topic 1: introduction to cost accountingocw.uniovi.es/pluginfile.php/5635/mod_resource... · 1.1:...

TRANSCRIPT

Ana Mª Arias Alvarez (University of Oviedo) Introduction to Cost Accounting OpenCourseWare

Topic 1:

Introduction to Cost Accounting

Ana Mª Arias Alvarez

University of OviedoDepartment of Accounting

School of Business AdministrationCourse: Cost Accounting and Management Control

Bachelor’s Degree in Management and Business Administration

Ana Mª Arias Alvarez (University of Oviedo) Introduction to Cost Accounting OpenCourseWare2/18

1.1. Cost Accounting as a source of information forinternal parties within the organization.

1.2. Costs and cost terminology.1.3. Classifications of costs.1.4. Relevant and irrelevant costs.

Ana Mª Arias Alvarez (University of Oviedo) Introduction to Cost Accounting OpenCourseWare

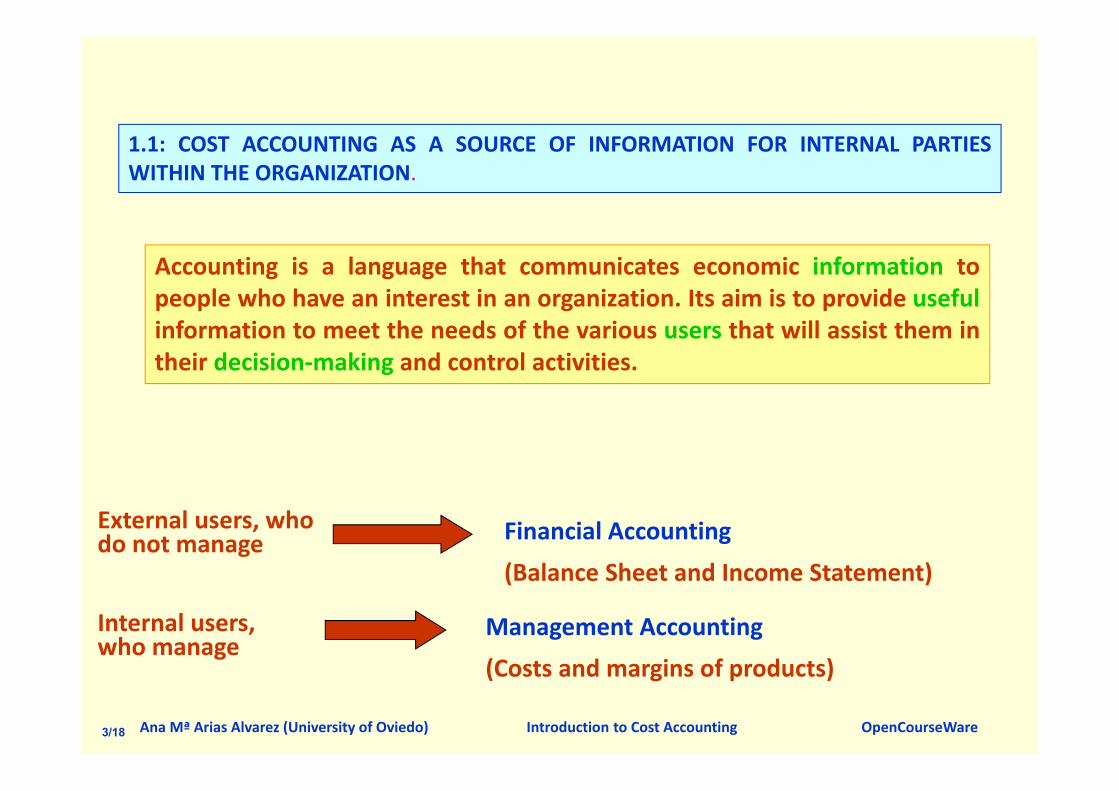

1.1: COST ACCOUNTING AS A SOURCE OF INFORMATION FOR INTERNAL PARTIESWITHIN THE ORGANIZATION.

Accounting is a language that communicates economic information topeople who have an interest in an organization. Its aim is to provide usefulinformation to meet the needs of the various users that will assist them intheir decision‐making and control activities.

External users, who do not manage

Internal users, who manage

Financial Accounting(Balance Sheet and Income Statement)

Management Accounting(Costs and margins of products)

3/18

Ana Mª Arias Alvarez (University of Oviedo) Introduction to Cost Accounting OpenCourseWare

EXTERNAL INCOME STATEMENT

Revenue 4,000– Raw materials used – 1,400– Personnel expenses – 500– Other operating expenses – 1,700RESULTS FROM OPERATING ACTIVITIES 400– Finance expenses – 200PROFIT BEFORE INCOME TAX 200 > 0

4/18

Ana Mª Arias Alvarez (University of Oviedo) Introduction to Cost Accounting OpenCourseWare

INTERNAL INCOME STATEMENT

CONCEPT TOTAL PRODUCT A PRODUCT B

Revenue 4,000 2,400 1,600

– Cost of goods sold – 3,400 – 2,500 – 900

Gross profit 600 ‐ 100 < 0 700 > 0

– Administration costs – 200

– Financial costs – 200

Net profit 200 > 0

5/18

Ana Mª Arias Alvarez (University of Oviedo) Introduction to Cost Accounting OpenCourseWare

MANAGEMENT ACCOUNTING

The branch of Accounting concerned with providing information to peoplewithin the organization to help them make better decisions and improvethe efficiency and effectiveness of existing operations:

• Measures and analyses those costs associated with producing goods andservices. It also measures performance and productivity.

•Measures and analyses those costs associated with the company’scentres in order to evaluate their performance.

6/18

Ana Mª Arias Alvarez (University of Oviedo) Introduction to Cost Accounting OpenCourseWare

1.2: COSTS AND COST TERMINOLOGY.

COST MEASURES THE ECONOMIC SACRIFICE

MADE TO ACHIEVE AN ORGANIZATION’S GOAL.

COSTQUANTITY

PRICE

x

7/18

Ana Mª Arias Alvarez (University of Oviedo) Introduction to Cost Accounting OpenCourseWare

DIRECT COSTS

INDIRECT COSTS

They can be specifically and exclusively identified with a particular cost object.

They cannot be identified specifically and exclusively with a given cost object.

COST OBJECT: Any activity for which a separate measurement of costs is necessary.

1.3: CLASSIFICATIONS OF COSTS.

1.3.1: DIRECT AND INDIRECT COSTS.

8/18

Ana Mª Arias Alvarez (University of Oviedo) Introduction to Cost Accounting OpenCourseWare

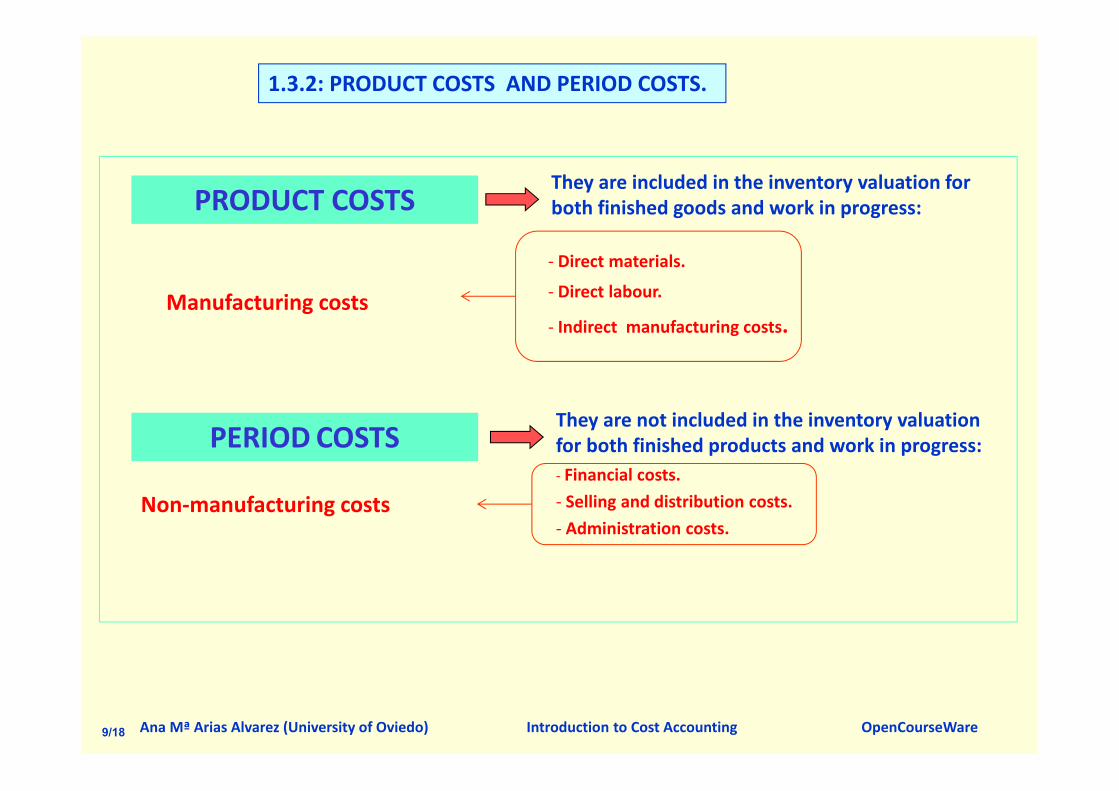

1.3.2: PRODUCT COSTS AND PERIOD COSTS.

PRODUCT COSTS

PERIOD COSTS

They are included in the inventory valuation for both finished goods and work in progress:

They are not included in the inventory valuation for both finished products and work in progress:‐ Financial costs.‐ Selling and distribution costs.‐ Administration costs.

Manufacturing costs

Non‐manufacturing costs

‐ Direct materials.

‐ Direct labour.

‐ Indirect manufacturing costs.

9/18

Ana Mª Arias Alvarez (University of Oviedo) Introduction to Cost Accounting OpenCourseWare

Direct materials

Direct labour

TOTAL MANUFAC‐TURING COSTS

+/‐ BEGINNING/ ENDING

INVENTORIES WORK IN PROGRESS

COST OFGOODS

MANUFAC‐TURED

+/‐ BEGINNING/ ENDING

INVENTORIES FINISHED GOODS

COST OF GOODSSOLD

Financial

costs

Selling and distribution

costs

DIRECTOR

PRIMARY COST

Administration costs

Indirectcosts

COSTS

COST STRUCTURE:

10/18

Ana Mª Arias Alvarez (University of Oviedo) Introduction to Cost Accounting OpenCourseWare

Task: try to solve problem 1.1.

11/18

Ana Mª Arias Alvarez (University of Oviedo) Introduction to Cost Accounting OpenCourseWare

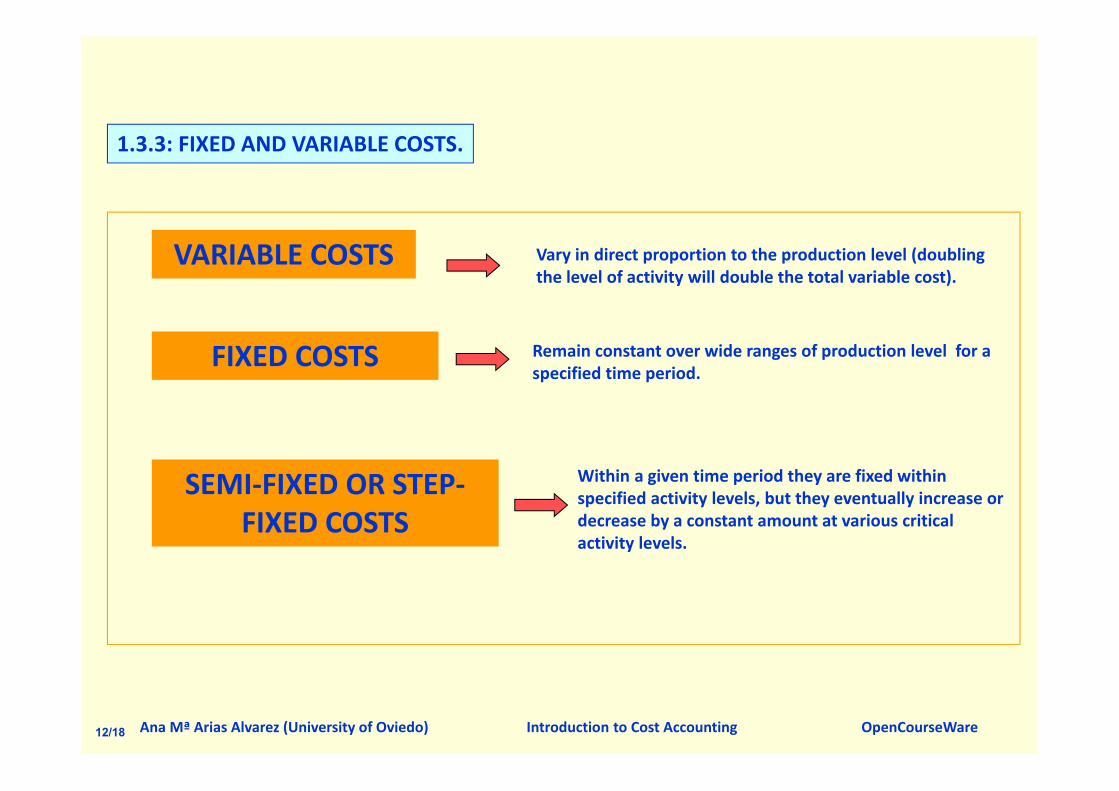

1.3.3: FIXED AND VARIABLE COSTS.

VARIABLE COSTS

FIXED COSTS

SEMI‐FIXED OR STEP‐FIXED COSTS

Vary in direct proportion to the production level (doubling the level of activity will double the total variable cost).

Remain constant over wide ranges of production level for a specified time period.

Within a given time period they are fixed within specified activity levels, but they eventually increase or decrease by a constant amount at various critical activity levels.

12/18

Ana Mª Arias Alvarez (University of Oviedo) Introduction to Cost Accounting OpenCourseWare

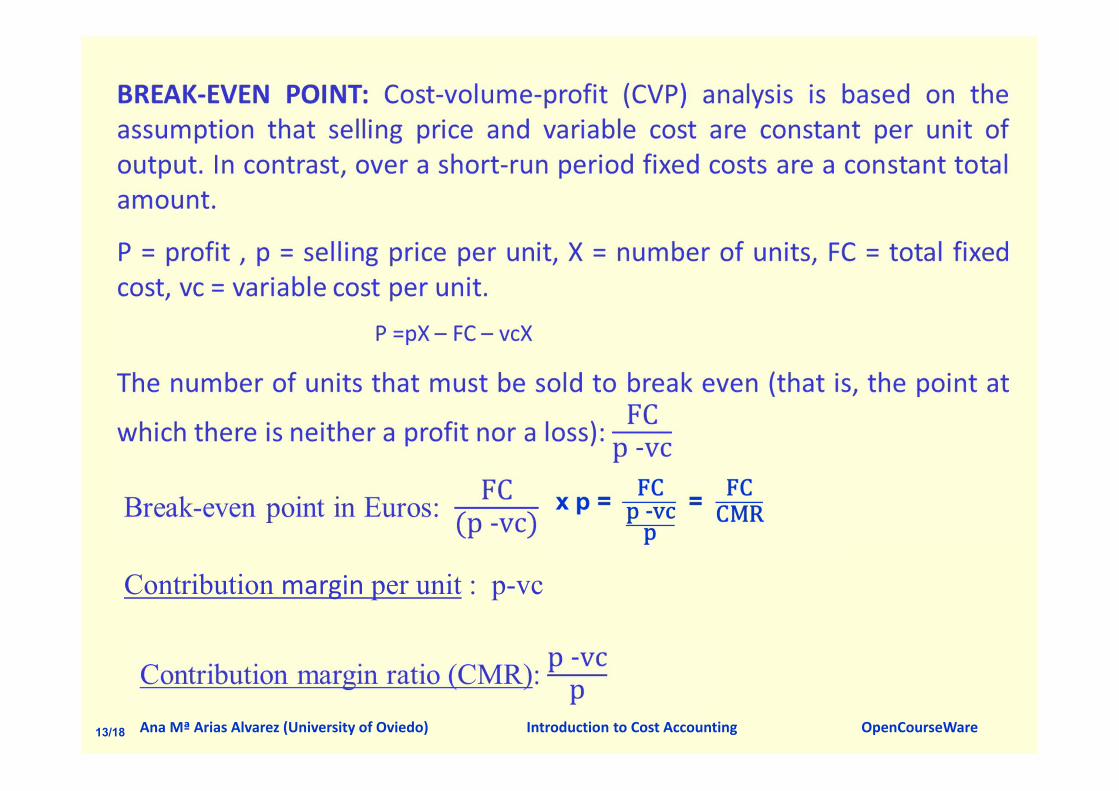

Contribution margin per unit : p-vc

13/18

Ana Mª Arias Alvarez (University of Oviedo) Introduction to Cost Accounting OpenCourseWare

FORNITURE Ltd. manufactures tables:

‐p = €150 per table (proposed selling price per table).

‐vc = €100 per table.

‐FC = €60,000 per month.

monthper tables,200 1 per table 100) - €(150

monthper 000 €60,pointeven Break

CONTRIBUTION MARGIN PER UNIT:

p – vc = 150 – 100 = €50 per table

14/18

Ana Mª Arias Alvarez (University of Oviedo) Introduction to Cost Accounting OpenCourseWare

Separation of costs into their fixed and variable elements

There are different techniques that can be used to separate costs in this way:

1. HIGH‐LOW METHOD: examining past costs and activity, selecting the highest andlowest activity levels and comparing the changes in costs that result from the twolevels. Assume that the following activity levels and costs are extracted:

Volume of production (units) Total costs (€)

Lowest activity 46 700

Highest activity 100 1,350

If variable costs are constant per unit and fixed costs remain unchanged, the increase in costs will be due entirely to an increase in variable costs:

1,350 – 700 = (100– 46) x vc

Variable cost per unit: €12.04 per unit

700 = (46 x 12.04) + FC

Fixed costs: €146.3015/18

Ana Mª Arias Alvarez (University of Oviedo) Introduction to Cost Accounting OpenCourseWare

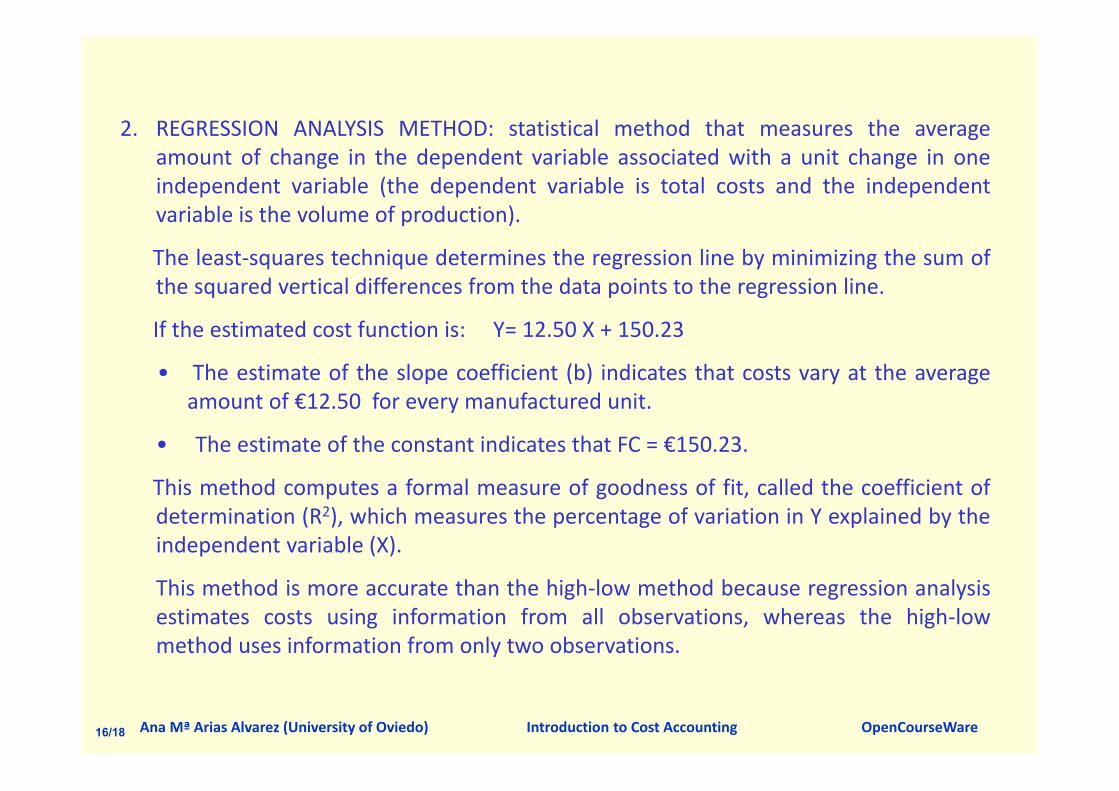

2. REGRESSION ANALYSIS METHOD: statistical method that measures the averageamount of change in the dependent variable associated with a unit change in oneindependent variable (the dependent variable is total costs and the independentvariable is the volume of production).

The least‐squares technique determines the regression line by minimizing the sum ofthe squared vertical differences from the data points to the regression line.

If the estimated cost function is: Y= 12.50 X + 150.23

• The estimate of the slope coefficient (b) indicates that costs vary at the averageamount of €12.50 for every manufactured unit.

• The estimate of the constant indicates that FC = €150.23.

This method computes a formal measure of goodness of fit, called the coefficient ofdetermination (R2), which measures the percentage of variation in Y explained by theindependent variable (X).

This method is more accurate than the high‐low method because regression analysisestimates costs using information from all observations, whereas the high‐lowmethod uses information from only two observations.

16/18

Ana Mª Arias Alvarez (University of Oviedo) Introduction to Cost Accounting OpenCourseWare

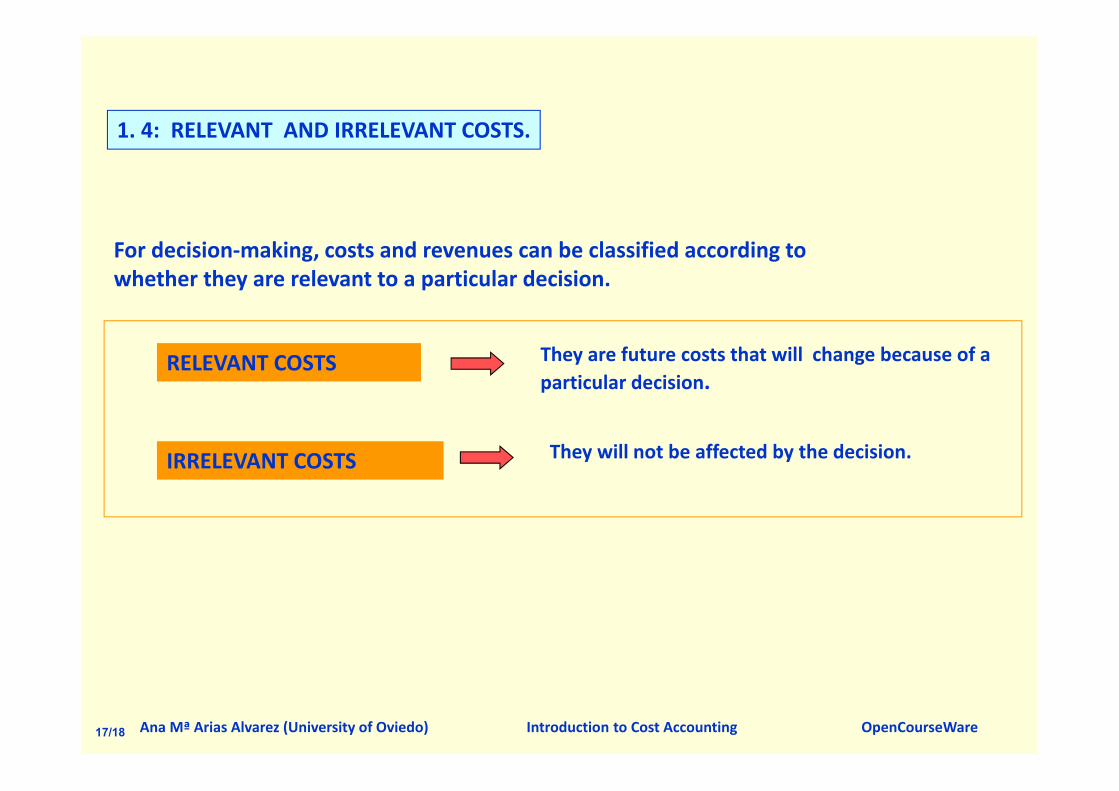

RELEVANT COSTS

IRRELEVANT COSTS

They are future costs that will change because of a particular decision.

They will not be affected by the decision.

For decision‐making, costs and revenues can be classified according to whether they are relevant to a particular decision.

1. 4: RELEVANT AND IRRELEVANT COSTS.

17/18

Ana Mª Arias Alvarez (University of Oviedo) Introduction to Cost Accounting OpenCourseWare

Task: try to solve problem 1.2.

18/18