tops

TRANSCRIPT

6bld0791_screenshow

INVESTOR PRESENTATION

January 2015

6bld0791_screenshow

DISCLAIMERForward‐Looking StatementsThis presentation contains forward‐looking statements regarding future events and financial performance. In some cases, you can identify these statements by words such as “may,” “might,” “will,” “should,” “except,” “plan,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” or “continue,” the negative of continue, these terms and other comparable terminology. These statements involve a number of risks and uncertainties and are based on numerous assumptions involving judgments with respect to future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond the Company’s control. There are or may be important factors that could cause our actual results to materially differ from our historical results or from any future results expressed or implied by such forward looking statements. These factors include, but are not limited to, those discussed under the section entitled “Risk Factors” in our Annual Report on Form 20‐F, filed February 14, 2014, which is available at the U.S. Securities and Exchange Commission website at www.sec.gov. The forward‐looking statements in this presentation are based upon management's reasonable belief as of the date hereof. The Company undertakes no obligation to revise or update publicly any forward‐looking statements for any reason.

2

6bld0791_screenshow

TOP SHIPS HISTORY

IPO July 2004 and follow-on after 3 months, raised abt $300 million

Fleet grew from 7 vessels in July 2004 to 33 vessels in October 2006

Became a major owner of double-hull MR and Suezmax tankers

2008-2013: well timed chartering and sale of vessels; Oct 2013 sold the entire fleet and focused on ECO MR Product Tankers

2014: acquired 6 ultra high spec ECO MR Product Tankers under construction at Hyundai Mipo

Follow-on June 2014, raised $21.3 million

3

6bld0791_screenshow

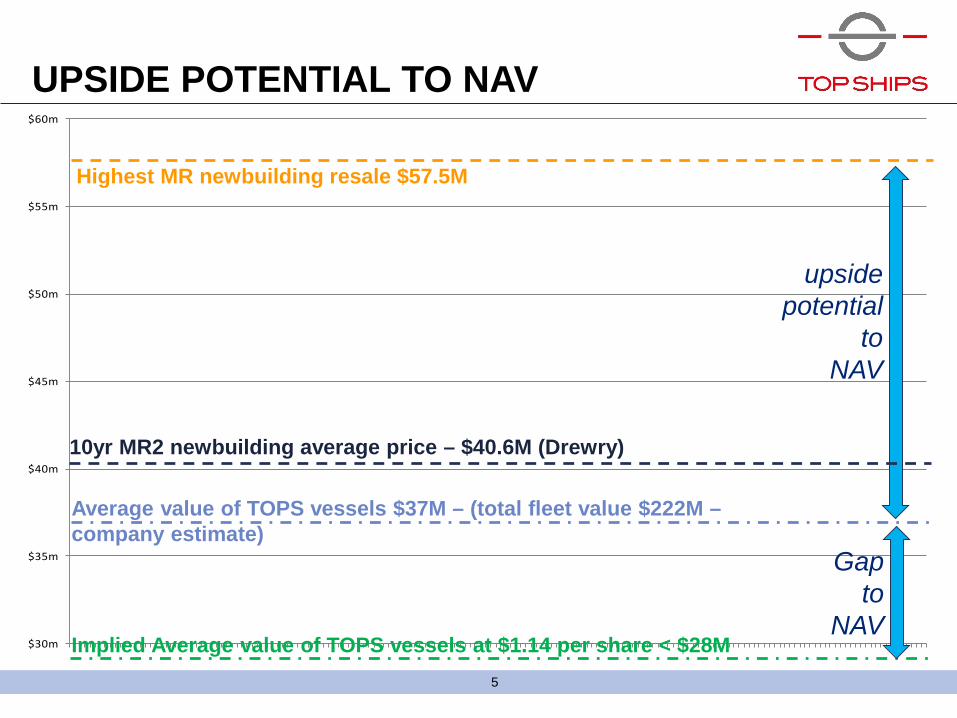

SUBSTANTIAL DISCOUNT TO NAV

STOCK AT A 72% DISCOUNT TO NAV (AS OF MARKET CLOSE 21 JANUARY 2015: $1.14)

Market Value of fleet (fully delivered basis - charter free)* 222.0 Less remaining CAPEX for newbuildings as of September 30, 2014 126.0 -

Less debt as of September 30, 2014 (net of unamortized financing fees) 19.9 -

Net Asset Value 76.1

Shares outstanding NAV/Share 4.01$

* market value is a company estimate

NET ASSET VALUE (amounts in $m)

NAV / Share18,969,989

4

6bld0791_screenshow

$30m

$35m

$40m

$45m

$50m

$55m

$60m

upside potential

to NAV

10yr MR2 newbuilding average price – $40.6M (Drewry)

Average value of TOPS vessels $37M – (total fleet value $222M –company estimate)

Highest MR newbuilding resale $57.5M

UPSIDE POTENTIAL TO NAV

Implied Average value of TOPS vessels at $1.14 per share < $28M

Gapto

NAV

5

6bld0791_screenshow

Ship Name M/T StenaWeco Energy (DELIVERED)

HULL - S407

HULL - S418

HULL - S419

HULL - S414

HULL - S417 ConstructionFirm contractsOptionsExpected delivery date

2014

$18,400

$16,000 $16,750

$15,200

$15,200

$16,000 $16,750

$16,800 $17,600

$16,200 $17,200 $18,000

2023$17,350

$16,200 $17,200 $18,000

2018 2019 2020 2021 2022$16,500 $18,100

2015 20172016

REVENUE VISIBILITY

Contracted revenue: $199 M ($124M firm / $75M options) Contracted days: 12,045 (7,665 firm / 4,380 options) Average duration of charters (firm

/ incl. options): 3.5 years / 5.5 years Average daily TCE (firm / incl. options): $16,114 / $16,538

1 vessel delivered, 5 vessels under construction with expected deliveries from Q1 2015 to Q3 2016; ALL ON TIME CHARTERS UPON DELIVERY

6

6bld0791_screenshow

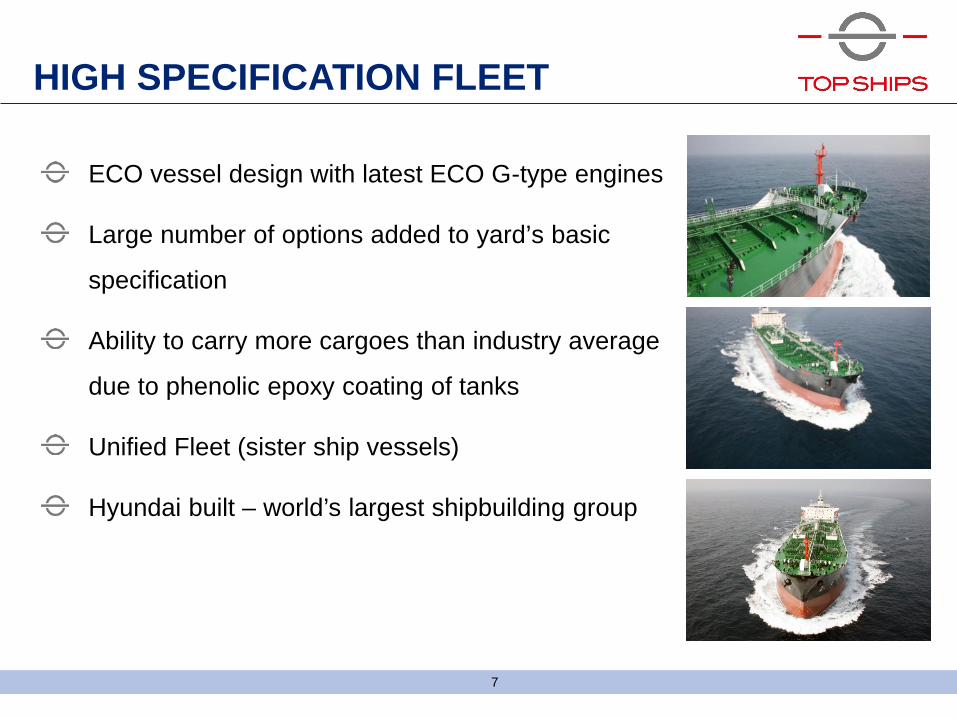

ECO vessel design with latest ECO G-type engines

Large number of options added to yard’s basic

specification

Ability to carry more cargoes than industry average

due to phenolic epoxy coating of tanks

Unified Fleet (sister ship vessels)

Hyundai built – world’s largest shipbuilding group

HIGH SPECIFICATION FLEET

7

6bld0791_screenshow

ECO FLEET – ECO VS NON ECO

ECO Vessel Characteristic Non-ECO vessel

24.3t/day Fuel consumption (NCR)* 32.6t/day

Higher by abt $2500**Fuel consumption saving

effect on daily Time Charter Equivalent rate

N/A

5% - 22%% of Fleet built from 2013onwards (currently and in

2017)***95% - 78%

Higher Charterers’ preference on vessel type Lower

Higher Rate of value

appreciation in goodmarket

Lower

Higher => Enhanced Tradeability Compliance to latest

environmental regulations

Lower => Reduced Tradeability

*** Source Drewry / Industry Sources** Assuming fuel oil cost at $300/ton* See Appendix

8

6bld0791_screenshow

9

Evangelos Pistiolis CEO and Founder22 yrs shipping experience

Alexandros Tsirikos CFO10 yrs shipping experience7 yrs with the company

Vangelis Ikonomou COO30 yrs shipping experience12 yrs with the company

Dimitris Souroullas CTO30 yrs shipping experience8 yrs with the company

92 years of combined shipping experience

STRONG MANAGEMENT TEAM

9

6bld0791_screenshow

“BP plc”, is a British multinational oil and gas company headquartered in London, England. It is one of the six oil and gas “supermajors”

“NORDEN A/S“ is a Danish shipping company that was founded and listed in 1871. It operates globally in dry cargo and tankers with an active fleet of285 owned and chartered vessels.

HIGH QUALITY CHARTERERS

Stena Weco A/S has a fleet of about 50 MR tankers with offices in Europe (Copenhagen, Denmark), USA (Houston, Texas) and Singapore. It is the joint venture between Stena Bulk and Weco, both established companies in the petroleum product transportation industry.

10

6bld0791_screenshow

New refining capacity closer to the oil reserves, Middle East in particular

Limited new refinery expansion in OECD countries combined with refinery closures due to poor margins

Arbitrage trading emerging as competing refineries are opening up in many different countries

INCREASE IN TONNE MILES DUE TO:RELOCATION OF REFINERIESFAVOURABLE MARKET FUNDAMENTALS

11

6bld0791_screenshow

INCREASE IN TONNE MILES DUE TO:NEW ROUTESFAVOURABLE MARKET FUNDAMENTALS

Established RoutesNew Routes

N. Europe – N. AmericaGasoline

Mid East – EuropeGasoline, Jet Fuel

S. Korea – JapanGasoline, Gas Oil

Intra AsiaNaphtha, Gas Oil

Asia – AustraliaGasoline, Gas Oil

Mid East – AsiaNaphtha

Asia – N. AmericaJet Fuel, Gas Oil, Diesel

Mid East – N. AmericaDiesel

Intra EuropeGasoline, Naphtha, Gas Oil

Caribbean – N. AmericaGasoline, Naphtha, Gas Oil

N. America – S. AmericaDiesel

N. America – EuropeDiesel

Seaborne Refined Products Trades

Principal Load/Discharge Zones

Source: Drewry

12

6bld0791_screenshow

US is now a major net exporter of products

US crude oil production has risen to levels unseen in 22 years

Due to restrictions in US crude oil exports, excess US crude oil is refined and exported to Europe, South America and Far East

Around 0.5m barrels per day of extra refining capacity has been added to US Gulf refineries in the last few years

FAVOURABLE MARKET FUNDAMENTALSINCREASE IN TONNE MILES DUE TO: RISE IN US PRODUCT EXPORTS

Source: Drewry

Exports of petroleum products

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

1/1/2002 1/1/2003 1/1/2004 1/1/2005 1/1/2006 1/1/2007 1/1/2008 1/1/2009 1/1/2010 1/1/2011 1/1/2012 1/1/2013 1/1/2014

United States Saudi Arabia India

13

6bld0791_screenshow

TOP SHIPS: A GROWTH PLATFORMKEY HIGHLIGHTS

TOPS is the only ECO MR Pure Play in the market

Stock at substantial discount to current NAV estimate

Upside potential for NAV as vessel values appreciate towards historical averages

High specification ECO Fleet

Strong management team with proven track record and familiarity with

growth

Revenue visibility with high quality Charterers

Favourable market fundamentals

14