thornhill bioenergy feasibility assessment - rdks.bc.ca · we are pleased to submit this...

TRANSCRIPT

ENSC 417 Designing Solutions in Environmental Engineering 2017 Capstone: Thornhill Bioenergy Feasibility Assessment 3333 University Way Prince George, BC V2N 4Z9 December 1st, 2017 Letter of Transmittal

Dear Sir/Madam, We are pleased to submit this engineering feasibility study for a bioenergy facility in Thornhill entitled “Thornhill Bioenergy Feasibility Assessment”. The assessment discusses in detail the findings of the study for developing a bioenergy industry in the Regional District of Kitimat Stikine. The study provides recommendations for using locally available biomass resources for bioenergy development with a focus on producing heat and biochar products. A complete economic, risk, and sustainability assessment of the proposed design is included in the study. The report has followed the given criteria as required by the instructor. Sincerely,

Kirsten Barlow ǀ Alec Busby ǀ Kris Nickerson ǀ Scott Tennant ǀ Georgia Ukpabi

Encl. Feasibility Study

ENSC 417 - Designing Solutions in Environmental Engineering The University of Northern British Columbia

THORNHILL BIOENERGY

FEASIBILITY ASSESSMENT Final Design Report

December 1st, 2017

Kirsten Barlow 230105011 Alec Busby 230102962 Kris Nickerson 230105163 Scott Tennant 230109777

Georgia Ukpabi 230114715

Page | i

CONTENTS 1 Executive Summary .................................................................................................................................... 1

1 Introduction .......................................................................................................................................... 2

1.1 Background ................................................................................................................................. 2

1.2 Problem Statement ..................................................................................................................... 3

2 Project Components ............................................................................................................................. 4

2.1 Location Selection ....................................................................................................................... 4

2.2 Feedstock Source ........................................................................................................................ 6

2.3 Technology & Process Flow ........................................................................................................ 7

2.4 District Heating ......................................................................................................................... 11

2.5 Bioproduct Market .................................................................................................................... 16

3 Economic Analysis ............................................................................................................................... 18

3.1 Capital Investment .................................................................................................................... 18

3.2 Operating & Maintenance Costs ............................................................................................... 19

3.3 Annual Benefits ......................................................................................................................... 19

3.4 Revenue Sensitivity ................................................................................................................... 21

4 Risk ...................................................................................................................................................... 23

4.1 Operational ............................................................................................................................... 23

4.2 Safety ........................................................................................................................................ 24

4.3 Social ......................................................................................................................................... 24

5 Sustainability Assessment ................................................................................................................... 24

5.1 Policy & Regulations.................................................................................................................. 26

5.2 Assessment of Potential Impacts .............................................................................................. 26

5.3 Emissions ................................................................................................................................... 29

6 Alternative Locations, Feedstock & Technology ................................................................................. 33

6.1 Diversifying Feedstock Supply................................................................................................... 33

6.2 District Heating & Electricity Generation Opportunities .......................................................... 33

6.3 Modular & Mobile Systems ...................................................................................................... 35

7 Recommendations .............................................................................................................................. 36

8 REFERENCES ........................................................................................................................................ 37

9 APPENDICES ...................................................................................................................................... A-1

Appendix A – Decision Matrix for Site Location ................................................................................ A-1

Appendix B – Heating Duration Curves .............................................................................................. B-1

Page | ii

Appendix C – District Heating Design for All Locations ...................................................................... C-2

Appendix D – District Heating Pipe Layout for All Locations .......................................................... D-11

Appendix E – Capital & Operating Cost Summary ............................................................................. E-2

Appendix F – Cash Flow Diagram for Thornhill Location ................................................................... F-1

Appendix G – Risk Matrix .................................................................................................................. G-1

Appendix H – Sustainability .............................................................................................................. H-1

Appendix I – Sample Calculations ....................................................................................................... I-1

Page | iii

FIGURES FIGURE 1: ELECTORAL AREA “E” OF THE UNINCORPORATED SETTLEMENT OF THORNHILL ......................................... 2 FIGURE 2: SIMPLIFIED POTENTIAL SITE LAYOUT FOR THORNHILL SITE. ........................................................................ 9 FIGURE 3: A SIMPLIFIED CONCEPTUAL PROCESS FLOW DIAGRAM OF THE BIOENERGY FACILITY. ............................. 11 FIGURE 4: DISTRICT HEATING PIPELINE LAYOUT. ........................................................................................................ 14 FIGURE 5: REVENUE SENSITIVITY FOR BAGGED AND BULK BIOCHAR PRICES AT 60% TOTAL PRODUCTION SOLD. ...... 21 FIGURE 6: PRICE SENSITIVITY BASED ON THE AMOUNT OF PRODUCED BIOCHAR THAT IS EFFECTIVELY SOLD. .......... 22 FIGURE 7: TERRACE HEAT DURATION CURVE. ........................................................................................................... B-1 FIGURE 8: DEASE LAKE HEAT DURATION CURVE. ...................................................................................................... B-1 FIGURE 9: THORNHILL OCP LAND USE PLAN MAP. .................................................................................................... H-1

TABLES TABLE 1: SITE LOCATION SUMMARY OF MAJOR CHARACTERISTICS. ............................................................................. 6 TABLE 2: ESTIMATED FEEDSTOCK COSTS FOR NORTHWEST BC ..................................................................................... 6 TABLE 3: ESTIMATED FEEDSTOCK SUPPLY NEAR TERRACE AND THORNHILL, BC ........................................................... 7 TABLE 4: ENERGY CONTENT AND EXPECTED FLOWRATES OF PROCESS ....................................................................... 8 TABLE 5: ENERGY INPUT AND OUTPUT, AS WELL AS ENERGY ....................................................................................... 8 TABLE 6: SIGNIFICANT SIZING AND OPERATIONAL CONSIDERATIONS FOR FACILITY EQUIPMENT. ............................ 10 TABLE 7: THORNHILL PEAK HEAT DEMAND FOR DISTRICT HEATING SYSTEM. ............................................................ 12 TABLE 8: THORNHILL PIPE SIZING REQUIREMENTS. .................................................................................................... 13 TABLE 9: MONTHLY NATURAL GAS COSTS AND AVERAGE HEAT DEMAND (GJ) FOR DISTRICT HEATING BUILDINGS.15 TABLE 10: CAPITAL COSTS FOR DISTRICT HEATING SYSTEM IN THORNHILL. .............................................................. 16 TABLE 11: AVERAGE RETAIL PRICES OF BIOCHAR PRODUCTS. ..................................................................................... 17 TABLE 12:THORNHILL MAJOR EQUIPMENT CAPITAL COST ESTIMATES. ..................................................................... 18 TABLE 13: ECONOMIC ANALYSIS SUMMARY FOR THORNHILL BIOENERGY FACILITY. .................................................. 20 TABLE 14: NPV SENSITIVITY TO CHANGING FACTORS. ................................................................................................. 21 TABLE 15: PARAMETER RANGES FOR MONTE CARLO SIMULATION. ............................................................................ 22 TABLE 16: RISK MATRIX. .............................................................................................................................................. 23 TABLE 17: VALUED ECOSYSTEM COMPONENTS (VECS) AND POTENTIAL EFFECTS ON THE ENVIRONMENT. ............. 26 TABLE 18: ANNUAL CO2E EMISSIONS FROM THE COMBUSTION OF NATURAL GAS AND WOOD WASTE. ................. 32 TABLE 19: CO2E EMISSIONS FROM THE DELIVERY OF ROADSIDE SLASH. ................................................................... 32 TABLE 20: DEASE LAKE PLANT CAPITAL COST ESTIMATE ........................................................................................... E-2 TABLE 21: TERRACE DOWNTOWN LARGE CAPITAL COST ESTIMATE......................................................................... E-2 TABLE 22: TERRACE DOWNTOWN SMALL CAPITAL COST ESTIMATE ........................................................................ E-2 TABLE 23: TERRACE INDUSTRIAL PLANT CAPITAL COST ESTIMATE ........................................................................... E-2 TABLE 24: THORNHILL PLANT CAPITAL COST ESTIMATE ........................................................................................... E-2 TABLE 25: SUMMARY OF OPERATING AND MAINTENANCE COSTS. ......................................................................... E-3 TABLE 26: COMPLETE MATRIX FOR PROJECT RISKS. ................................................................................................. G-1 TABLE 27: SKEENA SAWMILL (2015) ANNUAL HARVEST BREAKDOWN. ..................................................................... I-4 TABLE 28: SMALL-SCALE MILLS IN THE KALUM-KISPIOX REGION (2005) ANNUAL HARVEST BREAKDOWN. ............. I-4

Page | iv

LIST OF ACRONYMS

bf Board Feet CEAA Canadian Environmental Assessment Agency CEEI Community Energy and Emissions Inventory CO2e Carbon Dioxide Equivalents COD Commercial Operation Date EAO Environmental Assessment Office ECCC Environment and Climate Change Canada EPA Electricity Purchase Agreement GHG Greenhouse Gas GHGRP Greenhouse Gas Emissions Reporting Program GJ Giga Joule HJBEP Haines Junction Biomass Energy Project ICE Internal Combustion Engine IPCC Intergovernmental Panel on Climate Change NALS Northern Analytical Laboratory Services ODT Oven Dry Tonne PNCDS Pacific North Coast Development Society RDKS Regional District of Kitimat Stikine SNCIRE Skeena-Nass Centre for Innovation in Resource Economics SOP Standing Offer Program t Metric Tonne UNBC University of Northern British Columbia UNFCCC United Nations Framework Convention on Climate Change VECs Valued Ecosystem Components

Page | 1

1 EXECUTIVE SUMMARY This project presents a feasibility assessment for a bioenergy facility in Thornhill, BC. Five

site locations were assessed for their optimality with regards to district heat demand, social

impacts, and capital investment. We are pleased to have determined the Thornhill site as the top

choice to invest in for developing a future bioenergy industry within the Regional District of

Kitimat Stikine (RDKS).

The proposed design consists of a pyrolysis-gasifier system integrated with a district

heating system. Feedstock sourced from small-scale sawmills within the RDKS is expected to

meet the demand of 4,617 ODT of woody biomass on an annual basis to fuel the 527 kg/hr

facility. This feedstock is a combination of roadside slash and sawmill residues, and is expected to

be purchased at an average price of $49.50 per tonne.

The pyrolysis system is designed to annually produce approximately 1,614 tonnes of

biochar to market. Biochar as a soil amendment in bulk and bag form is estimated to sell at a

wholesale price of $400 per tonne and $35 per bag. Excess heat can be cost-effectively

distributed to the surrounding residential and commercial buildings as the plant is designed to

provide 80% of the peak energy demand, approximately 40,291 GJ yearly. Electricity generated

from syngas combustion can be used to power the facility’s operations and offset electrical costs

completely.

Project deliverables include:

a. Process flow of proposed technology

b. District heating system design for optimal location

c. Economic analysis including Class D cost estimates and sensitivity analysis

d. Sustainability assessment on the social, economical and environmental impacts

This report offers a sustainable, feasible, and progressive conceptual design that supports

the regional district’s intent to utilize forestry residuals, enhance local economy, and encourage

alternative energy initiatives in Northwest British Columbia.

Page | 2

1 INTRODUCTION

1.1 Background The purpose of this report is to propose and justify the development of a bioenergy

industry in Thornhill, BC. An investigation into available bioenergy technologies with scalable and

flexible capabilities, and the determination of an optimal size and type of facility for the Thornhill

site that meets the energy demand is proposed. A complete economic, risk, and sustainability

assessment is conducted to establish our final recommendations. The information presented is

intended to form a basis for assessing project feasibility.

Thornhill is an unincorporated settlement located approximately 575 kilometres west of

Prince George, in the Regional District of Kitimat Stikine (RDKS), and situated on the east bank of

the Skeena River directly across from the City of Terrace (Figure 1). Thornhill is within the

traditional territories of Kitselas, Kitsumkalum, Lax Kwa’laams, and Metlakatla First Nations

(Urban System Ltd., 2017). In 2016, the reported population was 3,993 and showing growth of a

mere 0.1% since 2011 (Canada, G. O., 2017). The total land area of the settlement is 16.5 square

kilometres.

Figure 1: Electoral Area “E” of the unincorporated settlement of Thornhill

.

http://www.rdks.bc.ca/sites/default/files/2017-07-06-thornhill_ocp_draft_for_website.pdf

Page | 3

The Skeena-Nass Forest is home to the majority of forest resources within the RDKS and

Thornhill lies predominantly in the biogeoclimatic zone of Coastal Western Hemlock Wet Sub-

maritime with the dominant tree species being Western Red Cedar, Western Hemlock, Balsam

and Sitka Spruce (Urban System Ltd., 2017). With hemlock in the range of 35% to 75% and

balsam making up 19% to 38% of this forest inventory, the species mix is commonly referred to

as hem-fir and is known for having low-quality high-moisture characteristics that make the area

economically challenging to harvest (SNCIRE, 2013).

1.2 Problem Statement Prior to 2000, Northwest BC’s forest industry was operating in full force with 17 major

timber processing facilities and approximately 5,000 direct jobs. A combination of factors,

including the high percent of low-value hem-fir logs, led to an industry collapse. By 2013, the

number of major timber processing facilities had declined to five with an approximate 700

remaining employees (SNCIRE, 2013). In response to this downturn, RDKS has invested research

efforts in exploring emerging bioenergy technology with the goal of renewing Northwest BC’s

forest economy.

A typical BC sawmill’s log input produces 40% residual wood chips and 12% sawdust or

shavings (SNCIRE, 2013). This near 50:50 waste to lumber ratio is what makes generating a profit

from wood waste material of high economic value to sawmills in the region. Bioenergy

technology allows mills to dispose of residual wood waste in a manner that is carbon neutral, if

not carbon negative, while also benefiting from heat and electricity production, as well as

marketable bioproducts.

There have been several demonstration and pilot plants proposed in Northwest BC aimed

at producing bioproducts and combined heat and power, however, none have been executed to

date. Currently, the regional district has expressed interest in a local bioenergy company, BC

Biocarbon, based out of McBride. BC Biocarbon’s slow-pyrolysis system effectively reduces high-

moisture wood waste into biochar, bio-oil, and syngas. This technology, along with similar

bioenergy processes, was explored for this study to determine the optimal location, size, and

bioproduct streams that will contribute to an economic renewal of the region’s forest industry.

Page | 4

2 PROJECT COMPONENTS

2.1 Location Selection Site selection was a major part of the design process. Site characteristics initially

considered for choosing the facility location include zoning, district heating demand, and land

availability. An initial survey of orthographic photos and maps of Thornhill, Terrace, and Dease

Lake was conducted to select four potentially suitable sites located on different lots and

exhibiting different strengths and weaknesses to be explored for the design. From these four

lots, five scenarios were considered: Terrace Downtown Small-Scale, Terrace Downtown Large-

Scale, Thornhill, Dease Lake, and Terrace Industrial.

Information on the properties was gathered and district heating scenarios were

developed for each site using a variety of sources including online GIS systems (Regional District

of Kitimat Stikine, 2017) and BC Assessment (2017). The size of each district heating scenario

varied, primarily due to the density of buildings in the immediate vicinity, and professional

judgement helped to determine which buildings to consider. The district heating scenario was

built out and specified for each of the scenarios using historical heat duration curves (Helle,

2017). These district heating scenarios were then directly applied to determine the appropriate

process size to provide 80% of the maximum heat demand. In this way, the selected sites had a

direct impact on the final process. In determining the most optimal site, factors in the following

categories were considered: district heating; social considerations; practical considerations;

feedstock; bioproduct; and economics. Full descriptions of these categories and rating results

are provided in Appendix A.

District heating considerations focused on the value of each system in terms of the

capital cost per unit heat provided, as well as the percentage of the district heating capital costs

allocated to piping costs. The latter indicator was used as an analog for efficiency wherein a

system with less piping to deliver a specific amount of heat has higher density, and is more

efficient in terms of energy losses and initial investment.

Social factors were assessed on the location’s proximity to sensitive land uses, such as

residential and commercial structures, and whether trucking routes went through urban areas.

These factors were evaluated with orthographic maps, community plans, and best judgement. A

Page | 5

site located on a main highway or in an industrial zone was considered to have a low trucking

impact, whereas a location within town and away from normal industrial areas posed a higher

trucking impact. Sensitive land uses were judged by building type, and residential or light

commercial buildings were considered sensitive land uses and scored lower in this aspect.

Practical considerations included the zoning, the cost and surface area of the lot,

whether the lots required clearing, the distance to markets, and the attractiveness of expanding

electricity production in the future. These considerations were meant to represent, in part, how

challenging and expensive it would be to establish a plant on each site. The attractiveness of

expanding into electricity was meant to give an advantage to the Dease Lake site since it is an

off-grid community. In general, electricity is more expensive in off-grid locations, and the process

for getting approved to sell power is less restrictive in off-grid communities.

The final considerations rated feedstock price and supply, financial performance, and

financial risk. The price and supply of feedstock was used to separate the Terrace sites from the

Dease Lake site; the presence of sawmills and logging activity near Terrace implied a larger

supply of lower price feedstock. The indicators of financial performance and financial risk were

both normalized by capital cost to lessen the bias towards selecting a larger facility. For both

considerations, a Monte Carlo simulation of the facility at each site was performed. The mean

net present value (NPV) normalized by the mean capital cost served as the financial performance

indicator. The standard deviation of the NPV normalized by the mean capital cost was used as

the financial risk indicator.

The decision matrix used both quantitative and judgmental considerations, normalized to

a 5-point scale to perform the comparison. Each consideration was then given a weight, also on a

5-point scale, based on the perceived relative importance of those considerations. Based on the

weighted decision matrix, the Thornhill site was selected for an in-depth economic analysis and

site layout. The Terrace industrial site came a close second, with the Dease Lake site exhibiting

the worst performance. Major characteristics for each site are summarized in Table 1 below.

Page | 6

Table 1: Site location summary of major characteristics.

2.2 Feedstock Source The feedstock requirement for the Thornhill plant has been estimated at 4,617 ODT/yr.

Feedstock sources should be acquired at an acceptable cost to meet this requirement. Typical

feedstock costs for Northwest BC are shown in Table 2 based on values from Sauder (2012). The

cost of delivered logs in the region are high due to challenging terrain and high decay factors.

Furthermore, whole logs and chipped logs from the forest are assumed to incur costs due to

development, harvesting and silviculture.

Table 2: Estimated feedstock costs for Northwest BC

Source Cost/Odt

Delivered log costs1 $151-157

In-woods chipped log costs1 $130-145

In-woods residue chipping costs1 $55-85

Assumed sawmill hog fuel costs1 $25-30

Assumed maximum acceptable feedstock price (CHP) 1 $60

Assumed feedstock costs for the Thornhill plant $50 1Sauder, 2012

Table 2 shows that forest residues are a lower cost option. Forest slash is estimated to be

abundant in the region, as seen in Table 2 (see details in Appendix II). The current practice is to

burn forest slash to decrease the fire hazard and improve forest accessibility. The plant must be

able to source enough biomass within a reasonable distance to meet feedstock requirements.

Technical limitations of machinery and operations for extracting forest residues adds additional

costs and restricts the amount of residues that can be collected (Yemshanov et al., 2014).

Site Land Value Lot Size

(m2)Zoning

Heat provided/

District Heating

Capital (GJ/$)

Net Present

ValueCapital

Standard

Deviation/

Capital

Decision

Matrix

Score

Terrace

Downtown

Large

318,000$ 4200 Light Industrial 14.6 $ 12,354,457 $ 8,367,673 1.03 91

Terrace

Downtown

Small

318,000$ 4200 Light Industrial 18.5 $ 429,537 $ 4,232,408 0.88 92

Terrace

Industrial275,000$ 9650 Industrial 13.7 $ 6,771,972 $ 6,171,817 1.05 125

Thornhill 242,000$ 7500Light Industrial/

Highway Commercial10.5 $ 551,984 $ 3,874,993 0.97 129

Dease Lake 24,700$ 4000 ICI 16 $ (9,740,487) $ 2,780,216 0.75 70

Page | 7

Table 3: Estimated feedstock supply near Terrace and Thornhill, BC

Feedstock source Sawmill chips (ODT/y)

Roadside slash (ODT/y)

Skeena sawmill (2015) 71,200 45,800

Small-scale mills (2005) 8,800 5,680

Total 80,000 51,480

Sawmill chips are considered the lowest cost option in Table 2. Sources of these residues

include the large and small-scale mills near Thornhill (see Table 3). Skeena Sawmill could serve as

a potential source of low cost wood chips. An IFS report for BC Hydro states there is currently no

buyer or outlet for the residual fibre in the region, and it is either stockpiled or land-filled since

the regional pulp mills shut down. However, it should be noted that there is indication Skeena

Sawmill is currently in the design phase of a new pellet plant with a capacity of 96,000 ton/yr

(87,000 tonnes/yr) from wood chips and shavings (Prodesa, 2017). Pellet plants typically require

clean wood chips and shavings to produce high quality pellets with low ash content (ENVINT,

2010). In such circumstances, Skeena Sawmill could be a potential source of hog fuel and lower

grade chips.

It is recommended that low costs sawmill residues be sourced. However, if mill sources

become uncertain or unavailable, another option is forest slash. An assumed feedstock cost for

the Thornhill plant was set at $50/ODT for this reason. Guaranteeing a cost-effective, long term

feedstock source is a way to minimize this risk. In addition, integrating different supply chains

can also mitigate this risk. Long-term supply contracts can be used as a source guarantee and

hedge against fluctuations in feedstock costs.

2.3 Technology & Process Flow

Process Sizing

An energy and mass balance approach was used to specify the major process equipment.

The process was sized based on the district heating system that was specified for each location;

the maximum heat output was set to be the amount of heat required to meet 80% of peak

energy demand. From that energy demand, and the expected energy demand for an internal

combustion engine used to provide the internal electricity requirements, the peak gas demand

Page | 8

for the system was calculated, using a literature value for the energy content of gasifier gas

(Basu, 2013). From the peak gas requirement, a gasifier was specified, using a literature value for

the efficiency of the gasifier (Basu, 2013). Based on the expected energy content and makeup of

the output from the pyrolysis unit, and the required energy to the gasifier, the size of the

pyrolysis unit was specified. In sizing for peak demand, it was assumed that all of the biochar

from the pyrolysis unit would be gasified at peak demand, and at lower demand the biochar not

required by the system would be kept aside for sale. The main assumption made about the

pyrolysis unit was the product breakdown (25% biochar, 25% pyrolysis gas, 50% pyrolysis oil),

which was based off of literature values (Basu, 2013). The energy content and chemical

composition of a representative sample of chips, as well as biochar produced by BC Biocarbon,

was determined by Northern Analytical Laboratory Services (NALS) at UNBC. These values are

within the range specified in the literature, so they were utilized in the calculations. The rest of

the energy values were literature based (Basu, 2013). A rough site layout is presented on the

next page.

Table 4: Energy content and expected flowrates of process products and intermediates at maximum heat demand.

Table 5: Energy input and output, as well as energy efficiency for key processes at maximum heat demand.

LHV, Dry Basis

(kJ/kg)

Flow Rates, Dry Basis

(kg/hr)

Chips 18157 527

Biochar 27523 132

Pyrolysis Oil 13000 264

Pyrolysis Gas 11000 132

Gasifier Gas 4000 1701

Energy (kW) Efficiency

Pyrolysis Input 2658

Pyrolysis Output 2362

Gasifier Input 2362

Gasifier Output 1889

Engine Input 358

Engine Output 86

Boiler Input 1531

Boiler Output 1378

89%

80%

24%

90%

Page | 9

This design gives a range of variability in operation; with the limiting steps being the

pyrolysis unit and the gasifier, due to the limitations on the low end of their operation. The

natural gas boiler has a high range of turndown, so it can run on any amount of gas that the

gasifier provides. The gasifier has a limited turndown; however, if the minimum heat production

exceeds the required heat production, then the excess gas can be flared.

If there is excess biochar that cannot be sold, that biochar can be used to displace fuel.

The pyrolysis unit can be run at the lowest end of production and excess stored biochar can be

fed into the gasifier along with all current products of the pyrolysis unit. If the pyrolysis vessel

has to be shut down, then the gasifier can be run on stored biochar until the pyrolysis process is

operating again. This method would reduce profits if that biochar could be sold otherwise, but it

would ensure that constant heat is supplied to the consumers, and displace fuel costs. Due to

the higher unit value of biochar than the feedstock chips, this operating method is not

economically beneficial. However; if that biochar would otherwise have to be given away or sold

at a very low rate, then offsetting fuel costs and maintaining the sale of heat would be beneficial.

Figure 2: Simplified potential site layout for Thornhill site.

Page | 10

Table 6: Significant sizing and operational considerations for facility equipment.

Conceptual Process Flow

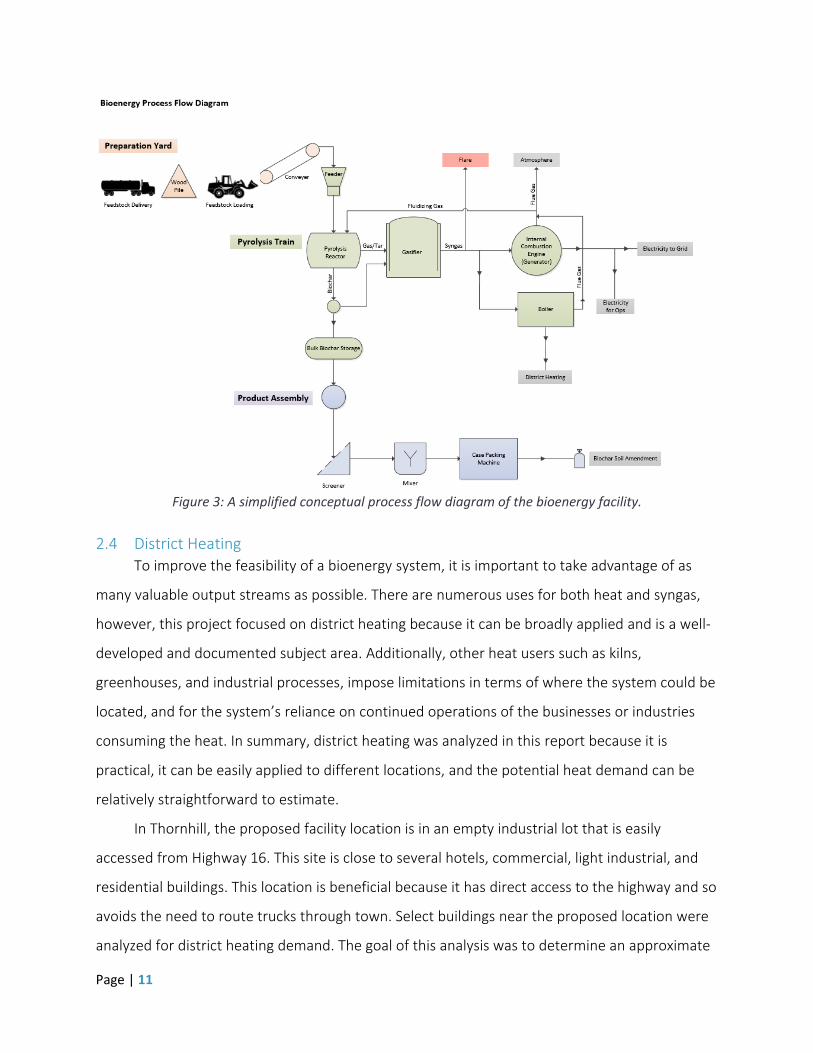

Starting in the preparation yard, wood waste is collected and conveyed into the pyrolysis

reactor. Gas and tar produced in the pyrolyzer is sent to a gasifier and further conditioned into a

cleaner syngas. The syngas can either be both fed into an internal combustion engine (ICE) for

electricity generation, and to a natural gas boiler for district heating. Flue gas exiting the ICE and

boiler is emitted to the atmosphere. Biochar produced during pyrolysis is either gasified, stored

as bulk, or further manufactured into a bagged soil amendment. Please see Figure 3 below.

Page | 11

Figure 3: A simplified conceptual process flow diagram of the bioenergy facility.

2.4 District Heating

To improve the feasibility of a bioenergy system, it is important to take advantage of as

many valuable output streams as possible. There are numerous uses for both heat and syngas,

however, this project focused on district heating because it can be broadly applied and is a well-

developed and documented subject area. Additionally, other heat users such as kilns,

greenhouses, and industrial processes, impose limitations in terms of where the system could be

located, and for the system’s reliance on continued operations of the businesses or industries

consuming the heat. In summary, district heating was analyzed in this report because it is

practical, it can be easily applied to different locations, and the potential heat demand can be

relatively straightforward to estimate.

In Thornhill, the proposed facility location is in an empty industrial lot that is easily

accessed from Highway 16. This site is close to several hotels, commercial, light industrial, and

residential buildings. This location is beneficial because it has direct access to the highway and so

avoids the need to route trucks through town. Select buildings near the proposed location were

analyzed for district heating demand. The goal of this analysis was to determine an approximate

Page | 12

heat demand and to ensure there were enough potential customers within reasonable distance

to the plant to ensure district heating would be economically viable.

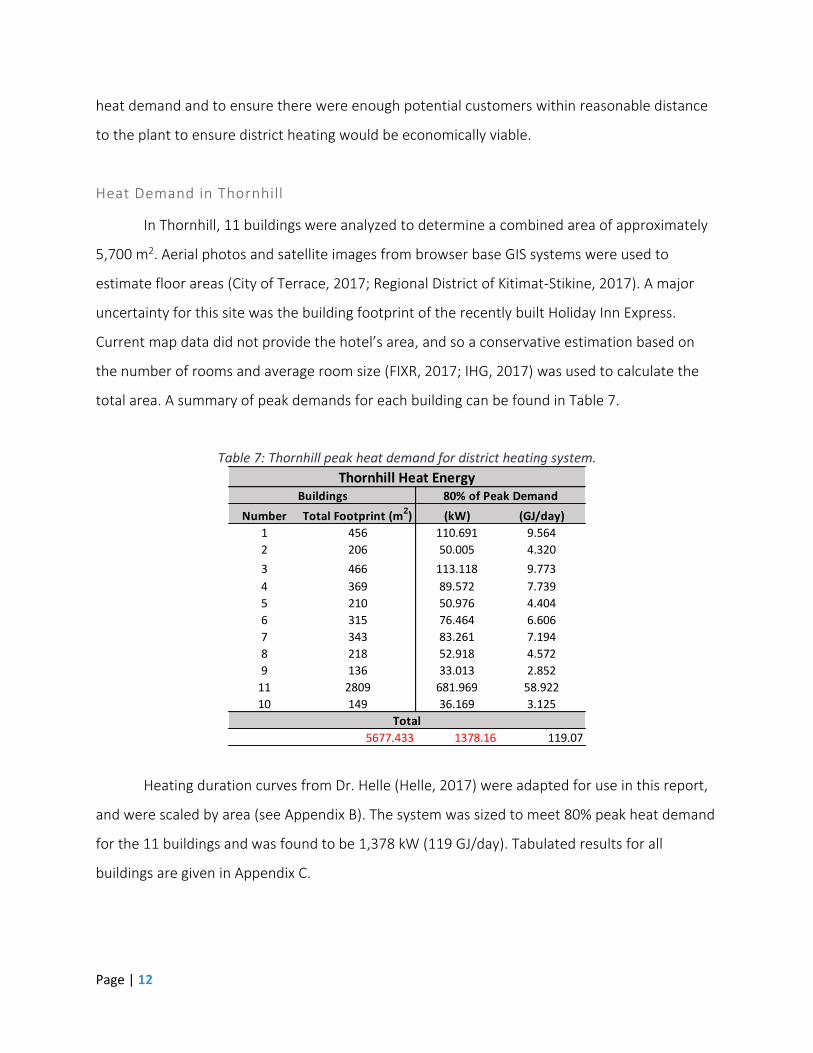

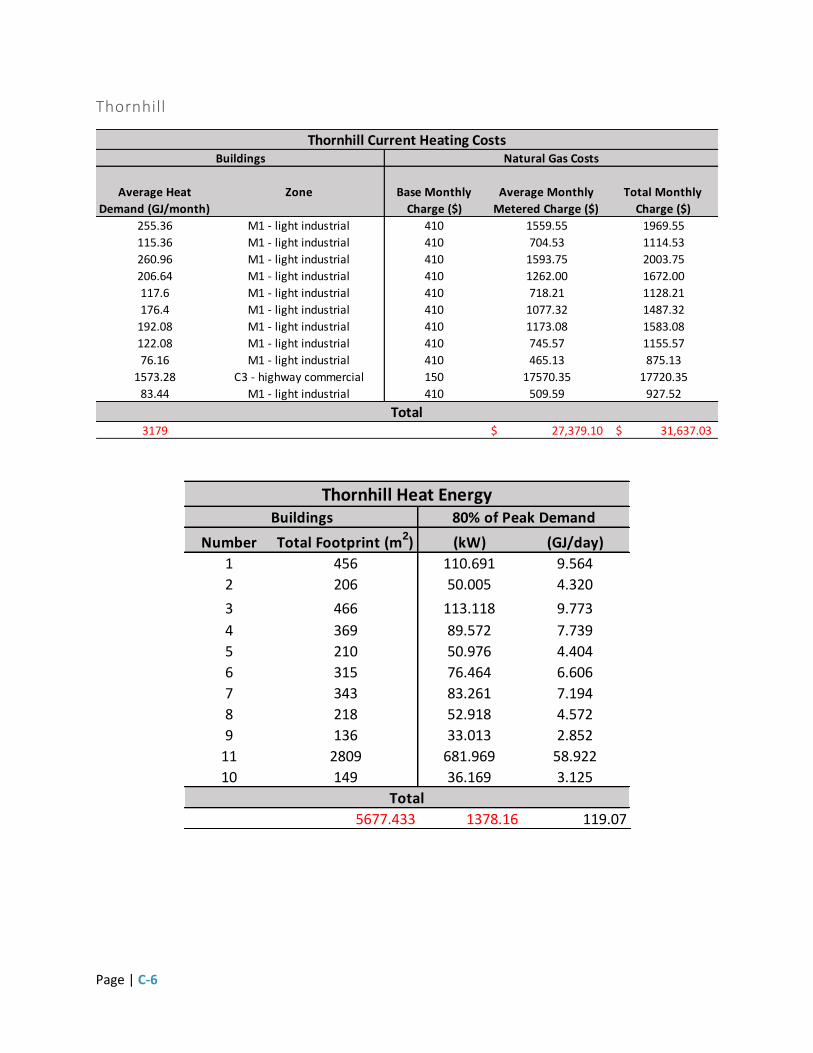

Heat Demand in Thornhill

In Thornhill, 11 buildings were analyzed to determine a combined area of approximately

5,700 m2. Aerial photos and satellite images from browser base GIS systems were used to

estimate floor areas (City of Terrace, 2017; Regional District of Kitimat-Stikine, 2017). A major

uncertainty for this site was the building footprint of the recently built Holiday Inn Express.

Current map data did not provide the hotel’s area, and so a conservative estimation based on

the number of rooms and average room size (FIXR, 2017; IHG, 2017) was used to calculate the

total area. A summary of peak demands for each building can be found in Table 7.

Table 7: Thornhill peak heat demand for district heating system.

Heating duration curves from Dr. Helle (Helle, 2017) were adapted for use in this report,

and were scaled by area (see Appendix B). The system was sized to meet 80% peak heat demand

for the 11 buildings and was found to be 1,378 kW (119 GJ/day). Tabulated results for all

buildings are given in Appendix C.

Number Total Footprint (m2) (kW) (GJ/day)

1 456 110.691 9.564

2 206 50.005 4.320

3 466 113.118 9.773

4 369 89.572 7.739

5 210 50.976 4.404

6 315 76.464 6.606

7 343 83.261 7.194

8 218 52.918 4.572

9 136 33.013 2.852

11 2809 681.969 58.922

10 149 36.169 3.125

5677.433 1378.16 119.07

Total

Thornhill Heat EnergyBuildings 80% of Peak Demand

Page | 13

Pipe Design

It is recommended that the district heating system be constructed from pre-insulated

PEX piping from Uponor. The pipes come in twin and single tubed pipes and can be placed

directly into pre-dug trenches. They have the added benefit of being able to circumvent

obstacles, such as boulders, this flexibility will cut down on installation costs. The pipes are

bought in large coils up to 1,000 feet in length which decreases pipe connections and further

minimizes costs.

Pipe sizing used the specific heat formula and was based on peak heat demand. Delta T

was approximated based on rules of thumb at a 30 degree drop from 85C-55C (Helle, 2017).

This formula was also used to calculate the required mass flow of the water travelling through

the pipes. The volume of water was determined using 2 m/s water velocity (Helle, 2017), and this

then lead to appropriate pipe diameter sizes for each line of the district heating system.

Table 8: Thornhill pipe sizing requirements.

Mass Flow

(kg/day)

Volume Flow

(m3/s)

Pipe Diameter

(inch)

Required Pipe Size to

Deliver Demand (inch)

76192.44 0.000882 0.9328 1

34420.27 0.000398 0.6270 1

77863.33 0.000901 0.9430 1

61655.73 0.000714 0.8391 1

35088.63 0.000406 0.6330 1

52632.94 0.000609 0.7753 1

57311.42 0.000663 0.8090 1

36425.34 0.000422 0.6450 1

22724.06 0.000263 0.5094 1

469424.49 0.005433 2.3154 2.5

24896.22 0.000288 0.5332 1

948635 0.0110 2.87 3

1.62 1.5

Thornhill Pipe Design

Total To Buildings in Line 1

To Buildings in Line 2

Maximum Energy Delivery (kW)

1378.16

Page | 14

Pipe Layout

The layout of the district heating system consists of two main pipelines leaving the site in

opposite directions. Line 1 is a 150m long 3-inch single pipe (Uponor twin pipes have a maximum

diameter of 2.5-inch) with an identical return pipe and leads southwest to buildings 1, 2, 3, 4,

and 11. Line 2 leads northeast connecting buildings 5, 6, 7, 8, 9, and 10, and splitting at

Desjardins Avenue. Line 2 then travels east for 115m to connect buildings 8, 9, and 10. An

orthographic view of the system layout is shown below.

Figure 4: District heating pipeline layout.

Current Energy

The site’s natural gas usage was researched to assess how much residents currently pay

for heat, and to get an idea of how to structure the system’s heat delivery. Terrace and Thornhill

residents are currently supplied with natural gas from Pacific Northern Gas Limited. Consumers

are charged a basic monthly rate coupled with a delivery and usage charge (PNG, 2017). These

charges depend on a “rate class” that is assigned according to zoning and activity that occurs on

the property.

The Thornhill site is largely zoned as M1-Light Industrial. This corresponds to a $410

monthly charge and one of the lowest usage rates of approximately $5.80/GJ. The largest

Page | 15

building in the district heating plan is the Holiday Inn and is zoned as C3-Highway Commercial. It

has a higher than average usage rate of approximately $10.60/GJ and accounts for 56% of the

total cost to heat the 11 buildings. The monthly GJ demand and charge for each building is

shown below in Table 9.

Table 9: Monthly natural gas costs and average heat demand (GJ) for district heating buildings.

Costs

The capital costs for installing a district heating system in Thornhill are split into two main

groups, the pipeline and the boiler system, each accounting for roughly 50% of the costs. As

mentioned previously, pipes were sourced from Uponor and cost $251.30 per meter of 3-inch

single pre-insulated pipe, and $173.70 per meter for the 1.5-inch twin pre-insulated pipe.

Installation costs for the pipes were determined based on reports of similar district heating

systems in the Kitimat-Stikine area, and were estimated to $200 per meter (Nairne, 2014;

Wunderlin, 2012; FVB Energy, 2011). The installation included trench digging, pipe fitting,

connections, labor etc. Boiler costs were determined using a common rule of thumb for

installation, engineering, and other equipment costs of about 3 times the capital cost for the

purchased boiler (Turton, 2009). Energy transfer station costs were approximated per m2 using

Average Heat

Demand (GJ/month)

Zone Base Monthly

Charge ($)

Average Monthly

Metered Charge ($)

Total Monthly

Charge ($)

255.36 M1 - light industrial 410 1559.55 1969.55

115.36 M1 - light industrial 410 704.53 1114.53

260.96 M1 - light industrial 410 1593.75 2003.75

206.64 M1 - light industrial 410 1262.00 1672.00

117.6 M1 - light industrial 410 718.21 1128.21

176.4 M1 - light industrial 410 1077.32 1487.32

192.08 M1 - light industrial 410 1173.08 1583.08

122.08 M1 - light industrial 410 745.57 1155.57

76.16 M1 - light industrial 410 465.13 875.13

1573.28 C3 - highway commercial 150 17570.35 17720.35

83.44 M1 - light industrial 410 509.59 927.52

3179 27,379.10$ 31,637.03$

Thornhill Current Heating CostsBuildings Natural Gas Costs

Total

Page | 16

numbers from the same reports of the installed district heating systems from nearby

communities (Nairne, 2014; Wunderlin, 2012; FVB Energy, 2011); this totaled to approximately

$7.40/m2. Exact capital costs are detailed in Table 10.

Table 10: Capital costs for district heating system in Thornhill.

2.5 Bioproduct Market

Apart from heat, a major by-product of the pyrolysis process is biochar. Since the facility

will output approximately 1,614 tonnes of biochar annually, it is highly recommended to explore

revenue options for generating a profit from this waste stream. Potential biochar products

requiring refining, such as activated carbon, were omitted from bioproduct options to keep

capital costs and operating requirements to a minimum.

Current retail prices of brand name bioproducts were averaged for bulk biochar soil

amendment, bagged biochar soil amendment, and bagged charcoal briquettes (see Table 11).

These prices are based on the average biochar bulk density of 264 kg/m3, the average charcoal

briquette density of 408 kg/m3, and the average bulk biochar market prices of $0.89 to $1.00

(USD) per pound (IBI, 2017 & The Char Team, 2015). These price estimates are expected to

change once a more precise characterization of the facility’s biochar bulk density is tested and

confirmed.

Pipe Length (m) 150

Pipe Cost ($) 75,393.00

Installation Costs ($) 30,000.00

Pipe Length (m) 260

Pipe Cost ($) 45,151.60

Installation Costs ($) 52,000.00

Energy Transfer Station Costs ($) 42,013.00

Boiler Cost ($) 38,588.36

Installation, Engineering, and Minor Equipment ($) 115,765.08

Total Cost ($) 398,911.04$

Thornhill District Heat System Cost

Line 1

Line 2

Page | 17

Table 11: Average retail prices of biochar products.

Bulk sales to agriculture on a contractual basis is an effective way to help ensure a fast

product turnover, to secure a steady revenue, and to minimize the burden of storing unsold

individually bagged products.

Biochar as a soil amendment does not need extensive applications to be effective. For

this reason, individually bagged biochar products are not likely to be bought very frequently

since gardeners do not need to use a lot of the product when applying it to their soils. To

maintain a steady consumer base, it is recommended that the soil amendment be marketed

internationally through an online platform, as is currently practiced by other successful

companies in this industry.

In comparison with the soil amendment option that requires no further processing to

create a final product, biochar briquettes may require the addition of a binding agent, such as

coal tar pitch, to help densify the briquette. Although the capital cost of a briquetting machine

may increase production costs for bagged briquettes, there may also be an opportunity to utilize

the machine for feedstock preparation of non-uniform or small-diameter wood wastes.

Page | 18

3 ECONOMIC ANALYSIS

3.1 Capital Investment

Installed capital cost estimates for the Thornhill plant are shown in Table 12. The values

are based on data from the EPA Biomass CHP Catalog of Technologies (2007), which were

obtained from published estimates and discussions with equipment suppliers by the Antares

Group, Inc. (2003). Plant costs depend on several major process steps including: biomass

collection, preprocessing, biomass conversion, gas cleanup, and product utilization. The main

cost for the pyrolysis-gasification train is the reactors, gas cleanup and syngas cooling. This

typically involves ash removal, quench, bag filter, wet scrubber, and heat exchangers. Heat

exchangers can provide heat to other parts of the process or contribute to district heating.

Table 12:Thornhill major equipment capital cost estimates.

Component Unit Quantity Unit cost Amount

Detailed feasibility study cost 1 $10,000.00 $10,000.00

Development cost 1 $10,000.00 $10,000.00

Pyrolysis and gasifier system kW 1889 $529.54 $1,000,530.38

ICE-genset kW 86 $1,101.49 $94,727.79

Biomass storage and handling kW 1464 $1,088.12 $1,593,010.17

Engineering % 10% $2,708,268.33 $270,826.83 Contingency % 10% $2,708,268.33 $270,826.83

Total cost $3,249,922.00

The capital cost estimate assumes the gasifier system operates with air at atmospheric

pressure and produces a low energy gas, typically from 4 to 6 MJ/m3 (EPA, 2007). The syngas

produced (1,889 kW) is used in different ways. A portion is sent to an ICE to generate a small

amount of electricity (86 kW), but the majority goes into district heating (1,378 kW). The cost for

biomass storage and product handling is another large costs for the plant, which has a calculated

feedstock requirement of 4,617 ODT/yr. Assumed costs for other plant requirements, such as

supplementary studies, development, engineering and contingency, have also been included as

shown in Table 12.

The total fixed capital investment for the Thornhill bioenergy facility is $3.89 million. This

cost includes the district heating system and boiler, the assessed land value of the chosen site,

Page | 19

and major equipment installed costs. To offset capital investment, potential project funding may

be available under the Northern Development Initiative Trust Funding Programs, the Federation

of Canadian Municipalities Green Municipal Fund, and the Innovative Clean Energy (ICE) Fund.

3.2 Operating & Maintenance Costs

Annual operating and maintenance costs amount to $1.62 million and are based on

feasibility level cost estimates adapted from (Turton, 2009). Of this total, approximately

$228,500 is allocated to purchasing feedstock at an average estimated cost of $49.50 per ODT.

Feedstock sourced from small-scale sawmills is estimated to provide 14,480 ODT/yr of wood

chips and slash, and the 527 kg/hr facility requires only 4,617 ODT/yr of this available fuel.

An estimated three to four plant operators are required year-round (49 weeks of the year to

account for holidays) on a 3-shift per day basis. Additional personnel to manage, coordinate, and

supervise operations are also accounted for in labour costs. It is expected that seasonal labour

for product assembly will be required for 4 months of the year when biochar products will be

manufactured.

Utilities costs omit water usage and waste treatment, and electricity consumption is

assumed negligible since operations are expected to run on the electricity produced from the

syngas combustion process. A complete table of operating and maintenance cost estimates for

the five potential locations is provided in Appendix E.

3.3 Annual Benefits

The Thornhill facility is designed to incur revenue from heat, and bulk and bagged biochar. A

revenue scenario was analyzed based on conservative parameters that included selling heat for

30% lower than the current average natural gas rate (~$14 per GJ natural gas is the average price

for all rate cases) at $11.44 per GJ, a discount rate of 5%, capital and operating costs inflated by

30%, and revenue incurred from 60% of the total annual biochar production.

Due to the minimal amount of farmland in central BC that could potentially secure a bulk

biochar market, the ratio of bioproduct sales was set to 40% bulk and 60% bagged. This ratio also

reflects the global biochar market where the majority of biochar sales (>90%) is attributed to

high-end niche markets like bagged soil amendment with the remainder sold for remediation

and agricultural purposes (Jirka, 2014). Briquettes were omitted from this scenario due to their

Page | 20

mediocre average retail price as well as to avoid manufacturing costs of a briquetting machine

and binding agent.

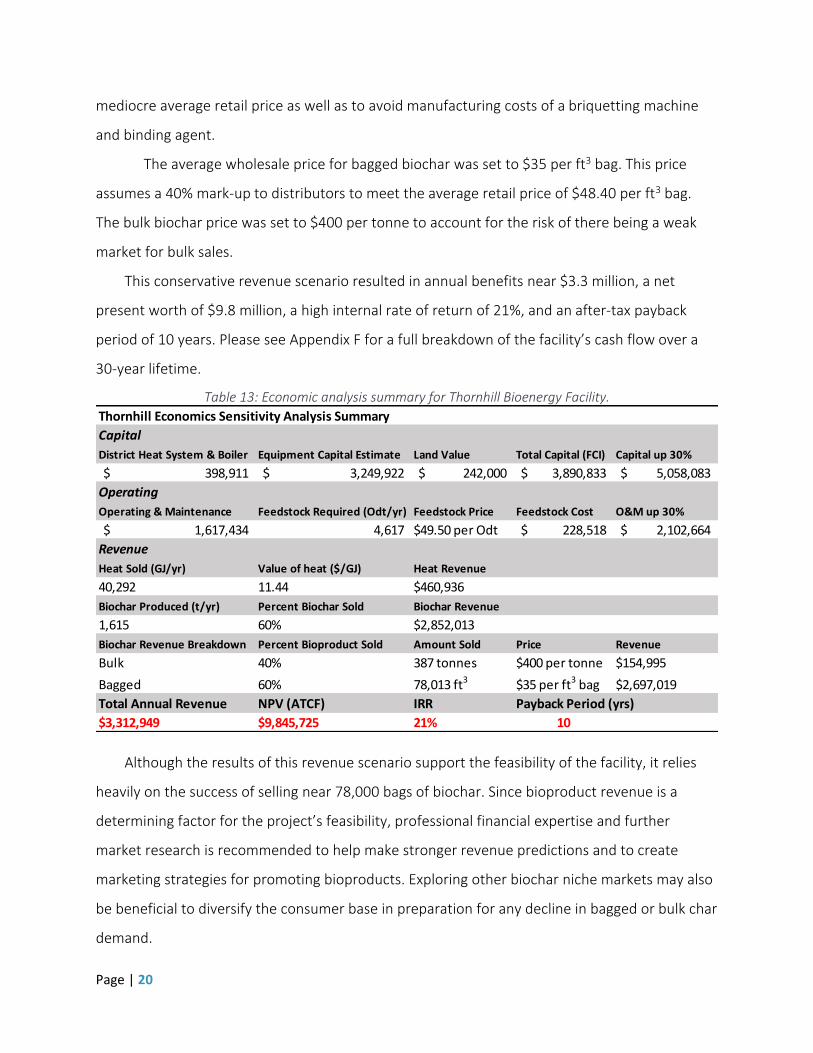

The average wholesale price for bagged biochar was set to $35 per ft3 bag. This price

assumes a 40% mark-up to distributors to meet the average retail price of $48.40 per ft3 bag.

The bulk biochar price was set to $400 per tonne to account for the risk of there being a weak

market for bulk sales.

This conservative revenue scenario resulted in annual benefits near $3.3 million, a net

present worth of $9.8 million, a high internal rate of return of 21%, and an after-tax payback

period of 10 years. Please see Appendix F for a full breakdown of the facility’s cash flow over a

30-year lifetime.

Table 13: Economic analysis summary for Thornhill Bioenergy Facility.

Although the results of this revenue scenario support the feasibility of the facility, it relies

heavily on the success of selling near 78,000 bags of biochar. Since bioproduct revenue is a

determining factor for the project’s feasibility, professional financial expertise and further

market research is recommended to help make stronger revenue predictions and to create

marketing strategies for promoting bioproducts. Exploring other biochar niche markets may also

be beneficial to diversify the consumer base in preparation for any decline in bagged or bulk char

demand.

Thornhill Economics Sensitivity Analysis Summary

Capital

District Heat System & Boiler Equipment Capital Estimate Land Value Total Capital (FCI) Capital up 30%

398,911$ 3,249,922$ 242,000$ 3,890,833$ 5,058,083$

Operating

Operating & Maintenance Feedstock Required (Odt/yr) Feedstock Price Feedstock Cost O&M up 30%

1,617,434$ 4,617 $49.50 per Odt 228,518$ 2,102,664$

Revenue

Heat Sold (GJ/yr) Value of heat ($/GJ) Heat Revenue

40,292 11.44 $460,936

Biochar Produced (t/yr) Percent Biochar Sold Biochar Revenue

1,615 60% $2,852,013

Biochar Revenue Breakdown Percent Bioproduct Sold Amount Sold Price Revenue

Bulk 40% 387 tonnes $400 per tonne $154,995

Bagged 60% 78,013 ft3 $35 per ft3 bag $2,697,019

Total Annual Revenue NPV (ATCF) IRR Payback Period (yrs)

$3,312,949 $9,845,725 21% 10

Page | 21

3.4 Revenue Sensitivity

To demonstrate how sensitive revenue is with regards to product pricing, the following chart

presents the wholesale price options required to break-even. These options depend on the ratio

of bulk to bag products sold and reflect the conservative revenue scenario, as previously

detailed. The bulk price can be driven down by selling a greater percentage of bagged product

and by increasing the bagged wholesale price.

Figure 5: Revenue sensitivity for bagged and bulk biochar prices at 60% total production sold.

The most critical responses to the net present value resulted from changes to the total

percent of biochar sold, followed by the price of the bags, and the percentage sold by bag.

Adjusting these factors by 10% lead to a change in the NPV of 30% or greater (Table 14). The

price of bulk biochar had a small effect relative to others, with just a 2.1% change in the NPV

from a 10% change in the bulk price. This is due to the bulk price being significantly lower than

the bagged price on a per tonne basis ($4640/tonne at $34.57 per ft3 bag, as compared to

$400/tonne bulk).

Table 14: NPV sensitivity to changing factors.

Factor NPV Response to 10%

Change in Factor

% Sold 39.2%

Price Bags 37.1%

% Bagged 33.9%

Price Bulk 2.1%

Page | 22

The total amount and form in which biochar is sold are key factors affecting the overall

NPV. An indicator of the price required to break even is simply the bulk price required to sell all

the char in bulk form. This number can also be viewed as the average price required to break

even given a certain percentage of the total biochar being sold, as illustrated in Figure 5. At 60%

sold, the average price rises to $2190 per tonne and increases as the percentage sold decreases.

Figure 6: Price sensitivity based on the amount of produced biochar that is effectively sold.

Further to the above sensitivity analysis, a Monte Carlo simulation computed a 50% chance

for the net present value of the Thornhill bioenergy facility to be $552,000. The simulation is

based on six parameters that are varied within a range of low, medium, and high values to

determine the most probable NPV. Revenue is based on a conservative bulk biochar price range,

and the capital and operating costs are varied by 30% from their original values. This simulation

indicates the project is a worthwhile investment due to a positive NPV at the 50th percentile.

Table 15: Parameter ranges for Monte Carlo simulation.

Page | 23

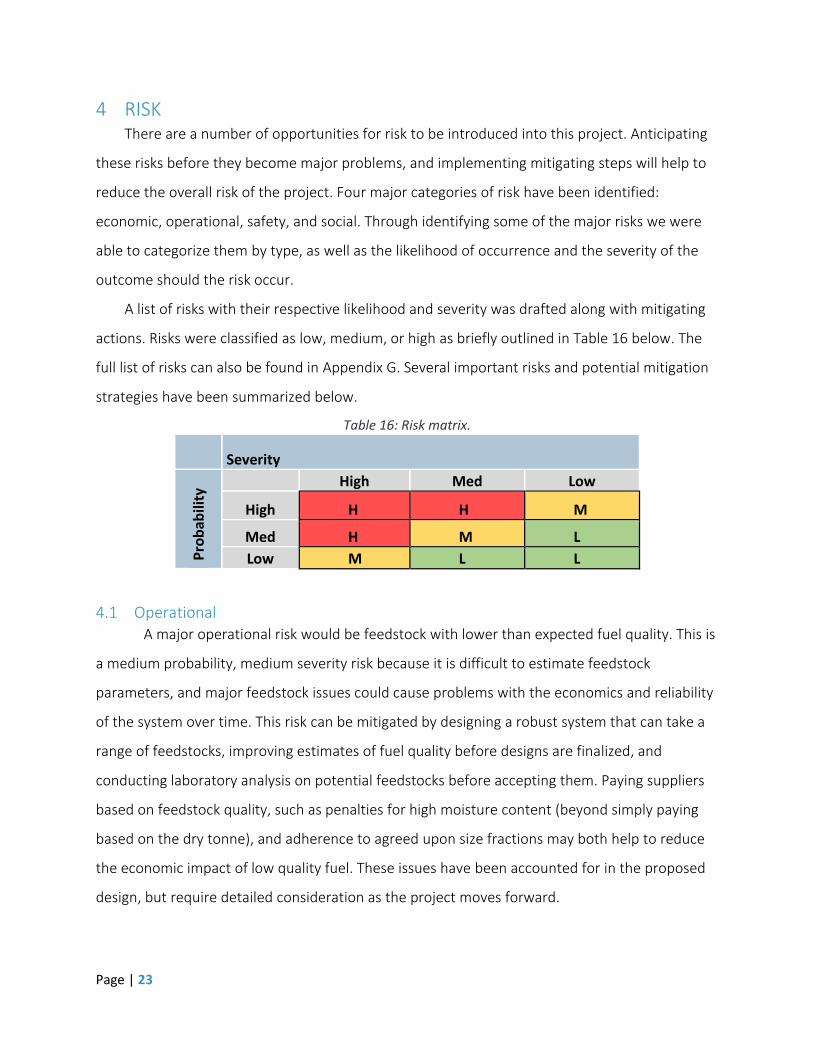

4 RISK There are a number of opportunities for risk to be introduced into this project. Anticipating

these risks before they become major problems, and implementing mitigating steps will help to

reduce the overall risk of the project. Four major categories of risk have been identified:

economic, operational, safety, and social. Through identifying some of the major risks we were

able to categorize them by type, as well as the likelihood of occurrence and the severity of the

outcome should the risk occur.

A list of risks with their respective likelihood and severity was drafted along with mitigating

actions. Risks were classified as low, medium, or high as briefly outlined in Table 16 below. The

full list of risks can also be found in Appendix G. Several important risks and potential mitigation

strategies have been summarized below.

Table 16: Risk matrix.

Severity

Pro

bab

ility

High Med Low

High H H M

Med H M L

Low M L L

4.1 Operational A major operational risk would be feedstock with lower than expected fuel quality. This is

a medium probability, medium severity risk because it is difficult to estimate feedstock

parameters, and major feedstock issues could cause problems with the economics and reliability

of the system over time. This risk can be mitigated by designing a robust system that can take a

range of feedstocks, improving estimates of fuel quality before designs are finalized, and

conducting laboratory analysis on potential feedstocks before accepting them. Paying suppliers

based on feedstock quality, such as penalties for high moisture content (beyond simply paying

based on the dry tonne), and adherence to agreed upon size fractions may both help to reduce

the economic impact of low quality fuel. These issues have been accounted for in the proposed

design, but require detailed consideration as the project moves forward.

Page | 24

4.2 Safety

The highest safety risk would be a major fire or explosion in the process. This occurrence

has a low probability and a high severity, leading to an overall medium rating on the risk matrix.

The probability can be reduced by strictly following a maintenance and inspection plan, using

high quality components, and having adequate monitoring and process control systems. In terms

of response to such an incident, an effective emergency response plan, staff training, and regular

emergency response drills would all help reduce the harm of such an incident.

4.3 Social

The social risk would entail public opposition to the project. This is a medium probability and

a medium severity event, because the public typically takes interest in local projects, and any

pushback or protests could slow down or halt the project. This could be caused by residents and

businesses having concerns over health and safety, most likely concerns over trucking, air quality

and safety. Mitigation strategies would include consulting with the public and having public

information sessions. It would be important to address any safety and air quality concerns while

explaining the environmental and economic benefits of such a system.

5 SUSTAINABILITY ASSESSMENT This sustainability assessment evaluates the potential significant adverse impacts that may

occur during the lifetime of this project with regards to: environment, economy, society, and

health. The following integrated approach accounts for the cumulative effects defined under the

Canadian Environmental Assessment Agency (CEAA) stating, “changes to the environment that

are caused by an action in combination with other past, present and future human activities.”

(CEA, 2016). Discussions of these potential effects on the community and the interests of First

Nation’s accounts for the practical means to prevent or reduce to an acceptable standard.

The project area lies within the asserted traditional territory of the Tsimshian First Nation.

Discussions regarding the project’s potential impacts to the Tsimshian First Nation’s asserted

aboriginal rights and title claims require initiation and continual consultation as the design

process moves forward.

The general provisions for the assessment procedures shall include the staging of the

assessment process and notice to the public. The assessment process institutes a pre-application

Page | 25

stage that engages in public consultation, first nation consultation, government agency

consultation, applications of terms of reference, and establishes a working group. Assessment

procedures includes the application review stage for the preparation and submission of the

application. Inclusion of the public consultation assessment, First Nations consultation

assessment, public consultation, First Nation consultation, and government agency consultation

processes is a requirement.

The environmental and socio-economic assessment approach studies the following aspects:

▪ Potential environment interactions;

▪ Estimation of releases to the environment;

▪ Potential for and magnitude of significant effects on the environment;

▪ Recommendations for assessment follow-up and monitoring.

Assessing the potential environmental interactions included: determining issues of concern;

evaluating environmental and socio-economic aspects to determine Valued Ecosystem

Components (VECs); sources and pathways of effects that may impact VECs; determining the

spatial and temporal boundaries for each VEC (FEED, 2013).

“For the purpose of environmental assessment in BC, Valued Components (VECs) are

components of the natural and human environment that are considered by the proponent,

public, Aboriginal groups, scientists and other technical specialists, and government agencies

involved in the assessment process to have specific, ecological, economic, social, cultural,

archaeological, historical, or other importance. (EAO, 2013)”

Scoping of the environmental assessment is conducted in order to compile and analyze the

available information to identify the potential environmental, economic, social, heritage, and

health issues. The regional values held by the public, Aboriginal groups, and other stakeholders

in the region may create project-specific issues. Other issues of concern may be reflected to the

scientific community and government.

A detailed environmental assessment does not account for interactions of feedstock harvesting

(FEED, 5.1). Table 17 addresses potential interactions associated with the site and forest

feedstock harvesting.

Page | 26

Table 17: Valued Ecosystem Components (VECs) and potential effects on the environment.

5.1 Policy & Regulations Decisions by the Provincial, Federal, and First Nation governments and regulatory

approvals is a requirement prior to any activities materializing from this feasibility study.

Required assessment by the according regulatory boards include regulations under the

Environmental Assessment Act, Environmental Management Act, Waste Discharge Regulations,

Canadian Council of Ministers of the Environment, and any other policies or standards in place.

In 2008, the Regional District of Kitimat-Stikine joined a province-wide action on climate

change to reduce greenhouse gases (GHGs) by signing on to the BC Climate Action Charter. The

Climate Action Charter requires communities to commit to becoming carbon neutral in its

operations, measuring and reporting on their community’s GHGs and striving for a compact,

more energy efficient community (OCP, 2017). Under the Greenhouse Gas Reduction Target Act

(2007), a province-wide target has been set to reduce GHG emissions by 33% from 2007 levels

by 2020. The City of Terrace has set GHG reduction targets of 11% below 2007 levels by 2020,

and 80% below 2007 by 2050. Despite Thornhill being an unincorporated settlement, it has

similar plans for emission targets as the City of Terrace. This bioenergy facility will support the

Thornhill’s commitment to becoming carbon neutral as it will implement an energy-efficient

renewable technology into the community.

5.2 Assessment of Potential Impacts

Potential impacts are identified and assessed based on their impact level. The

identification and selection of Valued Ecosystem Components (VECs) and their potential effects

is based on guidelines recommended by the Environmental Assessment Office (EAO) and as

required by BC’s Environmental Assessment Act. The process intention is for proponents and the

EAO staff to improve clarity, consistency, and quality of the Environmental Assessment

Page | 27

Certificate Application. Only impacts that will need supplementary assessment are discussed

further.

5.2.1 Groundwater & Freshwater Resources

Groundwater is considered a VEC as it is a source for potable, commercial, and industrial

water in the community of Thornhill; therefore, a careful assessment is required to eliminate the

potential for contamination of groundwater drinking water sources. Freshwater resources act as

watercourses and provide habitats for fish and aquatic species; this VEC indicates the overall

health of the freshwater ecosystem. Activities from the bioenergy plant are not expected to

significantly impact the freshwater environment, however, regulatory standards and policies

must be applied to both groundwater and freshwater resources, and mitigation measures must

be taken to minimize significant environmental impacts.

5.2.2 Human Health & Wellbeing

Plant operations must be conducted in a manner that minimizes health and safety risks to

the staff and public. It is the responsibility of the operating company to implement occupational

health and safety policies that comply to all required regulations. This includes training with

ongoing reviewal, inspection, and periodic audits to ensure safe practices and to identify areas of

improvement and development. A proper emergency response plan shall be established in the

case of unplanned events to ensure the safety of the workers. These protocols and regulations

shall be in place prior to the commissioning of the facility. It is essential that the facility does not

possess any components having the potential for accidents or failure.

5.2.3 Land Use & Infrastructure

Thornhill’s Official Community Plan provides an organizational layout to meet land use

objectives and policies. Included in the strategy is an establishment of the development permit

areas and guidelines. The development for commercial and industrial areas is required to be in

accordance with the Local Government Act s.488 1(1)(f) (OCP, 2017). The justification for this is

to assure that commercial development along Highway 16 is protected and is aesthetically

pleasing to residents and businesses. The proposed site is within the commercial and industrial

zoning regulations see Appendix H.

Page | 28

5.2.4 Transportation

Traffic affiliated with this project during the construction and operation will have minimal

interaction and environmental effects. During the construction phase, materials and supplies will

be transported to and from the site. The daily operations of the facility will involve the

transportation of feedstock to the site and shipments of biochar products from the site.

Compliance with the Ministry of Transportation and Infrastructure and the specific Acts and

Regulations in place for commercial vehicle safety and enforcement will be in place. Such acts

and regulations are the Motor Vehicle Act, Highway Act, and Commercial Transport Act. The

traffic being limited to several truckloads during the construction and operations will not

compromise the existing infrastructure and will be manageable. Despite the minimal waste

associated with construction and operation of the facility, any disposal of waste will be

transported to the Thornhill Transfer Station. Road transportation impacts will be inconsiderable

since existing infrastructure will be utilized, and the volume of traffic will not compromise the

efficiency or safety of current road networks.

5.2.5 Labour & Economy

The facility is expected to boost the local job economy from activities and works affiliated

in all stages of the project. The Regional District of Kitimat-Stikine’s interest in economic growth

will be stimulated from job creation and business expenditure from this project. Employment in

BC is regulated by the Employment Standards Act and will be adhered to. The construction phase

will require local labourers and contractors during the entire construction period. Facility

operations will offer long-term annual employment as well as short-term seasonal opportunities.

At the end of the plant’s lifetime, decommissioning will also present job opportunities. Overall,

this facility will have positive impacts on the economic development of the local economy from

increased employment and business expenditure.

5.2.6 Atmospheric Environment

The atmospheric environment is determined to be a VEC since the atmosphere acts as a

pathway for airborne contaminants. Receptors of such air contaminants include humans,

wildlife, vegetation, and the built environment (FEED, 2013). Noise pollution from operations is

Page | 29

dependent on the site’s proximity to residences and the design envelope, therefore, it is

recommended to conduct further analysis utilizing vendor information and sound surveys at the

proposed site location. The feedstock preparation operation may cause additional noise issues if

it is conducted on site.

5.3 Emissions Greenhouse gas emissions are a major concern with any future development due to their

strong correlation to climate change. A global initiative to reduce GHGs imposes the

responsibility for this project to ensure a minimal release of emissions. The project will need to

undergo a formal environmental assessment as required by criteria under federal and provincial

legislation, and appropriate measurements must be taken to ensure that guidelines for air

quality and GHG emissions are complied with as required by regulatory bodies such as the CEAA.

A further assessment on emissions dispersion is recommended for estimating ground level

concentrations of contaminants.

GHG emissions data is based on current conditions from Environment and Climate Change

Canada, the Province of BC, the Environmental Protection Agency (EPA), the Canadian

Environmental Protection Act, the Environmental Assessment Act, and Canada-Wide Standards.

The following sections address the current GHG emission guidelines and regulations and

background on potential construction and operation emissions followed by a detailed CO2

emission data from the combustion process.

5.3.1 Greenhouse Gas Emission Guidelines and Protocols

A general guidance for emission regulations and guidelines is addressed in this section to

provide an outline of Greenhouse Gas (GHG) protocol on a national and global scale. The United

Nations Framework Convention on Climate Change (UNFCCC) requires reporting guidelines

placing special consideration on reporting CO2 emissions from the combustion of biomass, in

which the ECCC is responsible for developing and reporting. Reporters to GHGRP are required to

report CO2 emissions from biomass combustion under the guidelines of the UNFCCC. These

guidelines incorporate the Intergovernmental Panel on Climate Change (IPCC) estimations on

GHGs. The 2006 IPCC Guidelines for National Greenhouse Gas Inventories (IPCC, 2006) is the

Page | 30

method utilized to estimate GHG emissions at a facility level. Additional regulations to biomass

combustion under IPCC Guidelines facilities requires the reporting and counting of CH4 and N2O

emissions. The 2006 IPCC Guidelines estimates carbon emissions in terms of the species which

are emitted. (IPCC 2016). The combustion process mostly releases carbon as CO2. A percentage

of the emissions will consist of carbon monoxide (CO), methane (CH4), or non-methane volatile

organic compounds (NMVOCs).

The IPCC provides default emission factors for CO2 that are applicable to all combustion

processes as CO2 emissions are independent of combustion technology, however CH4 and N2O

emissions have a strong correlation with technology. Because of this variability an averaged

emission factor is used, placing a level of uncertainty in the data (WRI/WBCSD, 2005)

Federal and provincial governments place regulatory requirements on the environmental effects

on the atmosphere. Air quality in B.C. is managed through several bodies that regulate air quality

through airshed management programs, Air Quality Management System (AQMS), and the

principle legislations, Environmental Management Act and Waste Discharge Regulation.

Under the airshed management program, BC has an obligation of communities to have airshed

plans that meet a Canada-wide Standards for Particulate Matter and Ozone.

5.3.2 Construction

Air quality during construction should be restricted to fugitive dust emissions during

ground preparation (FEED, 2013). Since the plant will be relatively small in scale, air

contaminants released from construction practices will be marginal, and few to none emissions

from heavy construction equipment on the site will occur, including fugitive dust. Air pollution

from the transportation of materials is expected to be insignificant and restricted to the site.

No consideration for emissions in the construction of forestry roads for harvesting

practices needs to be addressed since this feasibility study is based on feedstock sourced from

the waste of existing sawmills.

Page | 31

5.3.3 Operations

The facility will generate air emissions in the form of GHGs and particulate matter from

the combustion of woody biomass and syngas. Emission estimations reflect a 1.4 MW system to

assess emission rates for each contaminant and are based on an existing system, the Community

Power Corporation technology, researched by the Haines Junction Biomass Energy Project

(HJBEP). Similar to HJBEP, a direct scaling approach is used to size the Thornhill scenario. GHG

analysis is based on a calculation based method using fuel consumption data.

The release of other hazardous contaminants (volatile organic compounds, polycyclic

aromatic hydrocarbons, dioxins, and furans), is determined to be small and in similar nature to

other biomass combustion processes. Concerns for methane and nitrogen dioxide from facility

operations should be insignificant, therefore their evaluation is unnecessary.

Environment Canada has reporting requirements in place for emissions of GHGs which

support the annual mandatory reporting of GHG emissions by facilities under Environment and

Climate Change Canada’s (ECCC) Greenhouse Gas Emissions Reporting Program (GHGRP). Under

these regulations, a regulatory standard of 50,000 tonnes or more of GHGs annually must be

reported. The current plant will be well below this emission rate, therefore GHG emissions

reporting is not mandatory. Calculated carbon dioxide equivalents (CO2e) from the proposed

plant using sawmill waste is reported below in Tables 18 and 19.

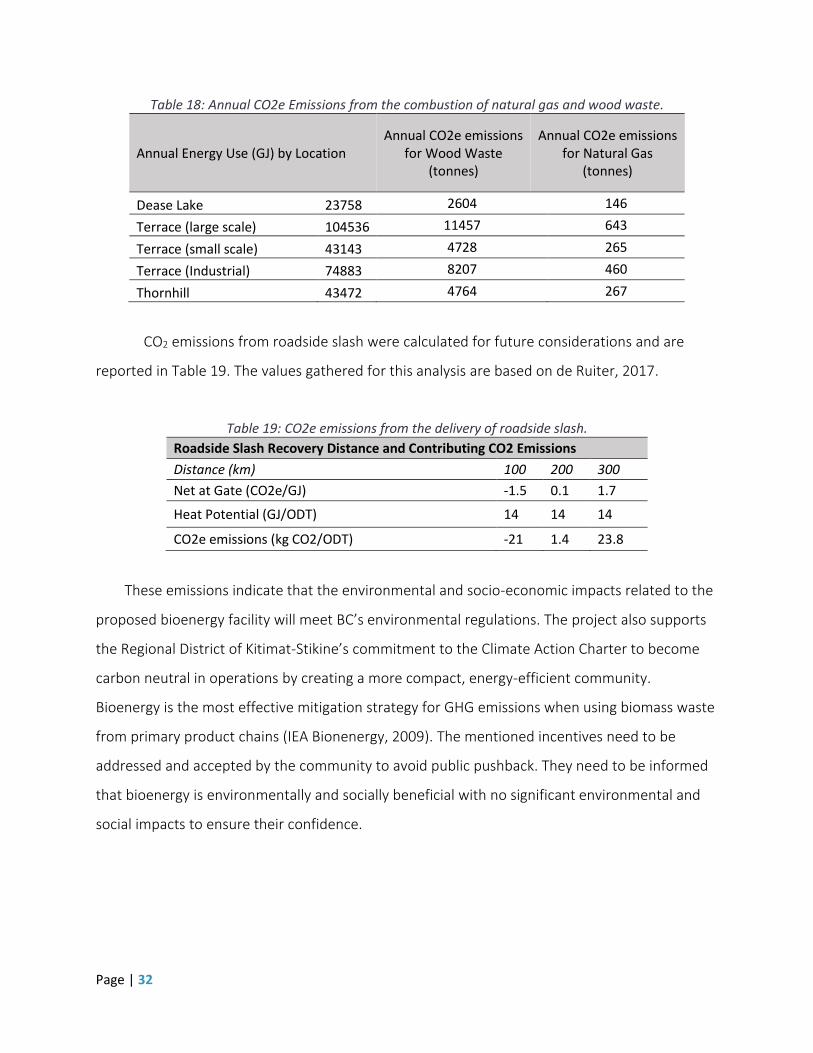

5.3.4 CO2 Emissions

The annual CO2e emissions for natural gas and wood waste for each scenario are

provided in Table 18. The emission values for the fuels only account for the combustion of the

fuel. Pre-processing, transportation, and any additional processes are not accounted for and are

considered minimal and insignificant. The values of 109.6 kgCO2/GJ for wood and 56.1 kgCO2/GJ

for natural gas are based on statistics provided by Fachbuch Regenerative Energie Systeme and

UBA.

Page | 32

Table 18: Annual CO2e Emissions from the combustion of natural gas and wood waste.

Annual Energy Use (GJ) by Location Annual CO2e emissions

for Wood Waste (tonnes)

Annual CO2e emissions for Natural Gas

(tonnes)

Dease Lake 23758 2604 146

Terrace (large scale) 104536 11457 643

Terrace (small scale) 43143 4728 265

Terrace (Industrial) 74883 8207 460

Thornhill 43472 4764 267

CO2 emissions from roadside slash were calculated for future considerations and are

reported in Table 19. The values gathered for this analysis are based on de Ruiter, 2017.

Table 19: CO2e emissions from the delivery of roadside slash.

Roadside Slash Recovery Distance and Contributing CO2 Emissions

Distance (km) 100 200 300

Net at Gate (CO2e/GJ) -1.5 0.1 1.7

Heat Potential (GJ/ODT) 14 14 14

CO2e emissions (kg CO2/ODT) -21 1.4 23.8

These emissions indicate that the environmental and socio-economic impacts related to the

proposed bioenergy facility will meet BC’s environmental regulations. The project also supports

the Regional District of Kitimat-Stikine’s commitment to the Climate Action Charter to become

carbon neutral in operations by creating a more compact, energy-efficient community.

Bioenergy is the most effective mitigation strategy for GHG emissions when using biomass waste

from primary product chains (IEA Bionenergy, 2009). The mentioned incentives need to be

addressed and accepted by the community to avoid public pushback. They need to be informed

that bioenergy is environmentally and socially beneficial with no significant environmental and

social impacts to ensure their confidence.

Page | 33

6 ALTERNATIVE LOCATIONS, FEEDSTOCK & TECHNOLOGY

6.1 Diversifying Feedstock Supply The proposed bioenergy system is designed to run on sawmill residues (chips), however,

the system will be able to handle different types of biomass if it is adequately prepared. An

alternative biomass of primary interest is roadside slash, the majority of which is presently

managed by open burning onsite. In comparison to sawmill residues, one of the major hurdles to

overcome when using slash as feedstock is transportation. Chips have already been transported

to town, and this cost is factored into the cost of the chips as feedstock, whereas slash is

normally dealt with on the landing and the shipping cost is an added expense to procuring slash.

Other considerations with slash are moisture content, and particle size and

characteristics. Unless slash dried out, the moisture content will be higher than in chips and will

reduce energy yields as compared to chips. Another challenge might be maintaining a proper

orientation of branches into the chipper to avoid irregular sized feed. This could result in poor

operation of the feed supply system and the pyrolysis reactor. However; if a carbon tax is placed

on burning slash piles, the economic incentive for finding alternative uses for slash will increase,

potentially making it a more viable fuel.

It has also been proven that dewatered biosolids (produced in wastewater treatment),

manure, plastic, and demolition and construction debris can all be gasified. However, debris with

halogenated compounds, heavy metals, and other contaminants would pose a problem to our

current system. These compounds, which are heavily regulated, would come out in the biochar

or air emissions. This would likely hinder biochar sales, and require sophisticated air emissions

controls. For this reason, plastics and construction and demolition debris would not be ideal

feedstocks. Manure and biosolids could be suitable feedstocks, but would have to be processed

into suitable sized particles (BC Biocarbon accomplishes this by using a briquetting machine), and

as with slash, the high water content of these fuels leads to a lower energy yield.

6.2 District Heating & Electricity Generation Opportunities