to be among the best performing retail-focused ... 24-25.11.2016/24.11_11.30-12.15.pdf · to be...

TRANSCRIPT

1

To be among the best performing retail-focused institutions in Europe

KBC wants to be among Europe’s best performing retail-focused financial institutions. This will be achieved by:

Strengthening our bank-insurance business model for retail, SME and mid-cap clients in our core markets, in a highly cost-efficient way

Focusing on sustainable and profitable growth within the framework of solid risk, capital and liquidity management

Creating superior client satisfaction via a seamless, multi-channel, client-centric distribution approach

By achieving this, KBC wants to become the reference in bank-insurance in its core markets

2

Well-defined core markets provide access to ‘new growth’

KBC Group’s core markets BE CZ SK HU BG

Loans and deposits

Investment funds

Life insurance

Non-life insurance

MARKET SHARE (END 2015)

21% 19% 11% 10%

3%

7% 18% 26% 40%

7% 17%

12% 4% 4%

10% 5% 3%

7% 9%

IRELAND

UK

BELGIUM

NETHERLANDS

GERMANY

CZ

FRANCE

SK

HU

BG

Macroeconomic outlook: based on GDP, CPI and unemployment trends / Inspired by the Financial Times

3

Overview of key financial data at 2Q 2016

Market cap: EUR 20bn

Net result 1H 2016: EUR 1.1bn

Total assets: EUR 266bn

Total equity: EUR 16bn

CET1 ratio (Basel 3 transitional): 14.9%

CET1 ratio (Basel 3 fully loaded): 14.9%

S&P Moody’s Fitch

Long-term (KBC Group)

A (Negative) BBB+ (Stable)

A1 (Stable) Baa1 (Stable)

A- (Positive) A- (Positive)

Short-term A-1 Prime-1 F1

Net result 1H 2016: EUR 1.0bn1

Total assets: EUR 230bn

Total equity: EUR 14bn

CET1 ratio (Basel 3 transitional): 13.5%

CET1 ratio (Basel 3 fully loaded): 13.6%

C/I ratio 1H 2016: 60%2

Net result 1H 2016: EUR 123m

Total assets: EUR 38bn

Total equity: EUR 3bn

Solvency II ratio: 187%

Combined operating ratio 1H16: 95%

KBC Group KBC Bank KBC Insurance

Credit Ratings of KBC Bank (KBC Group) as at 1 August 2016

1. Includes KBC Asset Management ; excludes holding company eliminations

2. Adjusted for specific items, the C/I ratio amounted to c.56% in 2Q 2016

4

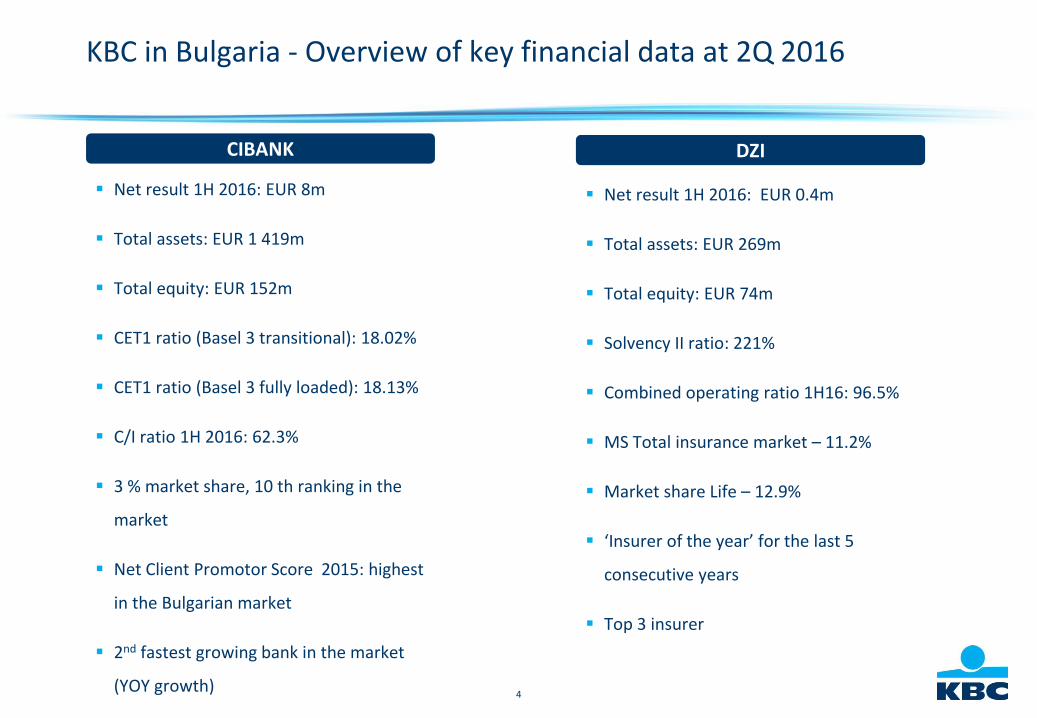

Net result 1H 2016: EUR 8m

Total assets: EUR 1 419m

Total equity: EUR 152m

CET1 ratio (Basel 3 transitional): 18.02%

CET1 ratio (Basel 3 fully loaded): 18.13%

C/I ratio 1H 2016: 62.3%

3 % market share, 10 th ranking in the

market

Net Client Promotor Score 2015: highest

in the Bulgarian market

2nd fastest growing bank in the market

(YOY growth)

CIBANK DZI

Net result 1H 2016: EUR 0.4m

Total assets: EUR 269m

Total equity: EUR 74m

Solvency II ratio: 221%

Combined operating ratio 1H16: 96.5%

MS Total insurance market – 11.2%

Market share Life – 12.9%

‘Insurer of the year’ for the last 5

consecutive years

Top 3 insurer

KBC in Bulgaria - Overview of key financial data at 2Q 2016

5

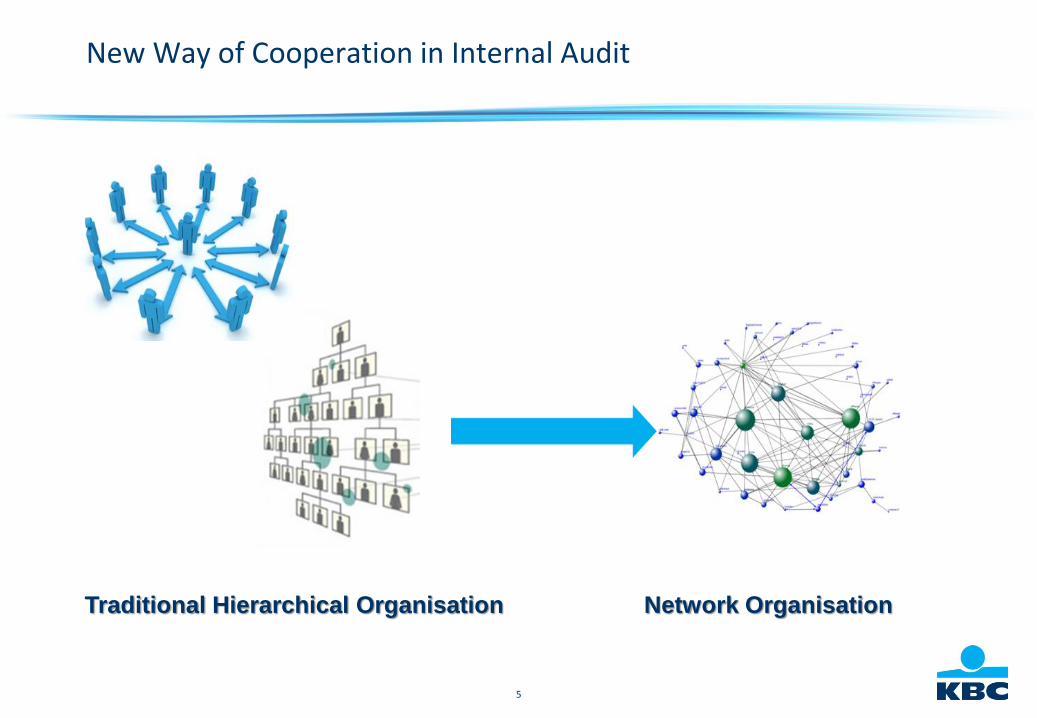

New Way of Cooperation in Internal Audit

Traditional Hierarchical Organisation Network Organisation

6

Core Objectives to guide Internal Audit

Be a trusted partner for Business;

Distribute knowledge;

Provide assurance regarding the status of the internal control system in a qualitative

manner and from an independent perspective;

Ensure relevant risks are identified and covered;

Be consistent throughout the group;

Provide clear and actionable recommendations that respect a balanced risk-return

environment;

Communicate in a timely, clear and comprehensive manner;

Get the job done in the most (cost) effective way;

Provide an inspiring environment for the employees in Internal Audit.

7

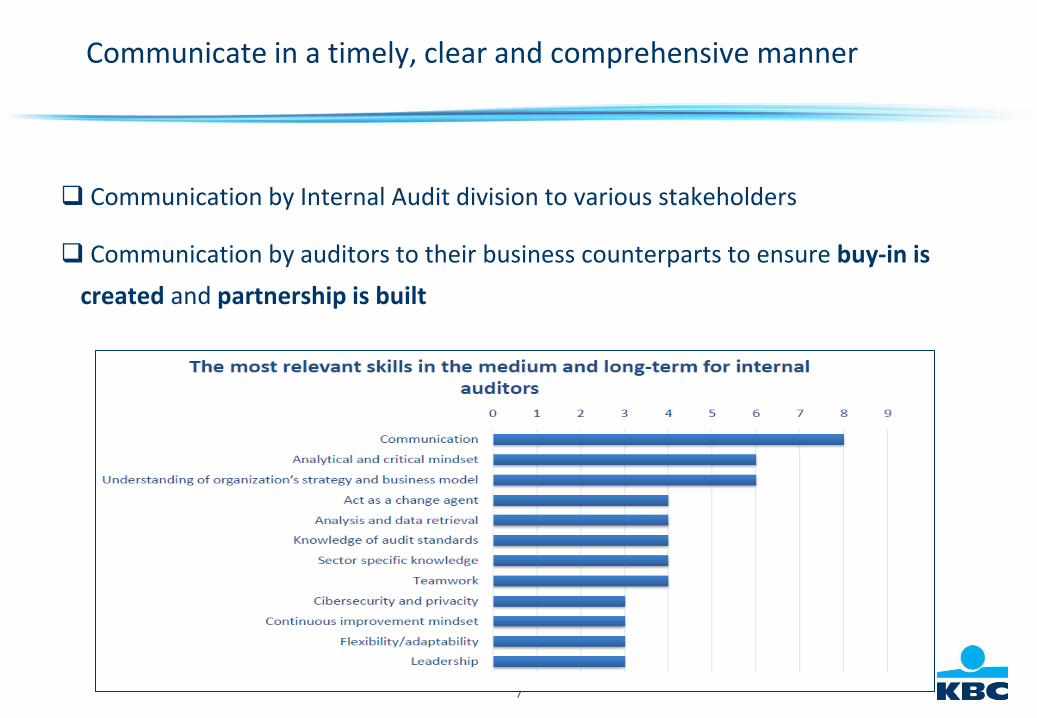

Communicate in a timely, clear and comprehensive manner

Communication by Internal Audit division to various stakeholders

Communication by auditors to their business counterparts to ensure buy-in is

created and partnership is built

8

Be a trusted partner for Business

Providing added value by:

Understanding the business dynamics

Consultancy/advisory services at the request of the Business

Organising the audit work in the least disruptive manner towards

the business activities

“In the end, you should become a Chief Challenging Officer. Someone the organisation can see as a coach in internal control, risk management and

governance.”

9

Get the job done in the most (cost) effective way

Quality comes at a cost (resource & time investment) but this needs to be

managed and there needs to be a balance between both

“newspaper editor attitude”

Efficiency Management should transcend the individual audit assignment and

should be applied portfolio-wise Plan realisation

10

Talking about the future – that is here

11

The impact of Technology

Automation, Standardization, digitalization, robotization, big data, IOT, internet sales,…

Putting standing business models under pressure but also creating opportunities. Need to: cut waste, simplify, standardize, fight bureaucracy Look for: innovation - new products, services and revenue streams Analyze: viability of (digital) strategies, investment cycles and saving opportunities

Examples of the banking sector: mobile digital distribution, fintech, immaterial, IP driven value of companies, new ways of financing- Crowdsourcing, start-ups, scale ups Blockchain applications

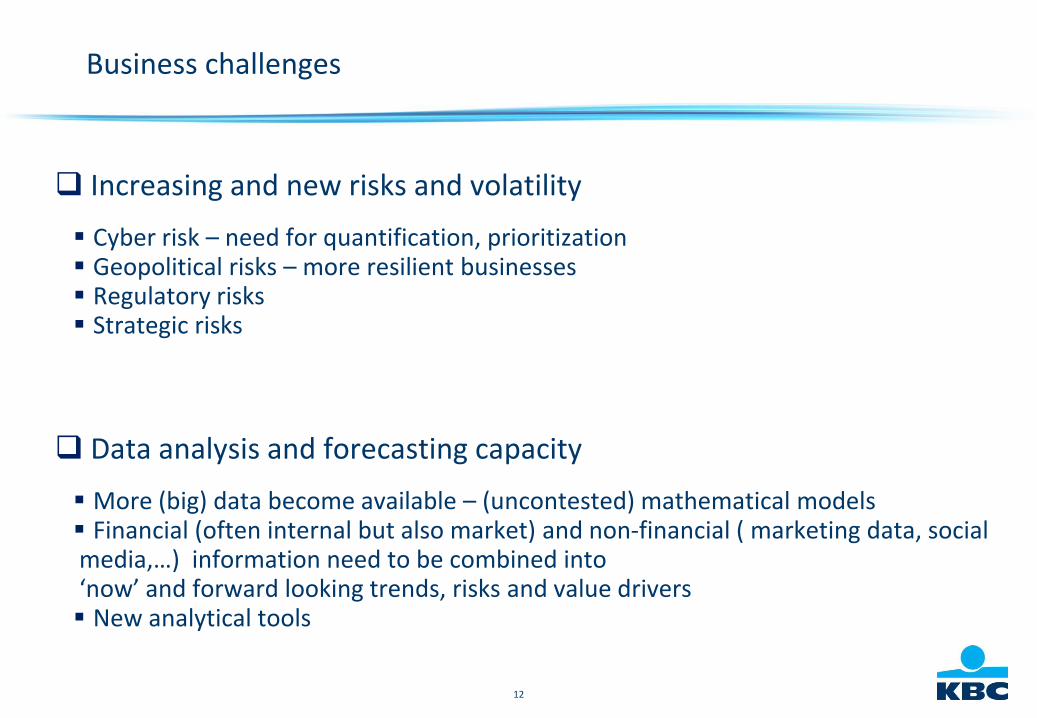

12

Business challenges

Increasing and new risks and volatility

Cyber risk – need for quantification, prioritization Geopolitical risks – more resilient businesses Regulatory risks Strategic risks

Data analysis and forecasting capacity

More (big) data become available – (uncontested) mathematical models Financial (often internal but also market) and non-financial ( marketing data, social media,…) information need to be combined into ‘now’ and forward looking trends, risks and value drivers New analytical tools

13

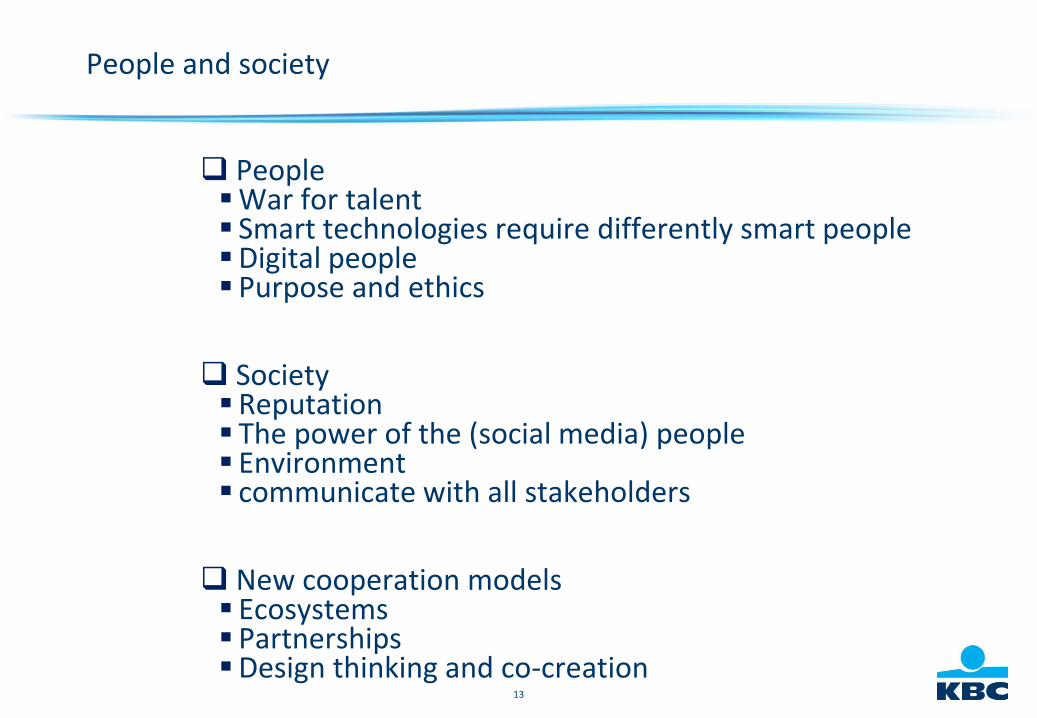

People and society

People War for talent Smart technologies require differently smart people Digital people Purpose and ethics

Society Reputation The power of the (social media) people Environment communicate with all stakeholders

New cooperation models Ecosystems Partnerships Design thinking and co-creation