timmint mi - uae insurance weekly report (issue 2014-19)

TRANSCRIPT

UAE INSURANCE

Weekly Report

Issue – 2014 Week 19

02 to the 08 of May, 2014

TIMMINT Market Intelligence UAE Insurance Weekly Report 02 to 08 May, 2014

2

From:

TIMMINT

Market Intelligence

To:

Whom it may concern

Subject:

Weekly Status Report, UAE

Insurance Industry.

Issue Year 2014, Week 19

Report Sections Page

UAE INSURANCE

NEWS 2

ABU DHABI

INSURANCE INDEX 5

DUBAI INSURANCE

INDEX 6

ABU DHABI MARKET

PERFORMANCE 7

DUBAI MARKET

PERFORMANCE 9

Who We Are Visit our website www.timmint.com

Disclaimer:

This report was prepared as an

account of work sponsored by the

Company. Certain information has

been obtained from published

sources and is given as of the dates

specified. All the information in this

publication is verified to the best of

the authors’ and publisher’s ability,

but neither the company nor the

Management Team makes any

warranty, express or implied, or

assumes any legal liability or

responsibility for the accuracy

completeness or the results of such

use of the information. All such

information is subject to change

without notice.

UAE INSURANCE NEWS

Dubai shows the way in health care

DHA is all set to help the emirate enter a new era of medical facilities and protection, making

them more credible, modern and accessible than before

To date, health care costs across the Gulf Cooperation Council (GCC) have been covered by

various governments. However, they are increasingly recognizing that they will not be able to

fund their citizens’ health care needs indefinitely and are looking at new ways of covering the

costs.

The Dubai Health Authority (DHA) has made progress on this front last

month, bringing significant and much-needed health care reforms to the

emirate. The DHA estimates that there are only one million people in Dubai

with health insurance, leaving around two million people not covered and

lacking access to even basic health care facilities.

Need of change

In light of this, change was needed and the DHA announced earlier this year a new directive for

compulsory health insurance for both residents of, and visitors to, the emirate. Under this new

framework, all residents of Dubai must be provided with at least a basic level of health

insurance by their employers and new visa applications will also require this as part of the entry

criteria.

While ensuring a positive step in protecting the health of the nation and the most vulnerable,

the new system will undoubtedly bring challenges to all parties involved. The government will

need to secure stakeholder support and understanding at many levels to ensure the

infrastructure for the transition is in place; insurance providers will need to have a consolidation

strategy ready; employers will need to look at ways to manage the new health care cost within

its organisation and be well-equipped to respond to claims; and regulators will need to look at

how the model is scalable across the region to address the health care burden at the GCC level.

New era of healthcare

In this move, Dubai aims to go from a partly insured to a 100 per cent insured society. The new

law is also an integral part of DHA’s vision and strategy to grow Dubai into a quality health care

hub, with a strong legislation and medical system and excellent hospitals, doctors and of course

equipment.

Source: Gulf News

The TIMMINT Group is

specialized in providing

professional services to the

worldwide business

community.

1 million covered

2 million uncovered

With its increasing focus on quality medicine — as well as the system to provide it —

DHA is set to make Dubai enter a new era of health care, making it more credible,

modern and accessible than ever before. The new regulations will be rolled out over the

next 18 months in several phases, with everyone entitled to at least a basic package of

cover, which must include emergency services, access to a general physician, referral to

specialists, tests and investigations, surgical procedures and maternity care.

TIMMINT Market Intelligence UAE Insurance Weekly Report 02 to 08 May, 2014

3

UAE Property/Casualty Insurance Sector Carries

Intermediate Industry and Country Risk Assessment, Says

S&P Report

Standard & Poor's Ratings Services has released further details regarding its insurance

industry and country risk assessment (IICRA) for the United Arab Emirates (UAE)

property/casualty (P/C) insurance sector (see "United Arab Emirates Property/Casualty

Insurance Sector Carries Intermediate Industry and Country Risk Assessment").

We assess industry and country risk for the UAE P/C sector as intermediate. Our assessment

reflects the risks typically faced by P/C insurers operating in the UAE, and is derived from our

view of moderate UAE country risk plus intermediate industry risk prevailing

for insurers of P/C lines of business in the country.

We assess the UAE country risk as moderate. This reflects the country's

economic risk trend, political risk, and financial system risk.

Under Standard & Poor's policies, only a Rating Committee can determine a Credit Rating Action

(including a Credit Rating change, affirmation or withdrawal, Rating Outlook change, or

CreditWatch action). This commentary and its subject matter have not been the subject of

Rating Committee action and should not be interpreted as a change to, or affirmation of, a

Credit Rating or Rating Outlook.

Source: Zawya

We assess the industry risk for the UAE P/C insurance market as intermediate, based on an

evaluation of five industry-related sub-factors. We see product risk as positive; profitability

(measured by return on equity), barriers to entry, and market growth as neutral; and the

institutional framework as weak.

Risk in UAE:

moderate

TIMMINT Market Intelligence UAE Insurance Weekly Report 02 to 08 May, 2014

4

UAE insolvency ratio lower than in Western Europe

The real insolvency ratio in the UAE is about 5-10 per cent, which is lower than most of the

developed Western European countries, according to an executive of a global credit insurance

company.

Massimo Falcioni, CEO of Euler Hermes for GCC, said insolvency claims ratio is “around 37 per

cent… but insolvency claims does not mean that they are not paying. It means there is a delay in

payment. Real insolvency is 5-10 per cent.”

According to Creditreform Economic Research Unit, insolvency in France was 28.3 per cent,

followed by 17.3 per cent in Germany, 11.4 per cent in Scandinavia and 10.6 per cent in Britain

in 2011-12.

Falcioni said this delay in payment is impacting companies because their working capital

waiting for payment gets hit. And this delay is rising especially in Saudi and UAE because

many companies in the UAE are trading outside the country in regions like Europe, where

there is a prolonged recession, Brazil and African countries.

Euler Hermes is a credit insurance company that offers bonding, guarantees and collections

services for the management of business-to-business trade receivables. Euler Hermes claims to

have a 50 per cent market share of credit insurance in the GCC.

Commenting on the impact of insolvency on Euler Hermes, Falcioni said: “Properly managed risk

will not impact our business… We have a lot of information that we gather in the field by

meeting customers before we give credit. We give credit only to those who merit for which we

have transparency of information so that we can assess and calculate the probability of default.”

He said construction and building material companies are the most sensitive with regards to

insolvency. “Risk is everywhere. There are no risk-free sectors; all the sectors are sensitive but

building materials companies’ margins are very low and competition is very strong.”

Debt collection

Commenting on debt collection, Euler Hermes CEO for GCC Falcioni said debt collection in the

region in the past year was quite difficult because some of the companies which went bankrupt

ran away from the UAE.

He said the debt collection is done not only in the region but also outside because of the nature

of the companies’ work as they are involved in trade and exports.

There are much more over dues registered so delay in payments is increasing, he said, adding

that thanks to the services of experts like Credit Insurance, this kind of issue is manageable.

Source: Emirates 24/7

Insolvency in France:

28.3%

Insolvency in Germany:

17.3%

Insolvency in Scandinavia:

11.4%

Insolvency in Britain:

10.6%

UAE Real Insolvency

ratio

5-10%

TIMMINT Market Intelligence UAE Insurance Weekly Report 02 to 08 May, 2014

5

ABU DHABI INSURANCE INDEX

Insurance Sector Performance:

The chart for Abu Dhabi Insurance Index illustrates the global performance of all Abu Dhabi insurance companies in the stock market for a period of one year, showing a year to date change of (5.57%)

Insurance Index - Year to Date Figures

Index as of 31 Dec Current Index YTD Change Indicator % Change

2,309.06 2,437.67 128.61

5.57%

Insurance Index (one year)

--- Abu Dhabi Insurance Index (ADII)

Insurance Index (last month)

--- Abu Dhabi Insurance Index (ADII)

AD Insurance vs. General Index (one year - %)

--- Abu Dhabi Insurance Index (ADII)

--- Abu Dhabi Index (ADI)

AD Insurance vs. General Index (last month - %)

--- Abu Dhabi Insurance Index (ADII)

--- Abu Dhabi Index (ADI)

TIMMINT Market Intelligence UAE Insurance Weekly Report 02 to 08 May, 2014

6

DUBAI INSURANCE INDEX Insurance Sector Performance:

The chart for Dubai Insurance Index illustrate the global performance of all Dubai insurance companies in the stock market for a period of one year, showing a year to date change of (0%)

Insurance Index - Year to Date Figures

Index as of 31 Dec Current Index YTD Change Indicator % Change

2,402.31 2,503.77 101.46

0%

Insurance Index (one year)

Insurance Index (last month)

DFM Index (one year)

DFM Index (last month)

Insurance Index - 52 Weeks Price

High Date Low Date Current Price

2,787.53 21/1/2014 1,950.00 8/9/2013 2,503.77

TIMMINT Market Intelligence UAE Insurance Weekly Report 02 to 08 May, 2014

7

ABU DHABI MARKET PERFORMANCE

The table hereunder reflects the performance of the 17 listed insurance companies in Abu Dhabi stock market during the week:

Companies Previous Closing

Close High Low Price Change No. of

Trades Volume Value

Value %

Abu Dhabi National Takaful Co. PJSC 7.20 - - - - - - - -

Abu Dhabi National Insurance Co. 7.00 6.30 6.30 6.30 (0.70) (10.0) 1 30,000 189,000

Al Ain Al Ahlia Insurance Co. 45.00 - - - - - - - -

Al Buhaira National Insurance Company 2.85 - - - - - - - -

Al Dhafra Insurance Co. 6.50 - - - - - - - -

Al Khazna Insurance Co. 0.87 0.80 0.80 0.80 (0.07) (8.05) 1 1,585 1,268

Al Wathba National Insurance Co. 5.35 - - - - - - - -

Emirates Insurance Co. 8.00 - - - - - - - -

Fujairah National Insurance Co. 300.00 - - - - - - - -

Green Crescent Insurance Company 1.20 1.11 1.17 1.06 - - 12 135,723 154,965

Insurance House P.S.C 1.40 - - - - - - - -

Methaq Takaful Insurance Co. 1.48 1.43 1.55 1.40 0.05 3.38 186 6,033,261 8,920,501

National Takaful Company 1.23 1.14 1.14 1.12 0.02 1.79 4 135,169 152,689

Ras Al-Khaimah National Insurance 3.18 - - - - - - - -

Sharjah Insurance Company 4.05 - - - - - - - -

Union Insurance Company 1.05 1.10 1.10 1.10 0.05 4.76 1 26,216 28,838

United Insurance Co. 2.00 - - - - - - - -

This chart shows the companies that had the highest

increase in % of change in the stock price over the week

This chart shows the companies that had the highest

volume over the last week.

4.76

3.38

1.79

Union Insurance Company Methaq Takaful InsuranceCo.

National Takaful Company

% change in price

MethaqTakaful

InsuranceCo.

GreenCrescentInsuranceCompany

NationalTakaful

Company

Abu DhabiNational

InsuranceCo.

UnionInsuranceCompany

6,033

136 135 30 26

Top 5 Most Active by Volume (last week)

TIMMINT Market Intelligence UAE Insurance Weekly Report 02 to 08 May, 2014

8

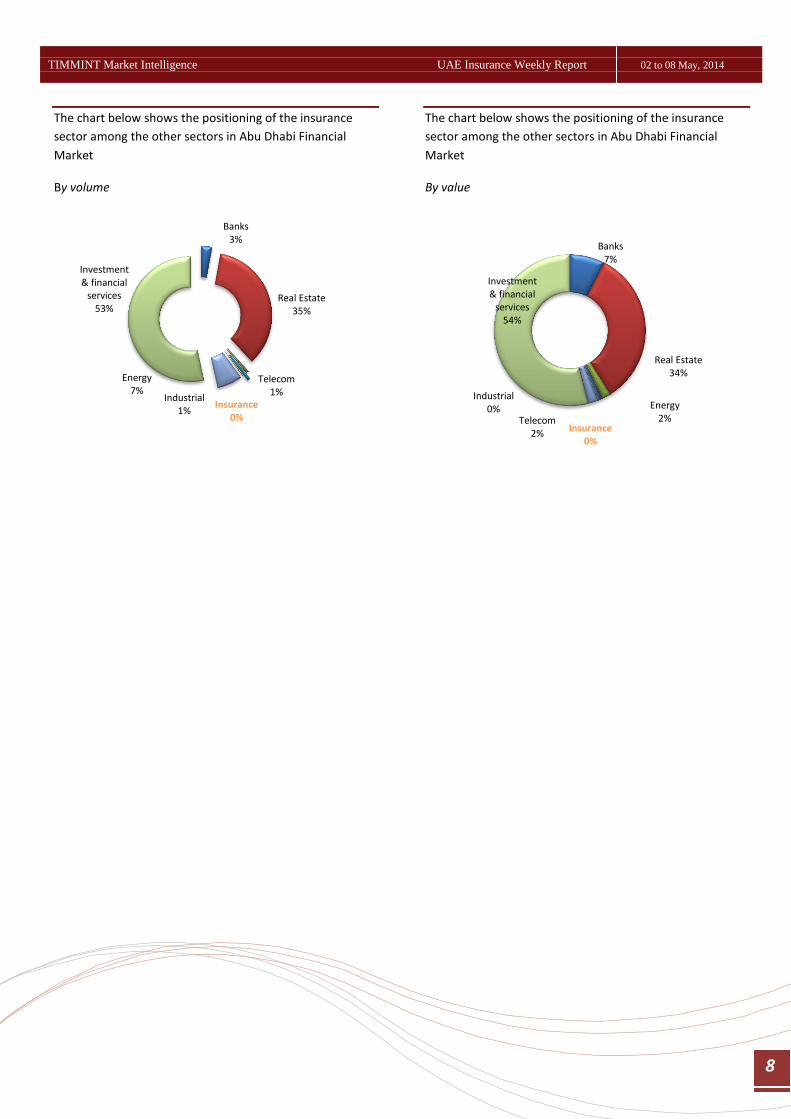

The chart below shows the positioning of the insurance

sector among the other sectors in Abu Dhabi Financial

Market

By volume

The chart below shows the positioning of the insurance

sector among the other sectors in Abu Dhabi Financial

Market

By value

Banks 3%

Real Estate 35%

Telecom 1%

Industrial 1%

Insurance 0%

Energy 7%

Investment & financial

services 53%

Banks 7%

Real Estate 34%

Telecom 2%

Industrial 0%

Insurance 0%

Energy 2%

Investment & financial

services 54%

TIMMINT Market Intelligence UAE Insurance Weekly Report 02 to 08 May, 2014

9

DUBAI MARKET PERFORMANCE

The table hereunder reflects the performance of the 13 listed insurance companies in Dubai stock market during the week:

Companies Previous Closing

Close High Low Price Change No. of

Trades Volume Value

Value %

Al Sagr National Insurance Company - - - - - - - - -

Alliance Insurance - - - - - - - - -

Arab Insurance Group P.S.C. 1.70 - 1.70 - - - 2.00 4,307 7,276

Arabian Scandinavian Insurance - - - - - - - - -

Dubai Insurance Co , PSC - - - - - - - - -

Dubai Islamic Insurance and Reinsurance

Co.

1.17 1.16 1.24

1.13

0.01 0.85 256.00 10,739,081 12,651,982

Dubai National Insurance & Reinsurance 3.60 - 3.60 - 0.35 9.72 7.00 51,601 169,157

Islamic Arab Insurance Company 1.10 1.13 1.23

1.10

0.03 2.73 1,544.00 127,607,502 149,241,846

National General Insurance Company PSC - - - - - - - - -

Oman Insurance Company (P.S.C.) - - - - - - - - -

ORIENT Insurance PJSC - - - - - - - - -

Takaful Emarat (PSC) 1.14 1.14 1.23

1.02

- - 463.00 21,096,940 23,938,960

Takaful House 1.08 1.07 1.14

1.02

0.01 0.93 295.00 11,197,075 12,068,306

This chart shows the percentage change in price of Dubai

insurance companies over the last week.

This chart shows the top insurance companies that were

the most active by volume over the last week.

9.72

2.73

0.93 0.85 0

Dubai NationalInsurance &Reinsurance

Islamic ArabInsuranceCompany

Takaful House Dubai IslamicInsurance andReinsurance

Co.

Takaful Emarat(PSC)

% change in price

Islamic ArabInsuranceCompany

Takaful Emarat(PSC)

Takaful House Dubai IslamicInsurance andReinsurance

Co.

Dubai NationalInsurance &Reinsurance

127,608

21,097 11,197 10,739

52

Top 5 Most Active by Volume (last week)

TIMMINT Market Intelligence UAE Insurance Weekly Report 02 to 08 May, 2014

10

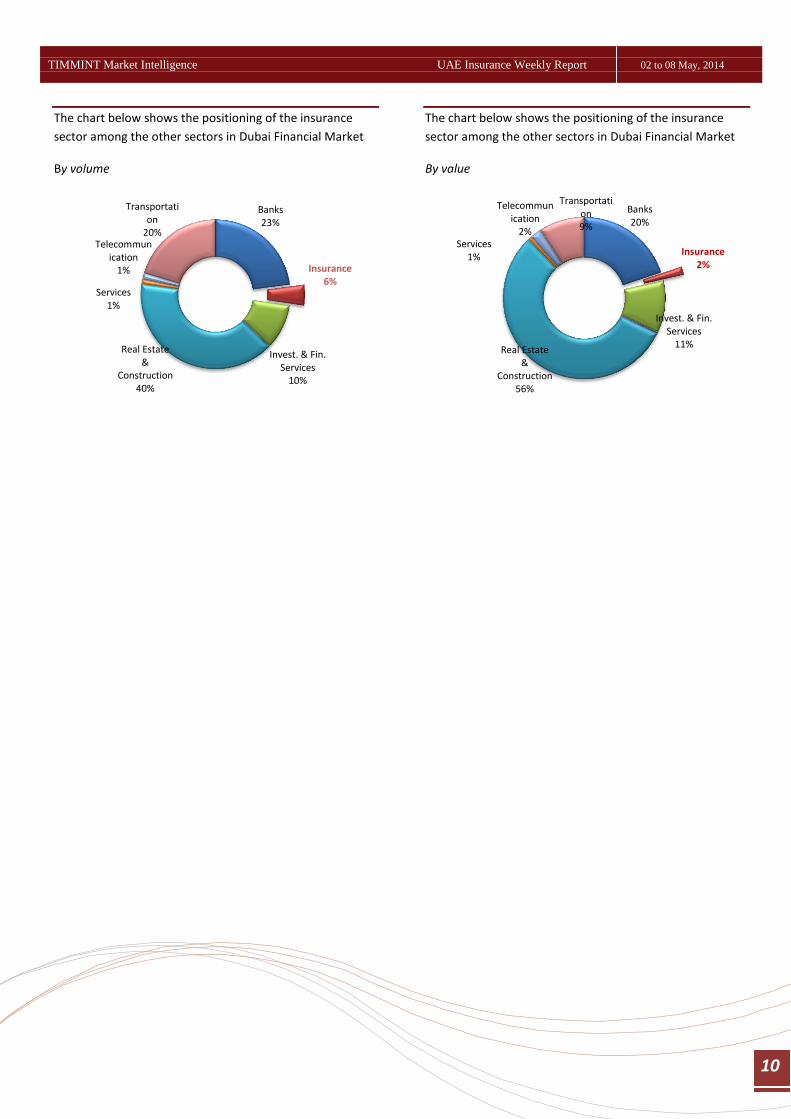

The chart below shows the positioning of the insurance

sector among the other sectors in Dubai Financial Market

By volume

The chart below shows the positioning of the insurance

sector among the other sectors in Dubai Financial Market

By value

Banks 23%

Insurance 6%

Invest. & Fin. Services

10%

Real Estate &

Construction 40%

Services 1%

Telecommunication

1%

Transportation

20%

Banks 20%

Insurance 2%

Invest. & Fin. Services

11% Real Estate

& Construction

56%

Services 1%

Telecommunication

2%

Transportation 9%

TIMMINT Market Intelligence UAE Insurance Weekly Report 02 to 08 May, 2014

11

Office – LEBANON

Scan the

QR code

for our

contact

details