to questions - sturm college of · pdf filequestions: 1. what are bank's duties as a...

TRANSCRIPT

QUESTION 4

ABC Company manufactures and sells heavy equipment to industrial users. ABC utilizes a manufacturing process known only to it and considers this process a valuable trade secret.

ABC borrowed $1,000,000 from Bank to use as operating capital. In exchange for the loan, ABC agreed to grant Bank a security interest in the following ABC property and assets:

All rights to payment including, without limitation, accounts, notes, and general intangibles; and all equipment, and any proceeds derived therefrom.

ABC defaulted on its loan and Bank repossessed ABC's equipment. Bank now has come to you seeking advice on how it should proceed. Bank informs you that it expects ABC's equipment and accounts to produce, a t best, no more than $250,000.

QUESTIONS:

1. What are Bank's duties as a secured party in possession of collateral?

2. May Bank, pending resale of the equipment, under any circumstances, permit periodic use by interested parties of any of ABC's equipment? Explain.

3. How can Bank best realize its interest in the receivables of ABC?

4. Is ABC's manufacturing process subject to the security agreement? Explain.

5. Is there any circumstance under which Bank may benefit from ABC's "trade secret"? Explain.

For purposes of the questions above, assume that the Uniform Commercial Code is in effect in this jurisdxtion, and that the security interest of Bank has been perfected.

DISCUSSION FOR QUESTION 4

Section 9-207(1) of the Uniform Commercial Code provides that a secured party must use "reasonable care" when it has collateral in its custody. The details of what constitutes reasonable care are fact specific and not raised by the question.

Section 9-207(4) of the UCC, by negative inference, prohibits the use of collateral by a secured party in possession except for the purpose of preserving the collateral or its value, or pursuant to court order or specific provision in the security agreement.

Under $9-502(1) of the UCC a secured party whose collateral consists of accounts may notify account debtors to remit payment directly to it a t any time that the debtor is in default. The secured party is also entitled to "take control" of proceeds of accounts which are perfected pursuant to §9-306 of the UCC. Here, since proceeds are specifically covered by the security agreement, the interest is perfected regardless of when the debtor received them. UCC 59- 306 (3) (a).

Trade secrets are general intangibles. UCC 59-106. An interest in trade secrets should be evidenced by specfically describing the trade secret or by including general intangibles as one of the categories of collateral in which a security interest is granted. Here, although the term "general intangibles" is included in the security agreement, i t seems to be used as a subset of "rights to payment" and not as a category of collateral in and of itself. A trade secret is not a right to payment and is arguably, therefore, not covered by the security agreement. However, the Bank may ultimately realize the value of the trade secret. It cannot be sold by the debtor without creating "proceeds," a "right to payment," or "accounts," all of which are collateral.

Examinee #

Final Score

SCORESHEET FOR QUESTION 4

ASSIGN ONE POINT FOR EACH STATEMENT BELOW

The Bank as a secured party must use reasonable care in the custody and possession of collateral in its possession.

Here, it does not appear that Bank, as secured party, may permit periodic use of the repossessed equipment.

A secured party's use of collateral in its possession is permitted:

3a. To preserve the collateral or its value;

3b. Pursuant to court order; or

3c. If permitted by the security agreement.

Bank should notify account debtors of ABC to make payment directly to it and secure any proceeds of accounts to which it is entitled.

Bank can sell accounts at UCC sale.

The manufacturing process is a general intangible.

Unclear whether Bank has an interest in general intangibles since its interest is one in "rights to payment includmg . . . general intangibles" and a trade secret may not be a "right to payment."

If Bank has a perfected interest in general intangibles it can sell the process; if it does not, it cannot (Bank sale).

Jf Bank's interest in the manufacturing process is not secured, Bank may still realize value through its interest in the debtor' receivables if the debtor utilizes the process again, or through execution on proceeds of sale (debtor sale), as a "right to payment" if the process is sold by the debtor.

/

QUESTION 4

Bank One loaned funds to the Appliance Center ("AC), a retail appliance store. To secure the loan, Bank One perfected a security interest in all AC's present and future inventory. Several months later, AC sold a refrigerator to Betty Buyer for a total price of $1,200. Buyer paid $100 down on the refrigerator and signed a Retail Sales Agreement in which she agreed to pay the balance in monthly installments of $100 each. The Retail Sales Agreement also stipulated that AC would retain title to the refrigerator until Buyer paid all the installments. AC immediately sold and delivered the written agreement Buyer signed to Credit Corporation. Credit Corporation then wrote Buyer a letter directing her to make her installment payments directly to Credit Corporation's office. AC filed for bankruptcy before Buyer made any installment payments.

QUESTIONS:

1. Discuss whether Bank One may recover the refrigerator from Buyer.

2. Discuss who has the rights to the installment payments Buyer will make on the refrigerator.

DISCUSSION FOR QUESTION 4

Issue One: Does a security interest in inventory have priority over the rights of a person who buys the inventory in the ordinary course of business?

A security interest in goods ordinarily continues in them notwithstanding their sale. UCC $9-306(2). A buyer in the ordinary course of business, however, takes free of any security interest created by his or her seller. UCC $8 9-307(1); 1-201(9). The rule protects the expectations of retail buyers.' I t obviates the need for elaborate investigations of title every time one purchases goods a t retail. In the problem, Rank One had security interest in the refrigerator Buyer purchased. I t was "inventory." UCC $9-109(4). Bank One's security interest was created by the Appliance Center, however. Because the Appliance Center was Buyer's seller, Buyer will take free of the interest if she is a buyer in the ordinary course of business.

Issue Two: Is a buyer on credit who purchases in good faith and without knowledge that the sale to her contravenes the interest of another nevertheless a "buyer in the ordinary course of business?

The Uniform Commercial Code defines a "buyer in the ordinary course of business" as any one who purchases goods from someone who sells goods of that kind in good faith, without knowledge that the sale contravenes the rights of others. UCC $5 1-20] (9); 9- 307(1). The Code's definition specifically includes persons who buy on credit. UCC $1- 201(9). In the problem, therefore, Buyer would enjoy the rights of a buyer in the ordinary course of business. Bank One could not recover the refrigerator from her.

Issue Three: Does Bank One have any right to the proceeds from the conditional retail sales agreement signed by Buyer?

The Uniform Commercial Code treats any reservation of title in a sale of goods as only the reservation of a security interest on behalf of the seller. UCC 2-401(1). I t also defines "chattel paper' as any writing which evinces both an obligation to pay money and creation of a security interest. UCC $9-105@). The retail installment contract Buyer signed thus meets both elements of the definition.

Issue Four: Does a security interest in inventory extend to chattel paper received upon the sale of the inventory?

Bank One would have a claim to the chattel paper Buyer signed. Generally, a security interest reaches anything received upon the sale or exchange of collateral. The chattel paper would be considered "proceeds" of Bank One's security interest in Appliance Center's inventory. UCC $9-306(1) and (2).

DISCUSSION FOR QUESTION 4 Page Two

Issue Five: Does a purchaser of chattel paper have priority over a secured party claiming the paper as "proceeds" of inventory?

Under the relevant priority rule of the Code, a person who purchases and takes possession of chattel paper in the ordinary course of its business will prevail over a secured party claiming the paper as "proceeds" of inventory. UCC 59-308(b). This priority rule applies even if the purchaser of the chattel paper knows of the secured party's interest in the inventory. UCC g9-308(b). Thus, Credit Corporation would have priority over Bank One in the chattel paper. I t would not matter that Bank One's financing statement was of record when Credit Corporation purchased the paper.

Essay 4 Gradesheet Seat m Please use blue or black pen and write numbers clearly

Bank One has a claim to the refrigeratorlcollateral even after the refrigerator is sold, as the refrigerator is part of the inventory. 1.

Buyer, however, has priority over the perfected security interest. 2.

2a. The refrigerator is consumer goods for buyer. 2a.

The refrigerator was purchased in the ordinary course of business which requires:

3a. Good faith purchase (bfp); 3a.

3b. No knowledge of bank's interest (bfp); 3b.

3c. Appliance Center deals in goods of that kind; and 3c.

3d. Buying includes sales on credit. 3d.

Bank One has some rights to the installment payments because a security interest extends to "proceeds" which is anything received upon sale of the collateral. 4.

Credit Corporation has a better claim to the installment payments than Bank One. 5.

5a. The contract obligating Buyer to pay the installments is "chattel paper." which embodies both an obligation to pay money and a security agreement. 5a.

5b. A purchaser of chattel paper who acquires it in the ordinary course of business has priority over a person claiming i t as proceeds of inventory. 5b.

5c. Perfection of paper is accomplished by possession. 5c.

QUESTION 1

Denver Electronic Business, Inc. (Denver) designs and markets computer software. In order to expand its business, Denver borrowed funds from First Bank & Trust Company ( Bank). Denver and Bank signed a security agreement which granted Bank a security interest in all Denver's "equipment, inventory, computer software and designs, now owned or hereafter acquired or developed."

Bank also had Denver sign a financing statement which identified the collateral in the same terms. Bank promptly filed the financing statement with the appropriate filing offices of the state and county in which Denver is headquartered and does business.

A few months later, Denver replaced its employees' computers and sold the old computers to Computer Sales, Inc. (Computer Sales), a business which buys and sells used computer equipment. A few weeks later, Betty Buyer (Buyer)purchased one of these machines from Computer Sale's retail store. Denver used $1,000 of the proceeds from the sale of its old computers to buy 100 shares of stock in TransWord, Corp. Denver received a fully executed stock certificate for the 100 shares from TransWord in Denver's name.

Unfortunately, Denver's business failed, forcing Denver to file bankruptcy. At the time of the filing, Denver's major asset was the successful word processing program it had developed, "Word-GO."

QUESTIONS:

1. Discuss who has priority in Word-GO and the Transword stock: Bank or the bankruptcy trustee.

2. Discuss whether Bank may recover the computer Buyer purchased from Computer Sales.

DISCUSSION QUESTION 1

Question 1: Who has priority in Word-GO and the Trans-Word stock?

A trustee in bankruptcy has the power to avoid unperfected security interests. This power is conferred by section 544(a)(1) of the Bankruptcy Code which grants the trustee the rights of a creditor who has obtained a judicial lien on all the debtor's assets. 11 U.S.C. Section 1 . The Uniform Commercial Code also recognizes the trustee's status as a lien creditor. Any lien creditor, including the trustee in bankruptcy, has priority over any unperfected security interest. UCC 9- 30l(l)(b). This power of the trustee to pull unperfected assets into the estate is often called the trustee's strong arm power.

A security interest is perfected when it has attached and the secured party has taken the steps required to complete perfection. 9-303(1). A security interest attaches once the debtor has acquired rights in the collateral, the secured party has given value and the parties have executed a written security agreement. 9-203(1). All these elements have been met, therefore First Bank's security interest has attached.

A security interest may also attach to after-acquired property as soon as the debtor acquires an interest in the property. Such an interest generally may be created only by specifically including in the security agreement an after-acquired property clause. A security interest attaches to proceeds of collateral whether or not the security agreement specifically so provides. The security agreement need not even mention proceeds. 9(306(2).

First Bank also seems to have taken all the steps the Code requires for perfection. Article Nine of the Code would classify computer software held for sale as inventory. 9-109(4). The intellectual property embodied in the software would be considered a general intangible. 9-106. In either case, a financing statement filed with the proper office would perfect the security interest. 9-302. By filing statements with the state, First Bank has done all that Article Nine requires. See, 9-401. Filing with the county is not required for this type of collateral, but this extra filing does not impair the valid filing.

Article Nine does not, however, apply to security interests subject to any statute of the United States and additional steps may be required for perfection under federal law. 9-104(a). A growing body of authority has held that security interests in copyrighted material, such as computer software, must be perfected by recording a copyright mortgage in the United States Copyright Office. See, e.g.,

National Peregrine, Inc. v. Capitol Federal Savings and Loan Association, (In re Peregrine Entertainment, Ltd.), 116 B.R. 194 (C.D. Cal. 1990). Therefore, the financing statements filed by First Bank may not have been enough to preserve its security interest in the word-processing program from avoidance by the bankruptcy trustee.

Finally, to perfect a security interest in certscated collateral, such as the TransWord stock certificates, the secured party must have physical possession of the stock and, unless it is a bearer certificate, the certificate must be endorsed by the named holder of the certificate. Since the bank does not have possession of the certificate, and it was not endorsed, the bank has no claim to the TransWord stock.

Question 2: May Bank recover the computer from Betty Buyer?

Generally, a buyer in the ordinary course of business takes free of only those security interests which were created by the buyer's seller. Buyers of used goods therefore may purchase them subject to pre-existing security interests. Computers used in a trade or business are classified as equipment under 9-109(2). A security interest in equipment is perfected by filing a financing statement so identifying the collateral. 9-302, 9-401, 9-402. The financing statements med by First Bank would, therefore, have perfected its security interest in all Debtor's computers.

A security interest will continue in collateral notwithstanding its sale. 9-306(2). The major exception to this rule is when the collateral is purchased by a buyer in the ordinary course of business. 9-307(1). That exception, however, only extends to security interests which were created by the buyer's seller. 9-307(1). Here, Betty Buyer purchased the computer from CSI which was not a party to the secured transaction creating the security interest in the computer. Thus, Article Nine does not by its terms give her priority over First Bank's security interest. It can be argued that the policy behind section 9-307 should be extended to protect Buyer. She, after all, purchased the computer from inventory from a merchant who deals in goods of that kind. In the interest of protecting free commercial interchange, the law arguably should not require such a purchaser to investigate title. The Code however seems to draw the line against purchasers of used goods. The "created by his seller9'_language of section 9-307 puts the onus on the purchaser of used goods to investigate title.

Essay I Gradesheet 21202

Seat 07 Please use blue or black pen and write numbers clearly

Who has ~rioritv in Word-Go and the TransWord stock?

A trustee in bankruptcy has the rights of a creditor who has obtained a judicial lien on the debtor's assets

A trustee has priority over any unperfected security interest

A security interest attaches if the debtor has rights in the collateral, the creditor has given value, and the debtor has signed a complete security agreement.

In order to be enforceable against third parties, an attached security interest must also be perfected.

Perfection is accomplished through controll possession, automatically or by filing

In this case, the security interest is perfected by filing.

A security interest may be taken in inventory, equipment and intangibles.

A security interest may attach to after-acquired property if stated in the security agreement.

A security interest attaches to proceeds of collateral whether or not the security agreement specifically so provides.

10. The cash fi-om the sale of the sale of the computers constitutes proceeds of collateralized equipment and is subject to the security interest.

1 1. To perfect a security interest in stock, the secured party must take possession/control.

12. The security interest in the TransWord stock is not perfected and the trustee prevails.

13. The Word-Go computer software is an intangible and may be subject to t h ~ perfected security interest.

14. Article 9 does not apply to security interests subject to any statute of the US such as copyrighted material, including software. Perfection is by recording a copyrighted mortgage with the US Copyright Office. .

Mav First Bank recover the computer from Betty Buyer?

15. A security interest in non-inventory items, such as the computer, continues notwithstanding its sale unless the security agreement provides otherwise.

16. Buyer is a buyer in due course without notice and normally would prevail.

17. While Article 9 does prevent a security interest from being effective against a buyer in due course, it does so only if the security interest was created by the buyer's immediate seller. The bank prevails.

QUESTION 4

On August 1, 2001, Acme Paving Corporation, a Delaware corporation with its principal place of business in Colorado, signed an agreement with Boulder Bank in which Boulder Bank agreed to finance Acme's operations with a $500,000 line of credit. The agreement granted Boulder Bank a security interest in "all equipment and inventory, now owned or hereafter acquired." At the time, Acme owned two old stone cutting machines. The Bank timely filed a financing statement with the Delaware Secretary of State which contained the names of the parties and which listed its collateral as "all inventory and equipment now owned or hereafter acquired." Neither party signed the financing statement. Nevertheless, the filing officer accepted the filing.

One year ago, Acme sold the two old stone cutting machines and purchased a new "Ramco Stone Cutter. "

Six weeks ago, Acme sold the Ramco Stone Cutter to the Endicott Stone Company which, in good faith, paid a fair price for the machine.

Acme has since defaulted on repayment of funds due Boulder Bank on the line of credit.

OUESTION:

Discuss whether Boulder Bank has a security interest in the Ramco Stone Cutter. Assume for purposes of this question that all relevant jurisdictions have adopted Revised Article 9 of the Uniform Commercial Code, effective July 1, 2001.

DISCUSSION FOR QUESTION 4

Generally, a security interest is not enforceable against the debtor under Revised Article 9 until it has attached. Rev. § 9-203 (a). Three steps are required for attachment of a security interest: value has been given, the debtor has rights in the collateral or the power to transfer rights in the collateral to the secured party, and the debtor has signed or authenticated a security agreement that provides a description of the collateral. Id. (b). Here the transaction between Bank and Acme has satisfied the three steps for attachment: Bank lent Acme $500,000, Acme had rights in its own inventory and equipment, and the parties signed a written security agreement describing the collateral. The after-acquired language is essential for the security interest to encompass later acquired equipment. Although the description of the collateral is quite general, Revised Article 9 states that a description of collateral reasonably identifies the collateral if it identifies the collateral by category or by a type of collateral defined in U.C.C. Rev. § 9-108 (b). Thus, Bank has an attached security interest in all of the debtor's current and after-acquired inventory and equipment, including the new Ramco Stone Cutter.

To be perfected, a security interest must have attached and the applicable steps necessary for perfection must have taken place. Rev. § 9-308 (a). Filing of a financing statement is one of the permissible methods of perfection for inventory and equipment (§ 9-3 10 (a). Boulder Bank did file a financing statement regarding its transaction with Acme. The only information on the financing statement was name of the debtor, the name of the secured party and a description of the collateral. These three pieces of information are the only items required on a financing statement. § 9-502 (a). The debtor's signature is no longer required on a financing statement, but the secured party is entitled to file a financing statement only if the debtor authorized the filing in an authenticated record. § 9-509 (a)(l). The filing is automatically authorized if the debtor authenticates a security agreement covering the same collateral that is described on the financing statement. Id. (b). In this case the debtor's signing of the security agreement describing the collateral is sufficient authorization of the filing.

Bank was correct in using the official corporate name of the debtor, Acme Paving Corporation, on the financing statement, and the description of the collateral is sufficient. §§ 9-503 (a)(l), 9-108 (b)(3). The place of filing of the financing statement is correct. The debtor's location controls the place of filing for nonpossessory security interests. Rev. § 9- 301 (1). A corporate debtor is deemed located in its state of incorporation. Rev. § 9-307 (e). Here the debtor is incorporated in the state of Delaware and the proper place of filing is with the Secretary of State of Delaware. Both the central filing is correct, Rev. § 9-501 (a)(2), and the chosen state is correct. Thus, Bank's security interest in Acme's inventory and equipment is perfected.

Boulder Bank will have a perfected security interest in the replacement cutter under the after acquired property clause in the financing statement. A security interest generally continues in collateral notwithstanding its sale. UCC §9-3 l5(a)(l). While buyers in the ordinary course of business take free of perfected security interests, other good faith purchasers do not. UCC §§9-320(a) and 9-3 17(b). To be a buyer in the ordinary course of business a person must purchase goods from a merchant who deals in goods of that kind. UCC §I-201(9). Here, Acme is not in the business of selling stone cutting machinery. The machinery is "equipment" in its business, not "inventory." As such, the sale of the machinery to Endicott was outside the ordinary course of Acme's business. Under the Uniform Commercial Code, Boulder Bank would be able to recover the machinery from Endicott even though Endicott purchased the machine in good faith without actual knowledge of Boulder Bank's security interest. Endicott is obligated to conduct a search of UCC filings to determine if there is a perfected security interest in the cutting machine. UCC §9-3 17(b).

7/03

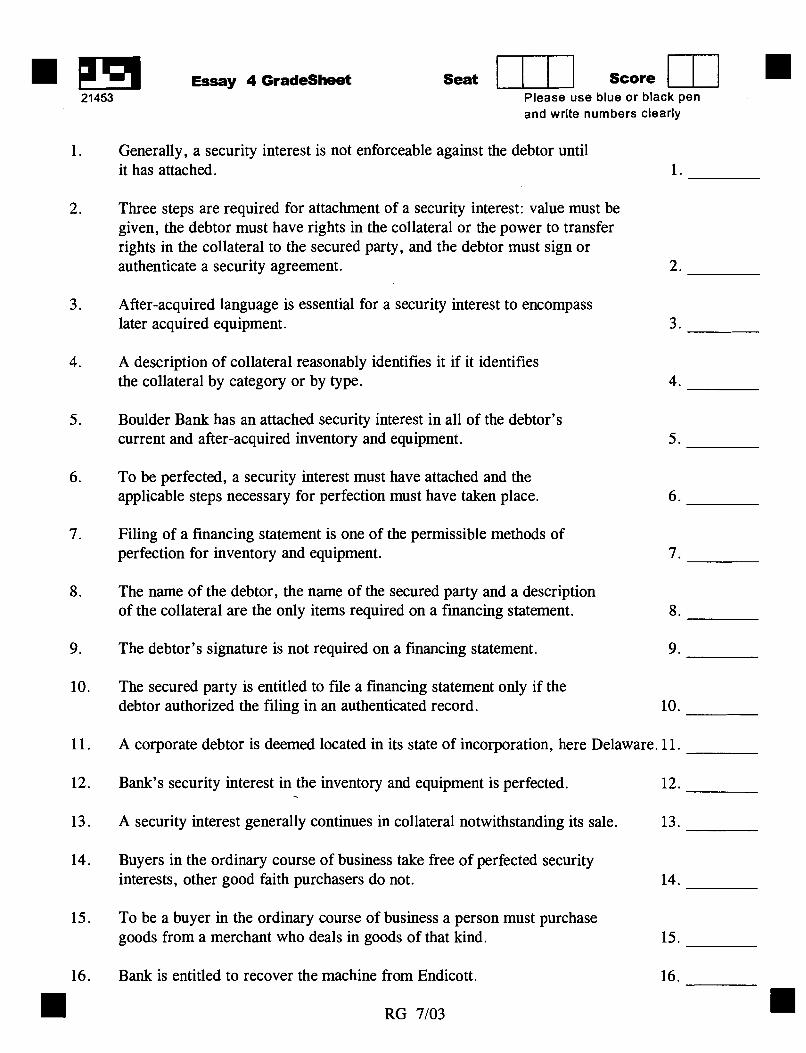

Essay 4 Gradesheet 21453

Seat score [77 Please use blue or black pen and write numbers clearly

Generally, a security interest is not enforceable against the debtor until it has attached.

Three steps are required for attachment of a security interest: value must be given, the debtor must have rights in the collateral or the power to transfer rights in the collateral to the secured party, and the debtor must sign or authenticate a security agreement.

After-acquired language is essential for a security interest to encompass later acquired equipment.

A description of collateral reasonably identifies it if it identifies the collateral by category or by type.

Boulder Bank has an attached security interest in all of the debtor's current and after-acquired inventory and equipment.

To be perfected, a security interest must have attached and the applicable steps necessary for perfection must have taken place.

Filing of a financing statement is one of the permissible methods of perfection for inventory and equipment.

The name of the debtor, the name of the secured party and a description of the collateral are the only items required on a financing statement.

The debtor's signature is not required on a financing statement.

The secured party is entitled to file a financing statement only if the debtor authorized the filing in an authenticated record.

A corporate debtor is deemed located in its state of incorporation, here Delaware. 11.

Bank's security interest in the inventory and equipment is perfected. . A security interest generally continues in collateral notwithstanding its sale. 13.

Buyers in the ordinary course of business take free of perfected security interests, other good faith purchasers do not. 14.

To be a buyer in the ordinary course of business a person must purchase goods from a merchant who deals in goods of that kind. 15.

Bank is entitled to recover the machine from Endicott. 16.

QUESTION 4

On March 5, 2002, Faucet Fabricating Corporation (Faucet), which has plants in three counties in Colorado, borrowed one million dollars from First Town Bank (First Bank) to finance its operations. Faucet and First Bank signed a security agreement giving First Bank a security interest in Faucet's "inventory, equipment, and accounts, now owned or hereafter acquired. "

On March 10, 2002, First Bank filed a financing statement with the Colorado Secretary of State which described the collateral as "inventory, equipment, and accounts" which was signed by Faucet's representative. The financing statement also contained the names and addresses of Faucet and First Bank. The debtor's name was listed as "Fabulous Faucets," the only trade name under which the debtor did business. The debtor's legal name, Faucet Fabricating Corporation, was not on the financing statement.

On December 8, 2002, Faucet borrowed $300,000 from Second Town Bank (Second Bank) to enable Faucet to purchase some sheets of gold to be used in a new line of gold-plated faucets.

On December 13, 2002, Faucet and Second Bank signed a security agreement giving Second Bank a security interest in the gold. The gold was delivered to Faucet's plant on December 17.

On December 19, 2002, Second Bank filed a proper financing statement with the Colorado Secretary of State. Second Bank had previously searched for financing statements under the name, "Faucet Fabricating Corporation," but did not find the financing statement filed by First Bank under the name "Fabulous Faucets."

Six months later Faucet defaulted on its loan obligations to First and Second Banks.

OUESTION:

Discuss the interests and priorities of each bank in Faucets' assets. You may assume that none of the items in question is a fixture under applicable state law and that the requirements for attachment ~f the security interest in the gold were met.

DISCUSSION FOR QUESTION 4

A security interest is not enforceable unless it has attached. An enforceable security interest requires that a creditor fulfill the requirements for attachment under UCC 5 9-203 by: having a written security agreement signed by the debtor and containing a description of the collateral (or possession of the collateral by the secured party pursuant to agreement); giving of value by the secured party to the debtor; and the debtor must have "rights in the collateral." First Town Bank meets all three requirements. It has a written security agreement signed by Faucet's representative and describing the collateral as "debtor's inventory, equipment and accounts, now owned or hereafter acquired;" it gave value to Faucet in the form of the million dollar loan, and Faucet presumably owns its current inventory, equipment, and accounts, which are the subject of the dispute.

Furthermore, the Code specifically validates after-acquired property clauses in security agreements. UCC 5 9-204(a). Thus First Town Bank's security interest attached to inventory, equipment, and accounts acquired by Faucet after the date the original security agreement was signed, as soon as Faucet acquired rights in them. First Town Bank has a valid enforceable security interest against Faucet.

A secured party may perfect a security interest in goods and accounts by filing a financing statement. UCC 5 9-3 10. A filed financing statement must contain certain minimal information--the names and addresses of the debtor and the secured party; and a statement describing the items or listing the types of collateral (and, if real property, a description of the property). UCC 5 9-502. First Town Bank complied with most of these requirements in the financing statement filed on March 10, 2002. The financing statement contained the names and addresses of the parties, and a statement listing the types of collateral--inventory, equipment, and accounts. The description "inventory, equipment, and accounts " is adequate to perfect a security interest in current and after-acquired property. James J. White and Robert S. Summers, Uniform Commercial Code 5 22-14(d) (4th ed. 1995).

The problem involves the debtor's name on the financing statement. The financing statement must not contain any seriously misleading errors. If the debtor is a registered organization (e.g., a corporation), the debtor's name is seriously misleading if it does not match the name under which the debtor was organized. Use of a trade name is insufficient, unless, under a "safe harbor" provision in the Code, the financing statement would be discovered in a filing office s'earch under the debtor's correct name. UCC 5 9-503, 9-506. Here, First Town Bank used only the debtor's trade name, "Fabulous Faucets," on the financing statement.

The issue becomes whether "Fabulous Faucets" is sufficiently similar to the corporation's legal name so that the financing statement would be discovered by third parties using the corporation's legal name. The answer is probably no, since Second Town Bank did not find the financing statement filed under "Fabulous Faucets".

DISCUSSION FOR QUESTION 4 Page Two

First Town Bank did file its financing statement in the correct location. The filing must be done centrally with the Colorado Secretary of State, as Colorado is both the location of the debtor and the location of the collateral. UCC 5 9-501(a)(2). However, because of the error in the debtor's name, it is likely that First Bank's security interest is unperfected.

Second Town Bank took a security interest in certain sheets of gold acquired by Faucet in December 2002 by executing a security agreement. Further, Second Town Bank properly perfected its security interest in the gold by filing a proper financing statement with the Colorado Secretary of State.

First Town Bank can claim the gold as part of Faucet's after-acquired inventory because raw materials are within the Code definition of inventory. UCC 5 9-102(a)(48). But if First Town Bank's security interest is arguably unperfected based on the reasoning above, Second Town Bank would have priority over First Town Bank in the gold because generally, a perfected security interest prevails over an unperfected security interest. UCC 5 9-322(a)(2).

However, if the error in the debtor's name is not deemed to prevent perfection of First Town Bank's security interest, then Second Town Bank, in order to assert priority, will have to assert a purchase money security interest (PMSI) superpriority for inventory financers under UCC 5 9-103. A PMSI in inventory is perfected if the filing takes place before the debtor gets possession of the inventory, and the second secured party delivers an authenticated notice of the PMSI to the first secured party who previously filed a security interest in the same inventory (i.e., the after-acquired property) before the debtor receives possession of the inventory. To assert the superpriority , Second Town Bank was required to file a financing statement before the debtor received possession of the gold. Faucet received the gold on December 17, and Second Town Bank made its filing on December 19. Moreover, Second Town Bank was required to give individual written notification of its interest to prior inventory secured parties with financing statements on file. It did not notify First Town Bank of its interest.

Therefore, if First Town Bank's filing is held to be adequate, the party first either to file or to perfect would contrijl, and First Town Bank as the first party to file against inventory would prevail. UCC 5 322(a)(l).

r COLORADO SUPREME COURT FEBRUARY 2004 BAR EXAM 1

ISSUE

Board of Law Examiners

ESSAY Q4

Regrade

SEAT mi A security interest is not enforceable unless it has attached.

Attachment of a security interest generally requires a written security agreement, description of collateral, secured party's giving value, and the debtor having rights in collateral.

A security interest may attach to after-acquired property.

First Town Bank has an enforceable security interest against Faucet.

First Town Bank may claim the gold is after-acquired property subject to its security interest.

A trade name instead of the corporate name on a financing statement is not sufficient,

6a. unless it is similar enough to find the financing statement under a filing office search of the correct name.

Because of the error in the name in the financing statement, First Town Bank's security interest is likely unperfected.

Second Town Bank has a perfected security interest in the gold purchased in December 2002.

A perfected security interest has priority over an unperfected security interest.

Second Town Bank has priority over First Town Bank in the gold based on the first-to-file or perfect rule.

Superpriority requires prior receipt of inventory by debtor:

1 1 a. filing the financing statement;

YES

1. 0

2. 0

3. 0

4. 0

5 . 0

6. 0

6a. 0

7. 0

8. o

9. 0

10. 0

11. 0

Ila. 0

1 lb. notice of the PMSI to other secured parties. l lb . 0

If First Bank's interest is perfected, Second Bank does not qualifL for the inventory 12. 0

purchase money security interest (PMSI) superpriority.

BLE Gradesheet v2.0 page I of I J

QUESTION 5

Note: all dates refer to the year 2004.

On March 1, BigBank made a $1 million loan to Music Makers, Inc., a corporation chartered under the laws of the state of Euphoria. Music Makers sells and leases pianos through its retail stores located throughout Euphoria. To secure repayment of the loan, Music Makers granted to BigBank an enforceable security interest in its inventory and equipment. The security agreement included an after-acquired property clause. On March 10, BigBank filed a financing statement against the collateral, which was proper in all respects, with the appropriate Euphoria officials.

On June 1, Music Makers changed its legal name to Essex Keyboards Company, effective as of that date, and requested its new name through the Euphoria Secretary of State.

On August 1, PianoMax sold ten grand pianos to Essex Keyboards. PianoMax retained an enforceable security interest in the grand pianos to secure repayment of the purchase price. On August 5, PianoMax sent a written notice of its security interest in the pianos to BigBank. The contents of the notice satisfied the statutory requirements of UCC Article 9. On August 9, BigBank received the notice. On August 16, PianoMax filed its financing statement, proper in all respects, with the appropriate Euphoria official. On August 18, PianoMax shipped the grand pianos from its New York City warehouse and delivered them to Essex Keyboards.

On November 1, Essex Keyboards bought a photocopier from the seller, Acorn Systems. Acorn retained an enforceable security interest in the photocopier to secure repayment of the purchase price. On November 7, Acorn delivered and installed the photocopier. On November 29, Acorn filed a proper financing statement against the photocopier with the appropriate Euphoria official. Acorn had knowledge of BigBank's financing statement, but Acorn never gave notice of its interest to BigBank.

OUESTIONS:

1. Discuss whose security interest in the ten grand pianos enjoys priority, BigBank's or PianoMax's. Assume that Essex Keyboards still owns all ten grand pianos.

2. Discuss whose security interest in the photocopier enjoys priority, BigBank's or Acorn's. Assume that Essex Keyboards still owns the photocopier.

DISCUSSION FOR QUESTION 5

U?zose security interest in the ten grand pianos enjoys priority between BigBank and PianoMax?

The facts state that BigBank has an "enforceable security interest" in the inventory and equipment of Music Makers. Therefore, a general discussion of attachment under UCC 9-203 is not required. Music Makers acquired the pianos after it executed the security agreement with BigBank, but the security agreement included an after-acquired property clause (as permitted by UCC 9- 204(a)). The after-acquired property clause permitted BigBank's security interest to attach to the pianos because the collateral description included "inventory." The pianos are inventory under UCC 9-102(a)(48)(B) because Music Makers holds the pianos for sale or lease in its ordinary course of business.

BigBank may perfect its security interest in the pianos under UCC 9-3 10 by filing a financing statement. The proper place to file the financing statement under UCC 9-301 (1) is in the state where the debtor is located. Music Makers is chartered under Euphoria law and is an example of a "registered organization" under UCC 9- 1 O2(a)(7O). As a registered organization, Music Makers is deemed to be located in the state of its incorporation, Euphoria, under UCC 9-307(e). Therefore, BigBank filed its financing statement in the proper jurisdiction (Euphoria) on March 10.

When "Music Makers, Inc." changed its name to "Essex Keyboards Company" on June 1, BigBank had four months to refile its financing statement under the new name (if the change is "seriously misleading") to have continued and unintempted perfection under UCC 9-507(c). The change is almost certainly seriously misleading because a filing under "Music Makers, Inc." would not be found in a search against "Essex Keyboards Company." BigBank's financing statement remained effective to perfect collateral owned by Essex Keyboards at the date of the change (June 1) and any collateral acquired by Essex within four months after the change (through September 30). Therefore, BigBank7s filing remained effective to perfect a security interest in the pianos because Essex purchased them in August (within the fbur-month period).

The facts state that PianoMax has an "enforceable security interest" in the pianos. Therefore, no discussion of attachment under UCC 9-203 is warranted. For reasons previously discussed, PianoMax perfected its security interest by filing a financing statement with the appropriate Euphoria official.

Under the first-to-file-orperfect rule of UCC 9-322(a)(l), BigBank's security interest enjoys priority beca~~se BigBank filed its financing statement on March 10 and PianoMax did not file its financing statement until August 16. As the pianos were acquired by Essex after BigBank filed its financing statement on March 10, its filing date trumps any later perfection date of either party.

Notwithstanding the result under UCC 9-322(a), PianoMax may argue that its security interest enjoys superpriority under UCC 9-324(b), available to a creditor holding a purchase-money security interest in inventory. (IJCC 9-324(b) trumps UCC 9-322(a) under UCC 9-322(f)(l).) PianoMax has a purchase-money security interest in the pianos under 9- 1 O3(a) and (b), as PianoMax

DISCUSSION FOR QUESTION 5 Page Two

sold the pianos to Essex Keyboards and the security interest secures repayment of the unpaid purchase price. The pianos are inventory because Essex Keyboards is in the business of selling and leasing pianos. PianoMax also must satisfy four other statutory requirements. PianoMax satisfied UCC 9-324(b)(l) because it perfected its security interest by filing on August 16, before delivering the pianos on August 18. PianoMax met UCC 9-324(b)(2) by sending a notice of its security interest to BigBank on August 5. The notice was timely under UCC 9-324(b)(3) because BigBank received the notice on August 9, before Essex Keyboards received the pianos on August 18. And UCC 9- 324(b)(4) is met because the facts state that the contents of the notice satisfied the requirements of UCC Article 9. Therefore, because PianoMax has satisfied all of the statutoryrequirements ofUCC 9-324(b), its purchase-money security interest in the pianos enjoys superpriority over BigBank's perfected security interest.

Whose security interest in the photocopier enjoys priorily between BigBank and Acorn?

As Essex Keyboard is in the business of selling and leasing pianos, the photocopier is "equipment" under UCC 9- 1 O2(a)(33). BigBank's security interest extends to the photocopier because its collateral description in the security agreement included "equipment" and the security agreement included an after-acquired property clause (as permitted by UCC 9-204(a)). However, Essex Keyboards acquired the photocopier on November 1, more than four months after its "seriously misleading" name change on June 1. Therefore, BigBank's financing statement is no longer effective to perfect the interest in this item under UCC 9-507(c)(2). Accordingly, BigBank has a security interest in the photocopier, but its security interest is unperfected.

The facts state that Acorn retained an "enforceable security interest" in the photocopier. As mentioned earlier, filing a financing statement with the appropriate Euphoria official will perfect a security interest in equipment. Therefore, Acorn's security interest became perfected when it filed its financing statement on November 29.

Acorn sold the photocopier to Essex Keyboards and retained a security interest in the item to secure repayment of the purchase price, so Acorn has a purchase-money security interest in the photocopier under UCC 9- 1 O3(a) and (b). Accordingly, Acorn may argue that its purchase-money security interest is entitled to superpriority under UCC 9-324(a) (available to non-inventory collateral, such as equipment), which does not require the purchase-money creditor (Acorn) to give any notice to any pre-existing creditor (BigBank). But Acorn filed its financing statement on November 29, more than twenty days after delivering the photocopier to Essex Keyboards on November 7, so Acorn is not entitled to superpriority under UCC 9-324(a). Nevertheless, Acorn's security interest enjoys priority under UCC 9-322(a)(2) because Acorn's security interest is perfected and BigBank's security interest in unperfected.

Board of Law Examiners

ESSAY Q5

ISSUE

JULY 2005 BAR EXAM Regrade

SEAT

BigBank may claim that it has priority on the 10 pianos because of its "after-acquired property" clause.

To perfect its interest BigBank must file in Euphoria, the State of MMI's registration.

When MMI changed its name to Essex Keyboards, Big Bank needed to file its UCC statement under the new name within 4 months to remain perfected.

Normally, BigBank would have priority over PianoMax because it filed its UCC statement first.

PianoMax would have priority over BigBank because it has a Purchase Money Security Interest in the 10 pianos.

PianoMax filed its UCC Statement before delivery of the pianos.

PianoMax sent a proper notice to BigBank before delivery of the piano.

The Notification sent asserted a PMSI and described the Inventory.

BigBank's UCC filing did cover the photocopier, as it is after-acquired equipment.

Since the photocopier was not acquired until more than four months after Music MakerIEssex Keyboard's name change, BigBank's UCC filing is ineffective.

POINTS AWARDED

1. 0

2. 0

3. 0

4. 0

5 . 0

6. 0

7. 0

8. 0

9. 0

10. 0

Since BigBank is unperfected on November 29, Acorn's UCC filing gives it priority. 11. 0

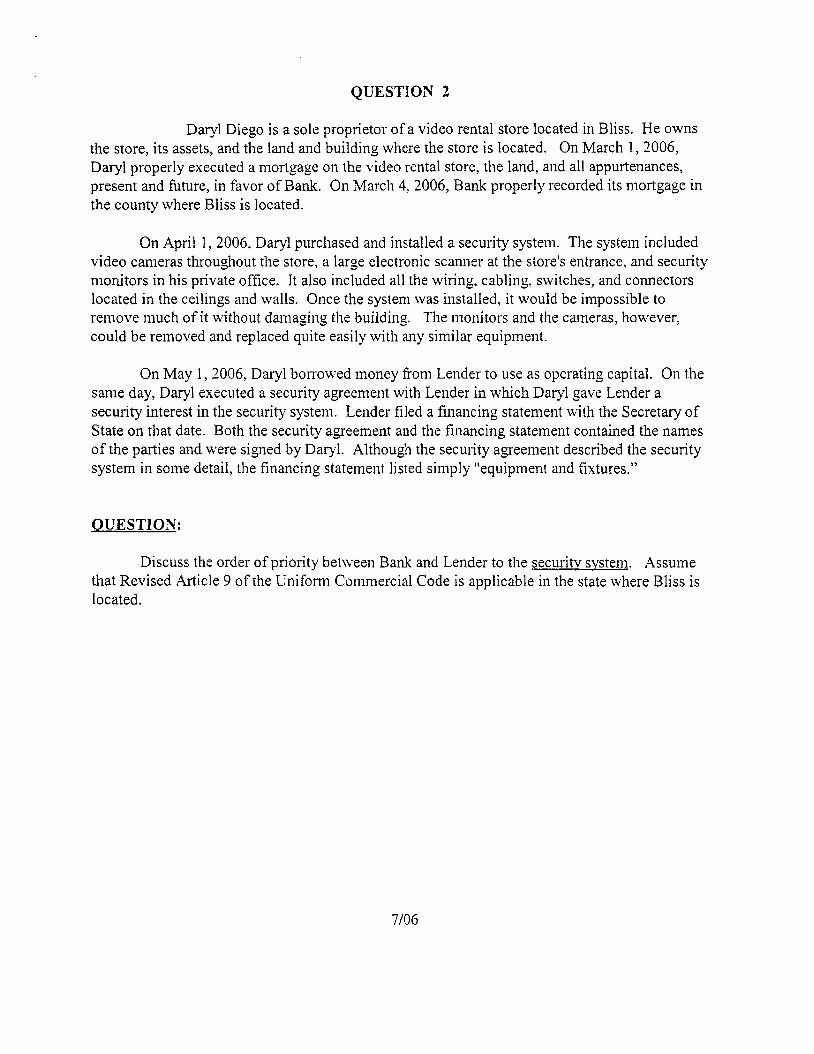

QUESTION 2

Daryl Diego is a sole proprietor of a video rental store located in Bliss. He owns the store, its assets, and the land and building where the store is located. On March 1,2006, Daryl properly executed a mortgage on the video rental store, the land, and all appurtenances, present and future, in favor of Bank. On March 4, 2006, Bank properly recorded its illortgage in the county where Bliss is located.

On April 1,2006, Daryl purchased and installed a security systetn. The syste~n included video canleras throughout the store, a large electronic scanner at the store's entrance, and security morcitors in his piivate office. It also included all the wiring, cabling. switches, and conllectors located in the ceilings and walls. Once the system was installed, it would be impossible to remove much of it without damaging the building. The nloilitors and the cameras, however, could be removed and replaced quite easily with any similar equipment.

On May 1,2006, Daryl borro~ved money from Lender to use as operating capital. On the same day, Daryl executed a security agreement with Lender in which Daryl _gave Lender a security interest in the security system. Lender filed a financing statement with the Secretary of State on that date. Both the security agreement and the financing statement contained the names of the parties and were signed by Dai-yl. Although the security agreement described the security system in some detail, the financing statement listed simply "equipment and fixtures."

QUESTION:

Discuss the order of priority between Bank and Lender to the security system. Assume that Revised Article 9 of the Unifarn~ Commercial Code is applicable in the state where Bliss is located.

DISCUSSION FOR QUESTION 2

1. Is the security system a fixture under state law?

Under Revised Article 9 of the Uniform Con~mercial Code, "[flistures rneans goods that have become so related to particular real property that an interest in them arises under real property law." Rev. 9-1 02(a)(41). In other words, the Code defers to 11on-Code state law definitions of fixtures. The bar examinee should note that parts of the security system are quitc firmly annexed to the video store, that removal of the basic structure of the system would take considerable effort and result in damage to the store building, and that Daryl owns the building to which the system was annexed. On the other hand, certain parts of the system, the video cameras and the monitors, can be easily removed. Unless thesc parts arc considered to be an integral part of that particular security system, then they might be classified as chattels. l.11 other words, if Daryl could use any cameras or monitors. not necessarily those particular ones. in the system, then they would not be viekvcd as uniqucly adapted to that system. If the cameras and monitors are not fixtures, they would be considered "equipment" under Article 9. Rev. 9 9-102(a)(33).

2. \\'hat does it take for a security interest to attach and perfect a security interest'!

There are three requirements for attachment of a security interest: (i) the parties must have an agreement authenticated by the debtor that the security interest attach; (ii) value must be given by the secured party; and (iii) the debtor must have rights in the collateral. W.C.C. $9- 203(b)]. The security agreement must be signed by thc debtor and must describe the collateral.

A security agreement alone is sufficient to give a lender priority over the borrower to the collateral. However, to give priority over third parties to the collateral. the security interest must be perfected. Here, perfection is through iiling a financing statement. The financing statement must contain the names of the debtor and creditor, a description of the collateral and for fixtures must describe the real property where the fixtures are located. Filing for chattels is with the Secretary of State and for fixtures is with the clerk and recorder of the county where the collateral is located. Priority is deternli~~ed by who is the first to properly file.

3. Did Bank file a proper mortgage covering equipment and fixtures?

Bank recorded a valid Inortgagc covering the video store, the surrounding land, and all appurtcnances, prcsent and fkturc. Thc mortgage was filed in the proper county. The UCC considers a mortgage that describes fixtures as a security agreement. The security system, as a fixture, would be considered an appurtenance to the real estate and thus subject to Bank's mortgage interest.

4. Did Lender's financing statement and security agreement satisfy the requirements of Article 9:'

Lender's security agreenlent \vith Daryl seeins to satisfy the Articlc 9 requirements for attachment

DISCUSSION FOR QUESTION 2 Page Two

that the debtor "has authenticated a security agreement that provides a description of the collateral." Lender and Daryl seem to have a conventional security agreement that Daryl has signed and that describes the security system in some detail.

A financing statement is sufficient only if it prcvides the pCarties1 names and "indicates the collateral covered by the financing statement." Rev. 5 9-502(a). Lender's financing statement provides the parties' names and an indication of the collateral. Under Rev. fj 9-504, an indication of collateral is sufficient if it provides a description that complies with Rcv. $ 9-108. Rev. S 9- 108 (b) provides that a description of collateral is sufficient if it identifies the collateral by a U.C.C. category. Thus, Lender's description of the collateral as "equipment and fixtures" would be sufficient since those terms are Code categories of collateral. Rev. $ 9-102(a)(33), (ill).

5. Assuming the security system is a fixture, did Lender file its financing statement in the appropriate office'!

Article 9 gives fixture financiers the option of making an ordinaty Article 9 filing or mal i lg a fixture filing. Re.ir. 5 9-501(a)(l). Both types of filings serve to perfect the secured party's security interest, but as against different groups of competing claimants. An ordinary chattel filing will perfect the interest of the fixture financier against the interests of other chattel claimants -- i.e., other Article 9 secured parties and lien creditors. In re Lucero, 203 B.R. 322 (B.A.P. 10'' Cir. 1996). A fixture filing will give protection against the interests of both chattel claimants and real estate clai~~iants, such as real estate mortgagees. Rev. 4 9-334 (d), (e)(l). Lender did not make a fixture filing here, but instead made a chattel filing in the Secretary of State's office. This filing is sufficient to perfect Lender's security interest in the security system as a fixture as against the claims of other chattel claimants.

6. As betveen Bank and Lender, who has priority in the security system?

Article 9 generally ranks secured creditors first in time, first in right. Rev. 5 9-322 (a)(l). Although Bank filed its mortgage before Lender, it filed only in the county and not with the Secretary of State. This perfects the security interest ia the fixtures, but the cameras and monitors may are not considered fixtures, but are chattels. Filing only in the county did not perfect the security interest in the chattels. Lender properly filed with the Secretary of State and, accordingly, perfected its security interest in the cameras and monitors. Bank will have priority in the fixtures while Lender will have priority in the chattels.

JULY 2006 BAR EXAM Board of Law Examiners Regrade

ESSAY Q2 SEAT

ISSUE POINTS AWARDED

1. To have a perfected security interest. a party must have a security agreement that attaches and 1. o is filed with the proper office.

2. Security Agreement must be signed by debtor and describe collateral.

3. Attachment defined

3a. Security Agreement; 3a. 0

3b. Value given by the secured party: 3b. 0

3c. Debtor has rights in the collateral. 3c. 0

4. Perfection requires tiling in the proper office

4a. Secretary of State for chattels: 4a. 0

4b. County clerk for real estate and fixtures. 4b. 0

5 . Fixtures are goods that have become so related to particular real property that an interest in 5 . 0 them arises under real property law.

6. Chattels defined as equipment and other property easily removed.

7. Monitors and camera are chattels/equipn~ent.

8. Balance of the security system attached to the building are fixtures.

9. First to perfect has priority.

10. Financing statement requires names of parties and description of collateral.

1 1. Describing "equipment and fi>tturesU is adequate.

12. After acquired property clauses are generally enforceable.

13. Bank has priority in fixtures.

14. Lender has priority i n equipment.

BLE Gradesheet v2.1 page I of 1