topic 6: prudential control and regulation in banking

TRANSCRIPT

Topic 6: Prudential Control and Regulation in Banking

Lecture Outline

Arguments for prudential control / regulation

Problems with external prudential regulations

Prudential control and regulations in the UK, USA and BG

Regulation: Introduction

All companies have to ensure capital adequacy, and (banks in particular) have to also ensure sufficient liquidity.

Control is necessary due to two conflicting objectives:Profit - high to keep shareholders happy.Liquidity- low/high to earn profit/serve

better and insure depositors.

Introduction

Should prudential controls or regulation be compulsory?

Should these regulations be imposed by the state?

Should they be imposed by the bank management itself?Bank also has an interest in long-term survival.

Why Should we Regulate?

Protection of the public’s savings.

Control of the money supply.

Asymmetric information and vulnerability of depositors.

Why Should we Regulate?

Contagion (panic or domino) effects.

Bank’s ability to diversify assets.

Competition and excessive risk taking.

Problems with Regulation

Cost

CompetitionHampers competition and innovation.

Competence?Question mark over competence of

supervisor.

Complexity

Problems with Regulation

Moral hazard

Asymmetric information

Government GuaranteeDeposit insurance has ended risk of

systematic failure (?)

Capital adequacy Capital adequacy has ended credit risk (?)

A Case for Free Banking

The Scottish System (1716 – 1844).Banks allowed to enter the market w/o chartering

or licensing.

Results: intense competition, innovation and economic

growthsystem introduces branch banking, interest paid

on deposits, overdraft facilities and private deposit insurance.

Regulation in the UK: Pre-1979

No specific banking law in the UK

Private banks treated like any other commercial concern

Individual agents or firms could accept deposits without any formal licence.

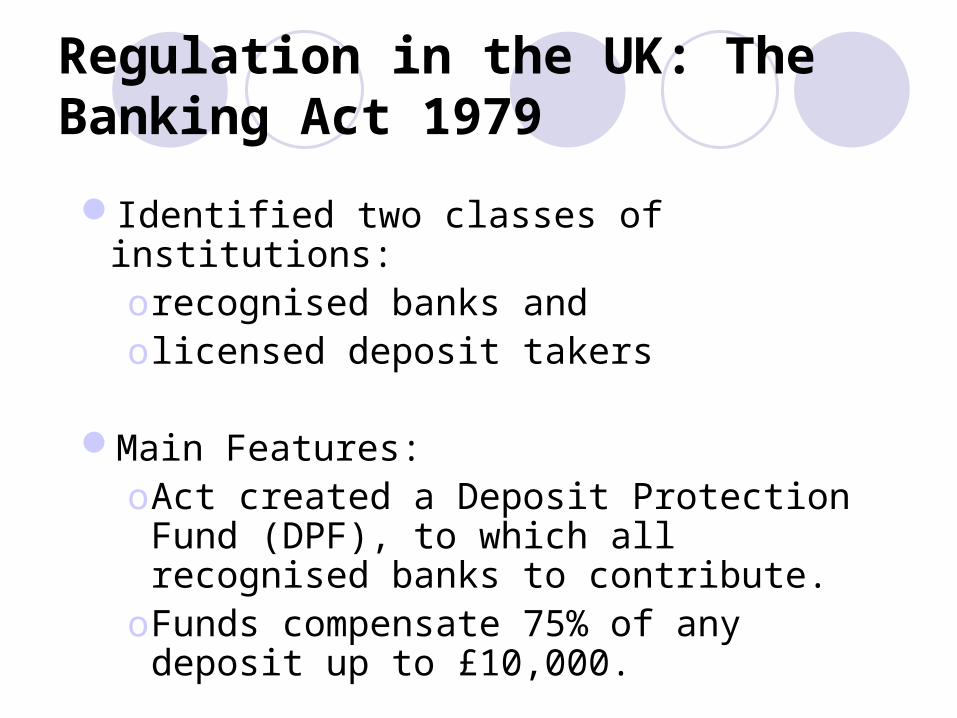

Regulation in the UK: The Banking Act 1979

Identified two classes of institutions:orecognised banks and olicensed deposit takers

Main Features:oAct created a Deposit Protection Fund

(DPF), to which all recognised banks to contribute.

oFunds compensate 75% of any deposit up to £10,000.

Regulation in the UK: 1987 Amendment

Collapse of Johnson Matthey Bank (JMB) paved the way for amendment to the 1979 Act.

Main Features:oCreated supervisory board headed by the

Governor of BOE.

oEliminated the distinction between deposit takers and banks.

1987 Amendment

Private auditors were given greater access to BOE information.

Exposure to a single borrower > 10% of banks capital reported to BOE. Supervisor consulted directly on any lending which exceeds 25% of bank capital to a single borrower.

Act also specified BOE control over the entry of foreign banks.

1987 Amendment

Act increased the deposit insurance limit to £20,000.

Under Act, BOE acts as a regulator.• The asset side of a bank balance sheet is

regulated through capital adequacy and liability side through liquidity adequacy.

1987 Amendment

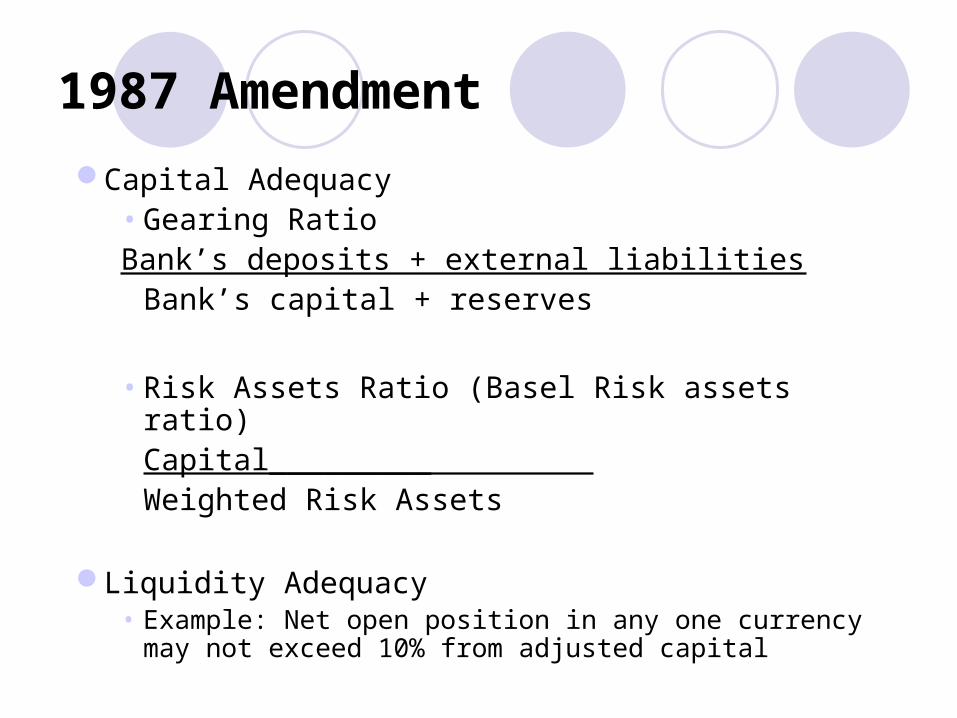

Capital Adequacy• Gearing RatioBank’s deposits + external liabilities

Bank’s capital + reserves

• Risk Assets Ratio (Basel Risk assets ratio)Capital_________

Weighted Risk Assets

Liquidity Adequacy• Example: Net open position in any one currency may not

exceed 10% from adjusted capital

Parallel regulations in BG

Main Regulator – the Bulgarian National BankBasic regulations:

Law on Bank Deposit Guarantee:• Last modified as of 31.12.2010• Amount secured: up to BGN 196.000• Exceptions:

Depositors with preferential terms Owners of shares entitling them with more than 5% of the

votes in General Meeting Members of the bank’s Management Board Auditors Own bank’s deposits

Parallel regulations in BG

Law on Bank Deposit Guarantee:• Managed by the Deposit Insurance Fund• The Fund is:

collecting entry and annual contributions from banks Investing the money in government bonds and/or

deposits in banks or the BNB• Contributions:

Entry contribution – 1% of bank’s capital, not less than BGN 100.000

Annual contribution – 0.5% of the total amount of the deposit base

Contributions are non-refundable

Parallel regulations in BG

Ordinance N8 on the Capital Adequacy

Capital Adequacy Ratio = Own Funds___Risk Weighted Assets

Own Funds = Tier One Capital + Tier Two Capital – specific investments in shares

Assets are granted specific weights according to their risk profile – 0%, 10%, 20%, 50% and 100%

The overall capital adequacy ratio may not be less than 12%

Tier One Capital adequacy ration may not be less than 6%

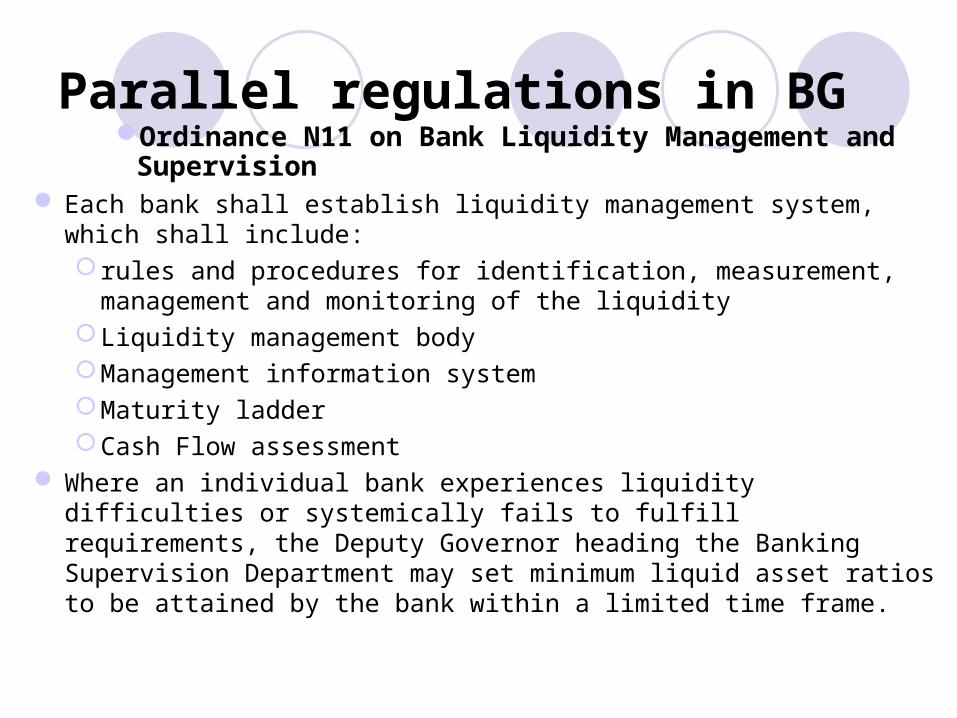

Parallel regulations in BGOrdinance N11 on Bank Liquidity Management and

Supervision Banks shall manage their liquidity in a manner that ensures they can

regularly and without delay meet their daily obligations, both in a normal banking environment and in a crisis situation.

Banks shall submit to the BNB monthly liquidity reports on a ‘going concern basis’ showing projected BGN cash flows and correspondingly the BGN equivalent of foreign currency-denominated assets and liabilities.

The Bulgarian National Bank shall monitor the amount and composition of banks’ liquid assets and, where appropriate, establish minimum liquidity ratios on a bank-by-bank basis

Parallel regulations in BGOrdinance N11 on Bank Liquidity Management and

Supervision Each bank shall establish liquidity management system, which shall

include: rules and procedures for identification, measurement, management

and monitoring of the liquidityLiquidity management bodyManagement information systemMaturity ladderCash Flow assessment

Where an individual bank experiences liquidity difficulties or systemically fails to fulfill requirements, the Deputy Governor heading the Banking Supervision Department may set minimum liquid asset ratios to be attained by the bank within a limited time frame.

USA Banking Regulation

Different to UK banking regulation:

Regularly turn to legislation to iron out perceived inefficiency

Protection of small depositors more important.Concern about potential collusion – ‘anti-trust’.

Regulatory Responsibility – The ‘FRS’

Federal Reserve - State ‘Member’ Banks

Controller of the Currency - National ‘Member’ Banks

FDIC examines the ‘Non-Member’ insured Banks.

Banks performance is monitored and assessed on a scale ranging from 1 to 5.

National Banking Act (1863,1864)

Passed during the civil war to help raise funding.

Created the treasury and the comptroller of the currency.

Created national banks with a Federal Charter.

Federal Reserve Act (1913)

Created the FRS

Created to provide a number of services to member banks. E.g. the authority to act as the lender of last

resort.

Today the FED controls the money supply and base interest rates.

You may remember…

McFadden-Pepper Act (1927)Prevented banks from expanding across state lines.Made national banks subject to the branching laws of their

state. International Banking Act (1978) tidied this up with respect

to international banks

Glass-Steagall Act (1933) Passed during the great depression.Separated investment and commercial banking.Created the FDIC.Fed given the power to set margin requirements.Prohibited interest to be paid on checking accounts.

US Banking Act (1933)

Created the FDIC membership compulsory for FRS membersNon-members can join if they meet admission

criteria

Members pay an annual insurance premium to the FDIC

FDIC purchases securities to provide a stream of funds (to cover deposits of up to $100,000).

Major USA Banking Regulation

FDIC Act 1935Gave the FDIC the power to examine banks

and take necessary action.Bank Merger Acts

All mergers must be approved by the appropriate regulating body.

Mergers must be evaluated in three areas:Effect on competition.Effect on the convenience and needs of the

community.Effect on the financial condition of the banks.

Bank Holding Company Act (1956)

Federal Reserve given the power to regulate bank holding companies

1966 Amendment reduced the tax burden of bank holding companies

1970 - Amended the definition of bank holding companies to include one-bank holding companies

Social Responsibility Acts

1968 – full information on terms of loans must be given.

1974 – cannot be denied a loan based on age, sex, race, national origin or religion.

1977 – cannot discriminate based on the neighborhood in which borrower resides.

1987 – banks must disclose full terms on deposit and savings accounts.

Riegle-Neal Act (1994)

Bank holding company can acquire banks nationwide.Consolidation of inter-state BHCs into branches.

Smaller well managed banks only need to be examined every 18 months.

Community development fund created to promote development of depressed local communities.

Gramm-Leach-Bliley Act (1999)

Permits banking-insurance-securities affiliations

Protections for consumers purchasing insurance through a bank.

Must disclose policies regarding the sharing of customers’ private information.Customers are allowed to ‘opt out’ of private

information sharing.

Conclusions

Regulation is a necessary tool for managing the modern bank and controlling risk exposure

o Drawbacks of Regulation – is the process necessary after all?

There are historical examples of free banking markets working to the advantage of society

o The Scottish Example

In the UK, we have observed a gradual shift in regulatory attitudes from relatively lax to relatively stringent.

o Particularly from 1978 (pre Banking Act) – 1987o However…….

Conclusions

There is a degree of contrast in terms of attitudes to regulation in the UK and USA

This is evidenced by the number of important regulations in each country

What about Germany?Follows EU regulation on Banking (See

Page 245-250 in Modern Banking in Theory and Practice)

Attitudes towards Universal Banking have helped shape EU policy