towards new cluster support schemes

TRANSCRIPT

ClusterAgentur Baden-Württemberg

- Towards a Systematic Cluster Support Scheme -

04. March 2015

CEO

Dr. Gerd Meier zu Köcker

ClusterAgentur Baden-Württemberg

Where are we today?

Current and Future Challenges

• Wind energy goes offshore

• Food & packaging advanced packages

•Manufacturing goes Industry 4.0

Industrial Transformation

Processes

• Biotech & Health

• ICT & Medical devices

• Communication technologies &

automotive

Increasing Convergence of

Technologies

•Creative industries

• Digital industries

• Experience industries

Emergence of New Industries

New policies

New support

schemes

Systematic

approaches to

support regional

competitiveness

© ClusterAgentur Baden-Württemberg 3

Implications

20.04.2015© ClusterAgentur Baden-Württemberg 4

• Better policies

• Better implementation of RIS / Smart Specialisation Strategies

• Implementation of new policies

• Better cluster support schemes

Cluster PolicyLevel

• Higher professionalisation

• Better services

• New services

• Stronger role / position

• Higher acceptance

Cluster Management

Level

•Roadmapping / Foresight

•Better prepared for future challenges

•Tailor-made transnational cooperation

•Higher efficiency in businessFirm Level

Better

framework

conditions

Better support

of cluster firms

Firms better

prepared for

future business

20.04.2015© ClusterAgentur Baden-Württemberg 5

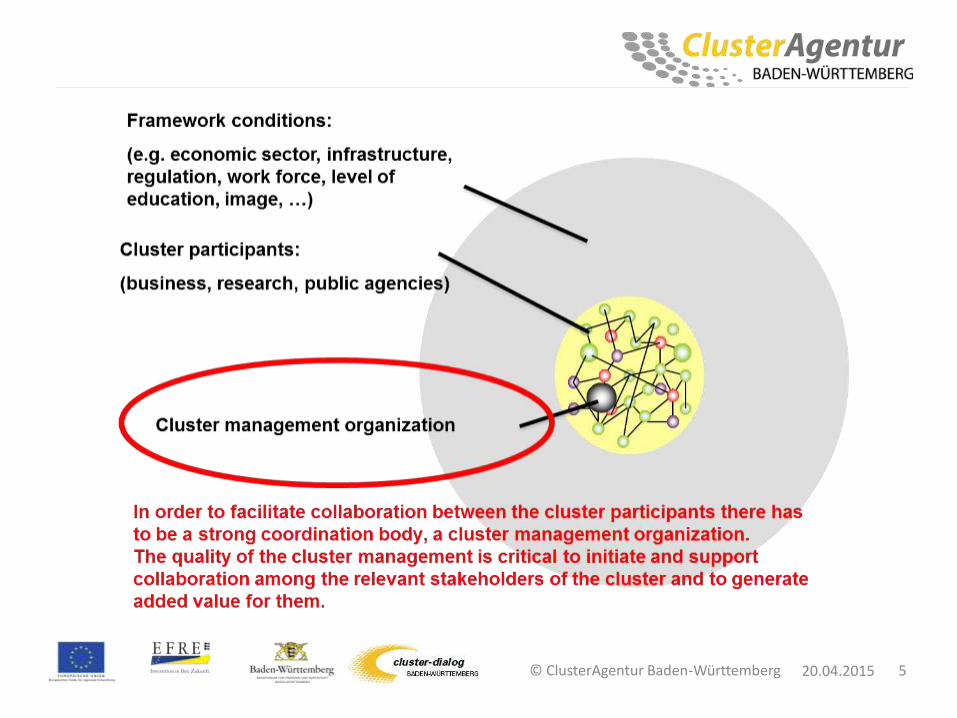

Why Cluster Management Matters

20.04.2015© ClusterAgentur Baden-Württemberg 6

Source: Lämmer-Gamp, Meier zu Köcker, Christensen, Clusters are Individuals, 2011

The Traditional Way

Funding of Cluster Organisations

Performance of Cluster Organisations basedon a Traditional Funding Approach

20.04.2015© ClusterAgentur Baden-Württemberg 8

7

7

7

7

7

Striving for Cluster Excellence In Baden-Württemberg

Diversity of Regions and Clusters in Terms of Innovation

© ClusterAgentur Baden-Württemberg

© ClusterAgentur Baden-Württemberg

Diversity of Regions and Clusters in Terms of Innovation (II)

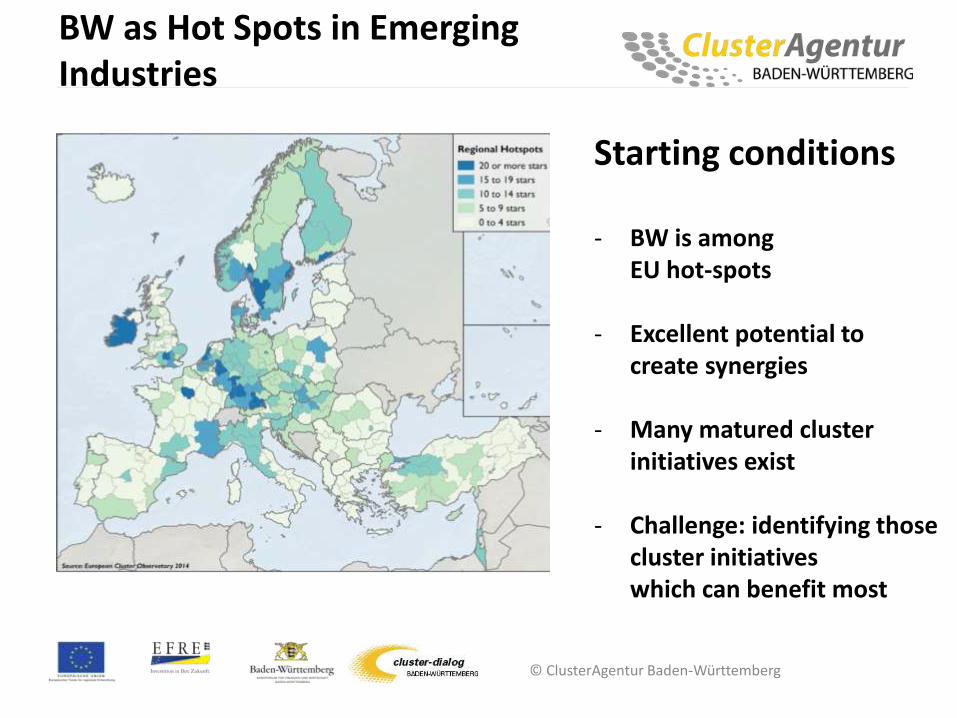

BW as Hot Spots in Emerging Industries

© ClusterAgentur Baden-Württemberg

Starting conditions

- BW is amongEU hot-spots

- Excellent potential tocreate synergies

- Many matured clusterinitiatives exist

- Challenge: identifying thosecluster initiativeswhich can benefit most

Starting Conditions

110 Cluster initiatives

16.000 Cluster participants

– On average: 150 cluster participants per cluster initiative

– About 76 % SME

FTE in Cluster organisations

20.04.2015© ClusterAgentur Baden-Württemberg 13

24%

22%

27%

27%

weniger als 0,5 FTE

0,6 - 1 FTE

1,1 - 2,5 FTE

> 2,5 FTE

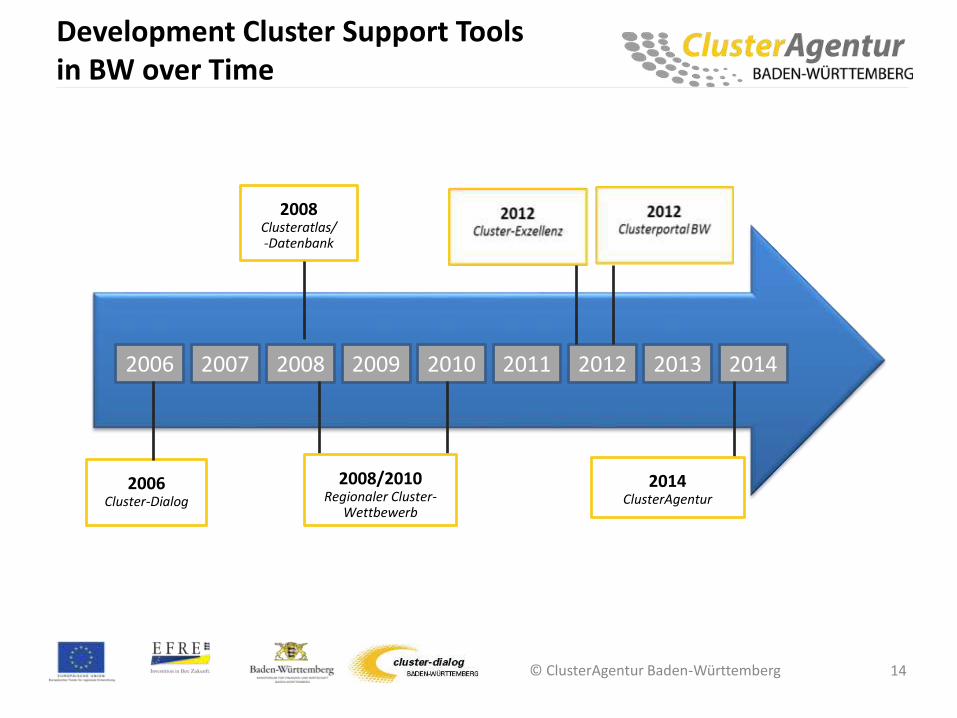

2006Cluster-Dialog

2008Clusteratlas/-Datenbank

© ClusterAgentur Baden-Württemberg

Development Cluster Support Toolsin BW over Time

14

2006 2007 2008 2009 2010 2011 2012 2013 2014

2008/2010Regionaler Cluster-

Wettbewerb

2014ClusterAgentur

-

© ClusterAgentur Baden-Württemberg

Support in defining, developing and implementingcluster strategies

Support in developing new business support services forcluster participants

Support of cluster management towards higherprofessionalisation

Governance and assessment of impact ofcluster organisations

Improved international visibility

SupportingClustermanagement Excellence

15

Strategydevelopment

New services

Professionalisation

Monitoring impacts

International visibility

New Approaches for Trans-national Strategic Partnerships

Sustainablestrategic

partnerships

Looking forexternal partners

Among clusteractors

Clusters are Driver for Innovation

Implementation of new technology transfer systems within clusters

– Cluster managements to become drivers for initiating innovations within clusterinitiatives

Setting-up of innovation partnerships

– Cluster managers to identify and initiate long-term partnerships with other regional, national or international partners

© ClusterAgentur Baden-Württemberg 17

Technology-Scouting

– Cluster managements to better identify and predicts relevant trends

– Application of toold (roadmapping etc.)

Cross-Clustering

– Cluster managements to initiate cross-sectoral cooperations

Contact

Dr.-Ing. Gerd Meier zu KöckerCEO

ClusterAgentur Baden-Württemberg

Willi-Bleicher-Straße 19

70174 Stuttgart

Gemany

E-Mail: [email protected]

Tel.: +49 711 123-3034

Further readings:

www.cluster-analysis.org

www.iit-berlin.de

© ClusterAgentur Baden-Württemberg 18

New Generation of European Cluster Observatory

New Generation of European Cluster Observatory

In the Spot: 10 Emerging Industries

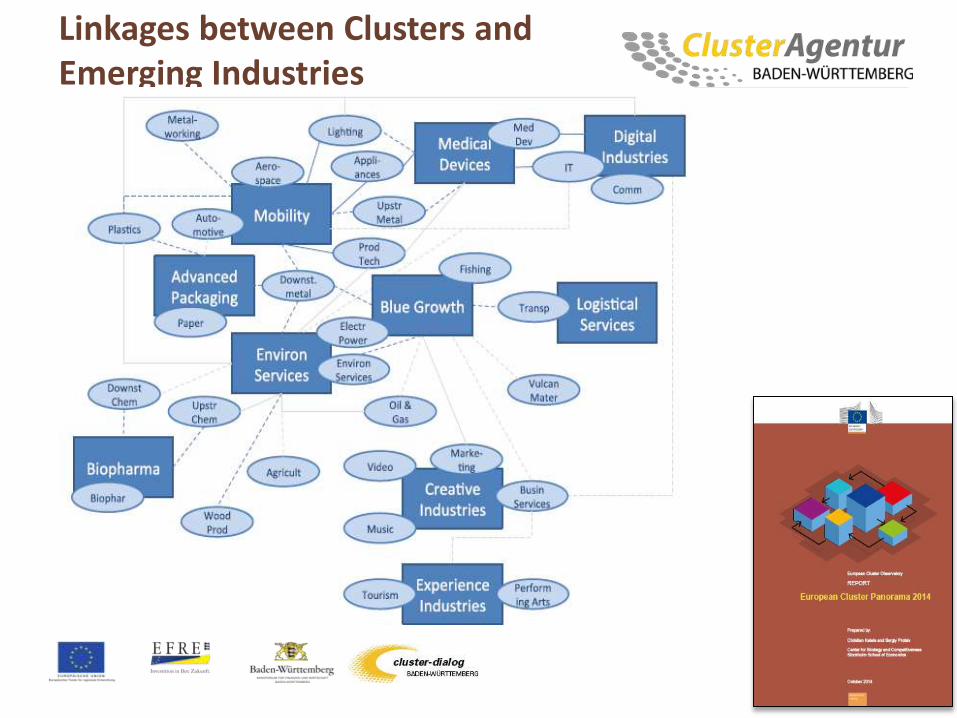

Linkages between Clusters andEmerging Industries

10 Emerging Industries at a Glance

© ClusterAgentur Baden-Württemberg

Homework

© ClusterAgentur Baden-Württemberg