through collaborative factory-to-shelf … · net result: ahold gain market share . 8 ... online...

TRANSCRIPT

1

THROUGH COLLABORATIVE FACTORY-TO-SHELF MANAGEMENT

2

The environment

Retailer initiatives

Manufacturer initiatives

Q&A Session

Close

AGENDA

3

We have talked about collaboration in the past…

WHAT’S CHANGED?

Internal focus to external advocacy

The Economy Data Technical

Readiness

4

WHAT IS THE GOAL?

The elimination of the zero-sum game

Service Savings Sustainability Consumer satisfaction

Speed to shelf

Manufacturer profitability

Retailer profitability

Reduction in miles

Smaller footprint

5

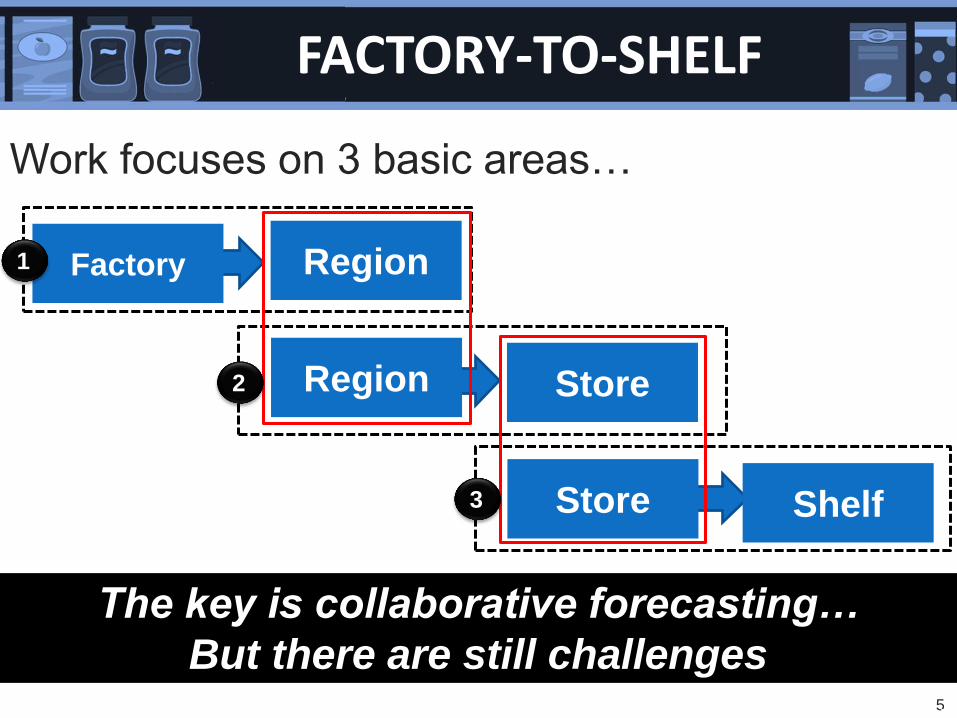

FACTORY-TO-SHELF

Factory

Region Store

Region

Store Shelf

The key is collaborative forecasting…

But there are still challenges

1

2

3

Work focuses on 3 basic areas…

6

CHALLENGES

We addressed the following:

POS data interpretation

Holistic data analysis

Communication: factory to shelf

Account vs region performances

7

WE KNOW IT WORKS

Hurricane Sandy

hits Mid-Atlantic

on 10-29-12

Shoppers stocked

up, wiping out

inventory

D2S fortified

stock-up pre-

storm and helped

stores rebound

post-storm

Net result: Ahold gain market share

8

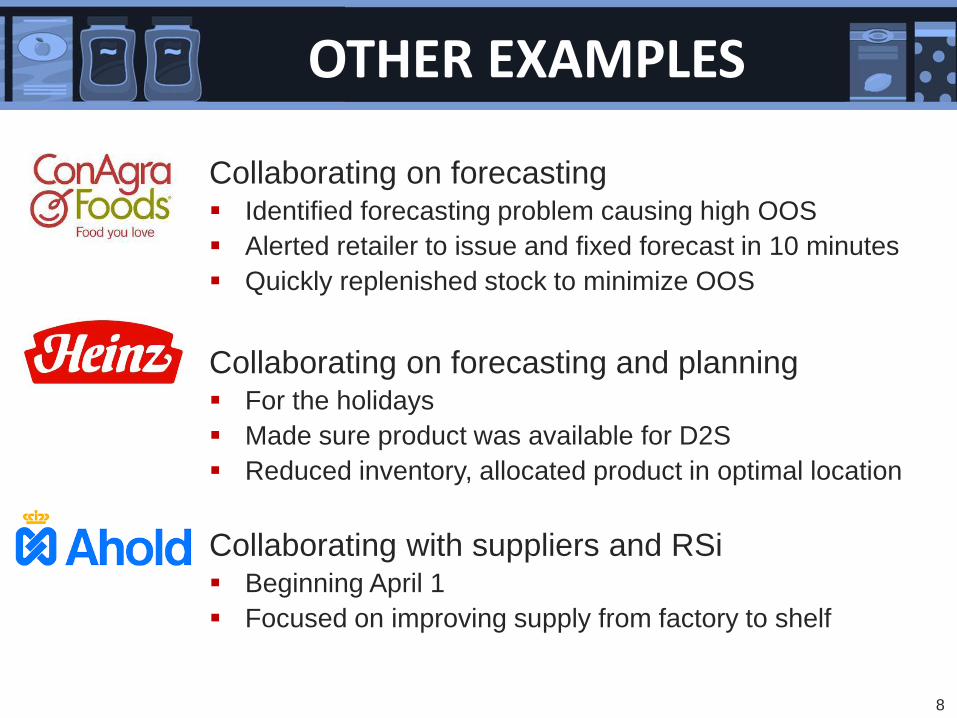

Collaborating on forecasting Identified forecasting problem causing high OOS

Alerted retailer to issue and fixed forecast in 10 minutes

Quickly replenished stock to minimize OOS

Collaborating on forecasting and planning For the holidays

Made sure product was available for D2S

Reduced inventory, allocated product in optimal location

Collaborating with suppliers and RSi Beginning April 1

Focused on improving supply from factory to shelf

OTHER EXAMPLES

9

Phase I – First Half 2012

• Building accurate models

• Developing sustainable metrics

• Analyzing root causes

Phase 2 – Second Half 2012

• Testing the models in the real world

• Found solutions to reduce promo OOS

ES3 OSA STUDY

We will share learning from the study today

10

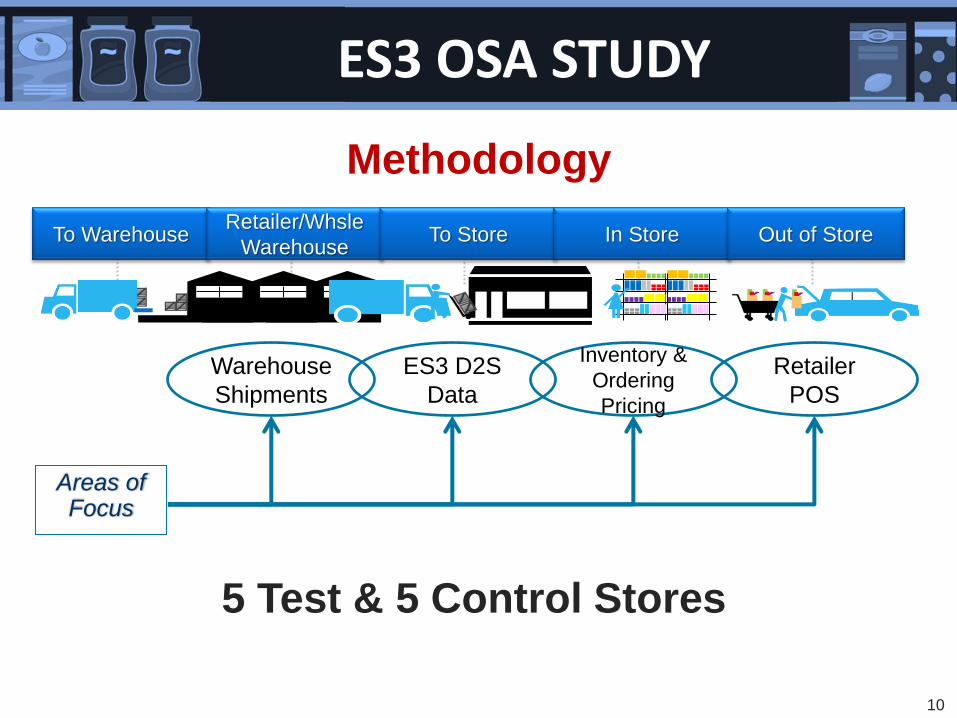

Methodology

ES3 OSA STUDY

To Warehouse Retailer/Whsle

Warehouse To Store In Store Out of Store

Warehouse

Shipments

ES3 D2S

Data

Inventory &

Ordering

Pricing

Retailer

POS

Areas of Focus

5 Test & 5 Control Stores

11

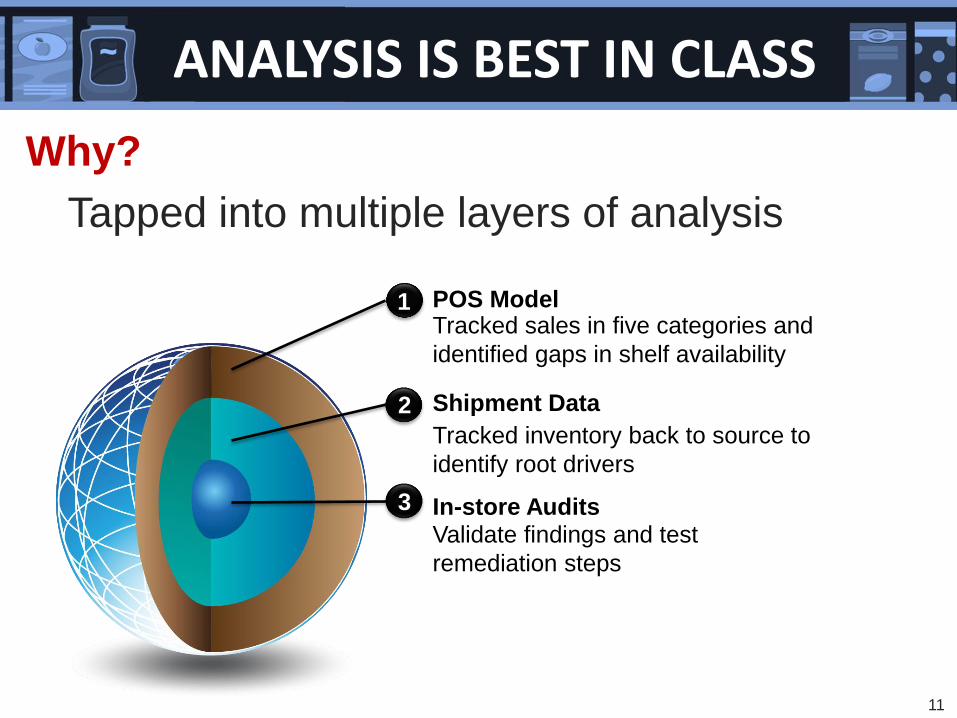

Why?

Tapped into multiple layers of analysis

ANALYSIS IS BEST IN CLASS

POS Model

In-store Audits

Shipment Data

1

2

3

Tracked sales in five categories and

identified gaps in shelf availability

Validate findings and test

remediation steps

Tracked inventory back to source to

identify root drivers

12

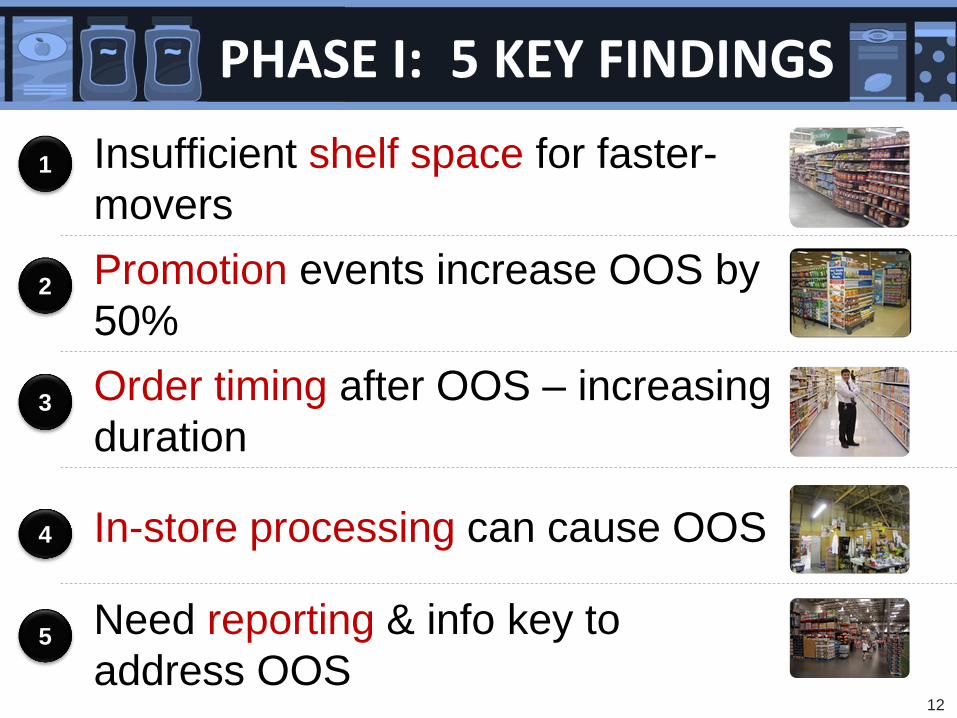

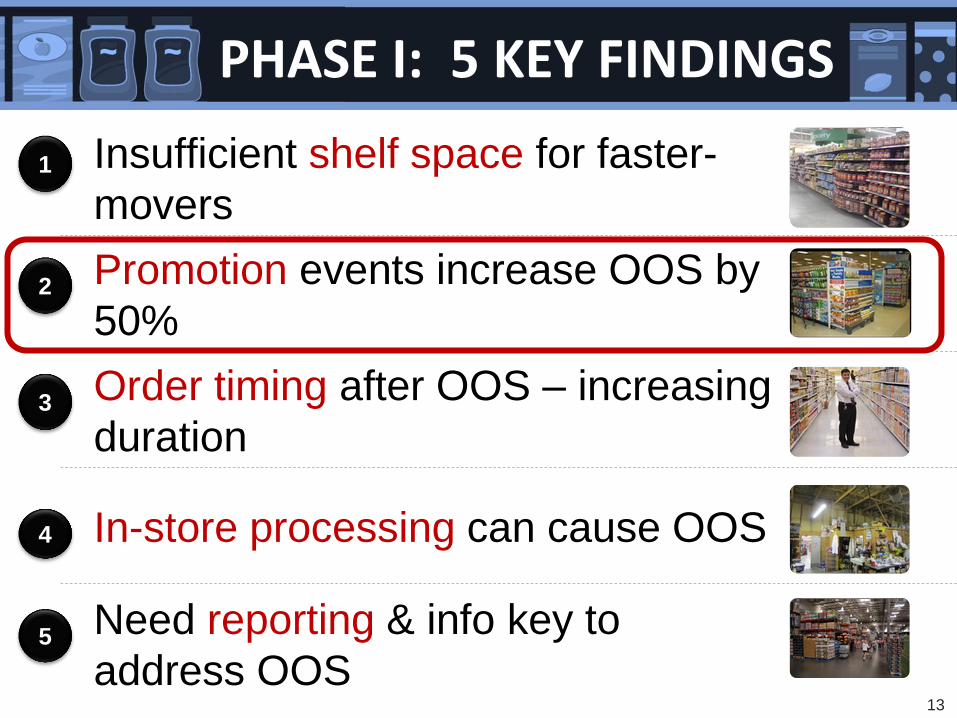

PHASE I: 5 KEY FINDINGS

Insufficient shelf space for faster-

movers

Promotion events increase OOS by

50%

Order timing after OOS – increasing

duration

In-store processing can cause OOS

Need reporting & info key to

address OOS

1

2

3

4

5

13

PHASE I: 5 KEY FINDINGS

Insufficient shelf space for faster-

movers

Promotion events increase OOS by

50%

Order timing after OOS – increasing

duration

In-store processing can cause OOS

Need reporting & info key to

address OOS

1

2

3

4

5

14

“How do you know?”

PHASE II: PROOF OF CONCEPT

15

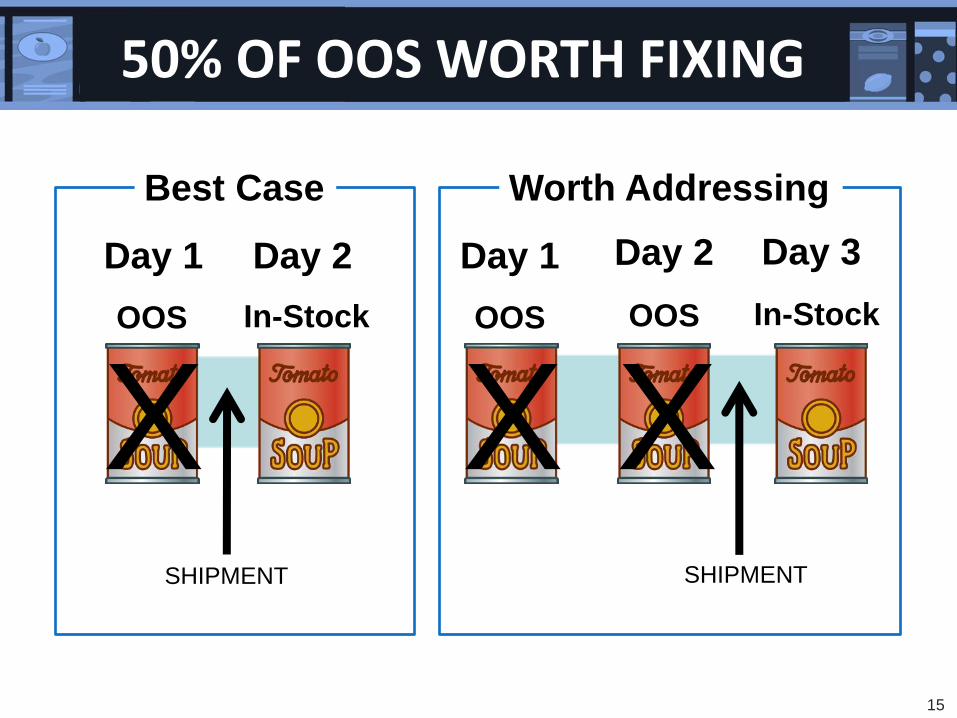

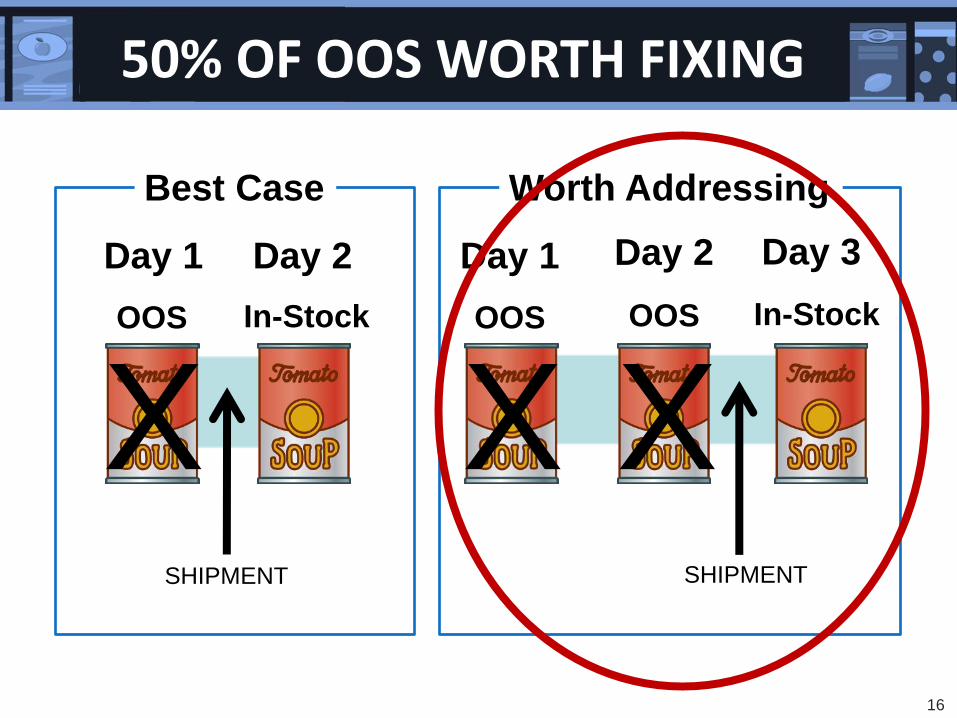

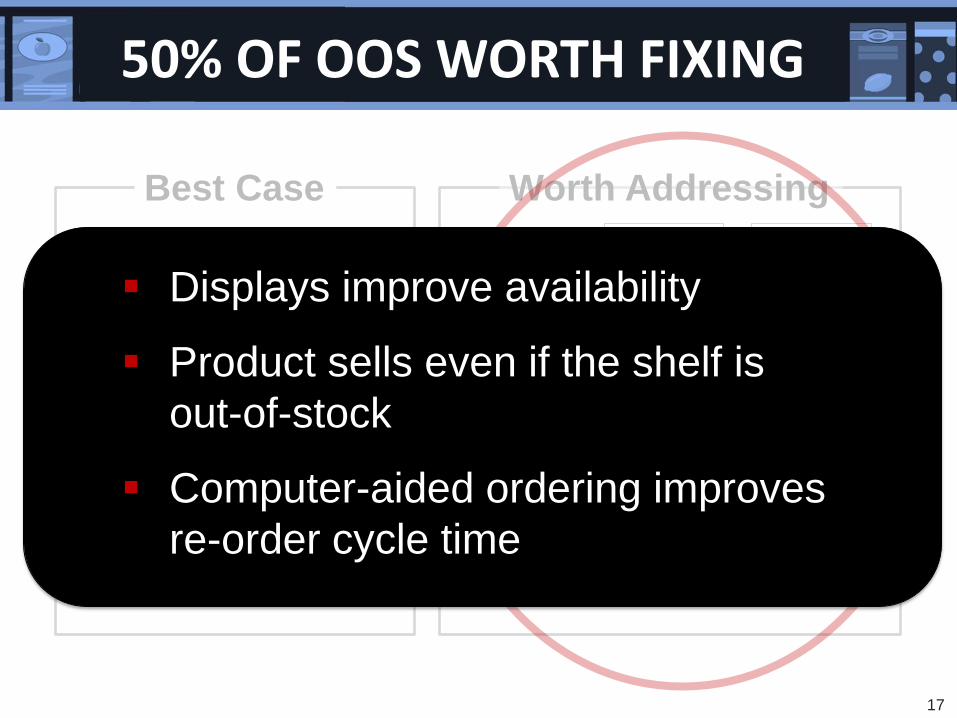

50% OF OOS WORTH FIXING

Day 1 Day 2 Day 3

SHIPMENT

OOS OOS In-Stock OOS In-Stock

Day 1 Day 2

SHIPMENT

Best Case Worth Addressing

X X X

16

50% OF OOS WORTH FIXING

Day 1 Day 2 Day 3

SHIPMENT

OOS OOS In-Stock OOS In-Stock

Day 1 Day 2

SHIPMENT

Best Case Worth Addressing

X X X

17

50% OF OOS WORTH FIXING

Day 1 Day 2 Day 3

SHIPMENT

OOS OOS In-Stock

X X OOS In-Stock

Day 1 Day 2

SHIPMENT

Best Case Worth Addressing

Displays improve availability

Product sells even if the shelf is

out-of-stock

Computer-aided ordering improves

re-order cycle time

18

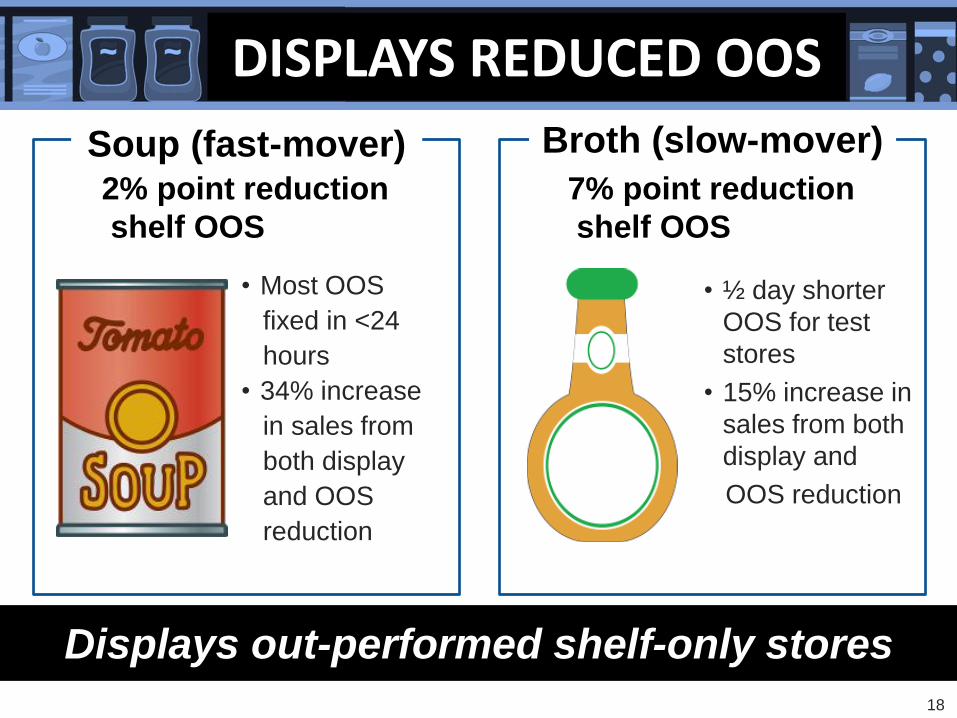

DISPLAYS REDUCED OOS

Soup (fast-mover)

• ½ day shorter

OOS for test

stores

• 15% increase in

sales from both

display and

OOS reduction

• Most OOS

fixed in <24

hours

• 34% increase

in sales from

both display

and OOS

reduction

2% point reduction

shelf OOS

7% point reduction

shelf OOS

Broth (slow-mover)

Displays out-performed shelf-only stores

19

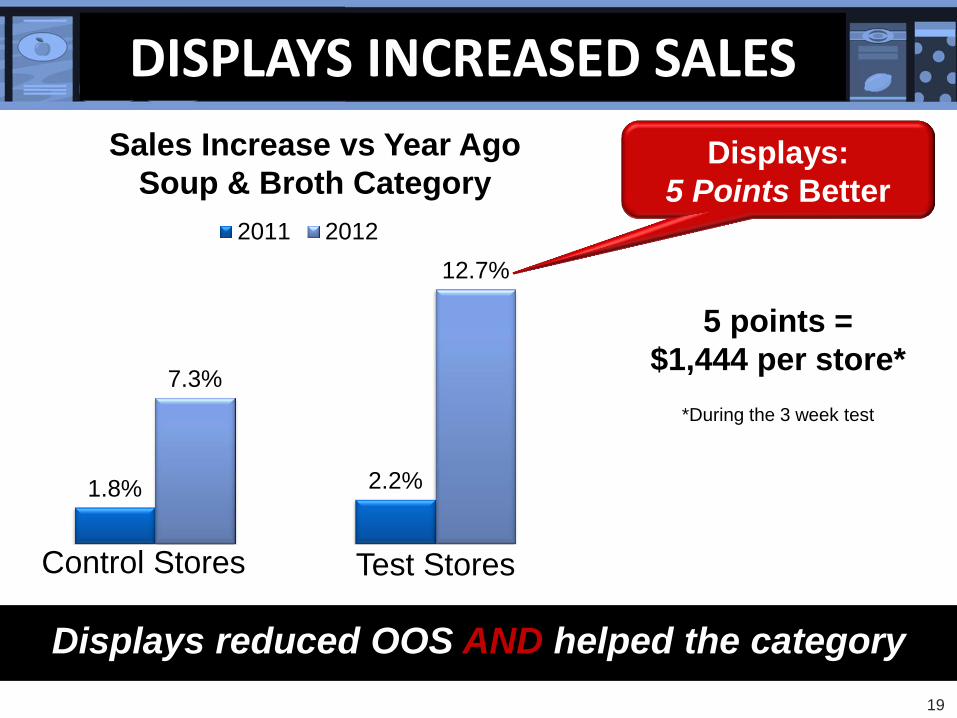

DISPLAYS INCREASED SALES

1.8% 2.2%

7.3%

12.7%

2011 2012

5 points =

$1,444 per store*

Control Stores

Sales Increase vs Year Ago

Soup & Broth Category

*During the 3 week test

Test Stores

Displays:

5 Points Better

Displays reduced OOS AND helped the category

20

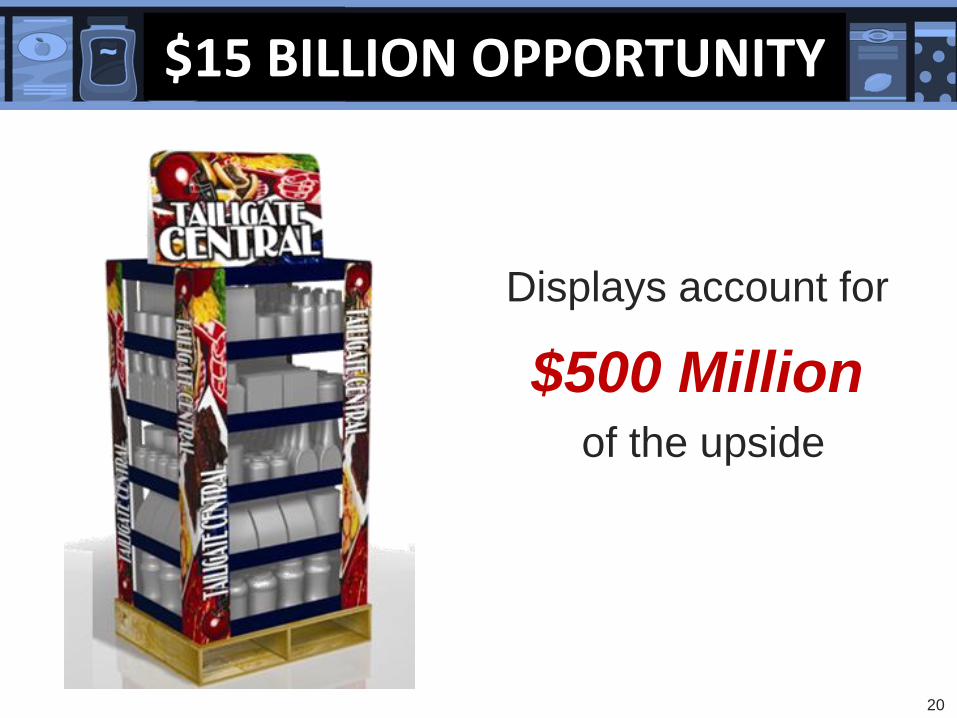

$15 BILLION OPPORTUNITY

Displays account for

$500 Million of the upside

21

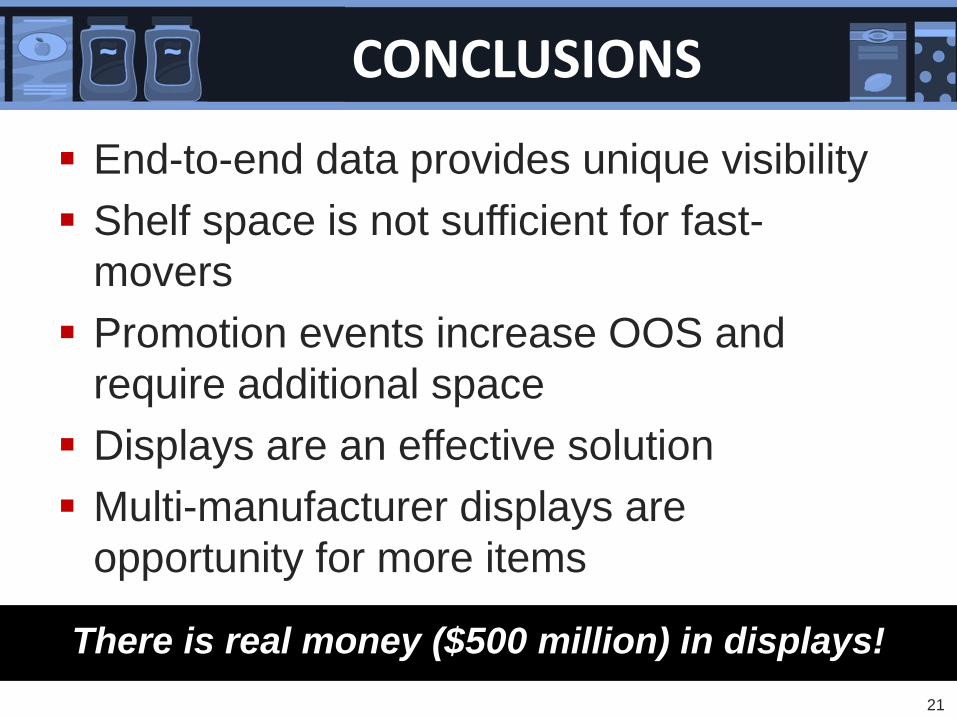

End-to-end data provides unique visibility

Shelf space is not sufficient for fast-

movers

Promotion events increase OOS and

require additional space

Displays are an effective solution

Multi-manufacturer displays are

opportunity for more items

CONCLUSIONS

There is real money ($500 million) in displays!

22

Tim Rohrbaugh Senior Director,

Non Perishables

Replenishment

Bob Masching Senior Vice President,

Supply Chain

Scott Steeves Director

Sales & Operations Planning &

Customer Supply Chain

PANEL DISCUSSION

23

Vendor Collaboration - DSR

24

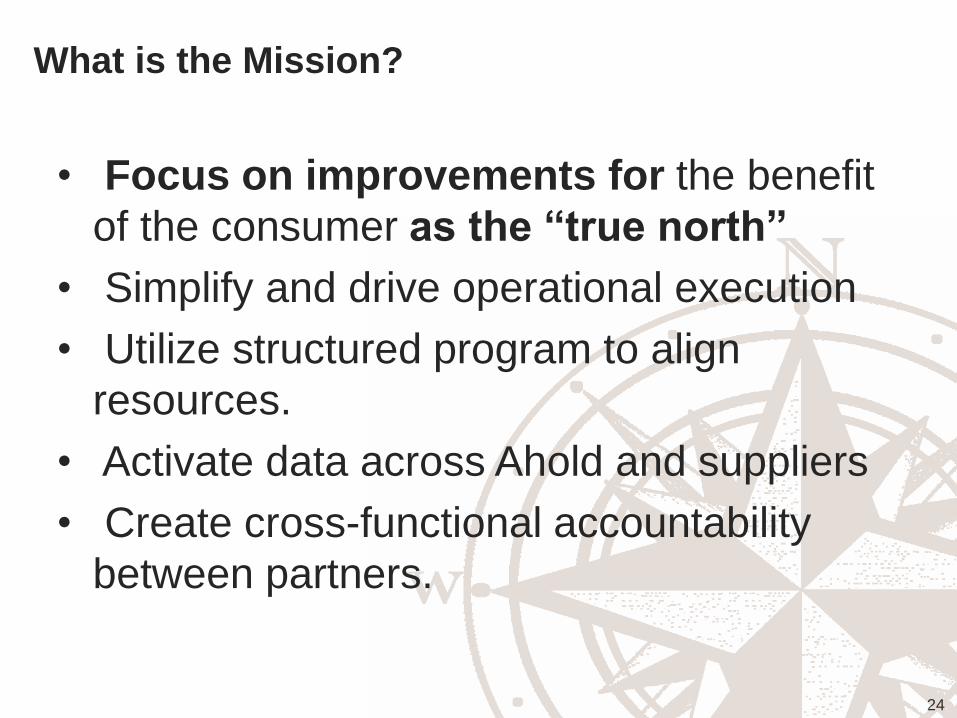

What is the Mission?

• Focus on improvements for the benefit

of the consumer as the “true north”

• Simplify and drive operational execution

• Utilize structured program to align

resources.

• Activate data across Ahold and suppliers

• Create cross-functional accountability

between partners.

25

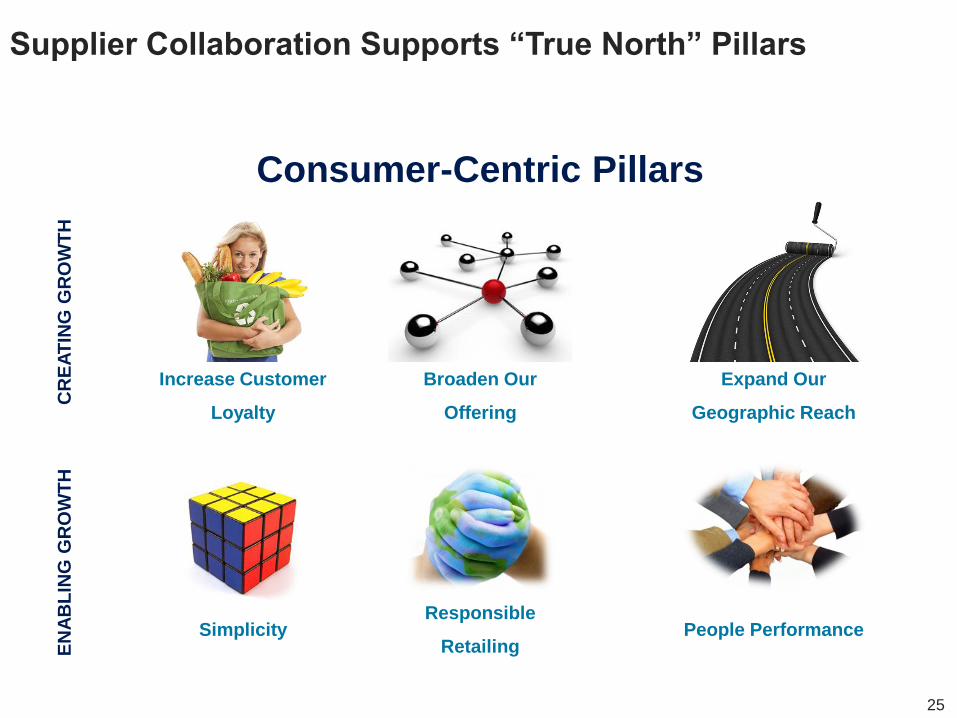

Consumer-Centric Pillars

Supplier Collaboration Supports “True North” Pillars C

RE

AT

ING

GR

OW

TH

E

NA

BL

ING

GR

OW

TH

Increase Customer

Loyalty

Broaden Our

Offering

Expand Our

Geographic Reach

Simplicity Responsible

Retailing People Performance

26

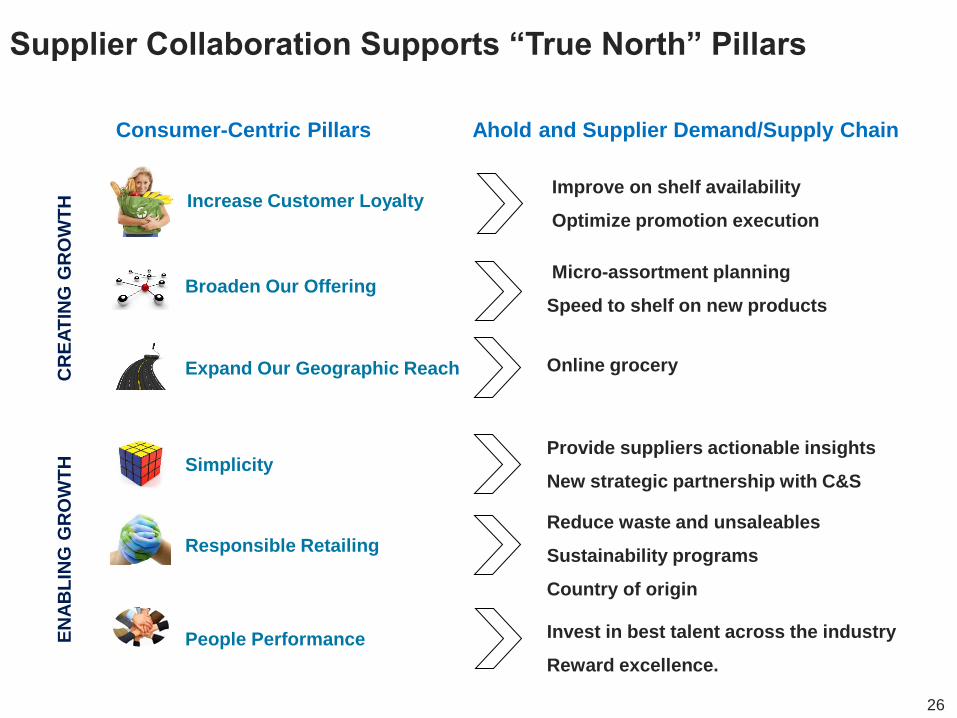

Supplier Collaboration Supports “True North” Pillars

Consumer-Centric Pillars

CR

EA

TIN

G G

RO

WT

H

EN

AB

LIN

G G

RO

WT

H

Increase Customer Loyalty

Broaden Our Offering

Expand Our Geographic Reach

Simplicity

Responsible Retailing

People Performance

Ahold and Supplier Demand/Supply Chain

Improve on shelf availability

Optimize promotion execution

Micro-assortment planning

Speed to shelf on new products

Online grocery

Provide suppliers actionable insights

New strategic partnership with C&S

Reduce waste and unsaleables

Sustainability programs

Country of origin

Invest in best talent across the industry

Reward excellence.

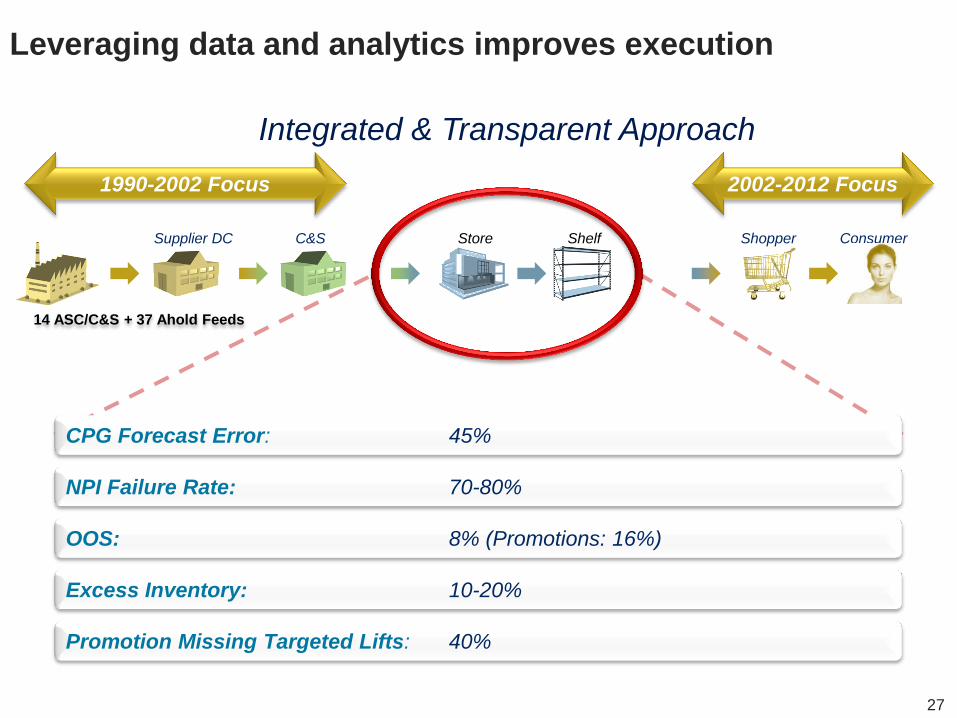

27

Supplier DC C&S Shopper

1990-2002 Focus

Excess Inventory: 10-20%

CPG Forecast Error: 45%

NPI Failure Rate: 70-80%

Promotion Missing Targeted Lifts: 40%

OOS: 8% (Promotions: 16%)

Store Shelf Consumer

2002-2012 Focus

14 ASC/C&S + 37 Ahold Feeds

Leveraging data and analytics improves execution

Integrated & Transparent Approach

28

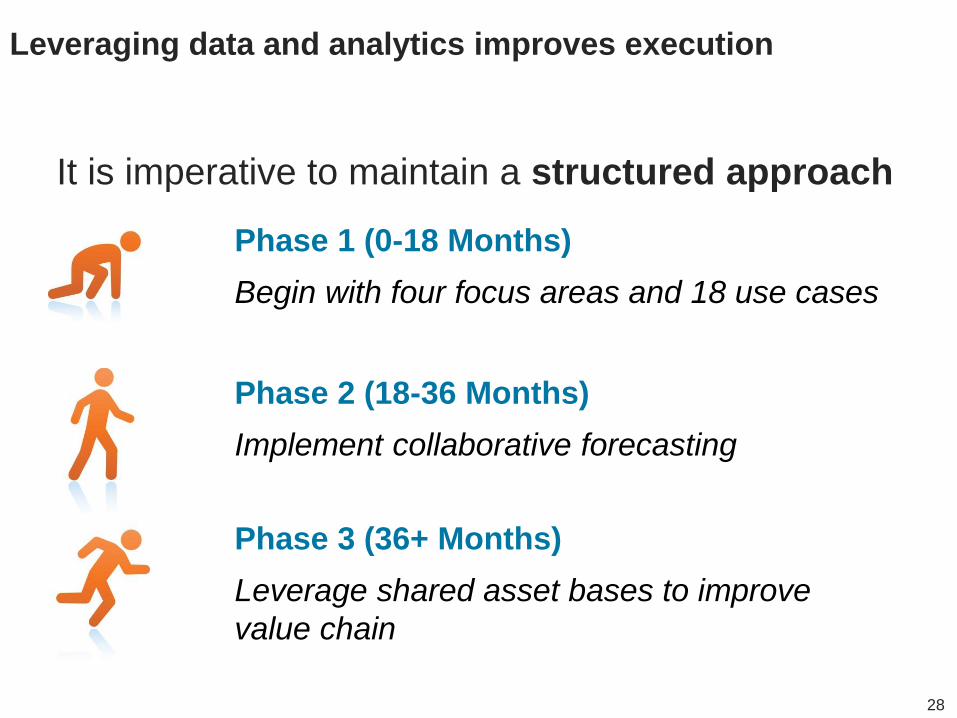

Leveraging data and analytics improves execution

It is imperative to maintain a structured approach

Phase 1 (0-18 Months)

Begin with four focus areas and 18 use cases

Phase 3 (36+ Months)

Leverage shared asset bases to improve

value chain

Phase 2 (18-36 Months)

Implement collaborative forecasting

29

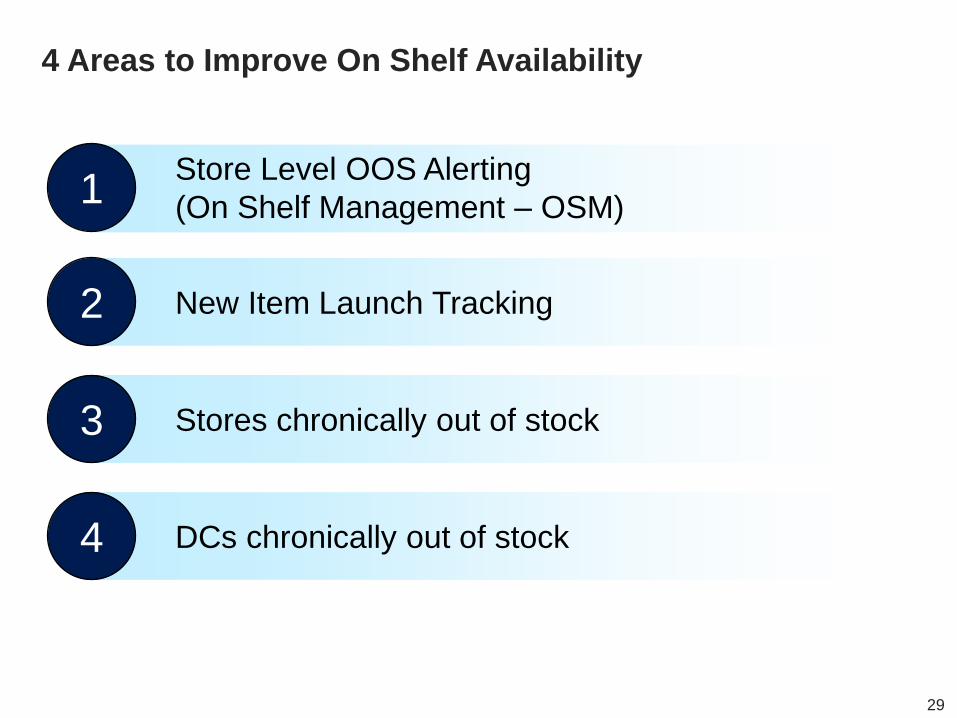

4 Areas to Improve On Shelf Availability

1

2

3

4

Store Level OOS Alerting

(On Shelf Management – OSM)

New Item Launch Tracking

Stores chronically out of stock

DCs chronically out of stock

30

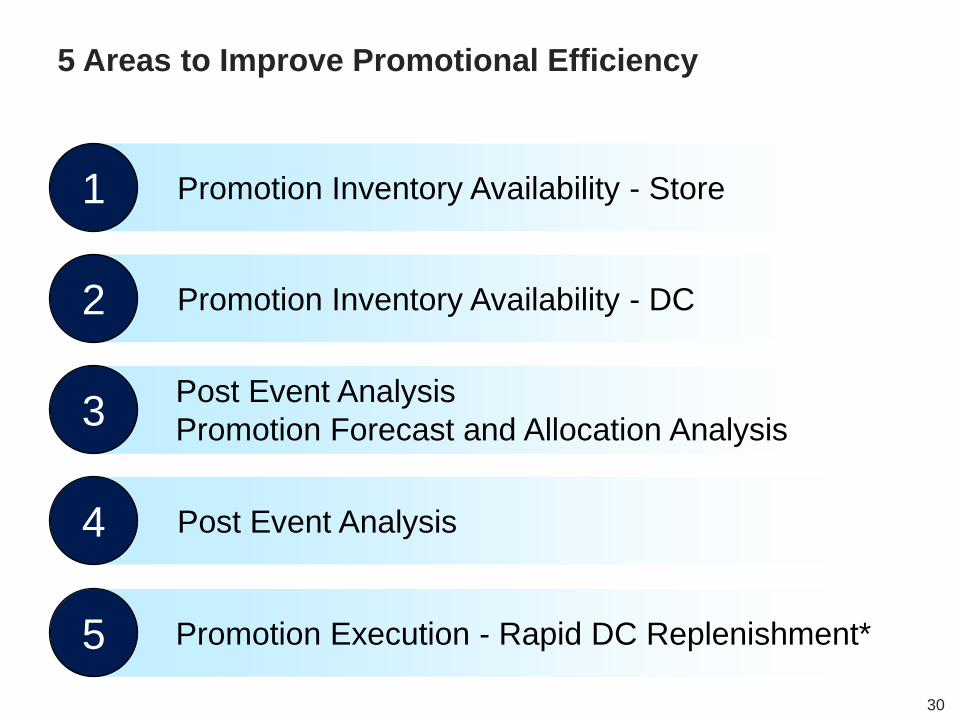

5 Areas to Improve Promotional Efficiency

1

2

3

4

Promotion Inventory Availability - Store

Promotion Inventory Availability - DC

Post Event Analysis

Promotion Forecast and Allocation Analysis

Post Event Analysis

5 Promotion Execution - Rapid DC Replenishment*

31

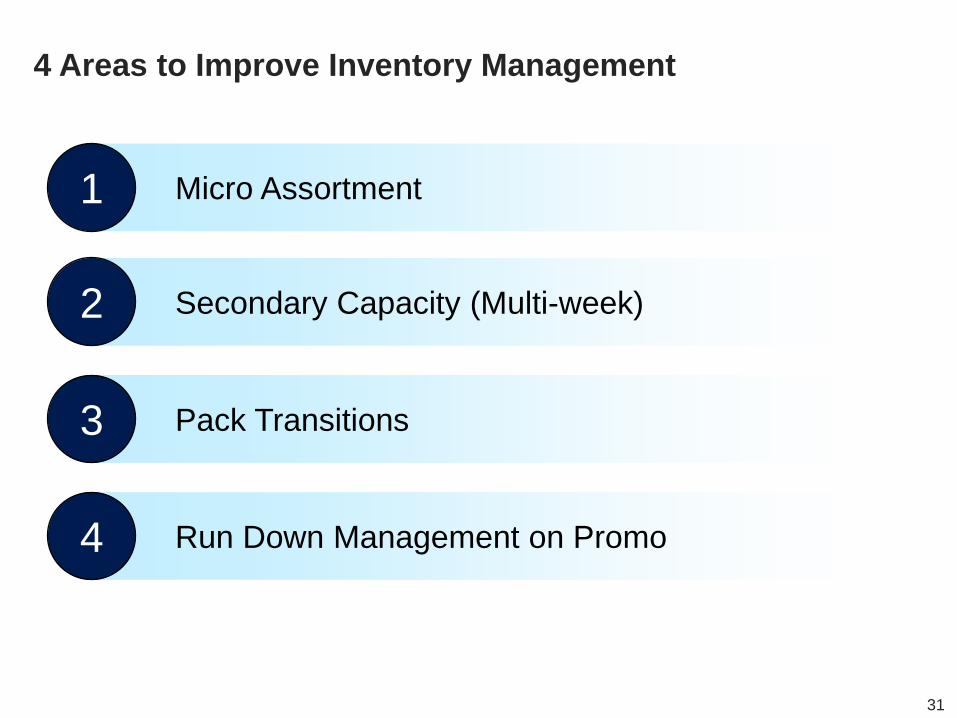

4 Areas to Improve Inventory Management

1

2

3

4

Micro Assortment

Secondary Capacity (Multi-week)

Pack Transitions

Run Down Management on Promo

32

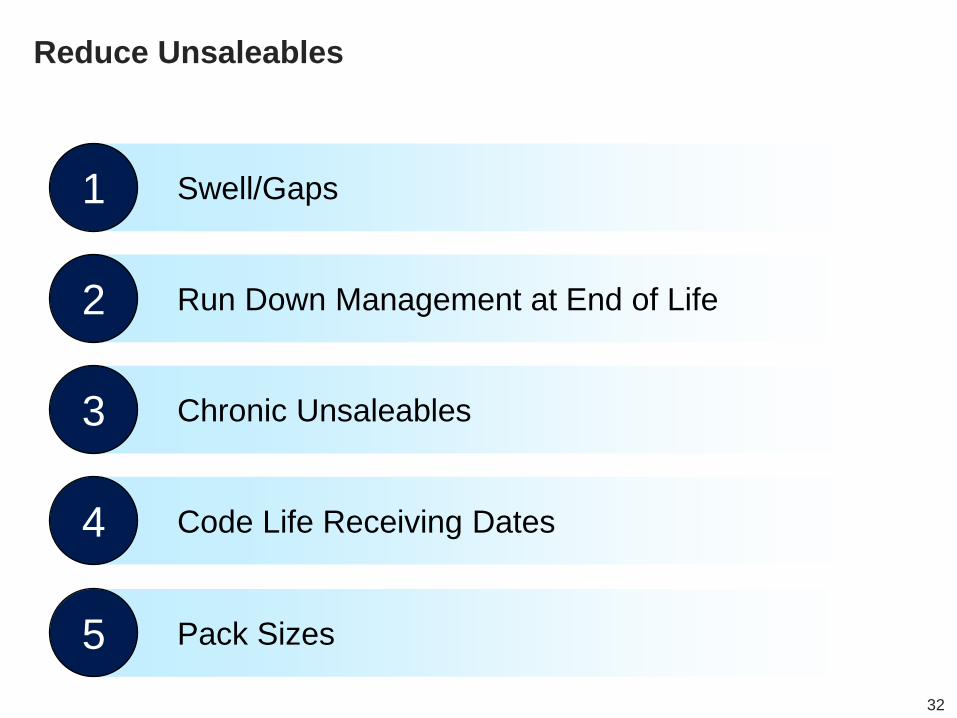

Reduce Unsaleables

1

2

3

4

Swell/Gaps

Run Down Management at End of Life

Chronic Unsaleables

Code Life Receiving Dates

5 Pack Sizes

33

1. Net Sales per Primary Selling Space 12. Total Loss vs Swell

2. Gross Profit per Primary Selling Space 13. Total Unsaleable Dollars

3. GMROII Average 14. Avg Days Remaining on Code Date at Time of Receipt

4. Avg Days on Hand - Store 15. Total Sales Amount

5. Avg Days on Hand - DC 16. TY vs LY Total Sales Amount % Change

6. Year on Year Assortment Count 17. Total Margin Percent

7. Speed-to-Shelf 18.Promoted Sales Percent Volume

8. Store Turn Service Level 19. On-Time Delivery %

9. Store Promo Service Level 20. Average Lead Time

10. Store Total Service Level 21. Fill Rate

11. Total Reclaim Value 22. Overall Vendor Score

Ahold and our vendor-partners will measure the improvements monthly

Health Scorecard

34

ConAgra Foods

Retailer

Collaboration

Bob Masching SVP

Supply Chain

ConAgra Foods portfolio:

$18 billion in sales

35

36

37

Strategies

Capabilities

Benefits

Fueling growth through an advantaged supply chain

Purpose

Supply Chain Strategies

38

uncompromised

QUALITY

flawless

INITIATIVE

DELIVERY

value-added

CUSTOMER

SERVICE

lowest

TOTAL

DELIVERED

COST

better return on INVESTED

CAPITAL

world class

SAFETY &

SUSTAINABILITY

High Performance Culture – 20,000+ Engaged

Associates

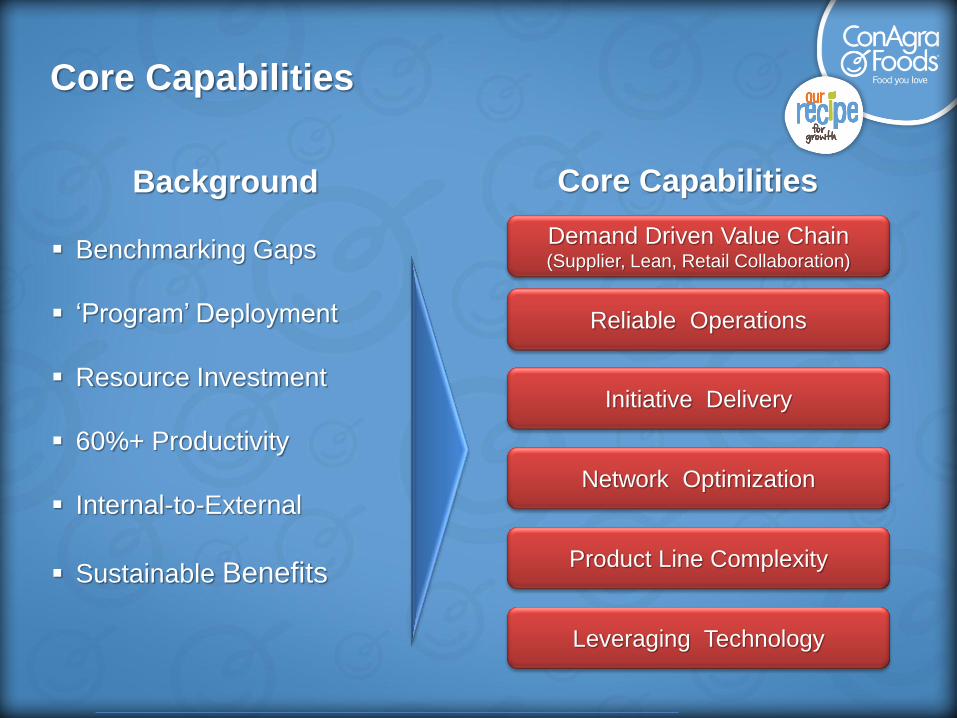

Core Capabilities

Core Capabilities Background

Benchmarking Gaps

‘Program’ Deployment

Resource Investment

60%+ Productivity

Internal-to-External

Sustainable Benefits

Reliable Operations

Initiative Delivery

Product Line Complexity

Network Optimization

Leveraging Technology

Demand Driven Value Chain (Supplier, Lean, Retail Collaboration)

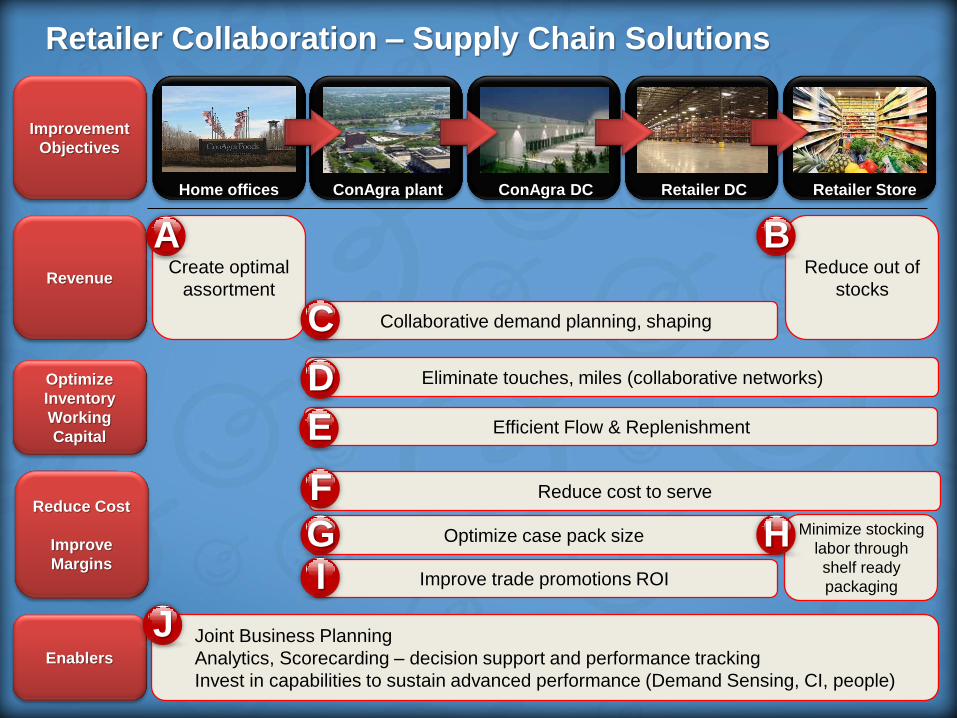

Revenue

Optimize

Inventory

Working

Capital

Grow

Margins

Create optimal

assortment

Reduce out of

stocks

Minimize stocking

labor through

shelf ready

packaging

Collaborative demand planning, shaping

Eliminate touches, miles (collaborative networks)

Reduce cost to serve

Optimize case pack size

Improve trade promotions ROI

Reduce Cost

Improve

Margins

Enablers

Joint Business Planning

Analytics, Scorecarding – decision support and performance tracking

Invest in capabilities to sustain advanced performance (Demand Sensing, CI, people)

Home offices ConAgra plant ConAgra DC Retailer DC Retailer Store

Improvement

Objectives

Retailer Collaboration – Supply Chain Solutions

A B

C

D

F

G H I

J

Efficient Flow & Replenishment E

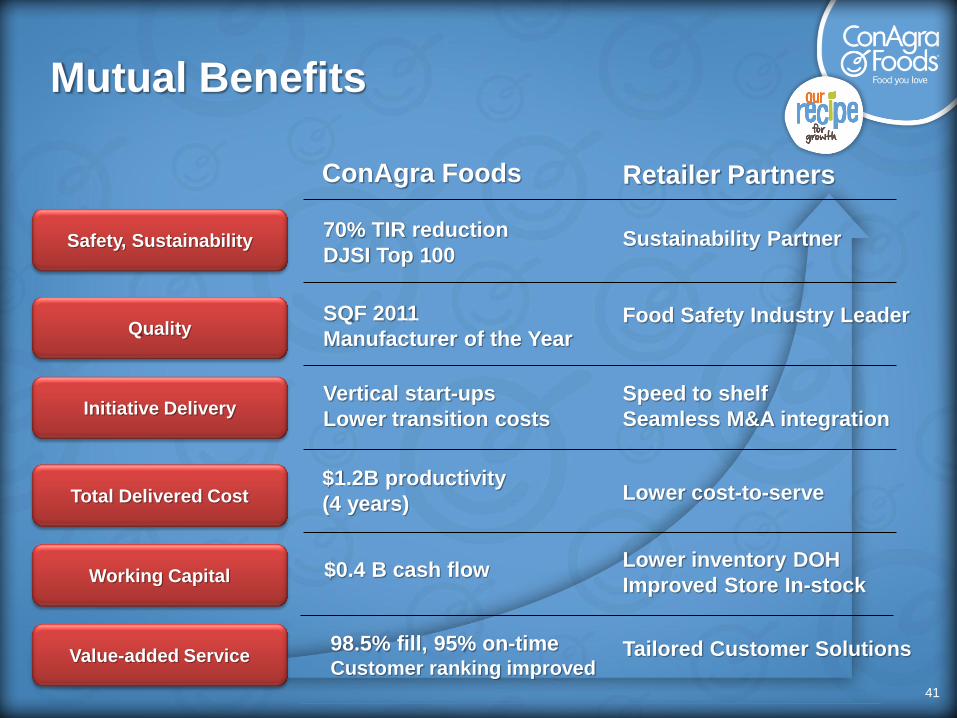

Mutual Benefits

41

Safety, Sustainability

Quality

Initiative Delivery

Total Delivered Cost

Working Capital

Value-added Service

Retailer Partners ConAgra Foods

Sustainability Partner

Food Safety Industry Leader

Speed to shelf

Seamless M&A integration

Lower cost-to-serve

Lower inventory DOH

Improved Store In-stock

70% TIR reduction

DJSI Top 100

SQF 2011

Manufacturer of the Year

Vertical start-ups

Lower transition costs

$1.2B productivity

(4 years)

$0.4 B cash flow

Tailored Customer Solutions 98.5% fill, 95% on-time Customer ranking improved

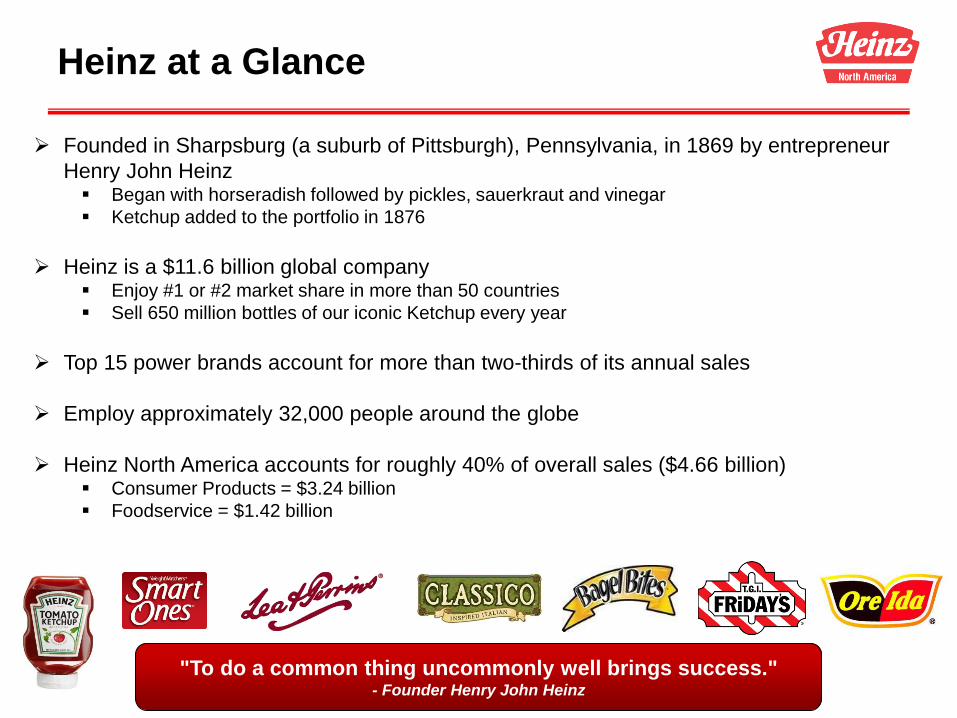

Heinz at a Glance

Founded in Sharpsburg (a suburb of Pittsburgh), Pennsylvania, in 1869 by entrepreneur

Henry John Heinz Began with horseradish followed by pickles, sauerkraut and vinegar

Ketchup added to the portfolio in 1876

Heinz is a $11.6 billion global company Enjoy #1 or #2 market share in more than 50 countries

Sell 650 million bottles of our iconic Ketchup every year

Top 15 power brands account for more than two-thirds of its annual sales

Employ approximately 32,000 people around the globe

Heinz North America accounts for roughly 40% of overall sales ($4.66 billion) Consumer Products = $3.24 billion

Foodservice = $1.42 billion

"To do a common thing uncommonly well brings success." - Founder Henry John Heinz

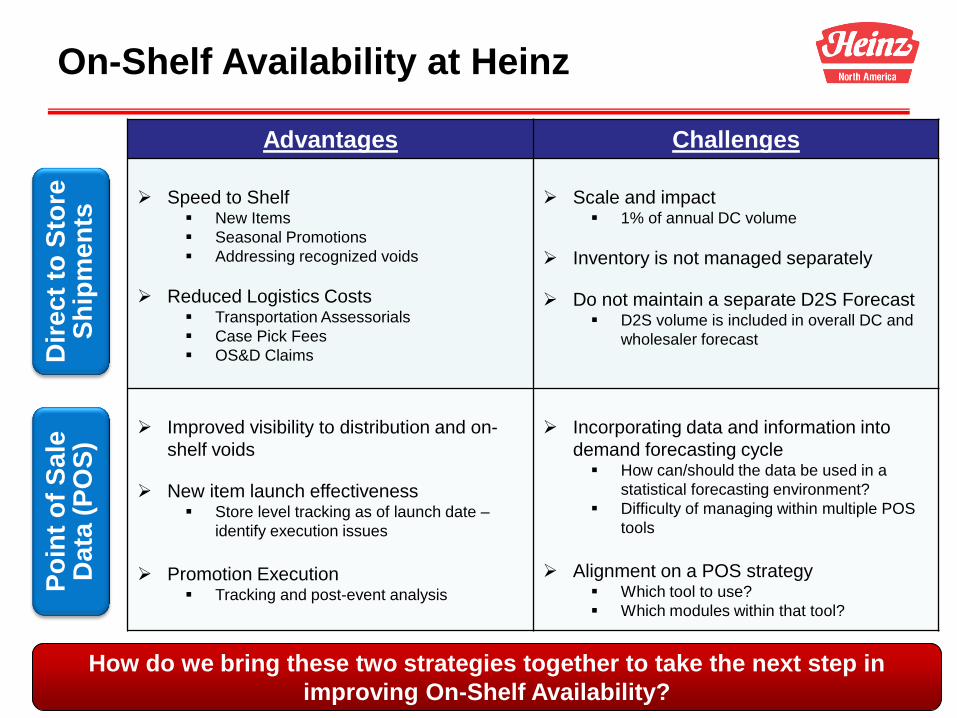

On-Shelf Availability at Heinz

How do we bring these two strategies together to take the next step in

improving On-Shelf Availability?

Dir

ec

t to

Sto

re

Sh

ipm

en

ts

Po

int

of

Sa

le

Data

(P

OS

)

Advantages Challenges

Speed to Shelf New Items

Seasonal Promotions

Addressing recognized voids

Reduced Logistics Costs Transportation Assessorials

Case Pick Fees

OS&D Claims

Scale and impact 1% of annual DC volume

Inventory is not managed separately

Do not maintain a separate D2S Forecast D2S volume is included in overall DC and

wholesaler forecast

Improved visibility to distribution and on-

shelf voids

New item launch effectiveness Store level tracking as of launch date –

identify execution issues

Promotion Execution Tracking and post-event analysis

Incorporating data and information into

demand forecasting cycle How can/should the data be used in a

statistical forecasting environment?

Difficulty of managing within multiple POS

tools

Alignment on a POS strategy Which tool to use?

Which modules within that tool?