AND EQUITY

LIABILITIES

Loans from banks and financing institution 14 716,826,299 475,395,230

Bonds payable and sukuk ijarah - net 2v,7,15 298,057,940 297,652,024

Trade payables to third parties 16 278,514,988 181,664,820

Other payables 2b,17 150,889,416 26,811,579

Due to related parties 2f,31 229,799,581 203,202,788

Accrued expenses 18 134,084,187 157,753,675

Taxes payable 19b 17,508,534 43,451,998

Employee benefits liabilities 2p,20 43,178,673 41,310,161

Deposits received 2o,21

Related parties 31 2,814,693 1,809,952

Third parties 2,671,810,372 2,391,525,252

Unearned revenues 2o,22,2v 196,741,919 159,788,420

Deferred tax liabilities - net 2s 1,683,759 1,539,907

Derivative liability 2v,13,14,35 157,392 201,204

TOTAL LIABILITIES 4,742,067,753 3,982,107,010

EQUITY

Share Capital 1b,24,25 687,314,084 687,314,084

Additional paid-in capital - net 1b,24,25 245,355,554 245,355,554

Differences arising from changes in the equity of Subsidiary

56,506 56,506

Retained earnings

Appropriated - reserve fund 26 45,892,133 43,557,354

Unappropriated 1,247,623,725 1,163,603,329

Equity Attributable to Owners of the Company 2,226,242,002 2,139,886,827

NON-CONTROLLING INTERESTS 2b,23 17,909,275 17,646,601

TOTAL EQUITY 2,244,151,277 2,157,533,428

TOTAL LIABILITIES AND EQUITY 6,986,219,030 6,139,640,438

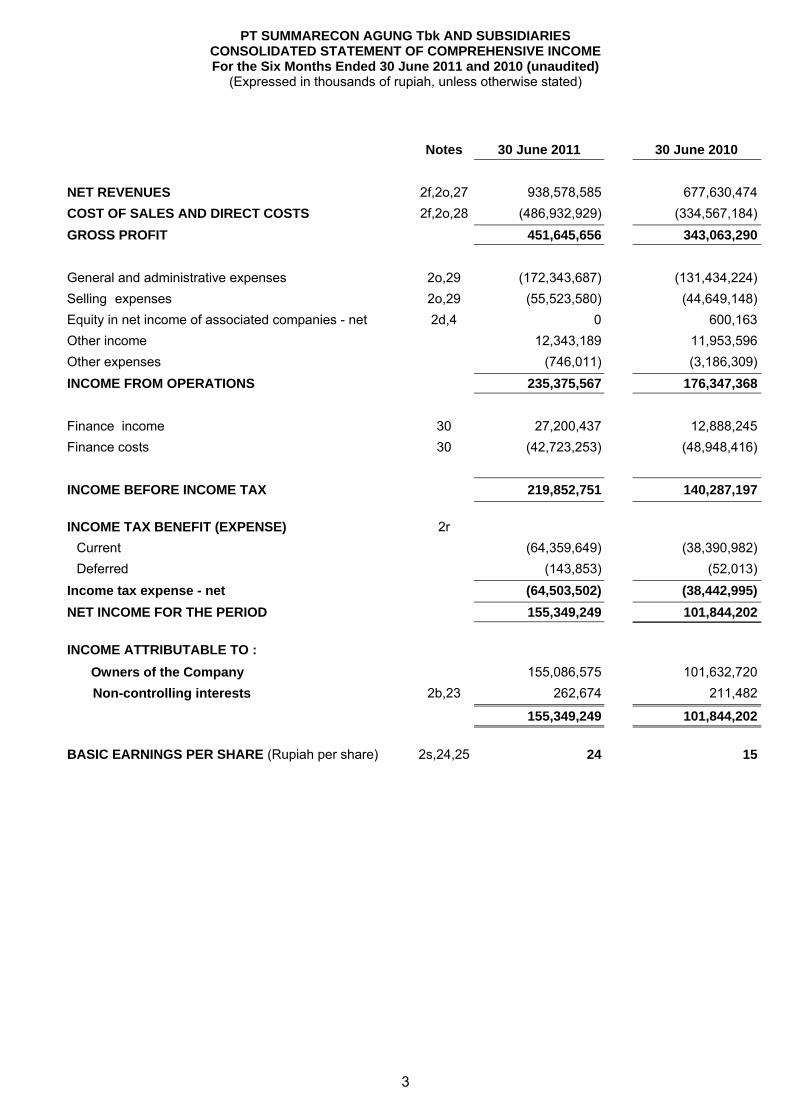

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME For the Six Months Ended 30 June 2011 and 2010 (unaudited)

(Expressed in thousands of rupiah, unless otherwise stated)

3

Notes 30 June 2011 30 June 2010

NET REVENUES 2f,2o,27 938,578,585 677,630,474

COST OF SALES AND DIRECT COSTS 2f,2o,28 (486,932,929) (334,567,184)

GROSS PROFIT 451,645,656 343,063,290

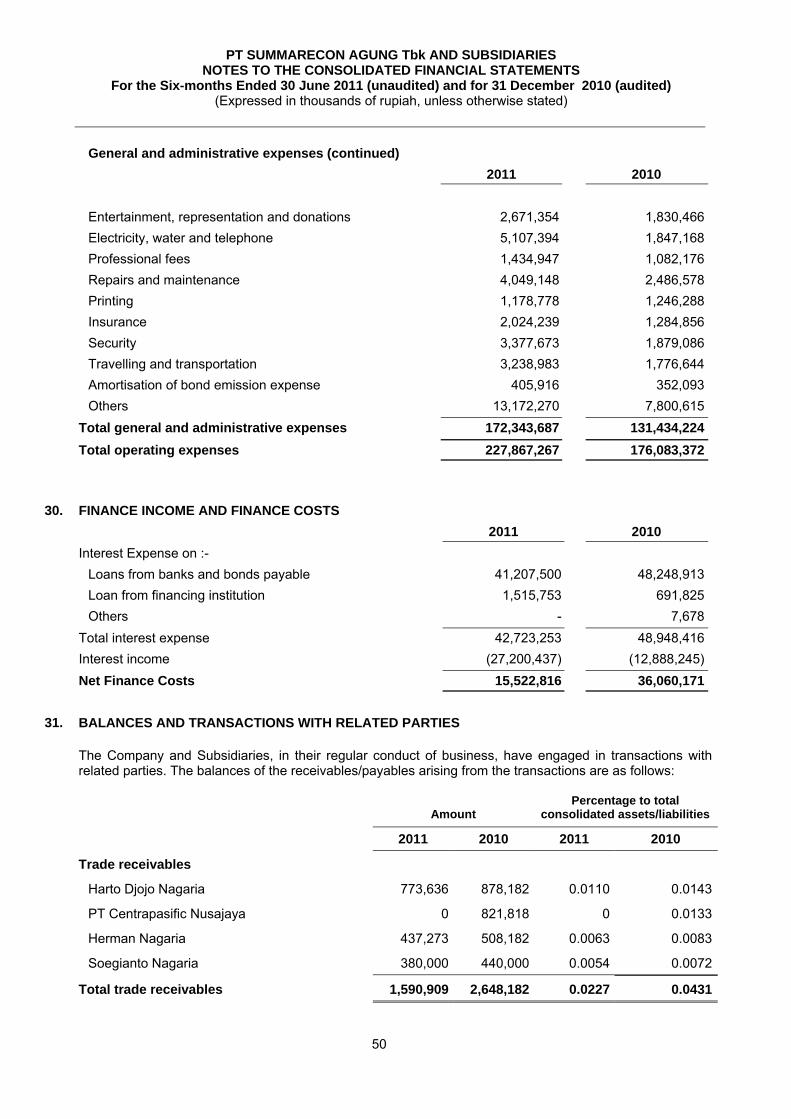

General and administrative expenses 2o,29 (172,343,687) (131,434,224)

Selling expenses 2o,29 (55,523,580) (44,649,148)

Equity in net income of associated companies - net 2d,4 0 600,163

Other income 12,343,189 11,953,596

Other expenses (746,011) (3,186,309)

INCOME FROM OPERATIONS 235,375,567 176,347,368

Finance income 30 27,200,437 12,888,245

Finance costs 30 (42,723,253) (48,948,416)

INCOME BEFORE INCOME TAX 219,852,751 140,287,197

INCOME TAX BENEFIT (EXPENSE)

2r

Current (64,359,649) (38,390,982)

Deferred (143,853) (52,013)

Income tax expense - net (64,503,502) (38,442,995)

NET INCOME FOR THE PERIOD 155,349,249 101,844,202

INCOME ATTRIBUTABLE TO :

Owners of the Company 155,086,575 101,632,720

Non-controlling interests 2b,23 262,674 211,482

155,349,249 101,844,202

BASIC EARNINGS PER SHARE (Rupiah per share)

2s,24,25

24

15

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

For the Six Months Ended 30 June 2011 and 2010 (Expressed in thousands of rupiah, unless otherwise stated)

4

Issued and fully

paid share capital

Retained earnings

Additional paid-in capital - net

Differences arising from changes in

the equity of Subsidiary

Appropriated - reserve fund Unappropriated Total

Non controlling interests

Total equity

Balance as of 31 December 2009 643,680,064 49,002,463 56,506 41,883,927 983,153,942 1,717,776,902 7,021,126 1,724,798,028

Transition adjustment of applying Statement of Financial Accounting Standards (PSAK) No. 55 (Revised 2006), “Financial Instruments: Recognition and Measurement” 0 0 0 0 3,292,140 3,292,140

0

3,292,140

Balance as of 1 January 2010 643,680,064 49,002,463 56,506 41,883,927 986,446,082 1,721,069,042 7,021,126 1,728,090,168

Exercise of warrants 43,634,020 196,353,091 0 0 0 239,987,111 239,987,111

Appropriation to general reserve 0 0 0 1,673,427 (1,673,427) 0 0 0

Cash dividend 0 0 0 0 (54,647,222) (54,647,222) 0 (54,647,222)

Net income for six months 0 0 0 0 101,632,720 101,632,720 211,482 101,844,202

Balance as of 30 June 2010 687,314,084 245,355,554 56,506 43,557,354 1,031,758,153 2,008,041,651 7,232,608 2,015,274,259

Balance as of 1 January 2011 687,314,084 245,355,554 56,506 43,557,354 1,163,603,329 2,139,886,827 17,646,601 2,157,533,428

Appropriation to general reserve 0 0 0 2,334,779 (2,334,779) 0 0 0

Cash dividend 0 0 0 0 (68,731,400) (68,731,400) (68,731,400)

Net income for six months 0 0 0 0 155.086.575 155.086.575 262.674 155.349.249

Balance as of 30 June 2011 687,314,084 245,355,554 56,506 45,892,133 1,247,623,725 2,226,242,002 17,909,275 2,244,151,277

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES CONSOLIDATED STATEMENT OF CASH FLOWS

For Six Months Ended 30 June 2011 and 2010 (unaudited) (Expressed in thousands of rupiah, unless otherwise stated)

The accompanying notes form an integral part of these consolidated financial statements.

5

Notes 30 June 2011 30 June 2010

CASH FLOWS FROM OPERATING ACTIVITIES

Receipts from customers 1,351,611,808 1,233,293,935

Payments to :

Suppliers (935,199,574) (564,098,869)

Employees (109,858,277) (88,255,591)

Payments for other operating expenses (106,953,262) (102,618,259)

Cash generated from operating activities 199,600,695 478,321,216

Receipts of interest income 27,200,437 12,888,246

Payments for :

Income taxes (133,074,446) (70,414,131)

Interest expense (40,486,909) (50,197,847)

Net cash generated from operating activities 53,239,777 370,597,484

CASH FLOWS FROM INVESTING ACTIVITIES

Increase in amounts due to related parties 31 26,596,793 11,414,313

Proceeds from sale of fixed assets and investment properties

0 737,977

Decrease (increase) in amounts due from related parties 31 (2,881,899) (14,189,347)

Acquisitions of fixed assets and investment properties 11,12 (144,159,931) (106,506,805)

Decrease (increase) in other assets (2,236,141) (205,968)

Investments in associated companies and others 4 (500,000) (384,181)

Net cash used in investing activities (123,181,178) (109,134,011)

CASH FLOWS FROM FINANCING ACTIVITIES

Proceeds from bank loans 14 253,156,395 65,729,265

Repayment of loans from banks and financing institution 14 (91,115,735) (267,413,268)

Cash dividends paid by the Company 7 (50,840,978)

Proceeds from (increase in) restricted cash in time deposit 13

11,651,500 9,244,546

Increase in capital share and additional paid-in capital 24,25 0 239,987,111

(Increase) decrease in derivative assets 0 (48)

Increase (decrease) in derivative liabilites 0 211

Net cash used in financing activities 173,692,167 (3,293,161)

NET INCREASE IN CASH AND CASH EQUIVALENTS 103,750,766 258,170,312

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES CONSOLIDATED STATEMENT OF CASH FLOWS

For Six Months Ended 30 June 2011 and 2010 (unaudited) (Expressed in thousands of rupiah, unless otherwise stated)

The accompanying notes form an integral part of these consolidated financial statements.

6

Notes 30 June 2011 30 June 2010

NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS (continued)

103,750,766

258,170,312

CASH AND CASH EQUIVALENTS AT BEGINNING OF YEAR 3 1,120,483,310 633,169,242

EFFECT OF FOREIGN EXCHANGE 14 (1,470,400) (1,719,348)

CASH AND CASH EQUIVALENTS AT END OF YEAR 3 1,222,763,676 889,620,206

Activities not affecting cash flows:

Acquisitions of fixed assets credited to:

Advances 1,468,548 671,077

Other payables 656,491 255,095

Loans from banks and financing institution 85,927,996 4,024,486

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

7

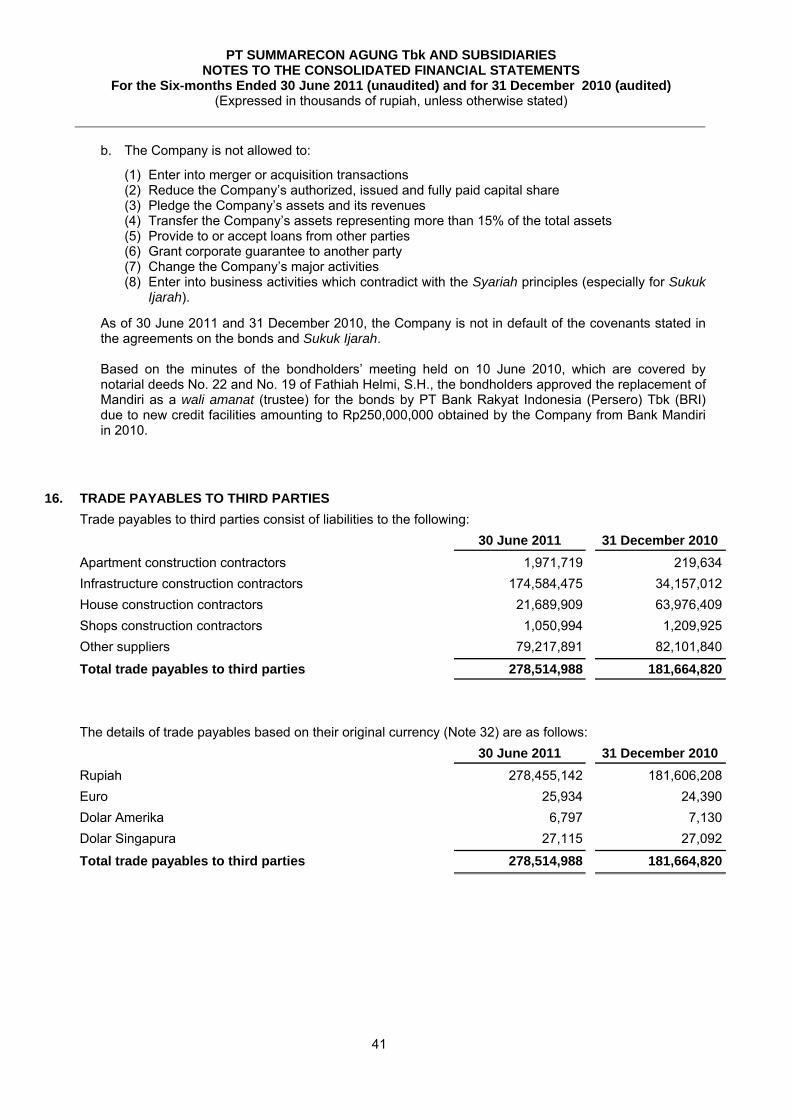

1. GENERAL a. The Company’s establishment

PT Summarecon Agung Tbk (the “Company”) was established within the framework of the

Domestic Capital Investment Law based on notarial deed No. 308 dated 26 November 1975 of Ridwan Suselo, S.H. The articles of association was approved by the Ministry of Justice in its Decision Letter No. YA 5/344/6 dated 12 July 1977 and was published in Supplement No. 597 of State Gazette No. 79 dated 4 October 1977. The articles of association has been amended from time to time, the latest amendments of which were drawn up in : (a) notarial deed No. 44 dated 18 July 2008 of Fathiah Helmi, S.H., which was published in Supplement No. 15805 of State Gazette No. 48 dated 16 June 2009, concerning the increase in the Company’s issued and fully paid capital share through the distribution of bonus shares from the capitalization of additional paid-in capital (Notes 24 and 25) and compliance with the Corporation Law No. 40 of Year 2007, which amendment was approved by the Ministry of Justice and Human Rights in its Decision Letter No. AHU-50104.AH.01.02 dated 12 August 2008, and (b) notarial deed No. 13 dated 5 June 2009 of Fathiah Helmi S.H., concerning the change in the composition of the Company’s boards of directors and commissioners, which amendment was acknowledged and recorded by the Ministry of Justice and Human Rights based on its Decision Letter No. AHU-AH.01.10-10706 dated 17 July 2009.

According to Article 3 of the Company’s articles of association, its scope of activities comprises real estate development, leasing of properties and operating recreational facilities and restaurants. The Company's head office is located in Plaza Summarecon, Jl. Perintis Kemerdekaan Kav. No. 42, Jakarta.

The Company started commercial operations in 1976.

b. The Company’s public offerings

The Chairman of the Capital Market and Financial Institutions Supervisory Agency (BAPEPAM and

LK), through his letter No. SI-085/SHM/MK.10/1990 dated 1 March 1990, declared effective at that date, the offering of 6,667,000 Company shares with a par value of Rp1,000 (full amount) per share to the public at an offering price of Rp6,800 (full amount) per share. The Company listed all its issued shares on the Indonesia Share Exchange on 14 August 1996 (Note 25).

Based on the minutes of the shareholders’ extraordinary meeting which were notarized under deed

No. 191 dated 21 June 1996 of Sutjipto, S.H., the shareholders approved the reduction in the par value of the Company’s shares from Rp1,000 (full amount) to Rp500 (full amount) per share. The amendment was approved by the Ministry of Justice in its Decision Letter No. C2.9225.HT.01.04.TH.96 dated 27 September 1996.

Based on the minutes of the shareholders’ extraordinary meeting which were notarized under deed

No. 99 dated 21 June 2002 of Sutjipto, S.H., the shareholders approved the reduction in the par value of the Company’s shares from Rp500 (full amount) to Rp100 (full amount) per share. The amendment was approved by the Ministry of Justice and Human Rights in its Decision Letter No. C-12844 HT.01.04.TH.2002 dated 12 July 2002.

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

11

The composition of the Company’s Audit Committee as of 31 December 2010 and 2009 is as follows:

Chairman : H. Edi Darnadi Member : Poespita Pelangiwati Member : Esther Melyani Homan

Salaries and other compensation benefits of the Boards of Commissioners and Directors amounted to approximately Rp13 billion (full amount) and Rp26.1 billion (full amount) on 30 June 2011 and 31 December 2010, respectively. The Company and Subsidiaries had 1,345 and 1,339 permanent employees (unaudited) as of 30 June 2011 and 31 December 2010, respectively.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The accounting and reporting policies adopted by the Company and Subsidiaries conform to generally accepted accounting principles in Indonesia. The significant accounting principles applied consistently in the preparation of the consolidated financial statements for the periods ended 30 June 2011 and 31 December 2010 are as follows: a. Basis of preparation of the consolidated financial statements

The consolidated financial statements have been prepared in accordance with generally accepted

accounting principles in Indonesia, which are based on Statements of Financial Accounting Standards (PSAK) and Capital Market and Financial Institution Supervisory Agency (BAPEPAM and LK) regulation No. VIII.G.7 (Revised 2000) concerning “Guidelines for Presentation of Financial Statements” and circular letter No. SE-02/PM/2002 dated 27 December 2002 of the Chairman of BAPEPAM and LK concerning “Guidelines for Financial Statement Presentation and Disclosures for Publicly-listed Companies Engaged in the Real Estate Industry”.

The consolidated financial statements have been prepared on the accrual basis using the historical

cost concept of accounting, except for certain short-term investments and derivative instruments which are stated at fair value, inventories which are stated at the lower of cost or net realizable value, certain investments in shares of share which are accounted for using the equity method and financial instruments which are valued at fair value. The consolidated statements of cash flows classify cash flows into operating, investing and financing activities. The cash flows from operating activities are presented using the direct method. The reporting currency used in the preparation of the consolidated financial statements is the Indonesian rupiah (Rp).

b. Principles of consolidation

The consolidated financial statements include the accounts of the Company and Subsidiaries whose shares are owned more than 50% by the Company, directly or indirectly; the joint operation (Kerja Sama Operasi), known as KSO Summarecon Serpong, between SCK and PT Jakaratabaru Cosmopolitan (JBC); and the KSO Summarecon Lakeview among SCK, PT Telaga Gading Serpong (TGS) and PT Lestari Kreasi (LTK). In accordance with PSAK No. 12, “Financial Reporting of Interests in Jointly Controlled Operations and Assets”, SCK’s participation in the joint operation has been accounted for in the consolidated financial statements using the proportionate consolidation method. In applying the proportionate consolidation method, the venturer combines its proportionate share in the assets and liabilities of the joint venture, and its interests in the joint venture revenues and expenses with the related accounts in the consolidated financial statements.

All significant intercompany accounts and transactions have been eliminated.

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

12

The proportionate share of the minority shareholders in the equity of the Subsidiaries is reflected as “Minority Interests in Net Assets of Consolidated Subsidiaries” in the consolidated balance sheets. When cumulative losses applicable to minority interests exceed the minority shareholders’ interests in the Subsidiaries’ capital share, the loss in excess of the minority shareholders’ interest is charged against the majority shareholder’s interest and is not reflected as an asset, except when minority shareholders have a binding obligation to cover such losses and the minority shareholders can fulfill their obligation. Subsequent profits earned by the Subsidiaries that are applicable to the minority interests shall be first allocated to the majority interest to the extent of the losses applicable to the minority interests which were previously absorbed by such majority interest. The excess of the acquisition cost of the investment over the Company’s interest in the net assets of Subsidiaries is recorded as ‘‘Excess of Cost Over Interest in Net Assets of Subsidiaries” and is amortized using the straight-line method over five years. When the cost of the acquisition is less than the Company’s interest in the net assets of the Subsidiaries, the excess is recognized as “Excess of Interest in Net Assets of Subsidiary Over Cost” (included as part of Other Payables in the consolidated balance sheets) and is amortized using the straight-line method over 20 years.

In accordance with PSAK No. 40, “Accounting for Changes in Equity of Subsidiary/Associated Company”, the differences between the carrying values of the Company’s investments in shares of share and its corresponding proportionate equity share in the underlying net asset values of its Subsidiaries and/or associated companies arising from changes in the latter’s equity, which are not resulting from transactions between the Company and the subject Subsidiaries/associated companies, are presented as a separate item under the Shareholders’ Equity section of the consolidated sheets as “Differences Arising from Changes in Equity of Subsidiary”.

c. Cash equivalents

Time deposits with maturities of three months or less at the time of placement, which are not restricted as to withdrawal or are not pledged as collateral for loans, are classified as “Cash Equivalents”. Cash in banks and time deposits which are restricted or pledged are presented as part of “Other Assets”.

d. Investments

Prior to 2010, investment in shares of share wherein the Company’s ownership interest is at least 20% but not exceeding 50% is accounted for under the equity method, whereby the cost of the investment is increased or decreased by the Company’s share in the net earnings or losses of the associated company and reduced by the dividends received. In accordance with PSAK No. 15 on “Accounting for Investments in Associated Companies”, under the equity method, if an investor’s share in the losses of an investee equals or exceeds the carrying amount of the investment, the investment shall be reported at zero value. Subsequent losses will be absorbed with a credit to liability only if the investor has guaranteed to pay the investee’s liabilities. If the investee subsequently reports a profit, the investor will recognize income only after its share in the profit exceeds its share in the net losses not recognized or absorbed. Starting 2010, investment on share of share wherein the Company’s ownership interest is less than 20% is classified as financial asset available for sale and is determined based on the policies outlined in Note 2v.

e. Allowance for impairment

Prior to 2010, allowance for impairment was provided based on a review of the status of the individual receivables at the end of the year. Starting 2010, the allowance, if any, is determined based on the policies outlined in Note 2v.

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

13

f. Transactions with related parties The Company and Subsidiaries have transactions with certain parties which are regarded as

having related party relationships as described by PSAK No. 7 on “Related Party Disclosures”. Significant transactions with related parties are disclosed in Note 31.

g. Inventories

Inventories are stated at the lower of cost or net realizable value. Cost is determined by the

specific identification method. The cost of land under development consists of cost of undeveloped land, direct and indirect

development costs related to real estate development activities and borrowing costs. Land under development is transferred to lots available for sale when the land development is completed. Total project cost is allocated proportionately to the saleable lots based on their respective areas.

The cost of land development, including land which is used for roads and infrastructure or other

unsaleable area, is allocated to the saleable area. The cost of buildings and apartements under construction is transferred to houses, shops and

apartments (strata title) available for sale when the construction is substantially completed. For residential property project, its cost is classified as part of inventories upon the commencement

of development and construction of infrastructure. For commercial property project, upon the completion of development and construction of infrastructure, its cost remains as part of inventories or is reclassified to the related fixed asset account, whichever is more appropriate.

Other inventories, consisting of food, beverages and other inventories, are stated at cost or net

realizable value, whichever is lower. Cost is determined using the first-in, first-out method (FIFO). h. Prepaid expenses

Prepaid expenses are amortized over their beneficial periods.

i. Undeveloped land

Undeveloped land is stated at cost or net realizable value, whichever is lower.

The cost of undeveloped land, consisting of pre-acquisition and acquisition cost of land, is transferred to land under development upon commencement of land development.

j. Fixed assets

Fixed assets are stated at cost less accumulated depreciation and impairment loss, if any, except for land which is not depreciated. Such cost includes the cost of replacing part of the fixed assets when that cost is incurred, if the recognition criteria are met.

Likewise, when a major inspection is performed, its cost is recognized in the carrying amount of

the fixed assets as a replacement if the recognition criteria are met. All other repairs and maintenance costs that do not meet the recognition criteria are recognized in the consolidated statements of income as incurred.

Depreciation is computed using the straight-line method over the estimated useful lives of the

assets as follows: Years

Buildings and infrastructures 2 - 40 Hotel facilities 2 - 5

Machinery and heavy equipment 10

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

14

Years Vehicles 5 - 10 Furniture and office equipment 2 - 5

Construction in progress is stated at cost and is accounted as part of fixed assets. The accumulated costs will be reclassified to the appropriate fixed assets or investment properties account when the construction is completed and the constructed asset is ready for its intended use.

In accordance with PSAK No. 47 on “Accounting for Land”, land is stated at cost and is not depreciated. Certain costs incurred relating to the cost or renewal of the legal title of a landright are deferred (included as part of Other Assets) and amortized over the estimated useful life of the landright or the term of the landright, whichever period is shorter.

An item of fixed assets is derecognized upon disposal or when no future economic benefits are expected from its use or disposal. Any gain or loss arising on derecognition of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the asset) is credited or charged to operations in the year the asset is derecognized.

The fixed assets’ residual values, useful lives and methods of depreciation are reviewed and adjusted prospectively, if appropriate, at each financial year end.

k. Investment properties

Investment properties are stated at cost including the transaction cost less accumulated depreciation and impairment loss, if any, except for land which is not depreciated. Such cost includes the cost of replacing part of the investment properties, if the recognition criteria are met, and excludes the daily expenses on their usage. Investment properties consist of land, building and infrastructures, and machinery and heavy equipment held by the Company and Subsidiaries to earn rentals or for capital appreciation or both, rather than for use in the production or supply of goods or services or for administrative purposes or sale in the ordinary course of business. Depreciation is computed using the straight-line method over the estimated useful lives of the investment properties as follows: Years

Buildings and infrastructures 3 - 40 Machinery and heavy equipment 10

An investment property should be derecognized on disposal or when the investment property is

permanently withdrawn from use and no future economic benefits are expected from its disposal. Gain or loss arising from the retirement or disposal of investment property is credited or charged to operations in the year the asset is derecognized. Transfers to investment property should be made when, and only when, there is a change in use, evidenced by the end of owner-occupation, commencement of an operating lease to another party or end of construction or development. Transfers from investment property should be made when, and only when, there is a change in use, evidenced by the commencement of owner-occupation or commencement of development with a view to sell.

For a transfer from investment properties to owner-occupied property, the Company uses the cost method at the date of change in use. If an owner-occupied property becomes an investment property, the Company records the investment property in accordance with the fixed assets policies up to the date of change in use.

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

15

l. Capitalization of borrowing costs

In accordance with PSAK No. 26 (Revised 1997) on “Borrowing Costs”, borrowing costs are generally expensed as incurred. Borrowing costs are capitalized if they are directly attributable to the acquisition, construction or production of a qualifying asset. Capitalization of borrowing costs commences when the activities to prepare the asset for its intended use or sale are in progress and the expenditures and borrowing costs are being incurred. Borrowing costs are capitalized until the assets are ready for their intended use. If the resulting carrying amount of the asset exceeds its recoverable amount or net realizable value, an impairment loss is recognized.

m. Impairment of non-financial asset value The recoverable amount of an asset is estimated whenever events or changes in circumstances

indicate that its carrying amount may not be fully recoverable. Impairment in asset value, if any, is recognized as loss in the current year’s consolidated statement of income.

n. Share issuance costs Costs incurred in connection with the issuance of capital share are presented as a deduction from additional paid-in-capital.

o. Revenue and expense recognition

Revenues from real estate sales are recognized in accordance with PSAK No. 44 on “Accounting for Real Estate Activities” as follows: (i) Revenues from sales of houses, shops and other similar property and related land are

recognized under the full accrual method if all of the following conditions are met: 1. A sale is consummated. 2. The selling price is collectible. 3. The seller’s receivable is not subject to future subordinated to other loan which will be

obtained by the buyer. 4. The seller has transferred to the buyer the usual risks and rewards of ownership in a

transaction that is in substance a sale and does not have a substantial continuing involvement with the property.

(ii) Revenues from sales of landplots that do not require the seller to construct the building are

recognized under the full accrual method if all of the following conditions are met:

1. Total payments by the buyer are at least 20% of the agreed selling price and the amount is not refundable.

2. The selling price is collectible. 3. The receivable is not subordinated to other loans that will be obtained by the buyer in the

future. 4. The land development process is complete so that the seller has no further obligations

related to the lots sold. 5. Only the lots are sold, without any requirement of the seller’s involvement in the

construction of the building on the lots. (iii) Revenues from sales of apartments, the construction of which has not been completed, are

recognized using the percentage-of-completion method if all of the following conditions are met: 1. The construction process has already commenced, that is the building foundation has

been completed and all of the requirements to commence construction have been fulfilled. 2. Total payments by the buyer are at least 20% of the agreed selling price and the amount is

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

16

not refundable. 3. The amount of revenue and the cost of the property can be reliably estimated.

If any of the above conditions is not met, the payments received from the buyer are recorded as

deposits received until all of the criteria are met.

The method used to determine the percentage of completion is the proportion of actual costs incurred to the estimated total development cost of the real estate project.

Rental and membership fees in sports club are recognized as income over the period of rental or

membership. Rental and membership fees received in advance are presented as “Unearned Revenues”. Revenues from restaurant operations are recognized when the goods are delivered or when the services have been rendered.

Revenue from hotel room occupancy is recognized on the basis of the period of occupancy.

Revenue from other hotel services is recognized when the services are rendered or the goods are delivered.

Expenses are recognized when incurred.

p. Employee benefits

The Company and Subsidiaries have defined contribution pension plans covering substantially all of their eligible employees and have recognized their unfunded employee benefits liability in accordance with Labor Law No. 13/2003 dated March 25, 2003 (“the Law”) and PSAK No. 24 (Revised 2004), “Employee Benefits”. The benefits under the Law have been calculated by comparing the benefits that will be received by an employee at normal pension age from the Pension Plan with the benefits as stipulated under the Law, after deducting the accumulated employee contribution and the related investment results. If the employer-funded portion of the Pension Plan benefit is less than the benefit as required by the Law, the Company and Subsidiaries provide for such shortfall. Under PSAK No. 24 (Revised 2004), the cost of providing employee benefits under the Law is determined using the projected-unit-credit actuarial valuation method. Actuarial gains or losses are recognized as income or expenses when the net cumulative unrecognized actuarial gains or losses for each individual plan at the end of the previous reporting year exceed the greater of 10% of the present value of the defined benefit obligation at that date and 10% of the fair value of plan assets at that date. These gains or losses are recognized on a straight-line basis over the expected average remaining working lives of the employees. Further, past service costs arising from the changes in the benefits payable of an existing plan are required to be amortized over the period until the benefits concerned become vested.

q. Foreign currency transactions and balances

Transactions involving foreign currencies are recorded at the rates of exchange prevailing at the time the transactions are made. At balance sheet date, monetary assets and liabilities denominated in foreign currencies are adjusted to reflect the prevailing rates as of balance sheet date and the resulting gains or losses are credited or charged to current operations.

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

17

As of June 30, 2011 and 2010 and December 31, 2010, the rates of exchange used were as follows (full amount) :

Transactions in other foreign currencies are considered not significant. r. Income tax

Based on Government Regulation No. 5 dated 23 March 2002, income from shopping center rental

is subject to a final tax of 10%, except for income on rental contracts signed prior to such regulation which is subject to 6%. On 4 November 2008, the President of the Republic of Indonesia and the Minister of Law and Human Rights signed Government Regulation No. 71/2008 (PP No. 71/2008) on “the third changes on PP No. 48/1994 regarding payment of income tax on income from transfer rights on land and/or building”. This regulation provides that, effective 1 January 2009, the income of a taxpayer from transactions of transferring rights on land and/or building, will be subjected to final tax of 5%.

Final income tax The differences between the carrying amounts of existing assets or liabilities related to the final

income tax and their respective tax bases are not recognized as deferred tax assets or liabilities. Current tax expense related to income subject to final income tax is recognized in proportion to total income recognized during the current year for accounting purposes. The difference between the final income tax paid and the amount charged as final income tax expense in the statements of income is recognized as prepaid tax or tax payable.

Non-final income tax Current tax expense is provided based on the estimated taxable income for the year which is

subject to non-final income tax rates. Deferred tax assets and liabilities are recognized for the temporary differences between the financial and the tax bases of assets and liabilities at each reporting date. Future tax benefits, such as the carry-forward of unused tax losses, are also recognized to the extent that realization of such benefits is probable.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply to the

period when the asset is realized or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted at the balance sheet date. Changes in the carrying amount of deferred tax assets and liabilities due to a change in tax rates are charged or credited to current year operations, except to the extent that they relate to items previously charged or credited to shareholders’ equity.

Amendment to a tax obligation is recorded when an assessment is received or, if appealed against

by the Company or Subsidiaries, when the result of the appeal is determined. s. Earnings per share

In accordance with PSAK No. 56 on “Earnings per Share”, basic earnings per share amount is calculated by dividing net income for the year by the weighted average number of outstanding shares during the year.

Diluted earnings per share amount is computed by dividing net income by the weighted average number of shares outstanding as adjusted for the effects of all potentially dilutive ordinary shares (i.e. warrants).

30 June 2011 31 December 2010 30 June 2010

1 European euro (Euro) 12,462 11,956 11,087

1 United States dollar (US$) 8,597 8,991 9,083

1 Singapore dollar (Sin$) 6,985 6,981 6,481

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

18

t. Segment reporting

The Company and Subsidiaries follow PSAK No. 5 (Revised 2000) which requires the presentation of financial information based on business segment and geographical segment. In accordance with the Company’s and Subsidiaries’ organizational and management structure and internal reporting system, the primary segment reporting of financial information is presented based on business segment as the risks and returns are dominantly affected by their different business activities.

The secondary segment reporting based on geographical location is not presented since all of the Company’s and Subsidiaries’ business activities are located in Jabotabek.

Financial information segment reporting as required by PSAK No. 5 (Revised 2000) is presented in Note 36.

u. Use of estimates

The preparation of consolidated financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect amounts reported therein. Due to inherent uncertainty in making estimates, actual results reported in future periods might be based on amounts which differ from those estimates.

v. Financial instruments Starting 1 January 2010, the Company and Subsidiaries have applied PSAK No. 50 (Revised

2006), “Financial Instruments: Presentation and Disclosures”, and PSAK No. 55 (Revised 2006), “Financial Instrument: Recognition and Measurement”, which superseded PSAK No. 50, “Accounting for Certain Investment in Securities”, and PSAK No. 55 (Revised 1999), “Accounting for Derivative Instruments and Hedging Activities”. PSAK No. 50 (Revised 2006) and PSAK No. 55 (Revised 2006) were applied prospectively.

PSAK No. 50 (Revised 2006) contains the requirements for the presentation of financial

instruments and identifies the information that should be disclosed. The presentation requirements apply to the classification of financial instruments, from the perspective of the issuer, into financial assets, financial liabilities and equity instruments; the classification of related interest, dividends, losses and gains, and the circumstances in which financial assets and financial liabilities must be offset. This PSAK requires the disclosure of, among others, information about factors that affect the amount, timing and certainty of an entity’s future cash flows relating to financial instruments and the accounting policies applied to those instruments.

PSAK No. 55 established the principles for recognizing and measuring financial assets, financial

liabilities, and some contracts to buy or sell non-financial items. This PSAK provides the definitions and characteristics of a derivative, the categories of financial instruments, recognition and measurement, hedge accounting and determination of hedging relationships, among others.

The transition effect from the prospective adoption of the above revised PSAK’s which amounted

to Rp3,292,140 has been recorded in the retained earnings at 1 January 2010.

i. Financial Assets

Initial Recognition

Financial assets within the scope of PSAK No. 55 (Revised 2006) are classified as financial assets at fair value through profit or loss, loans and receivables, held-to-maturity investments and available-for-sale financial assets. The Company and Subsidiaries determine the classification of their financial assets at initial recognition and, where allowed and appropriate, re-evaluate this designation at each financial year end.

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

19

Financial assets are recognized initially at fair value plus, in the case of investments not at fair value through profit or loss, directly attributable transaction costs.

Purchases or sales of financial assets that require delivery of assets within a time frame

established by regulation or convention in the marketplace (regular way purchases) are recognized on the trade date, i.e., the date that the Company and Subsidiaries commit to purchase or sell the assets.

The Company and Subsidiaries have determined financial assets are categorized as loans

and receivables and available-for-sale financial assets. Subsequent Measurement

● Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinable

payments that are not quoted in an active market. Such financial assets are carried at amortized cost using the effective interest rate method. Gains and losses are recognized in the consolidated statements of income when the loans and receivables are derecognized or impaired, as well as through the amortization process.

As of 31 December 2010, the Company’s and Subsidiaries’ have cash and cash

equivalents, trade and other receivables, due from related parties and other assets-restricted time deposits and cash in bank in this category.

● Available-For-Sale (AFS) financial assets AFS financial assets are non-derivative financial assets that are designated as available-

for-sale or are not classified as fair value through profit and loss, loans and receivables and held to maturity. After initial measurement, AFS financial assets are measured at fair value with unrealized gains or losses recognized in the shareholder’s equity until the investment is derecognized. At that time, the cumulative gain or loss previously recognized in the shareholder’s equity shall be reclassified to profit or loss as a reclassification adjustment.

The Company and Subsidiaries have other investments in shares of share that do not

have readily determinable fair value in which the ownership of equity interest is less than 20%. These investments are carried at cost.

ii. Financial Liabilities

Initial Recognition Financial liabilities within the scope of PSAK No. 55 (Revised 2006) are classified as financial

liabilities at fair value through profit or loss, loans and borrowings, or as derivatives designated as hedging instruments in an effective hedge, as appropriate. The Company and Subsidiaries determine the classification of their financial liabilities at initial recognition.

Financial liabilities are recognized initially at fair value which, in the case of loans and

borrowings, is inclusive of directly attributable transaction costs. As of 31 December 2010, the Company’s and Subsidiaries’ financial liabilities include loans

from banks and financing institution, bonds payable and sukuk ijarah - net, trade payables to third parties, other payables, due to related parties, accrued expenses, and deposits received - customer deposit and derivative liability.

The Company and Subsidiaries have determined that financial liabilities are categorized as

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

20

loans and borrowings and measured at fair value through profit or loss. Subsequent Measurement

● Loans and borrowings

After initial recognition, loans and borrowings are subsequently measured at amortized cost using the effective interest rate method.

Gains and losses are recognized in the consolidated statements of income when the

liabilities are derecognized as well as through the amortization process.

● Financial liabilities at fair value through profit or loss

Financial liabilities at fair value through profit or loss include financial liabilities held for trading and financial liabilities designated upon initial recognition at fair value through profit or loss.

Financial liabilities are classified as held for trading if they are acquired for the purpose of selling or repurchasing in the near term. Derivative liabilities are also classified as held for trading unless they are designated as effective hedging instruments.

Gains or losses on liabilities held for trading are recognized in the consolidated statements of income.

iii. Offsetting of financial instruments

Financial assets and financial liabilities are offset and the net amount reported in the

consolidated balance sheets if, and only if, there is a currently enforceable legal right to offset the recognized amounts and there is an intention to settle on a net basis, or to realize the assets and settle the liabilities simultaneously.

iv. Fair value of financial instruments

The fair value of financial instruments that are actively traded in organized financial markets is

determined by reference to quoted market bid prices at the close of business at the end of the reporting year. For financial instruments where there is no active market, fair value is determined using valuation techniques. Such techniques may include using recent arm’s length market transaction, reference to the current fair value of another instrument that is substantially the same, discounted cash flow analysis, or other valuation models.

Credit Risk Adjustment The Company and Subsidiaries adjust the price in the more observable market to reflect any

differences in counterparty credit risk between instruments traded in that market and the ones being valued for financial asset positions. In determining the fair value of financial liability positions, the Company’s and Subsidiaries’ own credit risk associated with the instrument is taken into account.

v. Amortized cost of financial instruments

Amortized cost is computed using the effective interest rate method less any allowance for

impairment and principal repayment or reduction. The calculation takes into account any premium or discount on acquisition and includes transaction costs and fees that are an integral part of the effective interest rate.

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

21

vi. Impairment of financial assets

The Company and Subsidiaries assess at each balance sheet date whether there is any objective evidence that a financial asset or a group of financial assets is impaired.

● Loans and receivables

For loans and receivables carried at amortized cost, the Company and Subsidiaries first assess whether objective evidence of impairment exists individually for financial assets that are individually significant, or collectively for financial assets that are not individually significant. If the Company and Subsidiaries determine that no objective evidence of impairment exists for an individually assessed financial asset, whether significant or not, the asset is included in a group of financial assets with similar credit risk characteristics, and the group is collectively assessed for impairment. Assets that are individually assessed for impairment and for which an impairment loss is, or continues to be, recognized are not included in a collective assessment of impairment.

If there is objective evidence that an impairment loss has occurred, the amount of the loss

is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows (excluding future expected credit losses that have not yet been incurred). The present value of the estimated future cash flows is discounted at the financial asset’s original effective interest rate. If a ”loans and receivables” financial asset has a variable interest rate, the discount rate for measuring impairment loss is the current effective interest rate.

The carrying amount of the financial asset is reduced through the use of an allowance for impairment account and the amount of the loss is recognized in the consolidated statements of income. Interest income continues to be accrued on the reduced carrying amount based on the original effective interest rate of the financial asset. Loans and receivables, together with the associated allowance, are written off when there is no realistic prospect of future recovery and all collateral has been realized or has been transferred to the Company and Subsidiaries. If, in a subsequent year, the amount of the estimated impairment loss increases or decreases because of an event occurring after the impairment was recognized, the previously recognized impairment loss is increased or reduced by adjusting the allowance for impairment account. If a future write-off is later recovered, the recovery is recognized in profit or loss.

● Available-For-Sale (AFS) financial assets

In the case of equity investments classified as an AFS financial asset, objective evidence would include a significant or prolonged decline in the fair value of the investment below its cost.

Where there is evidence of impairment, the cumulative loss - measured as the difference

between the acquisition cost and the current fair value, less any impairment loss on that investment previously recognized in profit or loss - is reclassified from shareholders’ equity to profit or loss. Impairment losses on equity investments are not reversed through the profit or loss; increases in their fair value after impairment are recognized in shareholders’ equity.

In the case of debt instruments classified as an AFS financial asset, impairment is

assessed based on the same criteria as financial assets carried at amortized cost. Future interest income is based on the reduced carrying amount and is accrued based on the rate of interest used to discount future cash flows for the purpose of measuring impairment loss. Such accrual is recorded as part of the “Interest income” account in the consolidated statement of income. If, in a subsequent period, the fair value of a debt instrument increases and the increase can be objectively related to an event occurring after the

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

22

impairment loss was recognized in profit or loss, the impairment loss is reversed through profit or loss.

vii. Derecognition of financial assets and liabilities

Financial Assets A financial asset (or where applicable, a part of a financial asset or part of a group of similar

financial assets) is derecognized when: (1) the rights to receive cash flows from the asset have expired, or (2) the Company and Subsidiaries have transferred their rights to receive cash flows from the asset or have assumed an obligation to pay the received cash flows in full without material delay to a third party under a “pass-through” arrangement; and either (a) the Company and Subsidiaries have transferred substantially all the risks and rewards of the asset, or (b) the Company and Subsidiaries have neither transferred nor retained substantially all the risks and rewards of the asset, but have transferred control of the asset.

Financial Liabilities

A financial liability is derecognized when the obligation under the liability is discharged or cancelled or has expired. When an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as a extinguishment of the original liability and the recognition of a new liability, and the difference in the respective carrying amounts is recognized in profit or loss.

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

23

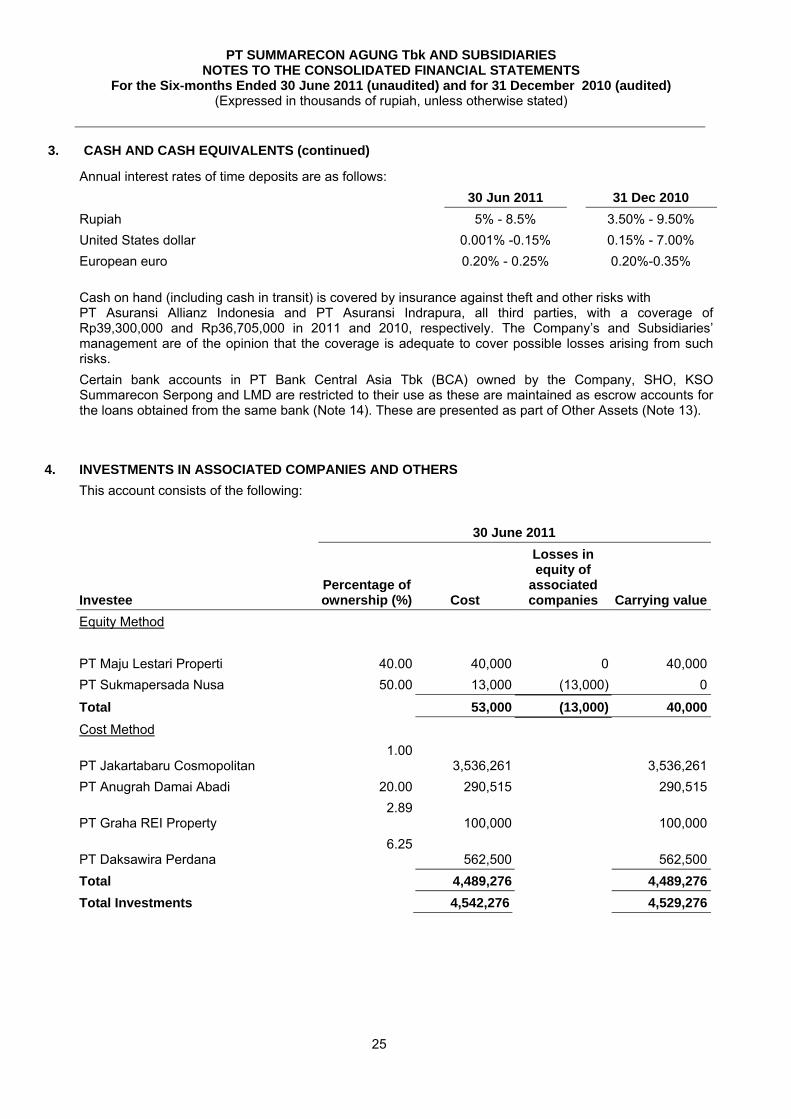

3. CASH AND CASH EQUIVALENTS

30 June 2011 31 December 2010

Cash and cash equivalents consist of the following:

Cash on hand

Rupiah 901,209 1,472,281

Foreign currencies 206,358 138,057

Total cash on hand 1,107,567 1,610,338

Cash in banks

Rupiah

PT Bank Central Asia Tbk 145,424,564 132,528,097

PT Bank Permata Tbk 45,620,106 17,867,312

PT Bank CIMB Niaga Tbk 9,636,462 10,691,776

PT Bank Bumi Arta Tbk 0 3,861,568

PT Bank Mega Tbk 1,785,911 3,794,919

PT. Bank Pan Indonesia Tbk 246,272 3,728,204

PT Bank Internasional Indonesia Tbk 83,908,901 2,401,080

PT Bank OCBC NISP Tbk 7,353,299 1,760,791

PT Bank Mandiri (Persero) Tbk 24,161,345 1,665,536

PT Bank UOB Buana 0 420,737

PT Bank Commonwealth 187,183 309,413

PT ANZ Panin Bank 0 232,297

PT Rabobank International Ind. 113,206 112,397

PT Bank Danamon Indonesia 0 4,572

PT Bank Resona Perdania 333,044 0

PT Bank Rakyat Indonesia 6,871 0

Lain-lain 733,720 56,972

United States dollar

PT Bank OCBC NISP Tbk 0 3,255,536

PT Bank CIMB Niaga Tbk 1,213,795 797,747

PT Bank Central Asia Tbk 756,695 316,386

PT Bank Resona Perdania 0 83,633

PT Bank Mandiri (Persero) 34,897 36,753

The ANZ Panin Bank 0 19,577

European euro

PT Bank OCBC NISP Tbk 0 1,081,529

The ANZ Panin Bank 46.026 44.845

Total cash in banks 321,562,297 185,071,677

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

24

3. CASH AND CASH EQUIVALENTS (continued)

30 June 2011 31 December 2010

Time deposits

Rupiah

PT Bank Mega Tbk 24,000,000 214,903,296

PT Bank Mega SyariahTbk 5,775,093 0

PT Bank Mandiri Tbk 238,370,768 207,130,619

PT Bank CIMB Niaga Tbk 117,060,175 117,748,352

PT Bank Permata Tbk 219,221,712 91,358,460

PT Bank OCBC NISP Tbk 37,310,877 77,855,694

PT Bank ICBC Indonesia 72,810,730 55,375,374

PT UOB Buana 86,200,000 34,993,241

PT Bank Central Asia Tbk 16,153,592 28,897,169

PT Bank Tabungan Negara 12,600,000 21,500,000

PT Bank Rakyat Indonesia 7,406,714 16,000,000

PT Bank Commonwealth 2,994,512 13,931,084

PT Bank Internasional Indonesia Tbk 7,000,000 12,982,219

PT Bank ICB Bumiputra Tbk 10,386,551 10,101,111

PT Bank Bumi Arta 0 10,000,000

PT Bank Capital Indonesia 5,143,831 5,013,041

PT Bank Pembangunan Daerah Jawa Barat dan Banten 1,400,000

1,400,000

PT Bank Resona Perdania 1,095,782 1,074,486

PT Bank Mayora 24,055,385 0

PT Bank Pan Indonesia Tbk 3,500,000 0

United States dollar

PT Bank Central Asia 15,461 6,048,014

PT Bank Resona Perdania 2,426,367 2,536,142

European euro

PT Bank Resona Perdania 3,918,191 3,756,767

PT ANZ Panin Bank 1,248,071 1,196,226

Total time deposits 900,093,812 933,801,295

Total cash and cash equivalents 1,222,763,676 1,120,483,310

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

25

3. CASH AND CASH EQUIVALENTS (continued)

Annual interest rates of time deposits are as follows:

30 Jun 2011 31 Dec 2010

Rupiah 5% - 8.5% 3.50% - 9.50%

United States dollar 0.001% -0.15% 0.15% - 7.00%

European euro 0.20% - 0.25% 0.20%-0.35%

Cash on hand (including cash in transit) is covered by insurance against theft and other risks with PT Asuransi Allianz Indonesia and PT Asuransi Indrapura, all third parties, with a coverage of Rp39,300,000 and Rp36,705,000 in 2011 and 2010, respectively. The Company’s and Subsidiaries’ management are of the opinion that the coverage is adequate to cover possible losses arising from such risks.

Certain bank accounts in PT Bank Central Asia Tbk (BCA) owned by the Company, SHO, KSO Summarecon Serpong and LMD are restricted to their use as these are maintained as escrow accounts for the loans obtained from the same bank (Note 14). These are presented as part of Other Assets (Note 13).

4. INVESTMENTS IN ASSOCIATED COMPANIES AND OTHERS

This account consists of the following:

30 June 2011

Investee Percentage of ownership (%) Cost

Losses in equity of

associated companies Carrying value

Equity Method

PT Maju Lestari Properti 40.00 40,000 0 40,000

PT Sukmapersada Nusa 50.00 13,000 (13,000) 0

Total 53,000 (13,000) 40,000

Cost Method

PT Jakartabaru Cosmopolitan

1.003,536,261

3,536,261

PT Anugrah Damai Abadi 20.00 290,515 290,515

PT Graha REI Property

2.89100,000

100,000

PT Daksawira Perdana

6.25562,500

562,500

Total 4,489,276 4,489,276

Total Investments 4,542,276 4,529,276

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

26

4. INVESTMENTS IN ASSOCIATED COMPANIES AND OTHERS (continued)

31 December 2010

Investee Percentage of ownership (%) Cost

Losses in equity of

associated companies Carrying value

Equity Method

PT Swaraeka Prasetia 25.33 7,600,000 (7,600,000) 0

PT Maju Lestari Properti 40.00 40,000 0 40,000

PT Sukmapersada Nusa 50.00 13,000 (13,000) 0

7,653,000 (7,613,000) 40,000

Cost Method

PT Jakartabaru Cosmopolitan

1.00 3,536,261

3,536,261

PT Anugrah Damai Abadi

20.00 290,515

290,515

PT Graha REI Property

2.89 100,000

100,000

PT Daksawira Perdana

6.25 62,500

62,500

3,989,276 3,989,276

Total Investments 11,642,276 4,029,276

In December 2010, the Company and BMS, a Subsidiary, sold all their shares of share in BNL for Rp6,771,114 based on the sale/purchase of shares agreement notarized under deeds No. 105 and No. 106 dated 23 December 2010 of Dewi Himijati Tandika, S.H. There was no gain on the sale. The principal activities of the above investees are as follows:

Investee Country of Domicile

Principal business activity

Equity Method

PT Swaraeka Prasetia Indonesia Real estate

PT Maju Lestari Properti Indonesia Real estate

PT Sukmapersada Nusa Indonesia Real estate

Cost Method PT Jakartabaru Cosmopolitan Indonesia Real estate

PT Anugrah Damai Abadi Indonesia Food & Beverage

PT Graha REI Property Indonesia Real estate

PT Daksawira Perdana Indonesia Real estate

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

27

5. TRADE RECEIVABLES

The details of trade receivables are as follows:

30 June 2011 31 December 2010

Related parties (Note 31)

Sale of landplots 1,590,909 2,648,182

Third parties

Sale of apartment units 3,700,199 7,228,565

Sale of houses, shops and landplots 23,681,949 72,174,388

Rental of retail and commercial investment properties 9,706,359 4,547,761

Hotel services 0 1,038,218

Rental of residential and office investment properties 4,615,050 765,510

Monthly membership fees in sports club 437,052 969,595

Fees in Apartment and clean water management 674,763 0

Total trade receivables 44,406,281 89,372,219

The aging analysis of trade receivables is presented below:

30 June 2011 31 December 2010

Current 23,567,136 35,308,240

Overdue:

1 to 30 days 9,700,463 30,599,521

31 to 60 days 9,090,299 7,983,762

61 to 90 days 463,250 6,928,679

Over 90 days 1,585,133 8,552,017

Total trade receivables 44,406,281 89,372,219

As of 30 June 2011 and 31 December 2010, trade receivables amounting to Rp6,236,759 and Rp5,255,013, respectively, are pledged as collateral for loans payable to BCA (Note 14).

Based on a review of the status of the individual receivables at the end of the year, the Company’s and Subsidiaries’ management believe that all trade receivables are fully collectible.

6. OTHER RECEIVABLES

This account consists of receivables from:

30 June 2011 31 December 2010

Mantolli International Corporation, Republic Mauritius 46,337,993 46,337,993

PT Jakarta Cakratunggal Steel 66,089,746 55,892,247

Others 3,053,229 19,724,970

Total other receivables 115,480,968 121,955,210

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

28

Based on the sale/purchase of shares agreement notarized under deed No. 28 dated 19 December 2003 of Dewi Himijati Tandika, S.H., the Company sold 39,800 shares of share of PT Jakartabaru Graha Permai (JGP) to Mantolli. Based on notarial deed No. 18 dated 30 October 2009 of Suzy Anggraini Muharam, S.H., the Company sold the remaining 77,275 shares of share of JGP to Mantolli (Note 4).

The receivable from Mantolli is non-interest bearing and is collateralized by shares of JGP owned by Mantolli. The Company has the right to take over the collateral if Mantolli is not able to pay the receivable. This receivable was initially due on 18 December 2009 but this date was extended to 20 December 2013 and is repayable in annual installments of Rp17,484,000 each starting from 2009, with the final installment being due on 30 December 2013. The first and second installments were paid on 30 December 2009 and 2010, respectively.

Based on the review of the status of individual receivables at the end of the year, management believe that all other receivables are fully collectible.

7. INVENTORIES

30 June 2011 31 December 2010

Inventories consist of:

Inventories available for sale

Land 0 71,268,876

Houses 22,121,918 93,798,572

Shops 4,336,239 7,893,122

Apartments 344,347 3,300,128

Total inventories available for sale 26,802,504 176,260,698

Inventories under development/construction

Apartments 40,288,594 38,652,425

Buildings 1,195,157,432 787,765,111

Land 234,995,206 298,169,848

Total inventories under development/construction 1,470,441,232 1,124,587,384

Others 22,994,892 7,585,275

Total inventories 1,520,238,628 1,308,433,357

The movements of houses and shops under development/construction are as follows:

30 June 2011 31 December 2010

Beginning balance of building inventories under development/construction

787,765,111

269,726,638

Production costs 599,964,934 1,058,500,800

Ending balance of building inventories under development/construction

(1,195,157,432)

(787,765,111)

Development costs 192,572,613 540,462,327

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

29

7. INVENTORIES (continued)

30 June 2011 31 December 2010

The movements of houses and shops available for sale are as follows:

Houses 93,798,572 6,752,589

Shops 7,893,122 20,172,005

Cost of sales:

Houses (224,772,092) (384,522,586)

Shops (43,034,058) (81,172,641)

Ending balance of houses and shops inventories available for sale 26,458,157 101,691,694

Real estate development inventories which are already covered by signed sales/purchase agreements but have not yet been recognized as sales are as follows:

30 June 2011 31 December 2010

Inventories available for sale

Houses 21,735,746 85,827,964

Shops 1,154,421 4,711,304

Total inventories available for sale 22,890,167 90,539,268

Inventories under development/construction

Buildings 728,204,243 267,071,762

Total inventories under development/construction 728,204,243 267,071,762

Total 751,094,410 357,611,030

As of 30 June 2010, inventories in such properties known as Royal Orchard 1, Ebony, Clover, New Batavia, Beryl, Jasmine, PHG-Jade, and PHG-Turquoise are available for sale, and inventories in Royal Orchard 2, Royal Orchard 3, Graha Boulevard, Palm Residence, Maple Residence, Acacia Residence, Crown, Dalton, Darwin, Grisea, Canary, Pascal, and New Jasmine are under development/construction. Houses, shops and apartment inventories are covered by insurance against fire and other risks with PT Asuransi Allianz Indonesia, PT Asuransi AXA Indonesia, PT Asuransi Jaya Proteksi, PT Kurnia Insurance Indonesia, PT Asuransi Indrapura, ACE INA Insurance, PT Tri Dharma Proteksi, PT MAA General Assurance, and PT Asuransi Ekspor Indonesia, all third parties, with total coverage of US$35,225,000 and Rp382,447,961 in 2011 and 2010. The Company's and Subsidiaries’ management are of the opinion that the above coverage is adequate to cover possible losses arising from such risks.

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

30

8. PREPAID EXPENSES

30 June 2011 31 December 2010

This account consists of prepayments to third parties for:

Rent 116,488 12,500

Insurance 1,993,068 2,181,333

Advertisement and promotion 7,543,522 0

Others 15,776,592 3,602,303

Total prepaid expenses 25,429,670 5,796,136

9. ADVANCES

This account consists of advances for: 30 June 2011 31 December 2010

Purchase of:

Land 286,974,711 313,273,186

Fixed assets 9,039,204 1,468,548

Construction materials 24,845,887 147,399,576

Others 53,348,740 6,796,115

Total advances 374,208,542 468,937,425

10. UNDEVELOPED LAND

30 June 2011 31 December 2010

Location Area (m2) Amount Area (m2) Amount

Gading Serpong 1,957,090 668,750,348 2,090,156 516,137,252

Pegangsaan Dua

Bekasi – Kota 2,199,482 483,727,199 1,897,234 411,047,216

Kelapa Gading 6,268 8,441,940 6,268 8,441,940

Cakung 188,374 122,810,950 188,374 124,423,650

Slipi 12,046 28,565,475 12,046 28,565,475

Pulo Gadung 2,944 427,821 2,944 427,821

Ciketing 149,220 306,342 149,220 306,342

Rorotan 24,300 97,953 24,300 97,953

Gede bage 77,382 260,502,026 54,120 13,709,644

Bali 1,200 3,600,000 0 0

Cisarua 2,900 56,933 2,900 56,933

Total undeveloped land 4,621,206 1,577,286,987 4,427,562 1,103,214,226

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

31

10. UNDEVELOPED LAND (continued)

The status of ownership of undeveloped land is as follows:

30 June 2011 31 December 2010

Status Area (m2) Area (m2)

Released rights (“pelepasan hak”) 2,988,578 3,014,094

Land certificates already issued 1,632,628 1,413,468

Total 4,621,206 4,427,562

As of 30 June 2011 undeveloped land properties of Rp316,790,097 are pledged as collateral for loans from PT BCA Tbk and bonds payable (Notes 14 and 15). As of 31 December 2010 undeveloped land properties of Rp.323,017,708, are pledged as collateral for loans from PT BCA Tbk, PT Bank Mandiri, and bonds payable (Notes 14,15).

11. FIXED ASSETS

The details of fixed assets are as follows:

30 June 2011

Balance as of 1 January 2011 Additions Deductions Reclassifications

Balance as of 30 June 2011

2011 Movements

Cost

Land 13,416,622 0 0 0 13,416,622

Buildings and infrastructures 296,600,275 1,810,753 74,188 29,650 298,366,490

Machinery and heavy equipment 42,712,937 3,797,999 0 0 46,510,936

Vehicles 47,598,688 10,677,406 3,818,533 267,376 54,724,937

Furniture and office equipment 93,185,806 9,555,359 214,479 242,033 102,768,719

493,514,328 25,841,517 4,107,200 539,059 515,787,705

Construction in progress 63,208,609 197,065,037 101,354 (984,552) 259,187,740

Total cost 556,722,937 222,906,554 4,208,554 (445,493) 774,975,445

Accumulated depreciation

Buildings and infrastructures 79,164,853 13,193,959 74,188 0 92,284,624

Machinery and heavy equipment 10,459,443 1,643,125 0 0 12,102,568

Vehicles 26,127,112 4,152,059 3,240,613 35,554 27,074,112

Furniture and office equipment 61,865,056 6,129,184 179,083 (10,569) 67,804,588

Total accumulated depreciation 177,616,464 25,118,327 3,493,884 24,985 199,265,892

Net book value 379,106,473 575,709,553

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

32

11. FIXED ASSETS (continued)

31 December 2010

Balance as of 1 January 2010 Additions Deductions Reclassification

Balance as of 31 Dec 2010

2010 Movements

Cost

Land 14,599,478 0 0 (1,182,856) 13,416,622

Buildings and infrastructures 208,245,849 5,223,950 502,965 43,206,838 256,173,672

Hotel facilities 0 40,426,603 0 0 40,426,603

Machinery and heavy equipment 12,867,726 25,725,845 0 4,119,366 42,712,937

Vehicles 39,894,073 10,708,161 2,979,173 (24,373) 47,598,688

Furniture and office equipment 79,542,141 16,069,638 445,867 (1,980,106) 93,185,806

355,149,267 98,154,197 3,928,005 44,138,869 493,514,328

Construction in progress 79,994,036 111,194,398 0 (127,979,825) 63,208,609

Total cost 435,143,303 209,348,595 3,928,005 (83,840,956) 556,722,937

Accumulated depreciation

Buildings and infrastructures 56,424,526 17,431,552 502,965 (176,227) 73,176,886

Hotel facilities 0 5,987,967 0 0 5,987,967

Machinery and heavy equipment 7,037,558 3,451,481 0 (29,596) 10,459,443

Vehicles 21,486,390 7,174,947 2,526,341 (7,884) 26,127,112

Furniture and office equipment 52,309,350 10,621,018 436,579 (628,733) 61,865,056

Total accumulated depreciation 137,257,824 44,666,965 3,465,885 (842,440) 177,616,464

Net book value 297,885,479 379,106,473

The details of construction in progress as of 30 June 2011 and 31 December, 2010 are as follows:

30 June 2011 31 December 2010

Project Amount

Percentage of completion (%) Amount

Percentage of completion (%)

Hotel Kelapa Gading

Summarecon Mall Seporng II 144,078,924 53 20,927,082 2

Pahoa boarding house 7,869,685 95 463,746 0

Hospital 34,513,593 95 18,633,298 61

Klub Kelapa Gading refurbishment 27,314,256 92 16,868,943 35

Orchard Junction 12,355,972 10 0 0

Others 33,055,310 6,315,540

Total 259,187,740 63,208,609

The percentages of completion of the construction in progress as of 30 June 2011 and 31 December 2010 are based on the actual expenditures incurred compared to the total budgeted project cost. Fixed assets, except land, are covered by insurance against fire, flood and other risks (all-risks) under

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

33

blanket policies with several companies, including PT Asuransi Mitsui Sumitomo Indonesia Group, PT Asuransi Allianz Indonesia, PT Asuransi Central Asia, PT Asuransi Indrapura, PT Kurnia Insurance Indonesia, PT Asuransi Umum Mega, PT Asuransi Sinar Mas, and PT Asuransi Himalaya Pelindung, all third parties, for US$22,543,550 and Rp48,536,909 in 2011 and 2010. SHO, a Subsidiary, also covered by insurance against terrorism and sabotage amounting to US$5,000,000 in 2011 and 2010, respectively. In addition, the Company and Subsidiaries obtained insurance against business interruption amounting to Rp36,199,485 and Rp47,369,170 in 2011 and 2010, respectively. The Company’s and Subsidiaries’ management are of the opinion that the above coverages are adequate to cover possible losses arising from such risks. As of 30 June 2011 and 31 December 2010, fixed assets with net book value of Rp59,128,232 and Rp29,182,935, respectively, are pledged as collateral for the loans from banks and financing institution (Note 14). Based on the Company’s and Subsidiaries’ assessment, there were no events or changes in circumstances which indicated an impairment in the value of fixed assets as of 30 June 2011 and 31 December 2010.

12. INVESTMENT PROPERTIES

The details of investment properties 30 June 2011 and 31 Desember 2010 are as follows:

30 June 2011

Balance as of 1 January 2011 Additions Deductions Reclassifications

Balance as of 30 June 2011

2011 Movements

Cost

Land 411,027,113 143,000 0 0 411,170,113

Buildings and infrastructures 990,100,753 5,485,890 57,900 (29,509,691) 966,019,052

Machinery and heavy equipment 186,009,967 5,609,009 1,114 29,382,858 221,000,720

Total cost 1,587,137,833 11,237,899 59,014 (126,833) 1,598,189,885

Accumulated depreciation

Buildings and infrastructures 235,346,963 12,250,301 (373,615) 247,223,649

Machinery and heavy equipment 73,401,673 9,780,146 1,224,286 84,406,049

Total accumulated depreciation 308,748,636 22,030,447 850,671 331,629,698

Net book value 1,278,389,197 1,266,560,187

PT SUMMARECON AGUNG Tbk AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the Six-months Ended 30 June 2011 (unaudited) and for 31 December 2010 (audited) (Expressed in thousands of rupiah, unless otherwise stated)

34

12. INVESTMENT PROPERTIES (continued)

31 December 2010

Balance as of 1 January 2010 Additions Deductions Reclassification

Balance as of 31 Dec 2010

2010 Movements

Cost

Land 410,490,356 536,757 0 0 411,027,113

Buildings and infrastructures 920,257,717 12,458,415 0 57,384,621 990,100,753

Machinery and heavy equipment 171,558,023 5,817,886 0 8,634,058 186,009,967

Total cost 1,502,306,096 18,813,058 0 66,018,679 1,587,137,833

Accumulated depreciation

Buildings and infrastructures 212,510,276 23,060,196 0 (223,509) 235,346,963

Machinery and heavy equipment 55,772,919 17,628,754 0 0 73,401,673

Total accumulated depreciation 268,283,195 40,688,950 0 (223,509) 308,748,636

Net book value 1,234,022,901 0 0 1,278,389,197