title: impact assessment (ia) - gov.uk · separately, the scrap metal industry is also regulated...

TRANSCRIPT

1

Title:

To amend the law relating to dealers in scrap metal IA No: HO0074

Lead department or agency: Home Office

Other departments or agencies:

Defra, Ministry of Justice, BIS and HM Treasury

Impact Assessment (IA)

Date: 09/7/12

Stage: Final

Source of intervention: Domestic

Type of measure: Primary legislation

Contact for enquiries: Home Office

Summary: Intervention and Options

RPC Opinion: AMBER

Cost of Preferred (or more likely) Option

Total Net Present Value

Business Net Present Value

Net cost to business per year (EANCB on 2009 prices)

In scope of One-In, One-Out?

Measure qualifies as

-£74.8m -£55.7m -£6.5m Yes IN

What is the problem under consideration? Why is government intervention necessary?

The scrap metal industry is recognised by ACPO as being the principal market for stolen metal. The Government believes that the regulation of this industry, the Scrap Metal Dealers Act 1964, is no longer effective and does little to prevent the trade of stolen metal into the industry. Incidences of metal theft are increasing rapidly inline with the rising price of certain metals on the world's commodity market. Driven by the widespread availability of valuable metals (e.g. copper & lead) , the ease with which stolen metals can be traded anonymously through scrap metal dealers and poor trading standards of the industry, metal theft has become a fast growing acquisitive crime with over 7,000 police reported crimes a month and an estimated annual cost of at least £220m. Government intervention is required to revise the regulation governing this industry to ensure it better reflects the twenty-first century scrap metal industry and the types of businesses who now operate as scrap metal dealers, and to improve trading standards.

What are the policy objectives and the intended effects?

The overall policy aim is to implement a robust, modernised and comprehensive regulatory regime for the metal recycling sector that enables agencies to tackle unlawful behaviour including failure to meet licence conditions and trading without a licence. In addition, we propose to better integrate the this regime with the separate environmental regulations overseen by the Environment Agency to ensure closer intelligence sharing and enforcement activity where possible. Option 2 (described below) could reduce crime for two main reasons. Firstly, the requirement from sellers to provide identification details is expected to be a major deterrent to criminals attempting to sell stolen metal; we have seen crime reduce where dealers require greater identification (Operation Tornado – see Section B). Secondly, the requirement for scrap metal dealers to implement better record keeping and the additional enforcement & compliance activity that they will observe is expected to deter dealers from facilitating metal theft, whether knowingly or not.

What policy options have been considered, including any alternatives to regulation? Please justify preferred option (further details in Evidence Base)

While current operations and taskforces are experiencing some success in tackling metal theft, revised legislation is required to prevent further increases in metal theft. The following options are being considered. Option 1: Do nothing – The Scrap Metal Dealers Act 1964 would continue to be the primary regulation of the scrap metal industry. Option 2: Amend the law relating to dealers in scrap metal by repealing the SMDA 1964 and introducing the Scrap Metal Dealers Bill 2012, a more robust, local authority administered licence regime Option 2 is the preferred option for the reasons set out in Section E, most notably the need to more effective regulate the industry.

Will the policy be reviewed? It will be reviewed. If applicable, set review date:

Does implementation go beyond minimum EU requirements? N/A

Are any of these organisations in scope? If Micros not exempted set out reason in Evidence Base.

Micro Yes

< 20 Yes

SmallYes

MediumYes

LargeYes

What is the CO2 equivalent change in greenhouse gas emissions? (Million tonnes CO2 equivalent)

Traded:

Non-traded:

I have read the Impact Assessment and I am satisfied that (a) it represents a fair and reasonable view of the expected costs, benefits and impact of the policy, and (b) that the benefits justify the costs.

Signed by the responsible Minister: Lord Henley Date: 9/7/12

2

Summary: Analysis & Evidence Policy Option 2 Description: Regulate the scrap metal industry through a new Scrap Metal Dealers Bill

FULL ECONOMIC ASSESSMENT

Price Base Year 2011

PV Base Year 2012

Time Period

Years 10

Net Benefit (Present Value (PV)) (£m)

Low: -4.0 High: -483.0 Best Estimate: -74.8

COSTS (£m) Total Transition (Constant Price) Years

Average Annual (excl. Transition) (Constant Price)

Total Cost (Present Value)

Low 0.25

1

1.0 8.3

High 1.0 57.1 491.2

Best Estimate

0.6 9.2 79.2

Description and scale of key monetised costs by ‘main affected groups’

Business: payment of licence fee (£0.4m), compliance with new requirements (£4.1m for dealers and £2.0m for customers who are businesses). Individuals (non-business customers): compliance with new requirements £2.0). Local Authorities: additional admin and enforcement (£0.4m). Environment Agency: IT set-up (£0.6m one-off) and support (£0.1m). CJS: increase in offences (£0.01m to CPS and HMCTS).

Other key non-monetised costs by ‘main affected groups’

Proposals could lead to appeals of licence refusal or revocation to the magistrates‟ court. Costs of these appeals are expected to be minimal, due to the small number estimated, but costs could not be estimated. There may be additional costs to business as a result of increased enforcement activity but this is thought to be minimal and could not be estimated.

BENEFITS (£m) Total Transition (Constant Price) Years

Average Annual (excl. Transition) (Constant Price)

Total Benefit (Present Value)

Low

-

0.5 4.3

High 1.0 8.3

Best Estimate

- 0.5 4.4

Description and scale of key monetised benefits by ‘main affected groups’

Business: Removal of license fee for end of life vehicle sites (£0.06m). Local Authorities: fee income (£0.4m). CJS: fine income from increased offences (£0.01m).

Other key non-monetised benefits by ‘main affected groups’

This Bill seeks to reduce metal theft. These proposals should reduce metal theft which would lead to savings to businesses and individuals. Under 4 per cent of the annual, lower estimate, £220m cost of metal theft would need to be saved in order to cover the costs of the policy with an estimated 95 per cent of any crime reduction benefits likely to fall to businesses.

Key assumptions/sensitivities/risks Discount rate (%)

3.5

Cost of business compliance assumes 5 minutes of time, 65 transactions per day, 10% of transactions relating to „new‟ customers, 50% of customers are businesses and 50% are individual sellers. 50% of dealers already comply voluntarily with proposals. Uncertainties mean cost could be lower or higher. Estimated cost of metal theft (£220m) likely to be under-estimate so potential benefits could be larger. Volume of dealer (2,631) likely to be lower bound estimate so associated costs could be higher. Sensitivity analysis demonstrates scale of potential error in assumptions. This is found in Section F.

BUSINESS ASSESSMENT (Option 2)

Direct impact on business (Equivalent Annual) £m: In scope of OIOO? Measure qualifies as

Costs: 6.5 Benefits: 0.06 Net: -6.5 Yes IN

3

Evidence Base (for summary sheets)

A. Strategic Overview

A.1 Background The scrap metal industry is principally regulated by the Scrap Metal Dealers Act 1964. The Government, as well as the scrap metal industry, believes that the Act has severe limitations and flaws, such as limited powers to tackle unlawful operators, lax record keeping requirements and it being a no fee earner for local authorities meaning that existing compliance is limited. We therefore want to create a new regulatory regime for the industry, putting in place a more robust, local authority administered and enforced, regulatory regime for the scrap metal industry. This would have a single national public register administered by the Environment Agency which will more closely align the scrap metal and environmental regimes. Separately, the scrap metal industry is also regulated under environmental legislation by the Environment Agency with requirements to obtain a permit to both carry out a waste operation and to transport waste amongst others. This is an entirely separate regime from the Scrap Metal Dealers Act 1964, but has many areas of duplication. The environmental regimes stem from the Waste Framework Directive (2008/98/EC). Specific domestic regulation includes the Environmental Permitting (England and Wales) Regulations 2010, Waste (England and Wales) Regulations 2011 and the Control of Pollution (Amendment) Act 1989. In addition, vehicle crime dismantlers are independently regulated by local authorities under the Vehicle (Crime) Act 2001. Initial legislative action was taken under the Legal Aid, Sentencing and Punishment of Offenders Act (a separate impact assessment was produced – HO0058) which took legislative steps including prohibiting cash to purchase scrap metal, amending police powers of entry and increasing the financial penalties under the existing Scrap Metal Dealers Act 1964. Legislative action was taken in that Act due to the uncertainty over when further legislative measures could be taken. The Act received Royal Assent on 2 May 2012 and is due for enactment in the autumn of 2012. Parliament has also debated the response to metal theft and ruled in a motion in February 2012 after a Backbench Committee Debate that legislative action was required to revise the Scrap Metal Dealers Act 1964. The Scrap Metal Industry The scrap metal industry in England and Wales plays a vital role in the green economy with the collection, processing, exportation and recycling of all scrap metals. However some parts also offer a low risk disposal route for stolen metals, often paying cash in hand with very few questions asked as to the identity of the seller and the ownership of the materials. We do not know how many scrap metal dealers operate in the UK. There is no central database for the number of scrap metal dealers registered by local authorities under the Scrap Metal Dealers Act 1964 and it would be cost prohibitive to ask each of the 350+ local authorities. However, as of 1 May 2012, the Environment Agency have permitted 831 metal recycling sites and a further estimated 1,800 metal recycling sites who have obtained a registered exemption. All of these will fall under this new regime. In addition, there are 1,775 registered end of life vehicle sites. It is likely that the majority of these sites will also have an environmental permit or have a registered exemption and so would be included within the number of permitted (or exempted) metal recycling sites.

4

Metal theft The previous LASPO impact assessment [HO0058]1 contains more detailed background information on metal theft. In addition to wanting to modernise the regulation of this industry, another objective of revising the Scrap Metal Dealers Act 1964 is to try to reduce current levels of metal theft. According to the Association of Chief Police Officers, elements of the scrap metal sector prove to be the major outlet of stolen metal with no intelligence to suggest the direct export of stolen metals without entering the scrap metal industry. While “metal theft” is not a separate crime defined in law, or recorded separately by police, it is estimated that there were between 80,000-100,000 police recorded metal theft offences in 2010/11 and figures from 18 police forces in 2011 showed a 56% increase in these offences for the first six months of the calendar year compared to the same period in 2010. In

2011/12, there were 491,5622 police recorded „other theft or unauthorised taking‟ offences – this recording category is where we would expect most metal theft offences to be recorded – this is a 2% increase from the previous year. Due to the size of the category we are unable to ascertain how many of these offences are related to metal theft. From 1 April 2012, police forces will separately identify metal theft offences as part of the Annual Data Requirement to allow for the collation of accurate offence data for the first time. It is not possible to ascertain the number of prosecutions for metal related theft and handling offences as there is currently no separate category for metal theft offences. The Ministry of Justice have supplied information in relation to prosecutions under the Scrap Metal Dealers Act 19643, 18 convictions were obtained from the Magistrates Court in the 2010 calendar year, with only 41 since 2006. We do not know the results of each conviction, but offences in the Act are summary only and carry a maximum level 3 fine on the standard scale, £1,000.

The impact has been felt across a range of sectors in the UK including power, transport and telecommunications. Other affected sectors include wireless, water supply, religious/heritage buildings, construction, local authorities and scrap metal dealers. This has resulted in a serious threat to the security of the national infrastructure. The most recent studies estimate the total cost of metal theft to the UK at between £220m-£260m per year (Deloitte, 2011) and £777m per year (ACPO, 2010). The Home Office estimates the cost at £220m (explained in Annex 1 of the LASPO impact assessment4) but acknowledges this as likely to be an underestimate. The scrap metal industry is also considerable victims of metal theft with the British Metals Recycling Association estimating that £500,000 worth of metal is stolen from yards each year.

The Home Office and ACPO believe that metal theft is viewed as a low risk (and potentially high yield) alternative to other acquisitive offences such as burglary, cash in transit robbery and vehicle crime. With household and vehicle security improving, metal theft is an appealing alternative. Under the current registration scheme it is difficult for police forces to prove theft offences; and where convictions have been obtained for theft offences, metal theft offenders have previously received lower sentences than other acquisitive crimes because the items that they stolen were often low in intrinsic value, despite causing significant direction costs (for example, the costs in relation to a theft of power cable). Courts have however recently started giving higher sentences reflecting the full costs relating to each theft with prosecutors bringing to the courts attention the full consequential costs (travel delays, peripheral damage, cost of replacement) of a relatively low level offence. Evidence from Operation Tornado, a joint police and industry operation in the North East which went live in January 2012, suggests that key changes, including requiring additional identification from the seller, could help to reduce metal theft. Operation Tornado is being rolled out nationwide and will be live across England and Wales by autumn 2012, which together with good practice issued by the industry, means that many scrap metal dealers are already voluntarily requiring additional identification from sellers.

1 http://www.justice.gov.uk/downloads/legislation/bills-acts/legal-aid-sentencing/laspo-metal-theft-ia.pdf

2 Crime in England and Wales: Quarterly First Release to March 2012, Office for National Statistics, July 2012

3 Justice Statistics Analytical Services - Ministry of Justice, June 2011

4 http://www.justice.gov.uk/downloads/legislation/bills-acts/legal-aid-sentencing/laspo-metal-theft-ia.pdf

5

The Home Office‟s overall approach to tackling metal theft is focused on three areas: 1) legislation; 2) enforcement; and 3) design solutions. Legislation It is widely accepted that more robust regulation of the scrap metal industry is needed. This is the subject of this impact assessment. Earlier legislative work was delivered through the Legal Aid, Sentencing and Punishment of Offenders Act 2012 (which commenced on 3 December 2012). In February 2012 a Backbench Committee Debate agreed a motion to introduce additional measures to regulate the scrap metal industry and tackle metal theft as “a matter of urgency”.5 Calls to revise the Scrap Metal Dealers Act 1964 have not just been made by Parliament. The Home Office has received significant volumes of correspondence since the Coalition was formed in 2010 on this subject, all supporting the need for change. This has included from the industry itself. The existing Scrap Metal Dealers Act 1964 has ten criminal offences, all summary with financial penalties varying between level 1 -3 (from 3 December they were raised to level 3-5 by the Legal Aid, Sentencing and Punishment of Offenders Act 2012). Enforcement Currently local authorities have the regulatory responsibility under the existing Act and the Home Office has worked with them and the Local Government Association to strengthen this activity. Work is also underway with the Association of Chief Police Officers (ACPO) and the police service to increase enforcement activity and ensure that forces are best placed to combat the recent growth in metal theft. With the rise in commodity prices driving an increase in offences, metal theft has grown in significance across the majority of police forces. This has been strengthened through additional Government funding in November 2011 to establish a dedicated National Metal Theft Taskforce across the United Kingdom. The Environment Agency additionally has a regulatory responsibility for this industry and undertakes enforcement activity to ensure the environmental compliance of scrap metal dealers.

Design The Home Office‟s Forum for Innovation in Crime Prevention brings together experts from across Whitehall and the academic world to develop design solutions to crime problems. Metal theft is one of four crime areas that the Forum is focussing on and considerable work is underway with the project being lead by the Institute of Materials, Minerals and Mining. Additionally, through the multi-agency ACPO Metal Theft Working Group, a range of actions are being taken to voluntarily tackle metal theft including making metal more difficult to steal; increasing the risk to the offender; reducing the rewards for stealing metal and increasing standards across the scrap metal dealer industry.

A.2 Groups Affected i) Scrap metal dealer industry – currently working to poor regulation, would need to comply with

the proposal of revised regulation. The British Metal Recyclers Association estimates that 8,000 individuals are employed in this industry.

ii) Public – members of the public who wish to recycle legitimately owned scrap metal.

iii) Local authorities – currently administer and ensure compliance under the existing Scrap

Metal Dealers Act 1964. Local authorities would have an enhanced role under any new regime, including full administration of the new regime, undertaking compliance and enforcement activity and ensuring the sharing of appropriate information with other law enforcement organisations. It is proposed that this additional burden will be funded through an additional licence fee, paid for by the scrap metal industry on receipt of a trading licence.

iv) Police forces – responsible for responding to the criminal offences under this new regime. The offences will not differ from current responsibilities.

5 Hansard reference: 7 Feb 2012 : Column 273

6

v) Environment Agency – would continue to separate permit and licence the scrap metal industry through environmental regulation, this would be unchanged. The only additional burden will be to host and maintain a public accessible register of licensed scrap metal sites, with the purpose of developing stronger links with the environmental regulation under the Environment Agency.

vi) Her Majesty‟s Revenue and Customs (HMRC), the Treasury – more transparent record

keeping by the industry as a result of a new regime in addition to cashless transactions should provide greater accuracy in what transactions businesses complete. This should lead to greater compliance with tax payment to close the existing tax gap that exists within this sector. SITA UK, a large metal recycling firm, have stated that the £1.5 billion of cash transactions each year creates the opportunity for tax fraud, avoiding direct and indirect taxes.

vii) Her Majesty‟s Courts and Tribunals Service, Crown Prosecution Service – there may be an

increase in the number of offences that enter the justice system.

viii) Business and the wider UK economy – any reductions in metal theft would reduce the social and economic costs estimated at around £220m per annum.

A.3 Consultation Within Government

These proposals have been developed in partnership with colleagues across Government – in particular the Department for the Environment, Food and Rural Affairs; the Environment Agency, the Department for Communities and Local Government, the Ministry of Justice and the Department for Business, Innovation and Skills. Discussions have also been had with the Cabinet Office and with the Department for Energy and Climate Change and the Department for Transport, both of whom are victims of metal theft. Discussions have also been had with the Welsh Government Assembly and the Scottish Government, as well as with overseas representatives including the Royal Canadian Mounted Police. Public Consultation No formal public consultation has taken place although the Home Office has met and obtained the views from the British Metals Recycling Association, the key representative body of the scrap metal industry, three scrap metal firms, the Local Government Association, the Association of Chief Police Officers and other members of the multi-agency Association of Chief Police Officers Metal Theft Working Group since Easter 2012. Prior to this, discussions have been held with a wide number of companies since the election, including with private industry, infrastructure providers, scrap metal dealers (including European and Worldwide sector representatives) and the third sector. It is widely accepted that the Scrap Metal Dealers Act 1964 has severe limitations and needs to be revised. This view is shared by, amongst others, the scrap metal industry. The British Metals Recycling Association, the trade association for the industry, said in a position paper6 released in April 2012 that they:

„continue to call for a rapid and comprehensive reform of regulations in order to tackle metal theft including a tough new licensing regime, a single national register of merchants and reform of the out-dated Scrap Metal Dealers Act (1964)‟.

In addition, core components of our proposal are already considered good practice by the industry and are included within the British Metal Recycling Association‟s voluntary code of practice which is adopted by their members. Seeking additional identification from the seller is part of this code of practice and is now commonly used as business as usual by the majority of scrap metal dealers. Identification also forms a key component of Operation Tornado which has been developed by

6 http://onlinenewsroom.co.uk/bmra/recycling-sustainability/bmra-demands-urgent-regulatory-reform-to-tackle-metal-theft/

7

ACPO in conjunction with the industry. Over 80 per cent of dealers in the North East have signed up to Operation Tornado.7 The Home Office has received similar support from other scrap metal firms and from those with an informed opinion of the matter8. SITA UK, a large business within the scrap metal industry, believes that the cash in hand nature and lax record keeping that dominates this industry is facilitating tax avoidance/evasion; they publically believe that £1 billion of transactions is avoiding tax each year. Tackling this was a significant driver behind our decision to seek a criminal offence of cash payments that we made through the Legal Aid, Sentencing and Punishment of Offenders Act. Through this proposal we seek to tighten up the record keeping requirements further, including requiring identification.

7 ACPO, 2011, Operation Tornado briefing

8 Support has been received in particular from SITA UK and Alchemy Metals, two leading scrap metal firms, and universal support from the

multi-agency ACPO Metal Theft working group including police, wider law enforcement, scrap metal industry and private industry/infrastructure providers.

8

B. Rationale As explained in Section A, metal theft is a serious problem estimated to cost at least £220m each year. If no action is taken to tackle metal theft, the scale of the problem is anticipated to rise, continuing to track the escalating commodity prices on the world market. Metal markets are predicting that prices will continue to rise, albeit at a slower rate, until 2015, reflecting demand from the Far East. The scrap metal market is believed to be the main route through which stolen metal can be traded. Outdated regulation of the scrap metal industry and poor trading standards within the industry are therefore key factors in relation to metal theft. For example, the requirement to keep a record of transactions is widely ignored, and where records are kept, there is no requirement for accuracy. The police have encountered examples of falsely kept records. There is also no requirement for the dealer to satisfy himself that the goods are not stolen or to verify the seller‟s identity. Despite the measures introduced through the Legal Aid, Sentencing and Punishment of Offenders Act 2012, there is therefore a risk that the current market structure is a relatively easy target for criminal exploitation.

Government involvement is therefore required to revise the regulation governing this industry to ensure it better reflects twenty-first century „scrap metal‟ and the types of businesses who now operate as scrap metal dealers, and to improve trading standards. Currently, local authorities are the main regulator under this Act. With registration transferring no fees to local authorities, resources are not sufficient to ensure sufficient compliance with existing requirements. The creation of a new fee for scrap metal dealers is therefore required in order to provide the resources needed by local authorities to more effectively enforce requirements. This will in turn lead to improved compliance and will therefore reduce the opportunity for stolen metal to be sold. The Home Office is aware that criminals may look to exploit other markets and that this crime could either be driven underground or be displaced elsewhere; discussions are ongoing to explore what this displacement could be and to develop effective strategies. For example, it is thought that metal diverted away from scrap yards could be directly exported; the Home Office is in discussion with port authorities, UK Border Agency and HMRC to look at how this option could be monitored and restricted.

Our proposals build upon the successes and limitations of a range of work that has already been delivered to tackle metal theft. A range of individual and multi-agency operations have been developed across the country, some by taskforce funding. The most recent, Operation Tornado, is a joint initiative between the British Transport Police, the three police forces in the North East of England (Durham, Northumbria and Cleveland) and the scrap metal industry requiring participating scrap metal dealers to take voluntary additional steps to check the identity of individuals selling scrap metal, and a more focused, coordinated law enforcement response. This operation went live in January 2012 and is now being rolled out across England and Wales, with full coverage by the autumn. This is the latest attempt to seek enhanced voluntary actions by the industry to increase trading standards. Operation Tornado is part funded through money made available from the National Infrastructure Plan, published in November 2011, which allocated £5m to set up a National Metal Theft Taskforce. This funding ends in March 2013. Most of the police activity as part of Tornado has come from existing police finances. Taskforce money has been used to fund the central coordination of the operation (by British Transport Police); to deliver awareness raising activity for police forces; to fund additional communications (both to the scrap metal sector and the public); to fund dedicated operations and days of action; and to deliver intelligence collating activity, including visiting all known scrap metal yards. This information that has been used by forces when rolling out and delivering Tornado. Operation Tornado has been used as a pre-cursor to a more robust scrap metal licensing scheme. It is unlikely that further funding will be available to support Operation Tornado very much beyond

9

this point but it will help to raise awareness of the changes that will take place when the new scheme is introduced in the autumn of 2013. In the lead up to each regions roll out, each registered scrap metal dealer was visited by the police and made aware of the Operation, their obligations if they joined the trial, and what they could expect. Each was also provided with promotional material for display. Those yards who did not sign up were visited for a second time and have subsequently received more focused police attention than participating scrap metal dealers. Regional roll outs were also accompanied by considerable regional media activity and public awareness campaigns. We are already using Operation Tornado to raise awareness of the change to a cashless model that will be introduced later this year. While no evaluation of Operation Tornado has been completed, figures from the first three months of the operation in the North East have been positive. Reductions in metal theft related offences of between 40 per cent to 55 per cent have been reported across the three police force areas from their police recorded crime data. One day of connected action resulted in 35 arrests at 10 scrap metal dealers. At one site, £600,000 in cash was recovered and plans are in place for asset seizures and court restraining orders. These reductions could be because Operation Tornado benefitted from higher than usual police focus and the possibility of displacement to non-Tornado regions. This Operation is based around the seller needing to provide photographic identification when selling metal to the scrap metal dealer; this will be a core component of the proposals set out in this document. The need for regulation The Home Office, in conjunction with a range of other partners, have delivered a range of non-legislative activity to tackle metal theft. Such activity includes:

- work to strengthen enforcement activity by police and all law enforcement organisations, including providing £5m of additional Government funds to expand all law enforcement activity;

- creating a new central intelligence unit for all metal theft information – hosted by the British Transport Police but with input from a range of public and private sector organisations;

- continuing activity to develop design solutions to both better protect metal and detect metal that is stolen;

- working with the scrap metal sector to seek to increase their trading standards voluntarily, both through Operation Tornado and through developing a Code of Practice with the British Metals Recycling Association – we have however failed to get full compliance from across the industry;

- awareness raising activity with local authorities and the Crown Prosecution Service about the criminal law that covers the scrap metal industry and metal theft; and

- communications activity with national and regional media, along with Crimestoppers, to increase public awareness of metal theft.

However with offence numbers continuing to rise, due to both the continuing attractiveness of metal as a criminal commodity and the accessibility of stolen metal markets, we have come to the conclusion that revising the regulation of the industry is a vital next step to replace the ineffective Scrap Metal Dealers Act 1964 which does very little to tackle metal theft and support an increase in trading standards. Initial legislative measures were taken in the Legal Aid, Sentencing and Punishment of Offenders Act 2012 to prohibit cash payments for scrap metal, to extend police entry powers and to increase the financial penalties under the Scrap Metal Dealers Act 1964. These were always seen as initial steps with the long term requirement being a reform of the regulation.

10

C. Objectives

The overall policy aim is to implement a robust, modernised and comprehensive regulatory regime for the metal recycling sector that supports law abiding businesses and tackles unlawful behaviour. Objectives include:

i) Ensure that new regulation recognises twenty-first century scrap metal and the twenty-first century scrap metal industry;

ii) Reduce the burden on the industry by joining together the scrap metal and vehicle

salvage schemes and have one national register under the Environment Agency, who also regulate the industry through environmental regulations;

iii) Provide the means to tackle unscrupulous scrap metal dealers and to remove those who

are deemed unsuitable to operate from the industry; iv) Shutting the principal stolen metals market; v) Seeking greater transparency of the transactions within and into the industry; vi) Raise trading standards across the industry, in doing so making the market place more

hostile for stolen metal; and vii) Support the localism agenda by empowering local authorities, police forces and wider

local partnerships with the powers they need to tackle illegal behaviour by the scrap metal industry.

Under this proposal, the intention is to replace the Scrap Metal Dealers Act 1964 with a more robust licence regime that will modernise the regulation of the industry. The current separate local authority scheme that regulates vehicle salvage will be brought within the new scrap metal scheme reducing the regulatory burden on the industry. Stronger links with the Environment Agency, another regulator of the industry, will be delivered by having a single national register, administered by them, into which local authorities will input their local licensing information. The regime will support the localism agenda by empowering local authorities, police forces and wider local partnerships with the powers they need to tackle illegal behaviour by the scrap metal industry. Local authority enforcement will allow more effective co-ordination of targeted action and intelligence sharing with local police forces.

11

D. Options

Option 1 - Make no changes at present (do nothing). Make no change to the regulation governing the scrap metal industry, the Scrap Metal Dealers Act 1964. There will be no direct additional cost to private, public or the third sectors as a result of this policy. It is anticipated that incidents of metal theft will remain, especially in light of predicted commodity costs continuing to rise until at least 2015. Incidences of metal theft will therefore continue to cause a cost to the UK economy, disruption to UK infrastructure and wider social costs. This Option will rely on existing enforcement activities to tackle metal theft and seeking to raise trading standards of the scrap metal industry voluntarily. Whilst Operation Tornado is currently successfully doing this, this Operation is vulnerable and relies on good will of the scrap metal dealers to participate. The ACPO believes the high compliance rates are as of a result of scrap metal dealers anticipating this new legislation; should the legislation not materialise they believe that compliance rates will reduce.

Option 2 – Introduce the Scrap Metal Dealers Bill to amend the law relating to scrap metal dealers. Option 2 is the preferred option. The proposed new regime The new regime is intended to cover all individuals and businesses who undertake commercial activity to „collect, purchase, process or sell‟ discarded metal. This would include all „scrap metal dealers‟ as currently defined by the Scrap Metal Dealers Act 1964 and other waste traders involved in scrap metal including metal brokers, carriers and itinerant collectors. In addition, we seek to integrate motor salvage operators as registered by local authorities under Part 1 of the Vehicle (Crime) Act 2001 and include them within the definition of a scrap metal dealer

Through the Scrap Metal Dealers Bill, we propose to put in place a more robust, local authority administered, regime for the scrap metal industry. This new regime will aim to support law abiding scrap metal dealers, whilst including further powers to ensure unscrupulous dealers can be adequately dealt with, including clear and enforceable responsibilities on scrap metal dealers. We also seek to better align the scrap metal and environmental permit regimes by creating a single national register, hosted by the Environment Agency.

Under the existing Act, local authorities are the principal regulators. We propose that this will continue, drawing on their experience and existing infrastructure, as well as their wider experience in administering and enforcing other licence regimes such as that under the Licensing (Alcohol) Act 2003. The Environment Agency regulates businesses undertaking environmental and waste activities and so scrap metal dealers are also required to register with the Agency under environmental permit regulations. We want to align the local authority and the Environment Agency regulatory regimes, thereby reducing the burden on the scrap metal industry. We therefore propose that the Environment Agency hosts a combined national register of scrap metal dealers, which local authorities will contribute to and covers both regulatory regimes.

We propose to introduce a licence fee for scrap metal dealers. This fee will be an essential component of the new regime and will provide local authorities with the funding they need to properly administer the regime and ensure compliance.

Currently those businesses who are involved in the disposal of vehicles are regulated by a separate regime under the Vehicle (Crime) Act 2011. A large but undefined proportion of these businesses are scrap metal dealers and we therefore propose that this scheme become part of the new scrap metal scheme thereby reducing the regulatory burden to industry and any additional costs. We propose to do this by repealing the relevant part of the 2001 Act and incorporating motor

12

salvage operators with the definition of a scrap metal dealer. Registration under the current regime comes at an annual cost of around £100; however the fee does differ between local authorities. The new licensing regime will have 11 criminal offences relating to the conduct of the scrap metal dealer. Combining the licensing regimes for scrap metal dealers and for motor salvage operators (who are separately currently regulated by the Vehicles (Crime) Act 2001), we are removing a total of 4 offences from the statute book. Each of the offences in the new regime will be triable by summary only with fines ranging between level 3 and level 5 on the standard scale. None of the offences carry a custodial sentence.

The Home Office believes that the provisions contained in the Scrap Metal Dealers Bill will contribute to a reduction in metal thefts for the following reasons:

That the Bill will ensure that only operators considered as being „suitable‟ can operate as a scrap metal dealer with the licensing authority having the power to refuse an application, or to revoke a licence, on grounds that it would be unsuitable for that business to trade as a scrap metal dealer. The courts will also have the power to close any operating unlicensed scrap metal dealers. Grounds of suitability include considering unspent relevant convictions for offences in the Theft Act 1968, the Scrap Metal Dealers Act 1964 and relevant environmental permitting legislation. As a result, the Home Office believes that unscrupulous dealers overtime, the dealers who offer the principal market for stolen metal, will be closed. With fewer markets to sell to, we believe this should reduce the attractiveness of metal as a criminal commodity.

This will be enhanced further by the Bill creating a new central public register, hosted by the Environment Agency, of all individuals and businesses licensed as scrap metal dealers. Whilst this register has many benefits, one will be providing local authorities and the Environment Agency with the ability to check what licences and environmental permits are held by scrap metal dealers to ensure that the dealers have obtained the licences required to operate. We would anticipate that the licensing authority and the Environment Agency will then take appropriate action to ensure that dealers have the correct licence. This will contribute to driving trading standards across the industry by ensuring that all scrap metal dealers are appropriately licensed/permitted to operate and that those businesses that are not identified and tackled.

The Bill will place an onus on the scrap metal dealers to verify the identity of individuals selling metal. The Home Office believes that one of the current drivers behind the theft of metal is the ability to sell it to certain scrap metal dealers anonymously. The Bill will require the scrap metal dealer to take steps to verify the seller‟s identity and to record it for a period of two years – this will be supported by a criminal sanction for any dealer who fails to fulfil this requirement or for a seller who provides false details. This provision is therefore expected to deter thieves who will now have to supply identification to sell stolen metals.

The Bill will incorporate the cashless offence, introduced via the LASPO Act, into this regime as a licence condition. The Home Office believes that cash in hand and the untraceable nature of the payment offers metal sellers a considerable reward for stealing metal; by requiring payment either by cross-cheque or electronic transfer will ensure that payments have greater traceability which should act as a further deterrent.

The Bill will widen the definition of scrap metal dealers, including itinerant collectors and motor salvage operators. This will include other businesses that it is felt could also purchase stolen metal, so further restricting the stolen metal markets.

Finally, the Bill will allow local authorities to charge a licence fee to cover the costs of administration and direct compliance activity of this regime. Under the 1964 Act, local authorities are not allowed to charge a fee to register scrap metal dealers; consequentially we have seen mixed compliance activity by local authorities with some doing very little. By allowing local authorities to charge and generate funds for a licence, it should result in considerable more activity by local authorities to ensure that licence holders are complying with the conditions of the licence; this should also act as a greater deterrent to get scrap metal dealers to comply.

13

E. Appraisal (Costs and Benefits)

GENERAL ASSUMPTIONS & DATA

The following appraisal considers the costs and benefits associated with the implementation of the proposed policy option in comparison with the baseline „do nothing‟ option. General assumptions used throughout the analysis are set out below. Any additional assumptions are discussed as they arise. As a number of assumptions have been made, sensitivity analysis has been completed and is presented in Section F. This demonstrates the scale and direction of potential error in the assumptions that have been made.

There are at least 2,631 registered scrap metal dealers. The exact number of dealers registered with local authorities is not collected centrally but, as of 1 May 2012, the Environment Agency have permitted 831 metal recycling sites and an estimated 1,800 metal recycling sites have obtained a registered exemption. This gives a lower bound estimate of 2,631.

There are approximately 1,775 registered end of vehicle life sites. These are assumed to be already registered as scrap metal dealers and included within the 2,631 figure.

Amendments to the Legal Aid, Sentencing and Punishment of Offenders Act are assumed to form part of the baseline unless stated otherwise.

Operation Tornado is assumed to have been rolled out nationwide, as this is due to happen before implementation of the proposals in this IA. As a result 25 per cent of scrap metal dealers are estimated to comply voluntarily with additional identification requirements proposed. This proportion is far lower than experienced in pilot regions but is expected to reflect a conservative estimate of continued voluntary compliance once Operation Tornado is finished.9

Poor data availability means that the total cost of metal theft to the UK is difficult to truly ascertain. We assume that the annual cost of metal theft to the UK as a whole is at least £220m, as reported in Annex A of the LASPO impact assessment10. This is likely to represent a conservative estimate. The majority of this cost (95%) is estimated to be for UK business.

The actual cost of metal theft will fluctuate against costs on the metal commodity market. If the price of certain metals continue to rise, it is likely that the incidence of metal theft will rise as well as their replacement cost. For simplicity, and because of the absence of a robust estimate of total cost, it has been assumed here that the total market value cost of metal will remain constant over the next 10 years.

The hourly cost of an employee is generally assumed to be £15, a standard assumption used in previously published impact assessments and based on the Standard Cost Model.

There is no direct evidence upon which to base estimates of the probable reduction in metal theft brought about through this policy option or the options considered in the LASPO impact assessment. However, it is believed that the potential reductions, as a proportion of the total estimated cost, could be very large because:

Metal theft is largely driven by opportunity (for example, rising prices, ease of disposal and availability of metals make it attractive in comparison to other acquisitive crimes) and is highly variable compared to other crime types: the number of copper thefts has more than doubled since January 2009, probably because of the rising price of copper. Therefore the imposition of a large risk and to offenders (through reducing the ease of disposal at scrap metal dealers and increasing their traceability) could produce a correspondingly large reduction in crimes.

The disposal of stolen metal at scrap metal dealers is thought to be the principle avenue for offenders to profit from stealing metal; estimated by ACPO to be in excess of 95% of the stolen metals market. ACPO do not currently have any intelligence to suggest that scrap metal is being directly exported, although they continue to work with law enforcement partners to monitor this. Taking steps to close the current market for stolen metal should

9 Sensitivity analysis demonstrates the potential impact and direction of error in this assumption. Results for between 0 and 50 per cent

voluntary compliance are presented in Section F. 10

Impact Assessment HO0058 published on the Ministry of Justice website (2011)

14

therefore reduce the attractiveness of stealing metal in the first place. We are conscious of displacement and a potential move to the direct export market and we are in discussion with law enforcement organisations, port authorities and others to identify strategies to tackle this.

The estimated number of scrap metal dealers is relatively small, making effective enforcement by police forces, local authorities, the Environment Agency and HM Revenue and Customs of the proposed changes more possible. There is considerable enforcement work already underway, however these agencies have been hampered by the inability to close unscrupulous dealers, the difficulties in obtaining evidence due to the lax record keeping requirements of the 1964 Act. In addition, local authorities have not been funded through this Act for such activity; the new Bill will provide them a fee to cover their compliance activities.

Motor salvage operators are current excluded from the regulation under the Scrap Metal Dealers Act 1964 which was considered a loophole that the scrap metal industry could exploit by pretending to be an operator as opposed to a scrap metal dealer; we have included them within this regime, repealing Part 1 of the Vehicles (Crime) Act 2001.

Existing schemes have reported significant successes, for example Operation Tornado‟s success as reported in Section B. And ACPO representatives estimated that the full range of proposed measures (including those covered in the LASPO impact assessment) could reduce metal theft by as much as 75% of which 30% might be due to a new license regime.

Despite the expectation that the policy options could result in large reductions in metal theft, we have not attempted to predict the crime or criminal justice system reduction benefit that could result from these measures. There is great uncertainty involved and reporting a very large range of potential crime reduction benefits is not considered helpful. As crime reduction benefits could not be estimated a breakeven analysis has been conducted. This demonstrates the crime reduction benefits necessary in order to outweigh the expected costs of the policy. This is presented at the end this section.

OPTION 2 – Introduce the Scrap Metal Dealers Bill to amend the law relating to scrap metal dealers.

COSTS The main additional costs resulting from implementing option 2 are:

cost to scrap metal dealers of applying for licences and complying with the licence conditions;

cost to local authorities of gathering evidence for licence applications and dealing with appeals of decisions to refuse scrap metal dealer licences;

cost to local authorities of enforcing licence conditions;

cost to Environment Agency of hosting a new, central register of scrap metal dealers;

cost of police-ordered review of licences; and

cost of additional offences prosecuted under the Scrap Metal Dealers Act. There are at least 2,631 registered scrap metal dealers. It is assumed that the proposals will not affect the number of dealers registering with local authorities. However, local authorities may, on completion of police and background checks, decide that certain dealers are not suitable to hold scrap metal dealer licences. The proportion of current dealers which this might affect is not known and the Environment Agency does not have details of the number of permit applications that they refuse. This analysis will assume that the number of dealers registered remains unchanged. Transition costs Transition costs of implementing the proposed changes will primarily fall to the Environment Agency in setting up a central register of scrap metal dealers. It is expected that this will be similar to the existing Flycapture database which holds information on flytippers. The costs are estimated by the Environment Agency to lie between £250k and £1m to set up a system with annual support costs falling between £50k and £175k. Staffing costs would be additional to this but could not be estimated. These estimated costs are preliminary and the Home Office will be working with the Environment Agency to ensure the most cost-effective approach to developing an appropriate system is taken.

15

Other transition costs are likely to fall to local authorities as they amend existing administrative systems for registering scrap metal dealers. This could include amending website application forms, as well as amending records they have of dealers‟ details. We assume this will require 6 hours of one administrative employee‟s time for each LA costing approximately £32,000 in total11. Licensing process Under these proposals, scrap metal dealers will have to pay a licence fee in order to register with local authorities. They will be expected to provide some limited additional information when applying for a licence such as the environmental permits they hold, previous scrap metal dealer licences and all commercial premises that the licence will cover.

Fee: estimated to be some £500 paid every three years on application or renewal of licence

Additional cost of completing application form: £3.75 – assumed to require 15 minutes of additional time for an employee earning £15 per hour12, every three years.

The fee will be set by local authorities. In order to give an indication of the possible impact on business, investigative work has been carried out in an attempt to determine the additional administrative costs of the new regime which the fee would cover. Estimates of costs were obtained from several local authorities in addition to known costs from local administration of gambling licences (thought to be a similar regime in terms of administration costs). Finally the range of fees paid by scrap metal dealers in Scotland was studied. These sources indicated that a fee in the region of £500 would be likely. However, since the actual fee level would be at the discretion of local authorities, it is acknowledged that the true business impact may differ from that estimated. The high cost scenario assumes the value of the fee would be £1,000. The total cost to business of paying the license fee is estimated at £440,000 per year. This figure reflects the lower bound of believed scrap metal dealers, the ones who are permitted by the Environment Agency; it is possible that more dealers will require a licence than we are aware of. In addition to the licensing costs, additional costs could be incurred by local authorities if a dealer chooses to appeal the refusal or revocation of a licence. In this case, appeals would follow existing procedures in place for other locally administered licensing schemes. There would be an opportunity cost for this system as time spent dealing with scrap metal dealers‟ licence appeals would prevent the panel from dealing with appeals against other licence refusal decisions. This would be an opportunity cost of approximately £1,300 per case to local authorities13 and a cost of £1,350 per case to businesses14. Since there are no refusals currently, we have had to assume a range of potential refusals. We assume an upper bound scenario where 5% of applications are refused annually and 50% of these are appealed and a lower bound of zero refusals. The best estimate assumes 2.5% of applications are refused and 50% appealed. A small number of appeals may ultimately lead to the magistrates‟ court to appeal decisions made at the local authority panel stage. We have not been able to monetise these costs but they would involve costs to the magistrates‟ court (HMCTS), as well legal counsel for the dealer and the local authority or police force. It is expected that only a few cases will be brought before a magistrates‟ court, so the costs are expected to be minimal. Enforcement Scrap metal dealers are already legally required to keep records of all transactions which must be made available to local authorities to ensure compliance with the regime. The only additional requirement of scrap metal dealers in order to comply with the revised regulations in Option 2 is to keep a copy of the identity documents provided by the seller. The Home Office have consulted with representatives of the scrap metal industry15 who already fulfil this requirement as part of their routine business. The two companies we spoke to both state that they can complete an identification check and record the identification of the seller on their internal systems within 3 minutes – their processes would meet their obligation under this Bill. They have also stated that

11

Assuming an administrative employee costs £15 per hour and there are approximately 350 local authorities. 12

Using a standard assumption that the cost of a scrap metal dealer‟s time is £15 per hour 13

Administrative cost of an appeal of the refusal of an alcohol licence. 14

Based on the cost to licence holders of companies applying for alcohol licences. 15

This assumption was made in consultation with two scrap metal dealers (Alchemy Metals and SITA UK).

16

transactions that involve repeat customers or customers who are aware of the process make completing the requirement even quicker. We have therefore assumed that it would take scrap metal dealers a maximum of five additional minutes of a dealer‟s time, per transaction from an unknown customer, to complete. It is assumed that 65 transactions are completed per dealer per day of which 10 per cent involve new customers16. The additional transaction unit cost for dealers is approximately £1.2517. This gives an annual cost per dealer of approximately £2,100. As initial compliance with Operation Tornado in the North East is over 80 per cent18 and Tornado will be national by the time this policy would be implemented, it is assumed that 25 per cent of dealers will already be voluntarily complying with this requirement - information from ACPO has illustrated that compliance rates across the country where Tornado is live are comparable, with more sites signing up as the Operation is launched and then matures in each region. These costs will only be relevant to those dealers not complying. It is estimated that approximately 1,315 dealers will be affected. This would lead to total estimated costs of £4.1 million per year. The Home Office believes that much of this cost could be opportunity in nature in that many businesses will be able to absorb the costs without having to employ additional resources. The additional transaction time is also a cost to customers. Our best estimate is that 50% of scrap metal customers are businesses and 50% are members of the public19. The average wage of these customers could differ from that of the scrap metal dealers. However, there is no detailed information on customers to help inform this. Therefore, for simplicity, we have assumed that the average wage, including on costs, is £15 per hour – the same as assumed for scrap metal dealers. The same assumptions as described above for proportion of new customers and proportion of dealers already complying remain the same. The annual cost to customers is therefore £2.0 million to business and £2.0 million to individuals. Note, however, that repeat customers to whom no cost applies (because dealers will already hold their details) are more likely to be businesses. The estimates above are therefore likely to overestimate the business impact and underestimate the individuals‟ impact. It is possible that businesses will also have to spend additional time demonstrating to local authorities that they are compliant with the proposed regulations. It is not envisaged that this will be a large additional burden as scrap metal dealers are already legally required to keep records of all transactions which must be made available to local authorities to prove compliance. The addition of identity documents to this requirement should not be onerous for scrap metal dealers. It is possible that, due to additional fee income for local authorities, that enforcement checks could become more frequent. As the extent to which these additional enforcement checks may occur cannot be forecasted (nor will there frequency be specified in legislation), it has not been possible to quantify the additional cost to scarp metal dealers. As the additional information that would need to be provided in order to prove compliance is the log of identity documents of sellers, this cost is thought to be minimal. In addition to enforcement activity carried out by local authorities and the Environment Agency (see „Additional Services‟ below), the police can also order a review of any scrap metal dealer‟s licence. This process would be administered by the local authority rather than the police so would represent an additional opportunity cost to local authorities. Additional costs to the police are likely to be small per review but may require a reallocation of resource. No additional police officers would be required. The unit cost of a police officer‟s time is £36.81 per hour20. The total opportunity cost to the police is dependent on the extent to which this power would be used which is unknown. It is thought that changes to the enforcement of existing scrap metal dealers could lead to an increase in the number of offences taken forward under the SMDA 1964. In 2010, 18 convictions were obtained and it is likely that this will increase under the new, stricter proposals, not least as a result of greater focus by local authorities with the funding given to compliance activity. It is unlikely

16

These assumptions come from anecdotal evidence provided by the British Metals Recycling Association. 17

Using a standard assumption that the cost of a scrap metal dealer‟s time is £15 per hour. 18

ACPO, 2011, Operation Tornado briefing 19

Based on the opinion of the British Metal Recycling Association. 20

This was calculated in 2008 using Annual Survey of Hours and Earnings (ASHE) and Chartered Institute of Public Finance and Accounts

(CIPFA) data. Estimates have uprated to account for inflation using the HM Treasury deflator series.

17

that there will be any more cases brought before courts under the Theft Act 1968 as it is understood that considerable numbers are already being brought. The offences are summary and will result in financial penalties of between level 3 to 5 on the standard scale. The offences will cover both individuals and businesses. Legal aid is not available for these offences, and none of the offences will have a custodial sentence. Therefore, there would be no impact on the Legal Services Commission, prisons or probation. The costs of these convictions are estimated as follows:

cost to HMCTS: for magistrates court time are approximately £525 per case, assuming 2 hours of court time is required;

cost to Crown Prosecution Service: for magistrates court are approximately £143 per case. These figures have been provided by the Ministry of Justice and are in 2011 prices. As stated above there are no costs to the Legal Services Commission, HM Prisons, or the National Offender Management Service (NOMS). This gives an average cost of £668 per offence. The number of additional offences likely to be prosecuted is not known so our best estimate assumes a doubling to 36 offences. This is to reflect the stricter proposals as well as any increase in enforcement activity. This would represent an additional cost of approximately £12,000 to the Criminal Justice System, almost £10,000 of which falls to HMCTS. These additional offences could lead to more fine enforcement activity being required, but this could not be quantified. Additional costs to the CJS system could result from the appeals process as described above. These costs could not be quantified. Additional Services Local authorities will need to undertake checks to ensure that dealers applying are suitable to hold a licence. This will involve consulting relevant police forces and running relevant background checks. Where applications are successful, the local authority will be required to input the relevant information onto the national database. The licence fee will be set to cover the costs to local authorities of running and enforcing the licensing scheme. As a result, the fees should offset the costs of issuing and enforcing licences. However, they will not offset any additional costs resulting from appeals of dealers who are unsuccessful in their applications for licences. This is considered in the sensitivity analysis in Section F. A range of agencies will continue to be involved in the enforcement of the proposed Scrap Metal Dealers Bill but most activity will be carried out by local authorities. As it currently the case, the relevant local authority will be responsible for ensuring compliance of the direct conditions of the licence. This includes ensuring that dealers are maintaining accurate records of transactions and not buying scrap metal for cash. Although local authorities are expected to already fulfil this compliance function, it is expected that compliance activity will increase because fee income from this new regime will enable more resources to be applied. The fee will be collected at the point of application. Enforcement costs will also fall to the Environment Agency. They will be responsible for comparing the new, central register of scrap metal dealers to their registers of environmental permits and deal with any discrepancies. The Environment Agency is also required to take compliance/enforcement action against scrap metal dealers who do not have the necessary environment permits; it is estimated that there are between 120 and 16021 dealers where enforcement action is being taken. This is routine business for the Agency. These additional services are to be funded by the new fee from scrap metal dealers. Therefore the combined value of the services is assumed to equal the total fee income (£440,000 per year). We have not been able to break down the cost of additional services between local authorities and the Environment Agency. The cost of any appeals of licence decisions are assumed to be outside this arrangement and the costs to local authorities have been considered separately. Please see annex A for further information on likely costs of this new regime. BENEFITS

21

As estimated by the Environment Agency.

18

Crime These measures are designed to tackle non-compliant scrap metal dealers more effectively than the current regulations set out in the Scrap Metal Dealer‟s Act 1964. Option 2 is likely to reduce metal theft for the reasons outlined in Section D. Recent Home Office estimates of the costs of metal theft suggest that it costs the UK £220 million each year22. As explained above, we have not estimated a crime reduction benefit, due to the large potential range of outcomes. Instead, the reduction that would be required in order to offset the net costs of each scenario is reported in the Net Effect section below: Fees Local authorities will receive fee income from scrap metal dealers. This is estimated to total £440,000 per year. This fee will cover the cost of administering the licence and LA enforcement of the requirements. Under the proposed changes in the Scrap Metal Dealers Bill, end of life vehicle sites will no longer need a separate licence in order to operate. As they currently pay a licence fee, this will represent a benefit to the 1,775 firms with these licences. The fee paid varies by local authority but is estimated to be approximately £100 every three years. This represents a total saving of £60,000 to businesses. There will also be a small additional saving to businesses that no longer have to complete the registration process for this licence scheme. This benefit has not been quantified. Additional Services Fee income will fund additional services as explained in the „Costs‟ section. While the benefits of the provision of additional services are expected to largely be in the form of a crime reduction effect, there may be other non-identified, non-quantified benefits. For instance, efficiency savings resulting from closer working relationships between authorities and scrap metal dealers. No such additional benefits have been quantified, however. CJS Fines If more convictions due to non-compliance are made then there will be additional fine income to the Criminal Justice System. Our best estimate assumes that the 18 convictions made in 2010 would double to 36 under the new Act. The average fine set for summary offences committed by companies and public bodies is £70523. Assuming that all convictions result in a fine for offenders, the total additional fine income is estimated to be approximately £13,000 per year. At present the money collected in relation to fines goes to Her Majesty‟s Treasury to the Consolidated Fund and the MoJ gets a proportion of this back under the Fines Incentive Scheme. NET EFFECT The net effect of this policy is a cost of £74.8 million over ten years as demonstrated in Table E.1. A number of assumptions were made in the calculation of the costs and benefits of Option 2. A sensitivity analysis has been conducted in order to demonstrate the scale and direction of potential error resulting form these assumptions. The details and results of this analysis can be found in Section F.

22

LASPO impact assessment, Annex 1 23

Taken from Ministry of Justice, Sentencing Statistics 2011.

19

Table E.1

Agency Annual Average Net Benefit (£m)

Present Value Net Benefit (£m)

Business -£6.5 -£55.7 Individual metal sellers -£2.0 -£17.4 Local authorities -£0.0 -£0.03 Environment Agency -£0.2 -£1.6 Criminal Justice System £0.0 £0.01

- HMCTS £0.0 £0.03 - CPS £0.0 -£0.02

Total -£8.7 -£74.8

The net present value is negative, however crime reduction benefits have not been included in the calculations. As we cannot forecast the extent to which crime will be reduced by Option 2, Table E.2 reports the reduction that would be required in order to offset the costs of the policy. This is reported for the „best estimate‟ scenario (as in Table E.1) and the low and high scenarios. Table E.2

Scenario Low Best High

Net cost (average annual) £0.5m £8.7m £56.1m Required crime reduction 0.2% 3.9% 25.5%

See Annex A, part 6 for explanation of breakeven analysis

ONE-IN-ONE-OUT (OIOO) This policy falls within the scope of one-in-one-out with the measures considered an IN. Costs (INs) The additional burden of paying a licence fee and complying with the new requirements for scrap metal dealers represents a regulatory IN. This is quantified as £6.5 million per year, with a 10 year present value of £56.2 million. Benefits (OUTs) The integrating of the motor salvage licences into the proposed Scrap Metal Dealers Bill would reduce the duplication of licences for some scrap metal dealers. The fees saved as a result of this are estimated to be £0.06 million per year, with a 10 year present value of £0.5 million. This is considered an OUT. Crime reduction benefits fall mainly to business but are considered indirect effects and therefore out of scope for OIOO. NET The net impact on business is estimated to be a cost of £6.5 million per year, with a 10 year present value of £55.7 million. It should be noted that much of the cost to business of complying with the new requirements could be opportunity in nature: many businesses are likely to be able to absorb the costs without having to employ additional resources.

20

F. Risks

OPTION 1 – DO NOTHING

Metal Theft continues to escalate

Mitigation:

Steps proposed in option 2 will re-regulate the scrap metal industry which will in turn tackle the substantial market for stolen metal.

Enforcement action by a number of agencies should continue, or could be enhanced, should it be considered a local problem.

OPTION 2 – REPLACE AND REVISE THE SCRAP METAL DEALERS ACT 1964.

Local Authorities do not prioritise enforcing this issue.

Mitigation:

Funding through a licence fee will equip local authorities with the additional resources they need to effectively administer and ensure compliance with this regime.

More effective deterrents for offences under the new regime including unlimited fines and the power to revoke licences should encourage local authority involvement.

Significant awareness raising is underway to promote action in this area amongst agencies.

Criminals by-pass legitimate scrap metal dealers, increasing the number of illegal sites/exports. Mitigation:

The Environment Agency has recently formed a new enforcement unit to tackle scrap metal dealers who do not have a permit and so are therefore acting illegally.

Border Force, SOCA, HMRC and Police are undertaking a greater focus on the ports to identify whether the export market for stolen metals.

Key Assumptions

The number of dealers - 2,631 - is thought to be a lower bound estimate. However there was no information available on which to base an upper bound estimate. Therefore this assumption brings with it a downside risk to the estimated net present values.

The estimated annual cost of metal theft - £220m – is likely to be an underestimate. Therefore this assumption brings with it an upside risk to estimated net present values. It is possible that the true cost of metal theft is significantly greater. For example, the Association of Chief Police Officers placed an annual cost of metal theft to the UK of £777m in 2010. Therefore the potential crime reduction benefits from this policy could also be significantly greater.

Business compliance - The major cost component of Option 2 arises from businesses being required to record details of clients. This calculation relies on an estimated number of dealers (see above), an estimated daily volume of transactions (65), an estimated number of working days, an estimated hourly wage (£15), an estimated proportion of „new‟ customers (10%), and an estimated existing compliance (25%). Some of these estimates are tested in the sensitivity analysis below but it should be noted that the estimated compliance cost to business is subject to considerable uncertainty. Fairly minor adjustments to these assumptions, when combined, could lead to the overall cost estimate, and the resulting net present value of the policy being considerably lower or higher.

Additional offences – 18 – is likely to be an overestimate of the number of additional offences resulting from Option 2 as this doubles the number of convictions obtained in 2010. However if additional offences were prosecuted, there could be additional costs for HMCTS and the CPS.

21

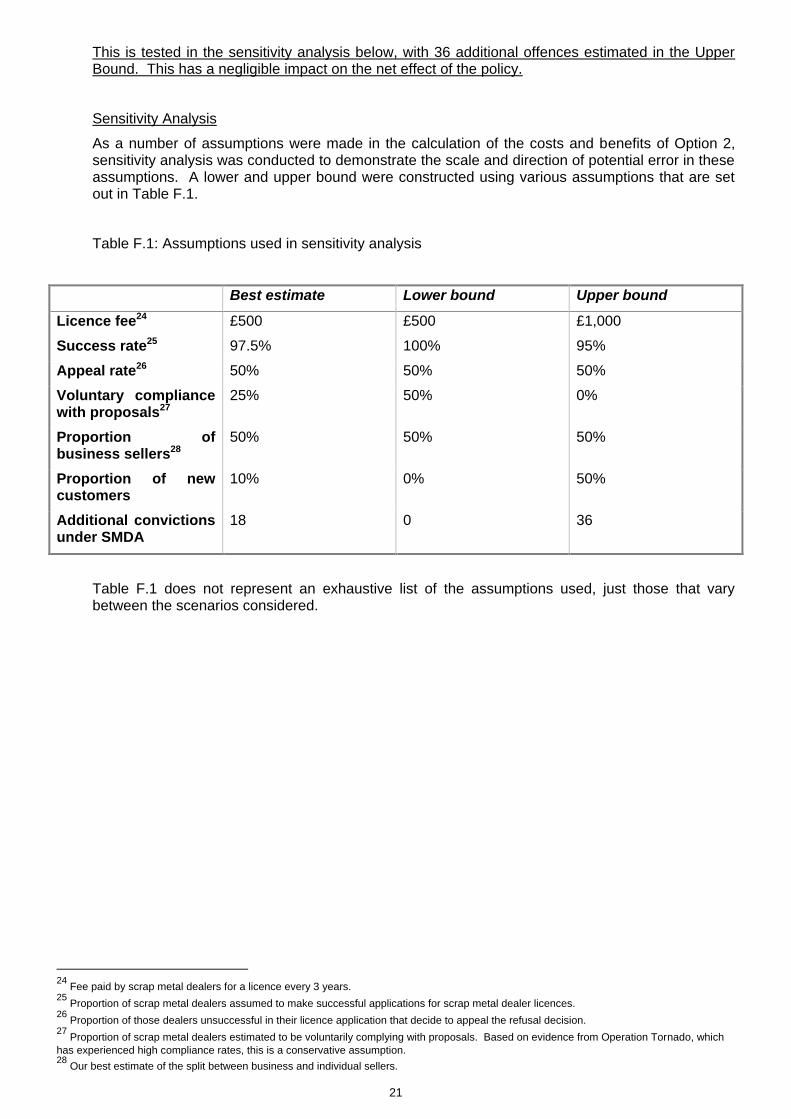

This is tested in the sensitivity analysis below, with 36 additional offences estimated in the Upper Bound. This has a negligible impact on the net effect of the policy.

Sensitivity Analysis

As a number of assumptions were made in the calculation of the costs and benefits of Option 2, sensitivity analysis was conducted to demonstrate the scale and direction of potential error in these assumptions. A lower and upper bound were constructed using various assumptions that are set out in Table F.1.

Table F.1: Assumptions used in sensitivity analysis

Best estimate Lower bound Upper bound

Licence fee24 £500 £500 £1,000

Success rate25 97.5% 100% 95%

Appeal rate26 50% 50% 50%

Voluntary compliance with proposals27

25% 50% 0%

Proportion of business sellers28

50% 50% 50%

Proportion of new customers

10% 0% 50%

Additional convictions under SMDA

18 0 36

Table F.1 does not represent an exhaustive list of the assumptions used, just those that vary between the scenarios considered.

24

Fee paid by scrap metal dealers for a licence every 3 years. 25

Proportion of scrap metal dealers assumed to make successful applications for scrap metal dealer licences. 26

Proportion of those dealers unsuccessful in their licence application that decide to appeal the refusal decision. 27

Proportion of scrap metal dealers estimated to be voluntarily complying with proposals. Based on evidence from Operation Tornado, which

has experienced high compliance rates, this is a conservative assumption. 28

Our best estimate of the split between business and individual sellers.

22

Table F.2: Sensitivity analysis results, annual average figures

Table F.2 demonstrates the costs and benefits associated with each estimated scenario.

Best estimate

Lower bound Upper bound

COSTS (£m) £9.1 £1.0 £57.0

- Business costs £6.5 £0.4 £41.9

- Individual costs £2.0 £0.0 £13.9

- LA costs £0.4 £0.4 £1.0

- EA costs £0.2 £0.1 £0.3

- CJS costs £0.01 £0.00 £0.02

BENEFITS (£m) £0.5 £0.5 £1.0

- Business benefits £0.1 £0.1 £0.1

- LA benefits £0.4 £0.4 £0.9

- CJS benefits £0.01 £0.00 £0.03

NET BENEFIT29 (£m)

-£8.7 -£0.5 -£56.1

- Business -£6.5 -£0.4 -£41.8

- Individuals -£2.0 £0.0 -£13.9

- LA £0.00 £0.00 -£0.09

- EA -£0.2 -£0.1 -£0.3

- CJS £0.01 £0.00 £0.01

HMCTS £0.03 £0.00 £0.06

CPS -£0.02 £0.00 -£0.04

29

Negative figures indicate net costs rather than the net benefits, that is the costs are greater than the benefits.

23

G. Enforcement

The SMDA 1964 is currently enforced by local authorities and police forces. We propose a similar approach with this proposal, but with local authorities primarily responsible for ensuring compliance. Police forces, local authorities, the Environment Agency, HM Revenue and Customs and the Serious and Organised Crime Agency are already undertaking significant enforcement activities against those committing metal theft offences and the unlawful scrap metal dealer industry across England and Wales. Such activities include individual and multi-agency operations and national days of action. The Police Response and the National Metal Theft Taskforce These activities have been complemented and expanded by £5m of additional Government funding through the National Infrastructure Plan in November 2011 to cover the 2011/12 and 2012/13 financial years. The Government made this funding available to support and enhanced law enforcement response to bridge the gap between new legislation which was considered necessary. Such activity also includes supporting multi-agency intelligence collation and analysis on all operating scrap metal dealers across the United Kingdom and the wider market for stolen metal. There have been no discussions across Government as to whether further funding will be provided after 2012/13. If no funding is provided, it is anticipated that all further compliance and enforcement activity will be delivered as part of routine business through existing budgets. The taskforce has six agreed key strategic objectives:

1) Reduce the theft of metal;

2) Increase the level of offenders brought to justice in relation to metal theft and non compliance

with current legislation;