to own right now for 1,000% gains - amazon web … explosive stock to own right now for 1,000% gains...

TRANSCRIPT

Paul Mampilly’s

Prof

3 Explosive Stocks to Own Right Now for

1,000% Gains

1

3 Explosive Stock to Own Right Now for 1,000% Gains

By Paul Mampilly, Editor of Profits Unlimited

THE stock market is primed and ready to run higher to 50,000, boosted with the help of a secret economic force.

In fact, this secret economic force has helped to fuel all the bull markets in the past. Starting with the first bull market started in 1897, stocks saw surge from massive population growth through “the Great Wave” — a time when over 25 million people immigrated to the United States. This flood of new people earned and spent … the economy grew … launching the stock market up 149%.

A second mass influx of people after the Great War, fueling the next bull market that saw stock rally 295%.

Of course, there was the boom that started in the 1982 was the biggest. The market exploded up 1,059% … more than the previous three bull market cycles combined. That’s because this last rally was directly tied back to the 77 million baby boomers … the largest demographic group America had ever seen.

1982 was when baby boomers started turning 34 years of age. This is critical, because 34 years of age is when people begin to elevate their careers, and make more money.

But, that money goes out the door fast because they are also entering their peak spending years. They are purchasing cars, having kids, buying houses, getting new appliances, and then buying bigger, newer cars; bigger, newer houses and so on. This all helped to drive the economy’s growth and push stocks significantly higher.

And now...

Millennials form the new wave of people are going to fuel the next growth in America. That’s because 92 million people … yes, 92 million people … are about to earn more, spend more, and invest more.

It’s like 1982 all over again.

Only bigger because there are 15 million millennials than the baby boomers.

And right now, they are entering the age where they will spend even more. Today, millennials account for $2.9 trillion in consumer spending. Next year that number is projected to hit $3.5 trillion. And according to Gallup, millennial spending will continue this rise for at least the next 15 years.

This is key, because for the first time ever, millennial spending will surpass baby boomer spending.

But unlike the baby boomers before them… this time, it’s bigger.

For this special report, I’ve selected three stocks that are set to explode higher over the next several years, benefitting from the growing buying power of the millennial generation.

A Rare Tech Stock Poised for a 300% Rise!IN 1979, Texas native Nelson Bunker Hunt controlled the silver market, notching gains of as much as $3.5

billion. He did it using the oldest trick in the book and several billions of dollars. Nelson and his brother, William Herbert Hunt, had already inherited billions from their father — legendary Texas wildcatter H.L. Hunt, who developed the East Texas Oil Field.

2

But that wasn’t enough. Nelson had a plan that could make them even richer. In early 1979, the price of silver was hovering around $6 per troy ounce when the Hunts began buying up as much physical silver as they could lay their hands on. They had such a hoard of the metal that Tiffany’s took out a full-page ad in The New York Times condemning their tactics.

But they still weren’t done. The Hunt brothers went on to load up on silver futures through the financial markets. When they ran out of their own money, they convinced sheikhs in Saudi Arabia to pour millions of petrodollars into the silver scheme. At one point, the brothers were estimated to hold one-third of the entire world supply of silver.

With too few sources to supply a steady stream of silver, the price of the metal skyrocketed, reaching a peak of $48.70 per troy ounce. A 712% rally! If you had been lucky enough to buy five troy ounces of silver at $6, that $30 investment would be worth $243 at the peak. Now imagine if you’d invested billions like the Hunt brothers….

With some careful planning and several billions of dollars, the Hunt brothers cornered the market. A corner creates a significant shift in the supply-and-demand balance of an asset by limiting the supply of that asset. By removing billions of dollars’ worth of physical silver from the market, the Hunt brothers crippled supply. Companies like Tiffany’s still needed to meet the demands of their customers if they wanted them to stay customers, so they had to pay higher and higher prices for silver.

It’s basic Econ 101 — shrinking supply in the face of steady or rising demand equals higher prices.

Now, cornering a market isn’t legal, and the Hunt brothers paid a steep price for their schemes. But that doesn’t mean a corner can’t still happen on occasion through natural alignments of various interests of investors. In this month’s issue, I’ll show you how a group of investors has made their own corner … however, they are not cornering silver.

They are cornering a stock. If you position yourself strategically, you could make up to 300%.

The Big PayoffI’ve been patiently watching this stock corner develop for almost five years now. Yes, five years! You see,

corners take time to develop. It’s almost like watching for stars in the sky to perfectly align. You don’t want to buy in the company too early, because the stock can be incredibly volatile while the corner is being executed.

But right now, we’re buying into a stock that I believe is effectively 100% cornered. In two or three months at the very latest, when people go to buy shares … they’re going to find none available. And the shares are going to soar. That means we have just a tiny window to get in.

And according to my research, a well-known billionaire, three major investment management companies and the company itself are the ones who have cornered the stock.

This stock is not some fly-by-night operation. It’s a major blue-chip technology company; an iconic American company that’s a major component of the Dow Jones Industrial Average and the S&P 500. In fact, the stock’s presence in these two major indexes is one of the reasons why I am so confident this corner is going to make us so much money.

The most important thing you need to understand is that we’re dealing with a time-sensitive issue. It’s absolutely critical you act on my information immediately. Once people figure out this stock has been cornered, everyone is going to rush to buy it. Just like everyone rushed to buy silver from the Hunt brothers in 1979.

If you’re late to the party with this stock, you’re going to miss out on some huge gains.

3

The Secret Reason Warren Buffett Broke His Own Rule

I don’t normally do this, but … it’s such a “boring” pick. More than a century old, this company’s products can be found in nearly every business around the globe and have touched countless lives. This blue-chip stock is a standard in conservative, predictable mutual funds. This is your father’s stock. No, your grandfather’s stock. It’s the old dog asleep in the sun on the porch, dreaming of the good ol’ days when it was running at the head of the tech pack. Now the Silicon Valley pack is snickering and laughing as it pulls ahead.

The company is IBM (NYSE: IBM).

But don’t brush it off already. This old dog has learned a new trick that is going to leave many of the Silicon Valley upstarts in the dust. And I’m not the only one to notice. Warren Buffett avoids technology stocks like the plague. He’s previously vowed to never buy a technology stock, preferring simple concepts, iconic brands and well-managed companies. But the “Oracle of Omaha” had found an exception to his rule. On November 14, 2011, Warren Buffett revealed on CNBC that he had bought a 5.5% stake in IBM for about $10.7 billion. That’s right: Buffett’s made a $10.7 billion investment in IBM.

He told CNBC that he did this over a couple of weeks. He’s revealed that his buy price was about $170. Since then, he’s upped his stake in IBM to where it’s now 8.6% of the company. He was the first piece in what was to become a massive cornering puzzle. Buffett was gobbling up IBM shares, removing them from the market.

So I started tracking IBM. Every quarter, I noticed that the company’s share count kept shrinking. I investigated further. That’s when I figured out the second culprit of this attack — IBM, the company itself! IBM has been swallowing up its shares like a whale eating minnows. You can see this in the chart below.

IBM has put in the second piece of the corner for its own stock by shrinking the supply of its shares by 36%. Nearly four out of every 10 shares that existed 10 years ago are gone now from the shares’ float — or total shares available for trading. And IBM is not done.

And IBM has set aside $4.7 billion to buy back even more shares in 2016. At current prices, that’s another 31.3 million shares that are going to leave the market. When you add in the 8.6% stake Warren Buffett owns, approximately 44% of the shares have effectively disappeared ... and won’t be available to buy.

IBM Shares Outstanding (in billions)

1.55

1.45

1.35

1.25

1.15

1.05

959.962008 2010 2012 2014 2016 million

4

Now, let’s add the third and final piece of the puzzle — the final group snatching up massive amounts of shares. You see, IBM is a component of the two biggest and most-followed stock indexes in the world — the Dow Jones Industrial Average and the S&P 500 Index. IBM represents 5.62% of the Dow Jones Industrial Average and 0.71% of the S&P 500. Huge amounts of money are invested in both these indexes. In fact, three big investment management companies dominate index funds — Vanguard, BlackRock and State Street. Between the three of them, they hold about 15% of IBM’s shares.

Index funds are the fastest-growing investment product in the world with growth of 361% over the last 10 years. That’s because investors around the world are choosing index funds as a way to invest in stocks for the long term.

The index funds represent permanent capital into IBM. The index funds holdings of IBM are never going to be sold as long as IBM remains a component of the indexes. As more money pours into index funds, you’re going to see rising demand for IBM stock.

What’s more, the S&P 500 is a cap-weighted index. That means funds that follow the S&P 500 are going to be forced to buy more stock as its value goes higher.

Right now, IBM’s weight in the S&P 500 is 0.71%. However, if I’m right about IBM’s future direction ... in a couple of years, the stock’s component weight could be as much as three times higher as the company continues to grow. As IBM’s component weight grows, index funds will need to buy up more and more shares to match the new weighting. Index fund demand for IBM is going to surge higher, sending the price skyrocketing.

While the Hunt brothers snatched up silver supplies, taking it off the market to drive up the price, we are seeing the same thing happen with IBM; but this time, it’s Buffett, IBM and investment management companies that are sucking up the supply. I think we can all agree that IBM stock is very scarce.

The Changing Face of IBMAs you can see, IBM is all set up for a corner. But a corner isn’t complete until the demand for IBM stock

shows up. IBM’s stock needs a catalyst that will draw hordes of investors to the shares. Demand for IBM stock has been quiet for years now. That’s because IBM has been transitioning itself from a company that made computers, software and services. These businesses were slowing in growth and dropping in profitability.

To stay nimble and profitable, IBM has sold businesses and cut costs as this transition has unfolded. During this time, IBM’s revenues have fallen because it’s simply impossible to remake a big company like IBM overnight. This is a multiyear process. And during this process, IBM has taken cash that its old businesses were generating and done two things with it. First, as I showed you earlier, it’s been buying huge amounts of stock.

Second, it’s invested into new businesses. The most important of these new businesses is a platform technology for artificial intelligence Watson platform. I believe that Watson is going to drive IBM’s future growth, generating huge sales and profits for the company, which will lure investors into buying the shares. And that will send the stock soaring.

A Machine That Understands HumansWatson is easily the most advanced form of artificial intelligence in the world. The technology has been in

development since 1989. That’s when three students from Carnegie Mellon were hired to create a machine that could beat a human at chess. This machine was called Deep Blue.

5

In 1996, Deep Blue was the first machine to beat a human being at chess. Deep Blue was the pre-Watson. Watson was officially created in 2007, and it benefited enormously from the lessons of Deep Blue. By 2011, Watson was so sophisticated that it beat humans at the TV game show Jeopardy. David Ferrucci, a Watson developer, says: “The goal is not to model the human brain. The goal is to build a computer that can be more effective in understanding and interacting in natural language, but not necessarily the same way humans do it.”

Watson is a machine built to understand humans. And Watson does this by analyzing what we say, how we say it and when we say things. For example, Watson understands when you use sarcasm. Watson knows when you’re serious and when you’re joking. Watson understands idiomatic expressions, such as “there’s no point crying over spilt milk” and “don’t put all your eggs in one basket.”

This may not seem like a big deal to you, but I can tell you that this is something that no other computer technology has ever been able to do in human history. And this ability gives Watson something that only humans were able to do. Watson “understands” us, and then uses that understanding to analyze things. Watson, by my calculations, has cost nearly $3 billion to develop over the last 10 years. It’s the largest amount being spent on artificial intelligence. And now IBM is ready to unleash its incredible power in health care, banking, pharmaceutical development, medical diagnostics, accounting analysis, business analysis and many more fields.

In 2014, IBM began working with Memorial Sloan Kettering Cancer Center (MSK) in New York. Nik Buescher, winner of Johns Hopkins Outstanding Recent Graduate Award and now executive director at Penn Medicine, wrote in to MSK. Buescher instantly got what Watson is going to do in cancer...

You are training your replacement. Bill Brody at Hopkins remarked recently that radiologists are on the cusp of obsolescence as software detection programs improve. You’re helping to show that medical specialties will be next. Sure, “caring” is important, but nurses and others on the cancer care team do more of that than the physician, and given the popularity/reputation of academic cancer centers, there is a big market for treatment centers where caring is trumped by effectiveness. A national network of Watsons capable of staying up to date on the latest cancer evidence in every sub-specialty, would be capable of real-time translational research, would know all of the best decisions to make at each juncture on the best pathways, would know the effectiveness of the best specialists for subsequent referrals, would always be on call, wouldn’t mistreat staff, wouldn’t balk at evening/weekend hours, would promptly communicate with primary care, and would have a frame of reference for treatment decisions that is exponentially more significant than a string of anecdotes over a single career. The list goes on, but as it becomes evident that high-quality cancer care comes from standardization of practice toward best evidence, computers will soon be most effective at both assessing the evidence and the patient and optimizing their treatment to both.

What Buescher wrote is precisely the future of cancer diagnosis and treatment when you have Watson’s artificial intelligence platform working for you.

You see, MSK is one of the best cancer treatment centers in the world. It attracts the best doctors and cancer scientists. It also treats patients with the latest drugs, and it participates in every major new cancer drug trial. The most difficult cases are referred to MSK, either for MSK to treat directly, or to have a consulting and advisory role with the doctor and hospital that could be thousands of miles away. In MSK’s computers are case files for every kind of cancer and the results of every kind of treatment used to treat these cases.

What’s missing is an all-knowing “cancer oracle” that can look at all this information accumulated through thousands of prior cases and diagnose your cancer with 95% precision. But not just that. Once it identifies your kind of cancer, it knows what drugs work best against it.

Well, Watson is now being used as the “cancer oracle” at MSK. It can read all the cases that MSK has on file, and then it can read the history of treatments that worked. Watson, because of its unique contextual

6

abilities, can see the particular circumstances of the case. And because of this ability, it can recommend a specific treatment for a specific cancer.

Also, as MSK feeds more cases into Watson, it learns more. At MSK, Watson picked out cancerous lesions with 95% accuracy; human doctors’ accuracy is somewhere between 75% and 84%. WellPoint, one of America’s biggest insurance companies and a Watson partner, says that its lung cancer diagnosis accuracy is 90% versus 50% for humans.

Watson also has taken in 600,000 pieces of medical evidence and 1.5 million patient case files. According to MSK, a human doctor uses about 20% of factual, evidence-based medical knowledge when treating a patient. With Watson, it would be 100%, and would be updated in real time with the latest information. MSK reports that it would take 160 hours of reading a week to keep up with new medical knowledge as it’s published. And it would take even longer to understand the relevance or how or when to use it. In short, humans just can’t keep up. Soon, Watson is going to be diagnosing around the world, and guiding doctors on what treatments give the patient the highest chance of recovery.

Expanding Watson’s ReachTo help Watson get smarter, IBM has begun buying up companies that have key information. For example,

in August 2015, IBM bought Merge Healthcare for $700 million. Merge has a treasure trove of 30 billion images, including X-rays, computerized tomography and magnetic-resonance imaging scans that will help Watson learn to diagnose cancer and heart disease. Merge has deals with 7,500 U.S. hospitals for their images and data to keep feeding Watson.

In February 2016, IBM bought Truven Health Analytics for $2.6 billion. Truven, like Merge, feeds Watson data on 300 million patient lives and brings relationships with over 8,500 clients, including U.S. federal and state government agencies, employers, health plans, hospitals, clinicians and life sciences companies.

Feeding more and more valuable data to Watson means that it will have more uses across the health care industry. Health care spending globally is estimated at $7.3 trillion, and IBM is set up to claim a slice of that pie. Getting even 1% of this spending means sales of $73 billion.

Now, I don’t want you to think that health care is the only thing IBM has focused Watson on. No, IBM is aiming Watson into agriculture, advertising, banking, government services, transportation, communication and more.

With all these industries, the recipe is the same as health care. Use Watson’s ability to understand human-generated data and then generate useful information to help the companies in these fields. Since the start of 2016, IBM has already bought June 2016 nine companies to feed Watson. Some of the more important acquisitions are:

• The Weather Company, for weather data that can be used in agriculture and in construction.

• IRIS Analytics, a real-time analytics company that will give Watson the ability to use data on payment fraud.

• Optivia, a business focused on customer relationship management for government services.

• Bluewolf Group, one of Salesforce’s top partners and a globally recognized leader in cloud consulting and implementation services.

• Resilient Systems, which developed an incident response platform that automates and orchestrates the many processes needed when dealing with cyber incidents — from breaches to lost devices.

7

• ecx.io is a full-service digital agency headquartered in Dusseldorf, Germany. The proposed acquisition of ecx.io extends the strategy and design expertise of IBM Interactive Experience (IBM iX) with new digital marketing, commerce and platform skills to accelerate clients’ digital transformations.

• Ustream, a provider of cloud-based, live-video streaming services. The move will extend the IBM cloud platform to help enterprise clients unlock the value of video, a rapidly evolving digital media and data asset.

The One Product Every Company Will Want to UseIBM’s Watson is a huge technology platform that can be used in many parts of the economy ... from

agriculture to weather. And the potential sales just from health care are in the hundreds of billions. The potential sales in banking and advertising and weather are also in the billions.

“We make markets, we create entire industries and that’s what we’re going to do with this,” says Watson Group Division Head Mike Rhodin. Watson is powerhouse technology that I believe is going to dominate the world of artificial intelligence. Right now, IBM’s goals for Watson are for it to generate $10 billion by 2023.

That’s pretty modest when you consider recent product introductions in computing, such as Amazon’s Web Services (AWS), have soared higher. AWS went from zero to $10 billion in 20 years and is expected to hit $30 billion by 2023. AWS, though, is just a storage technology.

Watson is artificial intelligence that gives you usable, actionable and profitable information that can help save lives, grow businesses and help you make decisions that could be the difference between life and death. Just $10 billion in 2023 seems puny to me, particularly when you consider that IBM’s customers are the cream of the crop. Almost every Fortune 500 company uses IBM for one of their services. Same with governments and large organizations.

For example, on April 1, 2016, IBM signed a $171 million deal with the Italian government to create a Watson Health Center in Milan.

On March 14, 2016, IBM signed a $200 million deal with Indosat Ooredoo, an Indonesian telecommunications company.

And in 2015, IBM signed a deal with the Abu Dhabi government airline Etihad for $700 million.

You get my point ... companies, governments and organizations around the world choose IBM because of its prestige, reputation, financial stability and technological capability. And you know that all of them are going to want to make a deal with IBM to get Watson artificial intelligence working for them too.

Maybe these deals seem small to you when you consider the scope of Watson and IBM. Just remember that Google became big because lots of people around the world began using it. IBM’s Watson is like Google ... you’ll have companies, governments, organizations ... everyone using it. It’ll all add up to being billions and billions in revenue.

However, it’s not here yet ... and that’s why IBM is still cheap.

Crazy Cheap, But It Won’t LastThe shares of IBM are trading so cheap that they’ll soar higher even if Watson just sees a little spike in

demand. That’s because most investors have been focusing purely on the fact that IBM’s sales have been dropping. However, this isn’t a surprise to anyone who’s been following the company. IBM laid down the plan

8

to transition from its existing business and made a big bet on Watson over the last five years. As a result, IBM is trading at very cheap levels — if you believe that Watson is going to be successful.

However, if you believe that Watson is going to be a game-changing, dominant technology ... IBM is trading at an insanely cheap level. Crazy-cheap prices, as I like to put it.

Right now, Wall Street is expecting IBM’s sales to stay flat in 2016 and 2017. However, IBM’s cash flow per share, which is the ultimate indicator of a business doing well, just hit an all-time record. A blue chip like Coca-Cola trades for 27 times its free cash flow per shares. 3M Company trades for 21 times its free cash flow per share.

IBM should trade for 15 or 20 times its cash flow per share, even though it’s going through a transition period. However, IBM is trading at 9.6 times its free cash flow per share. That’s crazy cheap.

On a price-to-earnings ratio (P/E), which many investors like to use as a measure of whether a stock is expensive, IBM is trading at 10 times its 2016 median earnings estimate. The average P/E for companies in the S&P 500 is 18. So IBM is incredibly cheap using P/E.

What’s more, IBM pays a dividend of $5.20 per share, which is a yield of 3.6%. The company’s balance sheet is rock solid, with $8 billion in the bank and free cash flow of $12.8 billion per year. IBM is not a risky stock by any measure you want to look at.

No one gets the incredible opportunity more than Warren Buffett. In interviews, he’s talked about how Wells Fargo Bank, one of his big holdings, has told him about how useful Watson is to their business. Berkshire Hathaway is also collaborating with Watson in its reinsurance business.

In Berkshire Hathaway’s 2011 annual report, Buffett lays out how scarce he expects the IBM stock situation is going to be: “If IBM’s stock price averages, say, $200 during the period, the company will acquire 250 million shares for its $50 billion. There would consequently be 910 million shares outstanding, and we would own about 7% of the company.”

Buffett understands that for a stock to soar, it needs to be scarce. I think we’re all in agreement that IBM shares are scarce.

Second, Buffett understands the stock needs to be cheap, and you must be getting value for your money.

IBM is crazy cheap for all the reasons I’ve explained. Now, as Watson makes sales and profits surge, investors will want to own IBM shares, and they’ll have to bid it up again and again to get it. I expect the stock price to

IBM Free Cash Flow Per Share

16.25

13.75

11.25

8.75

6.25

3.75

1.25

-1.251995 2000 2005 2010 2015

9

skyrocket by as much as 200% to a price of $450 over three years. It could go even higher than that if Watson starts to generate sales growth in 2017.

My stretch target price for IBM is $600, or a gain of nearly 300%. Now, you won’t benefit from everything I’ve told you unless you own IBM shares. And you need to get in now, before other people figure out what I’ve just told you.

Remember, Warren Buffett — the world’s greatest investor — is in on the IBM corner. And all the research I’ve done suggests that the corner is fully formed ... and IBM stock is set to go higher with the help of Watson.

Action to take: Buy the shares of IBM (NYSE: IBM) up to $165.

Most people don’t think about the demand and supply of a company’s stock when they go to buy it. It’s a critical error. For me, this is the most important thing.

You can see how important from the Hunt brothers’ corner. The Hunt brothers had hoards of silver, giving them control of the market. By controlling the market, they set the price of silver. If you wanted to buy, you paid what the Hunt brothers told you to pay.

The stock market works the same way. If a few people own the majority of IBM shares, they control the market. Now they set the price if you want to buy.

It’s an incredible power to have ... if you already own the thing that’s in short supply. Of course, the Hunt brother ran afoul of the law when they cornered silver. The previous metal is an important industrial commodity. When they cornered the market, the government got involved and the end result was the futures exchanges changing the rules, which forced the Hunt brothers to sell at a loss. In fact, the Hunt brothers had to declare bankruptcy.

But we’re in a different scenario with IBM shares. All the transactions are legal and meet government requirements. IBM stock can soar to the moon ... and no government or insiders are going to get hurt or lose money.

In fact, with Warren Buffett and big asset management companies such as Vanguard involved, we’re guaranteed that the IBM corner profits are safe.

That’s why this is such an incredible opportunity to buy IBM now. IBM stock is already up 13% in 2016, and I expect it to keep going up. Once everyone figures out what I’m telling you, they’ll push IBM stock higher, and you’ll miss out on hundreds of percent of gains over the next few months and years

In This Game of Duopoly, You WinWalk in any grocery store around the U.S. and covertly watch people buy soda. What you’ll see is that most

people pick either

Coke or Pepsi.

Go to a baseball game, you’ll either be served Coke or Pepsi. Same thing on a plane, in a restaurant, amusement park or movie theater.

In fact, almost anywhere you go in the U.S. — and a lot of places around the globe — there are mainly two choices when it comes to carbonated beverages: Coca-Cola and Pepsi.

These two soda companies almost completely dominate sales of soda around the world.

According to Grand View Research, as of 2014, Coca-Cola claimed roughly 48.6% of the carbonated beverage market while Pepsi had 27.5%. That’s 76% of a $340 billion market locked down by just two companies.

10

Everyone Wins in a Duopoly

— The Coca-Cola Company — Pepsico, Inc.

1980 1985 1990 1995 2000 2005 2010 2015

20,000%

16,000%

12,000%

8,000%

4,000%

0%

And then don’t forget that these two behemoths — worried about all the negative stories surrounding the unhealthiness of soda — have also snatched up a sizable chunk of the water, juice, energy drink and tea market.

The fact is that if you’re grabbing a quick drink either off the shelves at the grocery or at a restaurant, it’s very likely that you’re buying from one of these two companies.

It should really come as no shock then that the stock performance of these two companies has been incredible. Coca-Cola’s stock is up nearly 17,000%, and Pepsi is up nearly 20,000% since 1979.

That’s enough to turn a $10,000 investment into $1.7 million for Coca-Cola and $2 million for Pepsi.

It’s very likely that when you read about Coca- Cola or Pepsi, you imagine fierce competitors. One is trying to kill the other by getting everyone to dump whichever beverage they currently drink. You see advertising nonstop asking you to change your soda of choice.

However, the thing that is most important is that wherever you go, it’s just two choices: Coke or Pepsi.

That means each company is guaranteed to get tons of sales, because there are just two choices. This business setup is called a “duopoly” — an industry where two companies dominate sales.

And a duopoly like the one Coca-Cola and Pepsi have created is absolutely incredible for sales because it’s limited competition.

The duopoly allows Coca-Cola and Pepsi to maintain higher prices than what they’d otherwise be able to than if they were in an industry with five or 10 close competitors.

Of course, Coca-Cola and Pepsi have had their fair share of competitors — RC Cola, 7Up, Shasta, Dasani, Gatorade — that they’ve either crushed to the fringes or acquired.

Obviously, that’s good for profits. And if you’re in a duopoly, you’re always getting a large chunk of all the sales that are happening. All that advertising you see pitting Coca-Cola against Pepsi is actually designed to simply make you drink more of either.

As you know, Coca-Cola and Pepsi aren’t the only companies that have benefited from duopoly in their industry.

Another example is MasterCard and Visa.

Go to any store that accepts credit cards, and you’ll see that they each take MasterCard and Visa. If you’re

11

a business owner who has to pay MasterCard and Visa fees so that customers can use their cards, you find out quickly that their fees and transaction charges are nearly identical.

In other words, these companies are competitors in name only. They don’t really compete with each other.

As a result, they split the market between them for credit cards — Visa has 47.4% of the market while MasterCard comes in at 23%. As long as their industry is growing, they both do great.

And if you figured this out early and invested in their stocks, you’ve done incredibly well.

MasterCard is up nearly 900% since becoming a publicly traded company in 2007, while Visa has soared nearly 700% since 2008.

In the airline industry, there’s Boeing and Airbus. In the breakfast foods sector, there’s Kellogg and General Mills. And in the battery industry, there’s Energizer and Duracell.

The list goes on. The key thing to remember is that snatching up a company that dominates within a duopoly sets you up to profit from a huge winner … particularly if you buy into the stocks of these companies early.

And that’s what we’re going to do this month. We’re buying into a duopoly and the company makes a critical component for the massive Internet of Things mega-trend.

We’re poised to jump in as this sector is still young with ample room for explosive growth.

A Linchpin for the Internet of Things RevolutionQorvo (Nasdaq: QRVO) is one of the two companies that dominate the making of an obscure, but critical

component that goes into anything that needs to be connected to the Internet. This critical component is called a bulk acoustic wave filter, or BAW. Simply put, a BAW keeps signals straight.

While that might not sound like a big deal, it’s absolutely crucial as the Internet of Things expands to touch nearly every aspect of your life.

You see, each of us carries a cellphone, a tablet, a laptop or wireless headphones, and our cars are connected to satellites, while nearby buildings have Wi-Fi connections.

And then don’t forget that inside our houses, we have devices such as thermostats, refrigerators, baby monitors, security cameras, health monitoring devices, gaming systems, and even more gadgets — all of them connecting wirelessly.

If these connections were happening through the use of old-fashioned wires, it might look something like the image above. A regular rat’s nest of cords ready to tangle and or trip you.

Wires connect things one to one. However, there’s a physical limit to wires, which also creates a physical limit to the number of things you can connect.

It’s critical for the Internet of Things to be wireless so we can have more gadgets and tools available and talking to each other, sharing information and making our lives better.

There’s just one problem. Wireless spectrum is limited ... and lots of it is being used already for radio signals, TV signals, cellphone signals, Wi-Fi signals and emergency radio for fire, police and ambulances.

To make the Internet of Things to work, devices have to work with a very thin slice of the wireless spectrum. And you can’t have your device use anybody else’s part of the spectrum without causing major problems.

12

Unfortunately, most devices drift a little bit in their use of the spectrum — sort of like a car that drifts a bit to the right or left while traveling down the road. However, when it comes to wireless devices, the lanes are so tightly packed that even a small drift can cause a major accident.

And that’s where Qorvo’s BAW filters come in.

BAW in your cellphone keeps it in the narrow slice of the spectrum it’s supposed to stay in. It would be like having invisible barriers that keep the car in the exact lane it’s supposed to be in all the time.

For cellphone and tablet companies, they pack their devices with BAWs. These devices might communicate with a cellphone network, a Wi-Fi network or using a Bluetooth connection. Or all of them at the same time!

At all times, the BAWs are making sure that these connections stay in lane so that the device works properly.

50 Billion Devices Will Need What Qorvo SellsAccording to Cisco Systems, we’re going to have 50 billion devices that all have to communicate with

various networks and each other.

Most of these devices are going to be everyday things, such as the windows, doors and pipes in your house that can signal your phone. They’ll tell you things such as if your door is left open, if someone has broken in or if a pipe is leaking.

Another advancement is that your car will one day communicate with other cars so it knows when the car in front is braking or about to make a sudden left turn.

Another is little bracelets that let you know where your kids are at all times ... or perhaps your elderly parent.

And don’t forget that as these devices develop, we are regularly moving to new communication standards — 4G, 5G, etc. — which use thin slices of frequency spectrum. This will require new BAW filters to keep the devices working properly.

The key to all this happening is that these devices have to be able to communicate by Wi-Fi, Bluetooth or else by direct connection to the Internet or cellphone networks.

And for that they absolutely need a BAW filter.

Otherwise, they won’t be on the right frequency, and the message won’t go through.

The demand for newer and better wireless devices is going to soar and regardless of whether you’re talking about a cellphone or a refrigerator, the device will need a BAW filter. And there are just two companies that can make BAW filters in sufficient quantities to meet the voracious tech demands of the world.

Right now, Qorvo and its competitor Avago Technologies share 95% of the BAW market.

That means if you’re Apple or Samsung, you’re going to end up using BAW filters in your phones and tablets — not to mention the refrigerator that’s happy to send you selfies of its contents.

There’s also the big growth coming for Qorvo as a result of communication standards going from 4G to 5G around the world.

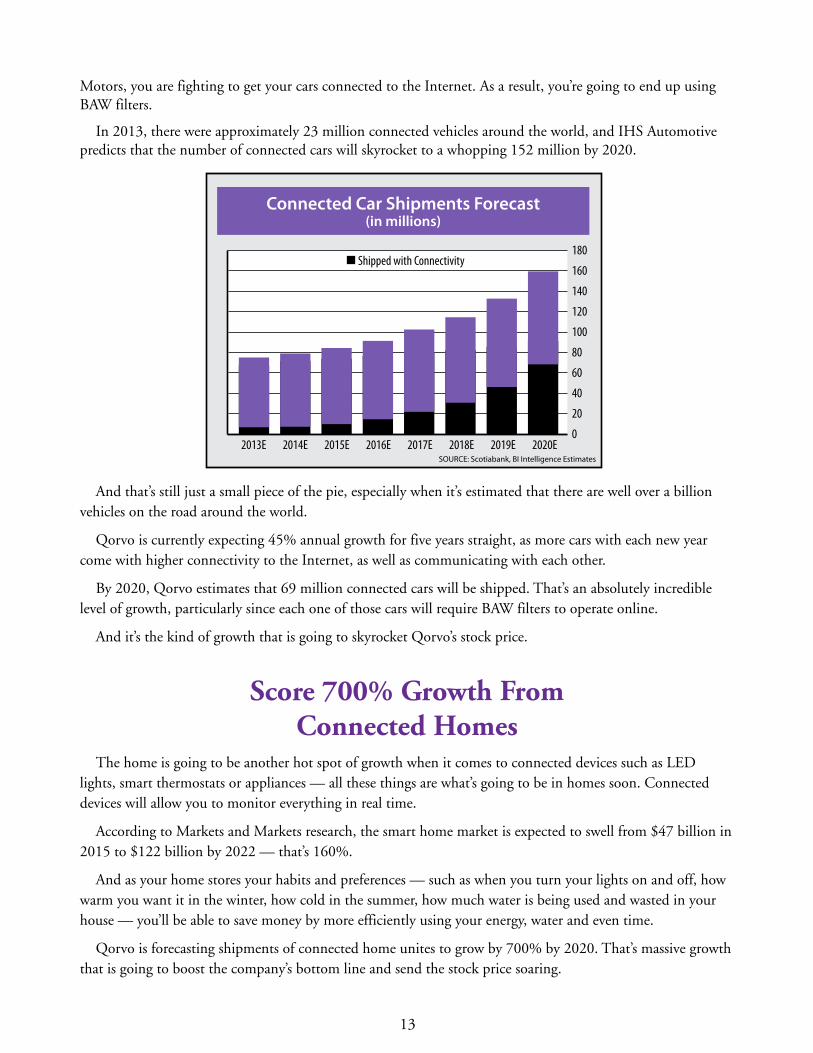

Connected Cars Could Add 45% GrowthThe auto industry definitely won’t be left out of the Internet of Things. If you’re Tesla, BMW or General

13

Connected Car Shipments Forecast(in millions)

2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E

180

160

140

120

100

80

60

40

20

0

Shipped with Connectivity

SOURCE: Scotiabank, BI Intelligence Estimates

And that’s still just a small piece of the pie, especially when it’s estimated that there are well over a billion vehicles on the road around the world.

Qorvo is currently expecting 45% annual growth for five years straight, as more cars with each new year come with higher connectivity to the Internet, as well as communicating with each other.

By 2020, Qorvo estimates that 69 million connected cars will be shipped. That’s an absolutely incredible level of growth, particularly since each one of those cars will require BAW filters to operate online.

And it’s the kind of growth that is going to skyrocket Qorvo’s stock price.

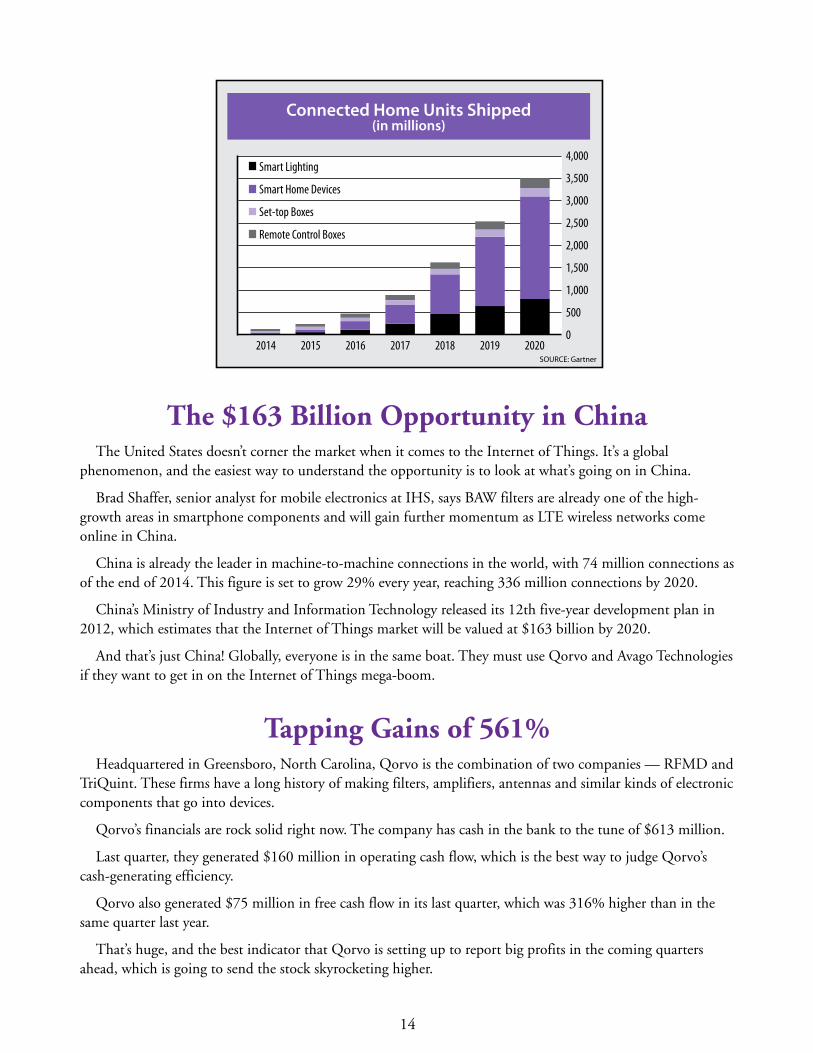

Score 700% Growth From Connected Homes

The home is going to be another hot spot of growth when it comes to connected devices such as LED lights, smart thermostats or appliances — all these things are what’s going to be in homes soon. Connected devices will allow you to monitor everything in real time.

According to Markets and Markets research, the smart home market is expected to swell from $47 billion in 2015 to $122 billion by 2022 — that’s 160%.

And as your home stores your habits and preferences — such as when you turn your lights on and off, how warm you want it in the winter, how cold in the summer, how much water is being used and wasted in your house — you’ll be able to save money by more efficiently using your energy, water and even time.

Qorvo is forecasting shipments of connected home unites to grow by 700% by 2020. That’s massive growth that is going to boost the company’s bottom line and send the stock price soaring.

Motors, you are fighting to get your cars connected to the Internet. As a result, you’re going to end up using BAW filters.

In 2013, there were approximately 23 million connected vehicles around the world, and IHS Automotive predicts that the number of connected cars will skyrocket to a whopping 152 million by 2020.

14

The $163 Billion Opportunity in ChinaThe United States doesn’t corner the market when it comes to the Internet of Things. It’s a global

phenomenon, and the easiest way to understand the opportunity is to look at what’s going on in China.

Brad Shaffer, senior analyst for mobile electronics at IHS, says BAW filters are already one of the high- growth areas in smartphone components and will gain further momentum as LTE wireless networks come online in China.

China is already the leader in machine-to-machine connections in the world, with 74 million connections as of the end of 2014. This figure is set to grow 29% every year, reaching 336 million connections by 2020.

China’s Ministry of Industry and Information Technology released its 12th five-year development plan in 2012, which estimates that the Internet of Things market will be valued at $163 billion by 2020.

And that’s just China! Globally, everyone is in the same boat. They must use Qorvo and Avago Technologies if they want to get in on the Internet of Things mega-boom.

Tapping Gains of 561%Headquartered in Greensboro, North Carolina, Qorvo is the combination of two companies — RFMD and

TriQuint. These firms have a long history of making filters, amplifiers, antennas and similar kinds of electronic components that go into devices.

Qorvo’s financials are rock solid right now. The company has cash in the bank to the tune of $613 million.

Last quarter, they generated $160 million in operating cash flow, which is the best way to judge Qorvo’s cash-generating efficiency.

Qorvo also generated $75 million in free cash flow in its last quarter, which was 316% higher than in the same quarter last year.

That’s huge, and the best indicator that Qorvo is setting up to report big profits in the coming quarters ahead, which is going to send the stock skyrocketing higher.

Connected Home Units Shipped(in millions)

2014 2015 2016 2017 2018 2019 2020

4,000

3,500

3,000

2,500

2,000

1,500

1,000

500

0

SOURCE: Gartner

Smart Lighting

Smart Home Devices

Set-top Boxes

Remote Control Boxes

15

Right now, the company has a market capitalization of just $7.24 billion. That’s ridiculously small when you consider how big the Internet of Things opportunity is for Qorvo. After all, we’re talking about a global market where Qorvo has an incredible duopoly with Avago Technologies.

For all practical purposes, it’s going to split a market that’s valued in the hundreds of billions. That’s why I believe that Qorvo can reach and even surpass its all- time high price of $370 reached during the last tech boom in the year 2000. From its current stock price of $56, that would mean a gain of 561%.

Now, to be fair, that’s not going to happen in a day. However, Qorvo stock is set to boom higher in 2016 by at least 30%. And I expect gains of between 30% and 50% for the next three to five years.

Qorvo is poised to benefit from a duopoly, just like Coca-Cola, Boeing and MasterCard. The limited competition with Avago Technologies means that the company is set to snag a big share of the connected- device market.

What’s more, this duopoly secures Qorvo’s pricing power. The lack of multiple competitors means that the firm won’t need to rely on razor-thin margins to stay ahead of its competition.

That’s why its latest business assumptions project that its gross profit margins are going to be 50% — for every $1 taken in, $0.50 is profit.

Building a Strong Position in the Next Tech Revolution

Both Qorvo and Avago Technologies have established a strong position within the industry. Now, it’s always possible for someone to invent a new way to do what Qorvo and Avago Technologies are doing.

But it won’t be easy. That’s because whoever invents this new thing would have to be able to produce it in scale, and by scale, I mean billions and billions of it, and around the world.

In other words, it’ll take a massive amount of capital — likely $3 billion or more. I can tell you from researching innovation that the people with this kind of capital are going to look at the duopoly industrial structure of Qorvo and Avago Technologies ... and say no thanks.

That’s because they know that Qorvo and Broadcom are going to protect their duopoly by copying the new invention quickly and selling it to their customers.

And their established customer base has a long history of dealing with Qorvo and Avago Technologies.

They know that these companies are well-capitalized and reliable. They know that these two firms can supply them around the world without a problem. That relationship is a huge deterrent to any new competition.

Plus, Qorvo spends 17% of sales on R&D — that was $459 million in 2015. They are investing plenty to keep themselves on the cutting edge and to keep competitors out.

Finally, the versatility of Qorvo’s BAW filters allows it access to virtually every Internet of Things device that’s going to be made around the world, whether it’s cellphones, cars, thermostats, tablets or appliances.

That’s 50 billion devices. The profit potential is huge.

And that’s why I’m so incredibly optimistic about Qorvo.

16

Beating Wall Street to the PunchCurrently, Wall Street analysts are being very conservative with their numbers on Qorvo. From my

experience, that’s typical Wall Street behavior ... and I’ve seen it happen many times at the bottom of cyclical companies like Qorvo.

Wall Street analysts are too gun-shy to model a recovery in sales and profits because they’ve been burned too many times by being too early.

Or else they sit on their hands so that their own traders can accumulate the stock cheaply ... so that they have a huge inventory of stock to sell to their institutional clients.

At the beginning of the cycle, analysts are conservative and don’t model high numbers because they don’t want to be wrong. However, later as the sales are accelerating, you’ll see numbers move higher.

My point is that analysts’ estimates for cyclical companies such Qorvo lag the actual numbers ... and that’s our opportunity.

We want to own Qorvo before analysts start raising their numbers, because you’re going to see the stock soar higher as a result of the optimism.

Personally, based on the weeks of research I’ve done for this issue, I would bet on Qorvo showing accelerating growth over the next three years, averaging between 20% and 30%.

Choosing the Winner in a Two-Horse RaceMany of you are probably wondering why I am choosing to buy Qorvo stock now instead of Avago

Technologies. There’s one big reason for this: growth.

Avago Technologies has more exposure to some slower-growing businesses, such as personal computers, than Qorvo. As a result, Wall Street analysts are expecting Avago Technologies to report flat revenue growth in 2016, and earnings-per-share growth over the next five years is forecast to be just 0.7%.

On the other hand, Qorvo is forecast to see sales to jump by over 7% this year and 8% next year. Long-term earnings-per-share growth is expected to surge higher by 15% this year and next. And the five-year growth rate for Qorvo is 12% per year.

What’s more, I think estimates for Qorvo are too low. The company is set to grow even faster than what these numbers are projecting. In short, Qorvo is positioned for much better growth than Avago Technologies.

However, you shouldn’t be surprised if one day soon you see me recommending Avago Technologies stock to you as well. Right now the choice is clear ... hands down, Qorvo is the superior stock investment.

GoingUpness System CheckOne thing I always do before I recommend any stock to you is to be certain that the stock has what I call

“GoingUpness.”

There are six parts to my GoingUpness system, and we’re going to go through them quickly with Qorvo so you can see how it works.

• InDemandness — which means that you can tell that Qorvo stock is being bought at current prices or higher regularly. The easiest way to do this is to see if the stock is trading at a price that’s above its 10-day

17

moving average and is at least 20% higher than its 52-week low. Right now, Qorvo easily meets both these conditions of GoingUpness.

• Insiderness — which is informed decision- making by the insiders of a company. In Qorvo’s case, the Insiderness condition is met by its merger of RFMD and TriQuint. This merger happened at the bottom of the business cycle of these companies, and it created a powerful duopoly.

• Buyness — Qorvo stock is rising, but in a volatile trading environment and on low volume. That’s exactly the kind of behavior that my system is looking for. That’s because this kind of trading in my experience is designed to make people uncomfortable and stops you from buying it when it’s cheap. So Qorvo meets my Buyness standard.

• ScarceAbility — which is making sure that the shares are scarce. Qorvo’s share count is declining, dropping from 151 million shares to 133 million shares over the last five quarters. That’s exactly what we want to see.

• ManageAbilty — which is a test to see if the management is credible. In this case, you can tell from management communications, which are clear, simple and easy-to-understand goals, that the management is credible.

• ValueAbilty — which is that it’s in control of a growing, profitable business. This condition is more than satisfied by the size of Qorvo’s

Internet of Things opportunities and its financial performance.

Qorvo’s stock is ready to rocket higher, because it has a duopoly with Avago Technologies in BAW filters — a critical component for the massive Internet of Things market that’s about to experience explosive growth.

Now, you won’t get the benefit of these gains unless you buy the stock. I’ve done all the work for you by laying out an absolutely phenomenal opportunity to make big money because of the Internet of Things trend. However, I can’t buy the stock for you. You have to own the stock to get the benefit of Qorvo stock going up.

Qorvo shares are already up 5.5% this year. You want to get in before the big money works out what you know.

Action to Take: Buy Qorvo (NASDAQ: QRVO) up to $70.

This Industrial Dinosaur Is Set to Roar … With the Internet of Things

When I look back now, I see I’ve always had a knack for sensing the next big thing…

In 1992, I bought my first computer. It was a clone … meaning it was assembled from mail-order parts by some guy in his garage, then sold to the likes of me. I don’t know why, but I had a sense that it was important to own such a machine, even though, at the time, I only had a vague idea of how it worked or why it was useful.

For a while, I wondered why I’d bothered. All the reasons for owning a computer at the time — figuring my household budget on a spreadsheet, or typing out a shopping list — seemed idiotic to do on a $1,000 piece of technology.

However, not long after, I bought a clunky dial- up modem and discovered the Internet (such as it existed in the early 1990s). And you know what? That early exposure to the Web gave me some great insights. I knew we would be in for some incredible, revolutionary developments for the rest of the decade.

18

And to think it all started when an obscure software company named Microsoft was hired little more than a decade earlier by IBM to design an operating system for the company’s groundbreaking personal computer (PC).

We know the rest of the story. Before long, there were dozens of companies making PCs (and cheap cloned machines like mine), selling a billion of them a year by 2002.

And at the humming, blinking digital heart of almost every one?

Microsoft’s operating system software.

The company became a cash machine. For every $100 someone spent buying a PC, the software giant was taking in $30 to $40 in profits. No wonder the company’s net income jumped by an astounding 500% between 1995 and 1999.

If you had put $1,000 into Microsoft stock when it went public in 1986, you’ have had $668,590 just 13 years later. It’s the kind of dream run that makes people rich, with very little volatility.

So why am I talking about Microsoft so much?

Today, we find ourselves on the cusp of a new technological revolution — the Internet of Things. Just like the start of the PC revolution, this one feels new and unfamiliar at first. But I can tell you how it feels to me — we’re right at the launch point, just like Microsoft in 1980.

My new recommendation has the potential to be just as big of a winner, too. It has a rapidly growing software platform, not unlike Microsoft’s Windows in its earliest days. The software is destined to connect millions upon millions of these new “devices” — the industrial machines, powerful engines and vast electromechanical systems — that form the heart of our 21st-century economy.

“Smart” MachinesAs I’ve explained in earlier issues of Profits Unlimited, the Internet of Things (IoT) is the next mega trend

to sweep our world.

We’re talking about 50 billion connected devices by 2020, generating economic growth equal to $19 trillion.

If you’ve heard of the IoT before, you may think of it as only relevant to your personal technology, such as your smartphone, tablet or fitness tracker.

But if you own a new car bought in the last few years, chances are it too is an Internet of Things on four wheels.

Digital sensors built into the engine, tires and other compartments transmit data all the time. The onboard computer monitors wear and tear on the engine and transmission, and on the emissions, airbag, braking and stability-control systems. If there’s a problem — maybe the tire pressure is a little low, or the oil filter needs changing — the system will let you know.

Internet of ThingsNumber of Connected Devices Worldwide in Billions

60

50

40

30

20

10

0 2012 2013 2014 2015 2016 2017 2018 2019 2020

50.1

42.1

34.828.4

22.918.2

14.411.28.7

SOURCE: ©Statista 2016

19

But that’s just a small slice of the pie. The biggest potential gains are going to come from industrial machines.

For example, when you get on a plane today, the pilot’s cockpit is, in essence, a computer-monitoring station, constantly measuring and comparing all the information pumped to it from the aircraft’s myriad systems — engine, flaps, fuel system, landing gear and all the rest. In the IoT era, even a single jet engine is itself made of many different subsystems — fans, manifolds, valves and combustor chamber — each fitted with its own digital sensors for temperature, pressure and speed.

Virgin Atlantic, with 17 advanced Boeing 787 Dreamliners in its fleet, is one airline that’s embracing the Internet of Things. The carrier estimates that each of its planes generates half a terabyte of data (roughly the equivalent of 110 DVD movies) because every engine and airplane part is connected to a computer all the time.

“If there is a problem with one of the engines,” says Virgin Atlantic’s Chief Technology Officer David Bulman, “we will know before the plane lands to make sure that we have the parts there.”

As a result, Virgin Atlantic runs a safer, more efficient airline, with improved bottom-line results. In its last quarter, Virgin Atlantic’s profits soared by 81%. That’s just one airline. Now, imagine the impact as every transportation fleet in the world, every factory and assembly plant, and all their many industrial machines, are constantly connected to the Internet.

The operator of a metal-stamping press knows, before it happens, when one of his machine’s parts is about to fail. He can anticipate maintenance, reduce downtime and improve efficiency. Same for the guy running a log-cutting machine at a lumber mill — he would know precisely when a blade or belt needs replacing, or have the information to intervene before a terrible industrial accident occurs.

That sequence of collecting data, analyzing it and using it to increase performance, efficiency, safety and, of course, profits is the Industrial IoT opportunity. This goes from machines that are in every factory or plant you see, whether they are making beer, cars or toys. The Industrial IoT is going to be in every single manufacturing site where machines are being used to make or produce things.

Market research firm IDC estimates that the industrial Internet of Things market is going to be valued at $1.7 trillion by 2020.

And the company that controls the software operating system for the industrial IoT is going to end up being a mega-growth company ... and a stock market blockbuster winner.

A Software Company in DisguiseThe company positioning itself to become a blockbuster is the perfect investment right now because Wall

Street is not pricing this monstrous opportunity into its stock price. The firm is a solid, dividend-paying company, and it’s trading dirt cheap when you compare it to software companies like Microsoft.

By purchasing the shares now, we’ll get the benefit of the stock market revaluing this company higher year after year after year, generating massive gains for us.

The company we’re buying this month is General Electric (NYSE: GE).

Yes, that General Electric — the company you most likely associate with washing machines and dryers. GE no longer makes washing machines and dryers — it sold that business in June 2016.

However, when I look at GE today, I see two companies.

GE still make machines — jet engines, electricity generation turbines, train locomotives, machinery for

20

oil and gas exploration, health care scanners and wind turbines. These are big machines that are going to be critical in the industrial IoT trend because they are going to be significantly improved as a result of using the software that GE has invented.

But before we look at what GE is going to become, let’s look at what GE is now. Wall Street still thinks of GE as a dinosaur, a holdover from the 20th-century industrial age — and values the stock accordingly.

For instance, if you divide GE’s billions of dollars in sales by its stock price — you get a price-to-sales ratio of 2.5. But Wall Street thinks each dollar of sales from a giant software company like Microsoft carries a lot more value. Do the math, and Microsoft gets a price-to-sales ratio of 5. Do the same thing for a highly regarded firm like Salesforce.com, which provides customer service management software, and you get a price-to-sales ratio of 8.

What does all that tell you? Software — not hardware, like turbines and engines — is where the money’s at.

Secondly, manufacturing companies struggled through the economic recovery. Many businesses, and even consumers, put off upgrading to new machines — that’s not good when you make machines that a company or person will buy once, and not buy again until years later.

Just look around your own household. The average lifespan of a washing machine is about 11 years; for a dishwasher, it’s nine years. Large enterprises like airlines aren’t much different. The average age of U.S. domestic commercial aircraft is 11 years. Sure, a manufacturer like GE — which builds and sells highly complex jet engines — can generate additional revenue from selling maintenance services and spare parts, but that’s still mostly a one-time sale.

However, because of the industrial IoT tech trend, a machine is no longer “just” a machine.

Connected to the Internet, machines begin generating massive amounts of information. Suddenly, that mass of data now is incredibly more valuable because it allows the company to monitor and analyze the machine, so they can make it run cheaper, faster and more efficiently, as well as make it last a lot longer.

A company can find out, in real time, if a part is wearing down and needs replacement. The enterprise can work out the optimal operating method for the machine for specific environments.

And best of all, if you’re the company whose product is generating all that information, you can build a “platform” that holds all that information. Other software developers around the world will then create apps and software programs to mine this data based on your software … just like Microsoft has seen happen with its own operating system.

Right now, investors see GE as a maker of plain old machines. Yes, those machines are highly complex — jet engines, locomotives, wind turbines and the like. But for Wall Street, that’s nothing to get excited about. Analysts know that a run-of-the-mill machine- maker makes — in good years — about 10% to 12% on its money, and value its stock accordingly.

But when GE begins to remake itself as a software and data company? Well, that’s when the real fun starts. As GE’s profits begin to ramp higher, Wall Street will catch on. I expect the stock to move sharply higher over time as analysts revalue the stock as a “software platform” company, rather than a manufacturer of industrial equipment.

GE’s Predix: The Power Behind Great Cost Savings

From studying Microsoft’s domination of the PC industry, I can tell you that it’s only a matter of time before GE’s software, cloud computing and data- services businesses completely dominate its sales and profits.

21

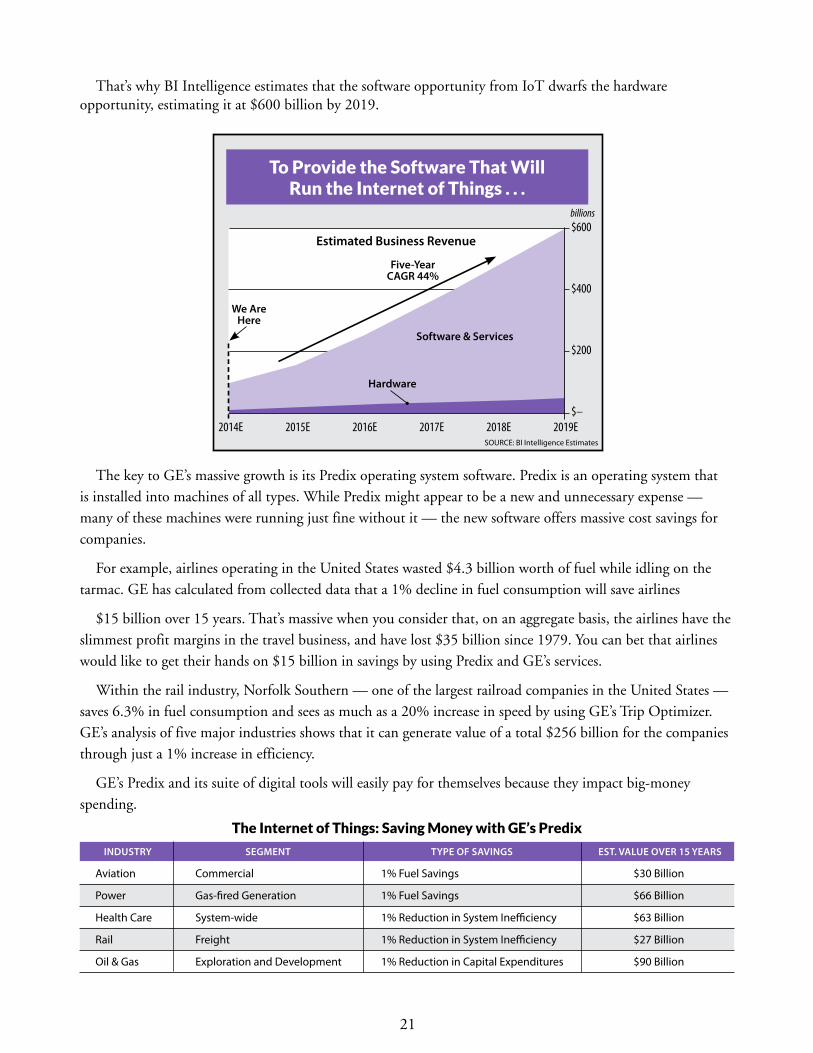

That’s why BI Intelligence estimates that the software opportunity from IoT dwarfs the hardware opportunity, estimating it at $600 billion by 2019.

The key to GE’s massive growth is its Predix operating system software. Predix is an operating system that is installed into machines of all types. While Predix might appear to be a new and unnecessary expense — many of these machines were running just fine without it — the new software offers massive cost savings for companies.

For example, airlines operating in the United States wasted $4.3 billion worth of fuel while idling on the tarmac. GE has calculated from collected data that a 1% decline in fuel consumption will save airlines

$15 billion over 15 years. That’s massive when you consider that, on an aggregate basis, the airlines have the slimmest profit margins in the travel business, and have lost $35 billion since 1979. You can bet that airlines would like to get their hands on $15 billion in savings by using Predix and GE’s services.

Within the rail industry, Norfolk Southern — one of the largest railroad companies in the United States — saves 6.3% in fuel consumption and sees as much as a 20% increase in speed by using GE’s Trip Optimizer. GE’s analysis of five major industries shows that it can generate value of a total $256 billion for the companies through just a 1% increase in efficiency.

GE’s Predix and its suite of digital tools will easily pay for themselves because they impact big-money spending.

To Provide the Software That Will Run the Internet of Things . . .

$600

$400

$200

$–2014E 2015E 2016E 2017E 2018E 2019E

billions

SOURCE: BI Intelligence Estimates

Estimated Business Revenue

Five-Year CAGR 44%

Software & Services

Hardware

We Are Here

INDUSTRY SEGMENT TYPE OF SAVINGS EST. VALUE OVER 15 YEARS

Aviation Commercial 1% Fuel Savings $30 Billion

Power Gas-fired Generation 1% Fuel Savings $66 Billion

Health Care System-wide 1% Reduction in System Inefficiency $63 Billion

Rail Freight 1% Reduction in System Inefficiency $27 Billion

Oil & Gas Exploration and Development 1% Reduction in Capital Expenditures $90 Billion

The Internet of Things: Saving Money with GE’s Predix

22

Two Paths to ProfitsTo give you a sense of the huge profits that will come GE’s way, let’s take a moment to look at the notion of

an “operating system.” The recent trends in the smartphone market provide the best example.

If you own an Apple iPhone, your operating system is called iOS. Anyone who wants to build and sell an app for iOS must first get a license from Apple, and then write the app to work with the operating system. You can’t sell an iPhone app without it using iOS.

It’s the same thing with a smartphone using Google’s Android operating system. If you’re a software developer who wants to create and sell an app for Samsung (or the many other device-makers which use Android), you have to build it so it will work using Google’s operating system.

Here’s the best part: For Apple and Google, each of them makes 30% for every app sold in its app store.

Those fees add up. Currently, the Apple app store generates about $200 million in sales per year, while Google’s app store generates more than $100 million in sales. In terms of downloads, Google generates 200 million downloads versus 100 million for Apple.

Google’s Android operating system works on the phones of many manufacturers — from Samsung to LG to Sony to HTC. Google makes money by getting these manufacturers to direct phone users to use Google’s search services, which is where it makes most of its money. Google gives a piece of the sales generated by each Android device back to the phone maker, which incentivizes the company to stay with Android.

Apple’s iOS just works on its own phones. Apple makes money by pricing its iPhones so that it includes the cost of its iOS operating system. And don’t forget

— Apple keeps 30% of the sales from its app store. For GE and its Predix software, the emerging business model is a combination of the strategies of both Google and Apple.

First, Predix is going to be loaded onto every machine GE makes — from its aircraft engines to electricity generation turbines to its diesel locomotives — among many others. For these machines, GE will be like Apple. It will take a cut of all the sales generated by the equivalent of the Predix app store.

GE will also sell these customers access to its cloud storage systems and its data analytics. The company has been collecting and analyzing data for its own machines for more than five years now. If you buy a GE machine, you’ll want access to this data, so that you’re running it in a way that’s optimal for your operation.

Lastly, Predix is being sold to other machine manufacturers who want to offer “connected” machines that collect their own data. This is similar to how Google’s Android works with other cellphone- makers. In GE’s case, it will give these other machine- makers a cut of the sales that Predix generates from apps, cloud services and data analytics.

Predix is still at an early stage in terms of its rollout. In February 2016, GE opened Predix up to developers to create apps, and the Predix app store was rolled out in August 2105. Right now, there are just 31 apps in the store. However, as Predix is adopted as the standard for the industrial IoT, the apps are going to skyrocket … like what happened with Apple and Google.

As GE transforms itself from machine-maker to software and data analytics company for a market that’s valued at $225 billion, it’s going to be able to vastly improve its profit margins.

As a start, GE expects to generate $15 billion in sales from selling software and access to data and analytics by 2020. Those new sales will increase its profit margins from 8% to 10% today to 30% or more, similar to what Microsoft sees.

23

New Software Creates New Growth Opportunity

With the domination of Predix as the software of the industrial IoT, GE stands to create what is called a network effect. A network effect is a phenomenon where a good or service increases in value as more people use it.

We saw Apple swell thanks to the network effect. People who bought and fell in love with their iPhone started buying Apple’s Mac computers and their iPad. Part of the reason is that Apple’s devices are all designed to work seamlessly together. When you sync an iPhone to a Mac computer, everything works perfectly with no effort at all. It’s simple and easy — an attractive combination for consumers.

You can bet on something similar happening with GE’s connected products. Over time, you’ll see GE’s aircraft engines start to gain market share, because customers will like the easy connectivity.

This reality is not here … yet. The network effect didn’t immediately kick in for Apple when it released iPhone in 2007. However, nine years later, you can see that the network effect is very real for Apple.

For example, in 2007, Apple’s Mac computers sales were 5.3 million. By 2015, Mac computer sales had skyrocketed to 20.6 million units — a 288% increase in a time when overall PC sales are shrinking.

GE believes its digital businesses will generate $6 billion in total orders this year — that includes Predix, plus revenue from its cloud and the data analytics operations, as well as supporting services.

But in just the next four years alone, GE believes those sales will more than double to over $15 billion. By then, based on my analysis of the company’s financial statements, its digital businesses will make up about 13% of GE’s total yearly sales.

But remember that these are digital businesses we’re talking about, with much higher 30% profit margins, in line with what a successful software company would receive. So that figure — $15 billion in digital sales by 2020 — means the company would book over $4.5 billion in profits. That’s huge! GE’s profits would jump by almost 30% compared to current levels.

A Sleeker, Smarter GEWall Street analysts don’t give GE any credit for this coming digital transition. GE has been a hated stock

for nearly eight years now, and there’s a good reason for that. The company nearly went bankrupt during the 2008 financial crisis.

Annual Worldwide App Downloads

250

200

150

100

50

02013 2014 2015

Inde

xed

Dow

nloa

ds

— iOS App Store — Google Play

Annual Worldwide App Revenue

250

200

150

100

50

02013 2014 2015

Inde

xed

Reve

nue

— iOS App Store — Google Play

24

After its near-death experience, GE refocused itself around what it knew best: industrial businesses. The company sold off $180 billion in financial business assets. At the end of 2015, GE took the last of its financial businesses and spun those off as a separate company — Symphony Financial.

As a result, GE’s total debt has gone from an incredible $410 billion to $186 billion — a 55% reduction.

The government also lifted special regulations from GE due to its financial business exposure. This lift releases billions of dollars that GE was forced to hold as reserves just in case we had a repeat of 2008.

As a shareholder, this is going to be great opportunity, as GE has laid out its plans to use the released capital to buy back stock and pay dividends. In total, GE plans to buy back $55 billion in stock and pay another $35 billion in dividends.

Remember, our GoingUpness system looks for companies buying back stock when it’s cheap, and this buyback certainly comes under this category.

Right now, Wall Street analysts are modeling GE’s future as if Predix doesn’t exist. Current estimates sit at 6% sales growth and 15% earnings growth for 2016. However, these estimates are too low from two perspectives.

First, they don’t account for the explosive growth potential of Predix on GE’s financials, because it’s a new business segment.

Second, the sale of so many businesses, the spin-off and the buybacks have created a moving target that’s hard to model. Analysts are going to be conservative in modeling numbers.

Personally, I expect the company to guide analysts to nearly 10% sales growth and 20% earnings growth.

As Predix takes off, I expect GE to generate sales growth between 10% and 15% and sustain earnings- per-share growth of between 15% and 25% on a regular basis.

That’s important because the stock market just absolutely loves companies that can generate high- level, consistent sales and earnings growth. And when it finds a company that keeps generating these kinds of numbers, it gives them a high P/E multiple.

Right now, when you look at GE’s operating earnings, you’ll see that it has a forward P/E of about 18 based on 2017 earnings. However, companies that put up 10% to 15% sales growth and earnings-per- share growth of between 15% and 25% usually have ratios of 30 or even 35.

That means, as Predix powers GE’s earnings higher, we’ll get a second lift from rising valuation levels as measured by the P/E ratio. That’s why I expect GE to generate gains of as much as 200% over the next three years.

GoingUpness ChecklistBefore I give you my instructions to buy GE, let’s quickly do a GoingUpness check.

• Insiderness — GE’s management has done several things to signal Insiderness. One is that its CEO Jeffrey Immelt and another member of his management team have bought shares at current levels in the last year. Second, GE has recently completed a spin-off to restructure the way the company operates to increase its value. That’s another form of Insiderness that I look for. So GE solidly meets my Insiderness test.

• InDemandness — GE’s stock is above its 10-day moving average. Even better, the stock just hit a 52- week high after being range-bound for nearly six months. That’s a great sign that there’s huge demand

25

from big-money buyers who are willing to push the stock higher to buy it. GE meets the InDemandness test.

• Buyness — Market insiders have been jamming GE stock up and down since October 2015. That’s right about the time when it became clear that GE’s IoT initiative and financial restructuring were going to power its sales and earnings higher. That’s classic Wall Street rodeo riding, where they try to get dumb money investors to sell their stock cheaply to them. And for us, it’s a great sign that we’re on to a huge winner.

• ValueAbility — GE is doing a massive $55 billion buyback, so the stock is going to become more scarce. In addition, Predix and the IoT are set to create incredible value for GE, so there’s no question that GE stock controls something phenomenally valuable that more and more people desire.

Finally, GE’s management is rock solid. Jeffrey Immelt is the architect of GE’s current strategy to simplify the company, sell the financial businesses and go back to its roots of making things ... and also of innovation.

While we’re not buying GE for its dividend, investors will enjoy a dividend of $0.92 per share, which is a yield of almost 3%. And I fully expect this dividend to keep going up.

Action to take: Buy General Electric (NYSE: GE) up to $38.

GE is going to power higher immediately and generate gains of as much as 200% in the next three years.

Regards,

Paul MampillyEditor, Profits Unlimited

26

The Sovereign SocietyP.O. Box 8378Delray Beach, FL 33482 USAUSA Toll Free Tel.: (866) 584-4096 Email: http://sovereignsociety.com/contact-us Website: www.sovereignsociety.com

Legal Notice: This work is based on what we’ve learned as financial journalists. It may contain errors and you should not base investment decisions solely on what you read here. It’s your money and your responsibility. Nothing herein should be considered personalized investment advice. Although our employees may answer general customer service questions, they are not licensed to address your particular investment situation. Our track record is based on hypothetical results and may not reflect the same results as actual trades. Likewise, past performance is no guarantee of future returns. Certain investments such as futures, options, and currency trading carry large potential rewards but also large potential risk. Don’t trade in these markets with money you can’t afford to lose. Sovereign Offshore Services LLC expressly forbids its writers from having a financial interest in their own securities or commodities recommendations to readers. Such recommendations may be traded, however, by other editors, Sovereign Offshore Services LLC, its affiliated entities, employees, and agents, but only after waiting 24 hours after an internet broadcast or 72 hours after a publication only circulated through the mail.

(c) 2016 Sovereign Offshore Services LLC. All Rights Reserved; protected by copyright laws of the United States and international treaties. This Report may only be used pursuant to the subscription agreement. Any reproduction, copying, or redistribution, (electronic or otherwise) in whole or in part, is strictly prohibited without the express written permission of Sovereign Offshore Services, LLC. P.O. Box 8378, Delray Beach, FL 33482 USA.