thor investor presentation december 2014

TRANSCRIPT

www.thorindustries.com

2

This presentation includes certain statements that are “forward looking” statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These forward looking statements are made based on management’s current expectations and beliefs regarding future and anticipated developments and their effects upon Thor Industries, Inc., and inherently involve uncertainties and risks. These forward looking statements are not a guarantee of future performance. There can be no assurance that actual results will not differ from our expectations. Factors which could cause materially different results include, among others, price fluctuations, material or chassis supply restrictions, legislative and regulatory developments, the costs of compliance with increased governmental regulation, legal issues, the potential impact of increased tax burdens on our dealers and retail consumers, lower consumer confidence and the level of discretionary consumer spending, interest rate fluctuations, restrictive lending practices, management changes, the success of new product introductions, the pace of obtaining and producing at new production facilities, the pace of acquisitions, the integration of new acquisitions, the impact of the divestiture of the Company’s bus business, the availability of delivery personnel, asset impairment charges, cost structure changes, competition, the potential impact of the strengthening of the U.S. dollar on international demand, general economic, market and political conditions and the other risks and uncertainties discussed more fully in ITEM 1A of our Annual Report on Form 10-K for the year ended July 31, 2014 and Part II, Item 1A of our quarterly report on Form 10-Q for the period ended January 31, 2015. We disclaim any obligation or undertaking to disseminate any updates or revisions to any forward looking statements contained in this presentation or to reflect any change in our expectations after the date of this presentation or any change in events, conditions or circumstances on which any statement is based, except as required by law.

Forward Looking Statements

3

Founded in 1980 by Wade Thompson & Peter Orthwein with the acquisition of Airstream, Inc.

The sole owner of operating subsidiaries that, combined, represent one of the world’s largest manufacturers of recreational vehicles

• #1 in overall RV 36.3% of market*

• #1 in Travel Trailers 36.1% of market*

• #1 in Fifth Wheels 49.7% of market*

• #2 in Motorhomes 23.7% of market**

Approximately 9,400 employees***

Operations through 120 facilities in 3 US states***

6.9 million square feet under roof***

Who is THOR

Source: *Statistical Surveys, Inc., YTD U.S. and Canada units through December 2014

**Motorhomes includes Class A, B and C, Statistical Surveys, Inc., YTD U.S. and Canada units through December 2014

*** as of July 31, 2014 (continuing operations)

4

Travel Trailers

Fifth Wheels

Specialty Trailers

THOR’s Product Range

Towable RV's

$2,722 77%

Motorized RV's $804

23%

FY2014 Sales*

*Fiscal year ended July 31, 2014,

sales, continuing operations ($ in

millions)

Class A

Class B & C

Towable RV Segment Products

Motorized RV Segment Products

5

THOR RV Group

6

At Thor we strive to provide RV consumers with superior products and services through innovative solutions which enhance the enjoyment of the RV lifestyle

Our decentralized operating structure and independent operating subsidiaries foster an entrepreneurial spirit and an unending focus on the needs of the users of our products – resulting in our drive to lead the industry with innovation, product quality and customer service

Our focus requires that we make decisions based on the long-term success of our Company:

• While we strive to lead the industry in market share, we will not strive for market share at the expense of quality or without regard to bottom-line impact

• Growth is important, but this is a business of relationships, and we realize that the key to long-term sustainable sales growth rests in the strength of our relationships with consumers, dealers and suppliers

• Our relationship with shareholders is important ― profits are a key driver to our long-term success and returns to our shareholders

• The path to long run success is seldom straight, so our leaders manage in a way that moves us closer to our goals, even though it might impact our results in the short term

THOR’s Strategic Vision

7

Disciplined, Profitable Growth

• Profitable every year since 1980 – 34 years without an annual loss, even during the recession of 2007-09

• All time record $3.5 billion sales from continuing operations in FY2014, up 9% from $3.2 billion sales in FY2013, which was up 23% from FY2012

• FY2014 net income from continuing operations of $175.5 million, up 16% from FY2013

• FY2014 diluted EPS from continuing operations of $3.29, up 15% from $2.86 in FY2013, FY2014 total diluted EPS of $3.35, up 16% from $2.88 in FY2013

Sustainable Business Model

• Successfully weathered a severe downturn and remained profitable

• Recent capital investments position Thor for growth and margin improvement over the long term

Solid Balance Sheet

• On January 31, 2015, cash and cash equivalents of $248.3 million

• Operations historically generate significant cash

• Strong history of returning cash to shareholders through dividends and share repurchases

− Regular quarterly dividend increased from $0.23 to $0.27 at the beginning of FY15

Why Invest in THOR

8

Proven business model:

• Entrepreneurial and decentralized

• No ivory tower: approximately 9,400 employees, only 42 in corporate staff*

• Decision-making driven by the needs of the customer

• Big, but nimble – highly responsive to changes in demand

• Best management team in the business, as proven by sustained performance

An innovator in each of its business segments

Long-term RV market leadership:

• Best positioned in towable RVs, historically highest volume area

• #2 in Motorhomes, poised for continued growth as the market continues to recover

• Well positioned as a leading innovator in the RV market to meet the demands of dealers and consumers

Strong balance sheet to support growth and shareholder returns

What Makes THOR Different

* as of July 31, 2014 (continuing operations)

9

No golden parachutes

No ‘pro forma’ earnings. We report net income, not adjusted earnings to cover up performance

Consistent focus on shareholder value

Simple compensation philosophy:

• Mainly cash compensation, without a cap, based on pre-tax income – a true pay for performance philosophy

• Restricted stock units also awarded based on performance to provide broader, long-term focus on overall Company results

Corporate Integrity

10

Focus on assembly - not heavy manufacturing• Limited vertical integration – only where it makes sense• Flexibility – performance in any market condition• Low overhead costs• High return on assets employed

Strong market share in the primary RV categories – Travel Trailers, Fifth Wheels and Motorized

• Provides scale and purchasing power• Low cost, high volume producer – generates improved margin

Balance sheet supports acquisitions and organic growth

Meaningful increases in production capacity during FY14 and FY15

Diversified lineup of innovative product offerings

Strong relationships in wholesale financing providers

Strength to pay warranty and honor repurchase agreements, which is important to dealers, lenders and consumers

THOR’s Competitive Advantages

11

Market is competitive and very entrepreneurial

Top three RV competitors account for 83.3% of industry retail sales*

Thor’s strength is a resource – since the recession, consumers, dealers and lenders seek to do business with the strongest players in the market

Industry better balanced today for supply and demand

Pricing and promotional environment remains competitive, but improved over prior year

Consumer confidence remains relatively strong, after several months of gains, final results fell to 95.4 in February 2015 from 98.1 in January, but rose from 81.6 a year ago. Consumer sentiment was affected by lower gas prices offset by the impact of harsh winter weather across much of the Midwest and East**

Wholesale and Retail lenders are prudent - applying “healthy discipline”

RV buyers seek the “power of choice” – want variety in brands and models

RV Industry Conditions

*Source: Statistical Surveys, Inc., U.S. and Canada YTD December 2014

** Source: University of Michigan final Consumer Sentiment Index for February 2015

12

A recent review of trends by Kampgrounds of America (KOA) revealed some interesting trends among RV consumers.

There are approximately 39.5 million active campers in North America, but only 9.1 million, or 23% of them, are RV campers. The remaining campers primarily use tents or cabins, which makes them a solid target market for the RV industry.

Baby Boomers (a prime RV target market for many years) represent 26% of the population. While we are focused on meeting the need of Boomers, we are also looking to the future and developing products to meet the needs of Generation X and Millennials as they seek more active outdoor experiences with their families.

Specific trends surrounding today’s RV consumer:

• 70% of today’s RVers plan to buy another RV. The typical trade-in cycle for RVs is every 3-5 years – this does not vary by product type!

• Adult outdoor enthusiasts are increasingly demanding “soft rugged” which is exactly what RVs provide – access to the outdoors with the comforts of home.

• RVs address several key needs of consumers, including spending more time with family and enjoying the great outdoors in an affordable and environmentally conscious way.

• RV consumers continue to develop new ways of utilizing their RVs. Whether used for extreme sports, youth sports leagues and tournaments, attending dog shows or craft shows, RVs are versatile.

The RV Consumer

13

RV Market Wholesale Trends: Units (000’s)2

95

.8 33

9.6

44

1.1

41

3.9

38

9.9

19

9.2

10

6.9 13

3.6

14

0.6

19

6.6

21

5.7

18

6.9

18

9.9

211

.7

21

5.8

18

7.9

17

3.1

16

3.1 2

03

.4

22

7.8 25

9.5

24

7.2

24

7.5

25

4.5 2

92

.7 32

1.2

30

0.1

25

6.8

311

.0

32

0.8

37

0.1

38

4.4

39

0.5

35

3.5

23

7.0

16

5.6

24

2.3

25

2.3 28

5.8 3

21

.2 35

6.7

36

1.4

197

4

197

5

197

6

197

7

197

8

197

9

198

0

198

1

198

2

198

3

198

4

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5 (

e)

Historical Data: Recreation Vehicle Industry Association, Calendar year 2015: RVIA

estimate as of Winter 2014

14

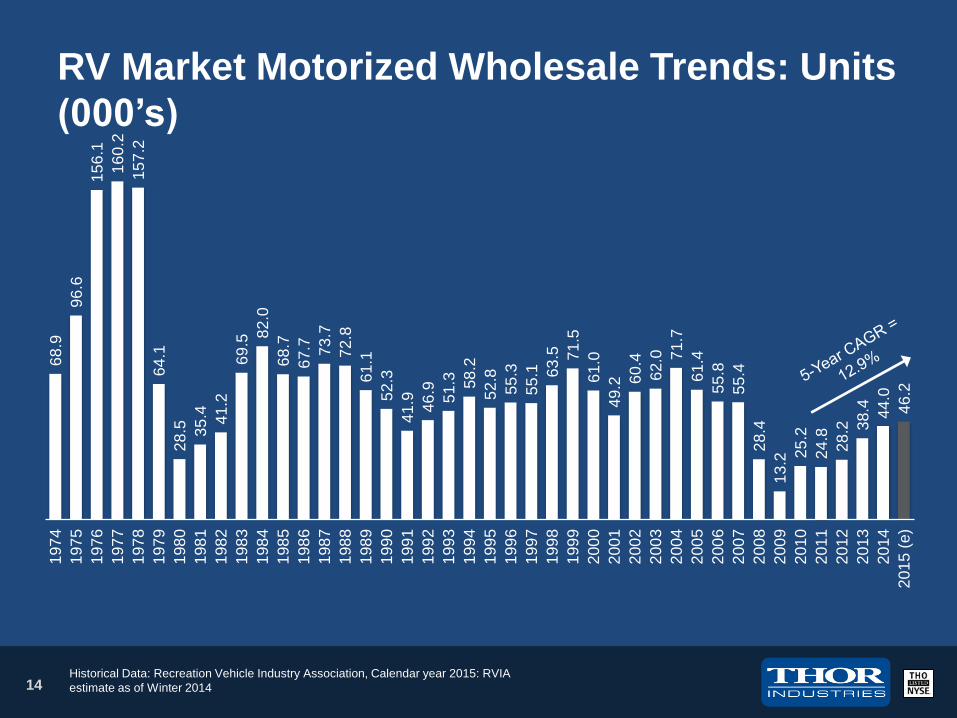

RV Market Motorized Wholesale Trends: Units

(000’s)

68

.9

96

.6

15

6.1

16

0.2

15

7.2

64

.1

28

.5 35

.4 41

.2

69

.5

82

.0

68

.7

67

.7 73

.7

72

.8

61

.1

52

.3

41

.9 46

.9

51

.3 58

.2

52

.8

55

.3

55

.1 63

.5 71

.5

61

.0

49

.2 60

.4

62

.0 71

.7

61

.4

55

.8

55

.4

28

.4

13

.2 25

.2

24

.8

28

.2 38

.4 44

.0

46

.2

197

4

197

5

197

6

197

7

197

8

197

9

198

0

198

1

198

2

198

3

198

4

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5 (

e)

Historical Data: Recreation Vehicle Industry Association, Calendar year 2015: RVIA

estimate as of Winter 2014

15

RV Market Towable Wholesale Trends: Units

(000’s)

22

6.9

24

3.0

28

5.0

25

3.7

23

2.7

13

5.1

78

.4 98

.1

99

.4

12

7.1

13

3.7

11

8.1

12

2.1

13

7.9

14

2.9

12

6.7

12

0.8

12

1.1 1

56

.5

17

6.5 20

1.3

19

4.3

19

2.2

19

9.5 2

29

.1 24

9.6

23

9.1

20

7.6

25

0.6

25

8.9

29

8.3 32

3.0

33

4.5

29

8.1

20

8.6

15

2.4

21

7.1

22

7.5 2

57

.6 28

2.8 3

12

.8

31

5.2

197

4

197

5

197

6

197

7

197

8

197

9

198

0

198

1

198

2

198

3

198

4

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5 (

e)

Historical Data: Recreation Vehicle Industry Association, Calendar year 2015: RVIA

estimate as of Winter 2014

16

Dealers

• Continued optimism

• Right-sized towable inventory

• Appropriate motorized inventory

• Access to wholesale credit

• Financial health

RV: State of Balance

RV 2015 2014 % change

Towables $626.1 $501.9 +24.7%

Motorized $316.0 $343.3 -7.9%

TOTAL $942.1 $845.2 +11.5%

Backlog: January 31 ($ millions)

Consumers

• Better access to retail credit

• Historically low interest rates

• Great demographic trends

• Renewed focus on family vacations

• Looking for value when considering vacation options

Increase in towable backlog due in part to acquisitions included in current year backlog but not included in prior year.

Decrease in motorized backlog due in part to increased capacity enabling the Company to better meet demand, as well

as initial channel orders for new Axis/Vegas product lines introduced in September 2013 included in prior year backlog.

17

THOR RV Dealer Inventory

Total Dealer inventory remains appropriate for current conditions, in

both the towable and motorized segments.

Dealer inventory at January 31, 2015, was up 27.1% compared with

January 31, 2014, which supports current industry retail trends.

Increase due in part to inventory of acquisitions which were not

included in prior year and winter weather which hurt deliveries in FY14.

Lenders still comfortable with current dealer inventory turns and

current credit line utilization, year-over-year turns have increased

modestly, resulting in a slight reduction in average age of Thor units on

dealers’ lots.

2015 2014 % change

RV 76,441 60,149 +27.1%

Dealer Inventory: January 31 (units)

18

Retail demand has driven rebound in towables and motorized

Wholesale units typically outpace retail in the early part of the calendar year; historically sales become more balanced as we reach the peak retail selling season

The RV Market Ahead

* Statistical Surveys, inc., includes US and Canada. 2011, 2012, 2013 & 2014 Full Year Actual

** RVIA wholesale shipments for full years 2011, 2012, 2013 & 2014

Calendar Year

2011 2012 2013 2014

Industry Retail

Registrations*

246,180 units

(+8.6%)

262,805 units

(+6.8%)

301,399 units

(+14.7%)

326,168 units

(+8.2%)

Industry

Wholesale

Shipments**

252,407 units

(+4.1%)

285,749 units

(+13.2%)

321,127 units

(+12.4%)

356,735 units

(+11.1%)

19

On January 5, 2015, Thor announced that its Heartland RV subsidiary acquired towable RV maker Cruiser RV (CRV) and luxury fifth wheel maker DRV Luxury Suites, both based in Howe, Indiana, for $47.4 million in cash, subject to post-closing adjustments.

CRV produces light-weight laminated travel trailers targeting the fast-growing entry- to mid-priced segments of the market while DRV is a leader in high-end luxury fifth wheels, including some custom units that complement Heartland’s luxury fifth wheel brands. CRV and DRV generated approximately $135 million in combined sales for calendar 2014.

With locations about 35 miles from Heartland’s main complex, CRV and DRV offer opportunities for expanded production for Heartland while drawing from a talented labor pool in an adjacent county.

Acquisition of Cruiser RV and DRV Luxury Suites

20

On May 1, 2014 Thor acquired RV manufacturer K-Z, Inc., based in Shipshewana, Indiana, for $55.3 million in cash, after post-closing adjustments.

K-Z generated sales of nearly $150 million in calendar 2013, and we expect the acquisition to be accretive to earnings. Approximately 20-25% of sales are to Canada.

K-Z manufactures travel trailers, fifth wheels and toy haulers under popular brands such as Sportsmen, Spree, Durango, StoneRidge and Inferno, as well as their Venture Sport Trek and Sonic.

Products are sold through a network of 220 North American dealers with very little overlap with Thor’s existing dealer base.

Acquisition of K-Z, Inc.

21

In mid-fiscal 2013, Thor’s management team developed a three-year Strategic Plan focused on growth and operational improvement. The rolling three-year plan has been updated to cover the FY15-FY17 periods.

Thor’s Strategic Goals:

RETURNS: Strive to be unceasingly attentive to margin maintenance and, when indicated, improvement, designed to offer our shareholders a long-term superior rate of return

INNOVATION: Focus on continually offering industry-leading product innovation, quality and customer service to our customers

MARKET LEADERSHIP: Remain a market share leader in the primary categories in which we compete

MOTIVATION: Dedicated to the continued success of our decentralized business model which promotes and rewards entrepreneurship within our operating subsidiaries

COMMUNITY LEADER: Strive to build on our positive reputation in the marketplace and communities where we work, provide competitive benefits and advancement opportunities to employees, foster respect and frequent engagement with employees, dealers and business partners

Three-Year Strategic Plan Update

22

Key Milestones to achieving the plan:

Mid-single-digit top line growth through FY17 driven by organic growth, strategic expansion of production and capacity, as well as opportunistic acquisitions.

Dedication to maintaining strong relationships with our dealers to sharpen our focus on providing the best product to the customer.

Enhance our understanding of our end consumers and their needs with greater interaction through social media and direct communication channels.

Expansion of a continuous improvement process designed to positively affect product quality and operating efficiency.

We have achieved the first 100 basis points of the original 200 basis point gross margin improvement target set in the original plan. The remaining gross margin improvement goal will likely be more challenging as we pursue this over the remaining plan horizon.

Three-Year Strategic Plan Update

23

Solid sales growth in both motorized and towable sales resulting in a 34% improvement in sales from continuing operations, to

$852.4 million in the second quarter. Results for the second quarter of fiscal 2014 were adversely affected by the harsh winter

weather conditions last year, which were not present in the second quarter of fiscal 2015.

Net income from continuing operations for the second quarter was $30.3 million, up 76% from $17.2 million in the prior-year second

quarter.

Diluted earnings per share (EPS) from continuing operations for the second quarter was $0.57, up 78% from $0.32 in the second

quarter last year.

Including discontinued operations from Thor’s former Bus business, net income was $28.6 million, up 77% from $16.2 million in the

second quarter of fiscal 2014. Diluted EPS including discontinued operations was $0.54, up from $0.30 in the second quarter last

year.

Towable RV revenue in the quarter was $675.1 million, up 43% from last year driven by market acceptance of new towable products

as well as incremental sales from acquisitions. Second-quarter towable income before tax was $40.3 million, more than double the

$18.9 million last year. Towable RV income before tax for the second quarter increased to 6.0% of revenues from 4.0% a year ago.

Motorized sales increased 9% to $177.3 million for the second quarter of 2015. Income before tax was $11.9 million, up 6% from

$11.2 million last year. As a percent of revenues, motorized RV income before tax fell slightly to 6.7% of revenues from 6.9% a year

ago.

Total backlog was up 11% to $942.1 million. Towable backlog increased 25% to $626.1 million while motorized backlog decreased

8% to $316.0 million. Towable backlog reflects market acceptance of new product as well as the inclusion of acquisitions made in

fiscal 2014 and 2015. Decrease in motorized backlog reflects the impact of new production capacity on the Company’s ability to

meet increasing demand more timely, as well as prior year backlogs being elevated due to initial orders for Axis/Vegas in 1Q14.

Comments on 2nd Quarter 2015 Results

24

Profitable every year since our founding in 1980 – 34 years of profitability

Successfully weathered a severe downturn in 2007-09 while remaining profitable

Recent capital investments position Thor for growth and margin improvement over the long term

#1 overall RV market share in North America*

Rock-solid balance sheet. Significant cash on hand and historic cash generation –history of returning cash to shareholders

Diversified and innovative products

Strong consumer, dealer and lender relationships

Experienced team

THOR - Key Takeaways

* Statistical Surveys, Inc., YTD U.S. and Canada units YTD December 2014

Appendix: Financial & Market Data

26

THOR’s RV Competitive Advantage

Source: Statistical Surveys, Inc., U.S. and Canada

* Thor adjusted to include historical results of Livin’ Lite, Bison Coach, K-Z, Inc., Cruiser RV and DRV Luxury Suites for all

periods presented ** Forest River includes Palomino, Coachmen, Prime Time, Shasta and Dynamax *** Jayco adjusted to

include historical results of Open Range **** Allied Recreation includes Fleetwood and Monaco

U.S. and Canada Retail Registrations (units)

Total Share % Total Share % Total Share % Total Share %

THOR* 118,380 36.3% 115,539 38.3% 102,780 39.1% 95,478 38.8%

Forest River** 111,765 34.3% 99,822 33.1% 81,873 31.2% 74,035 30.1%

Jayco*** 41,341 12.7% 37,942 12.6% 33,803 12.9% 32,024 13.0%

Winnebago 10,339 3.2% 8,661 2.9% 7,053 2.7% 5,549 2.3%

Allied Recreation**** 4,859 1.5% 6,034 2.0% 5,839 2.2% 6,168 2.5%

Grand Design 4,147 1.3% 893 0.3% - 0.0% - 0.0%

Subtotal 290,831 89.2% 268,891 89.2% 231,348 88.0% 213,254 86.6%

All Others 35,337 10.8% 32,508 10.8% 31,457 12.0% 32,925 13.4%

Grand Total 326,168 100.0% 301,399 100.0% 262,805 100.0% 246,179 100.0%

Y/E 12/31/13 Y/E 12/31/12 Y/E 12/31/11Y/E 12/31/14

27

Sales, Continuing Operations ($ millions)Fiscal years ended July 31, Year-to-Date through January 31

$1,115

$1,849

$2,340

$2,640

$3,242

$3,525

$1,435

$1,774

2009 2010 2011 2012 2013 2014 2014 YTD 2015 YTD

28

Net Income, Continuing Operations ($ millions)Fiscal years ended July 31, Year-to-Date through January 31

$2.5

$91.2 $91.6

$111.4

$151.7

$179.0

$53.6

$69.5

2009 2010 2011 2012 2013 2014 2014 YTD 2015 YTD

29

Diluted EPS, Continuing OperationsFiscal years ended July 31, Year-to-Date through January 31

$0.04

$1.72 $1.66

$2.07

$2.86

$3.29

$1.01

$1.30

2009 2010 2011 2012 2013 2014 2014 YTD 2015 YTD

30

Regular Quarterly Dividends Fiscal years ended July 31

$0.07

$0.10

$0.15

$0.18

$0.23

$0.27

2010 2011 2012 2013 2014 2015

In addition to regular quarterly dividends, Thor paid special dividends of $0.50 per share in FY11, $1.50 in FY13 and $1.00 in

FY14.

31

2nd Quarter Financial Summary

2015 2014 % Change

Net Sales $852.4 $635.3 34.2%

Gross Profit 102.0 70.3 45.0%

% of Sales 12.0% 11.1%

SG&A 54.3 43.8 24.1%

% of Sales 6.4% 6.9%

All Other 3.6 2.7

Income Before Tax 44.1 23.9 84.7%

% of Sales 5.2% 3.8%

Income Taxes 13.9 6.7

Net Income (cont. ops.) 30.3 17.2 75.8%

Diluted EPS (cont. ops.) $0.57 $0.32 78.1%

Order Backlog

Towables 626.1 501.9 24.7%

Motorized 316.0 343.3 -7.8%

Total 942.1 845.2 11.5%

*Amounts in millions except per share data

Net Sales by segment:

• Towables +43%, motorized +9%

Income before tax by segment:

• Towables 6.0%, up from 4.0%

• Margins improved from better

fixed cost absorption with

significantly higher sales levels

• Motorized 6.7%, down from 6.9%

• Impact of product mix shift to

lower cost units as well as

increased facilities costs from

new plants

• EPS from continuing operations of

$0.57, up from $0.32 in second

quarter of 2014

32

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1Q2006 1Q2007 1Q2008 1Q2009 1Q2010 1Q2011 1Q2012 1Q2013 1Q2014 1Q2015

Quarterly Thor RV Unit Shipments

33

Thor RV Retail Market Share: Units

*Source: Statistical Surveys Inc., U.S. and Canada, Historical results adjusted to include results of Heartland, Livin’ Lite, Bison

Coach, K-Z, Inc., Cruiser RV and DRV Luxury Suites for all periods presented

37.4%

41.2% 40.9% 41.2%40.2%

38.0%

16.1%17.8%

19.5% 20.0%

23.3%23.8%

6.7%

12.4%14.4%

16.7%

22.1% 21.9%

2009 2010 2011 2012 2013 2014

Towable Retail Share* Class A/C Retail Share* Class B Retail Share*

www.thorindustries.com