thomson reuters presentation template - …€¦ · · 2015-11-10or expense certain repair and...

TRANSCRIPT

Schedule C

Presented by: Tony Johnson, CPA

Copyright 2014 Thomson Reuters All Rights Reserved.

2

3

What’s New for 2015 From Instructions to Sch C (Draft)

Standard mileage rate. The business standard mileage rate for 2015 is 57.5 cents per mile.

Deduction and capitalization of expenditures related to tangible property. Final regulations under sections 162(a) and 263(a) provide guidance for taxpayers that acquire, produce, or improve tangible property. The final regulations clarify and expand the standards under sections 162(a) and 263(a). The regulations generally apply to tax years beginning on or after January 1, 2014. For additional information, see T.D. 9636, 2013-43 I.R.B. 331 available at www.irs.gov/irb/2013-43_IRB/ ar05.html.

4

What’s New for 2015 From Instructions to Sch C (Draft)

Eased reporting requirements for certain small businesses changing accounting methods to adopt new repair regulations. For tax years beginning on or after January 1, 2014, small business taxpayers may make certain changes to their accounting methods to adopt final tangible property repair regulations without filing Form 3115, Application for Change in Accounting Method. The final tangible property regulations, T.D. 9636, clarify the standards for determining whether to capitalize or expense certain repair and maintenance costs of tangible property. For additional information, see Rev. Proc. 2015-20, 2015-9 I.R.B. 694 available at www.irs.gov/irb/2015-9_IRB/ar09.html.

5

What’s New for 2015 From Instructions to Sch C (Draft)

Small Business and SelfEmployed (SB/SE) Tax Center. Do you need help with a tax issue or preparing your return, or do you need a free publication or form? SB/SE serves taxpayers who file Form 1040, Schedules C, E, F, or Form 2106, as well as small business taxpayers with assets under $10 million. For additional information, visit the Small Business and Self-Employed Tax Center at www.irs.gov/Businesses/Small- Businesses- &-Self-Employed/Small- Business-and-Self-Employed-Tax- Center-1.

6

The Tax Gap “Map” - 2006 ($billions)

6

7

Chances of Being Audited (FY 2014)

• All Tax Returns .7%

• All individual returns .9%

Schedule C $100-$200K 2.4%

Schedule C $200K+ 2.1%

C Corporations 1.3%

S Corporations .4

Partnerships .4

Source: IRS Data Book 2014

8

Filing Statistics (in 1,000s)

2012 2013 2014

• Schedule C 23,003 23,426 24,008

• C Corporations 2,263 2,248 2,221

• S Corporations 4,680 4,566 4,643

• Partnerships 3,626 3,686 3,799

9

Advantages and Disadvantages

Advantages

• Simplicity – No balance sheet required – Easy to start and easy to stop doing business – No payroll reporting for owner

• Single level tax

Disadvantages

• All income subject to self-employment tax

• No limit of liability

10

Who Must File Schedule C

• All trades or businesses with one owner

• Separate schedule C for each business

• Single Member LLC

• Husband and wife joint venture

415

11

Single –Member LLC Disregarded

415

12

Single –Member LLC Federal ID #

13

Husband and Wife Qualified Joint Venture

• Both materially participate in business

• No other owners

• Make an election by – Filing two separate Schedule Cs – Do not file another 1065 – Last 1065 filed is considered to be final

• Once made election can be revoked only with permission from IRS

415

14

415

15

Four Types of Workers

• Common law employees

• Statutory employees

• Statutory non-employees

• Independent contractors

16

Statutory Employees • Considered employees for FICA and

Medicare withholding

• They receive W2 Forms

• Statutory box will be checked

• Report W2 income on Schedule C

• Deduct related expenses on Schedule C

• Do not prepare Schedule SE

416

17

18

Statutory Employees Who are they:

• Drivers distributing beverages, meat vegetables, fruits, bakery products, laundry or dry cleaning

• Life insurance agents full time - primarily for one company

• Home workers

• Travelling sales agents

19

Hobby Loss Issues

Taxpayers must have an honest objective of making a profit. Factors to consider include:

• Manner of conducting business • Expertise of taxpayer • Time and effort devoted to business • Success in other business • History of income or loss • Financial status of taxpayer • Elements of personal pleasure or recreation

Presumed business if profitable three out of five years

416

20

Hobby Loss Issues

Estate of John F. Chow, TC Memo 2014-19 Gambling activities were a hobby: • Significant losses for three years • No business plan • No budget for gambling activities • No separate bank account • No research/consulting to improve chances Penalties were imposed

21

Hobby Loss Issues

Travis A Mathis, TC Memo 2013-294 Cutting horse farm activity a hobby: • Failed to prove profit motive • Did not operate in professional manner • “Did not take their activity seriously” No penalties were imposed • Demonstrated reasonable cause/good faith • They relied on longtime CPA

22

Hobby Loss Issues

Heinbockel, TC Memo 2013-294 Airplane chartering and vineyard a hobby: • Passionate flyer with one airplane • 3 year income $4k, $30k and $6k • Expenses $45 - $100k each year • Never planted a single grapevine • Farm losses of $49k, $13k and $8k Penalties imposed

417

23

Schedule C – General Information 419

24

ID Number

• Do not enter Social Security number on Line D

• Do not enter ID # issued to a Single Member LLC

• Enter ID # if you have employees or if you have a qualified retirement plan

• Otherwise leave Line D blank

419

25

ID Number 419

26

ID Number - Line D 419

27

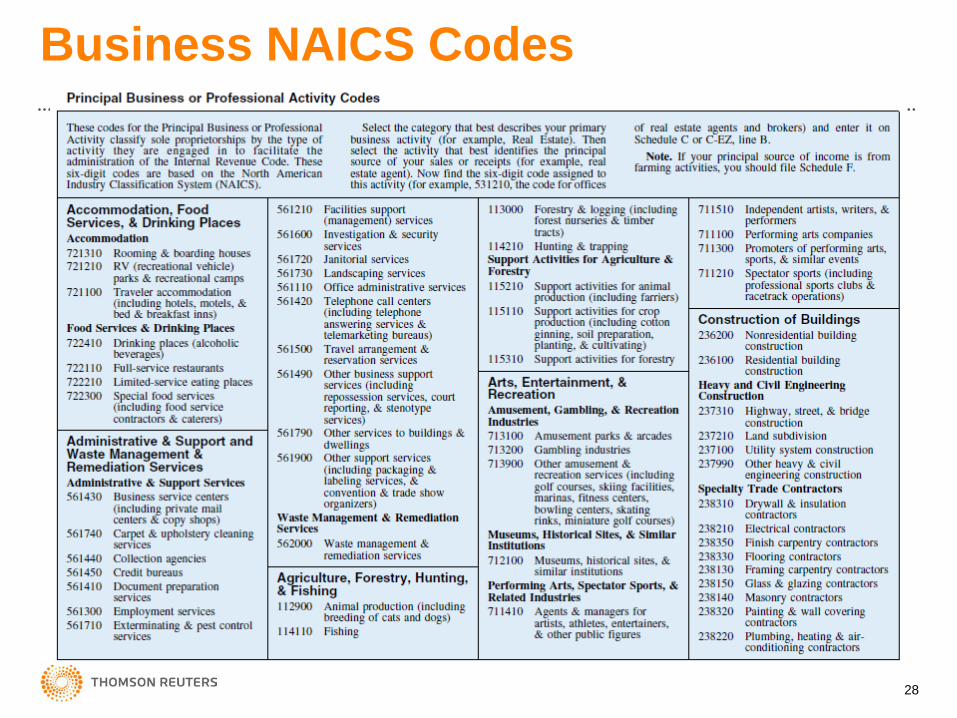

Business Code 419

28

Business NAICS Codes

29

Accounting Method 420

30

All Entities

Gang of 5

C Corporations

All Others

Service Providers QPSC’s Farms

1 Million 5 Million 10 Million No Limit

Who Can Use Cash Method?

31

Gang of Five

• Mining • Manufacturing • Wholesale Trades • Retail Trades • Information Industries These cannot use cash method if

sales exceed $1 million

32

Material Participation 421

33

Material Participation

• More than 500 hours • Substantially all participation • More than100 hours and as much as

anyone else • Materially participated 5 out of last ten

years • Personal service activity and materially

participated any 3 prior years • Based on facts and circumstances

421

34

Information Returns 421

35

Repeal of Enhanced 1099 Reporting Trade or business only prepare 1099’s for:

–Payment for services (Not products) –To Individuals and Partnerships (not

Corporations) –$600 or more annum Note: Payments of $600 or more to law corporations must also be reported on 1099

421

36

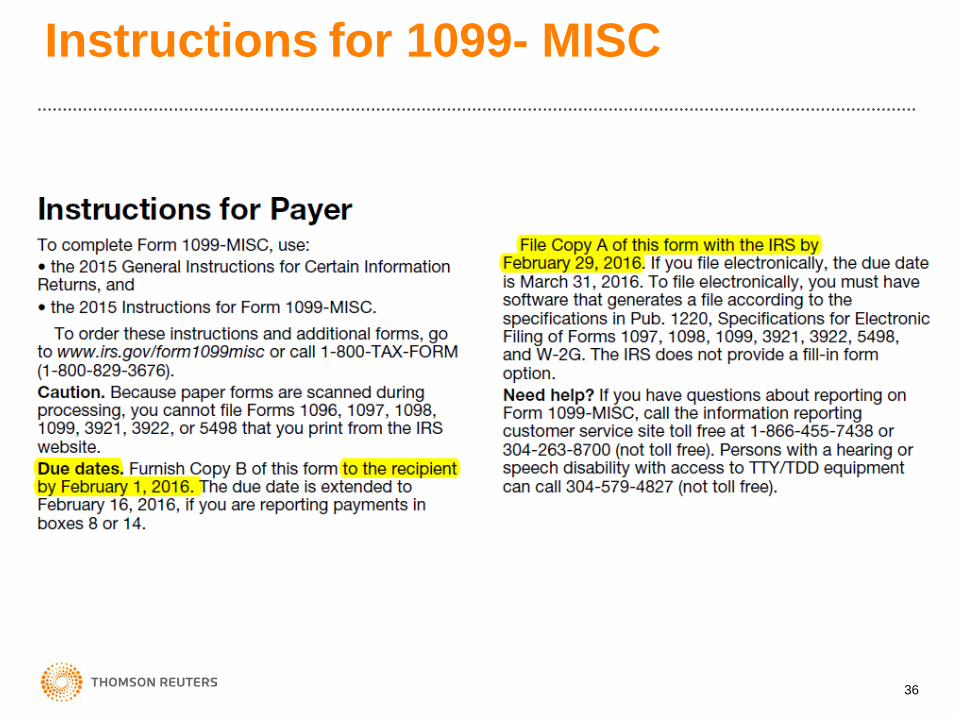

Instructions for 1099- MISC

37

Penalties for Late Filing/Non Filing

T1 Filed within 30 days (by March 30) $30 each

T2 Filed by August 1 $60 each

T3 Filed after August 1 or not filed $100 each

Intentional disregard $250 each

Separate penalties computed in the same manner are applied for failure to provide 1099 to payee

Essentially the penalty could be doubled

38

Maximum Penalty

Normal Small Bus

T1 $250,000 $75,000

T2 $500,000 $200,000

T3 $1,500,000 $500,000

Intentional No limit No limit

39

Gross Receipts

40

Gross Receipts – Sales tax

41

Cost of Goods Sold

42

Gross Profit Percentage

43

Other Income 422

44

Other income

Some of items to be reported on Line 6 • Business interest from finance charges etc. • Scrap sales • Business prizes and awards • Recovery of bad debts • Depreciation recapture • Section 179 recapture • Income from change in accounting method

422

45

Ordinary and Necessary Deductions

Not what it sounds like

Ordinary – One that is common and accepted in this

field of business

Necessary – One that is helpful and appropriate – Does not have to be indispensable

423

46

Donated Inventory

Amount deductible is lower of basis or FMV If purchased/manufactured in current year • Include as cost of goods sold

If purchased in prior year: • Remove cost of donated property from CGS • Reduce beginning inventory (Will not match

prior year ending inventory) • Deduct on Schedule A • Not allowed for SE Tax Special rule applies for donation of food

423

47

48

Recent Developments – Sec 199 Legal Advice 2013302F

• Photo processing and printing qualifies for DPAD • Deduct 9% under section 199 • Pharmacy with self service kiosks and photo labs • Customers can order prints, picture sheets,

enlargements, photo books, greeting cards, etc. • However burning pictures to CD or DVD do not

qualify • Similarly court decided putting together gift

baskets qualifies as DPAD – (Houdini Inc 2013 DC CA)

434

49

Tax Planning – Schedule C Put kids on payroll Put spouse on payroll • Avoid two schedule Cs • Achieve desired allocation for SE purposes • Institute 105 Plan (If no other employees) Allocate accounting fee to Schedule C Move interest income to schedule B Charity vs advertising/promotion Consider renting from spouse Consider single member LLC

Capitalization and Depreciation

Presented by: Tony Johnson, CPA

Copyright 2015 Thomson Reuters All Rights Reserved.

51

Cost Recovery (Depreciation) What’s New:

– In 2014 IRS issued new Regs – A nightmare – In 2015 Rev Proc 2015-20 provides significant relief – Sec. 179 $500,000 expired ($25,000 for 2015) – Sec. 179 phaseout $2,000,000 ($200,000 for 2015) – Bonus depreciation has expired – 15-year MACRS building improvements/restaurants has

expired – Additional $8,000 for autos has expired Will these come back retroactive to 1/1/15?

441

52

Rev Proc 2015-20 Benefits – Not necessary to file Form 3115 – Expensing policy ($500) does not have to be in

writing Downside – No audit protection – 6 year statute for overstatement of basis

443

53

New Final Regulations Capitalization vs Expense

• IRC Section 162(a) and Section 263(a) • 200 Pages • Substantially confirms previous regulations • New de minimis amounts • New expense policy safe harbor • New safe harbors for rental property • There are many examples in the regulations

to help us understand these new provisions • On 9/13/13 Regs became final • Effective date 1/1/14; may be used sooner

443

54

Capitalization vs Repairs

Other items addressed : • New definition of “materials and supplies” • A special 12- month rule • A $200 de minimus rule for materials and

supplies • Expensing policy limits $500 or $5,000 • Originally the regs required many taxpayers

make a change in method and file form 3115 • 3115 no longer required

435

55

Materials and Supplies

New definition of materials and supplies:

Not considered inventory and any one of following:

• Acquired to maintain, repair or improve property

• Fuel, lubricants etc consumed in less than 1 yr

• Unit of property with life of less than 1 year

• Acquisition or production cost of $200 or less

• Identified by IRS as materials and supplies

445

56

Materials and Supplies Economic Useful Life • For purposes of applying the 12-month rule, the

the economic useful life of a unit of property is not necessarily its inherent useful life, but is the period over which the property may reasonably be expected to be useful to the taxpayer

• The factors in Reg.1.167(a)-1(b) (e.g., wear and tear, climatic and other conditions particular to the taxpayer's business) are to be considered in determining this period

445

57

Materials and Supplies – When to Deduct

Incidental materials and supplies • Deduct when paid for

• These are: – Materials carried on hand – No record of consumption is kept – No beginning or ending inventory taken

Non-incidental

• Deduct in tax year in which used or consumed

Taxpayers may apply de minimis rule $500/$5,000

445

58

New Expensing Policy Must make an election with timely filed return Election cannot be revoked without permission Expense limits per item: • Applicable Financial Statement”(AFS) $5,000 • No AFS $500 Definition of AFS

• One that is required to be filed with the SEC or • Is a certified audited financial statement • For AFS policy must be in writing No 3115 required

446

59

Unit of Property - Generally UOP is based on functional interdependence

Placing a component in service is dependent on placing in service another component

All components functionally interdependent are one UOP

Example: Jet plane and jet engine are one UOP

Example: Laptop computer and Printer are not one UOP

448

60

Unit of Property - Buildings Old Rule:

• Looked to determine whether the expenditure improved the entire building

• For example, whether costs to replace some components of the roof were required to be capitalized was determined by assessing whether that activity resulted in an improvement to the building as a whole

449

61

Unit of Property - Buildings New Rule: In general, each building and its structural components are one UOP — “the building.”

Amounts are treated as paid for an improvement to a building if they improve: • The building structure or • Any designated building system

Under the new rule you look to see if the work done improves the roof (not the building as a whole)

449

62

Unit of Property - Building

UOP consists of building and components

Components are: • Walls • Partitions • Floors • Ceilings • Windows and doors • Roof • Other

449

63

Building Systems Following are building systems separate from the structure: • Heating, ventilation and air conditioning • Plumbing systems • Electrical systems • Escalators • Elevators • Fire protection and alarm • Security systems • Gas distribution system • Other identified in published guidance

449

64

Unit of Property - Buildings Example: • Peggy owns a unit in a condominium office building.

The condominium unit contains two restrooms, each of which contains a sink, a toilet, water and drainage pipes and bathroom fixtures

• She pays for labor and materials to perform work on the pipes, sinks, toilets, and plumbing fixtures

• Peggy must treat the individual unit that she owns, including the structural components as a single UOP

• If the work results in an improvement to the plumbing system then she must capitalize the costs to the entire building

65

Unit of Property - Buildings Example:

• Peggy spent $10,000 replacing the plumbing system

• She must capitalize this amount as part of the building

• She can deduct the undepreciated balance of the original plumbing system

• IRS provides guidance to determine this amount. Example:

Original cost of condo $200,000 Amount allocated to plumbing system $20,000 Less depreciation to date 12,400 Current deduction 7,600

66

Unit of Property - Buildings Observations :

• The downside is that many improvements will have to be capitalized

• The upside is that a loss deduction will be allowed on the disposition of the structural component before the building is sold

• A taxpayer won't have to capitalize and depreciate simultaneously amounts paid for both the removed and the replacement properties

• Keeping track of basis will be a pain

452

67

Routine Maint Safe Harbor- Building

Expense costs to keep buildings and components in efficient operating condition

Examples: • Inspection • Cleaning • Testing • Replacing damaged or worn parts

Must be incurred more than once in 10 years

(Other property more than once in class life)

458

68

New Safe Harbor- Small Taxpayers Average gross receipts $10 million or less for last three years Building with unadjusted basis of $1 million or less Expense improvements if total amount paid for: Repairs Maintenance and Improvements Does not exceed the lesser of: 2% of unadjusted basis $10,000 If total amounts paid exceed 2% or $10,000 expense repairs but do not expense improvements

458

69

New Safe Harbor- Buildings Example:

Original cost basis of building is $600,000 Routine repairs and maintenance $1,500 Improvements $8,000 Total paid $9,500

Amount expensed $9,500

Does not exceed $10,000

Does not exceed 2% of $600,000

70

New Safe Harbor- Buildings Example:

Original cost basis of building is $600,000 Repairs and maintenance $1,500 Improvements $11,000 Total paid $12,500

Amount expensed $1,500

Does exceed $10,000

Does exceed 2% of $600,000

71

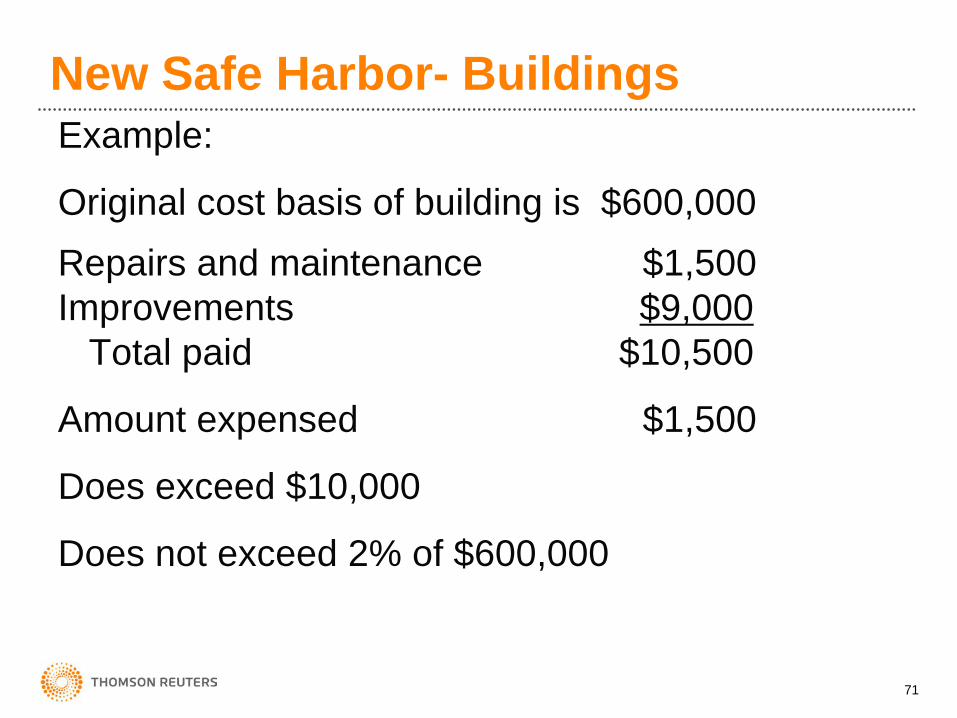

New Safe Harbor- Buildings Example:

Original cost basis of building is $600,000 Repairs and maintenance $1,500 Improvements $9,000 Total paid $10,500

Amount expensed $1,500

Does exceed $10,000

Does not exceed 2% of $600,000

72

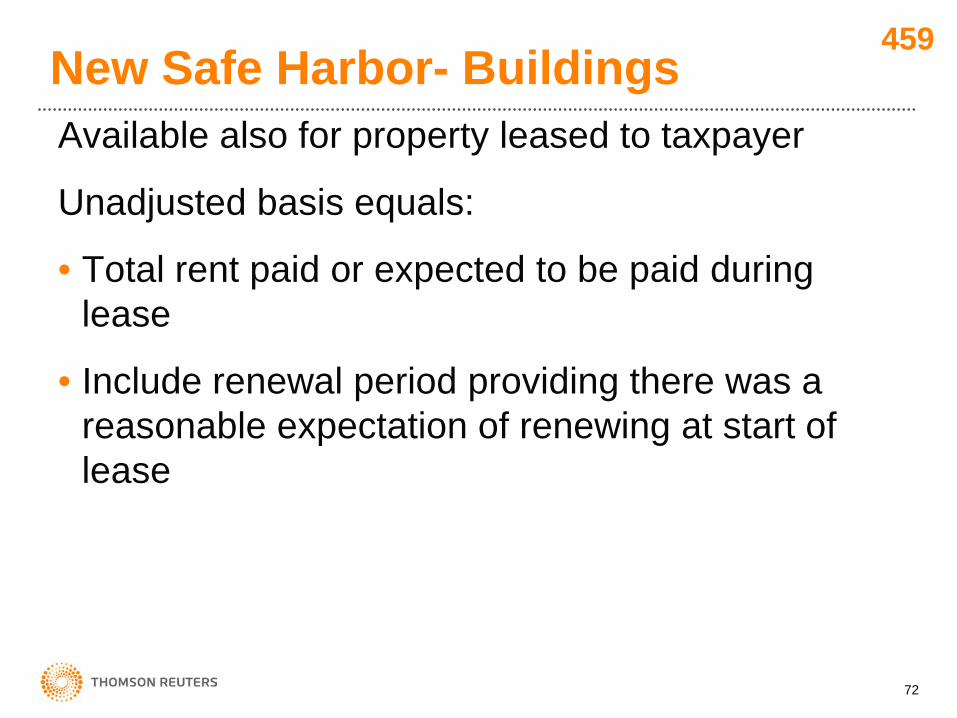

New Safe Harbor- Buildings Available also for property leased to taxpayer

Unadjusted basis equals:

• Total rent paid or expected to be paid during lease

• Include renewal period providing there was a reasonable expectation of renewing at start of lease

459

73

New Safe Harbor- Buildings Safe harbor is per building Annual election made on building by building basis Statement to be attached to return Effective date: Generally for years beginning on/after 1/1/14 May elect to apply to 2012 or 2013 File 1040X before 180 days after return due date including extensions Calendar year - 2012 file by 4/15/14 Calendar year - 2013 file by 4/15/15

74

IRC Sec. 179 Expense New Development

Information Letter 2013-0016

S corporation members are not subject to controlled group limitations

S corps can deduct up to the maximum

Caution in some circumstances S corps should limit section179 deductions if the deduction will be limited at the individual level

75

IRC Sec. 179 Expense Generalities:

• Generally limited to tangible personal property

• Limited by taxable income

• Excess above taxable income carried over

• Available for new or used property

• Recapture if business uses less than 50%

460

76

IRC Sec. 179 Expense 2002 $24,000

2003 $100,000 2004 $102,000 2005 $105,000 2006 $108,000 2007 $125,000 2008 $250,000 2009 $250,000 2010 - 2014 $500,000 2015 $25,000

460

77

IRC Sec. 179 Small Business Limits 2002 $200,000 2003 $400,000 2004 $410,000 2005 $420,000 2006 $430,000 2007 $500,000 2008 $800,000 2009 $800,000

2010 - 2014 $2,000,000 2015 $200,000

461

78

Deadline for IRC Sec. 179 Election May amend to revoke IRC Sec. 179 • Assets placed in service in 2002

– Originally filed return – Amend by due date of return

• Assets placed in service 2003–2014 – Originally filed return – Amend any open year

• Assets placed in service 2015 – Originally filed return – Amend by due date of return

459

79

Planning Pointers • IRC Sec. 179 cannot create a loss • Bonus depreciation does create a loss * • IRC Sec. 179 is available for used property • Bonus depreciation is available for original use

property * • IRC Sec. 179 can be used selectively • Bonus depreciation is automatic * • Taxpayers can elect out but election applies to

entire class of assets * • Election must be made by due date of return

including extensions(even if extension not filed)* *Bonus provisions expired after 2014

80

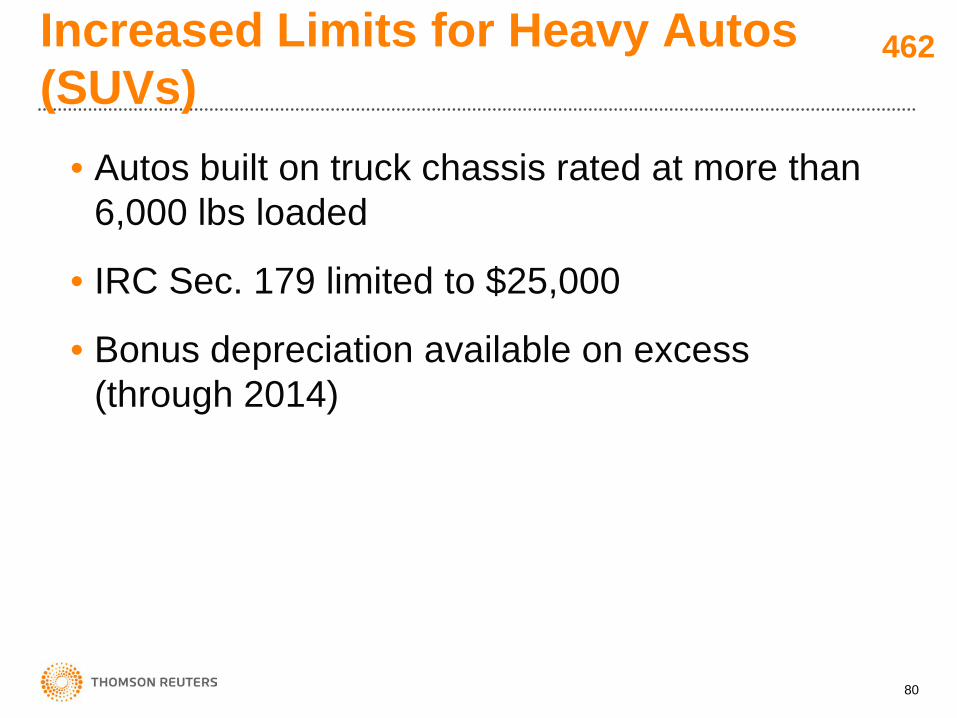

Increased Limits for Heavy Autos (SUVs)

• Autos built on truck chassis rated at more than 6,000 lbs loaded

• IRC Sec. 179 limited to $25,000

• Bonus depreciation available on excess (through 2014)

462

81

Increased Limits for Heavy Autos (SUVs) Example

• New SUV purchased for $60,000

• First take sec 179 25,000 35,000

• Then take bonus 50% (20 14) 17,500 17,500

• Then take MACRS 3,750

• Remaining basis 13,750

• Total taken this year 46,250

Assumes 100% business use

462

82

Luxury Auto - 2015 Depreciation

Chassis Autos Truck

Year 1 $3,160 $3,460

Year 2 $5,100 $5,600

Year 3 $3,050 $3,350

Year 4 and after $1,875 $1,975

463

83

Bonus Depreciation Limits for 2014

Chassis Autos Truck

Year 1* $11,160 $11,360

Year 2 $5,100 $5,400

Year 3 $3,050 $3,250

Year 4 and after $1,875 $1,975

* Add $8,000 for years 2010-2014

84

IRC Sec. 179 Available for Qualified Real Property • Qualified property

– Leasehold improvements – Restaurant property – Retail improvement property

• Assets placed in service 2010–2013 • No carryover beyond 2013 • Maximum amount $250,000

– Figured separately from other IRC Sec. 179 property

– Overall maximum still $500,000 – Necessary to allocate between two

Employee vs

Independent Contractor

Presented by: Tony Johnson, CPA

Copyright 2015 Thomson Reuters All Rights Reserved.

86

What’s New

• July 2015 - Independent Contractor cleaning homes scheduled through internet service provider sued for minimum wages

• June 2015 - CA says Uber driver is employee • June 2015 - FedEx sets up fund to pay $228

million to workers deemed employees by court • May 2015 – FL says Uber driver is employee Trend indicates leaning towards employee away from independent contractor

467

Employee Business Expenses

Presented by: Tony Johnson, CPA

Copyright 2015 Thomson Reuters All Rights Reserved.

88

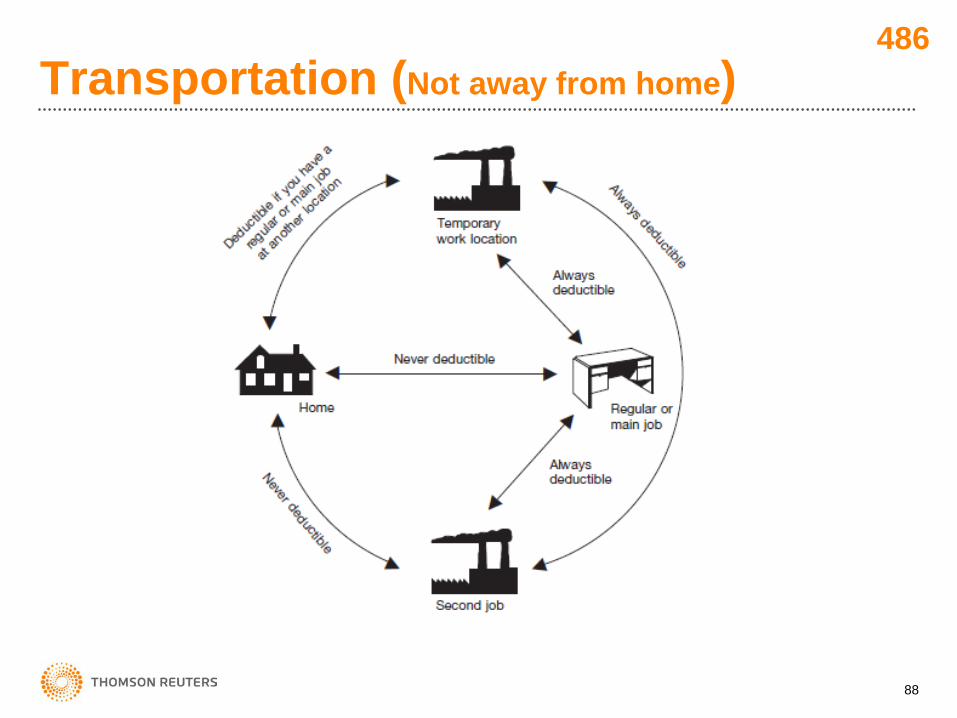

Transportation (Not away from home)

486

89

Transportation Commuting expenses are not deductible

• Including driving your car, bus, subway, taxi • No matter how far the commute • Even if you work during the commute

Parking fees • Not deductible at regular place of work • Deductible when visiting clients or customers

Advertising display on car • Does not convert to business use

486

90

Transportation Car pool costs (except for profit)

• Not deductible • Reimbursements from passengers not income

Hauling tools or instruments • Deduct only additional costs e.g. trailer

Union members from union hall to work • Not deductible

Office in home • Deduct trips to other regular work places only if office

at home is principal place of business

486

91

Auto

Standard mileage rates

2013 2014 2015 Business 56.5 56.0 57.5

Medical/Moving 24.0 23.5 23.0*

Charitable 14.0 14.0 14.0*

*Deduct actual gas and oil if greater

486

92

Auto Standard Mileage Rate (SMR)

Depreciation component included in SMR

2015 .24 2014 .22 2012-2013 .23 2011 .22 2010 .23 2008-2009 .21 2007 .19 2005-2006 .17 2003-2004 .16 2001-2002 .15

Used to compute gain or loss on disposition

487

93

Auto Leasing a car – Use either:

• Standard mileage rate

– Do not deduct lease payments

• Actual expenses

– Deduct business portion of lease payments

– Reduce deduction by amount per tables

488

94

Auto Leasing a car – Lease income inclusion:

Example:

On January 17, 2014 you lease a car with FMV of $32,250 for three years:

Year Amount Proration Bus % Inclusion 2013 $9 350/365 75% $6 2014 $20 365/365 75% $15 2015 $29 365/365 75% $22 2106 $35 16/365 75% $12

488

95

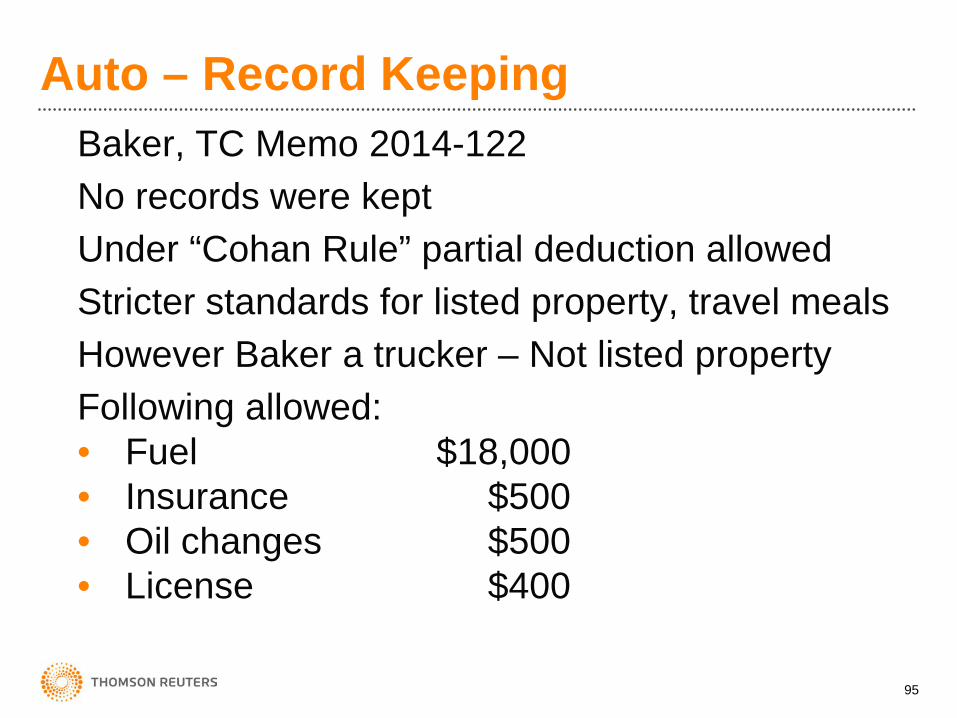

Auto – Record Keeping Baker, TC Memo 2014-122 No records were kept Under “Cohan Rule” partial deduction allowed Stricter standards for listed property, travel meals However Baker a trucker – Not listed property Following allowed: • Fuel $18,000 • Insurance $500 • Oil changes $500 • License $400

96

Travel Must be away from home:

Tax Home • Greater metropolitan area of regular work place • Not same as your family home

Substantially longer than ordinary day’s work • You need some sleep or rest • Short nap in a car does not count • Does not have to be from dusk till dawn

489

97

Liberalized - Away from Home Lodging New safe harbor (Proposed Reg 1.162-31(b) • Lodging necessary to attend meeting, conf.

etc. • Does not exceed 5 days more than one per

quarter • Employer requires remaining at function

overnight • Not lavish, extravagant, does nor provide

significant element of personal pleasure, recreation or benefit

489

98

Travel Temporary assignment or job

Tax home does not change providing: • Stay is expected to last for 1 year or less • Does in fact last 1 year or less

Tax home changes if: • Assignment is indefinite • Assignment is expected to last more than1 year

Going home on days off • Deduct travel expenses but not more than cost

had you stayed in temporary location

491

99

Travel Two per diem methods:

Regular federal per diem rate • Published at - www.gsa.gov/perdiem • Updated annually on Oct 1

High-low method 9/30/14 9/30/15 M&I

High $259 $275 $68 Low $172 $185 $57 M&I no longer includes transportation from hotel to

restaurants or cost of mailing back to office

492

Home Office

Presented by: Tony Johnson, CPA

Copyright 2015 Thomson Reuters All Rights Reserved.

101

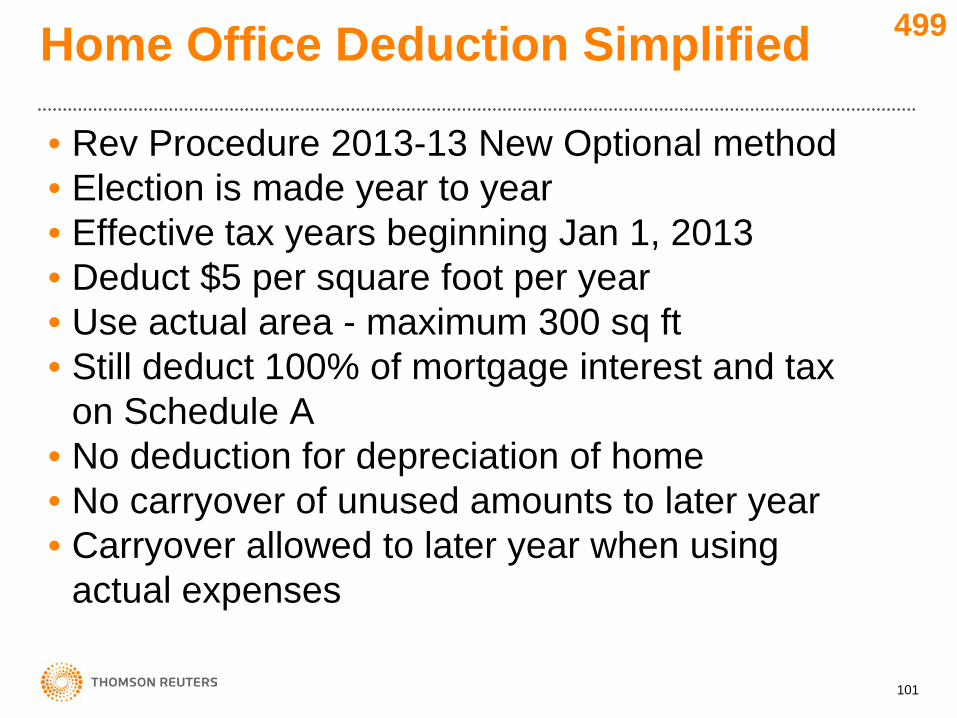

Home Office Deduction Simplified

• Rev Procedure 2013-13 New Optional method • Election is made year to year • Effective tax years beginning Jan 1, 2013 • Deduct $5 per square foot per year • Use actual area - maximum 300 sq ft • Still deduct 100% of mortgage interest and tax

on Schedule A • No deduction for depreciation of home • No carryover of unused amounts to later year • Carryover allowed to later year when using

actual expenses

499

102

103

104

Home Office Deduction Simplified Planning pointers

When not to use simplified method even though it may produce a larger amount:

• When deduction exceeds net income • When there is a deduction carried over from

previous year

Health Care Credit for

Small Business

Presented by: Tony Johnson, CPA

Copyright 2014 Thomson Reuters All Rights Reserved.

106

Small Employer Tax Credit

Per IRS only a small number of eligible employers have been claiming this credit Reason cited by employers: Credit too small and/or too complicated

106

539

107

Small Employer Tax Credit

Small business tax credit good for 6 years (Form 8941) Available for those offering health coverage After 2013 employer must buy insurance through an exchange After 2013 good for only two consecutive years For a qualified small business

― No more than 25 FTE with ― Average annual wage of no more than $51,600 ($50,800 for 2014)

Maximum credit—The lesser of: ― Actual insurance paid by the employer, or ― What ER would have paid had EE enrolled in coverage with a small

business benchmark premium (See instructions Form 8941) Multiplied by the percentages below ― 2010-2013: 35% ― 2014-2015: 50%

107

539

108

Form 8941 Instructions for 2013 Average Premiums—Selected States Single Family #1 Alaska $7,961 $16,808 #2 Massachusetts $6,323 $16,502 #3 Washington DC $6,133 $16,079 #13 Minnesota $5,588 $14,077 #17 W. Virginia $5,947 $13,734 #19 Texas $5,327 $13,313 #23 Virginia $5,449 $13,241 #29 California $5,345 $12,809 #32 Ohio $5,174 $12,710 #36 S Carolina $5,351 $12,473 #42 Nevada $5,417 $12,125 #50 Idaho $4,901 $10,738 #51 Arkansas $4,546 $10,575

109

Small Employer Tax Credit

Deduction for health insurance is reduced by the credit

Allowed for the AMT

Eligible employees include: Part-time and leased

Ineligible employees include: seasonal, sole proprietors, partners, 2% S shareholders, 5% company owners and those related to such persons

Definition of FTE: Total number of hours of service by eligible employees/2080

Note: Round down to the nearest whole number

110

Small Employer Tax Credit

Credit is available to tax-exempt employers

Calculations are the same except that

Credit is limited to sum of:

• Withholdings for federal income tax plus

• Employee and employer share of Medicare tax

The credit is refundable and reported on Form 990-T