thirty years of california library ballot measures presented by richard b. hall library consultant...

TRANSCRIPT

Thirty Years of

California Library Ballot Measures

Presented byPresented by

Richard B. HallRichard B. HallLibrary ConsultantLibrary Consultant

Assistance from Donna CorbeilAssistance from Donna Corbeil

Director, Berkeley Public LibraryDirector, Berkeley Public Library

Preface

1996 Dr. Bruce Cain Study1996 Dr. Bruce Cain Study

Results of 2009 SurveyResults of 2009 Survey

Full Study on CSL Website @Full Study on CSL Website @

http://www.library.ca.gov/lds/lds.html

Downloadable Excel SpreadsheetDownloadable Excel Spreadsheet

Future Updates?Future Updates?

CA Ballot Measure Environment

Survey includes Special & General TaxesSurvey includes Special & General Taxes

General Taxes = Simple MajorityGeneral Taxes = Simple Majority

May Fund Any ServiceMay Fund Any Service

Special Taxes = SupermajoritySpecial Taxes = Supermajority

May Fund May Fund ONLYONLY Specific Service Specific Service

Overview 307 Ballot Measures in 30 Years307 Ballot Measures in 30 Years

In 95 of 181 Library JurisdictionsIn 95 of 181 Library Jurisdictions

CA: 54% of all Measures PassedCA: 54% of all Measures Passed Compares poorly to 80% National RateCompares poorly to 80% National Rate

CA: AVG “Yes” Vote of 62%CA: AVG “Yes” Vote of 62% Same as National AVGSame as National AVG

Why? – Why? – Supermajority RequirementSupermajority Requirement

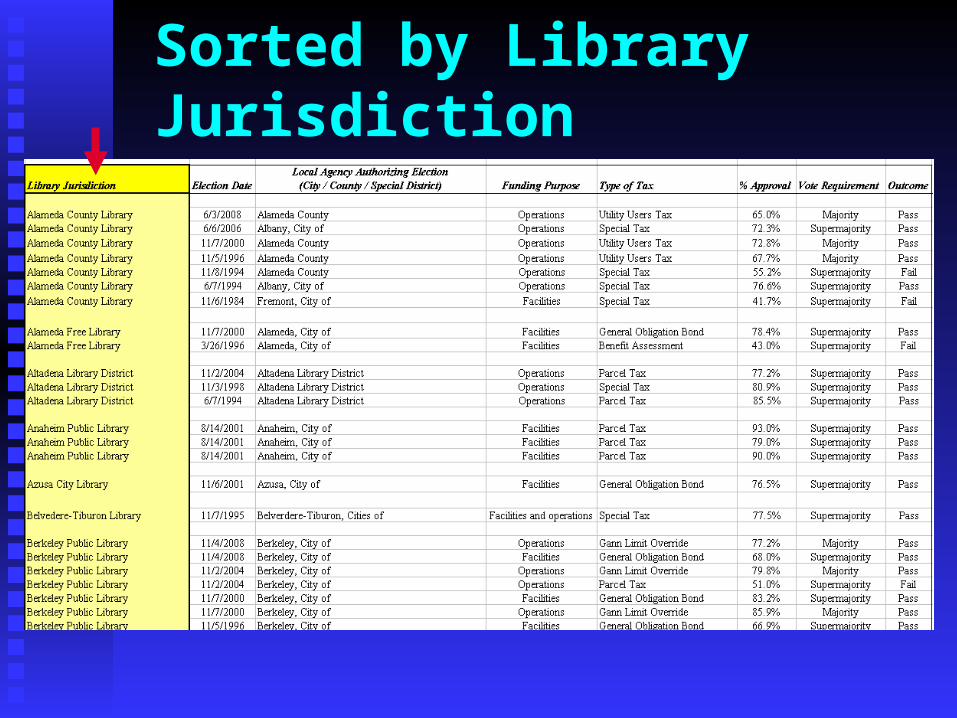

7 Data Elements Collected

Name of Library JurisdictionName of Library Jurisdiction

Election DateElection Date

Local Agency Authorizing ElectionLocal Agency Authorizing Election

Funding PurposeFunding Purpose

Type of TaxType of Tax

Vote RequirementVote Requirement

Election OutcomeElection Outcome

Sorted by Library Jurisdiction

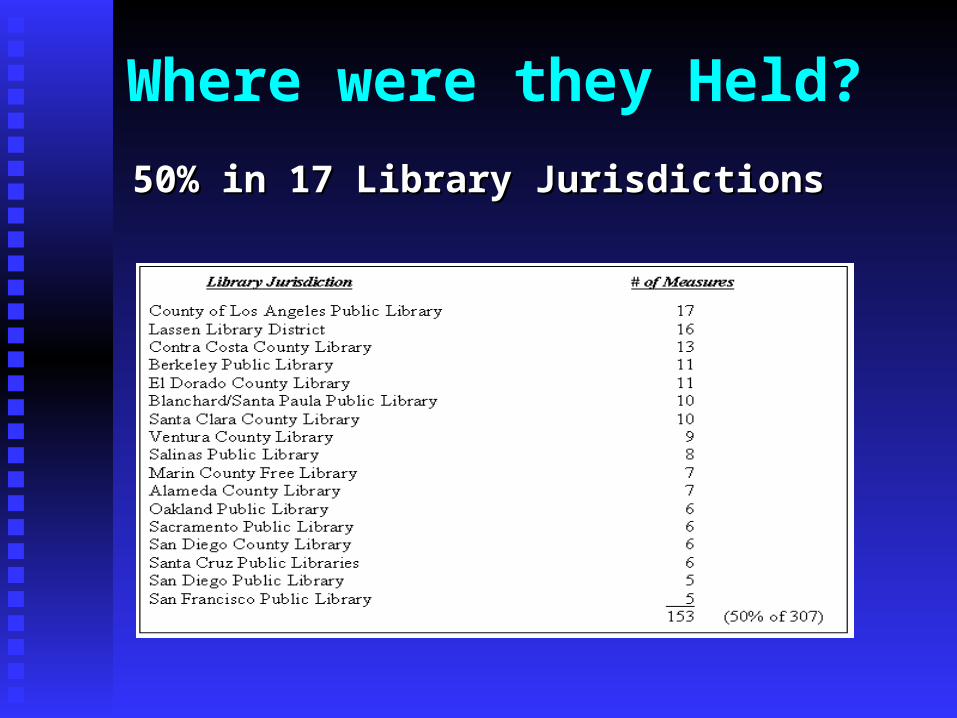

Where were they Held?

50% in 17 Library Jurisdictions50% in 17 Library Jurisdictions

Sorted by Local Agency

Over 150 Local AgenciesOver 150 Local Agencies

Sorted by Election Outcome

California: 53.7% PassedCalifornia: 53.7% Passed

80% Passed Nationally80% Passed Nationally

Sorted by “Yes” Vote Percentage

Average 62.1% (Same as National)Average 62.1% (Same as National) Range from 29% to 93%Range from 29% to 93%

Sorted by Election Date

30 Years: From 2009 back to 198030 Years: From 2009 back to 1980

Slight Improvement Each Decade

Sorted by Funding Purpose

Facilities, Operations, & Both TogetherFacilities, Operations, & Both Together

Most Measures for Operations

Facilities had Highest Approval RateFacilities had Highest Approval Rate

Facilities & Operations Lowest Approval RateFacilities & Operations Lowest Approval Rate

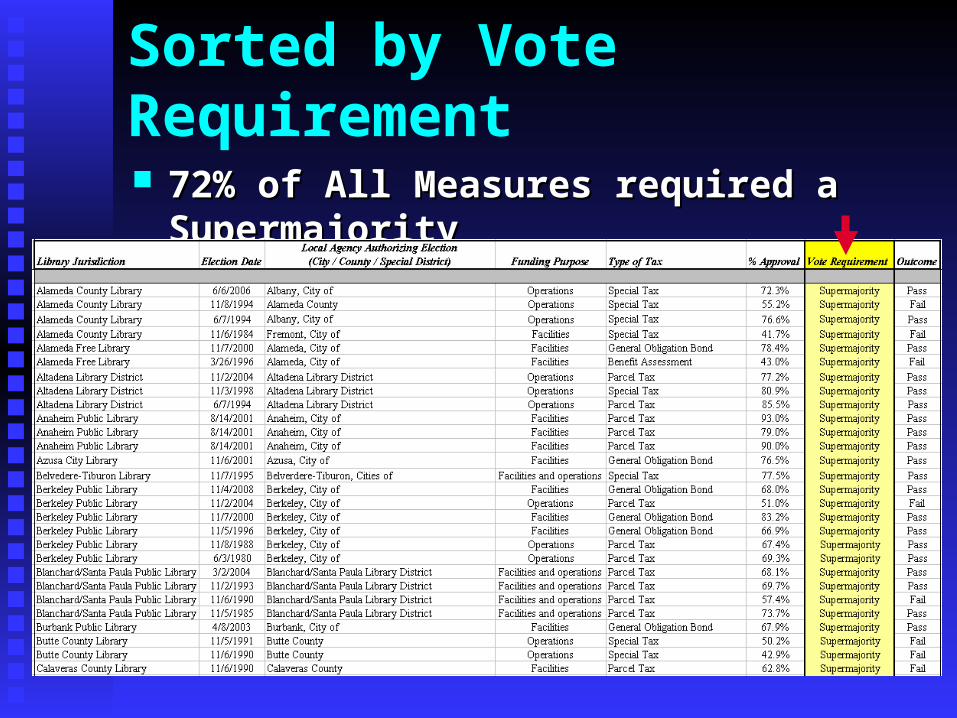

Sorted by Vote Requirement

72% of All Measures required a Supermajority72% of All Measures required a Supermajority

Supermajority vs Simple Majority

45% of Supermajority Measures Passed45% of Supermajority Measures Passed

77% of Simple Majority Measures Passed77% of Simple Majority Measures Passed

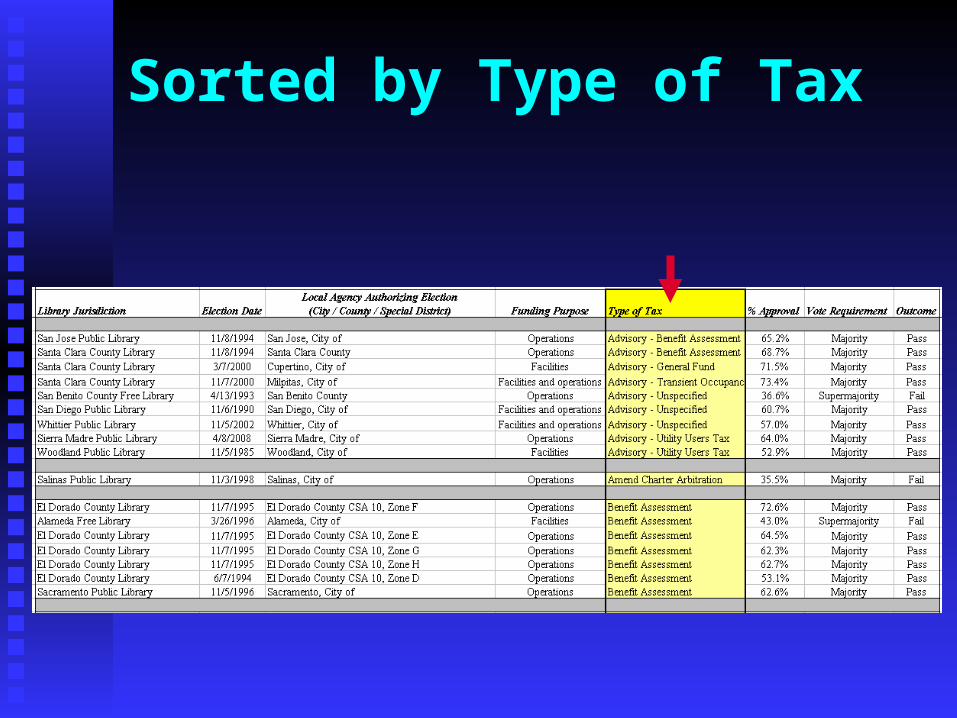

Sorted by Type of Tax

9 Types of Taxes

Benefit AssessmentBenefit Assessment Business License TaxBusiness License Tax Excise TaxExcise Tax General Obligation Bond General Obligation Bond Parcel TaxParcel Tax Sales TaxSales Tax Special TaxSpecial Tax Transient Occupancy TaxTransient Occupancy Tax Utility User TaxUtility User Tax

Parcel Tax

A parcel tax is generally one form of special A parcel tax is generally one form of special tax that is applied uniformly on a per-tax that is applied uniformly on a per-parcel basis and not on an ad-valorem basis parcel basis and not on an ad-valorem basis (in proportion to property value) like (in proportion to property value) like property taxes. It is established at a flat property taxes. It is established at a flat rate for each parcel type, e.g. residential or rate for each parcel type, e.g. residential or commercial, regardless of size or value of commercial, regardless of size or value of the property, or it may be levied according the property, or it may be levied according to some other formula such as acreage of to some other formula such as acreage of the lot or number of bedrooms.the lot or number of bedrooms.

Sales Tax

Also known as a transaction and use tax, Also known as a transaction and use tax, a sales tax is generally applied to the sale a sales tax is generally applied to the sale of goods and services usually as a percent of goods and services usually as a percent of the cost of the transaction. The of the cost of the transaction. The percentage is often described in terms of percentage is often described in terms of cents, i.e., a ½ cent sales tax (on every cents, i.e., a ½ cent sales tax (on every dollar expended).dollar expended).

General Obligation Bond

A general obligation (G.O.) bond is a debt A general obligation (G.O.) bond is a debt financing instrument which is used to financing instrument which is used to fund large capital facilities projects. In fund large capital facilities projects. In California, G.O. bonds must be approved California, G.O. bonds must be approved by a ballot measure and are for a specific by a ballot measure and are for a specific purpose such as to construct a new public purpose such as to construct a new public library building. The issuance of G.O. library building. The issuance of G.O. bonds are backed by the “full faith and bonds are backed by the “full faith and credit” of the funding agency. credit” of the funding agency.

Special Tax

Generically, a special tax is levied for a Generically, a special tax is levied for a specific purpose such as providing library specific purpose such as providing library services only. Special taxes “may be services only. Special taxes “may be applied on a uniform basis to real property applied on a uniform basis to real property or on the basis of benefit, cost of providing or on the basis of benefit, cost of providing services or other reasonable basis services or other reasonable basis (Government code section 53717.3).”5 The (Government code section 53717.3).”5 The use of the income from special taxes is use of the income from special taxes is limited to the specific program for which limited to the specific program for which the tax is levied, the tax is levied, andand the proceeds must be the proceeds must be placed in a separate account from the placed in a separate account from the general fund. general fund.

Utility Users Tax

A utility users tax is an excise tax levied A utility users tax is an excise tax levied on utility customers. In California, on utility customers. In California, “Cities are empowered to levy taxes upon “Cities are empowered to levy taxes upon the use of utilities (such as electricity, gas, the use of utilities (such as electricity, gas, telephone, and cable television) . . . .” 6telephone, and cable television) . . . .” 6

Most Commonly Use Type of Tax

Parcel Tax is Most Common @ 30%Parcel Tax is Most Common @ 30%

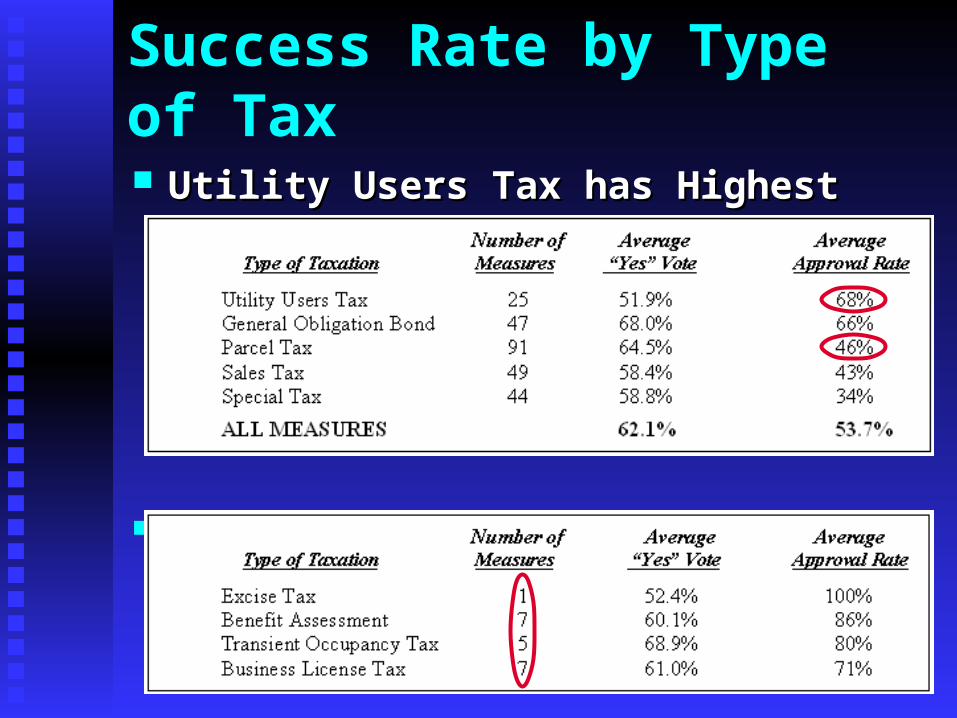

Success Rate by Type of Tax

Utility Users Tax has Highest Approval RateUtility Users Tax has Highest Approval Rate

Not Statistically SignificantNot Statistically Significant

Conclusion

The Supermajority RequirementThe Supermajority Requirement 45% Approval Rate for Special Taxes45% Approval Rate for Special Taxes 77% Approval Rate for General Taxes77% Approval Rate for General Taxes

Remarkable Consistency w/ Cain StudyRemarkable Consistency w/ Cain Study More In-depth Data & AnalysisMore In-depth Data & Analysis

CA Library Referenda CampaignsCA Library Referenda Campaigns Compares CA to National DataCompares CA to National Data

Future Data Collection?Future Data Collection?