topics by ganiyu abiola aliyu project … abiola aliyu.pdfemergence of recession in the global ......

TRANSCRIPT

1

TOPICS BY

GANIYU ABIOLA ALIYU PG/MBA/08/53302

PROJECT SUBMITTED IN PARTIAL

FULFILLMENT FOR THE REQUIREMENTS FOR THE AWARD OF MASTERS OF

BUSINESS ADMINISTRATION (MBA) IN MARKETING

DEPARTMENT OF MARKETING, FACULITY

OF BUSINESS ADMINISTRATION UNIVERSITY

OF NIGERIA ENUGU CAMPUS.

SUPERVISOR: DR (MRS) G.E

UGWUONAH JANUARY 2011.

2

Certification This is to certify that this study has been approved and accepted by department of marketing in partial fulfillment for the award of masters of business administration (mba) in marketing. ……………………………. …………………………… Dr. (mrs) G.E ugwuonah date (project supervisor) …………………………….. …………………………… Dr. (mrs) J.O nnabuko) date (H.O.D marketing)

3

Dedication This research work is dedicated to God Almighty Allah for his mercies in my life

4

Acknowledgement

5

TABLE OF CONTENTS

Title Page == == == == == == == == == i

Certification Page == == == == == == == ii

Dedication == == == == == == == iii

Acknowledgement == == == == == == iv

Abstract == == == == == == == == == v

Table of Contents == == == == == == vi

List of Tables == == == == == == == == vii

CHAPTER ONE: INTRODUCTION

1.1 Background of the Study == == == == == 1

1.2 Statement of Problem == == == == 4

1.3 Objectives of the study == == == == == 5

1.4 Research Question == == == == == 6

1.5 Research Hypothesis == == == == 7

1.6 Significance of Study == == == == == 8

1.7 Limitations of the Study == == == == 9

1.8 Definition of Terms

References == == == == == == == 10

6

CHAPTER TWO: LITERATURE REVIEW

INTRODUCTION == == == == == == == 11

2.1 Overview of Banking Operations == == == 14

2.2 Bank Marketing Versus Goods Marketing == == 17

2.3 The Process of Bank Marketing == == == == 19

2.4.1 The History of First Bank of Nigeria == == == 25

2.4.2 History Pre-Independence == == == == 26

2.4.3 Post Independence == == == == == == 26

2.5.1 Society for World Wide Interbank Financial

Telecommunication (SWIFT) == == == == 28

2.5.2 On-Line/real time service == == == == 28

2.5.3 Home banking == == == == == == 28

2.5.4 First bank smart card scheme == == == 28

2.5.5 Other Customers Services == == == == 29

2.6 The Changing Market Stage of the Bank == == 29

References == == == == == == == 37

CHAPTER THREE: RESEARCH METHODOLOGY

3.0 Introduction == == == == == == == 34

7

3.1 Research Design == == == == == == 34

3.2 Research Hypotheses == == == == == 37

3.3 Characteristics of Population == == == == 39

3.4 Determination of Sample Size == == == == 39

3.5 Data Collection == == == == == == == 40

3.6 Location of Data == == == == == == 42

References == == == == == == == 44

CHAPTER ONE

INTRODUCTION

8

1.1 BACKGROUND OF THE STUDY

The continuing evolution of the banking and financial

markets has created opportunities both for providers and for

users of financial products, and this evolution has been

beneficial to the economy. However, innovations in financial

products also have given rise to some new challenges for

market participants and their supervisors in the areas of

corporate governance and compliance. The events of the past

few years demonstrate again that fraudulent conduct and

weak corporate governance at a few firms can dramatically

change the cost of capital and impose additional regulatory

burden on even well-managed organizations.

We may recall that the current rises which began in the

United States, affecting banking sector, housing and credit

has gone global, hitting a wide range of economic activities. In

banking sector alone, affecting banks in the recently

concluded bank reforms by the apex bank Governor, Sanusi

Lamido Sanusi closed the fear at their all-time- year low pries.

Precisely, in 2009, Afribank Nigeria Plc, which recorded an all-

time year high of N10.06, closed the year at N2.55 per share,

while Intercontinental Bank Plc closed at N1, 61 per share

from an all-time year high of N13.65. Others include Oceanic

Bank International Plc, Union Bank of Nigeria Plc, Fin Bank

Plc. and Bank PHB Plc, as they all closed the year at N1.69,

N6.00, 53 kobo, and N1.32 respectively from an all-time-year

high of N12.05, N21.12, N4.45 and N10.24.

9

The place of banks in the national economy is a

significant one and it assists to stabilize the economic life of

any nation. The importance and significance of banks with

respect to economic and social development of a nation cannot

be overemphasized. Banks are known to perform many

functions. Deposit mobilization and lending are perhaps the

most significant of these functions. Leading is essentially a

follow-up of deposit mobilization. The banks are responsible

for the safety of the funds entrusted to them while also

responsible for channeling the funds into profitable activities

not only to ensure their recovery, but also to earn adequate

returns on the fund. The quality of the banks leading

decisions, significantly determines the extent of its customer

carriage. Apart from the fact that lending is a significant

function of the bank for the above reasons, loans and

advances have been found to constitute the largest portion of

the banks assets and this assets items possesses the highest

rate of returns relative to other alternative investments, it is

thus the most important source of Banks income. While it is

highly profitable, it also possesses perhaps the greatest risk

and consequently, less liquid. What makes loan portfolio

selection difficult is the need to find an appropriate balance

between profitability, risk and liquidity.

For now, it is all a game of trial and error! No one can say

with certainty what could be done to bring economies back to

the pre-meltdown era. Stimulus packages, bail-outs, etc are

10

used by national and transnational authorities to tackle the

meltdown. A direct result of the meltdown has been the

emergence of recession in the global economy. The United

States, Japan, and most Europeans countries have

acknowledged that their economies have entered into

recession. Simply put, an economy is said to be in recession,

when it experiences negative GDP for two consecutive

quarters.

Gross Domestic Product, GDP, measures the value of all

goods and services produced within the confines of a country

by both nationals and non-national resident within the

country.

It can be seen that the remora of many barriers affecting

the financial service marketing has a tremendous impact on

competition. As information of financial services flood in on

consumer – every – day-through the Television, the Internet,

radio, newspapers/magazines, and Junk mails, there is to

much to handle as quality is being eroded. There has been a

time of enjoyment of buoyant economy,

Which is followed by recession and now uncertainty.

Customers have become more financially prudent, and are

much more demanding in terms of service quality and

openness in service delivery. The dilemma for financial

services organization is no longer that of Saturday activity, but

that of 24-hours, banking throughout that year.

1.2 STATEMENT OF PROBLEM

11

The Seller’s market in which banks operate hitherto, and

which could be easily backed by highly conservative doctrines,

has now changed into a buyer’s market requiring new

concepts, ideas and orientation in the field of marketing.

Gradually, the line between the profession of banking and

marketing is in fact thinning. We now have more marketers in

banking as well as bankers in marketing than ever before.

There is also the increasingly blurring of the dichotomy in the

activities of banks. The question remains: To what extent has

the marketing of financial services improved the banking

operations?

The banks continue to examine and re-examine their

businesses with emphasis on future sustainable performance

as opposed to short-term gains. Also, the punitive measures

introduced by the failed banks tribunal hardly escape the

minds of operators. For the surviving one, it is a fight to

remain afloat, thus, it is now imperative for them to embrace

marketing strategy in their operational drive.

Questions of interpretation may arise in determining

whether and to what extent information in public or private,

especially for organizations operating in global markets. Does

material non public information on one name in an index fund

taint the entire index? Are the bank’s internal ratings or

changes in internal ratings private information? Issues of

“signaling” private information also arise when public-side

traders become aware of transactions entered into on the

12

private side. That is, to what extent can traders infer material

nonpublic information through action (or inaction) in private-

side business lines? Last, but certainly not least, information

may be confidential or proprietary even if it does not rise to the

level of material nonpublic information. The misuse of

confidential or proprietary information that is not material

nonpublic information may not give rise to securities law

violations, but it may give rise to common law claims.

1.3 OBJECTIVES OF THE STUDY The objective of this study is to determine the imminent

need for the use of promotional mix strategy in the marketing

of financial services and to ascertain approaches necessary as

well as find out how to meet up with the customer’s

satisfaction:

1. To determine whether the Marketing Strategies adopted

by commercial banks enhance their ability to gain more

customers

2. To critically examine whether the recent financial

meltdown indicate that strong and effective corporate

governance is require in the Nigerian economy.

3. To ascertain various marketing strategies, concepts and

ideas used by banks in satisfying the changing needs of

their numerous customers and meeting their

expectations

4. To examine the emphasis by the emerging trend whereby

banks are easily made the ”beast of burden” whenever

13

there are instances of unintended effects within the

economic management matrix of the nation.

5. To measure the effectiveness of the marketing strategies

employed by banks mainly on issues relating to banking-

customer relationship.

1.4 RESEARCH QUESTIONS The research questions formulated to guide this study

are as follows:

i. To what extent has the marketing of financial services

improved the banking operations in the face of Economic

melt down?

ii. What are the major service characteristics in a Bank

Marketing Environment?

iii. What role has marketing played in promoting customers

awareness in Banking and other Financial Industry in

Nigeria during the current Economic melt down?

iv. What has been the Marketing Strategy Banks employ to

ensure that customer’s needs are met?

v. What has been the prospect and problems of marketing

financial products by banks?

1.5 RESEARCH HYPOTHESES

14

Ho 1: Promotion Mix adopted by First Bank does not

significantly affect its services demand.

Ho 2: Marketing of goods and services on the internet by

banks do not have positive impact on the Nigerian economy.

Ho 3: The recent financial meltdown does not indicate

that strong and effective corporate governance is required in

the Nigerian economy if companies are to meet their

shareholders’ needs.

1.6 SIGNIFICANCE OF STUDY The information data so obtained would add to the field

of academic. The findings will enable the Banking Industry

know the extent to which marketing can contribute to achieve

the organizational goal. It will also enable the bankers to know the reaction of

their respective services, towards the adoption of promotional

mix to boost service delivery. Tied to this is the fact that the

bank will be in a position to know whether to continue

adopting the same method as at when necessary or to dump it

for a new promotional method.

However, is highlighted in the fact that a good knowledge

of brand loyal customers, the appropriate market segment and

15

the benefits it seeks will enable the bank plan and adopt the

necessary strategies, and also effectively manipulate its

marketing mix in order to ensure success in an increasingly

competitive environment.

The study, when completed, will serve as a reference

point and source of secondary data for future researchers in

the field.

Above all, it will form a useful addition to existing

literature in the marketing of financial services in the banking

sector in general:

a) The first Bank of Nigeria Plc. management and staff

b) The banking industry and other financial institutions.

c) The Nigerian economy as a whole

d) Subsequent research on the topic

1.7 LIMITATIONS OF THE STUDY The execution of this research was not without problems.

It has been particularly constrained by inaccessibility to some

relevant data for analysis. Some of these are considered by the

banks to be confidential.

Also, there are limitations of time as limits for

submission are always specified. Financial constraints also

limit the scope of research work that can be embarked upon

by students.

In view of the problems involved in data collection, time

and financial constraints, the study is limited to Marketing

16

Strategies in First Banks during the economic meltdown. The

scope of the study is limited to First Banks in Enugu. Hence,

the findings were not extended to other banks and

generalizations of the result of the finding are limited.

The execution of this research will therefore not be

general but rather specific to First Bank.

1.8 DEFINITION OF TERMS The following Words are defined as they will be in this study:

17

MARKETING: A social and managerial process whereby individuals

and groups obtain what they need and want through creating and

exchanging products and value with others.

BANK: A place where money is kept paid out, lent, borrowed, issued

or exchanged.

BANKER: A person conducting the business of a bank.

SERVICES: Any activity or benefit that one party can offer to another

that is essentially intangible and does not result in the ownership of

anything.

FINANCIAL SYSTEM: A financial system encompasses all institutions

and economic agents that either provides financial services provide

financial resources for the system or regulate the system.

FINANCIAL MARKET: Financial market refers to the money and capital

markets where short term, medium term and long term debt and equity

instruments are traded.

CAPITAL: The finance used to invest in a business with a view of

making a return from it in future years. It is used to purchase the other

resource inputs that enable an organization to carry out business

activity.

PRICING POLICY: This constitutes the general framework within

which pricing decisions are made. They provide the guidelines within

which management formulates and carryout pricing strategy.

DEREGULATION: Deregulation is a response to regulating failure which

occurs when the outcome of attempting to fight market failure are

inferior to what the situation would have been without regulation.

MARKETING STRATEGY: Designing an initial marketing objective

for a service or product based on concepts.

SEGEMENTED PRICING: Selling a product or service at two or more

prices, where the difference in prices is not based on differences in cost.

18

ADVERTISING: Any form of paid communicating by a sponsor about

goods, services or ideas for the purpose of informing and persuading

customers to buy.

MARKET: Consists of individuals and organizations that are interested

and willing to buy a particular product or service to obtain benefits that

will satisfy a specific need or want and who have the resource to engage

in such a transaction.

MARKETS PROFILE: A description of the geography, housing

population and economic activity in the primary and secondary areas

where a product is sold.

MARKET RESEARCH: The process of getting and analyzing factual

information about a specific market-its geography, customers and

competitors to understand better one’s own position.

MARKET SEGMENTATION: Dividing a market into distinct groups of

buyers on the basis of needs, characteristics, or behaviour who might

require separate products or marketing mixes.

MARKETING MIX: The combination of four marketing activities –

product development, pricing, promoting and distribution aimed at

creating demand among the target market.

REFERENCES

Abubakar, M. (2009), The Effects of Global Financial Crisis on Nigerian Economy, Retrieved from http://www.rrojasdatabank.info on 10/02/2010

19

Baker, Dean (2008) “The Housing Bubble and the Financial Crisis,” Center for Economic and Policy Research.

Central Bank of Nigeria (2008a), www.cenbank.org. on 10/02/2010 Economy, retrieved from http://www.rrojasdatabank.info on

10/02/2010 Leaven, L., and Valencia, F. (2008), ‘Systemic Banking Crises: a New

Database’ International Monetary Fund Working Paper 08/224. Mtango, E.E.E. (2008) “African Growth, financial Crisis and Implications

for TICAD IV” GRIPS-ODI-JICA joint seminar: African Growth in the Changing Global Economy paper presented by Ambassador of Tanzania and Dean of the African Diplomatic Corps in Japan retrieved from www.google.com on 24/02/10.

Nigeria-Unexplored Territory-with 84% of Money in Circulation Outside

the Banking System…”, the Banker, April, 2006. Ojo, D. (1988) “Towards Better Banking Services” Daily Times, 14 p. 7-8 Olashore Oladele (1985) “Policy issues in Nigeria Banking and Economic

Management” Published by International Bank for West Africa Limited.

Pezzulo, Mary Ann (1993) Marketing for Bankers; American Association

Bankers, USA. Soludo, C.C (2009), Global Financial and Economic Crisis: How

Vulnerable is Nigeria? Retrieved from http://www.cenbank.org on 10/02/2010

CHAPTER TWO

LITERATURE REVIEW

INTRODUCTION

20

Financial market innovation and the development of

increasingly complex structures for credit risk transfer also

may give rise to legal or reputation risk. In recent years, we

have seen considerable advances in the management and

transfer of credit risk, including credit default swap and

collateralized debt obligations. These practices and the

development of new and more liquid markets have come about

because of better risk measurement techniques. They have the

potentials, to substantially improve the efficiency of world

financial markets through the diversification benefits that

credit risk transfer mechanisms can provide. However, the

fundamental elements of risk management must be kept

firmly in mind if these innovations are to succeed. By their

design, credit risk transfer instruments segment risk for

distribution to the parties most willing to accept them. A key

point, however, is that market participants must be able to

recognize and understand the risks underlying the

instruments they trade and be able to successfully absorb and

diffuse any subsequent loss. Another consideration is whether

one party to the transaction is entering into the trade with an

21

unfair advantage by virtue of its role as a lender to the same or

a related entity.

The statement of principles fulfils a number of objectives.

The most critical, in my view, is the promotion of fair and

competitive markets in which the inappropriate use of material

nonpublic information is not tolerated. At the same time, the

statement allows lenders to effectively manage credit portfolio

activities to facilities borrower access to more – liquid and

more – efficient sources of credit. This effort recognizes that

the liquidity and efficiency of our financial markets are related

directly to the integrity of, and public confidence in those

markets. The joint statement describes two models of credit

portfolio management the “private side” model and the “public

side” model. In reality, most banking organizations appear to

have adopted a hybrid model that lies at some point along a

continuum between pure private and pure public. In general,

in a private – side model, credit derivatives traders may have

access to material nonpublic information, but traders must

pre-clear each transaction they execute. In a public-side

model, traders are walled off from private-side information and

22

personnel to prevent their access to material nonpublic

information: accordingly; the circumstance in which a

transaction is restricted because of the trader’s possession of

material nonpublic information is limited.

The capability to satisfy their personal financial management

need. Marketing, however, entails an ongoing process of

planning, executing those plans, monitoring their results, and

modifying them. In other words, marketing is a management

process, the business of marketing must be organized and

directed in order to be effective.

2.1 OVERVIEW OF BANKING OPERATIONS

The appropriate definition of what a bank or banker is

has a subject of debate over the decades. A good number of

attempts have been made to define what a bank actually is.

The banking Decree (1979) subsequently adopted Banking Act,

1979 defines a bank or banker as “any person who transact

banking business and whose business includes acceptance of

deposits withdrawable on demand “Nwankwo (2003) seems

less satisfied with this definition and he says “the central

question is: what is banking business? He stated that “rather

23

than attempts any precise definition of a bank or a banker, let

us try and know what a banker really does.

Undeniable, marketing is becoming increasingly

important in the current banking environment. This stems

from the increased competition fuelled by the introduction of

structural Adjustment programme within the banking and

other Financial Institutions. This view is corroborated by

Maiden (2003) when he said competition has geared banks

toward paying attention to marketing activities”. The question

can be asked: what are the marketable commercial banking

services? These are the various services offered by banks:

1. Deposit Collection Account

(a) Savings account

(b) Current account

(c) Fixed deposit account

2. Provision of credit to customers inform of loans and

advances, overdrafts, bill discounting, leasing,

acceptance of bill, bonds and guarantees.

3. Money transmission services, cheque cards, credit

transfer, direct debit, standing order, bank draft, banker

cheque, mail transfer, telegraphic transfer.

24

4. Provision of financial services likes project finance, loan

syndication (consortium lending), capital/debt

restructuring, counter – trade on non crude oil.

5. Special service/products – accident safe guard scheme,

customers, guest night, woman’s forum, statements

saving scheme, joint liability agriculture credit scheme.

6. Foreign transaction services, travelers’ cheque, foreign

currency, foreign draft, bills for collection and settlement

letters of credit either confirmed or unconfirmed, etc.

The marketing situation has surprisingly changed

recently due to global recession and need for an effective

marketing of banking services is now being felt more than ever

before. Agu (2008) believed that banking is now a large and

complex service industry whose business is rural, urban and

sub-urban. Therefore the task of identifying change needs is

complex, as marketing task in the product industry needs

modification. According to Maiden (2003), some of the factors

that will make marketing of bank services effective are

customer’s behaviour, attitude and segmentation. Nwankwo

(2003) also noted that the customers of the bank must be

25

placed in the forefront of the corporate plan, since the survival

of the whole business hinges on customer’s patronage. He

concluded by saying that with the marketing concept

approach, the bank no longer sees itself as offering travelers

cheque or safe deposit but marketing security, not issuing

cheque books or credit card but facilitating cash requirement,

and no longer offering loans but enabling customers to satisfy

their wants and need today instead of waiting till tomorrow,

when they would have saved enough money.

2.2 BANK MARKETING VERSUS GOODS MARKETING

Basic differences exist between the bank marketing and

goods marketing. This is due to the fact that bank services are

intangible in nature. The services rendered cannot be

separated from the sellers (Bankers); the output can also

neither be standardized nor stored. A fundamental

consideration, which must cover the attitude of bank

management, marketing and selling, can be summed up in the

phrase “fiduciary responsibility”. It is inconvenient but seldom

catastrophic if the goods sold are substandard, but a banker’s

failure to discharge his fiduciary responsibility for safe-keeping

26

of customer’s funds or to provide irresponsible advice on

financial matters can make a company bankrupt, or ruin an

individual’s life. For this reason, in marketing financial

services, organizations cannot be inhibited in the same way as

manufacturers of goods.

A second way in which bank marketing of financial

services differs from marketing in other industries is the

involvement of marketing not only to the provision of financial

services to the customers but the procurement of the raw

materials on which most of the services are based. The

provider of the services does not need to persuade his supplier

to provide the components or raw materials. The banking

industry can “buy” a proportion of raw materials (deposits) on

the money market, but an important proportion of the raw

materials has to be “gained” by persuading individuals and

corporate organizations to deposit their funds with it and have

persuasion becomes marketing function.

The fact that the main means of persuasion in attracting

deposits is the availability of services and that the raw

materials supplier at the same time customer adds a

27

fascinating element of complexity to the business of marketing

of financial services. Thus because of the two-sided nature of

banking, a banker has to attract customer to sell deposits to

him and at the same time attract them to take loans and

advanced from him. In essence, the banker has the difficult

task of selling services to the same members of public from

where it buys. Whereas on other hand, goods marketing is

narrowly concerned with satisfying perceived needs of the

customers at a profit. The producer will only consider the need

of his customers and get the customers to buy them.

Furthermore, in improper rendering of bank services may

injure the feeling of the customers, leading to loss of patronage

in some cases. While a shoddy presentation of goods may be

compensated for by the acceptable performance of the

product. Banking Industry must be market related due to the

perilous nature of its services. In other words, it must be

effective in selling its services.

2.3 THE PROCESS OF BANK MARKETING

For a successful bank marketing to occur there must be

a specially planned marketing process. Otherwise the notion of

28

an effective marketing may be an illusion. The process of

effective marketing can be examined as follows:

(a) market segmentation

(b) product planning and product life-cycle

(c) test marketing

(d) the marketing mix-product, price, promotion, place,

process, physical.

(a) Market Segmentation

The concept of market segmentation is based on the

notion that different groups of potential customers have

different characteristics, needs and wants and so a special or

a new product or service might be the best way of winning

their patronage Kotler and Kevin lane (2006) in their book

marketing management, planning and control, defines market

segmentation as “the subdividing of a market into

homogeneous subsets of customers. Where any subset may

conceivably be selected as target market to be reached with a

distinct market – MIX” for a truly market oriented firm, the

characteristics of the market where it operates must be known

so as to aid effective market planning. The market for banking

29

services can be divided into two distinct categories the

personal and corporate customers. Each segment can further

be sub-categorized i.e. the personal customers can be

segmented into age-group, income level, social classes mental

status, geographical location etc. while the co-operate

customers can be segmented into small-scale business,

medium-scale business and large-scale business or importers,

exporters or domestic traders. The segmentation analysis may

be used which entails segmentation influence decisions about

how many and what type of products and services are needed

to satisfy different demands. Alternatively, it is due to plan

different ways of selling the same products or service.

The essence of market segmentation to the banker may be

summed up as follows:

1. The bank can make adjustment to their services, which

gives them a more direct appeal by satisfying customer’s

need more specifically.

2. The bank is able to discover and develop market

opportunities more readily.

30

3. The bank can develop a marketing plan and programme

with a better perception of how distinct segments of the

bank will respond to the programme.

(b) Product Planning and Product-Life-Cycle.

Marketing planning for a product or a service could be likened

to an adage that says what goes up must come down, each

product or services is believed to have a life-cycle with at least

four stages as follows:

Production:

This is the product or services which are first introduced into

the market; it may not be profitable at first since market

demand will take time to build up.

Growth:

This is when the product/service begins to make profit with

increasing sales

Maturity:

When sales are steady after the period of growth: This stage is

the largest part of the life cycle of many successful product or

services since most of the profits are earned during this

period.

31

The Declining Period of Stage:

This is the last stage in the process of product life cycle. Sales

may begin to drop or decline due to market forces. According

to Andrew (2005) “the relevance of the product life-cycle

analysis for planning is that a company must have a sufficient

number of products at each stage in their life-cycle to ensure

continuity of succession. A bank must replace declining

services with new ones to ensure the achievement of its target

of profitability and growth.

(c) Test Marketing

this involves the sampling of selected group of customers

in order to derive some comment and suggestions on a newly

developed product or service in and will find favour with

customer’s e. g. how many customers might use the service

and what modifications can be made to the service. The tested

area should, as much as possible be a fair representation of

the total market in terms of advertising media and sales

outlets.

(d) Marketing Mix

32

The concept of marketing mix according to Borden, (1964)

consists of the combination of activities selected to achieve the

marketing goals and this includes the allocation of resources

to each activity. Simply put, it is the number and types of

services, which a bank makes available to customers at a

point in time. McCarthy (1979) popularized the definition of

marketing mix as four classifications called the 4ps. The 4ps

are product, Price, Promotion and Place. The important

feature of marketing mix is that every item in it is subject to

the control and manipulation of management. It is very vital in

the planning and implementation of decision about product,

place, promotion and place e. g. what services the customers

need? What is the right price to charge? How do we persuade

customers to sue them? From the above discussions, it can be

concluded therefore that the 4ps are very essential in any

marketing planning process.

i. Product or Service

This is what a business produces in order to satisfy their

customers needs, emphasis is more; the features, quality, and

modifications or innovation of the services or product. For

33

example product features in bank lending would include the

terms of the loans, variable or fixed interest rate etc. while on

the bank deposits, product features would include withdrawal

condition, interest rate paid, and conditions for operating and

account.

ii. Price

In banking, pricing according to Mulvihill (2005) means the

interest rates offered to depositors and borrowers, bank

charges and commissions for individual services, one of the

oligopolistic nature of banking services, the prices of services

are not a deeming factor in marketing strategic planning by

bankers, but the quality of service and no-quantifiable factors

are the measuring rod for customers preferences of one bank

to another. Coupled with the Market structure, there has been

regulatory constraint though the use of monetary policy,

circular and banker’s tariffs specifying the interest rate and

charges for all bankers thus making price strategy a passive

instrument. However with the introduction of new technology

the arrival of new and aggressive banks and recently the total

deregulation of interest rates, pricing strategy of bank now

34

becomes a critical ingredient in the marketing activities of a

bank. This according to Fulmer (2006) the price placed on

any product or service must be profitable to the seller (banker)

and must be affordable to the customers. Also the benefit

derived from the service or product must be commensurate

with the price paid out.

iii. Promotion

This involves the stimulation of market interest in the services

provide though the following means.

(a) Advertising through T.V Radio, Daily Papers

Periodicals. Journals, Hand bills Calendars etc.

(b) Using the slogans, i.e. chosen words to give precise

information about the bank e.g. “the wise choice in

banking”.

(c) Training of staff on the job to be more courteous

and efficient in rendering services to customers.

iv. Place (Distribution)

This is concerned with where the products or service is made

available to the customers or where the customers can obtain

the services. The crucial issue is that the customers must

35

have easy accessibility to a service. In banking, the aspects of

distribution (place) are as follows:

i. the existence of branch-network. As identified study text

in banking (1985) the strength of a dealing (commercial)

banks in domestic banking is their large network of high

street branches which bring banks closer, physically to

their customers. First bank’s network currently stands at

over 520 branches. However, the restricted opening

hours of banks have for sometime been a source of public

criticism. The advantage of local branches is removed if

they are not opened when customers want to visit them

for business. This is probably the reason why.

ii. In shop branches i. e. nine braches can be opened in big

hotels, university campuses, and in periodic trade fairs.

iii. Banking services provided by the method of money

transmission other than by cheque clearing e.g. direct

debiting, standing orders.

iv. Mail Banking (GIRO) banks make use of Post offices as a

system of distributing their services especially in areas

where no branches of the bank or any other bank exists.

36

2.4.1 THE HISTORY OF FIRST BANK OF NIGERIA

First Bank traces its ancestry back to the first major financial

institution founded in Nigeria; hence the name. The current

Chairman is Dr. Ayooola Oba Otudeko OFR. The bank is the

largest retail lender in the nation, while most banks gather

funds from consumers and loan it out to large corporations

and multinationals, first bank has create a small market for

some of its retail clients.

At the end of August 2006, the bank had assets totaling

650 billion NAIRA or $5 billion dollars. The bank was also the

most highly capitalized stock on the Nigerian stock exchange,

and had about 10 billion outstanding shares. It has a

subsidiary in the United Kingdom, FBN Bank (UN), which has

a branch in Paris. The bank also has representative offices in

South Africa and China.

The company was named the best bank in Nigeria by

Global finance magazine in September 2006. The firm’s

auditors are Akintola Williams. Deloitted and Touche

(chartered accountants) and KPMG audit (chartered

accountants). The firm has solid short and long term ratings

37

from Fitch and the Global Credit Rating Company partly due

to its low exposure to non-performing loans. The firm’s

compliance with financial laws has also strengthened with the

economic financial crimes commission giving it a strong

rating.

2.4.2 HISTORY – PRE-INDEPENDENCE

The bank traces its history back to 1894 and the Bank of

British West Africa. The bank originally served the British

shipping and trading agencies in Nigeria. The founder, Alfred

Levis Jones, was a shipping magnate who originally had a

monopoly on importing silver currency into West Africa

through his Elder Dumpster Shipping Company. According to

its founder without a bank economies were reduced to using

barter and a wide variety of mediums of exchange, leading to

unsound practices. A bank could provide a secure a secure

home for deposits and also a uniform medium of exchange.

The bank primarily financed foreign trade, but did little

leading to indigenous Nigerians, who has little to offer as

collateral for loans.

38

2.4.3 POST – INDEPENDENCE

In 1957, Bank of British West Africa changed its name to

Bank of West Africa (BWA). After Nigeria’s Independence in

1960, the bank began to extend more credit to indigenous

Nigerians. At the same time, citizens began to trust British

banks since there was an independent financial control

mechanism and more citizens began to patronize the new

Bank of West Africa.

In 1965, Standard Bank of South Africa acquired Bank of

West Africa and changed its acquisition’s name to Standard

Bank of West Africa. In 1969, Standard Bank of West Africa

incorporated its Nigerian operations under the name Standard

Bank of Nigeria listed its shares on the Nigerian Stock

Exchange and placed 13% of its share capital with Nigerian

investors. After the end of the Nigerian Civil War, Nigeria’s

military government sought to increase local control of the

retail – banking sector. In response, now standard chartered

Bank reduced its stock in Standard Bank Nigeria to 30%.

Once it had lost majority control, standard chartered wished

39

to signal that it was no longer responsible for the bank and the

bank changed its name to First Bank of Nigeria in 1979. by

then, the bank had re-organized and had more Nigerian

directors than ever. In 1982 First Bank opened a branch in

London, that in 2002 it converted to a subsidiary, FBN Bank

(UK). Its most recent International expansion was the opening

in 2004 of a representative office in Johannesburg, South

Africa. In 2005 it acquired MBC International Bank Ltd and

FBN (Merchant Bank Ltd. Paribas and a group of Nigerian

Investors had founded MBC in 1982 as a Merchant bank; it

has become a commercial bank in 2002. in June 2009,

Stephen Olabisi Onasanya was appointed Group Managing

Director (CEO), replacing Sanusi Lamido Sanusi who had been

appointed governor of the Central Bank of Nigeria. Onasanya

was formerly Executive Director of banking operations and

services.

2.5.1 SOCIETY FOR WORLD-WILD INTERBANK

FINANCIAL TELECOMMUNICATION (SWIFT)

40

Under SWIFT, a bank’s membership allows it to transmit

financial message globally within seconds while also receiving

a spot confirmation. The SWIFT network system is made of

computer based located around the world and interconnected

through telephone leased lines or package switches.

2. ON-LINE/REAL TIME SERVICE: This is an electronic

based which satisfies customer’s convenience. The

product enables customer’s access to his account

balance in various branches of the Bank.

3. HOME BANKING: The product enables customers to

access their transaction from their offices or homes. The

product is presently offered to Nasco Plc. Jos. Total

Nigeria Plc. Elf Nigeria Plc. Etc.

4. FIRST BANK SMART CARD SCHEME:

The bank is a member of the consortium of banks

handling the smart card project, under the brand name,

Value card. The card incorporates very important

security features. It uses plastic cards, embossed with

memory chips on which can be loaded various sum of

41

money (electronic purse) which can be disbursed

intermittently.

2.6 THE CHANGING MARKET STAGE OF THE BANK

Great publicity is being given to the process know as

deregulation in the Nigeria banking market, which is

happening because of change in market forces. These same

market forces operate the world over the effect of heightening

competition in all areas of banking business. At the same time

they affect the structure of banking business by changing its

economic operation. Banks in Nigerian will not have the same

need for enabling legislations as with other countries

especially African countries, because our frame work of

existing law is less rigid, but a new approaches is needed, as

her: -

(a) CONFIDENCE IN THE BANKING BUSINESS

The development of new skills by staff will lead to greater

confidence in themselves and in turn this will generate even

greater confidence in banks by customers. The proliferations

of bank services must not be allowed to in undated managers

42

and staff and the banks will have to give careful consideration

to the priorities, which they pass down the tone.

(b) COMPETITION VERSUS CO-OPERATION

It is an irony of banking that to offer an efficient, competitive

service; it is necessary for co-operation between banks to take

place in the area of payment system. The growth of ATM

networks has highlighted the problem of capital cost even for

the largest bank’. Bank customers will benefit greatly from

increasing reciprocity and even customers of building society

have not been left out. Despite the co-operation, modern

technology will provide the tools for competition in the future.

It will allow the reduction of costs and increase in productivity

necessary for bank services to be made available at all time

and in places more convenient to customer. To be successful,

banks must have to adopt a more anticipatory approach to

both market friends and public issues. The strategy of public

relations will have to become an important consideration. To

stand them in good stead, the banks have put certain

43

strategically structures in place wit necessary qualities to

carry them forward with confidence;

Increasing professionalism to enable them deal with

specialist market.

The adaptability to take a positive approach to chance.

The imagination to innovate and redesign their product

and services to cope with an ever more complex and

fragmented market.

Despite all the changes and changes, at the centre of its all

lies the banker-customer relationship. If they are to deserve

the trust and esteem of their customers they must make every

effort to bring them score to the business of banking and raise

their understanding of the function of banking as a force for

good in the community. Banking must demonstrate its unity

of purpose with the world at large.

44

REFERENCES

“First Bank HAULS GLOBAL Finance Awards,” Vanguard

(Nigeria) September 13, 2006. “First Bank Hauls Global Finance Financial Awards,”

Vanguard (Nigeria) September 13, 2006. Agu, C.C. (2008) “Nigeria Banking Structure and Performance”

The Banking Systems Contribution to Economic Development, African – FEP Publisher Ltd. Onitsha.

Alfred Jones: Banking in West Africa. Journal of Africa society.

Alfred Jonesi: Banking in West Africa. Journal of African Society

Capaldinin, P.F. (2004) Marketing for the Bank Executives,

Leviathan House, London. Chukwuma, J. (2008) ‘Marketing of African Products’ being a

seminar paper presented in P.H. August 20-21. Race (2008)

Fanning, D. (2001) “Productivity: the Human Asset Approach

to Bank Ranking” The Banker, November. Fulmer, Robert M (2006) “The New Marketing” Macmillan

Publishing Co Inc New York Jibrin Abubakar (5 June 2009), “Onasanya succeeds Senusi

as First Bank GMD”. Daily Trust. Retrieved 2010–03-01. Jibron abubakar (5 June 2009). “Onasanya succeeds Sanusi

as First Bank GMD”. Daily Trust. Retrieved 2010-03-01. Maiden, G.O (2005), the Role of Marketing Management

45

Mary Ann Pezzullo, (2006). Marketing for Bankers AAB, USA. Mulvihill, Donald F. (2005) “Developing Price Policies” in

Handbook of Modern Marketing, Buel, Victor P. Ed. Mc Graw Hill Inc.

Nigeria – Unexplored Territory – with 84% of money in

circulation outside the banking system, ..”, The Banker, April, 2006.

Nigeria-Unexplored Territory-with 84% of Money in Circulation

Outside the Banking System…”, the Banker, April, 2006. Nwankwo, G.O. (2003) Essential, of Bank Marketing, New

Dimension in Banking in Developing COUNTRIES “Collected Essay”, Mimio.

Richard Fry; Banking in West Africa. The story of the British

Bank of West Africa. Richard Fryi Banking in West Africa. The Story of the British

Bank of West Africa.

46

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 RESEARCH DESIGN

The present study has utilized the cross-sectional

approach in that the variables were being measured at a

particular point in time. However, this method is again divided

into two types – field study and field survey. We have therefore

chosen the field survey approach since we are interested in

determining financial service marketing in the Bank using a

representing sample. This study has utilized an appropriately

detailed and illustration instrument to collect primary

research data.

3.2 SAMPLING PROCEDURE

The study was restricted to Enugu Metropolis. The simple

random sampling technique was used for this purpose

selecting people from particular class and occupation from

every branch and area of banking operation, only people who

were literate enough to comprehend the contents of the

47

questionnaire accepted to fill it. A specific time interval was

allowed the respondents to fill the questionnaires.

3.3 DETERMINATION OF SAMPLE SIZE

To arrive at a sample size, the research conducted a pilot

survey to determine the proportion of the respondents that

may give positive responses as to whether marketing strategies

adopted by first banks enhances customer satisfaction. From

a randomly selected twenty (20) respondents in the banks,

eighteen (18) or 90% of the respondents indicated that

strategic adopted by First Banks enhances customer

satisfaction while two (2) or 10% of the respondents are of the

opinion that the marketing strategies do not enhance

customer satisfaction.

Based on these findings, a sample size was determined

using the following statistical formula

N = Z2Pq e2

Where:

N = Sample size to be computed

48

Z = Number of standard deviation for the desire level of

confidence (this is given by 1.96 at 5% tolerable error)

P = Percentage of positive responses (those who says

“yes”)

q = Percentage of negative responses (those who says

“no”)

e = The limit of tolerable error at 95% confidence level

The sample size can be determined based on the pilot survey

figures;

P = 90%

q = 10%

Therefore

N = 1.962 x 90 x 10 52

= 345.7 x 0.44 25 = 138.2976 = 138

Based on the computation, the sample size of 138 was used in

the study.

49

3.4 DATA COLLECTION

In the course of this research work the use of data was

unavoidable. The data being used for the study consist of:

(A) Primary Source

(i) Oral Interview: The researcher applied the oral

interview method of data collection wherein the responders

were met face to face, and asked necessary questions and

responses were recorded personally on the spot. The interview

was a form of structured interview method. The researcher

considered the oral interview as necessary because some

respondents could not understand the objective of the study

and tried to avoid completing the questionnaires. The

researcher also felt that the method is appropriate, as it will

afford one the opportunity to explain everything to the

respondents and to make on the spot assessment of the

situation.

(ii) Use of Questionnaire: A well-structured questionnaire

was designed by the researcher for the purpose. The

questionnaires were distributed in accordance the

characteristics of the population earlier explained above. The

50

research questionnaires were given also to both marketing

department staff and those in operations. For example:

Branch Staff. Head office, Department staff, and Domestic

treasury staff etc. the questionnaires were personally

administered to the respondents and were made up of printed

questions that the respondents had to fill in the answers

considered appropriate.

Mailing of these questionnaires was avoided by the research,

as this would have led to low responses rate, thereby affecting

the correctness of the study. Close end and structured

questioned that would enable the respondents to give uniform

responses in their questions were found useful. The replies to

the questionnaires provided by the respondents gave an

insight into the investigation’s subject matter for the purpose

of the study.

(B) Secondary Data Sources

(1) Publications: In the search of data and statistics about

the subject of the study, the researcher made enquiry and

investigations through several publications these included;

51

Magazines, Business, Newspapers, Journals, Periodicals,

Papers presented by the eminent scholars and orthodox

textbooks. Lecture notes and past research texts on this

subject were also used.

METHOD OF DATA PRESENTATION

The methods used in presentation of data in the study will be

analysed using SPSS for the determination of frequency table

and test of significance.

The method to be used for analysis of the data obtained shall

consist of

1. chi-squire X2

2. ANOVA

For instance, the chi-squire-X will be used for testing more

than one population as it provides a means of comparing a set

of observed frequencies with a set of expected frequencies.

The Analysis of variance is an inferential method for

comparing several means. Using F distribution, for detecting

differences among a set of population means.

52

REFERENCES

Abdellah, F. G. and Levine, E. (1979), Better Patient Care through Nursing Research. New York: Macmillan Publishing Co.

Cook, T. D. (1983), “Quasi-Experimentation: Its Ontology,

Epistemology, and Methodology” in Beyond Method. Morgan G. (ed) London: Sage Publication.

First bank Nigeria Plc. (2008) Published Market and opinion research Intercontinental (MOR),

(1983), An Report “Banking Service and the Consumers” Market Behaviour Ltd., (MBL) Appendix 11.

Nachmias, D. and Nachmias C (1976), Research Methods in

the Social Sciences UK. Edward Arnolds. Onwumere, J. (2005), Business and Economic research

methods, Lagos: Don Vinton Ltd.

53

CHAPTER FOUR

DATA PRESENTATION AND ANALYSIS

4.1 INTRODUCTION

This study focused on the financial services marketing in

the banking sector during Economic Meltdown. To carry out a

meaningful study First Bank Plc was used. A total of 138

questionnaires were administered. Only 100 were well filled

and formed the basis of the numbered used in testing of the

hypotheses, ANOVA and chi-square test were used.

4.2 RETURN OF QUESTIONNIARE

Table 4.2.1 SEX COMPOSITION OF RESPONDENTS

Gender

classification

Frequency Percentage [%]

Males 46 46

Females 54 54

Total 100 100

Source: Field data 2010.

54

The table above shows that out of 100 questionnaires

returned by the management and staff of First Bank of Nigeria

Plc, 46 [46%] were received from male respondents while 54

[54%] were received from the female respondents.

Table 4.2.2: NUMBER OF YEARS OF SERVICES

Years Frequency Percentage [%]

1-5 32 32.0

6-10 14 14.0

11-15 41 41.0

16-20 3 3.0

21 and above 1 1.0

Missing value 9 9.0

Total 100 100

Source: Field data 2010.

The table above shows that a summary of the

distribution of questionnaires by services years consideration.

32 [32%] were received from respondents within the range of

1-5years in services. 14 [14%] respondents were within 6-

55

10years in services, 41 [41%] respondents were within 11-

15years in service, 3 [3%] respondents were within 16-20years

in services while only 1 [1%] was within 21 and above. The

other 9 [9%] respondents did not indicate.

RESEARCH QUESTION 1:

Promotion mix are ways and means through which marketing

activities of organizations are boosted. Which of the following

mix does your Bank use?

Table 4.2.3: MIX ENHANCING MARKETING

Classification Frequency Percentage [%]

Sales promotion 17 17.0

Public relation 33 33.0

Personal selling 7 7.0

Publicity 3 3.0

Total 60 60.0

System 40 40.0

Total 100 100

Source: Field data 2010.

56

The table above depicts that out of a total of 100

respondents, 17 [17%] were of the opinion that sales

promotion is the means through which the bank boost its

marketing activities and its services. The other 33 [33%] were

also of the opinion that in marketing activities, first bank uses

public relation means to boost its products and services. 7

[7%] respondents believes that personal selling is the

marketing strategy adopted by First Bank. However, 3 [3%]

respondents were of the opinion that First Bank uses publicity

in boosting its marketing activities. The remaining 40 [40%]

respondents did not indicate. The result shows that, the

promotion needs First Bank Plc uses impact in reinforcing the

brand image and boost its marketing activities for continue

product. This is because 60% of the respondents agreed that

First Bank uses at least one of the promotion least above.

57

RESEARCH QUESTION 2:

In what way has the marketing strategy applied by your bank

contributed to the increase in customer satisfaction.

Table 4.2.4: CONTRIBUTION OF MARKETING STRATEGY TO

CUSTOMERS SARTISFACTION.

Classification Frequency Percentage [%]

Very large extent 13 13.0

Large extent 72 72.0

No large extent 13 13.0

No extent at all - -

Total 98 98.0

Missing value 2 2.0

Total 100 100

Source: Field data 2010.

In the table above, the data reveals that 13 [13%]

respondents were of the opinion that the marketing strategy

applied by First Bank Nigeria Plc has contributed to a very

large extent in increasing customers satisfaction. 72 [72%]

58

respondents have a positive view that marketing strategy of

FBN Plc has increase customers satisfaction to a large extent.

However, 13 [13%] respondents were of different view that the

marketing strategy of FBN Plc with regards to customers

satisfaction has contributed to no large extent. No respondent

chose to no extent at all. The remaining 2 [2%] respondents

not indicated. The result shows that marketing strategy

applied by First Bank Plc impact substantially in satisfying

customers because 85% of the respondents either agreed or

strongly agreed.

RESEARCH QUESTION 3:

How would you evaluate the problem of Bank marketing in

Nigeria?

59

Table 4.2.5: EVALUATION OF THE PROBLEM OF BANK

Classification Frequency Percentage [%]

Very large extent 4 4.0

Large extent 19 19.0

No large extent 12 12.0

No extent 63 63.0

Total 98 98.0

Missing value 2 2.0

Total 100 100

Source: Field data 2010.

The table above shows that 4 [4%] respondents were of

the opinion that the problem of bank marketing in Nigeria is to

a very large extent. However, 19 [19%] respondents were of the

opinion that the problem of bank marketing in Nigeria is to

large extent, 12 [12%] respondents were of the view that the

problem of bank marketing is to no large extent. 63 [63%]

opted for no extent at all. While the remaining 2 [2%]

respondents not indicated. The result shows that the problem

of bank marketing in Nigeria has greatly been reduced

60

because the services rendered cannot be separated from the

bankers that is why 75% of the respondents believe the

problem are “to no extent at all” or “to no large extent”.

RESEARCH QUESTION 4:

What has been the major problem of bank marketing in

Nigeria?

Table 4.2.6: THE PROBLEM OF BANK MARKETING IN NIGERIA?

Classification Frequency Percentage [%]

Domestic economic problem

32 32.0

Poor marketing technique

41 41.0

Persistent competition

7 7.0

Social factor 11 11.0

Total 91 91.0

Missing value 9 9.0

Total 100 100

Source: Field data 2010.

The result of table above reveals that 32 [32%]

respondents were of the opinion that major problem of bank

61

marketing in Nigeria is due largely to domestic economic

problems. 41 [41%] respondents, had the opinion that the

major problem of bank marketing is due to poor marketing

techniques. However, 7 [7%] of the sample sizes were of the

opinion that the major problem of bank marketing in Nigeria

was due to persistent competition. Nonetheless, 11 [11%] were

of the opinion that the major problem of bank marketing in

Nigeria was due to the social factors. the remaining 9 [9%]

respondents not indicated. The result shows that all the

problems above in one way or the other affect bank marketing

in Nigeria because 91% of the respondents either choose one

or another.

RESEARCH QUESTION 5:

To what extent has the marketing of goods and services on the

internet have impact on the Nigeria economy?

62

Table 4.3.7: INTERNET IMPACT ON NIGERIA ECONOMY

Classification Frequency Percentage [%]

Very large extent 20 20.0

Large extent 50 50.0

No large extent 22 22.0

No extent 3 3.0

Total 95 95.0

Missing value 5 5.0

Total 100 100

Source: Field data 2010.

The table above shows that 20 [20%] respondents were of

the opinion that marketing of good and services on the

internet have impact on the Nigerian economy to a very large

extent. 50 [50%] respondents believes it was to a large extent.

However, 22 [22%] respondents were of the view that internet

impact is to no large extent. 3 [3%] respondents opted for no

extent while the remaining 5 [5%] respondents no indicated.

this result means that marketing of goods and services on the

internet have impacted greatly on the Nigeria economy as 70%

63

of the respondents agreed that it is to very large extent or large

extent.

RESEARCH QUESTION 6:

To what extent the recent financial meltdown indicate that

strong and effective corporate governance is required in the

Nigerian economy if companies are to meet their shareholders’

needs?

Table 4.2.8: STRONG AND EFFECTIVE CORPORATE

GOVERNANCE

Classification Frequency Percentage [%]

Very large extent 10 10.0

Large extent 18 18.0

No large extent 68 86.0

No extent - -

Total 96 96.0

Missing value 4 4.0

Total 100 100

Source: Field data 2010.

64

The table above shows that 10 [10%] respondents were of

the opinion that strong and effective corporate governance is

required in Nigeria if companies are to meet their

shareholders’ needs is to a very large extent. 18 [18%]

respondents opted for a large extent. However, 86 [68%] were

of the opinion that is to no large extent, while the remaining

4[4%] respondents not indicated. The results shows that the

recent financial meltdown does not indicate that effective and

strong governance is required in Nigeria if companies are to

meet their shareholders because 86% of the respondents opted

for “no large extent”.

4.3 TEST OF HYPOTHESES

The hypotheses drawn from the objective of this research

work was tested using chi-square and ANOVA. The decision

rule is that anything less than .005 is significant. In that case

the null hypotheses [H0] will be rejected while alternative

hypothesis [H1] will be upheld.

65

HYPOTHESIS 1:

H0: Promotion Mix adopted by First Bank does not

significantly affect its services demand.

H1: Promotion mix adopted by First Bank Significantly affect

its services demand.

To test this hypothesis, response to question 3 of the

questionnaire was analysed.

Frequencies: Promotion mix are ways and means through

which marketing activities of organizations are boosted.

Which of the following mix does your bank use?

Table 4.3.1: showing the promotional mix used.

Classification Observed N Expected N Residual

Sales 17 15.0 2.0

Public relation 33 15.0 18.0

Personal selling

7 15.0 -8.0

Publicity 3 15.0 -12.0

Total 60

Source: Computer result

66

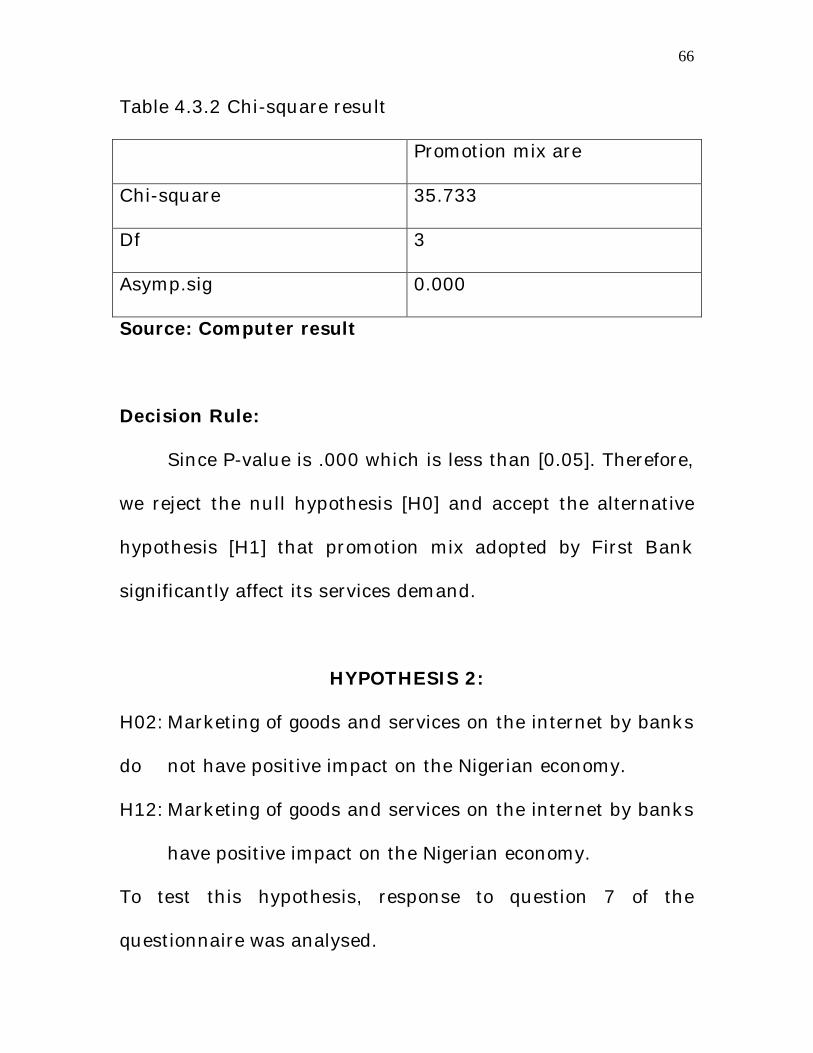

Table 4.3.2 Chi-square result

Promotion mix are

Chi-square 35.733

Df 3

Asymp.sig 0.000

Source: Computer result

Decision Rule:

Since P-value is .000 which is less than [0.05]. Therefore,

we reject the null hypothesis [H0] and accept the alternative

hypothesis [H1] that promotion mix adopted by First Bank

significantly affect its services demand.

HYPOTHESIS 2:

H02: Marketing of goods and services on the internet by banks

do not have positive impact on the Nigerian economy.

H12: Marketing of goods and services on the internet by banks

have positive impact on the Nigerian economy.

To test this hypothesis, response to question 7 of the

questionnaire was analysed.

67

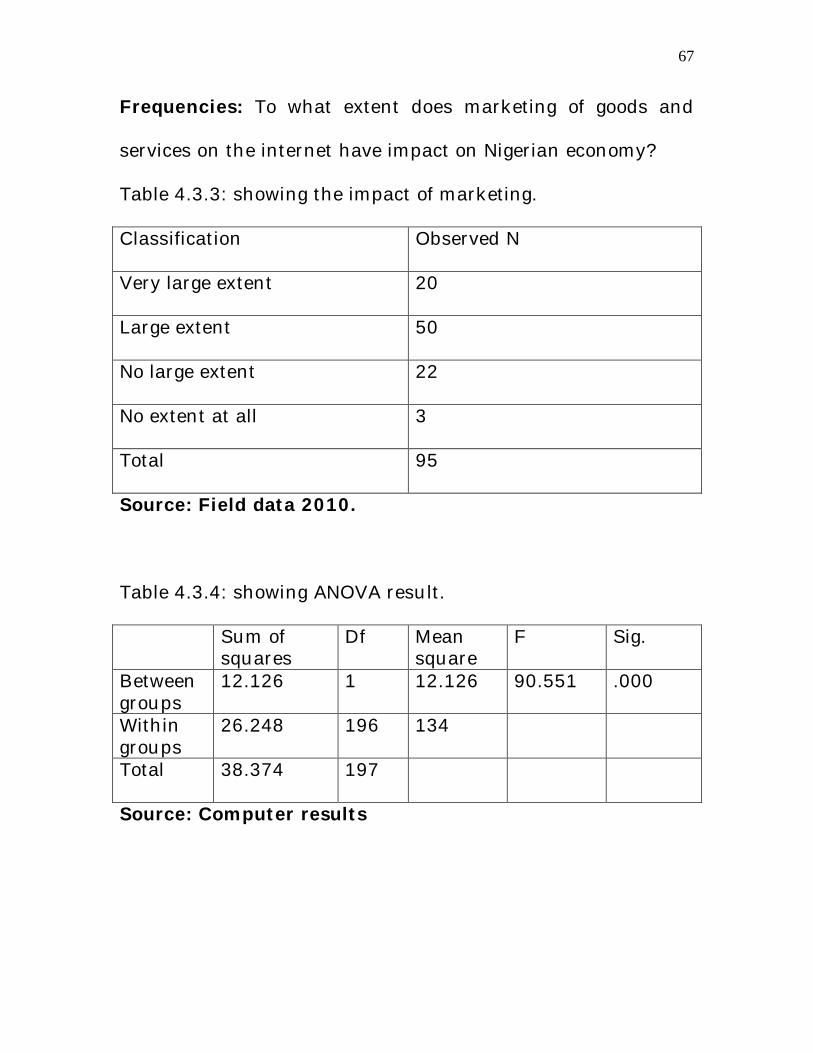

Frequencies: To what extent does marketing of goods and

services on the internet have impact on Nigerian economy?

Table 4.3.3: showing the impact of marketing.

Classification Observed N

Very large extent 20

Large extent 50

No large extent 22

No extent at all 3

Total 95

Source: Field data 2010.

Table 4.3.4: showing ANOVA result.

Sum of squares

Df Mean square

F Sig.

Between groups

12.126 1 12.126 90.551 .000

Within groups

26.248 196 134

Total 38.374 197

Source: Computer results

68

Decision Rule:

Since P-value is .000 which is less than [0.05]. Therefore,

we reject the null hypothesis [H0] and accept the alternative

hypothesis [H1] that marketing of goods and services on the

internet by banks have significant impact on the Nigerian

economy.

HYPOTHESIS 3:

H03: The recent financial meltdown does not indicate that

strong and effective corporate governance is required in the

Nigerian economy if companies are to meet their

shareholders’ needs.

H13: The recent financial meltdown indicates that strong and

effective corporate governance is required in the Nigerian

economy if companies are to meet their shareholders’

needs.

To test this hypothesis, response to question 8 of the

questionnaire was analysed.

69

Frequencies: To what extent the recent financial meltdown

indicate that strong and effective corporate governance is

required in the Nigerian economy if companies are to meet

their shareholders’ needs.

Table 4.3.5: strong and effective corporate governance

Classification Observed N

Very large extent 10

Large extent 18

No large extent 68

No extent at all -

Total 96

Source: Field data 2010.

Table 4.3 6: showing ANOVA result.

Sum of squares

Df Mean square

F Sig.

Between groups

59.836 1 59.836 270.987 .000

Within groups

42.837 194 .221

Total 102.672 195

Source: Computer results.

70

Decision Rule:

Since P-value is .000 which is less than 5, therefore we

reject the null hypothesis [Ho[ and accept the alternative

hypothesis [Hi] that, the recent financial meltdown indicated

that strong and effective corporate governance is required in

the Nigerian economy if companies are to meet their

shareholders’ needs.

71

CHAPTER FIVE

SUMMARY, CONCLUSION AND RECOMMENDATIONS

5.1 SUMMARY OF FINDINGS

This work reveals the well-informed perception customers

intend to gain with the use of necessary marketing tools in the

dissemination of bank services in the face of economic

meltdown.

In this study, we tried to identify the various marketing

approaches being adopted by the bank to ensure that their

existing customers are to a large extent being satisfied and

generate new customers.

We subjected the generated data to analyses and arising

from the conclusion reached proceeded to answer the research

questions outlined at the beginning of the research work.

A total 138 questionnaires were administered to the

various points including the department of marketing at the

Head Office and branches of First Bank Nigeria Plc. Out of

this, there was 100 responses returned questionnaires and 38

unreturned questionnaires.

72

The distribution depicts that male represents 46% while

54% respondents were females.

The 100 respondents representing 100% of the total

population were of the opinion that First Bank Nigeria Plc

renders all the services. Out of the 100 respondents, 81

representing 24% were of the opinion that First Bank uses Re-

Lunch method as a means of resuscitating failing/declining

product[s]/service. Another 81 representing percentage, 24

were of the view that the bank resuscitates a failing/decline

products/services through Re-Package method. Also 81

persons representing 24 was of the opinion that the bank uses

the method of creating new market for resuscitating

failing/declining products/services. But 95 respondents went

for “other please state” and this represents 28%.

Out of 100 respondents, 33 representing 33% were of the

opinion that Public Relation is the means through which the

bank books its marketing activities and its services. The other

7% respondent representing 6.54% was also of the opinion

that in marketing activities First Bank uses the personal

selling means to boost its products and services. 17

73

respondents representing 17% was of the opinion that First

Bank uses sales promotion mix in boosting its marketing

activities. However, 3 respondents representing 3% were of the

opinion that First Bank uses publicity, while the other 40

respondents [i.e. 40%] did not indicated.

The data reveals that out of a total of 100 respondents,

13 representing 13% were of the opinion that the market

strategy applied by First Bank of Nigeria Plc, has contributed

to very large extent in increasing customer satisfaction. 72

respondents had a positive view that marketing strategy of

First Bank of Nigeria Plc has increased to a large extent

customer’s satisfaction. However, 13 of the respondents were

of different view that the marketing strategy of First Bank of

Nigeria Plc with regard to customers satisfaction is to no large

extent while the remaining 2 respondents representing 2% did

not indicated.

The result further shows that out of 100 respondents, 4

were of the opinion that the problem of bank marketing in

Nigeria is to a very large extent. However, 19 respondents of

the total population representing 19% of the sampling size

74

were of the opinion that the problem of Bank Marketing in

Nigeria is to a large extent, 12 respondents were of the view

that the problem of bank marketing in Nigeria is to no large

extent. While 63 respondents were of the opinion that the

problem of bank marketing in Nigeria is to no extent at all. 2

respondents did not indicate.

Finally, the result reveals that of the whole

questionnaires distributed, 10 respondents representing 10%

were of the opinion that the recent financial meltdown

indicated that the strong and effective corporate governance is

required in Nigeria economy if companies are to meet their

shareholders’ needs. 18 respondents, representing 18% of the

total population had the opinion that the recent financial

meltdown. This represents 68 respondents out of the total

100. Nonetheless, 4 respondents not indicated.

5.2 RECOMMENDATIONS

Having come this far and having seen the results of the

data generated and analyzed, certain recommendations are

necessary;

75

a. Banks must increase their advertising budget. It is

discovered that banks are in the actual fact down

scaling and reducing costs. Market share care easily be

increased by the use of promotional market tools. It is

therefore advised that adequate effort should be made by

banks to create more awareness on the products and services

offered to the public.

b. In this age of unstable economy, there is need for

consistent research to constantly reduce cost and effectively

increase customer satisfaction to ensure that optimum

benefit is derived.

c. Financial services market should be adequately

segmented. Segmentation allows banks to tailor their

approach to the customers’ requirements, which could be

based on private individual behaviour that may be affected by

location etc. The manager needs to know how big the segment

is in volume terms, in order to decide whether to continue to

operate in the present market or to look elsewhere, where

profit may be higher.

76

d. Finally, the researcher is of the view that if the

recommendations are judiciously looked into and

implemented by the management of the firm, it will go a

long way towards improving company’s performance.

5.3 CONCLUSION

From our answers to the research, we reached the

following conclusions;

a. That consistent advertising can alter the customers’

preference and loyalty.

b. That shareholders and customers are strongly influenced

by economic factors in determining choice or service

preference.

c. That customers have their ordinal ranking of service

attributes which are respondent of any marketing mix.