this changes everything. why lock hain is…..?€¦ · •blockchain may just be as transformative...

TRANSCRIPT

This Changes Everything. Why BlockChain is…..?

CUNA

THE NATIONAL ROUNDTABLE

MWCUA

TECHNOLOGY PARTNERS: BEST INNOVATION GROUP AND EVERNYM

OCTOBER, 2016

Key Points

• Blockchain may just be as transformative as the internet was in the late 90’s.

• Introducing CULedger. Its an industry wide opportunity to create a managed BlockChain network: Deploy, Compete and Secure both inside our industry and outside our industry.

• Imagine no more passwords to reset and reduced calls to your call center.

Can BlockChain fix CyberSecurity?

• National CyberSecurity Awareness Month

• https://www.dhs.gov/national-cyber-security-awareness-month

• The National Credit Union Information Sharing and Analysis Center

o www.ncuisao.org is under construction

Leadership of the NCU-ISAO

• Boeing Employees Credit Union

• Payment Services for Credit Unions (PSCU)

• Open Technology Solutions (OTS)o Representing Bellco, Bethpage, and SECU

• Mountain West Credit Union Association

• Baxter Credit Union

• Spokane Teachers Credit Union

Back to BlockChain : JP Morgan wouldn’t spend billions of dollars on hype…

BlockChain Is NOT Bitcoin

It’s the elegant underlying technology that enables BITCOIN.

It is also known as ◦ Shared Ledger

◦ Distributed Ledger

A CU BlockChain Defined

•A type of distributed ledger, comprised of unchangeable, digitally recorded data in packages called blocks (rather like collating them on to a single sheet of paper). Each block is then ‘chained’ to the next block, using a cryptographic signature. This allows block chains to be used like a ledger, which can be shared and accessed by anyone with the appropriate permissions.

Blockchain Glossary - HASH

•A hash algorithm turns an arbitrarily-large amount of data into a fixed-length hash. The same hash will always result from the same data, but modifying the data by even one bit will completely change the hash. Like all computer data, hashes are large numbers, and are usually written as hexadecimal.

•dfdec888b72151965a34b4b59031290a

Blockchain Glossary - Cryptocurrency

•A form of digital currency based on mathematics, where encryption techniques are used to regulate the generation of units of currency and verify the transfer of funds. Furthermore, cryptocurrencies operate independently of a central bank.

Blockchain Glossary – Unpermissioned Ledger

• Unpermissioned ledgers such as Bitcoin have no single owner

• Indeed, they cannot be owned. The purpose of an unpermissioned ledger is to allow anyone to contribute data to the ledger and for everyone in possession of the ledger to have identical copies. This creates censorship resistance, which means that no actor can prevent a transaction from being added to the ledger.

Blockchain Glossary – Permission Ledger

• Permissioned ledgers may have one or many owners. When a new record is added, the ledger’s integrity is checked by a limited consensus process. This is carried out by trusted actors —government departments or Credit Unions, for example — which makes maintaining a shared record much simpler that the consensus process used by unpermissioned ledgers.

• Permissioned block chains provide highly-verifiable data sets because the consensus process creates a digital signature, which can be seen by all parties. A permissioned ledger is usually fasterthan an unpermissioned ledger.

2 Types of Blockchains

PERMISSIONLESS

Proof of work

Anyone with a computer anywhere can participate in a permissionless Blockchain as a node

No governance ◦ 60% of Bitcoin is now controlled by two entities

in China

Performance is slower

PERMISSIONED

Only known vetted identities can participate

Governance ◦ Entities are vetted

◦ Performance is monitored

No Anonymous nodes

Faster Performance

Permissioned versus Permissionless5 questions to help you determine which is which

5 QUESTIONS

1. Who maintains it?

PERMISSIONED

Anyone that wants toA group of permissioned

2. How are they incentivized to do it right

3. Who produces the underlying data or can send transactions

4. Who has access to that data?

5. Where is it stored?

Reputational Risk

Permissioned and vetted entities, i.e., Credit unions and third party providers

Small group of trusted entities and data owners

Servers on a known network

Rewards, carrot and stick, cash

Anyone that wants to

Anyone , transparency

Massively distributed

PERMISSIONLESS

Blockchain Glossary continued

• Transaction BlockoA collection of transactions on a network, gathered into

a block that can then be hashed and added to the BlockChain.

• Smart ContractsoSmart contracts are contracts whose terms are recorded

in a computer language instead of legal language. Smart contracts can be automatically executed by a computing system, such as a suitable distributed ledger system.

What are we Hearing?• As featured on CBRonline.com

• 200 banks surveyed

• 15% banks expect full BlockChain solutions by 2017

• 65% banks expect to have full BlockChain solutions running within the next three years

• Use cases that are leading include lending, payments, and reference datao The credit union industry is leading out with identity to tackle CNP Fraud and lending

• There is much work to do:o 56% said that regulatory constraints are the top barrier to success

o 54% cite immature technology

o 52% are concerned about a lack of clear return on investment

o Adoption is critical

How the Ledgers are chained up

• Each Ledger is tied to the previous Ledger via a hash (a unique ID)

• The next Ledger references the previous Ledger hash (unique id)

• Each Ledger could contain 1 or 1000’s of transactions , or any other kind of data

• Entities that need the transaction information are identified through cryptography

o Public Key’s and Private Key’s for entities

18

CU A

CU B

1. Credit Union A sends money to Credit Union B

2. Credit Union goes through CUFX Gateway to Distributed Ledger network

Gateway Node

3. Transaction is converted to a encrypted block

4. The ledger is broadcast to every part of the network

Validator Nodes

Validator Nodes

5. Each Node approves the transaction –Consensus is achieved

6. The ledger is then added to the chain which provides a indelible record of the event

7. The gateway is notified of a transaction for Credit Union B

8. Credit Union B receives

the transaction

Why is Blockchain Valuable?• Stored data is guaranteed availability

• You can run applications on them and be guaranteed an extremely high uptime

• You can run applications on them, and be guaranteed an extremely high uptime going very far into the future

• You can run applications on them, and show your users that the application’s logic is honest and is doing what you are advertising that it does

• You can run applications on them, and those applications can talk to each other with 100% reliability – even if the underlying platform has only 99.999% reliability

• You can build applications that very easily and efficiently take advantage of the data produced by other applications (eg. combining payments and reputation systems is perhaps the largest gain here)

Blockchain’s Potential• FINANCIAL

• NON – FINANCIAL

Blockchain’s Potential – Financial• Smart Contractso Indirect Lending

• Smart Asseto Titles

• Clearing and Settlemento Instant reconciliationo Its possible to have no more

holds

• Paymentso P2P

• Digital Identities

• Member

• Contract

Signed

Member App

Crypto Key

BC Client• Contract

• Key Match

Blockchain

• Contract Sense

• Response

Credit Union

• Member

• Contract

Update

Member App

• Smart Contract

Key Match

Blockchain• Contract

Attributes

• Crypto Key

BC Client

• Contract Sense

• New Attributes

Credit Union

Introduction To The CULedger “Research to Action” InitiativeTHE CREDIT UNION OWNED AND OPERATED BLOCKCHAINNETWORK THAT EVERYONE CAN PARTICIPATE IN AND PROFIT FROM- IF WE CHOOSE TO BUILD IT..

The CULedger Open Source Project

Concept• Explore creating a specialized Credit Union

Ledger

• Goals

o Remove barriers for entry for all Credit Unions

o Normalize platform before we start using

o Create interoperability among all Credit unions regardless of

Cores

Third Party products

Platforms

o Reach adoption and implementation sooner rather than later

CULedger Participation

• Over 80 organizations and credit unions from across the country

• Led by CUNA, Mountain West Credit Union Association, Best Innovation Group, and the National Credit Union Roundtable

• Raising an initial $1.5 Million for initial proof of conceptso Raised approximately half of that amount

Executive Steering Committee

CUNA

CO-OP

CSCU

PSCU

CU Direct

PenFed CU

MWCUA

Royal CU

United Nations FCU

Digital CU

Baxter CU

First Education FCU

Vancouver City Savings CU

Visions CU

Truliant CU

Mountain America

26

www.CULedger.com

Products to review◦ Evernym’s Sovrin Platform◦ RIPPLE◦ ETHEREUM◦ BITCOIN

CU/CUSO Participation◦ Programmers◦ Designers ◦ Product management ◦ Researchers◦ Funding

CU portal for signing up and getting involved

CUFX Compliant from Day 1 • Core integration

• Third party application integration

• Device integration

• High Availability

• High Security

• Industry controlled

• Platform intra-operability

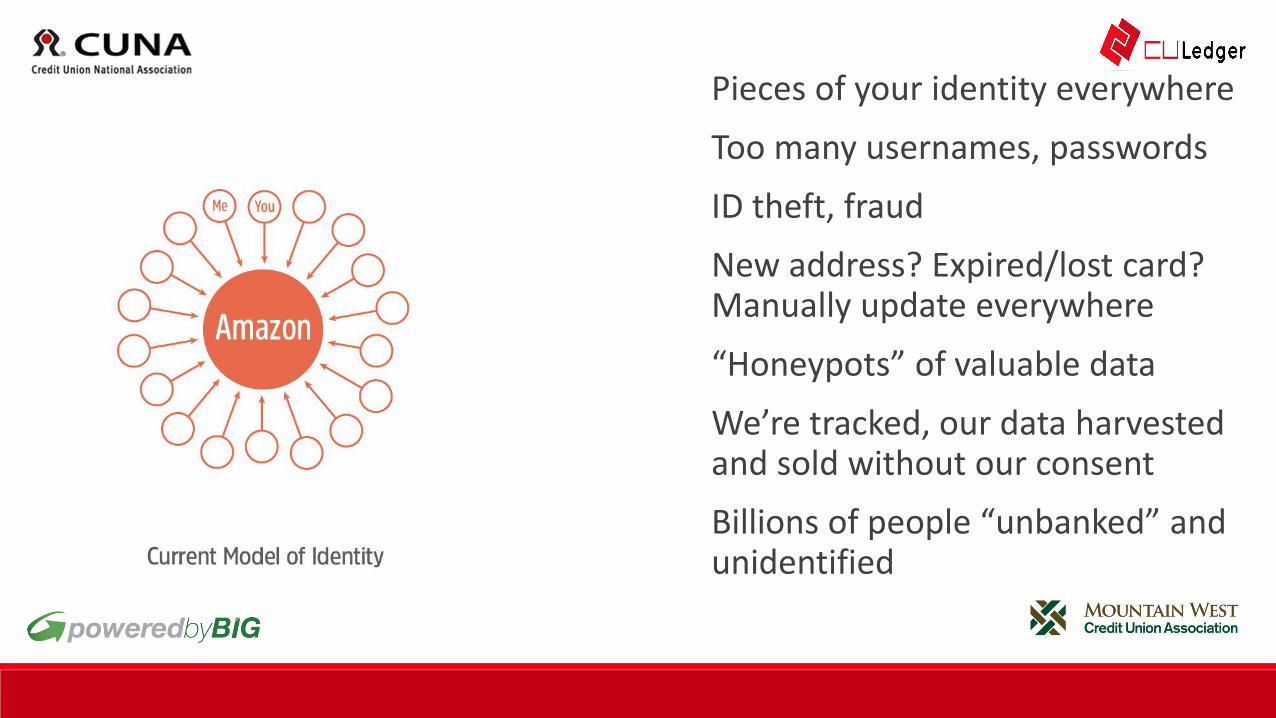

First things First; CU State of Identity• Home banking credential storageo Lack of CU control

o Sometimes in other Vendor’s solutions

o Cannot easily reuse the credentials for other applications

• Cumbersome multi-factor authenticationo Dysfunction between devices

o Continually playing catchup

o Costly integration

• Illegal activityo Phishing

o ACH fraud

o Bill Pay fraud

o Account takeover

Secure Single Sign-On (S-SSO) Digital Identity • Simplify and consolidate user names and passwords

• Simplify logins and improve security with EverAuth MF Authenticator

• “Strong” verified identity and biometrics

• Multiple devices and methods to authenticateo Voice prints

o Facial recognition

o Finger prints

• Reduce costs of integration

Universal Identity

• The “Holy Grail” of product positioning; it touches everything

• Nothing more intimate to users

• Might have 7 messaging apps, but only one identity

Can the CU Industry Win Universal Identity?

• It’s wide open, no one has solved it

• We have the right model, technology

• Credit unions have the power to create mass adoption

• It’s the first solution identified by CULedger

Webroot just did a survey and said: “People are stupid with their passwords”.

Pieces of your identity everywhere

Too many usernames, passwords

ID theft, fraud

New address? Expired/lost card? Manually update everywhere

“Honeypots” of valuable data

We’re tracked, our data harvested and sold without our consent

Billions of people “unbanked” and unidentified

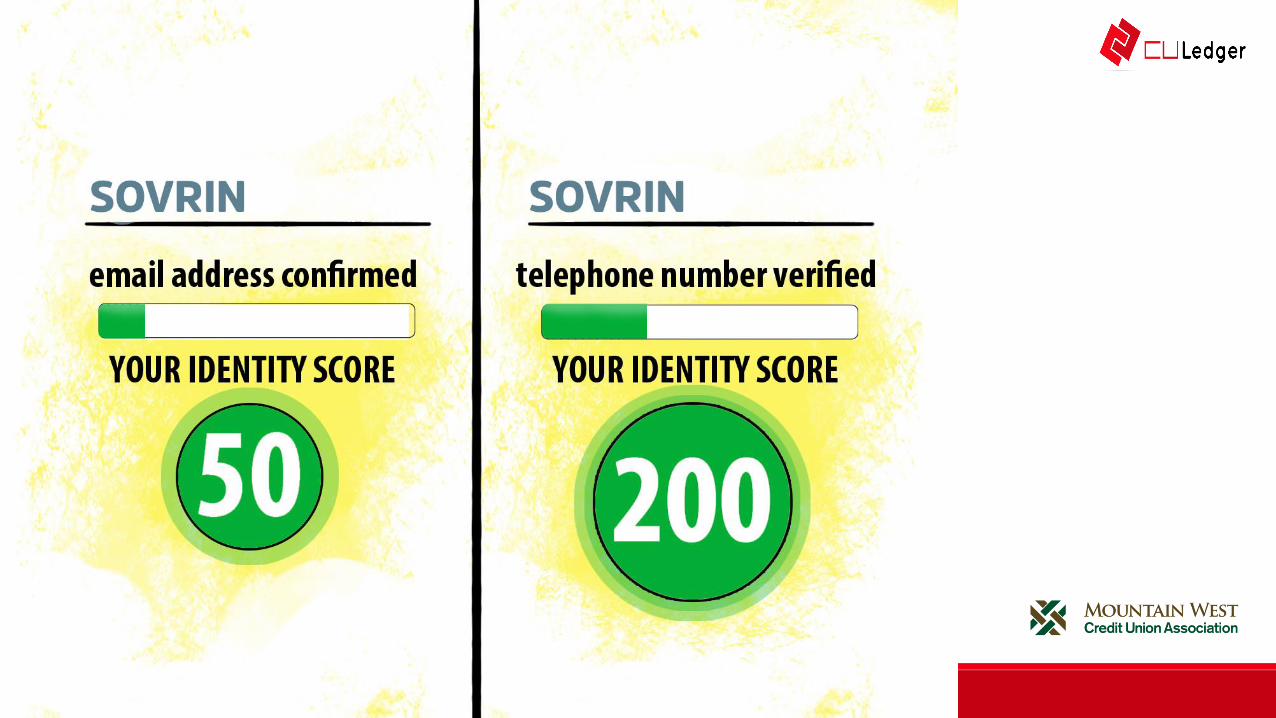

• “Sovrin” identity is now possible

• A presence you own and control

• Other people/entities link to you

• You become the source for:o Proof of identity

o Your correct info, data

o Your preferences for anything

o Your consent

o Your rules

• An “inversion of control”

• Private, super-secure

• Irrevocable

The Right Technology

• Must be distributed ledger

• Must be permissioned

• Must support your identity graph: oJoe Johnson, Joe2000, Alienblaster, etc.

• Must be attribute-based: oStreet, age, pilot’s license, college degree,

frequent flier #, etc.

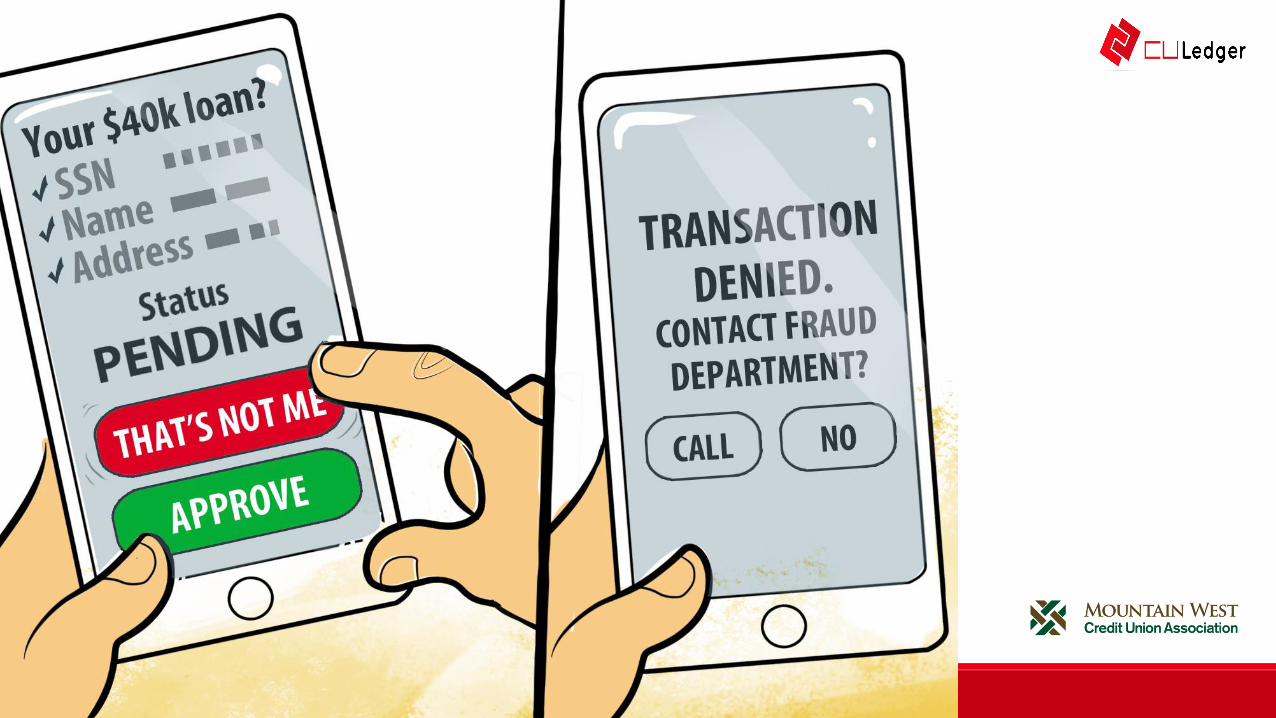

Unprecedented Safety

We now have the technology to:oPrevent card/account fraud

oPrevent SSN-based ID theft

The CU Industry Opportunity

• Financial products “baked in” to identity

• A pay button within user’s identity app, not a separate app

• A platform to launch new products:oRe-introduce bedrock financial products

oNew, previously impossible products

Want to know more? Want to get involved ?

• Join the movement by singing up at www.CULedger.com.

• Contact us for a one on one conversation to discuss investing in CULedger and how you can help change the industry