toiletries 2011

TRANSCRIPT

Market Report Plus 2011

24th Edition July 2011Edited by Sarah Walker

ISBN 978-1-84729-750-1

Toiletries

In today’s competitive business environment, knowledge and understanding of yourmarketplace is essential. With over 30 years’ experience producing highly respectedoff-the-shelf publications, Key Note has built a reputation as the number one sourceof UK market information. Below are just a few of the comments our business partnersand clients have made on Key Note’s range of reports.

"The test of any marketing strategy and plan lies in the quality of information used, upon whichmarketing judgments and decisions are based. Quality is the key word here. The Key Notereports are an excellent source of such quality information, covering a wide variety of productsectors."

The Chartered Institute of Marketing

"We have enjoyed a long-standing relationship with Key Note and have always received anexcellent service. Key Note reports are well produced and are always in demand by users of thebusiness library. Having subscribed to Market Assessment reports for a number of years, wecontinue to be impressed by their quality and breadth of coverage."

The British Library

"Key Note is an invaluable resource which is reliable and easy to use. With a wide range ofreports, it is useful for monitoring the outside world. Staff are always very helpful."

The National Trust

"The US Commercial Service in London has been subscribing to Key Note market researchreports for over 5 years. We find the reports an invaluable resource in our business counselingactivities to the US companies wishing to enter the UK market with products and services. Thereports’ market data, competition, and forecast sections are especially useful."

US Embassy

"I regard Key Note as the number one provider of UK market research. The way Key Notecontent is packaged and presented is appealing and easy to understand and therefore a mustfor my taught course students. Its products are complemented by remarkably high levels ofcustomer service."

University of Cambridge, Judge Business School

Toiletries Foreword

© Key Note Ltd 2011

Contents

Executive Summary 1

1. Market Definition 2

REPORT COVERAGE....................................................................................................................2

MARKET SECTORS.......................................................................................................................2

MARKET TRENDS.........................................................................................................................3

Suppliers Change Promotional Strategies.................................................................................3

Growing Popularity of Social Media..........................................................................................3

Private Labels Benefiting From Changing Consumer Spending Habits..............................3

ECONOMIC TRENDS....................................................................................................................4

Gross Domestic Product ...............................................................................................................4Table 1.1: UK Gross Domestic Product at Current and Annual Chain-Linked Prices(£m), 2006-2010..............................................................................................................................4

Inflation ..........................................................................................................................................4Table 1.2: UK Rate of Inflation (%), 2006-2010.......................................................................5

Household Disposable Income ...................................................................................................5Table 1.3: UK Household Disposable Income Per Capita (£), 2006-2010............................5

Population ......................................................................................................................................6Table 1.4: UK Resident Population Estimates by Sex (000), Mid-Years 2006-2010...........6

Unemployment ..............................................................................................................................6Table 1.5: Actual Number of Unemployed Persons in the UK (million), 2006-2010.........7

MARKET POSITION......................................................................................................................7

The UK..............................................................................................................................................7

Table 1.6: Consumer Expenditure on Miscellaneous Goods and Services for PersonalCare (£m), 2006-2010....................................................................................................................7

Overseas...........................................................................................................................................8

2. Market Size 9

THE TOTAL MARKET..................................................................................................................9

Manufacturers’ Sales ....................................................................................................................9Retail Sales.......................................................................................................................................9

Table 2.1: The Total UK Market for Toiletries by Sector by Value at Current Prices(£m at rsp), 2006-2010...................................................................................................................9

Toiletries Contents

© Key Note Ltd 2011

Figure 2.1: The Total UK Market for Toiletries by Value at Current Prices(£m at rsp), 2006-2010.................................................................................................................10

BY MARKET SECTOR.................................................................................................................10

Figure 2.2: The Total UK Toiletries Market by Sector Share (%), 2010.............................11

Personal Wash and Bathroom Toiletries ................................................................................11

Table 2.2: The UK Personal Wash and Bathroom Toiletries Sector by Subsectorby Value at Current Prices (£m at rsp), 2009 and 2010........................................................12

Skincare Products ........................................................................................................................12

Table 2.3: The UK Skincare Products Sector by Subsector by Value at Current Prices(£m at rsp), 2009 and 2010.........................................................................................................12

Hair Care Products.......................................................................................................................13

Table 2.4: The UK Hair Care Products Sector by Subsector by Value at Current Prices(£m at rsp), 2009 and 2010.........................................................................................................13

Oral Care Products ......................................................................................................................13

Table 2.5: The UK Oral Care Products Sector by Subsector by Value at Current Prices(£m at rsp), 2009 and 2010.........................................................................................................14

Shaving Products .........................................................................................................................14

Table 2.6: The UK Shaving Products Sector by Subsector by Value at Current Prices(£m at rsp), 2009 and 2010.........................................................................................................14

OVERSEAS TRADE......................................................................................................................15

Table 2.7: UK Imports and Exports of Toiletries by Value (£000), 2008-2010..................15

Imports...........................................................................................................................................15

Table 2.8: UK Intra-EU Arrivals and Extra-EU Imports of Toiletries by Categoryby Value (£000), 2010..................................................................................................................16

Exports............................................................................................................................................16

Table 2.9: UK Intra-EU Despatches and Extra-EU Exports of Toiletries by Categoryby Value (£000), 2010..................................................................................................................17

3. Industry Background 18

RECENT HISTORY.......................................................................................................................18

NUMBER OF COMPANIES.......................................................................................................18

Table 3.1: Number of UK VAT- and/or PAYE-Based Enterprises Engagedin the Manufacture of Perfumes and Toilet Preparations by Turnover Sizeband,2010................................................................................................................................................18

EMPLOYMENT............................................................................................................................19

Table 3.2: Number of UK VAT- and/or PAYE-Based Enterprises Engagedin the Manufacture of Perfumes and Toilet Preparations by Employment Sizeband,2010................................................................................................................................................19

REGIONAL VARIATIONS IN THE MARKETPLACE.............................................................20

DISTRIBUTION.............................................................................................................................20

Selective Distribution .................................................................................................................20

Specialist Retailers ......................................................................................................................20

Toiletries Contents

© Key Note Ltd 2011

High-Street Stores........................................................................................................................21

Department Stores ......................................................................................................................21

Supermarkets ...............................................................................................................................21

Direct Selling ................................................................................................................................21

HOW ROBUST IS THE MARKET?...........................................................................................21

LEGISLATION...............................................................................................................................22

Cosmetics Directive 1976............................................................................................................22

Cosmetics Products Regulations................................................................................................22

REACH............................................................................................................................................22

KEY TRADE ASSOCIATIONS....................................................................................................23

Cosmetic, Toiletry and Perfumery Association.......................................................................23

The European Cosmetics Association ......................................................................................23

4. Competitor Analysis 24

THE MARKETPLACE..................................................................................................................24

MARKET LEADERS — MANUFACTURERS..........................................................................24

Avon Cosmetics Ltd......................................................................................................................24

Estée Lauder Cosmetics Ltd .......................................................................................................25

L’Oréal (UK) Ltd............................................................................................................................25

Procter & Gamble (Health & Beauty Care) Ltd ......................................................................26

PZ Cussons PLC..............................................................................................................................26

Unilever PLC..................................................................................................................................27

MARKET LEADERS — RETAILERS ........................................................................................27

Alliance Boots Ltd .......................................................................................................................27

Table 4.1: Alliance Boots Group Revenue and Trading Profit by Division (£m), YearEnding 31st March 2011.............................................................................................................28

The Body Shop International PLC ............................................................................................29

Lush Cosmetics Ltd ......................................................................................................................29

Molton Brown Ltd ......................................................................................................................30

Superdrug Stores PLC .................................................................................................................30

OUTSIDE SUPPLIERS..................................................................................................................31

Research and Development ......................................................................................................31

Raw Materials ..............................................................................................................................31

Processing Machinery, Packaging and components ............................................................31

Outsourcing ..................................................................................................................................32

MARKETING ACTIVITY.............................................................................................................32

Main Media Advertising Expenditure .....................................................................................32

Table 4.2: Main Media Advertising Expenditure on Toiletries by Sector (£000), YearsEnding March 2010 and 2011....................................................................................................32

Table 4.3: Main Media Advertising Expenditure on Deodorants (£000), Year EndingMarch 2011....................................................................................................................................34

Toiletries Contents

© Key Note Ltd 2011

Table 4.4: Main Media Advertising Expenditure on Bath Toiletries and Shower Gels(£000), Year Ending March 2011...............................................................................................36

Table 4.5: Main Media Advertising Expenditure on Mass-Market Cleaners and Wipes(£000), Year Ending March 2011...............................................................................................37

Table 4.6: Main Media Advertising Expenditure on Liquid Foam Bath and LiquidHand Soap (£000), Year Ending March 2011..........................................................................37

Table 4.7: Main Media Advertising Expenditure on Mass-Market Bath and BeautyRanges (£000), Year Ending March 2011................................................................................38

Table 4.8: Main Media Advertising Expenditure on Skincare by Type (£000), YearEnding Marching 2011................................................................................................................38

Table 4.9: Main Media Advertising Expenditure on Mass-Market Women’s FacialSkincare (£000), Year Ending March 2011..............................................................................39

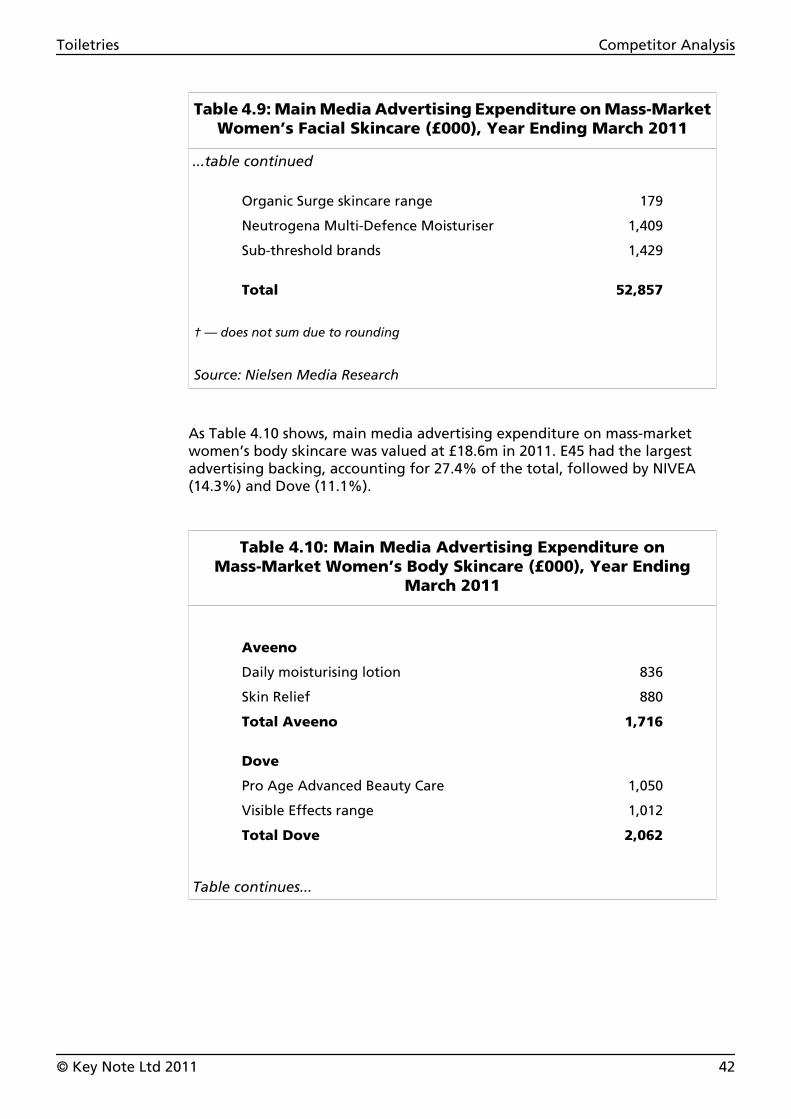

Table 4.10: Main Media Advertising Expenditure on Mass-Market Women’s BodySkincare (£000), Year Ending March 2011..............................................................................42

Table 4.11: Main Media Advertising Expenditure on Premium Women’s FacialSkincare (£000), Year Ending March 2011..............................................................................44

Table 4.12: Main Media Advertising Expenditure on Mass-Market Women’sMedicated Facial Skincare (£000), Year Ending March 2011..............................................45

Table 4.13: Main Media Advertising Expenditure on Mass-Market Men’s Skincare(£000), Year Ending March 2011...............................................................................................46

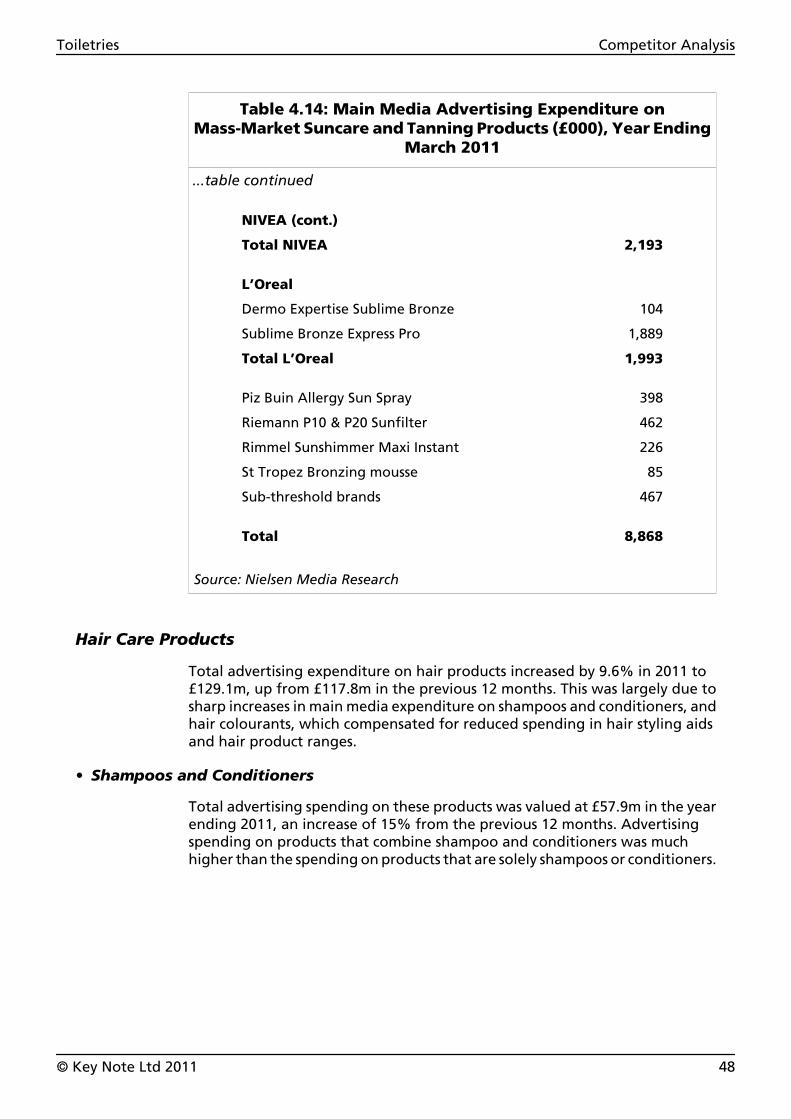

Table 4.14: Main Media Advertising Expenditure on Mass-Market Suncareand Tanning Products (£000), Year Ending March 2011......................................................47

Table 4.15: Main Media Advertising Expenditure on Shampoos and Conditionersby Type (£000), Year Ending March 2011...............................................................................49

Table 4.16: Main Media Advertising Expenditure on Shampoos and Conditioners(£000), Year Ending March 2011...............................................................................................49

Table 4.17: Main Media Advertising Expenditure on Hair Colourants (£000), YearEnding March 2011......................................................................................................................51

Table 4.18: Main Media Advertising Expenditure on Hair Product Ranges (£000),Year Ending March 2011............................................................................................................52

Table 4.19: Main Media Advertising Expenditure on Hair Styling Aids (£000), YearEnding March 2011......................................................................................................................53

Table 4.20: Main Media Advertising Expenditure on Hairsprays (£000), Year EndingMarch 2011....................................................................................................................................53

Table 4.21: Main Media Advertising Expenditure on Toothpastes and Polishes(£000), Year Ending March 2011...............................................................................................54

Table 4.22: Main Media Advertising Expenditure on Other Oral Hygiene Products(£000), Year Ending March 2011...............................................................................................56

Table 4.23: Main Media Advertising Expenditure on Wet Razors and Blades (£000),Year Ending March 2011............................................................................................................58

Table 4.24: Main Media Advertising Expenditure on Shaving Preparations (£000),Year Ending March 2011............................................................................................................59

Table 4.25: Main Media Advertising Expenditure on Depilatories and Bleach(£000), Year Ending March 2011...............................................................................................59

Exhibitions and Trade Fairs........................................................................................................60

Toiletries Contents

© Key Note Ltd 2011

5. Brand Strategy 61

INTRODUCTION..........................................................................................................................61

THE WORLD’S MOST VALUABLE BRANDS .......................................................................61

Table 5.1: Leading Global Brands of Cosmetics and Toiletries by Rank and Value($m), 2010......................................................................................................................................61

CEW AWARDS.............................................................................................................................62

LEADING BRANDS BY SECTOR..............................................................................................63

Personal Wash and Bathroom Toiletries ................................................................................63

Skincare Products.........................................................................................................................63

Hair Care Products ......................................................................................................................63

Oral Care Products ......................................................................................................................63

Shaving Products .........................................................................................................................64

6. Strengths, Weaknesses, Opportunities and Threats 65

STRENGTHS..................................................................................................................................65

WEAKNESSES..............................................................................................................................65

OPPORTUNITIES.........................................................................................................................66

THREATS.......................................................................................................................................66

7. Buying Behaviour 67

AVERAGE WEEKLY HOUSEHOLD EXPENDITURE............................................................67

Table 7.1: Average Weekly Household Expenditure on Personal Care (£), 2009............67

By Age............................................................................................................................................67

Table 7.2: Average Weekly Household Expenditure on Personal Care by Ageof Household Reference Person (£), 2009...............................................................................68

By Gross Income Decile Group...................................................................................................68

Table 7.3: Average Weekly Household Expenditure on Personal Care by GrossIncome Decile Group (£), 2009..................................................................................................69

CUSTOMER PENETRATION.....................................................................................................69

Hair Care Products ......................................................................................................................70

Table 7.4: Usage of Hair Care Products in the Last 12 Months by Sex (% of adults),2010................................................................................................................................................70

Shampoo........................................................................................................................................70

Table 7.5: Female Usage of Shampoo in the Last 12 Months by Age and Social Grade(% of adults), 2010......................................................................................................................71

Table 7.6: Types of Shampoo Used Most Often by Women in the Last 12 Months(%), 2010........................................................................................................................................71

Conditioner ..................................................................................................................................72

Toiletries Contents

© Key Note Ltd 2011

Table 7.7: FemaIe Usage of Conditioners (Excluding Treatments and Masques)in the Last 12 Months by Age and Social Grade (% of adults), 2010................................72

Hair Styling Products ..................................................................................................................73

Table 7.8: Usage of Hair Styling Products in the Last 12 Months by Sex, Ageand Social Grade (% of adults), 2010.......................................................................................73

Hair Colourants ...........................................................................................................................74

Table 7.9: Usage of Hair Colourants in the Last 12 Months by Sex, Age and SocialGrade (% of adults), 2010..........................................................................................................74

Other Toiletries ...........................................................................................................................75

Table 7.10: Usage of Other Toiletries Products by Women in the Last 12 Months(%), 2010........................................................................................................................................75

Table 7.11: Usage of Other Toiletries Products by Men in the Last 12 Months (%),2010................................................................................................................................................76

Toothpaste ...................................................................................................................................76

Table 7.12: Usage of Toothpaste in the Last 12 Months by Age and Social Grade(% of adults), 2010......................................................................................................................76

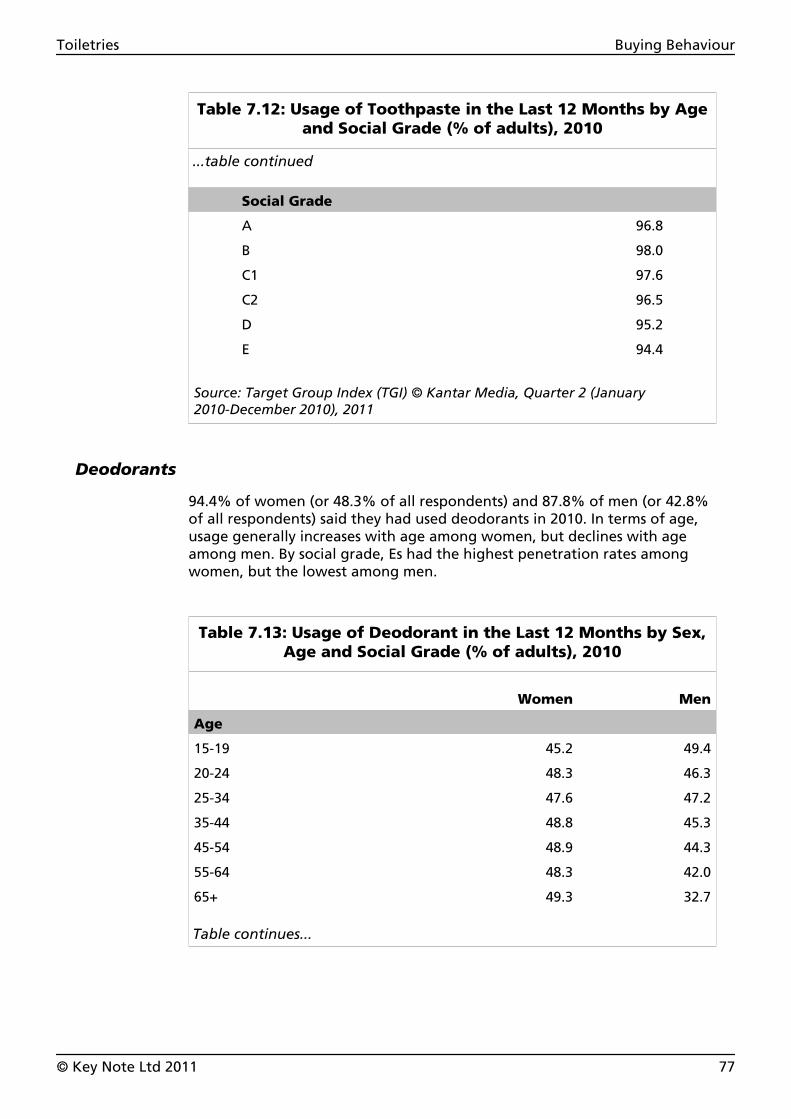

Deodorants ...................................................................................................................................77

Table 7.13: Usage of Deodorant in the Last 12 Months by Sex, Age and Social Grade(% of adults), 2010......................................................................................................................77

Face Creams and Lotions ...........................................................................................................78

Table 7.14: Usage of Face Cream and Lotions in the Last 12 Months by Sex, Ageand Social Grade (% of adults), 2010.......................................................................................78

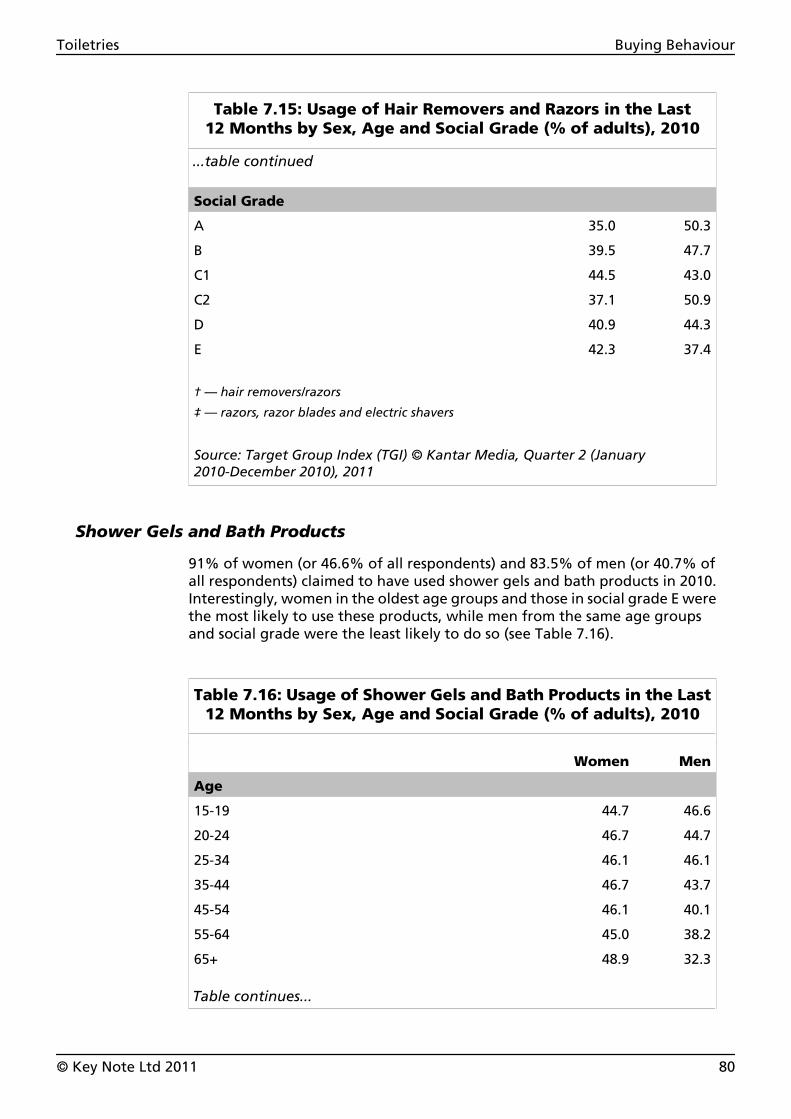

Hair Removers and Razors ........................................................................................................79

Table 7.15: Usage of Hair Removers and Razors in the Last 12 Months by Sex, Ageand Social Grade (% of adults), 2010.......................................................................................79

Shower Gels and Bath Products ...............................................................................................80

Table 7.16: Usage of Shower Gels and Bath Products in the Last 12 Months by Sex,Age and Social Grade (% of adults), 2010..............................................................................80

Cleansing Creams, Lotions and Wipes ....................................................................................81

Table 7.17: Usage of Cleansing Creams, Milks, Lotions, Toner, Wipes and Washesby Women in the Last 12 Months by Age and Social Grade (% of adults), 2010...........81

Liquid Soap/Handwash ..............................................................................................................82

Table 7.18: Usage of Liquid Soap/Handwash in the Last 12 Months by Age and SocialGrade (% of adults), 2010..........................................................................................................82

Bars of Soap .................................................................................................................................83

Table 7.19: Usage of Bars of Soap in the Last 12 Months by Age and Social Grade(% of adults), 2010......................................................................................................................83

Suntan and Sun Protection Products ......................................................................................84

Table 7.20: Usage of Suntan and Sun Protection Products in the Last 12 Monthsby Age and Social Grade (% of adults), 2010.........................................................................84

Toiletries Contents

© Key Note Ltd 2011

8. Current Issues 86

THE ECONOMY...........................................................................................................................86

RETAILERS ARE STRUGGLING................................................................................................86

RISING MATERIALS COSTS CAUSING PRICES HIKES........................................................87

UNILEVER AND P&G IN PRICE FIXING FINE.......................................................................87

NEW PRODUCTS.........................................................................................................................87

NIVEA..............................................................................................................................................87

L’Oreal ...........................................................................................................................................87

Dove ...............................................................................................................................................88

Sensodyne......................................................................................................................................88

Mandara.........................................................................................................................................88

Sk:n.................................................................................................................................................88

9. The Global Market 89

INTRODUCTION..........................................................................................................................89

EUROPE.........................................................................................................................................89

Table 9.1: Retail Sales of Cosmetics and Toiletries in the Top Five EU Member Statesby Value (€), 2009........................................................................................................................89

THE US...........................................................................................................................................90

SELECTED GLOBAL COMPETITORS .....................................................................................90

AS Watson Group.........................................................................................................................90

Avon Products Inc........................................................................................................................91

Beiersdorf AG................................................................................................................................91

Burt’s Bees ....................................................................................................................................91

Colgate-Palmolive Company .....................................................................................................92

Crabtree & Evelyn Ltd.................................................................................................................92

Estee Lauder Inc...........................................................................................................................92

Table 9.2: Estée Lauder Inc — Total Sales by Product Category ($m), Years Ending30th June 2009 and 2010...........................................................................................................93

L’Oreal SA......................................................................................................................................93

Mary Kay Inc..................................................................................................................................94

Procter & Gamble Company .....................................................................................................94

PZ Cussons ....................................................................................................................................94

Table 9.3: PZ Cussons — Group Revenue by Geographical Region (£m), Years Ending31st May 2009 and 2010.............................................................................................................95

Unilever PLC..................................................................................................................................95

Table 9.4: Unilever PLC — Sales by Geographic Region (€m), Year Ending31st December 2009 and 2010..................................................................................................96

Toiletries Contents

© Key Note Ltd 2011

10. Forecasts 97

INTRODUCTION..........................................................................................................................97

Population.....................................................................................................................................97

Table 10.1: Forecast UK Resident Population by Sex (000), Mid-Years 2011-2015.........97

Gross Domestic Product..............................................................................................................97

Table 10.2: Forecast UK Growth in Gross Domestic Product in Real Terms (%),2011-2015......................................................................................................................................98

Inflation.........................................................................................................................................98

Table 10.3: Forecast UK Rate of Inflation (%), 2011-2015...................................................98

Unemployment.............................................................................................................................98

Table 10.4: Forecast Actual Number of Unemployed Persons in the UK (million),2011-2015......................................................................................................................................99

FORECASTS 2006-2010.............................................................................................................99

Table 10.5: The Forecast UK Market for Toiletries by Sector by Value at CurrentPrices (£m at rsp), 2011-2015.....................................................................................................99

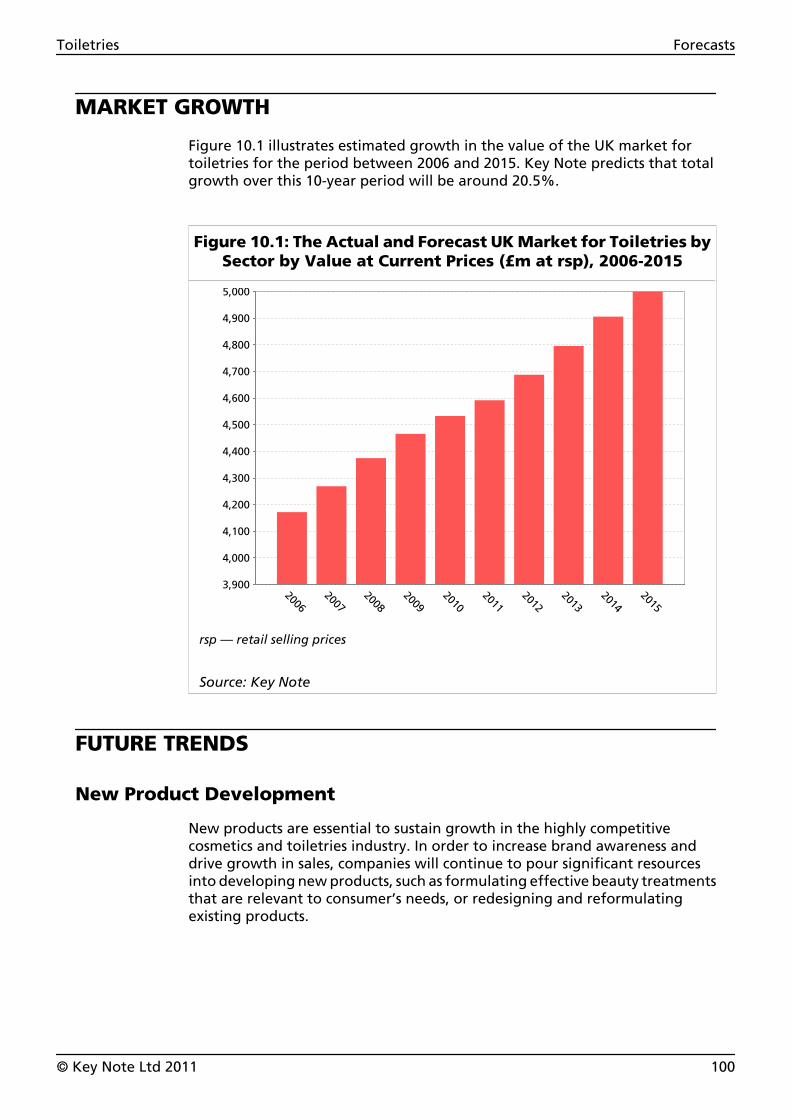

MARKET GROWTH..................................................................................................................100

Figure 10.1: The Actual and Forecast UK Market for Toiletries by Sector by Valueat Current Prices (£m at rsp), 2006-2015...............................................................................100

FUTURE TRENDS.......................................................................................................................100

New Product Development......................................................................................................100

Size of Products Set to Shrink..................................................................................................101

11. Company Profiles 102

AVON COSMETICS LTD..........................................................................................................103

ESTEE LAUDER COSMETICS LTD.........................................................................................105

L’OREAL (UK) LTD....................................................................................................................107

PROCTER & GAMBLE (HEALTH & BEAUTY CARE) LTD................................................109

PZ CUSSONS PLC......................................................................................................................111

SUPERDRUG STORES PLC......................................................................................................113

UNILEVER PLC...........................................................................................................................115

12. Company Financials 117

13. Further Sources 119

Associations...............................................................................................................................119

Publications...............................................................................................................................119

General Sources.......................................................................................................................120

Toiletries Contents

© Key Note Ltd 2011

Government Publications ....................................................................................................120

Other Sources...........................................................................................................................121

Key Note Sources ....................................................................................................................122

Understanding TGI Data 124

Number, Profile, Penetration..............................................................................................124

Social Grade...............................................................................................................................125

Standard Region......................................................................................................................125

Key Note Research 126

The Key Note Range of Reports 127

Toiletries Contents

© Key Note Ltd 2011

• “Product performance is the key tosuccess as consumers will only purchasebrands they can trust and rely on.Staying at the forefront of technologyand investing in brands will ensurecategory growth.”

Matt Close, VP Marketing, Unilever (The Grocer,5th February 2011)

• “Today’s savvy consumers arescrutinising the ingredients in personalcare products and driving the demandfor natural products that are safe,efficacious and sustainable.”

Kerty Levy, Kemin Industries,(www.cosmeticsbusiness.com)

• “The 2010 figures are consistent withprevious years, with personal care stillthe major driver in the UK. The sectoralso continues to show resilienceoverall, despite a difficult economicclimate.”

Sue Rogers, Director of British AerosolManufacturers’ Association,(www.cosmeticsbusiness.com)

Toiletries

© Key Note Ltd 2011

Executive Summary

This Key Note Market Report Plus examines the toiletries market in the UK.Characterised by a wide range of product types, the toiletries market isdominated by a small number of large multinational corporations includingProcter & Gamble, PZ Cussons, L’Oreal SA and Unilever.

The market itself is divided into five sectors: personal wash and bathroomproducts, skincare products, hair care products, oral care products and shavingproducts (for men and women). Key Note estimates that the total UK toiletriesmarket was worth £4.5bn in 2010, with personal wash and bathroom toiletriescomprising the largest sector by value (27.3%), followed by skincare products(27.1%) and hair care products (24.8%).

Compared with other industries — such as the construction and propertymarkets — the overall toiletries market weathered the recent economicdownturn relatively well. Many items, such as shampoos, soaps anddeodorants, etc., are regarded as daily essentials. Nevertheless, the economicdownturn did leave its mark on the industry.

One manifestation of this has been a change in consumer spending habits, withincreasing numbers trading down to value products. On the positive side, someconsumers are purchasing more premium products as they cut down on moreexpensive salon treatments, effectively transferring new business to thetoiletries market. Another noticeable impact of the strained economy has beenthe clear scaling down of some promotional activities, a result of suppliers’profit margins being squeezed as commodity prices have risen for almosteverything from oil to specialist beauty ingredients.

While television and print media remain popular, brands are increasinglyexperimenting with new digital channels as they seek more effective ways ofconnecting with their existing and potential clientele. The Internet and socialmedia sites such as Facebook, Twitter, and YouTube, are perceived to beeffective avenues for brands to communicate through, especially to both maleand younger buyers.

Although some sectors are reaching saturation point — and discountingcontinues to restrict value growth — outlook for the industry is positive. The‘necessary’ nature of its products and a strong sense of brand loyalty amongits customers are its strongest assets. The industry also features high levels ofinvestment in new product development (NPD), which continues to drive sales.Significant opportunities exist in the areas of cosmeceuticals and green/ethicalproducts.

Key Note forecasts retail sales of toiletries will grow by close to 10% between2011 and 2015, to reach £5.03m in the latter year. The sectors which areexpected to exhibit the strongest growth are skincare products, followed bypersonal wash and bathroom toiletries.

Toiletries Executive Summary

© Key Note Ltd 2011 1

1. Market Definition

REPORT COVERAGE

Cosmetic and toiletry products are defined as any substance or preparationintended to be placed in contact with the various external parts of the humanbody, or with the teeth and the mucous membranes of the oral cavity, with aview exclusively or mainly of cleaning them, perfuming them, changing theirappearance and/or correcting body odours, and/or protecting them or keepingthem in good condition. This Key Note report looks at the range of toiletryproducts that are primarily of a functional use. Cosmetics, which are of a purelydecorative nature, are not included, although the distinction is becomingincreasingly blurred with new types of product.

MARKET SECTORS

For the purpose of this report, the toiletries market will be divided into thefollowing sectors:

• Personal washing and related bathroom products — traditional bar soaps,liquid soaps, shower gels, bath liquids, deodorants, bodysprays and talcumpowder

• Oral care products — toothpaste, mouthwash, dental floss, etc.

• Hair care products — shampoos, conditioners, colourants and hair styling aidssuch as gels, mousses and sprays

• Skincare products — hand, body and facial moisturisers, cleansers and toners,exfoliating scrubs and sun filters/after-sun products

• Shaving products — wet-shave and after-shave products, and razors andblades, including those designed specifically for the women’s market;depilatory creams are also included.

Toiletries Market Definition

© Key Note Ltd 2011 2

MARKET TRENDS

Suppliers Change Promotional Strategies

In recent years, promotions in the toiletries market have been exerting a stronginfluence on consumer purchasing behaviour, with supermarkets being one ofthe most common places to buy toiletry products. The ’buy one, get one free’trend became so wide-spread that consumers rarely needed to buy certainproducts at full price. In 2010, however, as a result of suppliers being unableto sustain the level of promotions (following the increases in commodity prices,from oil to specialist beauty ingredients including geranium and lavender),deep discount promotion all but disappeared. Many suppliers believe thechange is necessary. As one brand manager of Beiersdorf put it: ‘If you promoteand promote, there will be no value left. That’s not beneficial to anybody. Noteven consumers, because it will stop brands investing in new productdevelopment (NPD). There needs to be some value, so that’s why we’re startingto do ’two for £4’ on our deodorants, rather than ’three for £3.50’.’

Growing Popularity of Social Media

While television and print media remain popular, social media is thefastest-growing marketing channel. Brands are increasingly experimentingwith these new digital channels, from which they are seeking to developstronger and deeper relationships with their existing and potential clientele.Lynx, for example, launched its Excite variant with a focus on digital activity,including a Facebook game — featuring Kelly Brook — aimed at maleaudiences. The Internet and social media sites, such as Facebook, Twitter,YouTube and Flickr, are perceived to be a particularly effective way for brandsto reach both male and younger buyers. Social media avenues may be used fordirect communication with consumers and for listening exercises, to promotebrand awareness or trial new product ideas, and to support larger mediacampaigns.

Private Labels Benefiting From Changing Consumer SpendingHabits

Economic turbulence has undoubtedly accelerated the growth of private-labelproducts, as a significant number of consumers seek out less expensivepurchases. This is evident from the number of private-label products that havebeen launched by retailers in recent years, examples of which are Tesco’sVitamin E skincare range and Boots’ No. 7 range. According to the Private LabelManufacturers Association (PLMA), private-label products now hold theirstrongest competitive position, accounting for one of every two products soldin the UK and Switzerland. Younger shoppers show particularly strong supportfor this sector.

Toiletries Market Definition

© Key Note Ltd 2011 3

ECONOMIC TRENDS

Gross Domestic Product

Between 2003 and 2008, the UK’s gross domestic product (GDP) grew at ayear-on-year rate of approximately 5%. This growth was principally driven byconsumer spending and low interest rates. In 2008, however, as a result of thefinancial crisis, growth slowed markedly to 2.9% — and dramatically moved toa contraction of 3.5% (at current prices) as the country entered recession in2009. The UK officially emerged from recession in January 2010, bringing to anend six consecutive quarters of contraction. In 2010, official figures confirmedthat the economy had begun to recover, as GDP increased by 4.2% (at currentprices) on 2009. However, annual chain-linked figures for 2010 indicate thatGDP growth remains well below levels registered prior to the recession.

Table 1.1: UK Gross Domestic Product at Current and AnnualChain-Linked Prices (£m), 2006-2010

2006 2007 2008 2009 2010

Current prices 1,328,363 1,404,845 1,445,580 1,394,989 1,453,616

% changeyear-on-year - 5.8 2.9 -3.5 4.2

Annual chain-linkedGDP 1,328,363 1,364,029 1,363,139 1,296,689 1,312,911

% changeyear-on-year - 2.7 -0.1 -4.9 1.3

GDP — gross domestic product

Source: Economic & Labour Market Review, May 2011, National Statistics website© Crown copyright material is reproduced with the permission of the Controllerof HMSO (and the Queen’s Printer for Scotland)

Inflation

UK inflation rose gradually in the years leading up to 2007, before droppingby 0.3 percentage points in 2008. By the end of 2009, despite the high price ofa number of commodities, including fuel, clothing and certain foods, inflationturned negative. However, it has since started to rise sharply, with the latestNational Statistics figures placing it at 4.6%, more than twice that of the Bankof England’s target of 2%. This sharp hike in inflation has been buoyed in partby the rise in VAT which came into effect in January 2011.

Toiletries Market Definition

© Key Note Ltd 2011 4

Table 1.2: UK Rate of Inflation (%), 2006-2010

2006 2007 2008 2009 2010

Inflation (%) 3.2 4.3 4.0 -0.5 4.6

Percentage point changeyear-on-year - 1.1 -0.3 -4.5 5.1

Note: inflation is at retail price index (RPI).

Source: Focus on Consumer Price Indices — Data for April 2011, published May2011, National Statistics website © Crown copyright material is reproduced withthe permission of the Controller of HMSO (and the Queen’s Printer for Scotland)

Household Disposable Income

Despite the current economic downturn, household disposable income percapita continued to increase year-on-year of approximately 3% over the reviewperiod, although growth in this measure slowed markedly to around 1.7% in2009. Rising household disposable income should, under normal circumstances,help to encourage consumer spending. However, since the recession, consumerconfidence has remained low and is likely to continue to do so as theGovernment’s proposed cuts to the public sector come into force.

Table 1.3: UK Household Disposable Income Per Capita (£),2006-2010

2006 2007 2008 2009 2010

Household disposableincome (£) 14,080 14,453 14,976 15,225 15,676

% change year-on-year - 2.6 3.6 1.7 3.0

Source: Economic & Labour Market Review, May 2011, National Statistics website© Crown copyright material is reproduced with the permission of the Controllerof HMSO (and the Queen’s Printer for Scotland)

Toiletries Market Definition

© Key Note Ltd 2011 5

Population

According to the Office for National Statistics, the UK’s population is currentlygrowing at an average annual rate of around 0.6% to 0.7% a year. At this rate,it is expected the 65 million-barrier will be exceeded by 2017. A growingpopulation is likely to contribute to an increase in consumer spending, whichin turn, will benefit the toiletries market.

Table 1.4: UK Resident Population Estimates by Sex (000),Mid-Years 2006-2010

2006 2007 2008 2009 †2010

Female 30,895 31,068 31,244 31,418 31,614

Male 29,689 29,918 30,154 30,374 30,609

Total 60,584 60,986 61,398 61,792 ‡62,222

% changeyear-on-year - 0.7 0.7 0.6 0.7

† — taken from Population Projections Database

‡ — does not sum due to rounding at source

Source: Time Series Data — Monthly Digest of Statistics (accessed June 2011)/Population Projections Database (2008-based projections), National Statisticswebsite © Crown copyright material is reproduced with the permission of theController of HMSO (and the Queen’s Printer for Scotland)

Unemployment

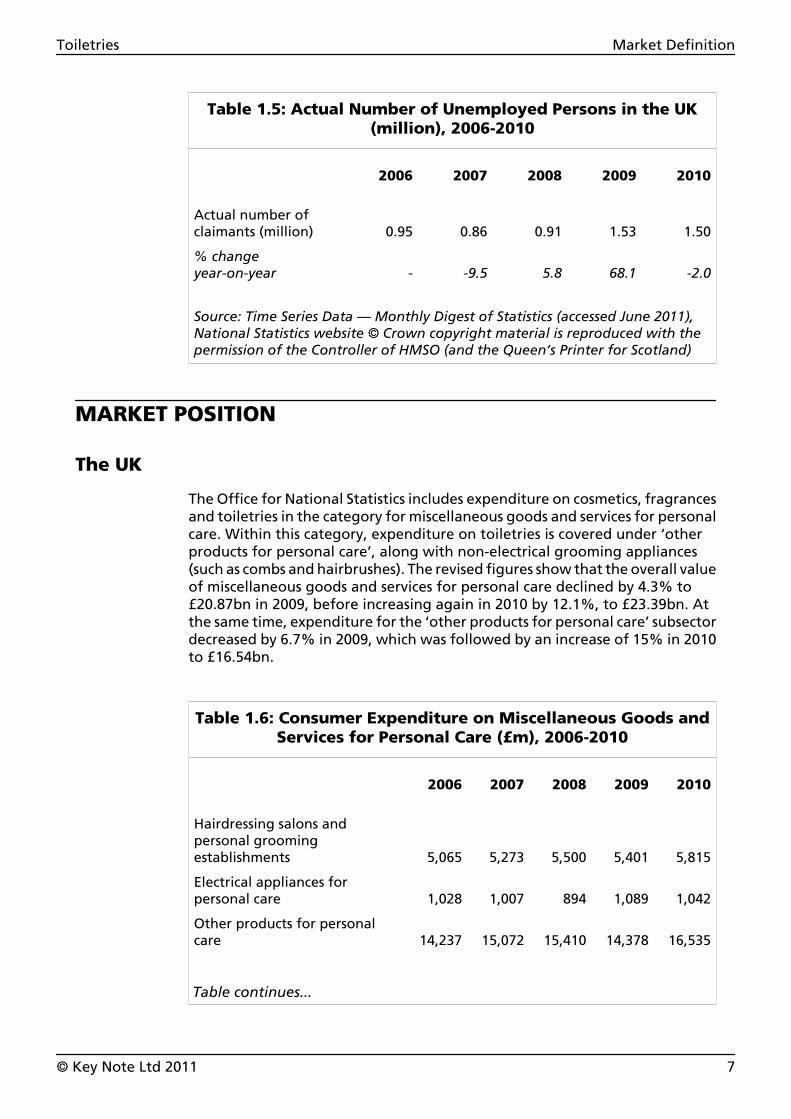

In 2004, the number of people unemployed in the UK stood at 850,000 — itslowest level in over a decade. This remained at a comparable level up until2007. Starting in March 2008, however, the economic downturn beganaffecting the labour market, sending UK unemployment figures rising. Theclaimant count reached 1 million in October 2008 and rose to a 13-year highof 1.53 million in 2009, before decreasing again in 2010. The latest figurespublished by National Statistics suggest that the number of peopleunemployed in the UK currently stands at 2.5 million. This figure is likely toincrease in the first half of 2011 as public sector cuts come into effect.

Toiletries Market Definition

© Key Note Ltd 2011 6

Table 1.5: Actual Number of Unemployed Persons in the UK(million), 2006-2010

2006 2007 2008 2009 2010

Actual number ofclaimants (million) 0.95 0.86 0.91 1.53 1.50

% changeyear-on-year - -9.5 5.8 68.1 -2.0

Source: Time Series Data — Monthly Digest of Statistics (accessed June 2011),National Statistics website © Crown copyright material is reproduced with thepermission of the Controller of HMSO (and the Queen’s Printer for Scotland)

MARKET POSITION

The UK

The Office for National Statistics includes expenditure on cosmetics, fragrancesand toiletries in the category for miscellaneous goods and services for personalcare. Within this category, expenditure on toiletries is covered under ‘otherproducts for personal care’, along with non-electrical grooming appliances(such as combs and hairbrushes). The revised figures show that the overall valueof miscellaneous goods and services for personal care declined by 4.3% to£20.87bn in 2009, before increasing again in 2010 by 12.1%, to £23.39bn. Atthe same time, expenditure for the ‘other products for personal care’ subsectordecreased by 6.7% in 2009, which was followed by an increase of 15% in 2010to £16.54bn.

Table 1.6: Consumer Expenditure on Miscellaneous Goods andServices for Personal Care (£m), 2006-2010

2006 2007 2008 2009 2010

Hairdressing salons andpersonal groomingestablishments 5,065 5,273 5,500 5,401 5,815

Electrical appliances forpersonal care 1,028 1,007 894 1,089 1,042

Other products for personalcare 14,237 15,072 15,410 14,378 16,535

Table continues...

Toiletries Market Definition

© Key Note Ltd 2011 7

Table 1.6: Consumer Expenditure on Miscellaneous Goods andServices for Personal Care (£m), 2006-2010

...table continued

2006 2007 2008 2009 2010

Total 20,330 21,352 21,804 20,868 23,392

% change year-on-year - 5.0 2.1 -4.3 12.1

Source: Consumer Trends 2010, National Statistics © Crown copyright material isreproduced with the permission of the Controller of HMSO (and the Queen’sPrinter for Scotland)

Overseas

According to the European Cosmetics Association (Colipa), the EU-27 marketfor cosmetics and fragrances including toiletries covered in this Key Note reportrepresents close to one-third of the global market. At retail prices, the marketwas valued at €69.5bn in 2009, marginally down — by 1.6% — from €70.6bnin 2008. The UK’s market was valued at €8.9bn, accounting for 12.8% of salesin the EU-27.

Toiletries Market Definition

© Key Note Ltd 2011 8

2. Market Size

THE TOTAL MARKET

Manufacturers’ Sales

According to the latest available figures from National Statistics, the value ofUK manufacturers’ sales of perfumes and toilet preparations (which coverscosmetics and perfumes, as well as products for personal care), was worth£2.25bn in 2009, having marginally declined — by 0.8% — from £2.27bn in2008. The value of manufacturers’ sales fell in most personal care productcategories, including shaving preparations, oral care, shampoos and skincareproducts.

Retail Sales

The total market for toiletries, as covered by this report, was valued at £4.53bnin 2010. Personal wash and bathroom toiletries make up the largest sector byvalue, accounting for 27.3% of the total. This is closely followed by skincareand hair care products, accounting for 27.1% and 24.8%, respectively in 2010.

Table 2.1: The Total UK Market for Toiletries by Sector by Valueat Current Prices (£m at rsp), 2006-2010

2006 2007 2008 2009 2010

Personal wash andbathroom toiletries 1170.0 1172.0 1175.0 1212.0 1237.0

Skincare products 978.0 1060.0 1140.0 1196.9 1229.0

Hair care products 1100.5 1106.5 1118.0 1120.0 1123.0

Oral care products 545.0 549.5 557.0 559.0 562.6

Shaving preparations,wet razors and blades,and depilatories 378.0 380.5 385.0 378.0 381.3

Total 4171.5 4268.5 4375.0 4465.9 4532.9

% change year-on-year - 2.3 2.5 2.1 1.5

rsp — retail selling prices

Source: Key Note

Toiletries Market Size

© Key Note Ltd 2011 9

Figure 2.1: The Total UK Market for Toiletries by Value atCurrent Prices (£m at rsp), 2006-2010

20062007

20082009

2010

3,000

3,250

3,500

3,750

4,000

4,250

4,500

4,750

5,000

rsp — retail selling prices

Source: Key Note

BY MARKET SECTOR

Figure 2.2 displays the market share percentage attributed to each sectorfeatured in this Key Note Market Report Plus.

Toiletries Market Size

© Key Note Ltd 2011 10

Figure 2.2: The Total UK Toiletries Market by Sector Share (%),2010

Shaving preparations,

wet razors and blades,

and depilatories

8.4%

Oral care products

12.4%

Hair care products

24.8%

Personal wash and bathroom toiletries

27.3%

Skincare products

27.1%

Source: Key Note

Personal Wash and Bathroom Toiletries

As shown in Table 2.2, the total value for personal wash and bathroomtoiletries increased by an estimated 2.1% from £1.21bn in 2009 to £1.24bn in2010. Although household penetration of personal wash and bathroomtoiletries remains high, potential value growth is restricted due to theprevalence of discounting. Moreover, retailers’ own brands are increasinglygaining market share over more expensive brands, as consumers are likely totrade down to less expensive products in the current economic climate.Notably, however, deodorants outperformed the sector as a whole, with salesincreasing in value by an estimated 3.8%. Continuing economic recovery, albeitslow, should see less discounting and returning consumer confidence.

Toiletries Market Size

© Key Note Ltd 2011 11

Table 2.2: The UK Personal Wash and Bathroom Toiletries Sectorby Subsector by Value at Current Prices (£m at rsp),

2009 and 2010

2009 2010% Change2009-2010

Bath/shower soaps, gels, additives andtalcum powder 690.0 695.0 0.7

Deodorants 522.0 542.0 3.8

Total 1,212.0 1,237.0 2.1

rsp — retail selling prices

Source: Key Note

Skincare Products

The market for skincare products, including sun care, was valued at £1.23bn in2010, an increase of 2.7% from the previous year. Growth in this marketcontinues to be driven by premium-priced products with anti-ageingformulations.

Table 2.3: The UK Skincare Products Sector by Subsector byValue at Current Prices (£m at rsp), 2009 and 2010

2009 2010% Change2009-2010

Facial skincare 680.0 702.0 3.2

Hand and body skincare 316.0 324.0 2.5

Suncare 200.9 203.0 1.0

Total 1,196.9 1,229.0 2.7

rsp — retail selling prices

Source: Key Note

Toiletries Market Size

© Key Note Ltd 2011 12

Hair Care Products

The value of the market for hair care products in 2010 increased by a marginal0.3%, from £1.12bn in 2009. The colourants and enhancers sector showed thestrongest growth with 1.3%, followed by conditioners with 0.8%. By contrast,sales of hairsprays and other styling aids decreased. The largest sector in thismarket segment is formed by shampoo, which accounts for just under a third(32.5%) of the total value of hair care products. This subsector is, however,another which is subject to heavy discounting, thereby restricting valuegrowth.

Table 2.4: The UK Hair Care Products Sector by Subsector byValue at Current Prices (£m at rsp), 2009 and 2010

2009 2010% Change2009-2010

Shampoo 364.0 365.2 0.3

Conditioners 238.0 240.0 0.8

Colourants and enhancers 221.0 223.8 1.3

Hairsprays 131.0 130.0 -0.8

Other styling aids 166.0 164.0 -1.2

Total 1,120.0 1,123.0 0.3

rsp — retail selling prices

Source: Key Note

Oral Care Products

Oral care products accounted for 12.4% of the toiletries market in 2010, saleshaving increased in value by a marginal 0.6%, to £562.6m. Householdpenetration of oral care products is high (see Chapter 7 — Buying Behaviour),and volume sales are helped by a growing population. It is, however, anothersector in which special price promotions are frequent, thereby keeping a checkon value growth.

Toiletries Market Size

© Key Note Ltd 2011 13

Table 2.5: The UK Oral Care Products Sector by Subsector byValue at Current Prices (£m at rsp), 2009 and 2010

2009 2010% Change2009-2010

Toothpaste, mouthwashes, etc. 425.0 428.6 0.8

Toothbrushes 134.0 134.0 0.0

Total 559.0 562.6 0.6

rsp — retail selling prices

Source: Key Note

Shaving Products

Shaving products account for the remaining 8.4% of the toiletries market andthis sector was worth an estimated £381.3m in 2010. The men’s sector has beendriven by new product innovation in recent years, although this trend notablyreversed during the economic downturn, as cost-conscious consumersincreasingly looked for less expensive — yet still high quality — alternatives.The sector experienced an increase in value of just under 1% in 2010,amounting to £381.3m.

Table 2.6: The UK Shaving Products Sector by Subsector byValue at Current Prices (£m at rsp), 2009 and 2010

2009 2010% Change2009-2010

Shaving preparations 88.0 89.0 1.1

Razors, blades and depilatories 290.0 292.3 0.8

Total 378.0 381.3 0.9

rsp — retail selling prices

Source: Key Note

Toiletries Market Size

© Key Note Ltd 2011 14

OVERSEAS TRADE

The UK has had a favourable trade balance in toiletries in the 3 years between2008 and 201, exporting a greater value than is imported. However, the tradebalance for 2010 decreased by 29.3% from £295.3m in 2009 to £208.7m in 2010.

Table 2.7: UK Imports and Exports of Toiletries by Value (£000),2008-2010

2008 2009 2010

Exports 1,012,512.0 1,097,203.3 1,045,949.3

Less imports 742,723.9 801,950.7 837,297.4

Balance of trade 269,788.1 295,252.6 208,651.9

Source: HM Revenue & Customs © Crown copyright material is reproduced withpermission of the Controller of HMSO (and the Queen’s Printer for Scotland)

Imports

Imports of toiletries from within the EU accounted for 76% of the value of totalUK imports of toiletries in 2010 (see Table 2.8). Hair care products representedthe highest-value category, accounting for 44.4% of total imports.Interestingly, this is one of only two sectors for which the cost of importsexceeded the value of exports, the other sector being perfumed bath salts andother bath preparations. The EU was the biggest source of imports in almostall sectors, with the exception of toilet soap. The UK’s main European sourcesof toiletries are Germany, France and Italy; while non-EU suppliers includeNorth America, the People’s Republic of China (PRC) and India.

Toiletries Market Size

© Key Note Ltd 2011 15

Table 2.8: UK Intra-EU Arrivals and Extra-EU Imports ofToiletries by Category by Value (£000), 2010

Intra-EU Extra-EU Total

Preparations for the hair 282,181.8 94,807.5 376,989.3

Preparations for oral or dental hygiene 106,394.7 26,718.5 133,113.2

Personal deodorants and anti-perspirants 104,259.5 11,124.6 115,384.1

Perfumed bath salts and other bathpreparations 40,226.4 15,396.3 55,622.7

Toilet soap 29,738.0 31,462.8 61,200.8

Pre-shave, shaving and after-shavepreparations 46,483.8 6,064.8 52,548.6

Depilatories and perfumery, cosmetic ortoilet preparations not elsewherespecified 26,753.6 15,685.1 42,438.7

Total 636,037.8 201,259.6 837,297.4

Source: HM Revenue & Customs © Crown copyright material is reproduced withpermission of the Controller of HMSO (and the Queen’s Printer for Scotland)

Exports

EU countries were the principal destinations for UK exports of toiletries,accounting for 70.1% of total exports in 2010, compared with 74.1% in 2009.The Netherlands, the Republic of Ireland (RoI), Germany, France, and Spainwere the most important EU destinations for UK exports of toiletries, whilenon-EU markets include North America, Russia, Australia and the United ArabEmirates.

Toiletries Market Size

© Key Note Ltd 2011 16

Table 2.9: UK Intra-EU Despatches and Extra-EU Exports ofToiletries by Category by Value (£000), 2010

Intra-EU Extra-EU Total

Preparations for the hair 208,637.7 62,838.8 271,476.5

Preparations for oral or dentalhygiene 170,349 57,544.1 227,893.1

Personal deodorants andanti-perspirants 173,600 45,971.3 219,571.3

Perfumed bath salts and otherbath preparations 30,634.6 14,183.7 44,818.3

Toilet soap 41,642.0 33,668.7 75,310.7

Pre-shave, shaving andafter-shave preparations 80,880.7 47,500.5 128,381.2

Depilatories and perfumery,cosmetic or toilet preparationsNES 27,177.5 51,320.7 78,498.2

Total 732,921.5 313,027.8 1,045,949.3

Source: HM Revenue & Customs © Crown copyright material is reproduced withpermission of the Controller of HMSO (and the Queen’s Printer for Scotland)

Toiletries Market Size

© Key Note Ltd 2011 17

3. Industry Background

RECENT HISTORY

The use of some form of personal care products can be traced back thousandsof years, and usage is evident in almost every society. Throughout time, peoplehave striven to make the most of their appearance with feature-enhancingpastes and dyes — such as henna — and perfumed oil, which was frequentlyused by the wealthy as a means to mask body odours.

By the 1970s, mounting pressure from environmentalists and animal-rightsactivists marked the beginning of closer scrutiny of industry practices. Despitestringent regulation, such as the European Cosmetics Directive of 1976 and theCosmetic Products (Safety) Regulations of 1996, as well as assurances fromindustry members, animal testing scandals still arise. Toiletries that areformulated using natural, plant-based ingredients have become the preferredchoice of many customers; this trend is exemplified by the success of The BodyShop International over the past couple of decades.

NUMBER OF COMPANIES

In 2010, according to UK Business: Activity, Size and Location, there were 320VAT- and/or PAYE-based enterprises involved in the manufacturing ofperfumes and toilet preparations. 46.9% of these had a turnover of more than£250,000, while nearly one third (29.7%) of these companies turned over £1mor more.

Table 3.1: Number of UK VAT- and/or PAYE-Based EnterprisesEngaged in the Manufacture of Perfumes and Toilet

Preparations by Turnover Sizeband, 2010

Number of Enterprises

Turnover Sizeband (£000)

0-49 55

50-99 60

100-249 55

250-499 30

500-999 25

Table continues...

Toiletries Industry Background

© Key Note Ltd 2011 18

Table 3.1: Number of UK VAT- and/or PAYE-Based EnterprisesEngaged in the Manufacture of Perfumes and Toilet

Preparations by Turnover Sizeband, 2010

...table continued

Number of Enterprises

Turnover Sizeband (£000)

1,000-4,999 55

5,000+ 40

Total 320

Source: UK Business: Activity, Size and Location, National Statistics website ©Crown copyright material is reproduced with the permission of the Controller ofHMSO (and the Queen’s Printer for Scotland)

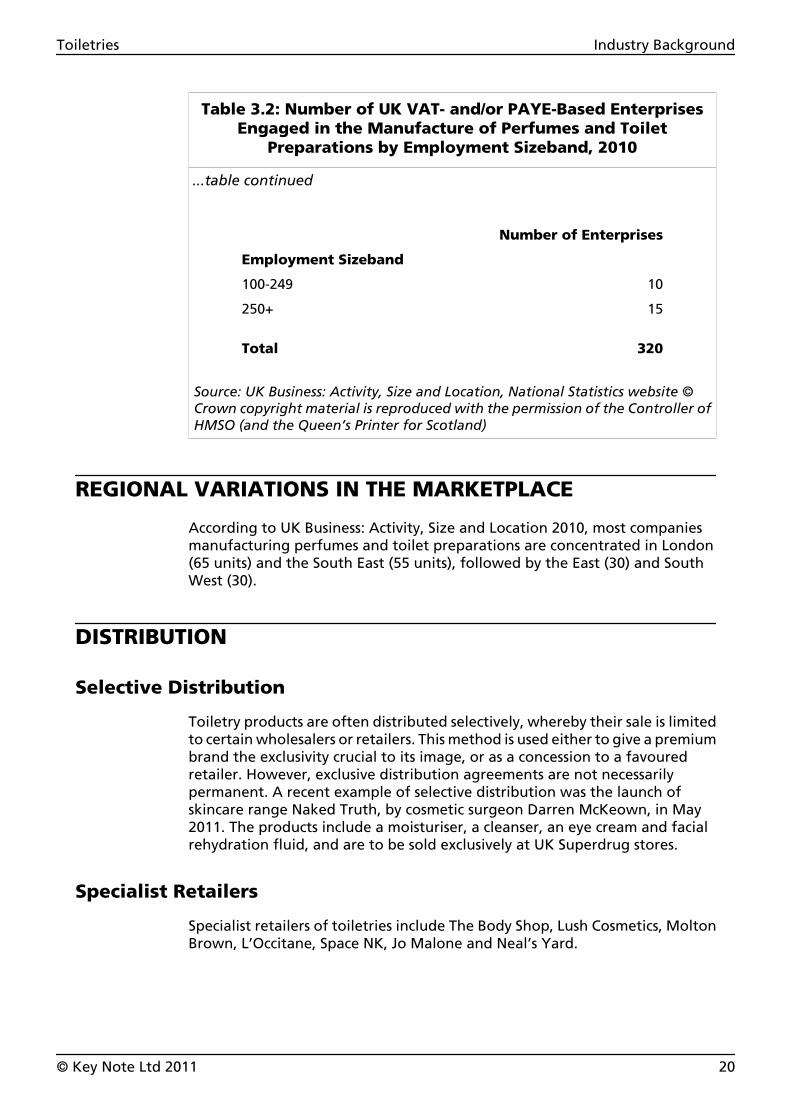

EMPLOYMENT

Table 3.2 shows the same number of UK VAT- and/or PAYE-based enterprisesthat in 2010 were involved in the manufacturing of perfumes and toiletpreparations, this time separated by employment sizeband. As can be seen,most are small enterprises, with nearly two-third (70.3%) of companiesemploying fewer than ten people and more than half (57.8%) of companiesemploying fewer than five.

Table 3.2: Number of UK VAT- and/or PAYE-Based EnterprisesEngaged in the Manufacture of Perfumes and Toilet

Preparations by Employment Sizeband, 2010

Number of Enterprises

Employment Sizeband

0-4 185

5-9 40

10-19 30

20-49 25

50-99 15

Table continues...

Toiletries Industry Background

© Key Note Ltd 2011 19

Table 3.2: Number of UK VAT- and/or PAYE-Based EnterprisesEngaged in the Manufacture of Perfumes and Toilet

Preparations by Employment Sizeband, 2010

...table continued

Number of Enterprises

Employment Sizeband

100-249 10

250+ 15

Total 320

Source: UK Business: Activity, Size and Location, National Statistics website ©Crown copyright material is reproduced with the permission of the Controller ofHMSO (and the Queen’s Printer for Scotland)

REGIONAL VARIATIONS IN THE MARKETPLACE

According to UK Business: Activity, Size and Location 2010, most companiesmanufacturing perfumes and toilet preparations are concentrated in London(65 units) and the South East (55 units), followed by the East (30) and SouthWest (30).

DISTRIBUTION

Selective Distribution

Toiletry products are often distributed selectively, whereby their sale is limitedto certain wholesalers or retailers. This method is used either to give a premiumbrand the exclusivity crucial to its image, or as a concession to a favouredretailer. However, exclusive distribution agreements are not necessarilypermanent. A recent example of selective distribution was the launch ofskincare range Naked Truth, by cosmetic surgeon Darren McKeown, in May2011. The products include a moisturiser, a cleanser, an eye cream and facialrehydration fluid, and are to be sold exclusively at UK Superdrug stores.

Specialist Retailers

Specialist retailers of toiletries include The Body Shop, Lush Cosmetics, MoltonBrown, L’Occitane, Space NK, Jo Malone and Neal’s Yard.

Toiletries Industry Background

© Key Note Ltd 2011 20

High-Street Stores

Health and beauty chains Boots and Superdrug are the leading high-streetstores, both selling a wide range of personal care products. Others includeLloyds Pharmacy, along with a number of smaller chains and independentstores.

Department Stores

Department stores, such as Debenhams, House of Fraser, Harrods, HarveyNichols, Selfridges and John Lewis, offer a range of branded as well asown-brand cosmetics and toiletries. Many stores also house concessions forbrands such as Molton Brown and L’Occitane.

Supermarkets

The supermarkets continue their expansion into the health and beauty sectorby offering products at discounted prices. Major UK supermarkets such asTesco, ASDA, Sainsbury’s, Morrisons and Waitrose also stock their own-brandtoiletry ranges, all sold at reasonable prices. It is the involvement of thesupermarkets and the price wars between them and other main competitors,that do much to keep down the value of sales of everyday toiletries.

Direct Selling

Avon is a prime example of the direct selling of cosmetics and fragrances, whichis carried out both online and through representatives. The Body Shop alsostarted its own ‘Body Shop at Home’ party plan, which offers 25% commissionto its sales representatives. VIE At Home is another company that specialises indirect selling of cosmetics, skincare and body care products in the UK. VIE AtHome was launched in 1996 and has more than 10,000 sales representatives.

HOW ROBUST IS THE MARKET?

The toiletries market was not impacted nearly as much by the global recessionas, for instance, the construction and property markets. Sales of toiletryproducts remained strong during the economic downturn as many of theseitems, such as shampoos, shower gels and deodorants, etc., are regarded asnecessities (see Chapter 2 — Market Size, and Chapter 7— Buying Behaviour).Nevertheless, there have been considerable changes in consumer behaviourand trends, predominantly in response to the ongoing economic uncertainty,rising energy and commodity prices, and a squeeze in households’ disposableincome. Combined, these factors are prompting consumers to adjust theirpriorities and spending habits. Consumers today are more likely to trade downto value products in order to save money, while others may view toiletryproducts as ‘feel good’ indulgences and stay loyal to their favourite brands. Intrading down, some consumers will be selecting premium products as analternative to salon beauty and spa treatments, effectively bringing new retailcustom to the toiletries market.

Toiletries Industry Background

© Key Note Ltd 2011 21

LEGISLATION

Cosmetics Directive 1976

All cosmetic, toiletry and perfumery products placed on the market in the UK(and throughout the EU) are regulated by European legislation, namely theCosmetics Directive (76/768/EEC). The primary purpose of these laws is toprotect human safety. The manufacturer or supplier of the cosmetic product isresponsible for ensuring it is safe; each cosmetic must be assessed for safety bya duly qualified safety assessor before it can be made available to the public.The Directive covers the composition, manufacturing, safety assessment andlabelling of all cosmetics products. The Cosmetics Directive also controls whatmay or may not be put in a cosmetic. There are lists of substances that mustnot be present and lists of substances that may be used as ingredients subjectto particular restrictions.

Cosmetics Products Regulations

The legislation that regulates cosmetic products in the UK is the CosmeticProducts (Safety) Regulations 2008. The Regulations are based on theCosmetics Directive (76/768/EEC) and are updated periodically, reflectingchanges to prohibitions of, and restrictions on, certain substances, andsubsequent amendments to the Cosmetic Products (Safety) Regulations 2008.

The Cosmetic Products (Safety) Regulations 2008 came into force on18th June 2008 and consolidated earlier Regulations, as well as implementingcurrent European Directives. Under the Cosmetic Products (Safety) Regulations2008, all cosmetic products sold in the EU must display a complete ingredientslist. New products are required to undergo a full safety assessment before theyare allowed onto the market. Safety assessments need to be carried out byqualified professionals and must cover the finished product, all ingredients andhow products will be used.

In July 2013, the EU Cosmetics Directive will be replaced by the EU CosmeticsRegulation (1223/2009), which will apply directly in all EU Member States.

REACH

Also relating to the industry is the Registration, Evaluation & Authorisation ofChemicals (REACH), a European regulation concerning the safety of chemicals.In order to ensure a high level of protection, this regulation requires data tobe provided concerning human and environmental safety. It applies to allchemicals made in the EU or imported into the EU, including certain naturalsubstances and other substances used in cosmetic products. It is intended toaddress any public concern about the use of chemicals.

Toiletries Industry Background

© Key Note Ltd 2011 22

KEY TRADE ASSOCIATIONS

Cosmetic, Toiletry and Perfumery Association

Founded in 1945, the Cosmetic, Toiletry and Perfumery Association (CTPA) is atrade association providing a voice for the UK cosmetic, toiletry and perfumeryindustry. Its members vary from small- and medium-sized companies to largemulti-nationals and include manufacturers, raw material suppliers and serviceproviders. The Association co-ordinates the industry’s viewpoint on key issues,such as science, innovation and safety, and maintains an open dialogue withthe Government, both in the UK and in Europe, as well as with internationalregulatory authorities and key opinion formers.

The European Cosmetics Association

Established in 1962 in Brussels, the European Cosmetics Association (Colipa)aims to be the voice of Europe’s cosmetic, toiletry and perfumery industry. Itrepresents the interests of more than 2,000 companies, ranging from majorinternational cosmetics manufacturers to small family-run businessesoperating in niche markets. Together, these companies employ more than500,000 people within the EU. The products that fall within the scope of Colipaextend across a diverse range and include essential personal hygiene products,such as deodorant, shampoo and toothpaste, as well as beauty preparations.The Association assists its members with the ongoing development of safe,innovative and effective products, while also meeting the demands ofconsumers through intensive market research.

Toiletries Industry Background

© Key Note Ltd 2011 23

4. Competitor Analysis

THE MARKETPLACE

The manufacture of toiletries is currently dominated by a small number ofmultinational corporations, such as Unilever and Procter & Gamble (P&G),which also produce a wide range of consumer goods for other markets outsideof the toiletry industry. Other specialist companies include L’Oreal, PZ Cussons,Estee Lauder and number of smaller, niche operations. On the retail side,principle retailers of toiletries include Alliance Boots, Superdrug and thegrocery multiples such as Tesco, which sell a much wider range of consumergoods than just toiletries.

MARKET LEADERS — MANUFACTURERS

Avon Cosmetics Ltd

Company Structure

Avon Cosmetics Ltd is one of the world’s leading direct sellers of beauty andrelated products, marketing to women in more than 100 countries throughapproximately 6.5 million independent sales representatives. Having enteredthe UK market in 1959, the company claims to be one of the top three beautybrands in the country today. The company’s head office is located inNorthampton and supports operations in both the UK and European market.

Current and Future Developments

In March 2011, over 5,000 independent Avon representatives joined AvonChairman and CEO Andrea Jung at a concert in Birmingham to mark Avon’s125th anniversary. In May, Avon Cosmetics Ltd was crowned the winner of theEnvironmental Award at the Direct Selling Association (DSA) Conference.

Financial Results

In the year ending 31st December 2009, Avon Cosmetics Ltd registered aturnover of £316.6m, a decrease of 0.6% from £318.6m in the previous year.Its pre-tax profit dropped significantly, from £20.6m to a loss of £7.1m over thesame period.

Toiletries Competitor Analysis

© Key Note Ltd 2011 24

Estée Lauder Cosmetics Ltd

Company Structure