to the board of trustees - hamburg township, michiganhamburg.mi.us/accounting/audited...

TRANSCRIPT

1

November 14, 2013 To the Board of Trustees Township of Hamburg We have audited the financial statements of the Township of Hamburg (the “Township”) as of and for the year ended June 30, 2013 and have issued our report thereon dated November 14, 2013. Professional standards require that we provide you with the following information related to our audit which is divided into the following sections:

Section I - Required Communications with Those Charged with Governance

Section II - Legislative and Informational Items

Section I includes information that current auditing standards require independent auditors to communicate to those individuals charged with governance. We will report this information annually to the board of trustees of the Township of Hamburg.

Section II contains updated legislative and information items that we believe will be of interest to you.

We would like to take this opportunity to thank the Township’s staff for the cooperation and courtesy extended to us during our audit. Their assistance and professionalism are invaluable.

This report is intended solely for the use of the board of trustees and management of the Township of Hamburg and is not intended to be and should not be used by anyone other than these specified parties.

We welcome any questions you may have regarding the following communications and we would be willing to discuss any of these or other questions that you might have at your convenience.

Very truly yours,

Plante & Moran, PLLC

Michael J. Swartz

To the Board of Trustees November 14, 2013 Township of Hamburg

2

Section I - Communications Required Under AU 260

Our Responsibility Under U.S. Generally Accepted Auditing Standards

As stated in our engagement letter dated July 8, 2013, our responsibility, as described by professional standards, is to express an opinion about whether the financial statements prepared by management with your oversight are fairly presented, in all material respects, in conformity with U.S. generally accepted accounting principles. Our audit of the financial statements does not relieve you or management of your responsibilities. Our responsibility is to plan and perform the audit to obtain reasonable, but not absolute, assurance that the financial statements are free of material misstatement.

As part of our audit, we considered the internal control of the Township of Hamburg. Such considerations were solely for the purpose of determining our audit procedures and not to provide any assurance concerning such internal control.

We are responsible for communicating significant matters related to the audit that are, in our professional judgment, relevant to your responsibilities in overseeing the financial reporting process. However, we are not required to design procedures specifically to identify such matters.

Planned Scope and Timing of the Audit

We performed the audit according to the planned scope and timing previously communicated to you in our meeting about planning matters on September 6, 2013.

Significant Audit Findings

Qualitative Aspects of Accounting Practices

Management is responsible for the selection and use of appropriate accounting policies. In accordance with the terms of our engagement letter, we will advise management about the appropriateness of accounting policies and their application. The significant accounting policies used by the Township of Hamburg are described in Note 1 to the financial statements. As described in Note 13, the Township changed accounting policies related to GASB Statement No. 63, Financial Reporting of Deferred Outlfows of Resources, Deferred Inflows of Resources, and Net Position. Accordingly, the accounting change has been retrospectively applied to prior periods presented as if the policy had always been used.

We noted no transactions entered into by the Township during the year for which there is a lack of authoritative guidance or consensus.

There are no significant transactions that have been recognized in the financial statements in a different period than when the transaction occurred.

To the Board of Trustees November 14, 2013 Township of Hamburg

3

Accounting estimates are an integral part of the financial statements prepared by management and are based on management’s knowledge and experience about past and current events and assumptions about future events. Certain accounting estimates are particularly sensitive because of their significance to the financial statements and because of the possibility that future events affecting them may differ significantly from those expected. There were no significant balances, amounts, or disclosures in the financial statements based on sensitive management estimates.

The disclosures in the financial statements are neutral, consistent, and clear.

Difficulties Encountered in Performing the Audit

We encountered no significant difficulties in dealing with management in performing and completing our audit.

Disagreements with Management

For the purpose of this letter, professional standards define a disagreement with management as a financial accounting, reporting, or auditing matter, whether or not resolved to our satisfaction, that could be significant to the financial statements or the auditor’s report. We are pleased to report that no such disagreements arose during the course of our audit.

Corrected and Uncorrected Misstatements

Professional standards require us to accumulate all known and likely misstatements identified during the audit, other than those that are trivial, and communicate them to the appropriate level of management. Management has corrected all such misstatements.

Significant Findings or Issues

We generally discuss a variety of matters, including the application of accounting principles and auditing standards, business conditions affecting the Township, and business plans and strategies that may affect the risks of material misstatement with management each year prior to retention as the Township’s auditors. However, these discussions occurred in the normal course of our professional relationship and our responses were not a condition of our retention.

Management Representations

We have requested certain representations from management that are included in the management representation letter dated November 14, 2013.

To the Board of Trustees November 14, 2013 Township of Hamburg

4

Management Consultations with Other Independent Accountants

In some cases, management may decide to consult with other accountants about auditing and accounting matters, similar to obtaining a “second opinion” on certain situations. If a consultation involves application of an accounting principle to the Township’s financial statements or a determination of the type of auditor’s opinion that may be expressed on those statements, our professional standards require the consulting accountant to check with us to determine that the consultant has all the relevant facts. To our knowledge, there were no such consultations with other accountants.

To the Board of Trustees November 14, 2013 Township of Hamburg

5

Section II - Legislative and Informational Items

Personal Property Tax

The personal property tax was repealed by the passing of several bills during the Legislature's lame duck session in December. This repeal is contingent upon a statewide vote in August 2014 to allow for a shifting of the use tax to a reimbursement fund. Key provisions of the act phase out the industrial portion of the tax over a nine-year period beginning in 2016. Also, businesses with less than $40,000 taxable value in industrial and commercial personal property in any jurisdiction would no longer pay the tax. For the July 2013 and December 2013 levies, it will be business as usual and communities will continue to levy as they normally have. However, for the July 2014 levy, this will change. Communities will not be able to levy businesses with less than $40,000 taxable value in industrial and commercial personal property. If during the statewide vote in August 2014 the proposed personal property tax legislation fails, for future levies the less than $40,000 taxable value will no longer be in effect. If this is the case, the communities will not be able to recover the amounts that were not levied in the July 2014 levy for the taxable values less than $40,000 for industrial and commercial personal property; this will just be lost. While the Township brings in a minimal amount of personal property tax, this is an important item to keep in mind.

As for the impact on local communities, in short, those local governments that would lose at least 2.3 percent of their property tax base as a result of the changes would be eligible to be reimbursed at 80 percent of the revenue the personal property tax currently provides. This reimbursement would come from the Metropolitan Area Authority, a newly created entity led by five members appointed by the governor. This authority would be responsible for distributing the use tax collections as well as monies generated from expiring tax credits.

In addition, local governments would have the option to assess a special assessment on industrial property (referred to as essential services assessments). This assessment would not require local voter approval and would reimburse police, fire, ambulance services, and jail operations to ensure they receive 100 percent of the funding that they now get from the personal property tax.

When working through upcoming budgets and longer-term projections, please keep these items in mind. The final act has not yet been published by the State.

The Michigan Municipal League has developed a tool to aid communities in calculating the potential impact of the personal property tax cuts:

http://www.mml.org/advocacy/inside208/post/PPT-calculation-spreadsheet-available.aspx

Township of Hamburg

Financial Report

with Supplemental Information

June 30, 2013

Township of Hamburg

Contents

Report Letter 1-3

Management's Discussion and Analysis 4-7

Basic Financial Statements

Government-wide Financial Statements:Statement of Net Position 8Statement of Activities 9-10

Fund Financial Statements:Governmental Funds:

Balance Sheet 11Reconciliation of the Balance Sheet to the Statement of Net Position 12Statement of Revenue, Expenditures, and Changes in Fund Balances 13Reconciliation of the Statement of Revenue, Expenditures,

and Changes in Fund Balances of Governmental Fundsto the Statement of Activities 14

Proprietary Fund:Statement of Net Position 15Statement of Revenue, Expenses, and Changes in Net Position 16Statement of Cash Flows 17

Fiduciary Funds - Statement of Fiduciary Net Position 18

Notes to Financial Statements 19-37

Required Supplemental Information 38

Budgetary Comparison Schedule - General Fund 39

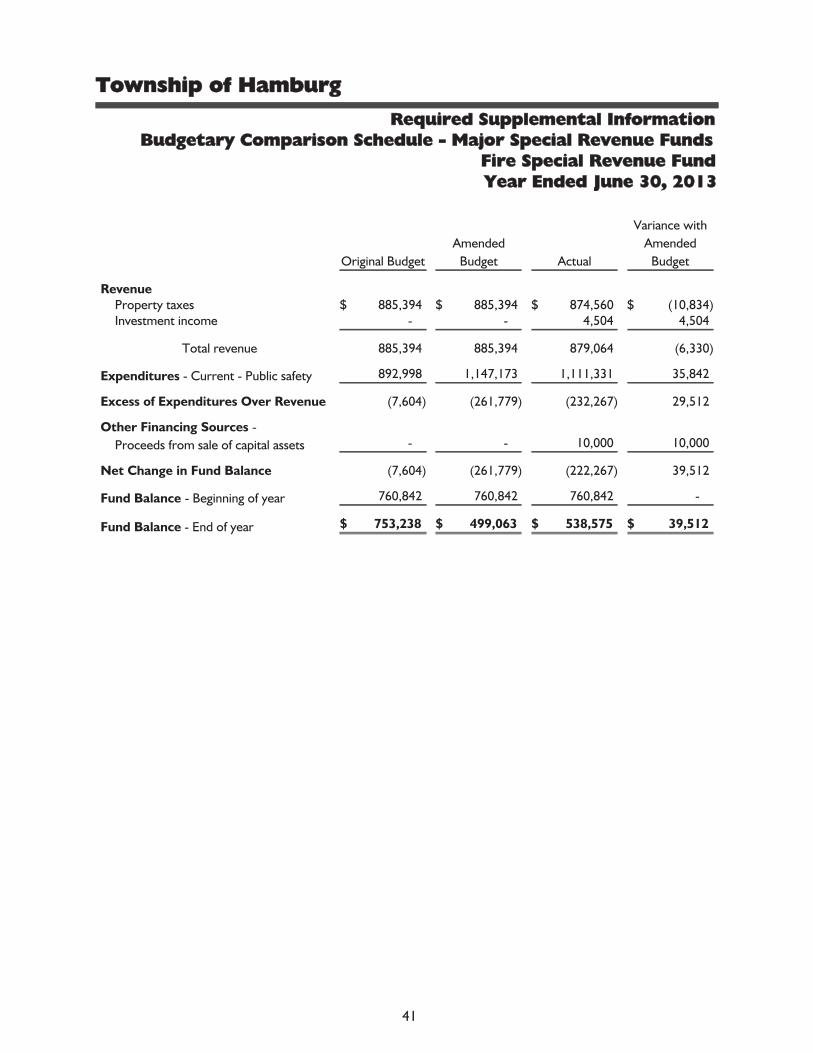

Budgetary Comparison Schedule - Major Special Revenue Funds 40-41

Note to Required Supplemental Information 42

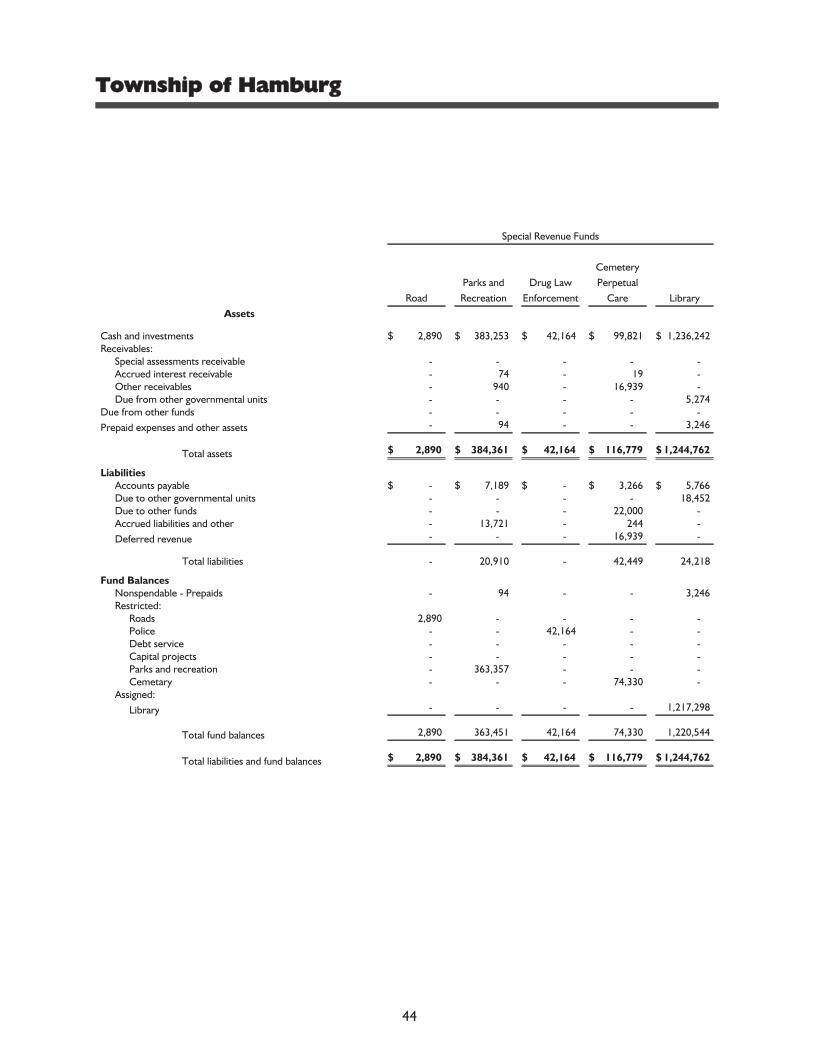

Other Supplemental Information 43

Nonmajor Governmental Funds:Combining Balance Sheet 44-45Combining Statement of Revenue, Expenditures, and Changes in Fund

Balances 46-47

Township of Hamburg Managements Discussion and Analysis

4

Our discussion and analysis of the Township of Hamburg’s (the “Township”) financial performance provides an overview of the Township of Hamburg’s financial activities for the fiscal year ended June 30, 2013. Please read it in conjunction with the Township’s financial statements.

Financial Highlights

As discussed in further detail in this discussion and analysis, the following represents the most significant financial highlights for the year ended June 30, 2013:

State-shared revenue, our largest revenue source other than property taxes, experienced an increase in fiscal year 2012-2013. The Township received approximately $22,000 more in 2013 than in 2012. In the fiscal years of 2008-2013, revenue sharing has steadily increased. Between 2001 and 2008, however, revenue sharing had decreased approximately 13 percent per year. The Township reacted to the decrease by cutting spending. Despite increases in the past five years, the Township remains proactive in monitoring spending to ensure that it adds to net position for funding during potential declines in the economy in the future.

Per GASB Statement No. 61, The Financial Reporting Entity: Omnibus, the Township restated its net position as of June 30, 2012 by reclassifying the Township’s library as a township fund and by excluding the Portage-Base Lake Area Water and Sewer Authority equity interest. Please see Note 13 for details.

Despite the GASB Statement No. 61 restatement of net position, net position for governmental activities still increased by $404,000 from fiscal year 2011-2012 to fiscal year 2012-2013.

Since fiscal year 2009-2010, the Township has been able to earmark over $545,000 for future maintenance, vehicle, equipment, and flood prevention expenditures.

Using this Annual Report

This annual report consists of four parts - the management’s discussion and analysis, the basic financial statements, required supplemental information, and other supplemental information that presents combining statements for nonmajor governmental funds. The basic financial statements include two kinds of statements that present different views of the Township. The first type of statements is the statement of net position and the statement of activities, which provide information about the activities of the Township as a whole and present a longer-term view of the Township’s finances. This longer-term view uses the accrual basis of accounting so that it can measure the cost of providing services during the current year and whether the taxpayers have funded the full cost of providing government services.

Township of Hamburg Managements Discussion and Analysis (Continued)

5

The second type of statements is the fund financial statements, which present a short-term view; they tell us how the taxpayers’ resources were spent during the year, as well as how much is available for future spending. Fund financial statements also report the Township’s operations in more detail than the government-wide financial statements by providing information about the Township’s most significant funds. The fiduciary fund statement provides financial information about activities for which the Township acts solely as a trustee or agent for the benefit of those outside of the government.

The Township as a Whole

The following table shows, in a condensed format, the current year’s net position and changes in net position compared to the prior two years (in thousands of dollars):

Governmental

Activities

Business-type

Activities Total

2013 2012 2013 2012 2013 2012

AssetsCurrent assets 7,389$ 7,518$ 750$ 1,010$ 8,139$ 8,528$ Capital assets 12,631 12,613 29,844 30,200 42,475 42,813 Noncurrent assets 1,974 2,001 9,295 10,608 11,269 12,609

Total assets 21,994 22,132 39,889 41,818 61,883 63,950

LiabilitiesCurrent liabilities 1,091 997 1,433 1,759 2,524 2,756 Long-term liabilities 5,023 5,659 10,889 12,561 15,912 18,220

Total liabilities 6,114 6,656 12,322 14,320 18,436 20,976

Net PositionNet investment in capital

assets 7,241 6,659 17,780 16,384 25,021 23,043 Restricted 3,091 4,389 9,206 10,567 12,297 14,956 Unrestricted 5,548 4,428 581 547 6,129 4,975

Total net position 15,880$ 15,476$ 27,567$ 27,498$ 43,447$ 42,974$

The Township’s combined net position increased by approximately 1.1 percent from a year ago - increasing to approximately $43,447,000. The governmental activities comprise approximately $15,880,000, up from $15,476,000, while the business-type activities, the Sewer Fund, make up approximately $27,567,000, an increase of 0.3 percent from a year ago.

Unrestricted net position, the part of net position that can be used to finance day-to-day operations, is approximately $5,548,000 for the governmental activities. Unrestricted net position for the business-type activities is approximately $581,000.

Township of Hamburg Managements Discussion and Analysis (Continued)

6

The following table shows the changes in net position during 2013 and 2012 (in thousands of dollars):

Governmental

Activities

Business-type

Activities Total

2013 2012 2013 2012 2013 2012

RevenueProgram revenue:

Charges for services 774$ 750$ 2,026$ 2,017$ 2,800$ 2,767$ Operating grants and contributions 114 56 - - 114 56 Capital grants and contributions 131 379 508 311 639 690

General revenue:Property taxes 3,886 3,900 - - 3,886 3,900 State-shared revenue 1,551 1,529 - - 1,551 1,529 Unrestricted investment earnings 22 33 225 327 247 360 Franchise fees 314 293 - - 314 293 Other income 35 17 - - 35 17 Gain on sale of capital assets 12 - - - 12 -

Total revenue 6,839 6,957 2,759 2,655 9,598 9,612

Program ExpensesGeneral government 2,395 2,153 - - 2,395 2,153 Public safety 3,288 3,010 - - 3,288 3,010 Public works 256 247 - - 256 247 Recreation and culture 306 356 - - 306 356 Interest on long-term debt 190 281 - - 190 281 Sewer - - 2,690 2,906 2,690 2,906

Total program expenses 6,435 6,047 2,690 2,906 9,125 8,953

Change in Net Position 404$ 910$ 69$ (251)$ 473$ 659$

Governmental Activities

The Township’s total governmental activities revenue totaled approximately $6.8 million, with state revenue sharing representing $1.6 million or 23 percent. Although the economy has improved enough to increase revenue sharing for 2013, the State’s possible future financial situation will continue to be monitored during the upcoming year.

Expenses for the fiscal year were approximately $6,400,000. The Township has closely monitored its spending in all areas and had revenue come in over budget in areas of state revenue sharing and cable franchise fees. There was a net increase in net position of approximately $404,000 from 2012 to 2013.

Township of Hamburg Managements Discussion and Analysis (Continued)

7

Business-type Activities

The Township’s business-type activities consist of the Sewer Fund. We provide sewage treatment through a Township-owned and operated sewage treatment plant, as well as through the use of a plant owned and operated by a neighboring community.

The Township Funds

Our analysis of the Township’s major funds follows the government-wide financial statements. The fund financial statements provide detail information about the most significant funds, not the Township as a whole. The Township board creates funds to help manage money for specific purposes as well as to show accountability for certain activities, such as special property tax millages. The Township’s major funds for 2012-2013 include the General Fund, the Police Special Revenue Fund, the Fire Special Revenue Fund, and the Water System Debt Service Fund.

The General Fund pays for most of the Township's governmental services. The most significant is police, which depended on the General Fund for $480,000 for the year ended June 30, 2013. Both the police and fire services are also supported by separate police and fire millages, which are recorded in the Police Special Revenue Fund and the Fire Special Revenue Fund.

General Fund Budgetary Highlights

Over the course of the year, the Township amended the budget to take into account events during the year. However, no significant changes to the budget were made.

Capital Asset and Debt Administration

At the end of fiscal year 2013, the Township had $42,475,000 invested in a broad range of capital assets, net of depreciation, including buildings, police and fire equipment, and sewer lines.

Economic Factors and Next Year’s Budgets and Rates

The Township’s budget for next year will need to be watched very closely once again, especially relating to the General Fund. Despite recent increases in revenue sharing as a result of increased state sales revenue, the economy will need to be monitored closely in order to determine if expenditures in the upcoming fiscal year need to be adjusted.

Contacting the Township’s Management

This financial report is intended to provide our citizens, taxpayers, customers, and investors with a general overview of the Township’s finances and to show the Township’s accountability for the money it receives. If you have questions about this report or need additional information, we welcome you to contact the Township clerk’s office at (810) 231-1000.

Independent Auditor's Report

To the Board of Trustees Township of Hamburg

Report on the Financial Statements

We have audited the accompanying financial statements of the governmental activities, thebusiness-type activities, each major fund, and the aggregate remaining fund information of theTownship of Hamburg (the "Township") as of and for the year ended June 30, 2013 and therelated notes to the financial statements, which collectively comprise the Township ofHamburg's basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statementsin accordance with accounting principles generally accepted in the United States of America; thisincludes the design, implementation, and maintenance of internal control relevant to thepreparation and fair presentation of financial statements that are free from materialmisstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. Wedid not audit the financial statements of the Library Fund which represents 13 percent, 16percent and 7 percent, respectively, of the assets, fund balance, and revenues of the totalgovernmental funds. Those financial statements were audited by other auditors, whose reporthas been furnished to us, and our opinion, insofar as it relates to the amounts included for theLibrary Fund, is based solely on the report of the other auditors. We conducted our audit inaccordance with auditing standards generally accepted in the United States of America. Thosestandards require that we plan and perform the audit to obtain reasonable assurance aboutwhether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts anddisclosures in the financial statements. The procedures selected depend on the auditor’sjudgment, including the assessment of the risks of material misstatement of the financialstatements, whether due to fraud or error. In making those risk assessments, the auditorconsiders internal control relevant to the entity’s preparation and fair presentation of thefinancial statements in order to design audit procedures that are appropriate in thecircumstances, but not for the purpose of expressing an opinion on the effectiveness of theentity’s internal control. Accordingly, we express no such opinion. An audit also includesevaluating the appropriateness of accounting policies used and the reasonableness of significantaccounting estimates made by management, as well as evaluating the overall presentation of thefinancial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide abasis for our audit opinions.

1

To the Board of Trustees Township of Hamburg

Opinion

In our opinion, based on our audit and the report of other auditors, the financial statementsreferred to above present fairly, in all material respects, the respectivefinancial position of thegovernmental activities, the business-type activities, each major fund, and the aggregateremaining fund information of the Township of Hamburg as of June 30, 2013 and therespectivechanges in its financial position and cash flows for the year then ended, in accordancewith accounting principles generally accepted in the United States of America.

Emphasis of Matter

As discussed in Note 13 to the basic financial statements, the 2012 basic financial statementshave been restated to reflect the lack of a defined equitable interest in joint ventures of thePortage Base Lakes Water Authority and to reflect the change in presentation of the HamburgTownship Library from a component unit to a governmental special revenue fund. Our opinionis not modified with respect to this matter.

Required Supplemental Information

Accounting principles generally accepted in the United States of America require that themanagement's discussion and analysis and the major fund budgetary comparison schedules bepresented to supplement the basic financial statements. Such information, although not a part ofthe basic financial statements, is required by the Governmental Accounting Standards Board,which considers it to be an essential part of financial reporting for placing the basic financialstatements in an appropriate operational, economic, or historical context. We have appliedcertain limited procedures to the required supplemental information in accordance with auditingstandards generally accepted in the United States of America, which consisted of inquiries ofmanagement about the methods of preparing the information and comparing the information forconsistency with management's responses to our inquiries, the basic financial statements, andother knowledge we obtained during our audit of the basic financial statements. We do notexpress an opinion or provide any assurance on the information because the limited proceduresdo not provide us with sufficient evidence to express an opinion or provide any assurance.

Other Information

Our audit was conducted for the purpose of forming an opinion on the financial statements thatcollectively comprise the Township of Hamburg's basic financial statements. The othersupplemental information, as identified in the table of contents, is presented for the purpose ofadditional analysis and is not a required part of the basic financial statements.

2

To the Board of Trustees Township of Hamburg

The other supplemental information is the responsibility of management and was derived fromand relates directly to the underlying accounting and other records used to prepare the basicfinancial statements. Such information has been subjected to the auditing procedures applied inthe audit of the basic financial statements and certain additional procedures, including comparingand reconciling such information directly to the underlying accounting and other records used toprepare the basic financial statements or to the basic financial statements themselves, and otheradditional procedures in accordance with auditing standards generally accepted in the UnitedStates of America. In our opinion, the other supplemental information is fairly stated in allmaterial respects in relation to the basic financial statements as a whole.

November 14, 2013

3

Township of Hamburg

Statement of Net PositionJune 30, 2013

Primary GovernmentGovernmental

ActivitiesBusiness-type

Activities TotalAssets

Cash and cash equivalents $ 6,916,277 $ 39,454 $ 6,955,731Receivables:

Customers and other 95,303 577,096 672,399Accrued interest receivable 1,268 - 1,268Restricted assets - 1,195,672 1,195,672Other receivables 17,930 - 17,930Due from other governmental units 325,006 - 325,006Special assessments receivable 1,510,680 4,395,452 5,906,132Allowance for doubtful accounts (3,635) - (3,635)

Internal balances (14,649) 14,649 -Inventory - 113,635 113,635Prepaid expenses and other assets 51,249 - 51,249Restricted assets 423,277 3,615,872 4,039,149Other current assets - 5,433 5,433Capital assets:

Assets not subject to depreciation 1,449,436 1,542,531 2,991,967Assets subject to depreciation 11,182,038 28,301,580 39,483,618

Unamortized bond issuance costs 39,871 88,245 128,116

Total assets 21,994,051 39,889,619 61,883,670

LiabilitiesAccounts payable 131,029 77,055 208,084Due to other governmental units 18,452 - 18,452Accrued liabilities and other 269,789 139,472 409,261Noncurrent liabilities:

Due within one year - Current portion of long-termdebt 671,938 1,216,550 1,888,488

Due in more than one year: Compensated absences - > 1 yr 304,064 20,852 324,916Long-term debt 4,718,611 10,868,503 15,587,114

Total liabilities 6,113,883 12,322,432 18,436,315

Net PositionNet investment in capital assets 7,240,925 17,779,910 25,020,835Restricted for:

Roads 2,890 - 2,890Debt service 1,418,733 - 1,418,733Capital projects 634,363 9,206,996 9,841,359Police and fire operations 580,759 - 580,759Parks and recreation 363,451 - 363,451Cemetery expenditures 91,269 - 91,269

Unrestricted 5,547,778 580,281 6,128,059

Total net position $ 15,880,168 $ 27,567,187 $ 43,447,355

The Notes to Financial Statements are anIntegral Part of this Statement. 8

Township of Hamburg

Program Revenue

ExpensesCharges for

Services

OperatingGrants and

Contributions

Capital Grantsand

Contributions

Functions/Programs

Primary government: Governmental activities:

General government $ 2,394,655 $ 561,938 $ 111,268 $ -Public safety 3,287,678 69,856 2,822 72,152Public works 255,927 113,101 - 59,315Recreation and culture 306,318 28,689 - -Interest on long-term debt 190,835 - - -

Total governmentalactivities 6,435,413 773,584 114,090 131,467

Business-type activities - Sewagedisposal 2,690,098 2,025,893 - 507,646

Total primary government $ 9,125,511 $ 2,799,477 $ 114,090 $ 639,113

General revenue:Property taxes State aid to libraries State-shared revenue Investment income Cable franchise fees Other income Gain on sale of fixed assets

Total general revenue

Change in Net Position

Net Position - Beginning of year (as restated) (Note 13)

Net Position - End of year

The Notes to Financial Statements are anIntegral Part of this Statement. 9

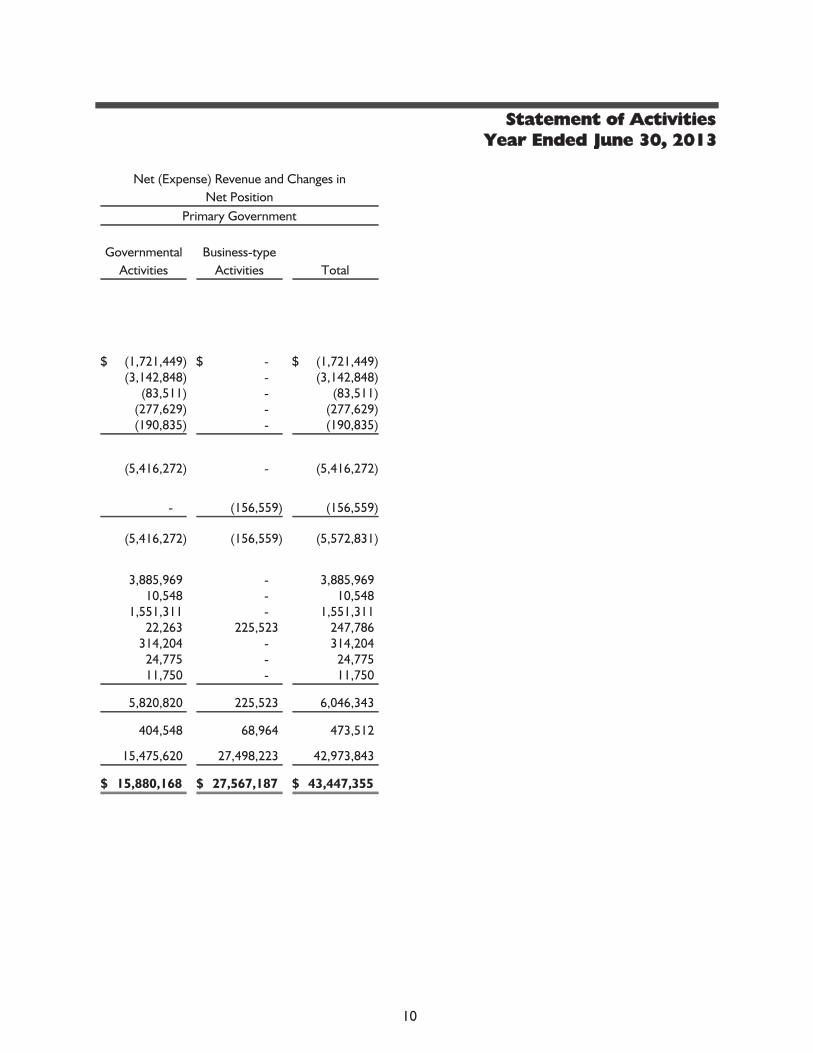

Statement of ActivitiesYear Ended June 30, 2013

Net (Expense) Revenue and Changes inNet Position

Primary Government

GovernmentalActivities

Business-typeActivities Total

$ (1,721,449) $ - $ (1,721,449)(3,142,848) - (3,142,848)

(83,511) - (83,511)(277,629) - (277,629)(190,835) - (190,835)

(5,416,272) - (5,416,272)

- (156,559) (156,559)

(5,416,272) (156,559) (5,572,831)

3,885,969 - 3,885,96910,548 - 10,548

1,551,311 - 1,551,31122,263 225,523 247,786

314,204 - 314,20424,775 - 24,77511,750 - 11,750

5,820,820 225,523 6,046,343

404,548 68,964 473,512

15,475,620 27,498,223 42,973,843

$ 15,880,168 $ 27,567,187 $ 43,447,355

10

Township of Hamburg

Governmental FundsBalance SheetJune 30, 2013

General FundPolice SpecialRevenue Fund

Fire SpecialRevenue Fund

Water SystemDebt Service

Fund

OtherNonmajor

GovernmentalFunds Total

Assets

Cash and cash equivalents (Note 2) $ 3,244,612 $ 791,815 $ 640,557 $ 1,090 $ 2,238,203 $ 6,916,277Receivables:

Special assessments receivable - - - 981,945 528,735 1,510,680Customers and other 90,673 995 3,635 - - 95,303Accrued interest receivable 756 153 122 81 156 1,268Other receivables - - - - 17,930 17,930Due from other governmental units 263,035 - - 56,697 5,274 325,006Allowance for doubtful accounts - - (3,635) - - (3,635)

Due from other funds (Note 4) 22,000 - - - 18,208 40,208Advances to other funds (Note 4) 359,841 - - - - 359,841Prepaid expenses and other assets 15,741 20,320 11,848 - 3,340 51,249Cash restricted for capital and debt - - - 423,277 - 423,277

Total assets $ 3,996,658 $ 813,283 $ 652,527 $ 1,463,090 $ 2,811,846 $ 9,737,404

Liabilities and Fund Balances

LiabilitiesAccounts payable $ 17,528 $ 20,280 $ 76,915 $ - $ 16,306 $ 131,029Due to other governmental units - - - - 18,452 18,452Due to other funds (Note 4) 18,208 - - - 36,649 54,857Advances from other funds (Note 4) - - - 359,841 - 359,841Accrued liabilities and other 115,185 47,293 37,037 - 15,610 215,125Deferred revenue (Note 3) - - - 981,945 545,674 1,527,619

Total liabilities 150,921 67,573 113,952 1,341,786 632,691 2,306,923Fund Balances

Nonspendable: Prepaids 15,741 20,320 11,848 - 3,340 51,249Long-term receivable 359,841 - - - - 359,841

Restricted (Note 1):Roads - - - - 2,890 2,890Police - (72) - - 42,164 42,092Fire - - 526,727 - - 526,727Debt service - - - 121,304 177,531 298,835Capital projects - - - - 298,245 298,245Parks and recreation - - - - 363,357 363,357Future cemetary expenditures - - - - 74,330 74,330

Committed: Township building maintenance 86,200 - - - - 86,200Equipment 82,500 - - - - 82,500Vehicles 26,000 - - - - 26,000Flood prevention 19,000 - - - - 19,000

Assigned: Library - - - - 1,217,298 1,217,298Police - 725,462 - - - 725,462

Unassigned 3,256,455 - - - - 3,256,455

Total fund balances 3,845,737 745,710 538,575 121,304 2,179,155 7,430,481

Total liabilities and fundbalances $ 3,996,658 $ 813,283 $ 652,527 $ 1,463,090 $ 2,811,846 $ 9,737,404

The Notes to Financial Statements are anIntegral Part of this Statement. 11

Township of Hamburg

Governmental FundsReconciliation of the Balance Sheet to the Statement

of Net PositionYear Ended June 30, 2013

Fund Balance Reported in Governmental Funds $ 7,430,481

Amounts reported for governmental activities in the statementof net position are different because:

Capital assets used in governmental activities are not financialresources and are not reported in the funds 12,631,474

Unamortized bond issuance costs do not represent financialresources and are not reported in the funds 39,871

Special assessment receivables are expected to be collected overseveral years and are not available to pay for current yearexpenditures 1,527,619

Bonds payable and capital lease obligations are not due and payablein the current period and are not reported in the funds (5,390,549)

Accrued interest is not due and payable in the current period and isnot reported in the funds (54,664)

Employee compensated absences are payable over a long period ofyears and do not represent a claim on current financial resources;therefore, they are not reported as fund liabilities (304,064)

Net Position of Governmental Activities $ 15,880,168

The Notes to Financial Statements are anIntegral Part of this Statement. 12

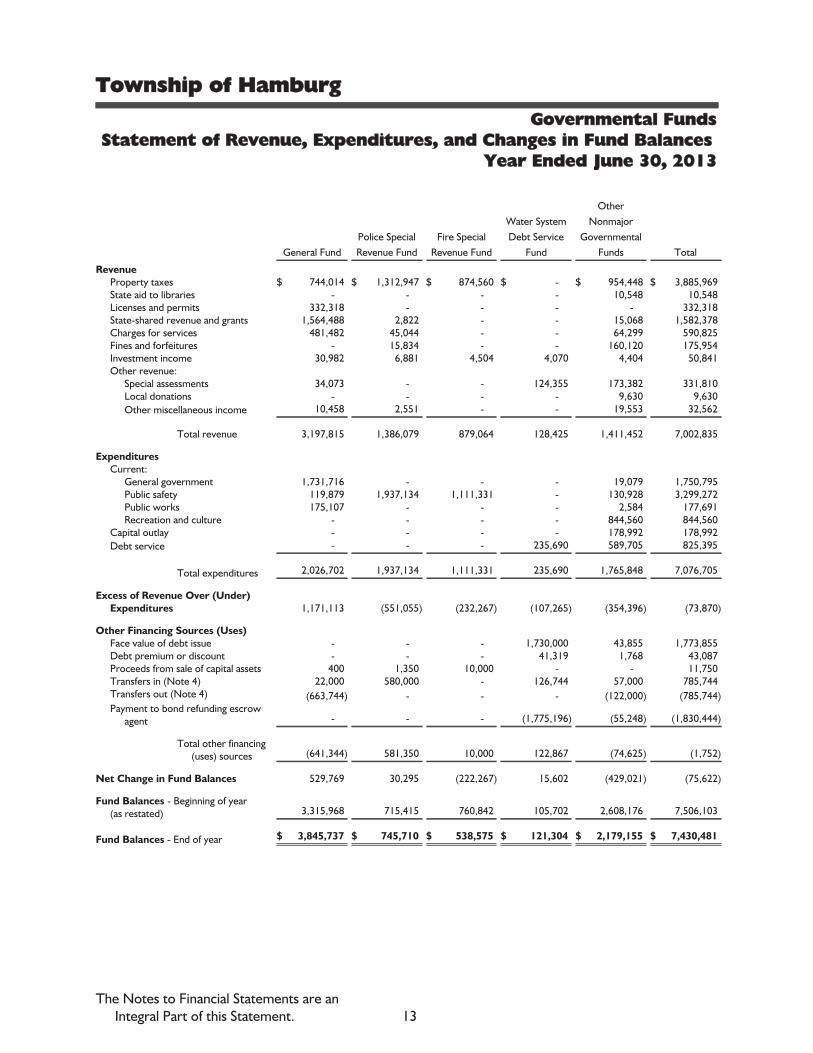

Township of Hamburg

Governmental FundsStatement of Revenue, Expenditures, and Changes in Fund Balances

Year Ended June 30, 2013

General FundPolice SpecialRevenue Fund

Fire SpecialRevenue Fund

Water SystemDebt Service

Fund

OtherNonmajor

GovernmentalFunds Total

RevenueProperty taxes $ 744,014 $ 1,312,947 $ 874,560 $ - $ 954,448 $ 3,885,969State aid to libraries - - - - 10,548 10,548Licenses and permits 332,318 - - - - 332,318State-shared revenue and grants 1,564,488 2,822 - - 15,068 1,582,378Charges for services 481,482 45,044 - - 64,299 590,825Fines and forfeitures - 15,834 - - 160,120 175,954Investment income 30,982 6,881 4,504 4,070 4,404 50,841Other revenue:

Special assessments 34,073 - - 124,355 173,382 331,810Local donations - - - - 9,630 9,630Other miscellaneous income 10,458 2,551 - - 19,553 32,562

Total revenue 3,197,815 1,386,079 879,064 128,425 1,411,452 7,002,835

ExpendituresCurrent:

General government 1,731,716 - - - 19,079 1,750,795Public safety 119,879 1,937,134 1,111,331 - 130,928 3,299,272Public works 175,107 - - - 2,584 177,691Recreation and culture - - - - 844,560 844,560

Capital outlay - - - - 178,992 178,992Debt service - - - 235,690 589,705 825,395

Total expenditures 2,026,702 1,937,134 1,111,331 235,690 1,765,848 7,076,705

Excess of Revenue Over (Under)Expenditures 1,171,113 (551,055) (232,267) (107,265) (354,396) (73,870)

Other Financing Sources (Uses) Face value of debt issue - - - 1,730,000 43,855 1,773,855Debt premium or discount - - - 41,319 1,768 43,087Proceeds from sale of capital assets 400 1,350 10,000 - - 11,750Transfers in (Note 4) 22,000 580,000 - 126,744 57,000 785,744Transfers out (Note 4) (663,744) - - - (122,000) (785,744)Payment to bond refunding escrow

agent - - - (1,775,196) (55,248) (1,830,444)

Total other financing(uses) sources (641,344) 581,350 10,000 122,867 (74,625) (1,752)

Net Change in Fund Balances 529,769 30,295 (222,267) 15,602 (429,021) (75,622)

Fund Balances - Beginning of year(as restated) 3,315,968 715,415 760,842 105,702 2,608,176 7,506,103

Fund Balances - End of year $ 3,845,737 $ 745,710 $ 538,575 $ 121,304 $ 2,179,155 $ 7,430,481

The Notes to Financial Statements are anIntegral Part of this Statement. 13

Township of Hamburg

Governmental FundsReconciliation of the Statement of Revenue, Expenditures,

and Changes in Fund Balances of Governmental Fundsto the Statement of Activities

Year Ended June 30, 2013

Net Change in Fund Balances - Total Governmental Funds $ (75,622)

Amounts reported for governmental activities in the statementof activities are different because:

Governmental funds report capital outlays as expenditures;however, in the statement of activities, these costs are allocatedover their estimated useful lives as depreciation:

Capital outlay 742,338Depreciation expense (723,810)

Special assessment revenue is recorded in the statement of activitieswhen earned; it is not reported in the funds until collected orcollectible within 60 days of year end (159,394)

Bond proceeds provide financial resources to governmental funds,but issuing debt increases long-term liabilities in the statement ofnet position (1,817,561)

Repayment of bond principal is an expenditure in the governmentalfunds, but not in the statement of activities (where it reduceslong-term debt) 551,273

Change in accrued interest payable and other 14,765

Payment to bond refunding escrow agent is an expenditure in thegovernmental funds, but not in the statement of activities 1,869,378

Decrease in accumulated employee sick and vacation pay and othersimilar expenses reported in the statement of activities do notrequire the use of current resources and therefore are notreported in the fund statements until they come due for payment 3,181

Change in Net Position of Governmental Activities $ 404,548

The Notes to Financial Statements are anIntegral Part of this Statement. 14

Township of Hamburg

Proprietary FundStatement of Net Position

June 30, 2013

Sewer FundAssets

Current assets:Cash and investments $ 39,454Receivables - Customers and other 577,096Due from other funds (Note 4) 14,649Inventory 113,635Other assets 5,433

Total current assets 750,267

Noncurrent assets:Cash restricted for capital and debt (Note 11) 3,615,872Assets restricted for capital and debt (Note 11) 4,395,452Restricted assets (Note 11) 1,195,672Capital assets (Note 5):

Assets not subject to depreciation 1,542,531Assets subject to depreciation 28,301,580

Unamortized bond issuance costs 88,245

Total noncurrent assets 39,139,352

Total assets 39,889,619

LiabilitiesCurrent liabilities:

Accounts payable 77,055Accrued liabilities and other 139,472Current portion of long-term debt (Note 6) 1,216,550

Total current liabilities 1,433,077

Noncurrent liabilities:Compensated absences - > 1 yr 20,852Long-term debt (Note 6) 10,868,503

Total noncurrent liabilities 10,889,355

Total liabilities 12,322,432

Net PositionNet investment in capital assets 17,759,058Restricted - Capital projects 9,206,996Unrestricted 601,133

Total net position $ 27,567,187

The Notes to Financial Statements are anIntegral Part of this Statement. 15

Township of Hamburg

Proprietary FundStatement of Revenue, Expenses, and Changes in Net Position

Year Ended June 30, 2013

Sewer FundOperating Revenue

Sewage disposal charges $ 1,239,678Debt service charges and other 786,215

Total operating revenue 2,025,893

Operating ExpensesOperation and maintenance 1,370,905Depreciation 918,019

Total operating expenses 2,288,924

Operating Loss (263,031)

Nonoperating Revenue (Expense)Investment income 225,523Interest expense (401,174)

Total nonoperating expenses (175,651)

Loss - Before contributions (438,682)

Capital Contributions - Tap fees 507,646

Change in Net Position 68,964

Net Position - Beginning of year 27,498,223

Net Position - End of year $ 27,567,187

The Notes to Financial Statements are anIntegral Part of this Statement. 16

Township of Hamburg

Proprietary FundStatement of Cash Flows

Year Ended June 30, 2013

Sewer Fund

Cash Flows from Operating ActivitiesReceipts from customers $ 1,222,955Payments to suppliers (604,435)Payments to employees (558,705)Internal activity - Payments to other funds (159,800)Other receipts 808,029

Net cash provided by operating activities 708,044

Cash Flows from Capital and Related Financing ActivitiesReceipt of capital grants 418,040Collection of principal and interest on customer assessments 989,764Purchase of capital assets (789,107)Principal and interest paid on capital debt (2,179,211)Collection from developers for the construction of new sewer lines 89,605

Net cash used in capital and related financing activities (1,470,909)

Cash Flows from Investing Activities - Interest received on investments 12,601

Net Decrease in Cash and Cash Equivalents (750,264)

Cash and Cash Equivalents - Beginning of year 5,601,262

Cash and Cash Equivalents - End of year $ 4,850,998

Balance Sheet Classification of Cash and Cash EquivalentsCash and investments $ 39,454Restricted cash and cash equivalents resulting from bond sale 1,195,672Segregated bank deposits and investments for future capital investments 1,432,315Segregated bank deposits and investments resulting from special assessments 2,183,557

Total cash and cash equivalents $ 4,850,998

Reconciliation of Operating Loss to Net Cash from Operating ActivitiesOperating loss $ (263,031)Adjustments to reconcile operating loss to net cash from operating activities:

Depreciation and amortization 926,538Changes in assets and liabilities:

Receivables 4,119Prepaid and other assets 667Accounts payable 36,880Due to/from other funds 200Accrued and other liabilities 2,671

Net cash provided by operating activities $ 708,044

The Sewer Fund refunded bonds in the current year. As a result, there was a $2,551,145 noncash transactionduring the year ended June 30, 2013.

The Notes to Financial Statements are anIntegral Part of this Statement. 17

Township of Hamburg

Fiduciary FundsStatement of Fiduciary Net Position

June 30, 2013

Agency Funds

Assets - Cash and cash equivalents $ 72,297

LiabilitiesDue to other governmental units $ 1,592Performance bonds 65,211Other 5,494

Total liabilities $ 72,297

The Notes to Financial Statements are anIntegral Part of this Statement. 18

Township of Hamburg

Notes to Financial StatementsJune 30, 2013

Note 1 - Nature of Business and Significant Accounting Policies

The accounting policies of the Township of Hamburg (the "Township") conform toaccounting principles generally accepted in the United States of America (GAAP) asapplicable to governmental units. The following is a summary of the significantaccounting policies used by the Township of Hamburg:

Reporting Entity

The Township of Hamburg is governed by an elected seven-member board of trustees.As required by accounting principles generally accepted in the United States of America,these financial statements present the Township of Hamburg.

Government-wide and Fund Financial Statements

The government-wide financial statements (i.e., the statement of net position and thestatement of activities) report information on all of the nonfiduciary activities of theprimary government and its component units. For the most part, the effect of interfundactivity has been removed from these statements. Governmental activities, normallysupported by taxes and intergovernmental revenues, are reported separately frombusiness-type activities, which rely to a significant extent on fees and charges forsupport. Likewise, the primary government is reported separately from certain legallyseparate component units for which the primary government is financially accountable.

The statement of activities demonstrates the degree to which the direct expenses of agiven function or segment are offset by program revenues. Direct expenses are thosethat are clearly identifiable with a specific function or segment. Program revenuesinclude (1) charges to customers or applicants who purchase, use, or directly benefitfrom goods, services, or privileges provided by a given function or segment and(2) grants and contributions that are restricted to meeting the operational or capitalrequirements of a particular function or segment. Taxes and other items not properlyincluded among program revenues are reported instead as general revenue.

Separate financial statements are provided for governmental funds, proprietary funds,and fiduciary funds, even though the latter are excluded from the government-widefinancial statements. Major individual governmental funds and major individual enterprisefunds are reported as separate columns in the fund financial statements.

19

Township of Hamburg

Notes to Financial StatementsJune 30, 2013

Note 1 - Nature of Business and Significant Accounting Policies(Continued)

Measurement Focus, Basis of Accounting, and Financial StatementPresentation

The government-wide financial statements are reported using the economic resourcesmeasurement focus and the accrual basis of accounting, as are the proprietary fund,fiduciary fund, and component unit financial statements. Revenue is recorded whenearned and expenses are recorded when a liability is incurred, regardless of the timing ofrelated cash flows. Property taxes are recognized as revenue in the year for which theyare levied. Grants and similar items are recognized as revenue as soon as all eligibilityrequirements imposed by the provider have been met.

Governmental fund financial statements are reported using the current financialresources measurement focus and the modified accrual basis of accounting. Revenue isrecognized as soon as it is both measurable and available. Revenue is considered to beavailable if it is collected within the current period or soon enough thereafter to payliabilities of the current period. For this purpose, the Township considers revenues tobe available if they are collected within 60 days of the end of the current fiscal period,including state-shared revenue. Conversely, special assessments and federal grantreimbursements will be collected after the period of availability; receivables have beenrecorded for these, along with a "deferred revenue" liability.

Expenditures generally are recorded when a liability is incurred, as under accrualaccounting. However, debt service expenditures, expenditures relating to compensatedabsences, and claims and judgments are recorded only when payment is due.

The Township reports the following major governmental funds:

The General Fund is the Township's primary operating fund. It accounts for all financialresources of the general government, except those required to be accounted for inanother fund.

The Police and Fire Special Revenue Funds are full-service departments whose mainsource of revenue comes from voter-approved millages on all real property. The fundsprovide safety, fire suppression, fire prevention, and emergency medical services in theTownship.

The Water System Debt Service Fund accounts for debt service payments related to thewater system. The main source of revenue is collection of special assessments. TheGeneral Fund makes advances to this fund to meet current obligations.

The Township reports the following major proprietary fund:

The Sewer Fund accounts for the results of operations that provide sewer services tocitizens and is financed primarily by a user charge for the provision of those services.

20

Township of Hamburg

Notes to Financial StatementsJune 30, 2013

Note 1 - Nature of Business and Significant Accounting Policies(Continued)

Additionally, the Township reports an agency fund. The agency fund accounts for assetsheld by the Township in a trustee capacity. Agency funds are custodial in nature (assetsequal liabilities) and do not involve the measurement of results of operations.

As a general rule, the effect of interfund activity has been eliminated from thegovernment-wide financial statements. Exceptions to this general rule are chargesbetween the Township's water and sewer function and various other functions of theTownship. Eliminations of these charges would distort the direct costs and programrevenues reported for the various functions concerned.

Amounts reported as program revenue include (1) charges to customers or applicantsfor goods, services, or privileges provided; (2) operating grants and contributions; and(3) capital grants and contributions, including special assessments. Internally dedicatedresources are reported as general revenue rather than as program revenue. Likewise,general revenue includes all taxes.

When an expense is incurred for purposes for which both restricted and unrestrictednet position or fund balance are available, the Township's policy is to first applyrestricted resources. When an expense is incurred for purposes for which amounts inany of the unrestricted fund balance classifications could be used, it is the Township'spolicy to spend funds in this order: committed, assigned, and unassigned.

Proprietary funds distinguish operating revenue and expenses from nonoperating items.Operating revenue and expenses generally result from providing services in connectionwith a proprietary fund's principal ongoing operations. The principal operating revenueof the proprietary Sewer Fund relates to charges to customers for sewer services. TheSewer Fund also recognizes the portion of tap fees intended to recover current costs(e.g., labor and materials to hook up new customers) as operating revenue. The portionintended to recover the cost of the infrastructure is recognized as nonoperatingrevenue. Operating expenses for the proprietary fund include the cost of services,administrative expenses, and depreciation on capital assets. All revenue and expensesnot meeting this definition are reported as nonoperating revenue and expenses.

Property Tax Revenue

The taxable valuation of the Township totaled $882 million. Property taxes are leviedon each December 1 on the taxable valuation of property as of the precedingDecember 31. Taxes are considered delinquent on March 1 of the following year, atwhich time penalties and interest are assessed.

21

Township of Hamburg

Notes to Financial StatementsJune 30, 2013

Note 1 - Nature of Business and Significant Accounting Policies(Continued)

The Township's approximate property tax levy for the year ended June 30, 2013 was asfollows:

Millage Rate Levy

Operating 0.8442 $ 745,000Police 1.5000 1,323,000Fire 1.0000 882,000Fire debt 0.3932 347,000Library 0.4418 390,000Parks and recreation 0.2500 220,000

Total 4.4292 $ 3,907,000

Assets, Liabilities, and Net Position or Equity

Bank Deposits and Investments - Cash and cash equivalents include cash on hand,demand deposits, and short-term investments with a maturity of three months or lesswhen acquired.

Receivables and Payables - In general, outstanding balances between funds arereported as "due to/from other funds." Activity between funds that are representativeof lending/borrowing arrangements outstanding at the end of the fiscal year is referredto as "advances to/from other funds." Any residual balances outstanding between thegovernmental activities and the business-type activities are reported in the government-wide financial statements as "internal balances."

All trade and property tax receivables are shown as net of allowance for uncollectibleamounts.

Inventories and Prepaid Items - Inventory in the enterprise funds is valued at cost ona first-in, first-out basis, which approximates market value.

Restricted Assets - Restricted assets in the Sewer Fund consist of cash and cashequivalents restricted for debt payments and capital improvements.

Capital Assets - Capital assets, which include property, plant, equipment, intangibles,and infrastructure, are reported in the applicable governmental or business-typeactivities column in the government-wide financial statements. Capital assets aredefined by the Township as assets with an initial individual cost of more than $2,500 andan estimated useful life in excess of one year for noncomputer-related assets and $500for computer equipment. Such assets are recorded at historical cost or estimatedhistorical cost if purchased or constructed. Donated capital assets are recorded atestimated fair market value at the date of donation.

22

Township of Hamburg

Notes to Financial StatementsJune 30, 2013

Note 1 - Nature of Business and Significant Accounting Policies(Continued)

Infrastructure, intangibles, buildings, equipment, and vehicles are depreciated using thestraight-line method over the following useful lives:

Governmental activities: Buildings and building improvements 5-50 years Machinery and tools 3-15 years Vehicles, boats, and related equipment 3-7 years Office furnishings and equipment 3-10 years Library collection materials 10 years Leasehold improvements 50 yearsBusiness-type activities - Utility system 3 to 50 years

Compensated Absences - It is the Township's policy to permit employees toaccumulate earned but unused sick and vacation pay benefits. All vacation pay isaccrued when incurred in the government-wide, proprietary, and fiduciary fund financialstatements. A liability for these amounts is reported in governmental funds only foremployee terminations as of year end.

Long-term Obligations - In the government-wide financial statements and theproprietary fund types in the fund financial statements, long-term debt and other long-term obligations are reported as liabilities in the applicable governmental activities,business-type activities, or proprietary fund-type statement of net position. Bondpremiums and discounts, as well as issuance costs, are deferred and amortized over thelife of the bonds using the effective interest method. Bonds payable are reported net ofthe applicable bond premium or discount. Bond issuance costs are reported as deferredcharges and amortized over the term of the related debt. In the fund financialstatements, governmental fund types recognize bond premiums and discounts, as well asbond issuance costs during the current period. The face amount of debt issued isreported as other financing sources. Premiums received on debt issuances are reportedas other financing sources while discounts are reported as other financing uses. Issuancecosts are reported as debt service expenditures.

Fund Equity - In the fund financial statements, governmental funds report the followingcomponents of fund balance:

Nonspendable: Amounts that are not in spendable form or are legally orcontractually required to be maintained intact

Restricted: Amounts that are legally restricted by outside parties, constitutionalprovisions, or enabling legislation for use for a specific purpose

23

Township of Hamburg

Notes to Financial StatementsJune 30, 2013

Note 1 - Nature of Business and Significant Accounting Policies(Continued)

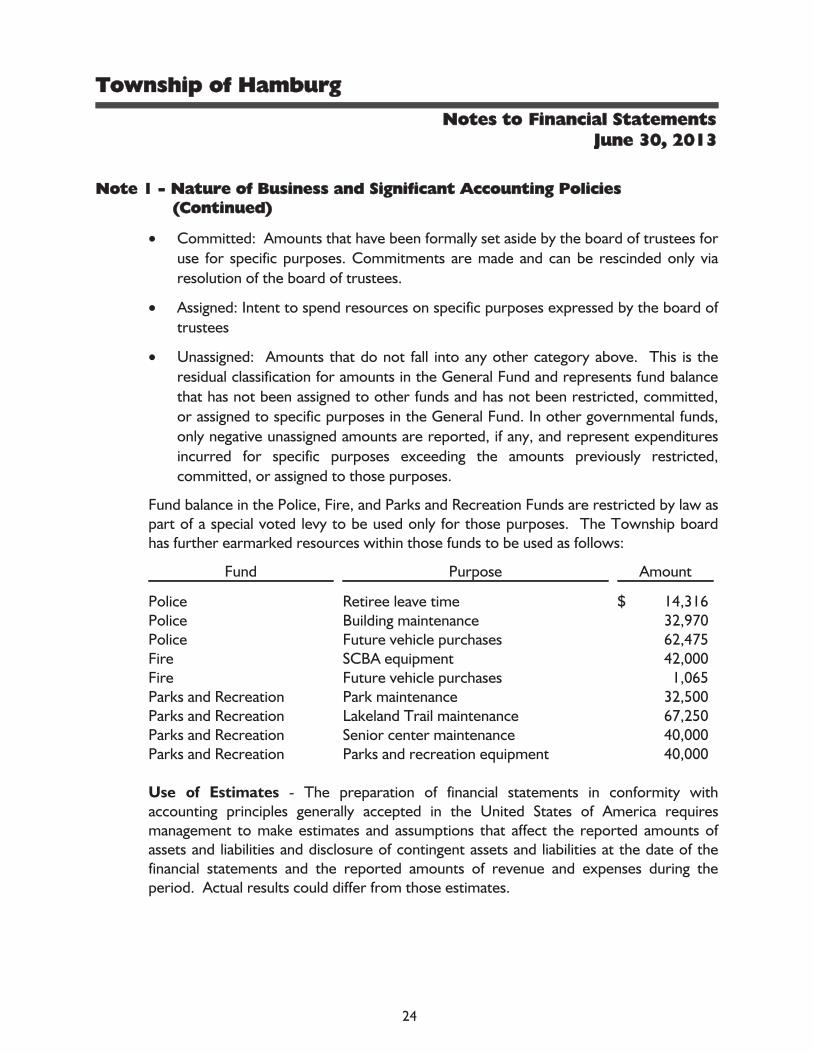

Committed: Amounts that have been formally set aside by the board of trustees foruse for specific purposes. Commitments are made and can be rescinded only viaresolution of the board of trustees.

Assigned: Intent to spend resources on specific purposes expressed by the board oftrustees

Unassigned: Amounts that do not fall into any other category above. This is theresidual classification for amounts in the General Fund and represents fund balancethat has not been assigned to other funds and has not been restricted, committed,or assigned to specific purposes in the General Fund. In other governmental funds,only negative unassigned amounts are reported, if any, and represent expendituresincurred for specific purposes exceeding the amounts previously restricted,committed, or assigned to those purposes.

Fund balance in the Police, Fire, and Parks and Recreation Funds are restricted by law aspart of a special voted levy to be used only for those purposes. The Township boardhas further earmarked resources within those funds to be used as follows:

Fund Purpose Amount

Police Retiree leave time $ 14,316Police Building maintenance 32,970Police Future vehicle purchases 62,475Fire SCBA equipment 42,000Fire Future vehicle purchases 1,065Parks and Recreation Park maintenance 32,500Parks and Recreation Lakeland Trail maintenance 67,250Parks and Recreation Senior center maintenance 40,000Parks and Recreation Parks and recreation equipment 40,000

Use of Estimates - The preparation of financial statements in conformity withaccounting principles generally accepted in the United States of America requiresmanagement to make estimates and assumptions that affect the reported amounts ofassets and liabilities and disclosure of contingent assets and liabilities at the date of thefinancial statements and the reported amounts of revenue and expenses during theperiod. Actual results could differ from those estimates.

24

Township of Hamburg

Notes to Financial StatementsJune 30, 2013

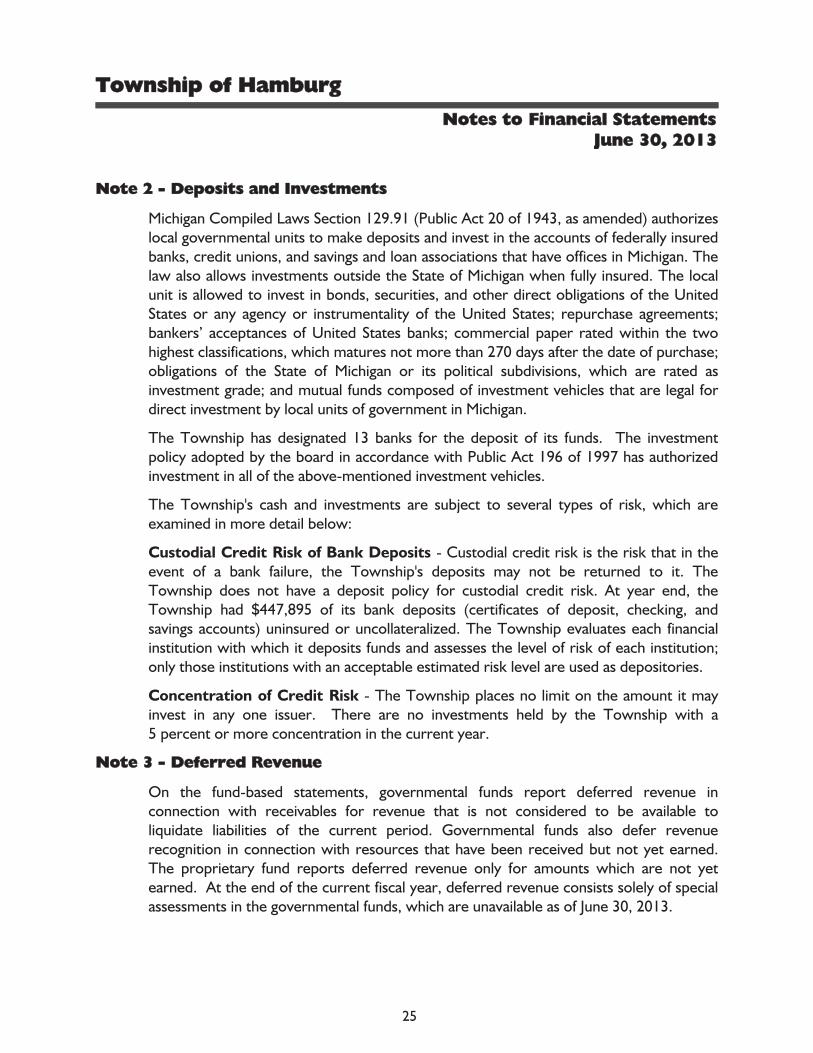

Note 2 - Deposits and Investments

Michigan Compiled Laws Section 129.91 (Public Act 20 of 1943, as amended) authorizeslocal governmental units to make deposits and invest in the accounts of federally insuredbanks, credit unions, and savings and loan associations that have offices in Michigan. Thelaw also allows investments outside the State of Michigan when fully insured. The localunit is allowed to invest in bonds, securities, and other direct obligations of the UnitedStates or any agency or instrumentality of the United States; repurchase agreements;bankers’ acceptances of United States banks; commercial paper rated within the twohighest classifications, which matures not more than 270 days after the date of purchase;obligations of the State of Michigan or its political subdivisions, which are rated asinvestment grade; and mutual funds composed of investment vehicles that are legal fordirect investment by local units of government in Michigan.

The Township has designated 13 banks for the deposit of its funds. The investmentpolicy adopted by the board in accordance with Public Act 196 of 1997 has authorizedinvestment in all of the above-mentioned investment vehicles.

The Township's cash and investments are subject to several types of risk, which areexamined in more detail below:

Custodial Credit Risk of Bank Deposits - Custodial credit risk is the risk that in theevent of a bank failure, the Township's deposits may not be returned to it. TheTownship does not have a deposit policy for custodial credit risk. At year end, theTownship had $447,895 of its bank deposits (certificates of deposit, checking, andsavings accounts) uninsured or uncollateralized. The Township evaluates each financialinstitution with which it deposits funds and assesses the level of risk of each institution;only those institutions with an acceptable estimated risk level are used as depositories.

Concentration of Credit Risk - The Township places no limit on the amount it mayinvest in any one issuer. There are no investments held by the Township with a5 percent or more concentration in the current year.

Note 3 - Deferred Revenue

On the fund-based statements, governmental funds report deferred revenue inconnection with receivables for revenue that is not considered to be available toliquidate liabilities of the current period. Governmental funds also defer revenuerecognition in connection with resources that have been received but not yet earned.The proprietary fund reports deferred revenue only for amounts which are not yetearned. At the end of the current fiscal year, deferred revenue consists solely of specialassessments in the governmental funds, which are unavailable as of June 30, 2013.

25

Township of Hamburg

Notes to Financial StatementsJune 30, 2013

Note 4 - Interfund Receivables, Payables, Advances, and Transfers

The composition of interfund balances is as follows:

Receivable Fund Payable Fund Amount

Due to/from Other Funds

Other nonmajor governmentalfunds General Fund $ 18,208

General Fund Other nonmajor governmentalfunds 22,000

Sewer Fund Other nonmajor governmentalfunds 14,649

Total $ 54,857

Receivable Fund Payable Fund Amount

Advances from/to Other Funds

General Fund Water System Debt ServiceFund $ 359,841

These balances result from the time lag between the dates that goods and services areprovided or reimbursable expenditures occur, transactions are recorded in theaccounting system, and payments between funds are made.

Interfund advances reported in the fund financial statements are related to the purchaseof the water system assets and payment of the related debt. The advance is due fromthe Water System Debt Service Fund to the General Fund, with payment due once thesystem generates revenue from the user charge for the provision of water services.

26

Township of Hamburg

Notes to Financial StatementsJune 30, 2013

Note 4 - Interfund Receivables, Payables, Advances, and Transfers(Continued)

Interfund transfers reported in the fund financial statements are comprised of thefollowing:

Receivable Fund Payable Fund Amount

General Fund Police Fund (2) $ 480,000Water System Debt Service

Fund (1) 126,744Other nonmajor governmental

funds (3)(4) 57,000

Total General Fund 663,744

Other nonmajor governmentalfunds Police Fund (2) 100,000

General Fund (1) 22,000

Total other nonmajorgovernmental funds 122,000

Total $ 785,744

(1) Transfers for debt service(2) Transfers for general operations(3) Transfers for capital projects(4) Transfers for parks and recreation

27

Township of Hamburg

Notes to Financial StatementsJune 30, 2013

Note 5 - Capital Assets

Capital asset activity of the Township's governmental and business-type activities was asfollows:

Governmental ActivitiesBalance

July 1, 2012 Reclassifications Additions DisposalsBalance

June 30, 2013

Capital assets not being depreciated:Land $ 1,449,436 $ - $ - $ - $ 1,449,436Construction in progress 167,632 (375,519) 207,887 - -

Subtotal 1,617,068 (375,519) 207,887 - 1,449,436

Capital assets being depreciated:Water well - Intangible rights 365,889 - - - 365,889Buildings and improvements 13,109,412 - 178,016 (6,741) 13,280,687Machinery and equipment 644,156 - 148,878 (3,951) 789,083Vehicles 1,570,757 375,519 77,999 (61,698) 1,962,577Office furnishings 1,192,040 - 80,816 (16,911) 1,255,945Library collection materials 847,535 - 29,049 - 876,584Land improvements 686,985 - 19,693 - 706,678

Subtotal 18,416,774 375,519 534,451 (89,301) 19,237,443

Accumulated depreciation:Water well rights 21,954 - 7,318 - 29,272Buildings and improvements 3,896,530 - 298,367 (6,741) 4,188,156Machinery and equipment 551,083 - 58,633 (3,951) 605,765Vehicles 1,142,358 - 202,654 (61,698) 1,283,314Office furnishings 933,914 - 109,281 (16,911) 1,026,284Library collection materials 791,472 - 33,817 - 825,289Land improvements 83,585 - 13,740 - 97,325

Subtotal 7,420,896 - 723,810 (89,301) 8,055,405

Net capital assets being depreciated 10,995,878 375,519 (189,359) - 11,182,038

Net capital assets $ 12,612,946 $ - $ 18,528 $ - $ 12,631,474

28

Township of Hamburg

Notes to Financial StatementsJune 30, 2013

Note 5 - Capital Assets (Continued)

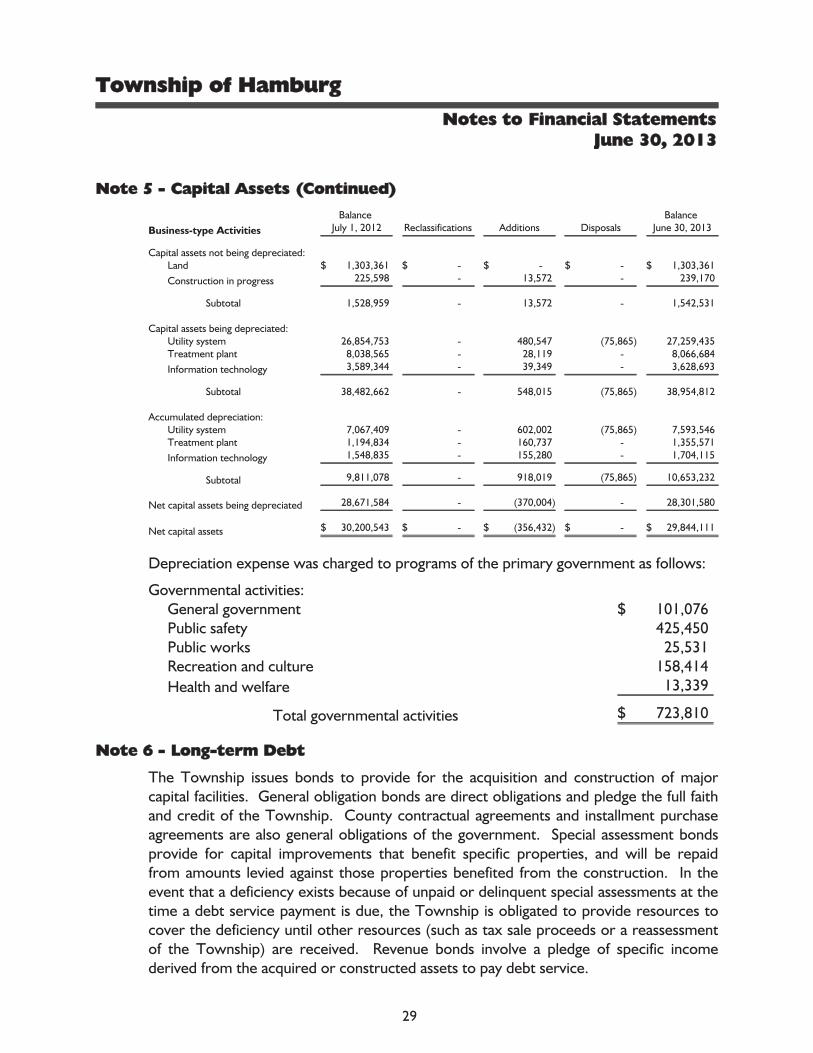

Business-type ActivitiesBalance

July 1, 2012 Reclassifications Additions DisposalsBalance

June 30, 2013

Capital assets not being depreciated:Land $ 1,303,361 $ - $ - $ - $ 1,303,361Construction in progress 225,598 - 13,572 - 239,170

Subtotal 1,528,959 - 13,572 - 1,542,531

Capital assets being depreciated:Utility system 26,854,753 - 480,547 (75,865) 27,259,435Treatment plant 8,038,565 - 28,119 - 8,066,684Information technology 3,589,344 - 39,349 - 3,628,693

Subtotal 38,482,662 - 548,015 (75,865) 38,954,812

Accumulated depreciation:Utility system 7,067,409 - 602,002 (75,865) 7,593,546Treatment plant 1,194,834 - 160,737 - 1,355,571Information technology 1,548,835 - 155,280 - 1,704,115

Subtotal 9,811,078 - 918,019 (75,865) 10,653,232

Net capital assets being depreciated 28,671,584 - (370,004) - 28,301,580

Net capital assets $ 30,200,543 $ - $ (356,432) $ - $ 29,844,111

Depreciation expense was charged to programs of the primary government as follows:

Governmental activities:General government $ 101,076Public safety 425,450Public works 25,531Recreation and culture 158,414Health and welfare 13,339

Total governmental activities $ 723,810

Note 6 - Long-term Debt

The Township issues bonds to provide for the acquisition and construction of majorcapital facilities. General obligation bonds are direct obligations and pledge the full faithand credit of the Township. County contractual agreements and installment purchaseagreements are also general obligations of the government. Special assessment bondsprovide for capital improvements that benefit specific properties, and will be repaidfrom amounts levied against those properties benefited from the construction. In theevent that a deficiency exists because of unpaid or delinquent special assessments at thetime a debt service payment is due, the Township is obligated to provide resources tocover the deficiency until other resources (such as tax sale proceeds or a reassessmentof the Township) are received. Revenue bonds involve a pledge of specific incomederived from the acquired or constructed assets to pay debt service.

29

Township of Hamburg

Notes to Financial StatementsJune 30, 2013

Note 6 - Long-term Debt (Continued)

Long-term debt activity can be summarized as follows:

Interest RateRanges

PrincipalMaturityRanges

BeginningBalance Additions Reductions Ending Balance

Due WithinOne Year

Governmental Activities

General obligation bonds -Fire station construction bonds:

Amount of issue - $3,500,000Maturing through 2016

4.125 -4.50%

$375,000 -$550,000 $ 1,900,000 $ - $ 400,000 $ 1,500,000 $ 450,000

2012 Water system projectrefunding bond:

Amount of issue - $1,730,000Maturing through 2031

2.00% -3.50%

$60,000 -$115,000 - 1,730,000 - 1,730,000 65,000

Revenue bonds -2002 Water System Project:

Amount of issue - $2,000,000Maturing through 2032

4.5% -5.00%

$50,000 -$125,000 1,775,000 - 1,775,000 - -

Special assessment bonds:1997 Limited Tax G.O.:

Amount of issue - $710,000Maturing through 2017

5.25% -5.50%

$40,000 -$45,000 220,000 - 40,000 180,000 45,000

2004 Special Assessment:Amount of issue - $5,660,000Portion related to governmental

$95,7554.00% -4.65%

$4,652 -$5,075 53,890 - 53,890 - -

2007 Special Assessment:Amount of issue - $170,000Maturing through 2017 4.61% $18,889 75,555 - 18,889 56,666 18,889

2008 Special Assessment:Amount of issue - $1,435,000Maturing through 2028

3.00% -4.20%

$50,000 -$125000 1,350,000 - 50,000 1,300,000 50,000

2010 Special Assessment:Amount of issue - $445,000Portion related to governmental

activities - $431,240Maturing through 2030

3.25% -5.75%

$19,382 -$24,225 406,980 - 24,220 382,760 24,225

2012 Special Assessment:Amount of issue - $2,595,000Portion related to governmental

activities - $43,855Maturing through 2023

2.00% -4.00%

$205,000 -$250,000 - 43,855 4,225 39,630 4,225

Installment purchase agreement -Mausoleum debt:

Amount of issue - $244,158Maturing through 2022 4.617%

$12,190 -$21,906 172,343 - 13,934 158,409 14,599

Add deferred charge on refunding N/A N/A - 43,084 - 43,084 -

Total bonds payable 5,953,768 1,816,939 2,380,158 5,390,549 671,938

Accumulated compensated absences N/A N/A 307,248 281,654 284,838 304,064 -

Total governmentalactivities $ 6,261,016 $ 2,098,593 $ 2,664,996 $ 5,694,613 $ 671,938

30

Township of Hamburg

Notes to Financial StatementsJune 30, 2013

Note 6 - Long-term Debt (Continued)

Interest RateRanges

PrincipalMaturityRanges

BeginningBalance Additions Reductions Ending Balance

Due WithinOne Year

Business-type Activity - Sewer

Special assessment bonds:1998 Series:

Amount of issue - $430,000Maturing through 2018

4.75% -5.00% $20,000 $ 120,000 $ - $ 20,000 $ 100,000 $ 20,000

1999 Series:Amount of issue - $4,580,000Maturing through 2014

5.15% -5.25%

$295,000 -$300,000 590,000 - 295,000 295,000 295,000

2004 Special Assessment:Amount of issue - $5,660,000Portion related to business-type

activities - $5,564,2454.00% -4.65%

$270,348 -$294,925 3,131,117 - 3,131,117 - -

2010 Special Assessment:Amount of issue - $445,000Portion related to business-type

activities - $13,760Maturing through 2030

3.00% -5.75% $618 - $775 13,020 - 775 12,245 775

2011 Refunding SAD bonds:Amount of issue - $2,235,000Maturing through 2021

2.00% -4.00%

$215,000 -$250,000 2,015,000 - 215,000 1,800,000 230,000

2012 Sewer and Contract RefundingSAD bonds:

Amount of issue - $2,595,000Portion related to business-type

activities - $2,551,145Maturing through 2023

2.00% -4.00%

$205,000 -$250,000 - 2,551,145 245,775 2,305,370 245,775

Revenue bonds -2007 Waste Water Treatment

Plant:Amount of issue - $4,590,000Maturing through 2028

3.60% -4.20%

$210,000 -$300,000 3,665,000 - 210,000 3,455,000 235,000

State Revolving Fund Bonds:2009 Limited Tax G.O. bonds:

Amount of issue - $1,235,202Maturing through 2030 2.50%

$49,202 -$80,000 1,139,202 - 50,000 1,089,202 55,000

2010 Limited Tax G.O. bonds:Amount available: $3,265,000 of

which $3,206,514 has beendrawn down

Maturing through 2031 2.50%$125,000 -$205,000 3,081,514 58,486 130,000 3,010,000 135,000

Installment purchase agreements:Amount of issue - $736,629Maturing through 2013 3.25%

$80,939 -$83,621 83,621 - 83,621 - -

Add deferred charge on refunding N/A N/A - 18,236 - 18,236 -

Total bonds andinstallment purchaseagreements 13,838,474 2,627,867 4,381,288 12,085,053 1,216,550

Accumulated compensated absences N/A N/A 21,445 20,852 21,445 20,852 -

Total business-typeactivities $ 13,859,919 $ 2,648,719 $ 4,402,733 $ 12,105,905 $ 1,216,550

31

Township of Hamburg

Notes to Financial StatementsJune 30, 2013

Note 6 - Long-term Debt (Continued)

Annual debt service requirements to maturity for the above bonds and note obligationsare as follows:

Governmental Activities Business-type ActivitiesYear Ending

June 30 Principal Interest Total Principal Interest Total

2014 $ 671,938 $ 216,828 $ 888,766 $ 1,216,550 $ 414,245 $ 1,630,7952015 722,611 189,520 912,131 906,550 370,004 1,276,5542016 793,316 159,460 952,776 896,550 339,052 1,235,6022017 250,150 125,833 375,983 951,550 302,309 1,253,8592018 205,765 114,987 320,752 941,719 263,097 1,204,816

2019-2023 1,118,177 454,573 1,572,750 4,235,201 850,061 5,085,2622024-2028 1,106,745 221,322 1,328,067 2,188,255 270,624 2,693,8792029-2033 478,763 33,618 512,378 730,442 25,702 756,144

Total $ 5,347,465 $ 1,516,141 $ 6,863,603 $ 12,066,817 $ 2,835,094 $ 15,136,911

Revenue Bond - The Township has pledged substantially all revenue of the SewerFund, net of operating expenses, to repay the above sewer revenue bonds. Proceedsfrom the bonds provided financing for the construction of the wastewater treatmentplant. The bonds are payable solely from the net revenue of the sewer system. Theremaining principal and interest to be paid on the bond total $4,606,413. During thecurrent year, net revenue of the sewer system was $751,807 compared to the annualdebt requirements of $379,469.

Defeased Debt - In prior years, the Township defeased certain bonds by placing theproceeds of new bonds in an irrevocable trust to provide for all future debt servicepayments on the old bonds. Accordingly, the trust accounts' assets and liabilities for thedefeased bonds are not included in the basic financial statements. At June 30, 2013,$10,895,000 of bonds outstanding are considered defeased.

Current Refunding - During the year, the Township issued $2,595,000 in SpecialAssessment Refunding Bonds with interest rates ranging from 2.00 percent to4.00 percent. The proceeds of these bonds were used to advance refund $3,185,000 ofoutstanding Series 2004 Special Assessment General Obligation bonds with interestrates ranging from 4.00 percent to 4.65 percent. The net proceeds of $2,699,586 wereused to purchase U.S. government securities. Those securities were deposited in anirrevocable trust with an escrow agent to provide for all future debt service paymentson the original bonds. As a result, the bonds are considered to be defeased and theliability for the bonds has been removed from the governmental long-term debt accountgroup. The advance refunding reduced total debt service payments over the next nineyears by approximately $390,000, which represents an economic gain of approximately$303,000.

32

Township of Hamburg

Notes to Financial StatementsJune 30, 2013

Note 6 - Long-term Debt (Continued)

Also, during the year, the Township issued $1,730,000 in Limited Tax GeneralObligation Refunding Bonds with interest rates ranging from 2.00 percent to 3.50percent. The proceeds of these bonds were used to advance refund $1,725,000 ofoutstanding 2002 Water System revenue bonds with interest rates ranging from 4.50 to5.00 percent. The net proceeds of $1,771,319 after payment of underwriting fees,insurance, and other issuance costs were used to purchase U.S. government securities.Those securities were deposited in an irrevocable trust with an escrow agent to providefor all future debt service payments on the original bonds. As a result, the bonds areconsidered to be defeased and the liability for the bonds has been removed from thegovernmental long-term debt account group. The advance refunding reduced total debtservice payments over the next seven years by approximately $370,000, whichrepresents an economic gain of approximately $285,000.

Note 7 - Defined Contribution Pension Plan

The Township provides pension benefits to all of its full-time employees, except policeofficers, through a defined contribution plan. In a defined contribution plan, benefitsdepend solely on amounts contributed to the plan plus investment earnings. Asestablished by the Township board, the Township contributes 10 percent of employees'gross earnings. In accordance with these requirements, the Township contributedapproximately $170,000 during the year.

Note 8 - Defined Benefit Pension Plan

Plan Description - The Township participates in the Michigan Municipal Employees'Retirement System (MMERS), an agent multiple-employer defined benefit pension planthat covers all employees of the Township. MMERS provides retirement, disability, anddeath benefits to plan members and their beneficiaries. The Michigan MunicipalEmployees' Retirement System issues a publicly available financial report that includesfinancial statements and required supplemental information for MMERS. That reportmay be obtained by writing to the system at 1134 Municipal Way, Lansing, MI 48917.

Funding Policy - The obligation to contribute to and maintain MMERS for theseemployees was established by negotiation with the Township's competitive bargainingunits and requires a contribution from the employees of 7 percent of wages. TheTownship is responsible for the remainder of the cost of the plan.

33

Township of Hamburg

Notes to Financial StatementsJune 30, 2013

Note 8 - Defined Benefit Pension Plan (Continued)

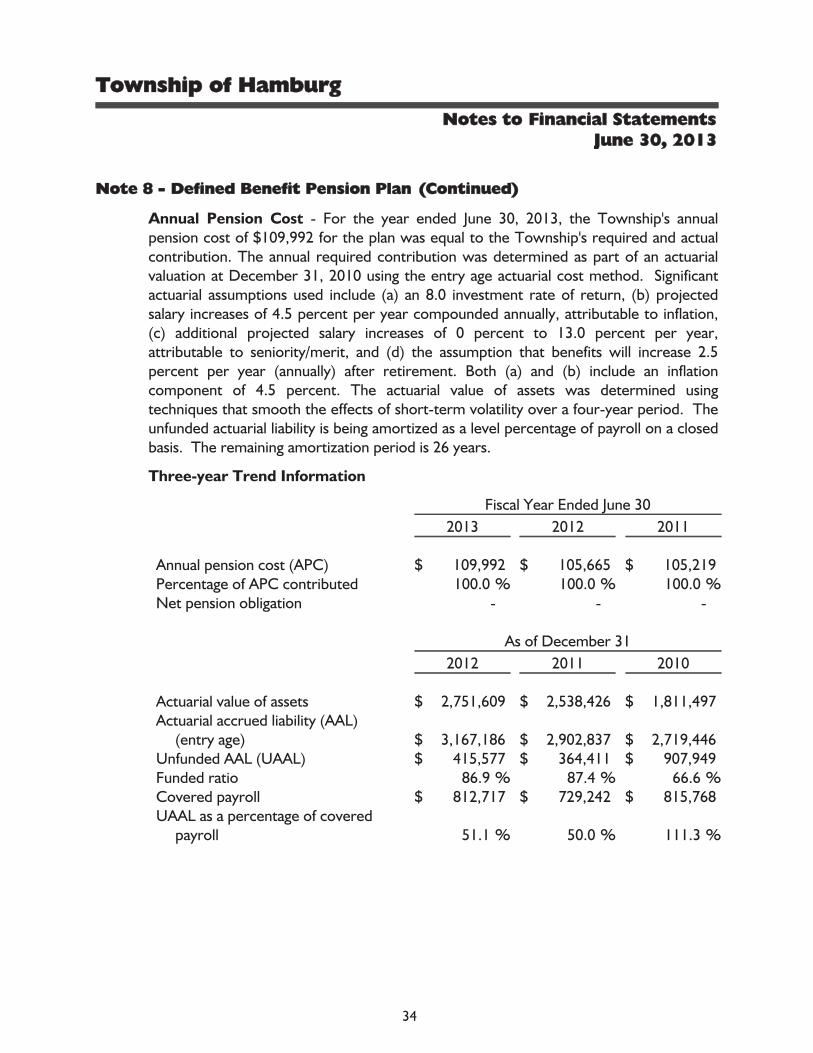

Annual Pension Cost - For the year ended June 30, 2013, the Township's annualpension cost of $109,992 for the plan was equal to the Township's required and actualcontribution. The annual required contribution was determined as part of an actuarialvaluation at December 31, 2010 using the entry age actuarial cost method. Significantactuarial assumptions used include (a) an 8.0 investment rate of return, (b) projectedsalary increases of 4.5 percent per year compounded annually, attributable to inflation,(c) additional projected salary increases of 0 percent to 13.0 percent per year,attributable to seniority/merit, and (d) the assumption that benefits will increase 2.5percent per year (annually) after retirement. Both (a) and (b) include an inflationcomponent of 4.5 percent. The actuarial value of assets was determined usingtechniques that smooth the effects of short-term volatility over a four-year period. Theunfunded actuarial liability is being amortized as a level percentage of payroll on a closedbasis. The remaining amortization period is 26 years.

Three-year Trend Information

Fiscal Year Ended June 302013 2012 2011

Annual pension cost (APC) $ 109,992 $ 105,665 $ 105,219Percentage of APC contributed %100.0 %100.0 %100.0Net pension obligation - - -

As of December 312012 2011 2010

Actuarial value of assets $ 2,751,609 $ 2,538,426 $ 1,811,497Actuarial accrued liability (AAL)

(entry age) $ 3,167,186 $ 2,902,837 $ 2,719,446Unfunded AAL (UAAL) $ 415,577 $ 364,411 $ 907,949Funded ratio %86.9 %87.4 %66.6Covered payroll $ 812,717 $ 729,242 $ 815,768UAAL as a percentage of covered

payroll %51.1 %50.0 %111.3

34

Township of Hamburg

Notes to Financial StatementsJune 30, 2013

Note 9 - Investment in Joint Ventures