title customer valuation and value-based strategies ervin

TRANSCRIPT

Title Customer Valuation and Value-Based Strategies

Author(s) Ervin, Kirke; 平敷, 徹男

Citation 琉球大学経済研究(78): 81-130

Issue Date 2009-09

URL http://hdl.handle.net/20.500.12000/14251

Rights

Customer Valuation and Value-Based Strategies

Ervin Kirke

TABLE OF CONTENTS

I. INTRODUCTION 82

E. THE RELATIONSHIP MARKETING PARADIGM 83

m. THE VALUATION OF CUSTOMERS 84

A. Customer Value 85

B. Customer Valuation 86

C. Valuation Data and their Sources 87

IV. APPROACHES TO CUSTOMER VALUATION 91

A. Implementation of Customer Value Models 91

B. Recency, Frequency, Monetary (RFM) Analysis 93

C. Customer Profitability Analysis (CPA) 98

D. Time-Driven Activity-Based Costing (ABC) 102

E. Customer Lifetime Value (CLV) 105

F. Share Of Wallet (SOW) Analysis 112

V. VALUE-BASED STRATEGIES 113

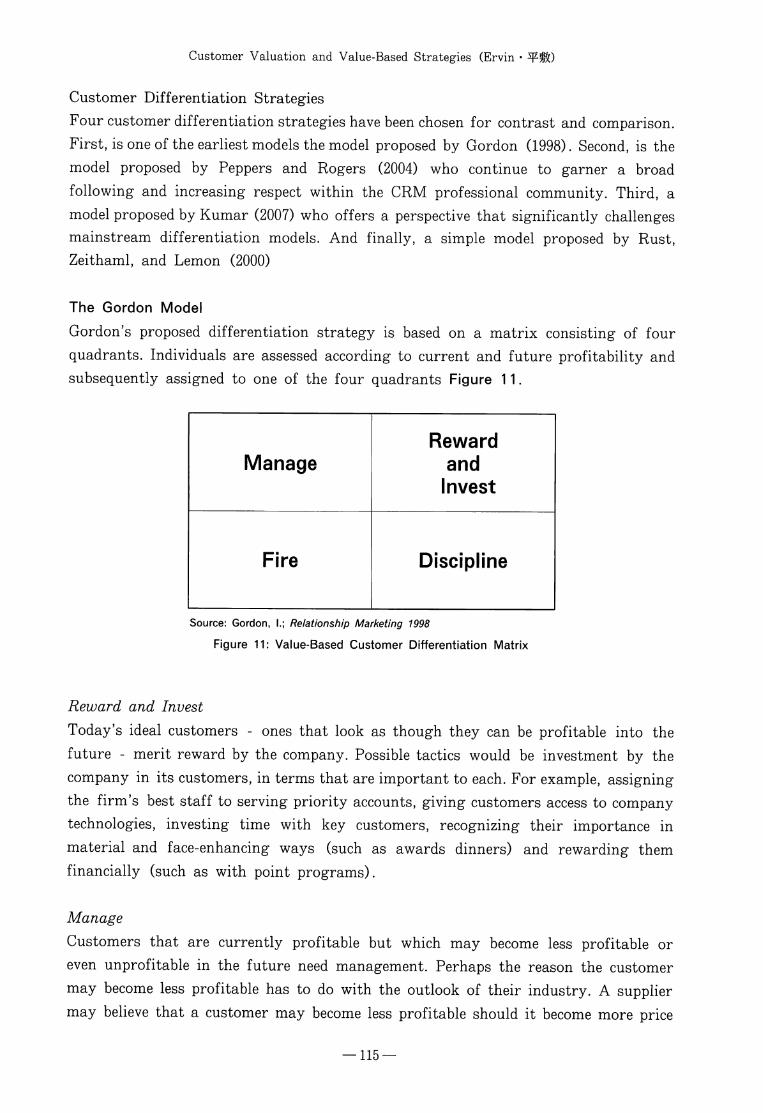

A. Value-Based Customer Differentiation 113

B. Allocation of Marketing Resources 120

VI. CONCLUSIONS 124

VE. FUTURE CONSIDERATIONS 126

W. REFERENCES 127

— 81 —

2009^9^

INTRODUCTION

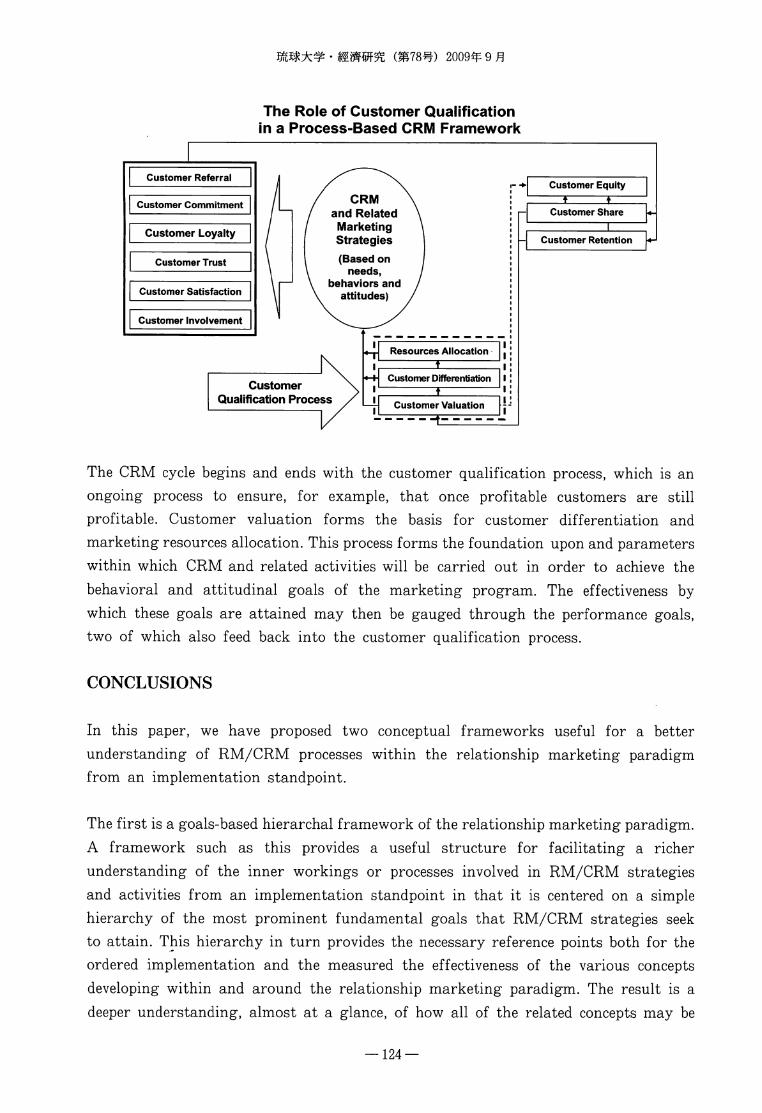

This paper proposes two separate frameworks. The first is a goals-based hierarchal

framework which conceptualizes the integration of the various related disciplines

that have developed within and around the relationship marketing paradigm. The

second is a procedural framework for the customer qualification process based

largely on a survey of extant academic literature.

We will begin with a brief background concerning the relationship marketing paradigm,

and the role and present circumstances surrounding CRM. We will then present a

proposed goals-based framework and its constituent elements. Next, We posit a survey

of extant academic literature on customer valuation methodologies and approaches

which will be the main focus of this paper. Finally, we will end with a proposed customer

qualification framework for the valuation and differentiation of customers, and the

optimized allocation of marketing resources based on customer value.

The second framework, which aims to provide a meaningful point of departure for a

deeper and broader understanding of the customer qualification process which is

necessary for gauging the feasibility of investing in long-term customer relationships,

consists of a customer valuation model and two subsequent value-based strategies;

customer differentiation and allocation of marketing resources. In order to maintain

focus on the valuation processes and their key components and characteristics,

complex computations are not expounded upon however relevant equations are

offered for the sake of clarity. The resulting framework model illustrates how the

qualification process forms the prerequisite foundation for CRM related goals and

strategies. The scope of this paper is limited to the treatment of current

customers, and does not consider the acquisition of new or former customers.

The concept of customer qualification is not new. Gronroos (1994) stated that the

function of relationship marketing is not seeking the retention of all customers but

rather making every relationship with the customer profitable. He later pointed out

in particular that relationships between the buyer and the seller must be profitable;

therefore customers must first be assessed according to the value created by them

for the company, and only later other marketing instruments can be applied for the

deepening of their "knowledge" - to determine the trends of their customer behavior

and needs for the goods/services provided (Gronroos, 1997).

— 82 —

Customer Valuation and Value-Based Strategies (Ervin

THE RELATIONSHIP MARKETING PARADIGM

Relationship marketing has undoubtedly become the dominant paradigm in marketing

today. Even publishers are demanding a steep inclination to relationship marketing in

all introductory textbooks (Hennig-Thurau 2000). And with its dominance, customer

relationship management (CRM) has emerged as its central focus. Global CRM

expenditures have reached $U.S.14 billion annually (24-7 Press Release 2008).

However, as Gupta and Lehman (2005) point out, while some companies have used CRM

databases with spectacular results, most have failed, and that many studies show

that 55-75% of all CRM initiatives have neither strengthened customer relationships nor

shown any significant return on investment. (See for example, Caulfield 2001; Day

2002; Dignon 2002; Mellow 2002; Rigby and Ledingham 2004) This can be largely

attributed to the apparent unawareness of the importance of beginning with gaining

a thorough understanding of the customer valuation process to ensure the selection

and effective implementation of viable CRM strategies and approaches, rather than the

integration of supporting IT infrastructure. Without a clear understanding of the

customer valuation process and the necessity of gradualness and care in its

implementation, many CRM efforts will be doomed to failure for some time to come.

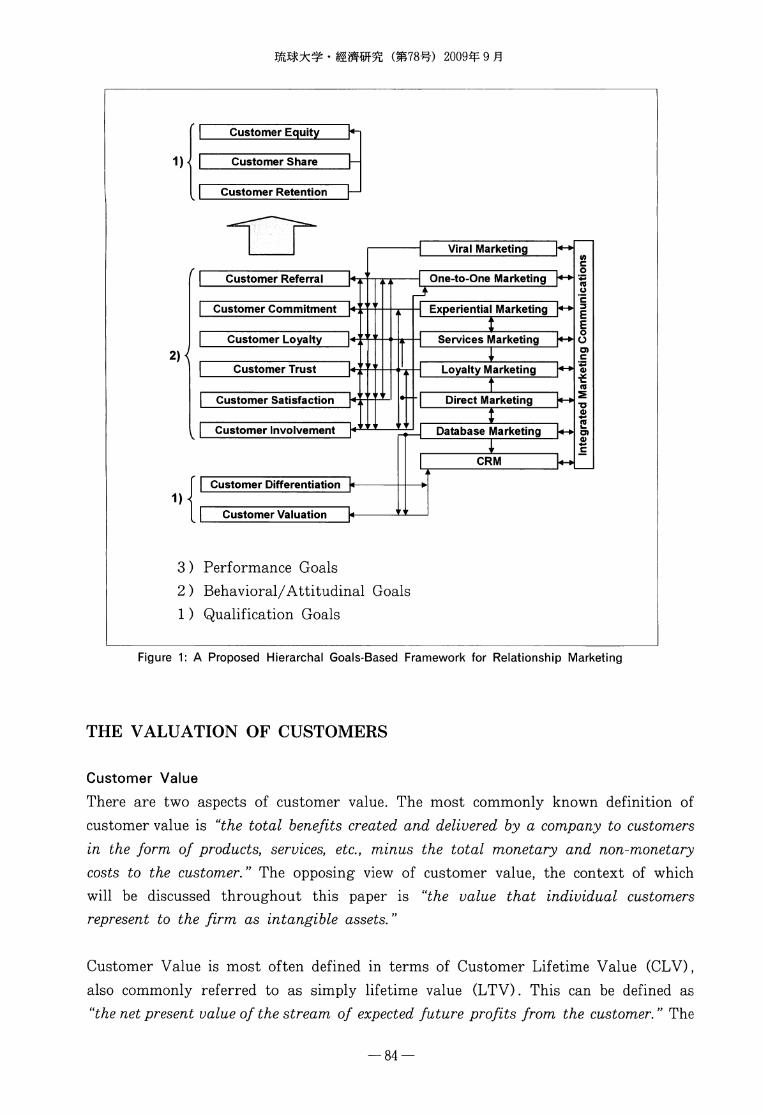

After reviewing the literature on the various disciplines or "components" of relationship

marketing, it became apparent that in order to conceptualize a strategic framework

that would consider their order of implementation, some point or points of reference

would be required on which to base any assumptions. Since goals and objectives are

the bases for all effective strategies, and the framework that was to be conceptualize

needed to be both strategic in nature and viewed from an implementation standpoint,

the next task was to determine through further review of the literature, the most

prominent goals of the relationship marketing paradigm. As a result of this review,

eleven customer-based goals were identified which were considered essential to the

success of any relationship marketing program or CRM effort (Figure 1 ). For further

clarity, these goals were categorized into three types: Qualification goals (customer

valuation and customer differentiation); behavioral/attitudinal goals (customer

involvement, customer satisfaction, customer trust, customer loyalty, and customer

referral); and performance goals (customer retention, customer share, and customer

equity). The latter two categories (behavioral/attitudinal, performance) recur

extensively in recent literature in particular. The qualification goals, however, are

treated less extensively. Specifically customer valuation, though emerging as a focal

point of recent research still appears to be widely misunderstood by many academics

and marketers, alike This is ironic because customer valuation strikes at the one of

the root principles of relationship marketing, which is to form "profitable" long-

term relationships and avoid "unprofitable" ones.

— 83 —

2009^ 9 n

| Customer Equity

Customer Share

Customer Retention |—'

| Customer Referral

| Customer Commitment

| Customer Loyalty |«+- p

Customer Trust

| Customer Satisfaction

I Customer Involvement

H Viral Marketing >-»

-| One-to-One Marketing |*

1)

| Customer Differentiation |+

Customer Valuation

\ Experiential Marketing |«-»

-| Services Marketing |«-»

■] Loyalty Marketing |

t| Direct Marketing p

1■I Database Marketing |«-»

CRM

3) Performance Goals

2) Behavioral/Attitudinal Goals

1) Qualification Goals

Figure 1: A Proposed Hierarchal Goals-Based Framework for Relationship Marketing

THE VALUATION OF CUSTOMERS

Customer Value

There are two aspects of customer value. The most commonly known definition of

customer value is "the total benefits created and delivered by a company to customers

in the form of products, services, etc.f minus the total monetary and non-monetary

costs to the customer." The opposing view of customer value, the context of which

will be discussed throughout this paper is "the value that individual customers

represent to the firm as intangible assets."

Customer Value is most often defined in terms of Customer Lifetime Value (CLV),

also commonly referred to as simply lifetime value (LTV). This can be defined as

"the net present value of the stream of expected future profits from the customer." The

— 84 —

Customer Valuation and Value-Based Strategies (Ervin

term "profits" is often substituted by the terms "financial contribution/7 "contribution

margins" or just "margins," and in some cases "benefits" in the various literature. Net

present value is a financial term that takes into account the fact that the value of

a particular currency today will not be worth the same in the future. Therefore, in

order to calculate future cash flows accurately, they must be discounted to reflect

their present value.

Peppers and Rogers (2004), expands the definition of customer value to be viewed as

being comprised of two distinct concepts - actual value and potential value. They describe

actual value as the customer's value as an asset to the enterprise, given what is currently

known or predicted about their future behavior assuming there are no major

changes in the marketing environment. This is equivalent to the CLV definition

above. Potential value is all the value that this customer could represent if the firm

were to apply a conscious strategy to improve it by changing the customer's future

behavior in some way. According to this view, the value of a customer can be

thought of not only as a function of the customer's own inertia (i.e. what the customer

is currently spending and intends to continue spending), but also of whatever

changes in the customers future purchasing behavior could be brought about

through the marketer's own initiative. (Jill Collins; Convergency Case Study in

Peppers & Rogers 2004, p. 128). From a similar perspective, potential value can be

viewed as the gap between a firm's share of wallet for a given customer and that

customer's total wallet size for a given product or service category.

McNab (2005) describes three other measurements of customer value; Present value,

Current value, and Historic value. Present value, like CLV, is a future oriented

measurement, which typically considers the future revenue and cost streams of the

customers existing business. This measure is usually only extended to include the

contractual lifetime of ongoing products or services. Revenues and costs are projected

into the future and then discounted to the present as with customer lifetime value.

Current value looks to a shorter time frame, often a month, in order to coincide

with reporting cycles. Current value is often volatile, since cyclical factors in the

relationship are often not reflected within a single month.

Historical value of a customer reveals the value earned for a customer relationship

over an extended period of time, such as prior fiscal quarter, prior year, or since the

beginning of the relationship. It can be measured as a simple average of previous

periods or can be weighted, placing higher emphasis on recent periods.

— 85 —

2009^ 9 n

Customer Valuation

Meckley and Toscano (2005) defines customer valuation as the analytical process of

increasing knowledge of customers, at various levels, in order to determine and

improve the value of customer relationships, interactions with customers or corporate

programs. Understanding the value of customers affects every aspect of the way a

business interacts with customers. It requires an in-depth understanding of customer

behavior, as well as using past behavior to predict future actions. As such, customer

value analysis is often performed in conjunction with a customer data warehouse

and customer analysis where detailed historical behavior can be tracked to predict

trends and actions (Kinekin 2001). It also requires understanding and anticipating

customer needs, and developing strategies and approaches that serve these needs in

a way that is affordable to the organization. (Carlin 2007).

At an individual level, sales and service approaches can be tuned to manage the

growth of customer relationships. The enterprise can devote the greatest portion of

its internal resources to serving its most valuable customers, determine how to keep

customers longer, grow them into bigger customers, make them more profitable, and

serve them more efficiently (Kinikin, 2001; Peppers and Rogers 2004; Carlin 2007).

Watching for shifts in the customer value itself can reveal changes in customer

behavior. Early intervention to reward higher value activities or address customer

dissatisfaction is often key to maintaining or enhancing customer value. This

approach is most effective in industries with highly predictable periodic customer

purchases, such as retail. It can also be used in many business sales with fairly

predictable upgrade or replacement cycles, such as high-tech and heavy manufacturing,

or on an aggregate basis to track the relative value of different customer segments.

(Kinekin 2001)

Predicting the value of a customer can also be an important part of deploying

marketing campaigns. Two prospects may both have the same percentage of

responding to a company's offer, but prospect "A" might generate $10 in profits

while prospect "B" might generate $50 in profits. While the cost of acquiring each

prospect might be the same, the impact to the bottom line is very different.

At a segment level, customer value analysis can identify gaps between actual value

and potential value (Kinekin, 2001). It can show both what customers do buy, and

what they could buy, based on their likely purchase levels in the product categories

being evaluated. For example, in two different SIC codes, companies of equal size

may purchase from a given supplier, an equal amount on average. Through customer

analysis, it can be determined that one SIC code uses five times more of the product

than the other, but it is penetrated more heavily by competitors. It is thus possible

— 86 —

Customer Valuation and Value-Based Strategies (Ervin

to quantify the difference between these groups, and target large potential buyers

who otherwise may have been ignored. (Weber 2008)

Firms can also identify customer/client behaviors and interactions based on a customer

segment and attach a financial component to each type (Carlin 2007). Channels of

interaction and their associated costs, for example, vary widely. While interaction via

internet is currently the cheapest channel by far, the use of sales force is the most

expensive. Purchase behavior such as recency, frequency and amount of purchase

provide valuable insight for segmentation decisions based on behavior as well.

Further, value analysis allows the firm to understand the relative value of current

customers and identify and seek ways to eliminate those customers that will never

be profitable (Kinekin 2001). From a promotional standpoint, direct marketing, sales

and Web information can be tailored to a retention or growth strategy at a segment

level as well (Peppers and Rogers 2004).

In summary, customer value can be viewed in terms of revenue, behavior (i.e.,

responsiveness, purchase frequency, channel usage), profitability, and other non-

monetary contributions to the firm. It can be viewed as historic (past), current or

future; actual or potential. Valuation approaches are also varied, and can be

operationalized at the individual, segment or management level. While important

points will be acknowledged concerning each of these levels, the main focus of this

paper is centered on customer valuation at the individual level. A detailed discussion of

various approaches and their limitations will be discussed in detail in the following

chapter.

Valuation Data and their Sources

Understanding the value of each customer is critical to balancing the value between a

business and its customers. The process of understanding this value begins by creating

a consolidated source of customer information such as a data warehouse. Because of

the potential expense and time required to create sophisticated LTV models, proxy

variables that allow initial rank-ordering of customers by value are a good starting

point. Then, as an enterprise evolves in its CRM capabilities and its metrics mature,

it typically moves from simply measuring sales revenue to measuring profitability,

and even measuring potential profitability and other useful qualitative values such

as customer referral value, collaboration value, etc. The ultimate goal is to model the

actual lifetime value of each customer, as well as the customer's potential value.

Firms often find that starting with overlay data is a low-risk first step. These overlay

data are then enriched over time with basic scores and segmentation. Integrating actual

behavioral data not only provides tremendous value for marketing and personalization,

but also for strengthening and expanding upon scores, segmentation, and value

— 87 —

(^78^) 2009^ 9 n

assessment metrics. In general, explicit dialogue information is one of the last (but

potentially most powerful) categories of data collected and applied to managing

customer relationships. (Peppers and Rogers 2004)

Customer valuation naturally requires software and storage for the data. Although

initially, calculations can be achieved using a simple spreadsheet program (Peppers

and Rogers 2004; Novo 2004), meaningful CLV measurements, especially for larger

firms with many customers, will eventually require a marketing database (data

warehouse). Databases vary in capacity and cost. For many small businesses, an

"off the shelf" database program may suffice, whereas a medium-sized or larger

business will invariably require a third party database of significant size in the long run.

Most importantly, firms should minimize IT spending for CRM until they understand

the processes that the software is designed to support (Rigby and Ledingham 2004).

Before actually constructing the data warehouse, the first step in customer valuation

would be to define the customer type(s) served by the firm. Gupta and Lehman

(2003) point out that defining the customer properly is a fundamental and critically

important step that is often not given the proper attention by marketers. The term

"customer" should first be carefully defined either as an individual, household, company,

or division, etc. who has purchased or ordered something from, or registered with

the firm. Many banks, for example, consider their relationships being built with

households - that is - they defined their relationships in terms of the number of

products sold to customers with a common account address. Large companies with

multiple branches will either order their products centrally, or each branch will

order supplies individually. In this case, the supplier must decide whether to treat

each branch as separate customers or treat the company as one large customer.

Furthermore, the account name may well be the name of the organization, but the

actual customer may be an engineer, a purchasing agent, or even some cross-functional

team within the organization. Another factor involved with defining customers is

initial purchase volume. In a B2B setting, for example, if an organization's initial

purchase is substantially large, in that the supplies purchased will likely be consumed

over time, that organization can safely be considered a customer worth retaining. On

the other hand, if the initial purchase is negligible, this organization is probably just

evaluating the product for whatever its own purposes may be. This organization

would probably be better classified as a prospect, and more research performed as to

its needs and purchasing motivations. Customers must also be defined as contractual or

non-contractual. This is very important because the valuation metrics may be different

for each of these classifications. With contractual customers, a critical metric for

valuation is the customer retention rate. However, for non-contractual customers

retention rate has much less meaning, and thus a different metric such as recency

Customer Valuation and Value-Based Strategies (Ervin

or P (Active) will probably become the most important metric.

Once the enterprise has clearly defined its customer types, the next step is to identify

its customers. For business-to-business relationships, this can easily be done through

contract, billing, or shipping information. However for consumer relationships,

customers may have to be asked to divulge some type of information to be used as an

identifier, such as a combination of name and address or name and phone number, etc.

Credit card payments and web site visits are also possible methods. Each customer

should be identified and recognized at every touch point in order to more accurately

measure purchaes and other behavior. The linking of that information allows the

company to see each customer completely, as one customer throughout the organization,

and enables a company to compare, or differentiate customers from one another.

(Peppers and Rogers 2004)

Once the customer types have been defined and the individual customers identified,

another important step is to decide how the data which will be used in the selected

valuation model will be classified. There are various ways of classifying customer

data. The following examples are provided to illustrate the various perspectives from

which an organization may view the data and their possible uses.

In their earlier works, The One to One Field Book (1999), Peppers and Rogers postulated

the following four categories:

1. Current facts and figures

2. Imputable and Computable Customer Data

3. Observable Customer Data

4. Obtainable Customer Data

In their most recent work, Managing Customer Relationships (2004), they offer the

following three major classifications for customer data:

1. Overlay Information

2. Actual Behavior Data

3. Dialog Information

Shepherd (1999) classifies data directly supplied by the customer into three types:

1. Behavioral data,

2. Attitudinal data,

3. Demographic (i.e. "descriptive")

— 89 —

(^78^) 2009^ 9 ft

Vavra (1992) provides an extensive list of the types of customer data which can be used

in a customer information file for both consumers and business-to-business customers:

1. Identification

2. Customer Rating

3. Background

4. Pre-Sale Communication

5. Purchase Behavior

6. Post-purchase behavior

7. Decision Makers (B2B)

8. Decision Making (B2B)

9. Influences (B2B)

10. Post-purchase behavior

11. Predicted Behavior

12. Channels (B2B)

13. Pricing (B2B)

14. Creditworthiness

15. Attitudes and Perceptions

16. Selected Relevant Information

Further, data used in calculation of customer value can be categorized as either

quantitative or qualitative. Although, the computation of quantitative data is relatively

straightforward, qualitative data must be weighted in a way that will provide accurate

and meaningful input to the lifetime value calculation. Customer referrals, for example

could be weighted not only to according monetary value, but also to frequency, as

well as the resulting CLV of the customer (s) referred. A customer's suggestion for

a new or modified product design may be itself qualitative in nature, however, once

implemented and offered to other customers, its value could be quantified in terms

of acceptance, sales, or costs.

Once the customers have been defined, the data classifications have been determined,

and the database constructed accordingly, customer data can be collected from their

sources.

Data sources can be classified into three types (Peppers and Rogers 2004):

1. Data generated from internal operations

Data generated from internal operations, which can make significant contributions,

include transaction details, information relating to billing and accounting status,

customer service interactions, back orders, product shipment, product returns,

— 90 —

Customer Valuation and Value-Based Strategies (Ervin

claims history, and internal operating costs. This type of information can

significantly affect an enterprise's understanding of its customers.

2. Data directly supplied by the customer

Directly supplied data consists of data obtained directly from customers, prospects,

or suspects. It is generally captured from lead generation questionnaires, customer

surveys, warranty registration cards, customer service interactions, website

responses, interviews, focus groups, or other direct interactions with individuals.

3. Data supplied by third parties

B2C customer information can be purchased or rented from any number of com

mercial databases. Trade publications, research services, online business-

information services, and individual company annual reports and/or websites can

also be consulted for usable customer data.

As can be seen by the above examples, which are by no means exhaustive, there is

virtually no limit to the amount and types of data that can be collected on individual

customers. There are also numerous internal and external sources from which to access

that data as well. On the other hand, however, there are two very important points

to be kept in mind when considering the collection of data. First, in order to load

the valuation model with meaningful data, the firm must first define and identify its

customers. Secondly, to control costs, internally generated data should be used first,

and only data that will be used should be collected. As Khan (1998) pointed out,

unless companies start to make use of the information they collect, there seems to

be little justification for collecting it. Furthermore, the costs of data collection

frequently outweigh the advantages gained (O'Malley 1998). Therefore, this aspect

of data collection must also be monitored to avoid cost overruns.

APPROACHES TO CUSTOMER VALUATION

Implementation of Customer Value Models

The Customer Lifetime Value model has become the most widely accepted method of

measuring individual customer value (Peppers and Rogers 2004). Most statistical

variations offer much more precise and thorough measurements than other valuation

methods. But calculating the precise value of customers can be a tricky process.

Companies have found that going directly from mass-marketing measures to actual

customer value is too large of a chasm to cross all at once. The time and expense

that is required to understand the revenue, fixed and variable costs, and margins

associated with every interaction can be overwhelming. A series of steps is often

taken prior to developing an actual customer value calculation. While lifetime value

— 91 —

2009^ 9

is the variable an enterprise wants to know, the enterprise may first find some

proxy variable that allows initial rank-ordering of customers by value to be nearly as

useful as a good starting point. A proxy variable should be easy to measure, but it

obviously will not provide as clear a picture when it comes to qualifying a customer's

actual or potential value.

Customer valuation can be conducted in various ways. In general, a company can

begin by tracking the total revenues of individual customers over a given period of

time. While an estimated value such as RFM can be a good start, an actual value,

calculated by customer, is desirable. Subtle differences between estimated value and

actual profitability can cause a person to make different decisions. (Peppers and

Rogers 2004)

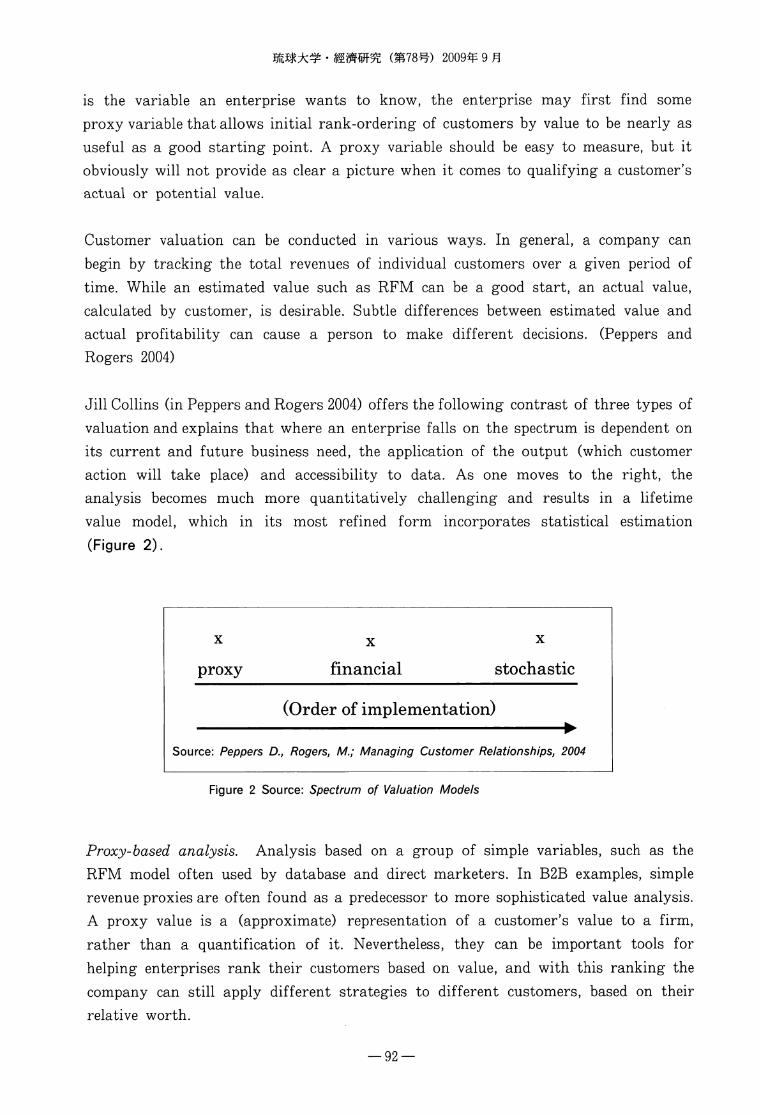

Jill Collins (in Peppers and Rogers 2004) offers the following contrast of three types of

valuation and explains that where an enterprise falls on the spectrum is dependent on

its current and future business need, the application of the output (which customer

action will take place) and accessibility to data. As one moves to the right, the

analysis becomes much more quantitatively challenging and results in a lifetime

value model, which in its most refined form incorporates statistical estimation

(Figure 2).

x

proxy

x

financial stochastic

(Order of implementation)

Source: Peppers D., Rogers, M.; Managing Customer Relationships, 2004

Figure 2 Source: Spectrum of Valuation Models

Proxy-based analysis. Analysis based on a group of simple variables, such as the

RFM model often used by database and direct marketers. In B2B examples, simple

revenue proxies are often found as a predecessor to more sophisticated value analysis.

A proxy value is a (approximate) representation of a customer's value to a firm,

rather than a quantification of it. Nevertheless, they can be important tools for

helping enterprises rank their customers based on value, and with this ranking the

company can still apply different strategies to different customers, based on their

relative worth.

— 92 —

Customer Valuation and Value-Based Strategies (Ervin

Financial analysis. A quantitative analysis based on revenue, and if possible, cost

information at the individual level. Discounted cash flow or other spreadsheet models are

used. Likely to be used for hospitality (hotels), automotive, some B2B, and others.

Statistical analysis. Builds on proxy-based analysis and financial analysis. In calculating

discounted cash flows, assumptions are made as to the length of a customers relationship

and future growth. Statistical analysis incorporates a more rigorous analysis behind

these assumptions, such as estimating the probability to purchase. Variables used in

the estimation could be those adopted in the earlier stages of customer valuation

with proxy-based analysis. Most likely found in a company with tens of millions of

data points, such as credit card companies or telecommunications firms.

Recency, Frequency, Monetary (RFM) Analysis

Because of the highly technical nature of RFM, for which a true understanding

requires a thorough knowledge of database technology, an exhaustive explanation is

beyond the scope of this paper. However, a certain degree of description is warranted in

order to facilitate a better understanding of how it may be used as a proxy customer

valuation tool. The overview and explanations of coding procedures are extracted

from Hughes (2006), and the individual characteristics of each attribute were compiled

from the works of Libey and Pickering (2005). The contributions of other authors

are cited as they appear. Our own remarks are either introductory to, or fall at the

end of a paragraph in order to illuminate the relevance to customer valuation or related

strategies when the relationship may not appear to be obvious. We conclude this section

with a brief list of RFM limitations.

RFM (Recency, Frequency, and Monetary) works with both consumer and B2B

customer files. It works in any type of industry in which firms communicate with

their customers for marketing purposes. However, it only works with customer files.

It cannot be used with prospects because it requires knowledge of the customer's

prior purchase history with the firm. Prospects, by definition, have no such history.

Recency refers to the most recent purchase, order, visit or other desirable action by

the customer. Frequency refers to the frequency of those actions performed within

that time period. Finally, Monetary indicates the total (or average) amount of

goods or services purchased during the same time period

In preparation for an RFM analysis, the database must be "coded" for each attribute

(recency, frequency, and monetary amount).

Coding for Recency, Frequency and Monetary

In order to code the customer base for Recency, it is first necessary for one vital

— 93 —

2009^ 9

piece of information to be stored in every customer's database record: the most recent

purchase date. Every time the database is updated, this date must be updated as

well. To create the Recency code, the entire database must be sorted by this date,

with the most recent at the top. The database is then divided into five exactly equal

parts, or quintiles, which are numbered from 5 (most recent) to 1 (most ancient) as

shown in Figure 3. Next, each customer record in the database is coded anywhere

from one to five according to the group that they fall into.

The criterion for deciding Recency will differ among industries. A telephone company,

for example couldn't use the payment date because all customers would end up having

the same code. Therefore, the last time they changed their service (added or dropped

a line, signed up for a cell phone service, etc.), would be the Recency in that case.

A Bank on the other may use the last time a customer opened an account or bought

financial products.

11/04/2005

Most recent

purchase date

06/09/1998

Recency

quintile

codes

Source: Hughes, A; Strategic Database Marketing, 2006

Figure 3: Sorting by Recency

The process for sorting and coding the database records for Frequency is identical

to that for recency. However, the information used here is the total (or average)

number of purchases from each customer during a given period (Figure 4).

3,254

Total products

purchased

per period

Frequency

quintile

codes

Source: Hughes, A; Strategic Database Marketing, 2006

Figure 4: Sorting by Frequency

— 94 —

Customer Valuation and Value-Based Strategies (Ervin

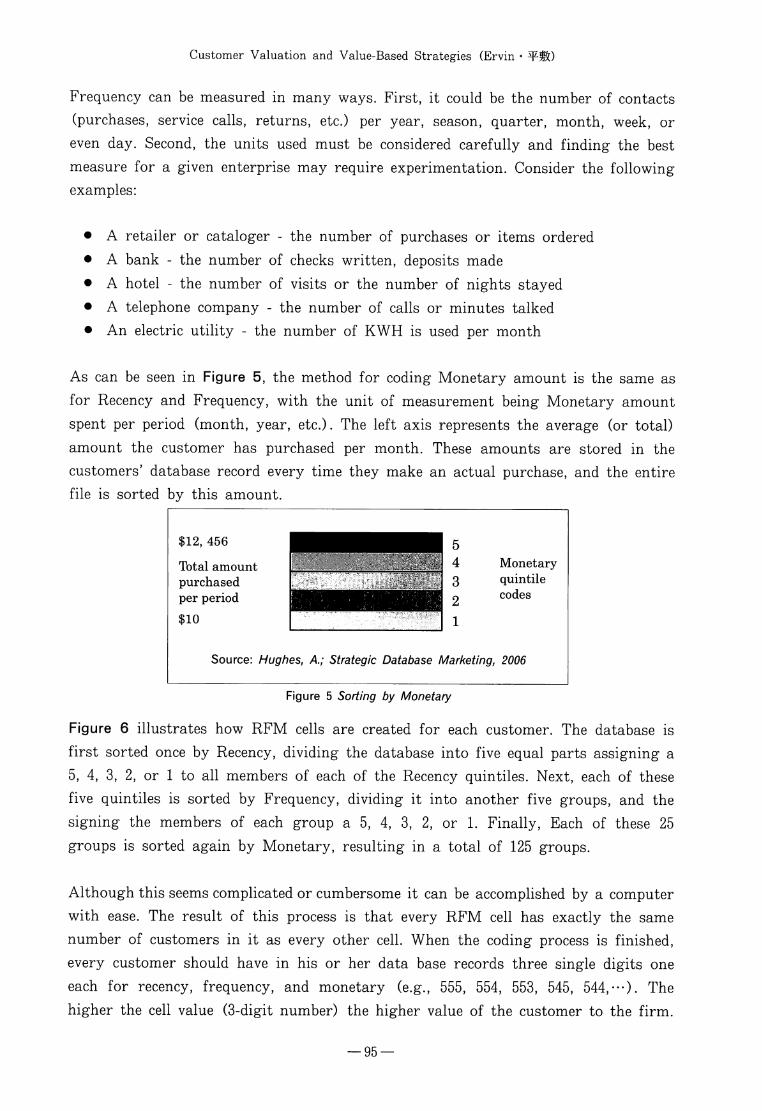

Frequency can be measured in many ways. First, it could be the number of contacts

(purchases, service calls, returns, etc.) per year, season, quarter, month, week, or

even day. Second, the units used must be considered carefully and finding the best

measure for a given enterprise may require experimentation. Consider the following

examples:

• A retailer or cataloger - the number of purchases or items ordered

• A bank - the number of checks written, deposits made

• A hotel - the number of visits or the number of nights stayed

• A telephone company - the number of calls or minutes talked

• An electric utility - the number of KWH is used per month

As can be seen in Figure 5, the method for coding Monetary amount is the same as

for Recency and Frequency, with the unit of measurement being Monetary amount

spent per period (month, year, etc.). The left axis represents the average (or total)

amount the customer has purchased per month. These amounts are stored in the

customers' database record every time they make an actual purchase, and the entire

file is sorted by this amount.

$12, 456

Total amount

purchased

per period

$10

Source:

Hi

Hughes, A;

wsmnsmm

■milmi ii

Strategic Database /

5

3

2

1

Marketing,

Monetary

quintile

codes

2006

Figure 5 Sorting by Monetary

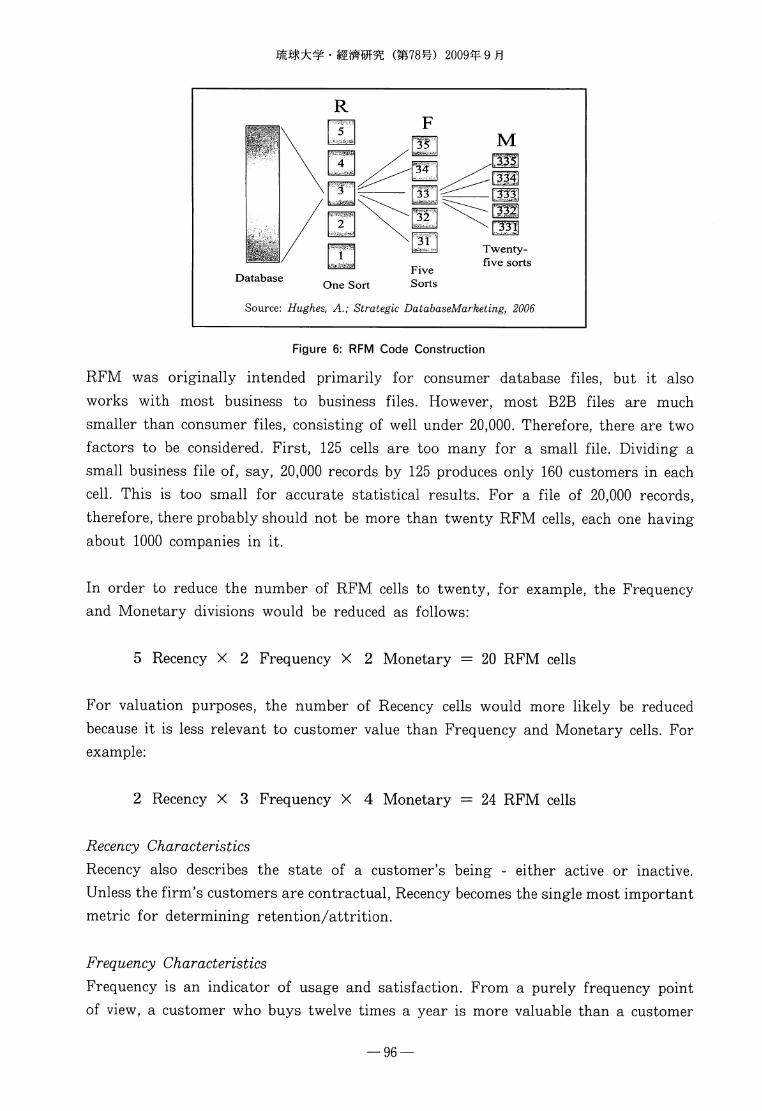

Figure 6 illustrates how RFM cells are created for each customer. The database is

first sorted once by Recency, dividing the database into five equal parts assigning a

5, 4, 3, 2, or 1 to all members of each of the Recency quintiles. Next, each of these

five quintiles is sorted by Frequency, dividing it into another five groups, and the

signing the members of each group a 5, 4, 3, 2, or 1. Finally, Each of these 25

groups is sorted again by Monetary, resulting in a total of 125 groups.

Although this seems complicated or cumbersome it can be accomplished by a computer

with ease. The result of this process is that every RFM cell has exactly the same

number of customers in it as every other cell. When the coding process is finished,

every customer should have in his or her data base records three single digits one

each for recency, frequency, and monetary (e.g., 555, 554, 553, 545, 544,---). The

higher the cell value (3-digit number) the higher value of the customer to the firm.

— 95 —

Twenty-

five sorts

DatabaseOne Sort

Source: Hughes, A.; Strategic DatabaseMarketing, 2006

Figure 6: RFM Code Construction

RFM was originally intended primarily for consumer database files, but it also

works with most business to business files. However, most B2B files are much

smaller than consumer files, consisting of well under 20,000. Therefore, there are two

factors to be considered. First, 125 cells are too many for a small file. Dividing a

small business file of, say, 20,000 records by 125 produces only 160 customers in each

cell. This is too small for accurate statistical results. For a file of 20,000 records,

therefore, there probably should not be more than twenty RFM cells, each one having

about 1000 companies in it.

In order to reduce the number of RFM cells to twenty, for example, the Frequency

and Monetary divisions would be reduced as follows:

5 Recency X 2 Frequency X 2 Monetary = 20 RFM cells

For valuation purposes, the number of Recency cells would more likely be reduced

because it is less relevant to customer value than Frequency and Monetary cells. For

example:

2 Recency X 3 Frequency X 4 Monetary = 24 RFM cells

Recency Characteristics

Recency also describes the state of a customer's being - either active or inactive.

Unless the firm's customers are contractual, Recency becomes the single most important

metric for determining retention/attrition.

Frequency Characteristics

Frequency is an indicator of usage and satisfaction. From a purely frequency point

of view, a customer who buys twelve times a year is more valuable than a customer

— 96 —

Customer Valuation and Value-Based Strategies (Ervin • ^fISO

who only buys once, i.e., twelve opportunities to engage the customer are better

than one. Every interaction is, potentially, an opportunity to strengthen the loyalty,

bond and reliance between the company and the customer, thereby lowering the

attrition rate. Further, a customer who purchases twelve times provides that may

chances for cross-selling or up-selling. Frequency is perhaps influenced to the greatest

degree by satisfaction and satistied customers are considered more valuable.

There are two ways to define and track Frequency, and each method requires a

different database structure. Multiple purchases can be counted on an annual basis

or on a lifetime (cumulative) basis. A pitfall involved in counting frequency at a

life-to-date (LTD) rather than a rolling twelve months: Customer A made five

purchases - four of those purchases being made over thirty-six months ago and one

made recently. Customer B made one purchase a month for the past five months.

Although each of these customers made five purchases, customer B is clearly a better

customer from a valuation standpoint.

Monetary Value Characteristics

Monetary value is how much a customer spends, and is an indicator of just that-

monetary value. As with Frequency, Monetary value can be measured in two ways;

it can be expressed as the total amount spent in the current year, or as the total

amount spent during the lifetime of the customer. Only monetary value can validate

the hierarchy of customer value described by recency and frequency.

Limitations of RFM

RFM was developed to measure and predict responsiveness. It only measures

profitability indirectly. (Hughes 2006).

RFM lacks information such as the costs of the product or service and other costs

associated with making the sale and serving customers (direct costs, such as the

costs of supporting the customers on-line, repairs, restocking, etc.). (Gordon 1998)

RFM Can only be applied to available historic customer data and not on data related

to prospects. Although it does uncover some aspects of customer buying behavior

that have an impact on future buying behavior, the actual score fails to reveal key

information to marketers, such as whether a customer is loyal, when a customer is

likely to buy next, and how profitable a customer will be in the future. (Kumar

2007)

— 97 —

2009^ 9 n

Customer Profitability Analysis

Customer profitability is the single most important variable of customer value and

forms the most essential basis for customer lifetime value and resource allocation. It

can be said that without an eventual measure of customer profitability, the customer

valuation process is an exercise in futility.

Kotler and Keller (2006) remind us that it is not necessarily the company's largest

customers who yield the most profit. The largest customers demand considerable

service and receive the deepest discounts. The smallest customers pay full price and

receive minimal service, but the costs of transacting with small customers reduce

their profitability. The midsized customers receive good service and pay nearly full

price and are often the most profitable.

In this section we present a survey of essential considerations important for formulating

an effective customer profitability analysis as perceived by various authors, followed

by a brief overview of a customer profitability analysis offered by Kotler and Keller

(2006).

Revenue Sources

McNab (2005) submits that the main choice to be made concerning revenue is

whether it will be recognized on a Cash or Accrual basis. In some industries, such

as construction, banking, and franchising this is an important issue and special rules

are laid down by accounting authorities as to how to treat certain items of revenue.

In general, accrual accounting provides a smoother recognition of profit in any given

period, and is desirable for any purpose other than management of cash flow or

business valuation. Most companies will choose to adopt an accrual basis of a counting

for customer revenue. As the types of revenue that occur in the firm's business is

analyzed, care should be given that the treatment of that revenue is as good an

approximation of the business as is possible - even if it differs from the company's

finance policies. It must be remembered that the profitability analysis is a management

information measurement not a financial reporting system.

Kinekin (2001) offers a comprehensive explanation of both customer revenue and

cost sources used for customer profitability/value calculations:

Initial Revenue: The revenue generated by goods and services the customer purchases

initially. The initial reading of profitability isn't a good indicator of long-term customer

value. A customer or segment can be unprofitable initially but vastly more profitable

overtime because of the service revenue, up-sell revenue, and influence value. At the

same time, revenue now is better than revenue later, both because of the increased

— 98 —

Customer Valuation and Value-Based Strategies (Ervin

risk and the time value of money.

Future Revenue: The value of future purchases depends on the amount the frequency of

incremental purchases and the customer's loyalty (which determines the length of

time the customer continues to purchase). Also included is ongoing recurring revenue

for services.

• Incremental Purchases: For industries with periodic transactions (such as insurance,

some retail, telecom, or other services), incremental purchase estimates are

relatively simple. For others, customer purchase history can help determine

typical purchase patterns for a given time period. The company may also find

that purchase value or customer loyalty increases with the number of purchases,

so they adjust marketing and sales programs to move customers more quickly

to a higher value state.

• Service and Support Revenue: The amount of services the customer typically

buys in a given time period is often a percent of product cost. In more mature

industries, service revenue may be more valuable - and more profitable - than

product revenue. For example, automotive suppliers now claim to lose money on

every car sale but they make it up on service. Many high-tech vendors charge

annual maintenance fees for service and support, which for more mature products

can now be lucrative profit centers.

Cost Sources

Initial Costs: The cost of making the sale plus the cost of the actual good or service

sold.

• Acquisition Cost: a rough way to estimate the acquisition cost is to take total

sales and marketing costs (assuming most of these are variable costs) for the

company or business unit, and estimate the percentage spent for new customer

acquisitions (as opposed to customer retention). Then divide that number by the

number of customers acquired. Companies with better sales and marketing

reporting mechanisms can use finer-grained cost-per-sales numbers for common

sales and marketing activities.

Another good indicator of sales cost for B2B transactions is the length of the

sales cycle. Initial sales costs are usually higher than those for repeat sales, and

sales costs vary significantly by customer type (major account, new business,

small and medium-sized enterprise).

Sales and marketing costs also vary widely by industry, with customer acquisition

costs ranging from tens of dollars in online retail to thousands of dollars for

business services. The firm should try to get an appropriate acquisition cost for

each type of customer.

— 99 —

• Products Cost: product cost can be calculated based on a typical product or

product mix sold. For companies providing custom or configured products, the

cost of the product can vary significantly based on the amount of nonstandard

work required (in high tech, this could include cost of additional features added

to make the sale; in manufacturing or service industries in could include the cost

of additional process steps). Care should be taken to include as many of the

variable costs as possible to reflect the true cost of the transaction.

Future Costs: Similar to initial costs, this includes the cost of the incremental products

purchased, the cost to make the incremental sale, and the cost for ongoing service.

• Incremental Product Costs: this is the cost of the product that the customer

purchases. Again, care must be taken to include variable production or fulfillment

costs specific to a customer or group of customers.

• Incremental Sale Cost: typically, sales costs for repeat sales are about 20 percent

of the cost to make the initial sale. However, that number varies by industry

and customer segment, and should be validated with customer examples.

• Ongoing Service and Support Costs: In many industries, customers require ongoing

management and service outside incremental transactions. These cost typically

include customer service and support calls, and back-office processing costs (e.g.,

billing statements) and may include ongoing sales account management or customer

retention programs (e.g., newsletters, frequent shopper, or customer loyalty

awards). The service and support costs may or may not be billed to the customer.

Egan (2004) offers the following insight pertaining to acquisition and retention costs

and their allocations.

Front-end costs

The industries chosen most frequently as examples of customer retention strategies

appear all to have high front-end acquisition costs inherent in their make-up, e.g.,

banks, credit card and insurance companies. Those costs that occur most frequently

are:

• The high cost of personal selling

• Commission payments

• Direct and indirect costs of detailed information gathering

• Supply of equipment

• Advertising and other communication expenditure

— 100 —

Customer Valuation and Value-Based Strategies (Ervin

Personal selling

The higher the degree of complexity involved in the product or service, the higher

propensity for the need of personal selling. Personal selling costs can include salary,

commissions, expenses, and fringe benefits. The cost per customer acquisition can be

high where personal selling is a major component in the customer's decision making

process (Egan p. 60).

Commission

If commissions are payable on sales, the fixed costs of personal selling may be reduced

but the variable costs of acquisition increase. Acquisition costs will therefore likely

be high relative to retention costs.

Data Collection

The Where data collection required is significant and the issue of contracts or other

expensive material is involved, initial costs may be high as well. In these cases the

company may not be able to turn a profit for a year or more into the contract.

Supply of equipment

This refers to long-term equipment supply, etc., free or subsidized supply of satellite or

digital TV receivers) where the investment is written off over the lifetime of the

contract. Any contract that terminates prior to the full write-off period is loss making,

while any contract which lasts beyond that point represents additional profit.

Advertising and other communication costs

Where advertising is used to promote "front of the mind awareness" then the cost of

maintaining this awareness may be justifiably included in the cost of customer

acquisition.

Industries that have high front end costs would benefit from writing those costs off

over an extended period of time. The longer the relationship, the lower the cost relevant

to the income and the higher the profit is likely to be. At the other end of the

acquisition costs spectrum, for example FMCG retailing, the costs of customer

acquisition appear marginal as intense personal selling, commissions, detailed

information gathering, etc. are not always necessary to make an individual sale.

Measurement and Analysis

As can be seen, measuring customer profitability requires detailed information (such as

that outlined above). While assigning revenues to customers is often easy, assigning

costs is much more difficult. The cost of goods sold obviously gets assigned to the

customers based on the goods each customer purchased. Assigning the more indirect

— 101 —

2009^ 9

costs may require the use of some form of Activity-Based costing (ABC). Finally,

there may be some categories of costs that will be impossible to assign to the customer.

If so, it is probably best to keep these costs as company costs and be content with the

customer profit numbers adding up to something less than the total company profit

(Farris, Bendle, Pfeifer, and Reibstein 2006). As mentioned, customer profitability is

management information so there are no set rules that have to be followed, so the

choice of accounting methods depends on the internal needs of the decision makers.

(McNab 2005)

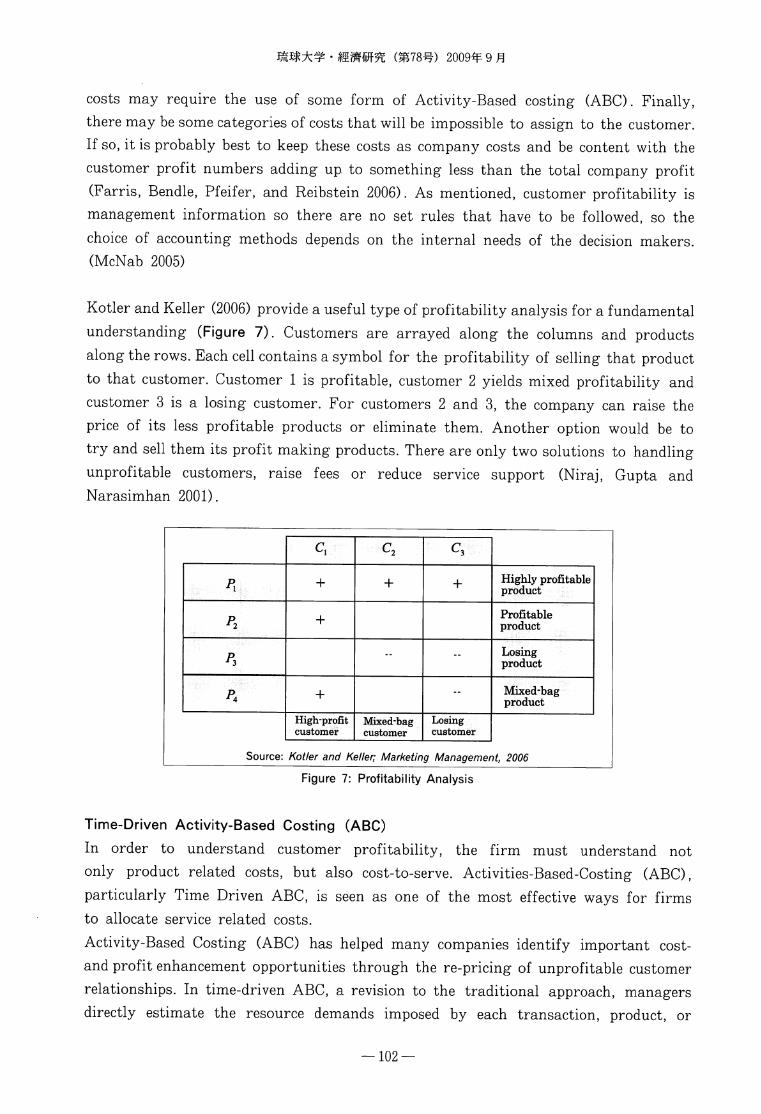

Kotler and Keller (2006) provide a useful type of profitability analysis for a fundamental

understanding (Figure 7). Customers are arrayed along the columns and products

along the rows. Each cell contains a symbol for the profitability of selling that product

to that customer. Customer 1 is profitable, customer 2 yields mixed profitability and

customer 3 is a losing customer. For customers 2 and 3, the company can raise the

price of its less profitable products or eliminate them. Another option would be to

try and sell them its profit making products. There are only two solutions to handling

unprofitable customers, raise fees or reduce service support (Niraj, Gupta and

Narasimhan 2001).

Pr

P2

P3

P*

+

+

+

High-profit

customer

c2

+

--

Mixed-bag

customer

c3

+

--

Losing

customer

Highly profitableproduct

Profitableproduct

Losing

product

Mixed-bagproduct

Source: Kotler and Keller; Marketing Management, 2006

Figure 7: Profitability Analysis

Time-Driven Activity-Based Costing (ABC)

In order to understand customer profitability, the firm must understand not

only product related costs, but also cost-to-serve. Activities-Based-Costing (ABC),

particularly Time Driven ABC, is seen as one of the most effective ways for firms

to allocate service related costs.

Activity-Based Costing (ABC) has helped many companies identify important cost-

and profit enhancement opportunities through the re-pricing of unprofitable customer

relationships. In time-driven ABC, a revision to the traditional approach, managers

directly estimate the resource demands imposed by each transaction, product, or

— 102 —

Customer Valuation and Value-Based Strategies (Ervin

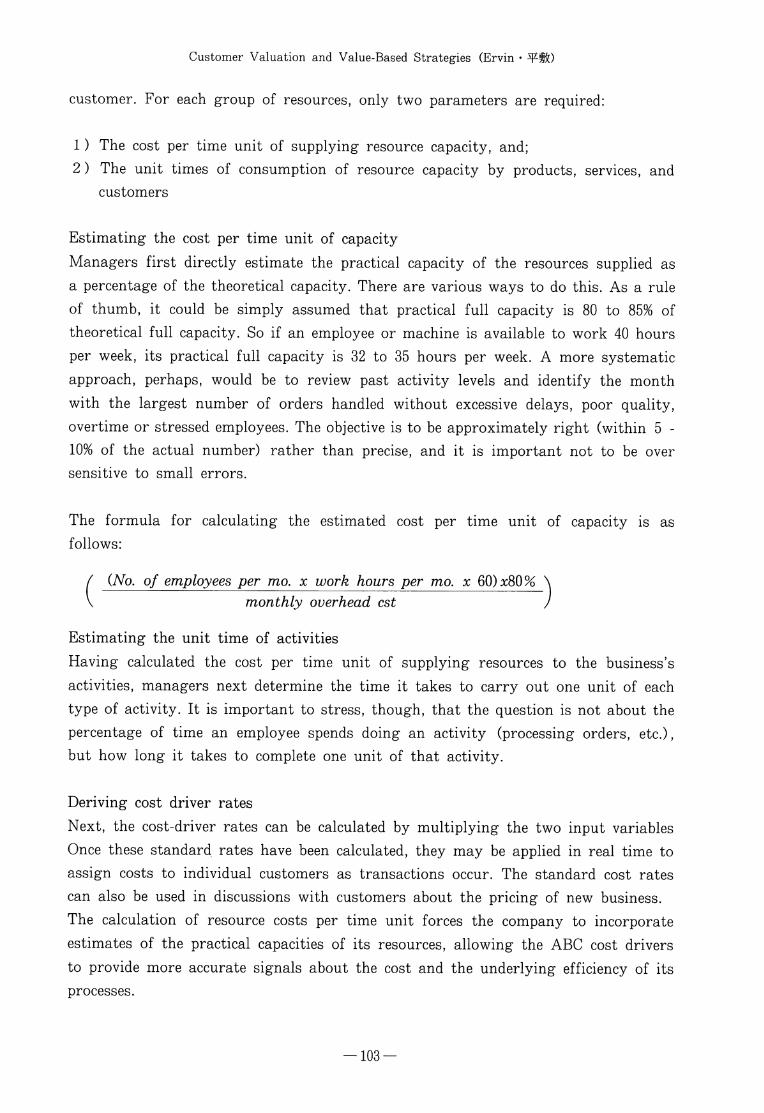

customer. For each group of resources, only two parameters are required:

1) The cost per time unit of supplying resource capacity, and;

2) The unit times of consumption of resource capacity by products, services, and

customers

Estimating the cost per time unit of capacity

Managers first directly estimate the practical capacity of the resources supplied as

a percentage of the theoretical capacity. There are various ways to do this. As a rule

of thumb, it could be simply assumed that practical full capacity is 80 to 85% of

theoretical full capacity. So if an employee or machine is available to work 40 hours

per week, its practical full capacity is 32 to 35 hours per week. A more systematic

approach, perhaps, would be to review past activity levels and identify the month

with the largest number of orders handled without excessive delays, poor quality,

overtime or stressed employees. The objective is to be approximately right (within 5 -

10% of the actual number) rather than precise, and it is important not to be over

sensitive to small errors.

The formula for calculating the estimated cost per time unit of capacity is as

follows:

(No. of employees per mo. x work hours per mo. x 60)x80%

monthly overhead cst

Estimating the unit time of activities

Having calculated the cost per time unit of supplying resources to the business's

activities, managers next determine the time it takes to carry out one unit of each

type of activity. It is important to stress, though, that the question is not about the

percentage of time an employee spends doing an activity (processing orders, etc.),

but how long it takes to complete one unit of that activity.

Deriving cost driver rates

Next, the cost-driver rates can be calculated by multiplying the two input variables

Once these standard rates have been calculated, they may be applied in real time to

assign costs to individual customers as transactions occur. The standard cost rates

can also be used in discussions with customers about the pricing of new business.

The calculation of resource costs per time unit forces the company to incorporate

estimates of the practical capacities of its resources, allowing the ABC cost drivers

to provide more accurate signals about the cost and the underlying efficiency of its

processes.

— 103 —

mmmn 2009^9 n

Analyzing and reporting costs

Time-driven ABC allows managers to report their costs on an ongoing basis in a

way that reveals both the costs of a business' activities as well as the time spent on

them. Managers can review the cost of the unused capacity and contemplate actions

to determine whether and how to reduce the cost of supplying unused resources in

subsequent periods; they can monitor those actions over time (Figure 8).

Activity

Process customer orders

Handle customer inquiries

Perform credit checks

Total Used

Total Supplied

Unused Capacity

Quantity

51,000

1,150

2,700

Unit

Time

8

44

50

Total Time

Used (min)

408,000

50,600

135,000

593,600

700,000

106,400

Cost-Driver

Rate

$6.40

$35.20

$40.00

Total

Cost

$326,400

$40,480

$108,000

$474,880

$560,000

$85,120

Source: Kaplan R. S., Anderson, S.R.; Time-Driven Activity-Based Costing,

Figure 8: Cost Analysis

Updating the model

Managers can easily update their time-driven ABC models to reflect changes in operating

conditions. To add more activities for a department they can simply estimate the

unit time required for each new activity. They can also easily update the cost-driver

rates. Two factors can cause these rates to change:

1) Changes in the prices of resources supplied affect the cost per time unit of

supplying capacity.

2) A shift in the efficiency of the activity can also cause a change in the activity

cost-driver rate.

Examples of a shift in efficiency include quality programs, continuous improvement

efforts, reengineering, or the introduction of new technology, which can enable the

same activity to be performed in less time of with fewer resources. When permanent

sustainable improvements in a process have been made, the ABC analyst recalculates

the unit time estimates (and therefore the demands on resources) to reflect the process

improvements.

To accommodate the improvement, the unit time estimate may simply be changed

and the cost driver rate will automatically reflect the new value upon recalculation.

In this case, the cost impact of any purchases required to obtain those efficiencies

must be added back in by updating the cost per time estimate.

— 104 —

Customer Valuation and Value-Based Strategies (Ervin

By updating the ABC model on the basis of events rather than the calendar (quarterly,

annually, etc.), you get a much more accurate reflection of current condition. Any

time analysts learn about a significant shift in the costs of resources supplied or the

practical capacity of those resources, or about a change in the resources required to

perform the activity, they update the resource cost per time unit, or resource cost

rate, estimates. And any time they learn of a significant and permanent shift in the

efficiency with which an activity is performed, they update the unit time estimate.

Time Equations to Capture Complexity

Time-driven ABC can accommodate the complexity of real-world operations by

incorporating time equations, a feature that enables the model to reflect how order

and activity characteristics cause processing times to vary. The key insight is that

although transactions can easily become complicated, managers can usually identify

what makes them complicated. The variables that affect most such activities can be

precisely specified and are typically already recorded in a company's information

system.

Many companies' ERP systems already store data on order, packaging, distribution

method and other characteristics. These order and transaction specific data enable

the particular time demands for any given order to be quickly determined using a

calculation like the one above.

The ability of time-driven ABC to identify and report complex processes in a simple way

also provides a powerful negotiation tool when it comes to dealing with customers.

The Bottom Line

Time-driven ABC offers a transparent, scalable methodology that is easy to implement

and update. It draws on existing databases to incorporate specific features for particular

orders, processes, suppliers, and customers. Activity-based costing is no longer a

complex, expensive financial-systems implementation; the time-driven ABC innovation

provides managers with meaningful cost and profitability information, quickly and

expensively.

Customer Lifetime Value

Customer lifetime value is the present value of all current and future profits generated

from a customer over the life of his or her business with the firm. It is an important

concept in that it encourages firms to shift their focus from quarterly profits to the

long-term health of their customer relationships (Farris, Bendle, Pfeifer and

Reibstein). It is also the only metric that incorporates all the elements that drive

customer profitability: revenue, expense and customer behavior, thus keeping the focus

— 105 —

mmmn (mm) 2009^9 r

on the customer rather than the product as the driver of profitability. It provides

the best measurement of both loyalty and profitability within one metric. In very simple

terms, CLV is a multi-period evaluation of a customer's value to the firm. Calculating

the CLV can be the basis for formulating and implementing customer-specific strategies

for maximizing customers' lifetime profits and increasing their lifetime duration. It

can also be considered as the metric that guides the allocation of resources for ongoing

marketing activities in a firm. A firm has limited resources and ideally wants to

invest in those customers who bring maximum return to the firm. It helps the firm

to know how much it can invest to retain the customer so as to achieve a positive

return on investment. This is possible only by knowing that cumulated cash flow of

a customer over his or her entire lifetime with the company. Once this is known the

firm can optimally allocate its limited resources to achieve maximum return.

(Kumar 2008)

In comparison to other valuation approaches, Kumar (2007) states that a major

shortcoming of other metrics is that they are not forward-looking and hence do not

consider whether a customer is going to be active in the future. They consider only

the observed purchase behavior, which is then extrapolated to the future to arrive at

the future profitability of a customer. Egan (2004) on the other hand, warns that

the downsides of customer lifetime value is that there is no guarantee that the

customer will continue to patronize a supplier at the same level as previously or that

he or she will even stay with the company. This is particularly true in businesses

with low exit barriers and in rapidly changing, competitive markets (e.g. telecom).

Models of customer lifetime value originated many years ago in the field of direct

and database marketing and continue, to a large extent, to focus in this tactical

domain (Gupta and Lehman 2005). Over the past decade or so, CLV has become a

topic of much research (Heskett, Sasser and Schlesinger). Since then, there appears

to be two schools of thought in the research of customer lifetime value. On the one

hand there is a growing body of research with the aim of providing relatively exact

calculations of CLV through the use of sophisticated models (e.g., Kumar 2007, 2008;

Rajkumar, Venkatesan and Kumar 2004; Werner, Reinartz and Kumar 2000), while

on the other hand there are those who advocate that rough estimates of lifetime

value are sufficient for most top-level managerial decisions (e.g. Gupta and Lehman

2005; Heskett, Sasser and Schlesinger).

In this paper, we have chosen two models for brief typification. The model proposed

by Gupta and Lehman (2005) because of its ease, and the model proposed by Kumar

(2008) because of its treatment of non-contractual customers and because it is based

on two previous empirical studies (Reinartz and Kumar 2000; Venkatesan and

Kumar 2004).

-106 —

Customer Valuation and Value-Based Strategies (Ervin

Gupta and Lehman Model

This model was chosen for typification because of its relative ease of calculation,

thereby making the ability to grasp the fundamental concepts of Customer Lifetime

Value considerably more intuitive to those who are initially unfamiliar with the

concept. Gupta and Lehman maintain that even with detailed data and sophisticated

modeling, we have at best imprecise and approximate estimates of CLV. What is

needed, they say, is a simple metric that is easy to understand and captures the

spirit of customer lifetime value. They maintain that simple and approximate methods

are far more likely to actually be used than their complex counterparts. Further, for

most decision-making purposes it is enough to know the approximate value of the

customer. Therefore, companies should start with simple methods and see how they

affect decisions. After becoming comfortable, the firm can begin to seek precision

and sophistication when the situation warrants doing so.

Gupta and Lehman postulate the following benefits to their approach to estimating

the value of a customer:

• Designed to be transparent to both company executives and investors

• Not requiring large amounts of data

• Simple to understand and use for decision-making purposes

• Providing a good approximation of more detailed and data intensive methods

Based on three simple assumptions, they postulate that for typical situations, the

lifetime value of a customer is simply 1 to 4.5 times the annual dollar margin that

is generated from this customer:

a) profit margins remain constant over time

b) retention rate for customers remain constant over time

c) customer lifetime value is estimated over an infinite horizon

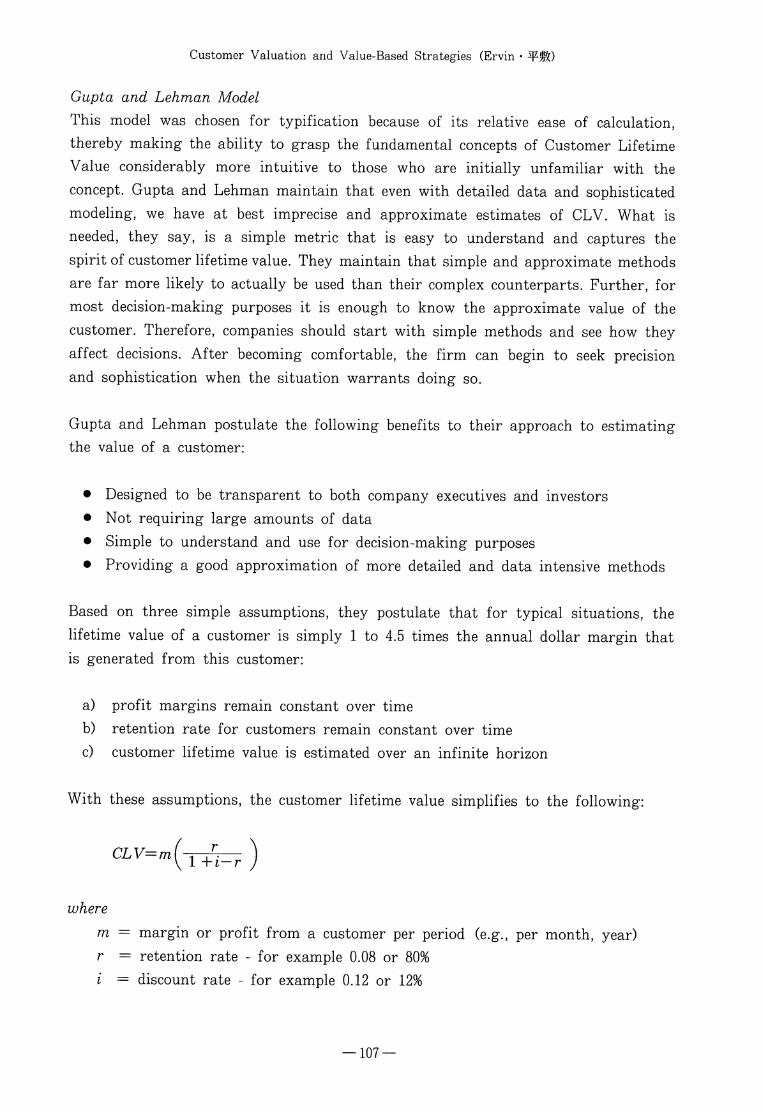

With these assumptions, the customer lifetime value simplifies to the following:

CLV=m

where

m = margin or profit from a customer per period (e.g., per month, year)

r = retention rate - for example 0.08 or 80%

i = discount rate - for example 0.12 or 12%

— 107 —

) 2009^ 9 £

The portion of the formula enclosed in brackets is termed the "margin multiple" and

depends on customer retention rate (r) and the company's discount rate (i). For

most companies, retention rates are in the range 60 — 90%. The discount rate is a

function of the company's cost of capital and depends on the riskiness of its business

and its debt-equity structure. For most companies, they range between 8% andl6%

(Brealey and Meyer, 2002; Damodaran, 2001). Based on these percentage ranges, the

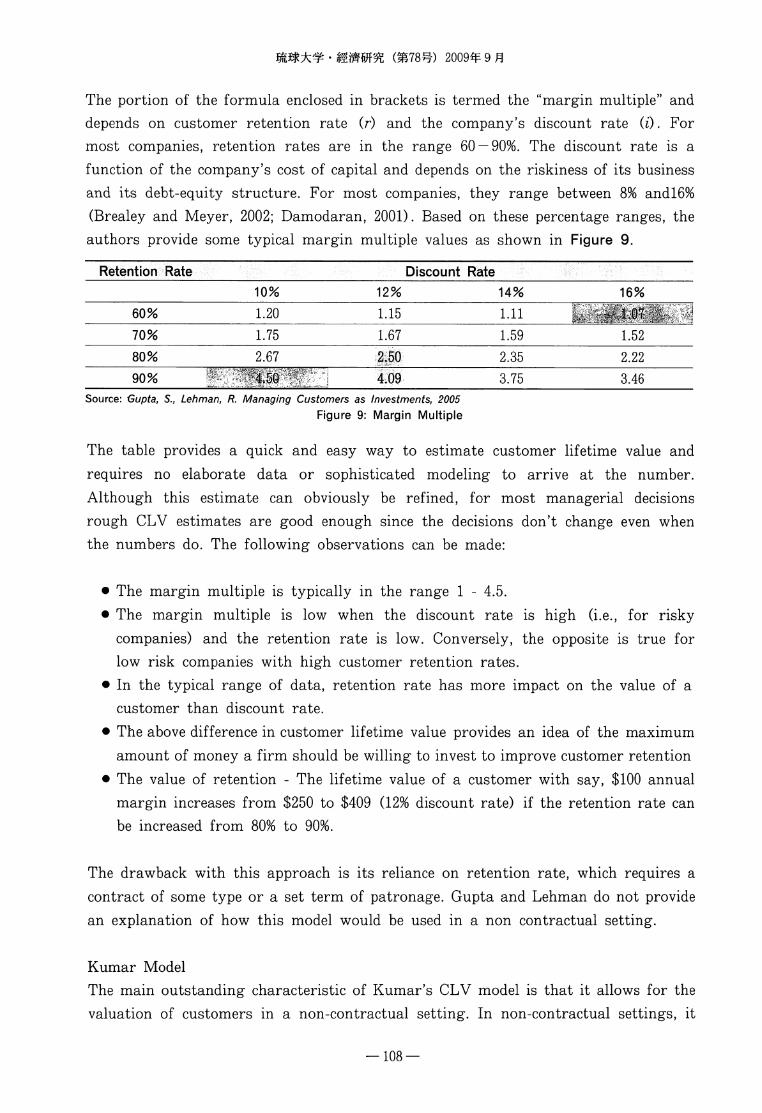

authors provide some typical margin multiple values as shown in Figure 9.

Retention Rate Discount Rate

10% 12% 14% 16%

60% L20 U5 Ul i§| ,—^.,~,^-,...is

70% L75 L67 L59 L52_

80% 2.67 2.50 2.35 2.22

90% Wl'J3PII1Wi:Ii 4-09 3/75 3.46Source: Gupta, S., Lehman, R. Managing Customers as Investments, 2005

Figure 9: Margin Multiple

The table provides a quick and easy way to estimate customer lifetime value and

requires no elaborate data or sophisticated modeling to arrive at the number.

Although this estimate can obviously be refined, for most managerial decisions

rough CLV estimates are good enough since the decisions don't change even when

the numbers do. The following observations can be made:

• The margin multiple is typically in the range 1 - 4.5.

• The margin multiple is low when the discount rate is high (i.e., for risky

companies) and the retention rate is low. Conversely, the opposite is true for

low risk companies with high customer retention rates.

• In the typical range of data, retention rate has more impact on the value of a

customer than discount rate.

• The above difference in customer lifetime value provides an idea of the maximum

amount of money a firm should be willing to invest to improve customer retention

• The value of retention - The lifetime value of a customer with say, $100 annual

margin increases from $250 to $409 (12% discount rate) if the retention rate can

be increased from 80% to 90%.

The drawback with this approach is its reliance on retention rate, which requires a

contract of some type or a set term of patronage. Gupta and Lehman do not provide

an explanation of how this model would be used in a non contractual setting.

Kumar Model

The main outstanding characteristic of Kumar's CLV model is that it allows for the

valuation of customers in a non-contractual setting. In non-contractual settings, it

— 108 —

Customer Valuation and Value-Based Strategies (Ervin • ^

might be difficult to ascertain the duration for which the customer has been associated

with a firm. In the absence of a contract that guarantees future revenue generation,

it is difficult to predict how long the customer is going to stay with the firm. In

such a scenario, predicting the lifetime duration of a customer by observing buying

patterns and other explanatory factors assumes importance.

Kumar advocates computing the CLV of a customer over a three year time period

for most applications and gives the following four reasons:

• No one truly knows how long the customer is going to live

• Given that future cash flows are discounted heavily, the contribution beyond

three years might be quite small

• The predictive accuracy of the models being used can also declined over longer

forecasting times

• A major purpose of computing CLV is for resource allocation; resources have

to be allocated today based on the customer's value in the near future

He gives two exceptions to this three year measurement - the automobile industry

(20 years, with at least 3 purchases) and the insurance industry (7 to 10 years to

recover in the acquisition costs).

The CLV measurement approach illustrated in Figure 10 gives clarity to the calculations

involved in the process.

Recurring

Revenues

Recurring

Costs

Gross Contribution

Margin

Marketing

Costs

Net

Margin XExpected Number of

Purchases over Next 3 Years

Accumulated

Margin

Acquisition

Costs

C Adjusted ^NPresent Value )

Source: Kumar, V. Managing Customers for Profit, 2008

Figure 10: CLV Calculation Process

Customer

lifetime

— 109 —

Kumar offers three approaches to the calculation of customer lifetime value, the

aggregate approach, calculating the average CLV of cohorts or segments, and the

individual level approach. This paper is will be concerned only with the individual

level approach.

At the individual level, CLV is calculated as the sum of cumulated cash flows -

discounted using the WACC - of a customer over his or her entire lifetime with the

company. It is a function of the predicted contribution margin, the propensity for a

customer to continue in the relationship, and the marketing resources allocated to

the customer. In its general form, CLV can be expressed as follows:

nTTT_ yi (Future contribution mrgnlt—Future cstit

CLV'~M oT^

where

i = customer index

t = time index

T = number of periods considered for estimating CLV

d = discount rate

P (Active)

Kumar maintains that in order to calculate the future contribution of a customer in

a noncontractual setting, firms should know the probability of the customer being

active with the firm at future time periods. In such circumstances, P (Active) is used

to calculate the probability that the customer continues to be active in a subsequent

time period. Calculation of this probability at an individual level is essential for CLV

calculation at an individual level because each customer is likely to have different

purchase patterns and inactive periods.

Given the customers past purchasing behavior, one can predict the probability of

individual customers being active in subsequent time periods using a simple formula.

P (Active) = (T/N)n

where

n = number of purchases

T = time period of the most recent purchase

N = current time period For which P (Active) needs to be determined

Kumar acknowledges that there are a few limitations applied to the use of this

approach to calculate the P(Active). First, this model is applicable only to those

situations in which a customer has a fixed SOW in a given time period. Therefore,

— 110 —

Customer Valuation and Value-Based Strategies (Ervin • ^fISO

the more the customer buys earlier on, the less is available for future time periods.

Also, the model penalizes higher frequencies of buying because any fraction raised to a

higher power (which is the frequency of buying) results in a lower profitability. These

limitations can be relaxed if the focus is on modeling the expected inter-purchase time.

Average Monthly Gross Contribution

Firms attain the average gross contribution margin (AMGC) by deducting the average

cost of goods sold for the average monthly revenue from a customer. This is calculated

based on the customer's past purchases and is obtained for all customers (i) and for

the time period (t) for which the lifetime value is being estimated. To arrive at the

present value of the future contribution, the AMGC of the customers is adjusted

with a discount rate (d), for the number of time periods (n).

Net Present Value (NPV)

The NPV of the expected growth contribution (EGO can be calculated by taking the

product of the P(Active) of customers at period n and the discount-adjusted AMGC

for all customers (0, and adding this quantity over all future time periods (T). This

is calculated as follows:

NPV of EGC.= fiP(Active) uX ff^?t=\ { L -ra)t

where,

AMGCu = average gross contribution margin in period t based on all prior

purchases

i = customer index

t = period for which NVP is being estimated

T = number of periods beyond t

d = discount rate

P(Active) u = probability that customer i is active in period t

Finally, the CLV can be calculated as follows

CLV of customer i j]P'(Active)ftX ,. , '''- £Afi«x( , ]_ , )l-Ait=\ ( 1 + a) t=\ \ i T a /

where,

AMGCu = average gross contribution margin in period t based on all prior

purchases

i = customer index

— 111 —

t = period in which NPV is being estimated

T = future time period

d = discount rate

P(Active)*,* = probability that customer i is still active in period n

M = marketing costs of the firm

A = acquisition costs of the firm

Note that acquisition costs (A) and marketing costs (M) incurred at future time periods

have to be deducted from the NPV of ECG of a customer. Also, the marketing costs

at future time periods should be discounted at the appropriate rate (d) to arrive at

the present value of these costs. The discounted marketing costs (M) and acquisition

cost (A) are then subtracted from the NPV of EGC to arrive at the CLV of a customer.

(This calculation presumes that the marketing costs are accounted for at the beginning

of a given time period and the gross contribution at the end of a time period.)

Share Of Wallet (SOW) Analysis

Share of Wallet (SOW), also known as Share Of Customer/Client (SOC) or Share of

requirements, is the measurement of the amount of money a customer is spending on

a particular brand versus other brands. Being a measure of consumption behavior, it is

presumed to be more reliable than attitudinal measures such as satisfaction (Kumar

2007). Many marketers view share of wallet as a key measure of loyalty. This metric can

guide the firm's decisions on whether to allocate resources towards efforts to expand

a category, to take customers from competitors, or to increase share of wallet

among its best customers (Farris et. al.). For example, two customers spendig the

same amount of money on products and services may have vastly different potential

for a company depending on how much they spend on other products and services of