thoughtware higher education - bkd

TRANSCRIPT

4/6/2020

1

Higher Education

THOUGHTWARE®

Higher Education & the CARES Act

Tuesday, April 7, 2020

4/6/2020

2

To Receive CPE Credit

• Individuals• Participate in entire webinar• Answer polls when they are provided

• Groups• Group leader is the person who registered & logged on to the webinar• Answer polls when they are provided• Complete group attendance form • Group leader sign bottom of form• Submit group attendance form to [email protected] within 24 hours of webinar

• If all eligibility requirements are met, each participant will be emailed their CPE certificate within 15 business days of webinar

Today’s Presenters

Adam W. Smith, [email protected]

Kevin Ensminger, [email protected]

4/6/2020

3

• CARES Education Stabilization Fund & Higher Education Emergency Relief Fund

• Overview• Challenges, Issues & Questions

• Institutional Refunds & Related Considerations

• CARES & Title IV Compliance

• Other Developments in Play

• Tax Day Postponed

• Families First Coronavirus Response Act

• CARES Act – Tax Perspective

Agenda

CARES Education Stabilization

4/6/2020

4

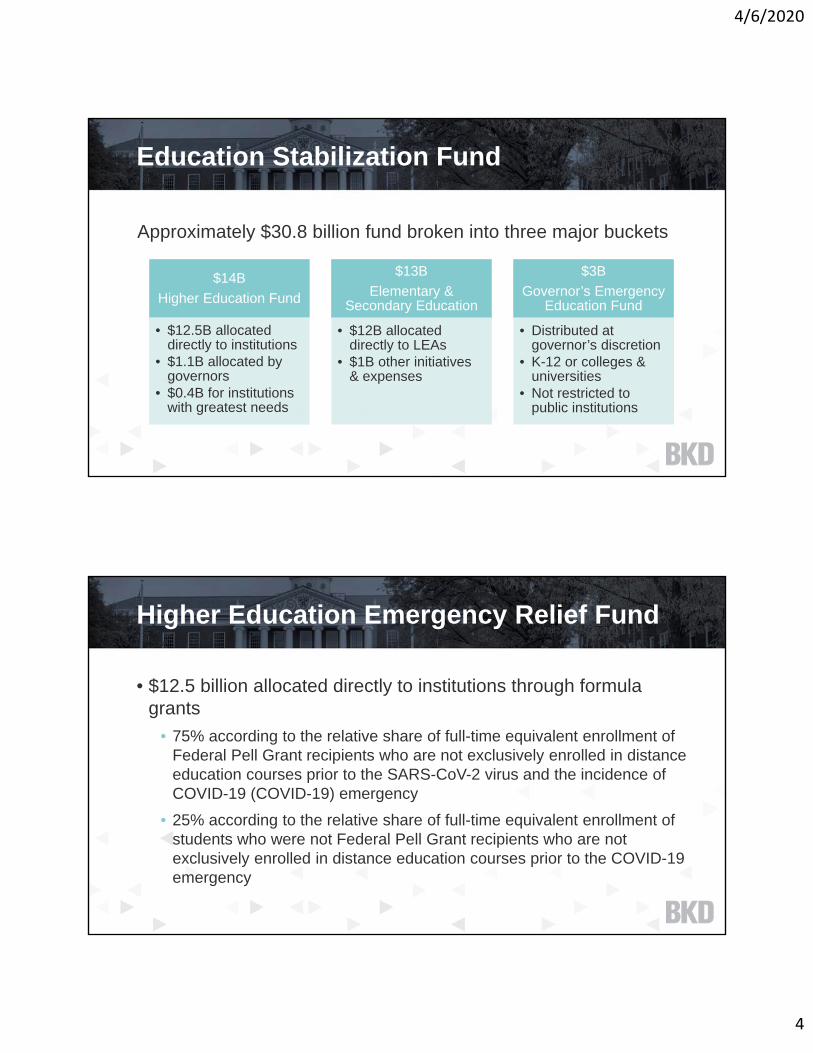

Education Stabilization Fund

Approximately $30.8 billion fund broken into three major buckets

$14B Higher Education Fund

• $12.5B allocated directly to institutions

• $1.1B allocated by governors

• $0.4B for institutions with greatest needs

$13BElementary &

Secondary Education

• $12B allocated directly to LEAs

• $1B other initiatives & expenses

$3BGovernor’s Emergency

Education Fund

• Distributed at governor’s discretion

• K-12 or colleges & universities

• Not restricted to public institutions

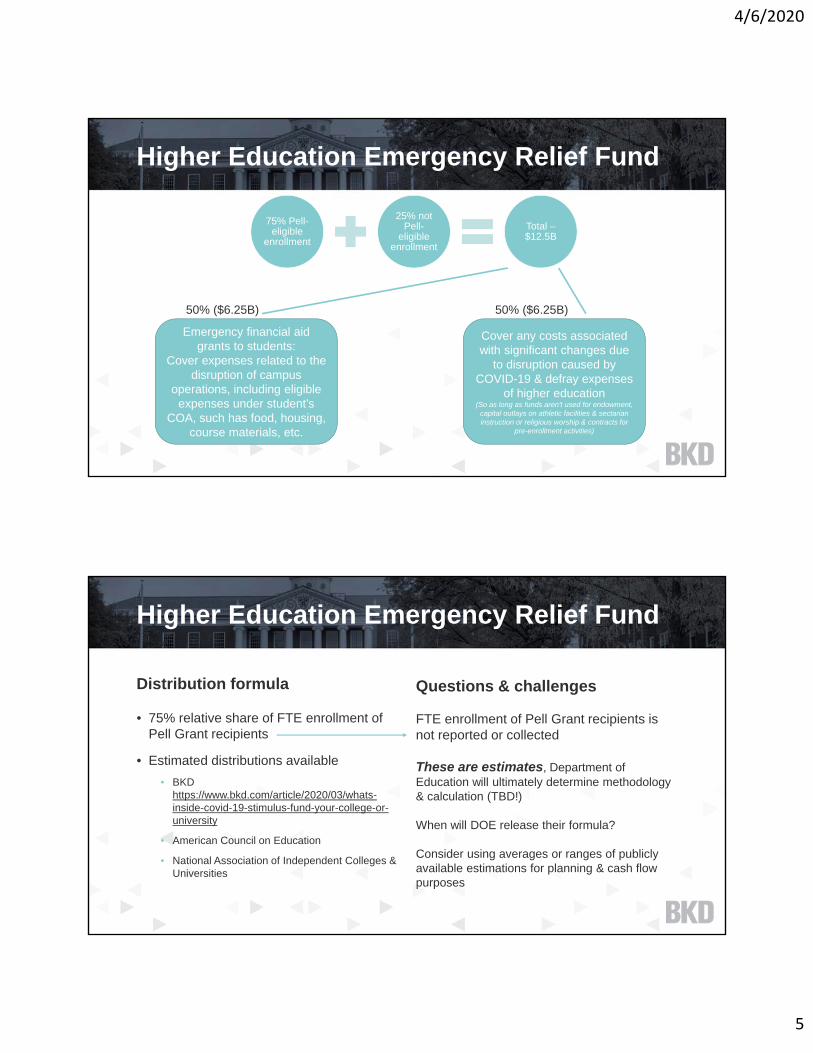

Higher Education Emergency Relief Fund

• $12.5 billion allocated directly to institutions through formula grants

• 75% according to the relative share of full-time equivalent enrollment of Federal Pell Grant recipients who are not exclusively enrolled in distance education courses prior to the SARS-CoV-2 virus and the incidence of COVID-19 (COVID-19) emergency

• 25% according to the relative share of full-time equivalent enrollment of students who were not Federal Pell Grant recipients who are not exclusively enrolled in distance education courses prior to the COVID-19 emergency

4/6/2020

5

Higher Education Emergency Relief Fund

75% Pell-eligible

enrollment

25% not Pell-

eligible enrollment

Total –$12.5B

Emergency financial aid grants to students:

Cover expenses related to the disruption of campus

operations, including eligible expenses under student’s

COA, such has food, housing, course materials, etc.

Cover any costs associated with significant changes due

to disruption caused by COVID-19 & defray expenses

of higher education(So as long as funds aren’t used for endowment,

capital outlays on athletic facilities & sectarian instruction or religious worship & contracts for

pre-enrollment activities)

50% ($6.25B) 50% ($6.25B)

Higher Education Emergency Relief Fund

Distribution formula

• 75% relative share of FTE enrollment of Pell Grant recipients

• Estimated distributions available• BKD

https://www.bkd.com/article/2020/03/whats-inside-covid-19-stimulus-fund-your-college-or-university

• American Council on Education

• National Association of Independent Colleges & Universities

Questions & challenges

FTE enrollment of Pell Grant recipients is not reported or collected

These are estimates, Department of Education will ultimately determine methodology & calculation (TBD!)

When will DOE release their formula?

Consider using averages or ranges of publicly available estimations for planning & cash flow purposes

4/6/2020

6

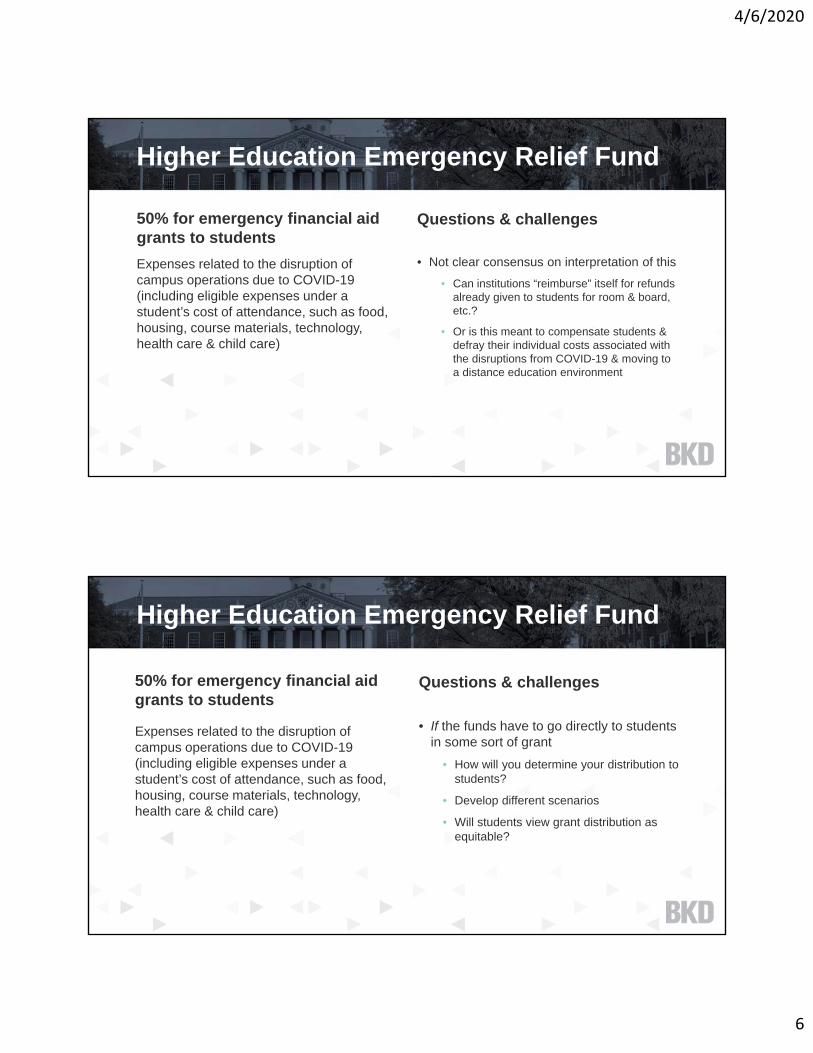

Higher Education Emergency Relief Fund

50% for emergency financial aid grants to students

Expenses related to the disruption of campus operations due to COVID-19 (including eligible expenses under a student’s cost of attendance, such as food, housing, course materials, technology, health care & child care)

Questions & challenges

• Not clear consensus on interpretation of this• Can institutions “reimburse” itself for refunds

already given to students for room & board, etc.?

• Or is this meant to compensate students & defray their individual costs associated with the disruptions from COVID-19 & moving to a distance education environment

Higher Education Emergency Relief Fund

50% for emergency financial aid grants to students

Expenses related to the disruption of campus operations due to COVID-19 (including eligible expenses under a student’s cost of attendance, such as food, housing, course materials, technology, health care & child care)

Questions & challenges

• If the funds have to go directly to students in some sort of grant

• How will you determine your distribution to students?

• Develop different scenarios

• Will students view grant distribution as equitable?

4/6/2020

7

Higher Education Emergency Relief Fund

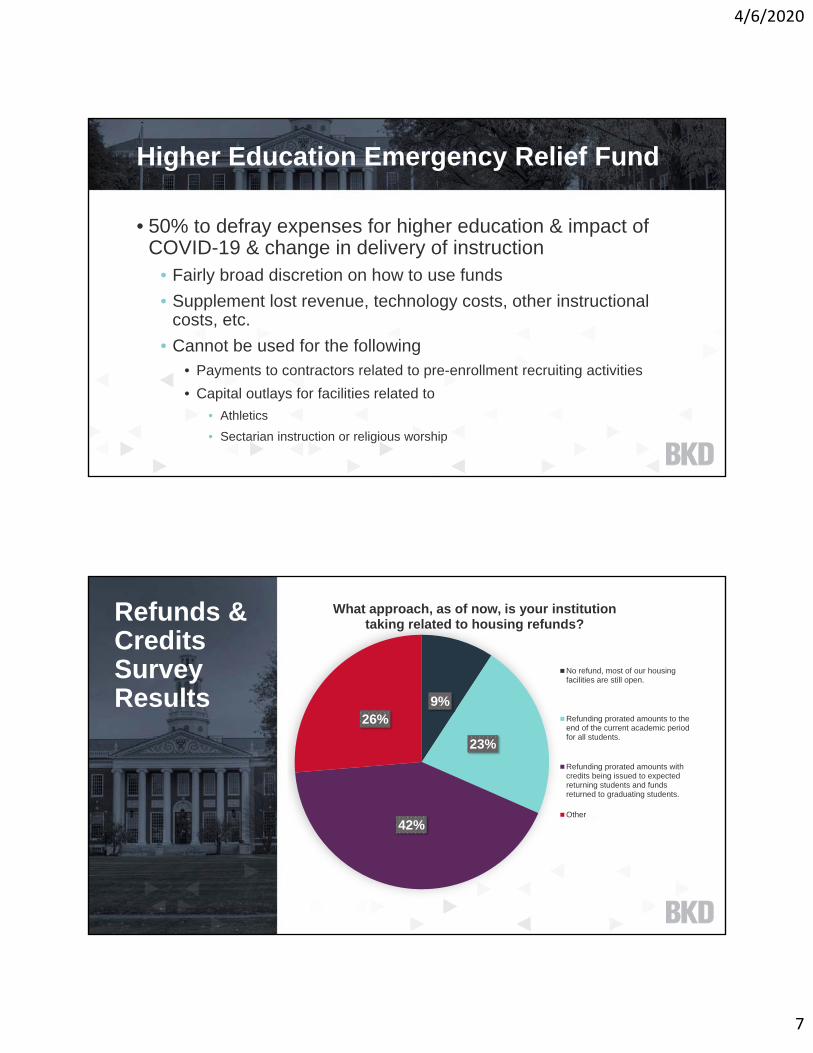

• 50% to defray expenses for higher education & impact of COVID-19 & change in delivery of instruction

• Fairly broad discretion on how to use funds• Supplement lost revenue, technology costs, other instructional

costs, etc.• Cannot be used for the following

• Payments to contractors related to pre-enrollment recruiting activities• Capital outlays for facilities related to

• Athletics• Sectarian instruction or religious worship

Refunds & Credits Survey Results 9%

23%

42%

26%

What approach, as of now, is your institution taking related to housing refunds?

No refund, most of our housingfacilities are still open.

Refunding prorated amounts to theend of the current academic periodfor all students.

Refunding prorated amounts withcredits being issued to expectedreturning students and fundsreturned to graduating students.

Other

4/6/2020

8

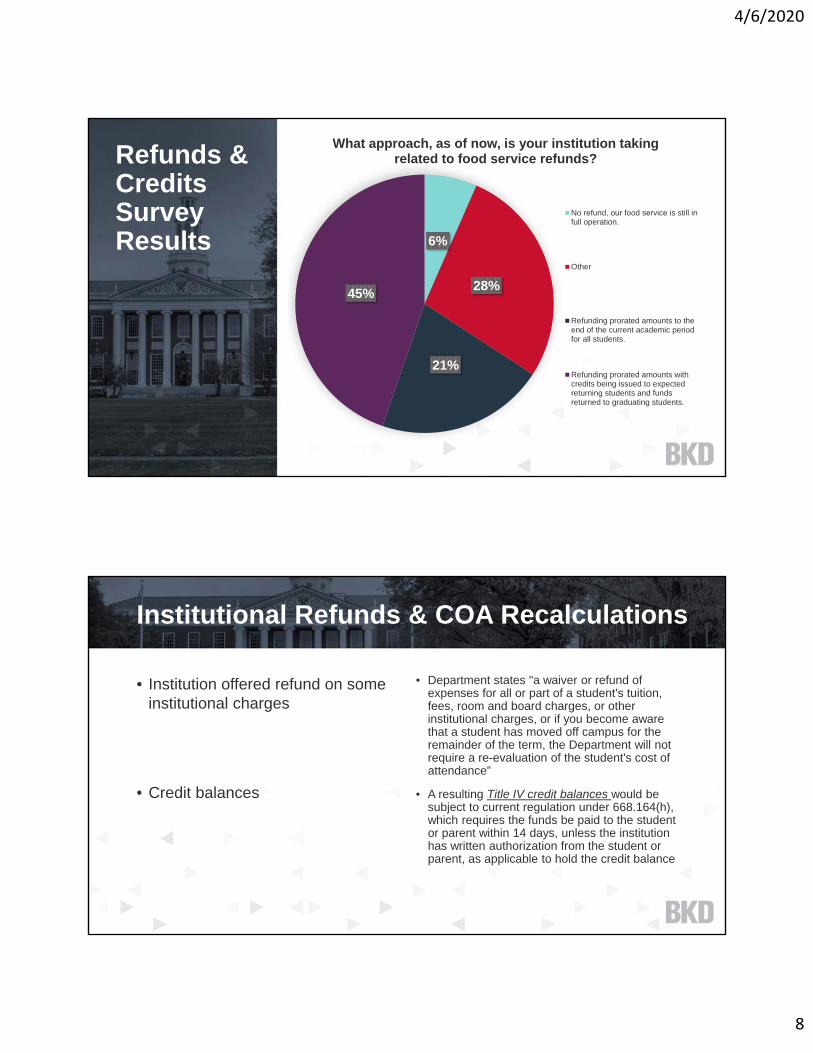

Refunds & Credits Survey Results 6%

28%

21%

45%

What approach, as of now, is your institution taking related to food service refunds?

No refund, our food service is still infull operation.

Other

Refunding prorated amounts to theend of the current academic periodfor all students.

Refunding prorated amounts withcredits being issued to expectedreturning students and fundsreturned to graduating students.

Institutional Refunds & COA Recalculations

• Institution offered refund on some institutional charges

• Credit balances

• Department states "a waiver or refund of expenses for all or part of a student's tuition, fees, room and board charges, or other institutional charges, or if you become aware that a student has moved off campus for the remainder of the term, the Department will not require a re-evaluation of the student's cost of attendance”

• A resulting Title IV credit balances would be subject to current regulation under 668.164(h), which requires the funds be paid to the student or parent within 14 days, unless the institution has written authorization from the student or parent, as applicable to hold the credit balance

4/6/2020

9

Institutional Refunds – Other Considerations

• Questions & issues• Students may be getting two “refunds/distributions” – 1) from

institution on R&B refund 2) potential student emergency grant from HE emergency fund

• Consider how those potentially intersect & impact each other

• Student & parents perception on refund amount given & credits being issued for next academic term

CARES & Title IV Compliance Considerations

4/6/2020

10

CARES & Title IV Compliance Considerations

• For not-for-profit institutions CARES waives the matching (institutional share) of campus-based aid programs (FWS & FSEOG)

• Waived for both 2019-2020 & 2020-2021 award years• Evaluate & assess the budget impact on operations

CARES & Title IV Compliance Considerations

• Return of Title IV waivers• Institutions do not need to perform R2T4 calculations & returns

for students who withdrew or dropped out as a result of COVID-19

• Student is not required to return Pell Grants or federal students loans

• Institution is still required to report information relating student & amounts that would have been returned

4/6/2020

11

CARES & Title IV Compliance Considerations

• Additional FSEOG Grants• May use FSEOG funds to award additional grants to students

affected by COVID-19 outbreak• Provide up to $6,195• Can transfer up to 100% of unused FWS funds to FSEOG to

fund this initiative• Additional grant does not count as estimated financial

assistance that would reduce

CARES & Title IV Compliance Considerations

• Lifetime limit eligibility waivers• Students who withdraw or drop out as a result of COVID-19

• Term is excluded from counting towards lifetime federal subsidized loan eligibility

• Term is excluded from counting towards lifetime federal Pell eligibility

4/6/2020

12

CARES & Title IV Compliance Considerations

• Other Title IV relief measures• Allows institutions to issue work-study payments to students who are unable to work

due to workplace closures as a lump sum or in payments similar to paychecks

• For students who dropped out of school as a result of COVID-19, the students’ grades do not affect their federal satisfactory academic progress requirements to continue to receive Pell Grants or student loans

• Authorizes the Secretary of Education to defer payments on current Historically Black Colleges and Universities (HBCU) Capital Financing loans during the national emergency period so HBCUs can devote financial resources to COVID-19 efforts

• Grant matching requirements – allows institutions to seek waivers of the matching requirements for certain grant programs

Other Developments in Play

4/6/2020

13

Other Items in Play Currently

• H.J. Res. 76 – joint resolution nullifies new Borrower Defense Rules issued on September 23, 2019, & effective July 1, 2020

• Would roll back to Obama-era BDR rules

• Is heading to President Trump’s desk

• If gets signed & no other changes, the financial responsibility rules & reporting requirements would stand as current

• New triggering events & reporting would be void

• Other advocacy actions in play• Department of Education Financial Responsibility Composite

Score Relief• Higher Education Emergency Relief Fund

• Distribute & make funds available as quickly as possible• Clarify the statutory language regarding acceptable uses of the funds,

i.e., can the emergency grants to students be used to reimburse institutions

Other Items in Play Currently

4/6/2020

14

• Standard delays & deferral of effective dates• FASB will discuss effective date deferral requests for

significant standards not yet effective at April 9 meeting• GASB announced it will consider postponing all statements &

implementations guides with effective dates that begin on or after reporting periods beginning after June 15, 2018

• OMB Single Audit extension: six month of the single audits for fiscal year-ends through June 30, 2020

Other Items in Play Currently

Tax Day Postponed (for Some)

4/6/2020

15

• April 15 tax filing & payment deadline postponed to July 15, 2020 (no interest or penalties) for all federal income tax returns & estimated tax payments

• Postponement does not apply to information returns due April 15, 2020, including Forms 990, 990-EZ & 990-PF (November 30 & May 31 FYE-exempt organizations)

• Form 990-Ts due April 15, 2020, are postponed to July 15, 2020, including any required payments

• No limit on amounts that can be deferred

• Form 990 series returns due May 15, 2020, have not been postponed

• State return postponed dates may vary – be sure to check for any returns due April 15, 2020

• IRS FAQ: https://www.irs.gov/newsroom/filing-and-payment-deadlines-questions-and-answers

Tax Day Postponed

Coronavirus Aid, Relief and Economic Security (CARES) Act

4/6/2020

16

CARES Act: Expanded EIDL & Emergency Grants

• Economic Injury Disaster Loans (SBA 7(b) Loans)• Available to small businesses & tax-exempt organizations

with fewer than 501 employees• SBA has industry-specific sizing standards – NAICS code

• Working capital loans up to $2,000,000, up to 30 years• Fixed interest rate: 3.75% for businesses, 2.75% for

nonprofits

CARES Act: Expanded EIDL & Emergency Grants

• Emergency grants through December 31, 2020• Applicant may request an advance of up to $10,000 from SBA

• To be funded within three days after SBA received application

• Applicant must self-certify they are an eligible business for EIDL

• Not required to be paid back – even if not eventually approved for EIDL

• Do not have to accept the loan

• Remain eligible for the Paycheck Protection Program (PPP) loan (will cover next), just not for the same use

• Will reduce the amount of eligible loan forgiveness under the PPP loan

• May be refinanced into the PPP loan

4/6/2020

17

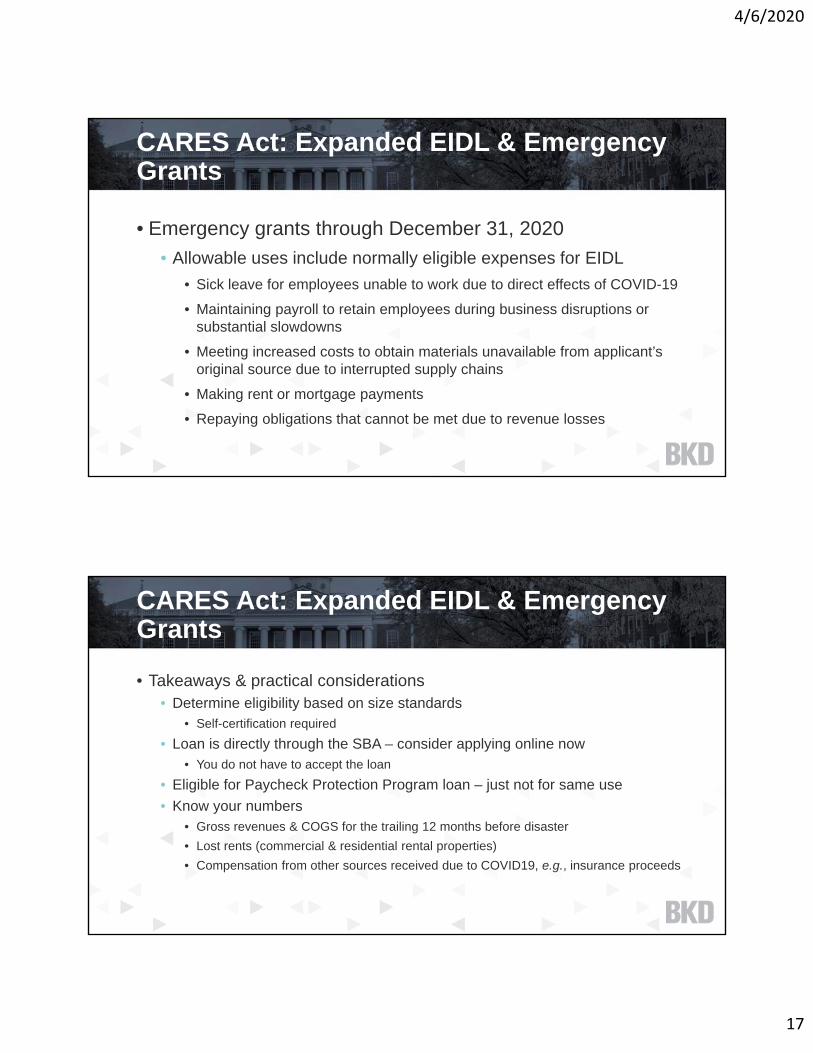

• Emergency grants through December 31, 2020• Allowable uses include normally eligible expenses for EIDL

• Sick leave for employees unable to work due to direct effects of COVID-19• Maintaining payroll to retain employees during business disruptions or

substantial slowdowns• Meeting increased costs to obtain materials unavailable from applicant’s

original source due to interrupted supply chains• Making rent or mortgage payments• Repaying obligations that cannot be met due to revenue losses

CARES Act: Expanded EIDL & Emergency Grants

• Takeaways & practical considerations• Determine eligibility based on size standards

• Self-certification required• Loan is directly through the SBA – consider applying online now

• You do not have to accept the loan• Eligible for Paycheck Protection Program loan – just not for same use• Know your numbers

• Gross revenues & COGS for the trailing 12 months before disaster • Lost rents (commercial & residential rental properties)• Compensation from other sources received due to COVID19, e.g., insurance proceeds

CARES Act: Expanded EIDL & Emergency Grants

4/6/2020

18

CARES Act: Paycheck Protection Program(PPP)

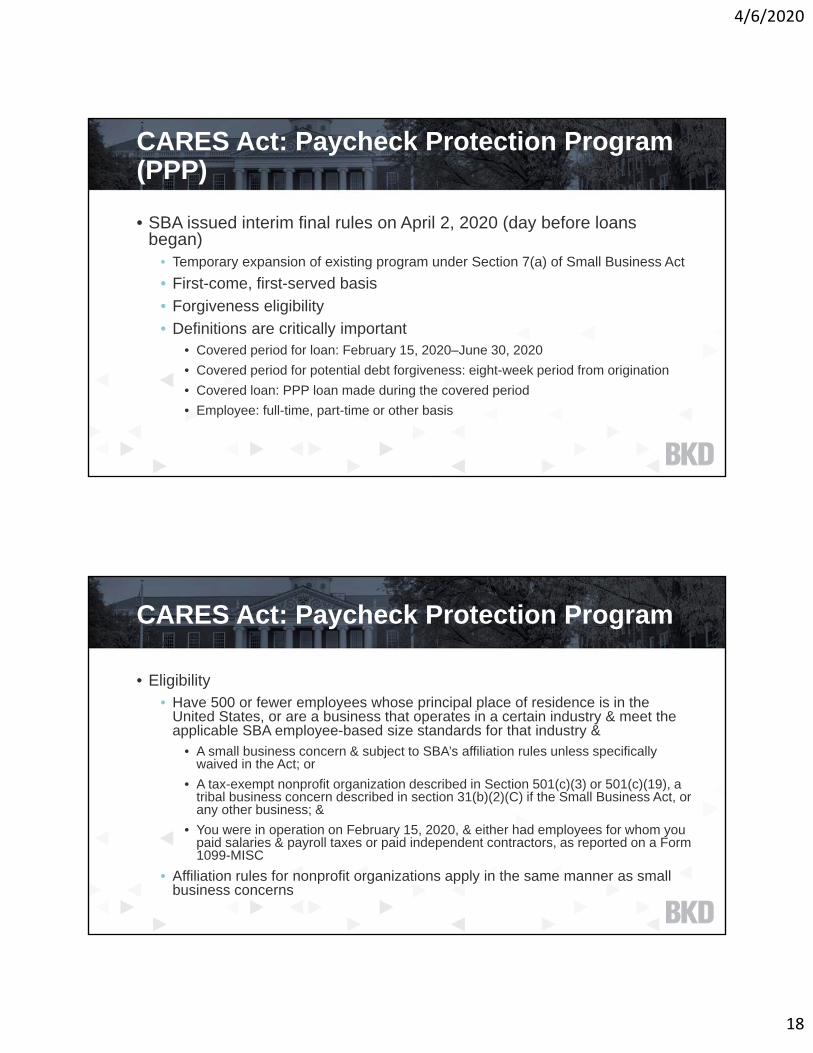

• SBA issued interim final rules on April 2, 2020 (day before loans began)

• Temporary expansion of existing program under Section 7(a) of Small Business Act• First-come, first-served basis• Forgiveness eligibility • Definitions are critically important

• Covered period for loan: February 15, 2020–June 30, 2020• Covered period for potential debt forgiveness: eight-week period from origination• Covered loan: PPP loan made during the covered period• Employee: full-time, part-time or other basis

CARES Act: Paycheck Protection Program

• Eligibility• Have 500 or fewer employees whose principal place of residence is in the

United States, or are a business that operates in a certain industry & meet the applicable SBA employee-based size standards for that industry &

• A small business concern & subject to SBA’s affiliation rules unless specifically waived in the Act; or

• A tax-exempt nonprofit organization described in Section 501(c)(3) or 501(c)(19), a tribal business concern described in section 31(b)(2)(C) if the Small Business Act, or any other business; &

• You were in operation on February 15, 2020, & either had employees for whom you paid salaries & payroll taxes or paid independent contractors, as reported on a Form 1099-MISC

• Affiliation rules for nonprofit organizations apply in the same manner as small business concerns

4/6/2020

19

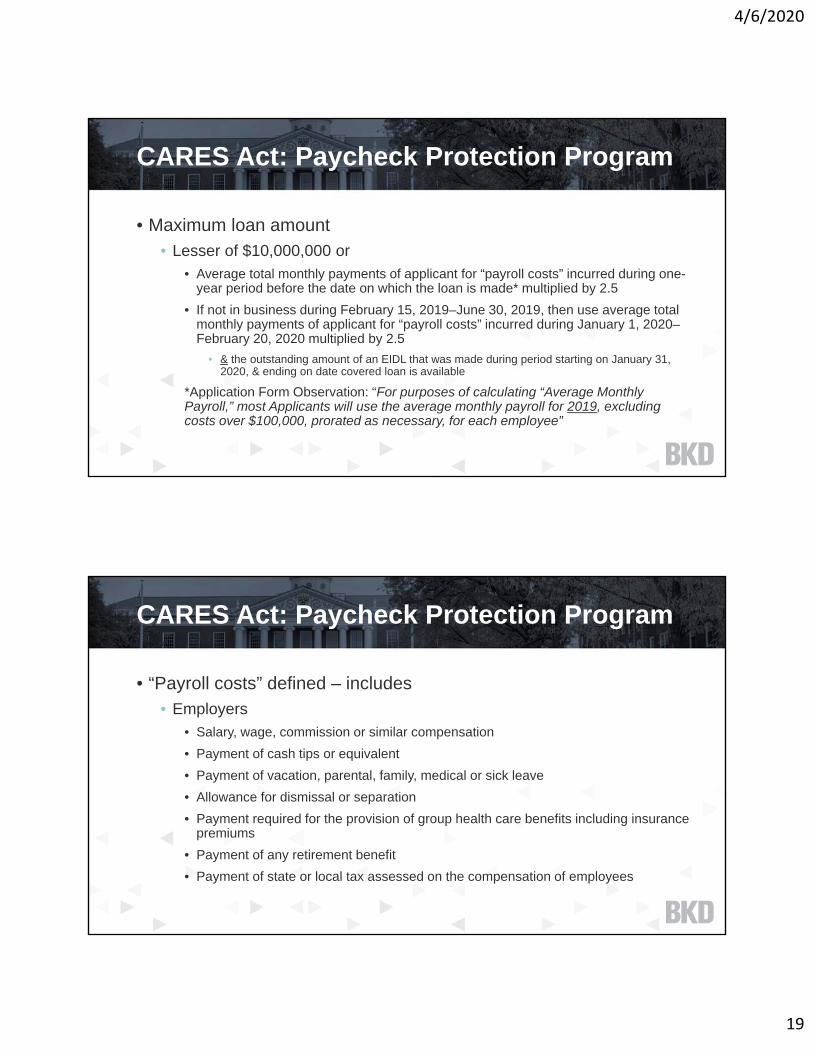

• Maximum loan amount • Lesser of $10,000,000 or

• Average total monthly payments of applicant for “payroll costs” incurred during one-year period before the date on which the loan is made* multiplied by 2.5

• If not in business during February 15, 2019–June 30, 2019, then use average total monthly payments of applicant for “payroll costs” incurred during January 1, 2020–February 20, 2020 multiplied by 2.5

• & the outstanding amount of an EIDL that was made during period starting on January 31, 2020, & ending on date covered loan is available

*Application Form Observation: “For purposes of calculating “Average Monthly Payroll,” most Applicants will use the average monthly payroll for 2019, excluding costs over $100,000, prorated as necessary, for each employee”

CARES Act: Paycheck Protection Program

• “Payroll costs” defined – includes • Employers

• Salary, wage, commission or similar compensation• Payment of cash tips or equivalent• Payment of vacation, parental, family, medical or sick leave• Allowance for dismissal or separation• Payment required for the provision of group health care benefits including insurance

premiums• Payment of any retirement benefit• Payment of state or local tax assessed on the compensation of employees

CARES Act: Paycheck Protection Program

4/6/2020

20

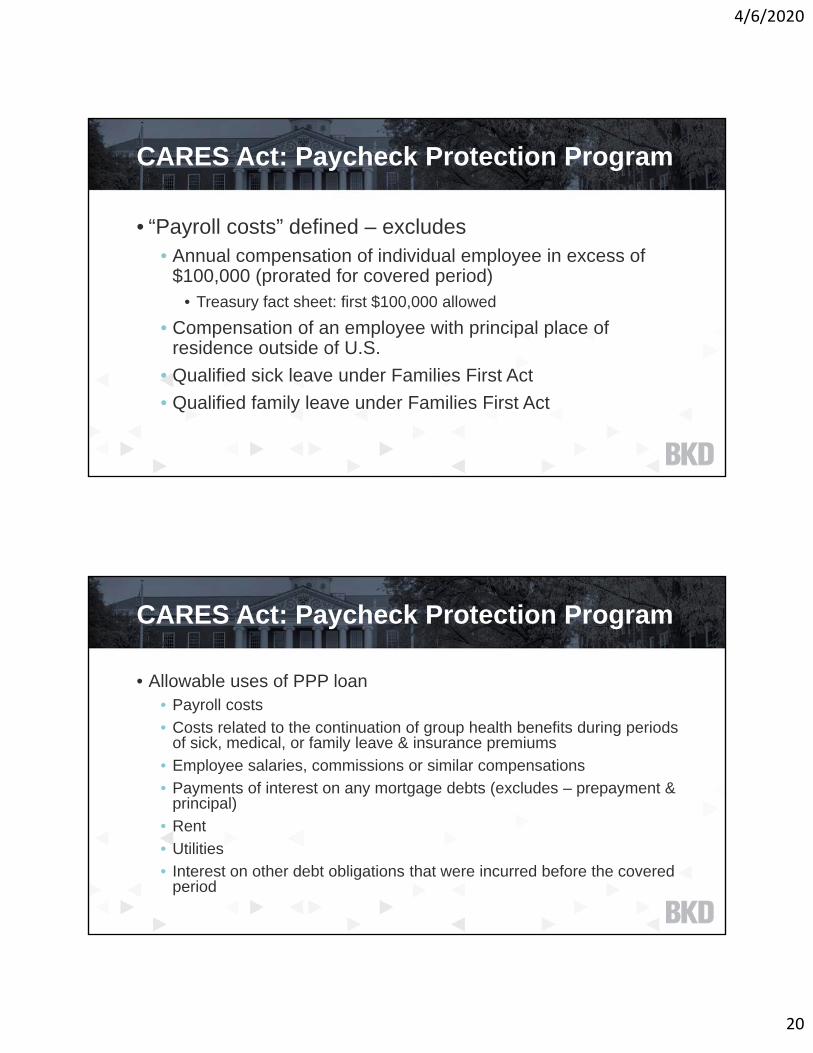

• “Payroll costs” defined – excludes• Annual compensation of individual employee in excess of

$100,000 (prorated for covered period)• Treasury fact sheet: first $100,000 allowed

• Compensation of an employee with principal place of residence outside of U.S.

• Qualified sick leave under Families First Act• Qualified family leave under Families First Act

CARES Act: Paycheck Protection Program

• Allowable uses of PPP loan• Payroll costs • Costs related to the continuation of group health benefits during periods

of sick, medical, or family leave & insurance premiums• Employee salaries, commissions or similar compensations• Payments of interest on any mortgage debts (excludes – prepayment &

principal)• Rent• Utilities• Interest on other debt obligations that were incurred before the covered

period

CARES Act: Paycheck Protection Program

4/6/2020

21

• Other items to note• No application fee• Waive requirement that applicant be unable to obtain credit

elsewhere• No personal guarantee nor collateral required• Payment deferral for at least six months, not greater than one year• Applicants are not prohibited from also obtaining an EIDL for a

purpose other than PPP’s allowable uses (defined earlier)• Loan term of two years & rate of 1%

CARES Act: Paycheck Protection Program

• Potential loan forgiveness feature• For PPP’s covered costs incurred & payments made during eight-week

period starting on day of loan origination to only include• Payroll costs • Interest on covered mortgage obligations• Payments of covered rent obligation• Payments on covered utility payment

• Forgiveness shall not exceed principal• Amounts forgiven shall be considered canceled indebtedness but not

taxable

CARES Act: Paycheck Protection Program

4/6/2020

22

• Potential loan forgiveness feature• Limits on forgiveness: reduction based on reduced number of FTEs

• Average full-time equivalents per month during the eight-week covered period after loan origination as compared to the average full-time equivalents per month during the February 15, 2019–June 30, 2019, period

• Can elect to substitute the monthly average full-time equivalent count from the 2019 period to the January 1, 2020–February 29, 2020, period

• Calculation of average number of employees• Average full-time equivalent = average FTE for each pay period falling in a month

• Not more than 25 percent of the loan forgiveness amount may be attributable to nonpayroll costs

CARES Act: Paycheck Protection Program

• Potential loan forgiveness • Exemption for rehires

• Reductions in workforce, salaries & wages that occur from February 15, 2020 to April 26, 2020 (30 days after signing into law), will be disregarded for purposes of reducing the forgiveness amount so long as the reductions are eliminated by June 30, 2020

• Other exemptions coming?• SBA & Treasury may prescribe additional regulations granting de

minimis exemptions from these requirements

CARES Act: Paycheck Protection Program

4/6/2020

23

• Correlation with other provisions in CARES• Acceptance & receipt of the PPP loan eliminates the

applicant’s eligibility to obtain employee retention credits as made available in a separate provision of the CARES Act

• In addition, should any PPP indebtedness be forgiven, the delayed payments options for the employer’s share of payroll taxes will not be available to the applicant

CARES Act: Paycheck Protection Program

CARES Act: Midsize Loan Program

• Largely undefined loan program to be created by the Treasury Department• Intended for organizations between 500 & 10,000 employees• To be administered by local financial institutions• Expressly applies to nonprofit organizations• Intended use is to retain 90% of workforce at full wages & benefits through

September 30, 2020• Interest capped at 2% with no principal or interest in first six months• Expressly prohibits loan forgiveness• Waiting for details & guidance

4/6/2020

24

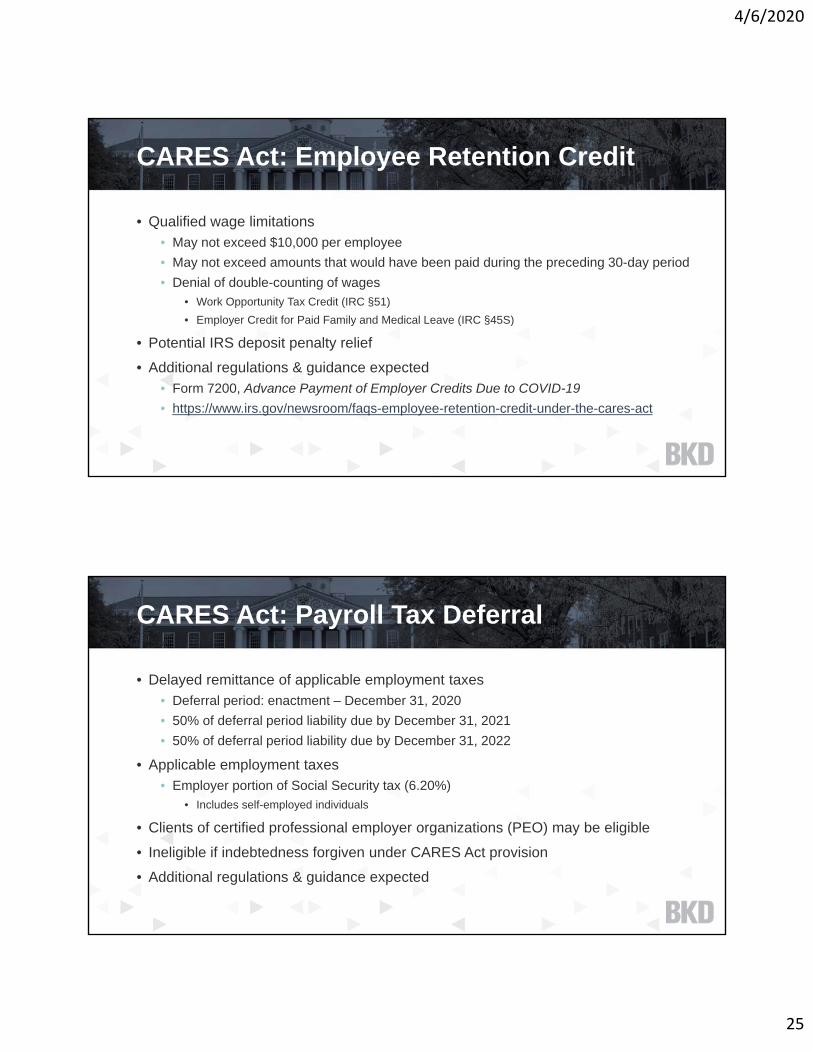

CARES Act: Employee Retention Credit

• Credit against applicable employment taxes• 50% of qualified wages up to $10,000 ($5,000 maximum credit per employee)

• Effective dates – wages paid after March 12, 2020 and before January 1, 2021

• Employer eligibility (includes tax-exempt organizations)• Carrying on a trade or business during calendar year 2020 &• The operation of that trade or business is either

• Fully or partially suspended due to orders from a governmental authority limiting commerce, travel or group meetings due to COVID-19; or

• Receiving gross receipts, for at least one calendar quarter, that are less than 50% of the gross receipts during the same calendar quarter(s) in the prior year (applicable until quarter exceeds 80% of same calendar quarter in prior year)

CARES Act: Employee Retention Credit

• Ineligible employers• Employer’s receiving Small Business Interruption loan under the CARES Act (PPP loan)• Federal, state & local government employers

• Qualified wages• Based on average number of full-time employees (aggregation rules under IRC §52

apply)• More than 100 full-time employees – only eligible if employee is unable to provide services due to

one of identified circumstances• 100 or less full-time employees – eligible for credit regardless of whether employee is able to

provide services (must meet one of previously identified circumstances)

• Includes• Wages as defined by IRC §3121(a) & compensation as defined by IRC §3231(e)• Qualified health plan expenses (IRC §5000(b)(1))

4/6/2020

25

CARES Act: Employee Retention Credit

• Qualified wage limitations• May not exceed $10,000 per employee• May not exceed amounts that would have been paid during the preceding 30-day period• Denial of double-counting of wages

• Work Opportunity Tax Credit (IRC §51)• Employer Credit for Paid Family and Medical Leave (IRC §45S)

• Potential IRS deposit penalty relief• Additional regulations & guidance expected

• Form 7200, Advance Payment of Employer Credits Due to COVID-19

• https://www.irs.gov/newsroom/faqs-employee-retention-credit-under-the-cares-act

CARES Act: Payroll Tax Deferral

• Delayed remittance of applicable employment taxes • Deferral period: enactment – December 31, 2020• 50% of deferral period liability due by December 31, 2021• 50% of deferral period liability due by December 31, 2022

• Applicable employment taxes• Employer portion of Social Security tax (6.20%)

• Includes self-employed individuals

• Clients of certified professional employer organizations (PEO) may be eligible• Ineligible if indebtedness forgiven under CARES Act provision• Additional regulations & guidance expected

4/6/2020

26

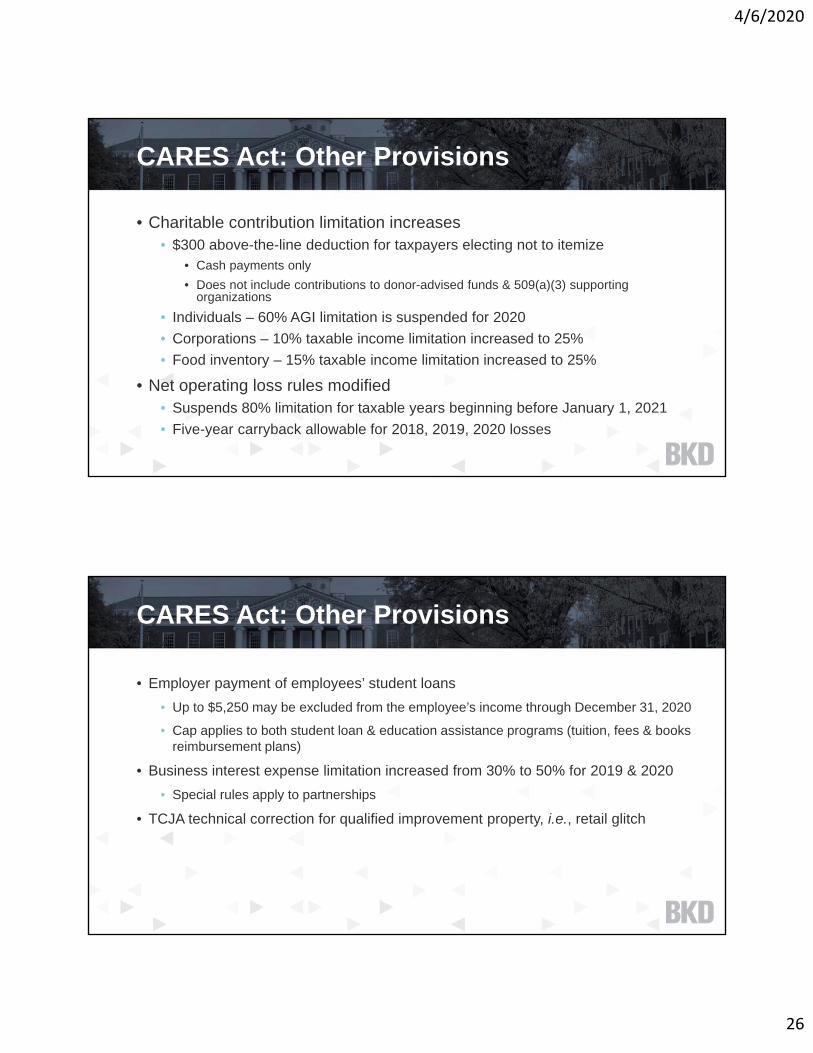

CARES Act: Other Provisions

• Charitable contribution limitation increases• $300 above-the-line deduction for taxpayers electing not to itemize

• Cash payments only• Does not include contributions to donor-advised funds & 509(a)(3) supporting

organizations• Individuals – 60% AGI limitation is suspended for 2020• Corporations – 10% taxable income limitation increased to 25%• Food inventory – 15% taxable income limitation increased to 25%

• Net operating loss rules modified• Suspends 80% limitation for taxable years beginning before January 1, 2021• Five-year carryback allowable for 2018, 2019, 2020 losses

CARES Act: Other Provisions

• Employer payment of employees’ student loans• Up to $5,250 may be excluded from the employee’s income through December 31, 2020

• Cap applies to both student loan & education assistance programs (tuition, fees & books reimbursement plans)

• Business interest expense limitation increased from 30% to 50% for 2019 & 2020• Special rules apply to partnerships

• TCJA technical correction for qualified improvement property, i.e., retail glitch

4/6/2020

27

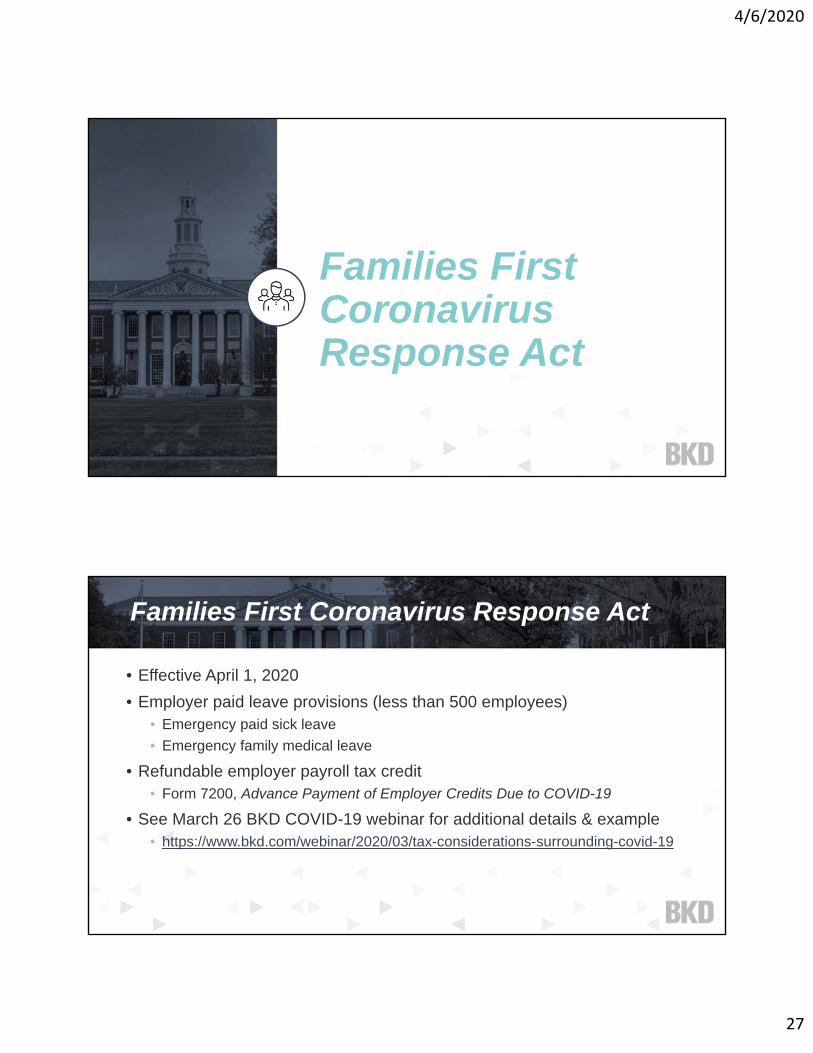

Families First Coronavirus Response Act

• Effective April 1, 2020• Employer paid leave provisions (less than 500 employees)

• Emergency paid sick leave• Emergency family medical leave

• Refundable employer payroll tax credit• Form 7200, Advance Payment of Employer Credits Due to COVID-19

• See March 26 BKD COVID-19 webinar for additional details & example• https://www.bkd.com/webinar/2020/03/tax-considerations-surrounding-covid-19

Families First Coronavirus Response Act

4/6/2020

28

For more information, please visit BKD's COVID‐19 Resource Center atbkd.com/covid‐19‐resource‐center

4/6/2020

29

Continuing Professional Education (CPE) Credit

BKD, LLP is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: www.nasbaregistry.org

The information contained in these slides is presented by professionals for your information only & is not to be considered as legal advice. Applying specific information to your situation requires careful consideration of facts & circumstances. Consult your BKD advisor or legal counsel before acting on any matters covered

To Receive CPE Credit

• CPE credit may be awarded upon verification of participant attendance

• For questions, concerns or comments regarding CPE credit, please email the BKD Learning & Development Department at [email protected]

4/6/2020

30

bkd.com/higher-ed | @BKDHigherEd

BKD Thoughtware®

• Webinars, seminars & articles

• Many are CPE-eligible

• Thoughtware – Higher Ed