thursday talk - vat update autumn 2015

TRANSCRIPT

VAT Update

Autumn 2015

8 October 2015

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 20152

VAT Update – Autumn 2015

2

1

3

5

E-Archiving / E-Filing

CJEU case update

Are you FAIA ready?Our solutions

SAF-T / FAIA updateBackground and scope

4

SAF-T / FAIA updateAnother tax requirement or a business opportunity?

© 2015 Deloitte Tax & Consulting.

E-Archiving / E-filing

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 20154

10 years (from date of issuance for invoices; or from31 December of the closing year for accounts)

Anywhere… subject to conditionsElectronic storage: can be outside Luxembourg ifcertain conditions are met (otherwise Luxembourg)

Inform VAT Authorities through VAT returnsStorage in a country allowing access and download

How long ?

Conditions?

Where?

E-ArchivingBackground Storage requirements in respect of VAT

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 20155

Law of 25 July 2015 in respect of the digitalisation and storage of documentsdata:

- Creates scope and rules applicable to the suppliers of digitalisation andelectronic storage services (e.g. authorization to be received from ILNAS)

- Defines conditions of digitalisation and storage of digital documents

- Defines the rules for considering digital copies to be similar to the original

Direct impact on VAT rules?

Not really, but shows the will of the administration tomove towards an even more paperless position

E-ArchivingWhat’s new?

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 20156

E-FilingWhat’s new?

Draft Grand Ducal Decree on e-filing:

• Move from

• Why?

• When?

To

Automatic checks/reconciliations between the AnnualAccounts and the Annual VAT Returns

eCDF is a more recent platform and will offer greatercommunication possibilities for accounting software

Gradually from 1 January 2016

VAT returns up to 31/12/2014 and EC Sales lists eTVA

VAT returns from 1/01/2015 eCDF (still possible with eTVAduring a transition period)

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 20157

VAT Update – Autumn 2015

2

1

3

5

E-Archiving / E-Filing

CJEU case update

Are you FAIA ready?Our solutions

SAF-T / FAIA updateBackground and scope

4

SAF-T / FAIA updateAnother tax requirement or a business opportunity?

© 2015 Deloitte Tax & Consulting.

CJEU case update

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 20159

CJEU Case Update

Agenda

1. Independent group of persons

2. Investment funds

3. Deduction of VAT by holding companies

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201510

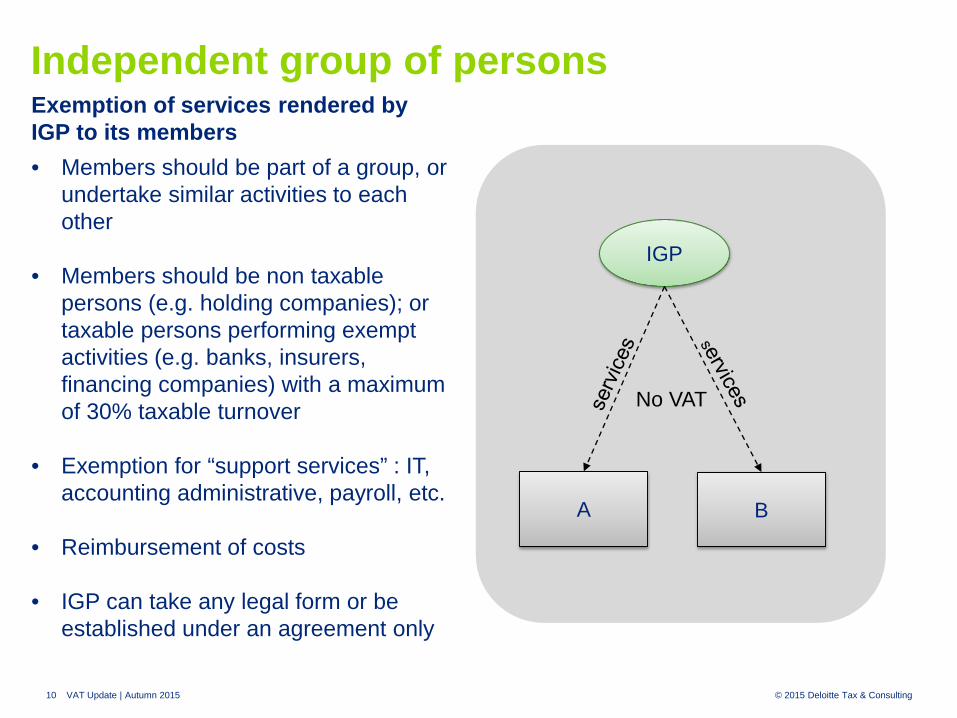

Independent group of persons

IGP

A B

Exemption of services rendered by IGP to its members• Members should be part of a group, or

undertake similar activities to each other

• Members should be non taxable persons (e.g. holding companies); or taxable persons performing exempt activities (e.g. banks, insurers, financing companies) with a maximum of 30% taxable turnover

• Exemption for “support services” : IT, accounting administrative, payroll, etc.

• Reimbursement of costs

• IGP can take any legal form or be established under an agreement only

No VAT

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201511

Infringement action brought against the Luxembourg IGP regime (C-274/15, introduced on 8 June 2015)

3 challenges made by the Commission:

1. Threshold of taxable turnover

2. Deduction by the members of VAT incurred by the IGP

3. No taxation of “contributions” made by members to an IGP without legal personality

Probably the most important point, in practice

• Introduction of VAT group as an alternative?

Independent group of persons

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201512

Case referred by Latvia (DNB Banka AS (C-326/15) introduced on 1st July 2015)

• Should a cross border IGP be obliged to meet the requirements of all of the different Member States where its members are established?

• Must the IGP be set up as a distinct legal entity?

• If not, could the existence of the IGP be proved through the contracts for services concluded by it, or through documentation relating to transfer pricing?

Luxembourg case!

• Could a TP adjustment be applied?

• Could a non-EU entity be part of an IGP?

Independent group of persons

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201513

Investment funds

Fund

Pension fundA

Pension fund B

VAT exemption for fund management services (“X fiscal eenheid X NV cs”, C-595/13)

• Could a real estate fund qualify as a fund for the VAT exemption?

• If so, could the following services be VAT exempt:

• managing the assets, in particular the properties, including buying and selling properties;

• acting as managing director, carrying out statutory and administrative tasks, financial reporting, data processing and internal audit; and

• finding investors.

VAT?

Service provider

Services

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201514

Investment fundsVAT exemption for fund management services (“X fiscal eenheid X NV cs”, C-595/13)

Favourable conclusions from the Advocate General (20 May 2015) and new criteria :

• Eligibility of a RE fund:

- No specific restriction - Objective of the exemption is to facilitate investments- In competition with other funds- Risk spreading

New: “Specific public supervision”

• Eligibility of services:

- “Specific” to the fund activity: new: maintain and increase the value of the assets

- Part of the tasks of an AIFM manager

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201515

Deduction of VAT by holding companies

OpCo

Holding

ManagementServices + VAT

Holding companies which also make supplies of services to their subsidiaries (Larentia+Minerva and Marenave, C-108 and 109/14, 16 July 2015)

• 1 economic activity = full VAT deduction

Including costs in relation to the acquisition of the shares

• Unless services don’t grant the right to recover VAT (e.g. financing)

• No VAT deduction if no services: allocation to be made

• Position of Luxembourg?

Deduction of VAT?

Serviceprovider

Services + VAT

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201516

VAT Update – Autumn 2015

2

1

3

5

E-Archiving / E-Filing

CJEU case update

Are you FAIA ready?Our solutions

SAF-T / FAIA updateBackground and scope

4

SAF-T / FAIA updateAnother tax requirement or a business opportunity?

© 2015 Deloitte Tax & Consulting.

SAF-T / FAIA UpdateBackground and scope

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201518

Need toupdate

IT systems

Production of compliant

standard data

Yesterday• Manual keying of data

• Slow and uncertaintransmission of returns

• Risk of loss of documents and penalties

Today• Automatic or semi

automatic keyingof data

• Automaticproduction of

reporting documents

Tomorrow (already today?)

• New form ofautomatic controls

• In theory faster, surer, more precise, more

efficient• Issue: need for standardised

documents for taxpayers IT systems

Today• Safe transmission

of data• Automatic

consistency checksperformed

• Unconstestableproof of filing

From taxpayers’ information systems to authorities’ audit software

SAF-T / FAIA updateBackground

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201519

In the U.S., strict requirements have been enactedto identify potential weaknesses of tax processes

In Europe, the trends show a move to e-audits and delivery ofa Standard Audit File for tax to the authorities; • France –

Computerized Tax audits since 1982

• UK – Senior Accounting Officer

• NL – Tax Control Framework

• Spain – digital provision of invoice content

• Portugal – SAF-T has been mandatory since 2008

In Australia, since 2010 largebusinesses have beenassigned a risk rating by theAustralian Tax Office. Thisrisk rating is derived fromextending and enhancingdata analytics and riskprofiling techniques

In China, new regulationsrequire large taxpayers togrant the tax authoritiesincreased access to theirinternal tax risk controlsystems

In India, the strategy seems to be to have moreaudit-based controls, as opposed to physicalcontrols. Relaxation of physical controls iscoupled with the introduction of strict penaltyprovisions, including provisions forprosecution

SAF-T / FAIA updateInternational environment – Increased scrutiny from tax authorities

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201520

All taxpayers impacted by FAIA in Phase 2 (timing not yet determined)

All taxpayersexcept

Taxpayers impacted by FAIA (Phase 1)

Taxpayers exempt from Standard

Charter of Accounts (PCN) obligations

Taxpayers subject to the simplified VAT return regime

Taxpayers whose annual turnover is below 112.000,00€

Small taxpayers with few transactions (+/-

500), where a manualcheck is easier than

submission of an electronic file

SAF-T / FAIA updateScope

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201521

Need to updateIT systems

Production of compliant

standard data

Transmission to the VAT Authorities

General ledgerChart of accounts

General ledger – Journals

Customer master files

Invoices

Payments

Supplier master files

Invoices

Payments

Fixed assets

Payroll

Others

Accounts receivable –Journals

Accounts payable –Journals

Journals to othersub-systems

Header

Master files

General ledger entries

Source documents

Sales invoices

Purchase invoices

Payments

–

–Audit file –

+

–

+

+

+

+

–

–

General ledger

Customer

Supplier

Tax table

+

+

+

+1.00

1.00

SAF-T / FAIA updateContent

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201522

• Only upon request of the Luxembourg VAT Authorities in case of (on-site) control but:

- Objectives for 2015: increase of e-Audits based on FAIA- Numerous taxpayers have received a FAIA file request, or, at least, a status request

• Is your IT system compliant?

• FAIA ready systems:- SAP- BOB- Navision- Dynamics

- Not ready / under development- Oracle- PeopleSoft- JD Edwards- Internal systems

SAF-T / FAIA updateAre you ready?

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201523

VAT Update – Autumn 2015

2

1

3

5

E-Archiving / E-Filing

CJEU case update

Are you FAIA ready?Our solutions

SAF-T / FAIA updateBackground and scope

4

SAF-T / FAIA updateAnother tax requirement or a business opportunity?

© 2015 Deloitte Tax & Consulting.

Are you FAIA ready?Our solutions

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201525

Starting point: FAIA PRA

“FAIA Preliminary Readiness Assessment” / “FAIA Comfort”

FTD – FAIA Technical Development

.

FTT: FAIA Technical Test

Technical review of your file

Free assessment of your FAIA status based on: - An online questionnaire - An on-site FAIA comfort test: free

1h meeting to debrief

OK OK

FTD: FAIA Technical Development

Technical development of your file

NOT OK

NOT OK

OK

VAT Assessment VAT review of the transactions pre-Audit

Are you FAIA ready?Our solutions

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201526

SAF-T / FAIA updateScope, type of FAIA, readiness ? Try our test !

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201527

SAF-T / FAIA updateScope, type of FAIA, readiness ? Try our test !

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201528

SAF-T / FAIA updateScope, type of FAIA, readiness ? Try our test !

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201529

Production

• Support your IT team in building up the VAT audit file;• Provide data extracted from your IT systems; and• Construction of the VAT Audit file from Excel reports.

Assessment

• Assess whether the FAIA file is acceptable by AED standards• Perform default Quality and Accounting control tests

Are you FAIA ready?Our solutions

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201530

FAIA Dashboard Overview

Are you FAIA ready?Our solutions

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201531

We produce an error report to be analysed by our experts, from which they can provide recommendations.

The FAIA file is ready to be transmitted to the AED

Are you FAIA ready?Our solutions - FAIA Assessment

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201532

The SupplierID is a unique key and cannot be duplicated within the Customer section. “0000001673” exists for 2 occurrences of SUPPLIER-TEST with different addressesOriginal entry:

<Supplier><RegistrationNumber>21778401</RegistrationNumber><Name>SUPPLIER-TEST</Name><Address>

<StreetName>ROUTE DE LONGWY 000</StreetName><City>LUXEMBOURG</City><PostalCode>1940</PostalCode><Country>LU</Country><AddressType>StreetAddress</AddressType>

</Address><TaxRegistration>

<TaxRegistrationNumber>LU12345678</TaxRegistrationNumber></TaxRegistration><SupplierID>0000001673</SupplierID><AccountID>2211000</AccountID>

</Supplier><Supplier>

<RegistrationNumber>21778401</RegistrationNumber><Name>SUPPLIER-TEST</Name><Address>

<StreetName>15 Rue de Cents</StreetName><City>Howald</City><PostalCode>2529</PostalCode><Country>LU</Country><AddressType>StreetAddress</AddressType>

</Address><TaxRegistration>

<TaxRegistrationNumber>LU12345678</TaxRegistrationNumber></TaxRegistration><SupplierID>0000001673</SupplierID><AccountID>2211000</AccountID>

</Supplier>

Proposition:

<Supplier><RegistrationNumber>21778401</RegistrationNumber><Name>SUPPLIER-TEST</Name><Address><StreetName>ROUTE DE LONGWY 000</StreetName><City>LUXEMBOURG</City><PostalCode>1940</PostalCode><Country>LU</Country><AddressType>StreetAddress</AddressType>

</Address><Address><StreetName>15 Rue de Cents</StreetName><City>Howald</City><PostalCode>2529</PostalCode><Country>LU</Country><AddressType>StreetAddress</AddressType>

</Address><TaxRegistration><TaxRegistrationNumber>LU12345678</TaxRegistrationNumber>

</TaxRegistration><SupplierID>0000001673</SupplierID><AccountID>2211000</AccountID>

</Supplier>

<AccountID> MUST refer to an Account declared in the General Leger Accounts section

AddressType is an enumeration list (“FAIA_V_2.01_reduced_version_A” Documentation Page 52)The value must be one of the items:• StreetAddress • PostalAddress • BillingAddress• ShipToAddress• ShipFromAddress

Are you FAIA ready?Our solutions - FAIA Assessment – Examples of common errors and corrections

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201533

We can assist you with the production of your FAIA file by providing Excel templates with documentation and sample files.

Each template is a step to help you build up your FAIA file:

• General Ledger accounts• Customers• Suppliers• Tax codes• Products• General Ledger entries• Invoices

Are you FAIA ready?Our solutions - FAIA Production

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201534

Based on Excel/CVS reports, we can build the FAIA file up step-by-step.At each step, we analyse the content and report any issues with data quality

Are you FAIA ready?Our solutions - FAIA Production

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201535

VAT Update – Autumn 2015

2

1

3

5

E-Archiving / E-Filing

CJEU case update

Are you FAIA ready?Our solutions

SAF-T / FAIA updateBackground and scope

4

SAF-T / FAIA updateAnother tax requirement or a business opportunity?

© 2015 Deloitte Tax & Consulting.

SAF-T / FAIA updateTax constraint or business

opportunity?

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201537

Creation of mandatory FAIA may be a tax constraint…

But it also is a business opportunity…

A simple example: using FAIA as an archiving tool

SAF-T / FAIA updateTax constraint or business opportunity?

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201538

• A major issue common to businesses is the determination of the scope of the data to bearchived and the organisation of its archival

• Usually businesses do not clearly differentiate between backups and archives

‒ Backups: Continuity of the data-processing exploitation Depends on the technical environment and its evolution Advantage: “Easy” to proceed Drawback: Necessary to preserve the technical environment in order to ensure similarity of the

information after retrival

‒ Archives: Long term availability

Advantage: Independent of the technical environment, i.e. “techno-independent“

Difficulties: Complexity of realisation (preliminary analyses, etc....) and identification of"relevant" data

Availability of data and archiving process

SAF-T / FAIA updateTax constraint or business opportunity?

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201539

• Storage of the history of the data does not necessarilymean compliance with tax requirements when:‒ Aggregated data is retained instead of detailed data; and‒ When data covers incomplete parts of the Information

System• Generally, online data in ERPs is not secured:‒ It may vary over time, weakening the quality of the

audit trail‒ It is difficult to reconcile, three or more years later,

the online data with the information filed in tax returns• Lack of testing of the restoration process of backups

or archived dataArchives

Sauvegardes

ClientsNumCliNomAdresseCodeTarif

ProduitsCodeProdDésignationCodeTVA

Taux TVACodeTVATauxTVA

EntêteFactureNumFactNumCliDateFactTotalHTTotalTVA TotalTTC

TarifsCodeTarifCodeProdPrixUnit

LigneFactureNumFactCodeProdQtéTxRemise

EntêteFactureNumFactNumCliDateFactNomAdresseTotalHTTotalTVA TotalTTC

LigneFactureNumFactCodeProdDésignationTauxTVAPrixUnitQtéTxRemise

Backups versus Archives

ExamplesDifferences in time scales between management(working today/preparing tomorrow) and tax and legal(organizing legal proof and justifying tax and legalevents three, four, five… years behind) timeframes

SAF-T / FAIA updateTax constraint or business opportunity?

Sauvegardes

Continuité de l’exploitation informatique :Tributairede son environnement. et de ses évolutions,

Point fort : « facilité » de réalisation;

Point faible : nécessité de conserver l’environnement technique (pour la restauration « à l’identique »).

Archives

Disponibilité sur le long termeNon tributaire de l’envir.

Point fort : « technico-indépendant » (pas de contrainte liée à l’environ.)

Point critique : complexité de réalisation (analyse préalable, etc.…) et sélection des données « pertinentes »

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201540

• The use of a FAIA file ensures:

• static storage • of historic data• in a standardized way

• It also results in a better quality of internal control by, potentially:

Validating / reconciling the FAIA content against the VAT returns before filing

Making sure of the nature and quality of the data that will be processed, both by businesses and by tax administrations in the event of audits

Using FAIA data to implement VAT / CIT / Controlling data analytics and improve the quality and efficiency of your internal controls

SAF-T / FAIATax constraint or business opportunity?

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201541

Q&A

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201542

Raphaël GlohrPartnerTAX-Indirect tax +352 45145 [email protected]

Christian DeglasPartnerTAX-Indirect tax +352 45145 [email protected]

Cédric Tussiot DirectorTAX-Indirect tax +352 45145 [email protected]

Antoine FarioliDirectorTAX-Indirect tax +352 45145 [email protected]

Michel LambionDirectorTAX-Indirect tax +352 45145 [email protected]

Thijl DuvalSenior ManagerTAX- Tax center+352 45145 [email protected]

© 2015 Deloitte Tax & ConsultingVAT Update | Autumn 201543

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries, Deloitte brings world-class capabilities and deep local expertise to help clients succeed wherever they operate. Deloitte's approximately 193,000 professionals are committed to becoming the standard of excellence.