town of welsh - louisianaapp1.lla.la.gov/publicreports.nsf/3976e2792c28fd82862573c90074f935/...town...

TRANSCRIPT

TOWN OF WELSH, LOUISIANA

ANNUAL FINANCIAL REPORT

MAY 31,2007

Under provisions of state law, this report is a publicdocument. A copy of the report has been submitted tothe entity and other appropriate public officials. Thereport is available for public inspection at the BatonRouge office of the Legislative Auditor and, whereappropriate, at the office of th^parish clerk of court.

Release Date // '

TOWN OF WELSH, LOUISIANA

ANNUAL FINANCIAL REPORTYear Ended May 31, 2007

TABLE OF CONTENTS

Page

INTRODUCTORY SECTION

Title PageTable of Contents 2-3List of Principal Officials 4

FINANCIAL SECTION

Report of Independent Auditors 5-6

Required Supplementary Information:Management's Discussion and Analysis 7-14

Basic Financial Statements:Government-Wide Financial Statements:

Statement of Net Assets 16-17Statement of Activities 18-19

Fund Financial Statements:Governmental Funds

Balance Sheet - Governmental Funds 21-22Statement of Revenues, Expenditures and Changes in

Fund Balances 23-26Reconciliation of Statement of Revenues, Expenditures

and Changes in Fund Balances of Governmental Fundsto the Statement of Activities 27

General Fund:Statement of Revenue, Expenditures and Changes in

Fund balance - Budget and Actual - General Fund 28-29

Sales Tax 1996:Statement of Revenue, Expenditures and Changes in

Fund balance - Budget and Actual - Sales Tax 30

Page

Proprietary Fund - Utility Enterprise Fund:Statement of Net Assets 31Statement of Revenues, Expenditures and Changes in

Net Assets 32Statement of Cash Flows 33

Notes to Financial Statements 34-53

Other Supplementary Information - Nonmajor Governmental Funds:

Combining Balance Sheet-Nonmajor Governmental Funds 55-56Combining Statement of Revenues, Expenditures, and Changes in

Fund Balance-Nonmajor Governmental Funds 57-58Schedule of Compensation Paid to Governing Board 59Schedule of Number of Utility Customers-Public Utility

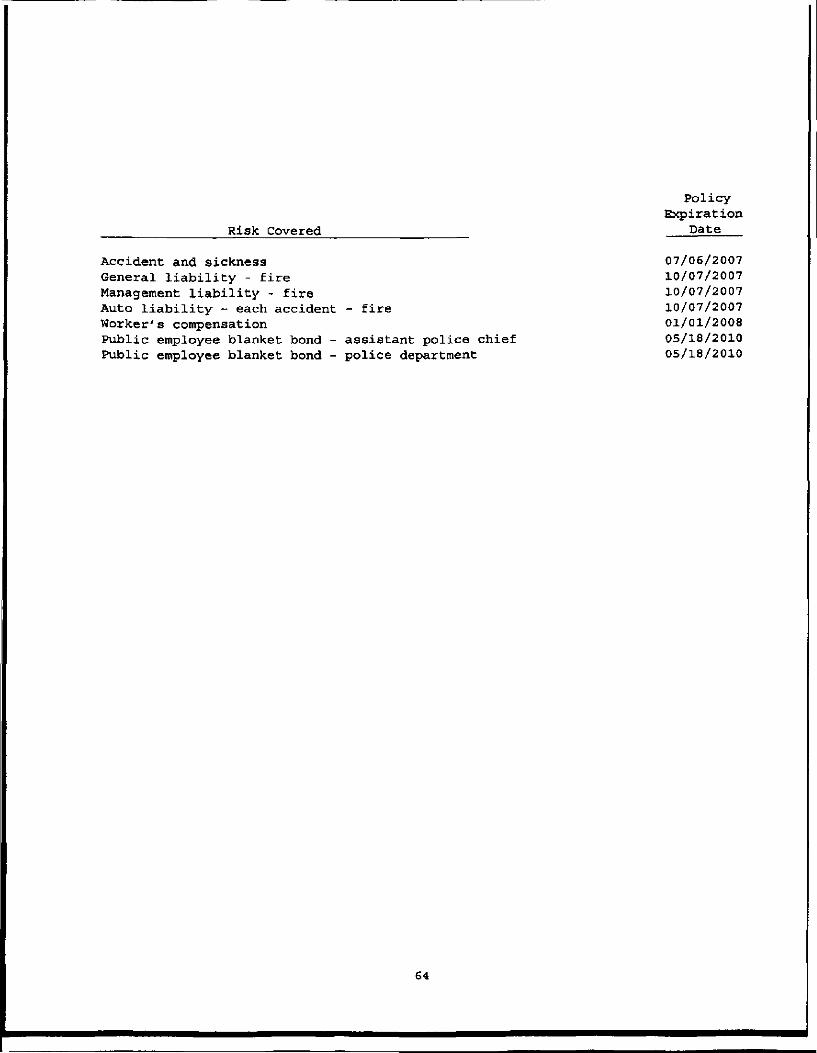

Enterprise Fund 60Schedule of Insurance in Force 61-64

REPORT OF INDEPENDENT AUDITORS ON INTERNAL CONTROL ANDCOMPLIANCE

Report on Compliance and on Internal Control OverFinancial Reporting Based on an Audit of FinancialStatements Performed in Accordance with GovernmentAuditing Standards 66-68

Schedule of Findings and Questioned Costs 69-70

Summary Schedule of Prior Audit Findings Based on anAudit of Financial Statements Performed in Accordancewith Government Auditing Standards 71

TOWN OF WELSH, LOUISIANA

May 31, 2007

MAYOR

The Honorable Carolyn Louviere

BOARD of ALDERMAN

Mr. Allen Ardoin Ms. Leona VanicorMr. Charles Drake Mrs. Gloria VineyMs. Becky Hudson

LEGAL COUNSEL

Mr. Richard M. Arceneaux

TOWN CLERK

Ms. Linda LeBlanc

MCELROY, QUIRK & BURGHA ProfessionaJ Corporation • Certified Public Accountants • Since 1925

800 Kirby Street • P.O. Box 3070 • Lake Charles, LA 70602-3070

337 433-1063 • Fax 337 436-6618 • Web page: www.mqb-cpa.com

09418.000 Town 0( Mel in Audit 5/31/07 nelsh FR

Cari W. Comeaux, CPAGus W. Schram, III, CPA, CVAMartin L Chchoisky, CPA, CFERobert M. Gani, CPA, MTMollie C. Brouward, CPAJason L. Gurllory, CPACregP.Nwiuiii,CPA,CFP™Billy D. Fisher, CPAJoe G. fehoff, II, CPA. CVA

MQBOtray J. Woods, Jr., CPA, InactiveRobert R Cargile, CPA, InactiveWilliam A. Mancuso, CPA, RetiredBarbara Mutton Gonzales, CPA, RetiredJudson J. McCann, Jr., CPA, Retired

CFE - Certified Fraud ExaminerMT - Mitten of TaxationCVA - Certified Valuation tuntymCFI* - Certified Financial Planner

REPORT OF INDEPENDENT AUDITORS

Honorable Mayor and Board of AldermanTown of WelshWelsh, Louisiana

We have audited the accompanying financial statements of the governmentalactivities, the business-type activities, each major fund, and the aggregateremaining fund information of the Town of Welsh, Louisiana as of and for the yearended May 31, 2007, which collectively comprise the Town's basic financialstatements, as listed in the table of contents. These financial statements are theresponsibility of the Town's management. Our responsibility is to express opinionson these financial statements based on our audit.

We conducted our audit in accordance with auditing standards generally acceptedin the United States of America and the standards applicable to financial auditscontained in Government Auditing Standards issued by the Comptroller General of theUnited States. Those standards require that we plan and perform the audit to obtainreasonable assurance about whether the financial statements are free of materialmisstatement. An audit includes examining, on a test basis, evidence supporting theamounts and disclosures in the financial statements. An audit also includesassessing the accounting principles used and significant estimates made bymanagement, as well as evaluating the overall financial statement presentation. Webelieve that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, inall material respects, the respective financial position of the governmentalactivities, the business-type activities, each major fund, and the aggregateremaining fund information of the Town of Welsh, Louisiana as of May 31, 2007, andthe respective changes in financial position and cash flows, where applicable,thereof and the budgetary comparison for the general fund and major special revenuefund for the year then ended, in conformity with accounting principles generallyaccepted in the United States of America.

Members American Institute of Certified Public Accountants * Society of Louisiana Certified Public Accountants

In accordance with Government Auditing Standards, we have also issued a reportdated November 12, 2007, on our consideration of the Town of Welsh's internalcontrol over financial reporting and our tests of its compliance with certainprovisions of laws, regulations, contracts and grants. The purpose of that reportis to describe the scope of our testing of internal control over financial reportingand compliance and the results of that testing and not to provide an opinion on theinternal control over financial reporting or on compliance. That report is anintegral part of an audit performed in accordance with Government Auditing Standardsand should be read in conjunction with this report in considering the results of ouraudit.

Management's discussion and analysis on pages 7 through 14 is not a requiredpart of the basic financial statements but is supplementary information required byaccounting principles generally accepted in the United States of America. We haveapplied certain limited procedures, which consisted principally of inquiries ofmanagement regarding the methods of measurement and presentation of the requiredsupplementary information. However, we did not audit the information and express noopinion on it.

Our audit was conducted for the purpose of forming opinions on the financialstatements that collectively comprise the Town of Welsh's basic financial statements.The introductory section combining nonmajor fund financial statements and othersupplementary information are presented for purposes of additional analysis and arenot a required part of the basic financial statements. The combining nonmajor fundfinancial statements have been subjected to the auditing procedures applied in theaudit of the basic financial statements and, in our opinion, are fairly stated inall material respects in relation to the basic financial statements taken as awhole. The introductory section and other supplementary information have not beensubjected to the auditing procedures applied in the audit of the basic financialstatements and, accordingly, we express no opinion on them.

Under Louisiana Revised Statute 24:513, this report is distributed by theLegislative Auditor as a public document.

Lake Charles, LouisianaNovember 12, 2007

MANAGEMENT'S DISCUSSION AND ANALYSIS

Within this section of the Town of Welsh Louisiana's annual financial report, theTown's management is pleased to provide this narrative discussion and analysis of thefinancial activities of the Town for the fiscal year ended May 31, 2007. The Town'sfinancial performance is discussed and analyzed within the context of theaccompanying financial statements and disclosures following this section.

FINANCIAL HIGHLIGHTS

• The Town's assets exceeded its liabilities by $8,638,567 (net assets) for thefiscal year reported. Of this amount, $2,233,513 (unrestricted net assets)may be used to meet the government's ongoing obligations to citizens andcreditors in accordance with the Town's fund designation and fiscal policies.

• Total expenditures of $5,643,515 exceeded total revenues of $6,559,314, whichresulted in a current year surplus of $915,799.

• The Town's governmental funds reported a total ending fund balance of$2,958,537 this year. This compares to the prior year ending fund balance of$2,524,079 reflecting an increase of $434,458 during the current year.

The above financial highlights are explained in more detail in the "financialanalysis" section of this document.

USING THE ANNUAL REPORT

This annual report consists of a series of financial statements. The Statement ofNet Assets and the Statement of Activities provide information about the activitiesof the Town as a whole and present a longer-term view of the Town's finances. Forgovernmental activities, these statements tell how these services were financed inthe short-term as well as what remains for future spending. Fund financialstatements also report the Town's operations in more detail than the government-widestatements by providing information about the Town's most significant funds.

Reporting the Town as a Whole

One of the most important questions asked about the Town's finances is, uls the Townas a whole better off or worse off as a result of the year's activities?" TheStatement of Net Assets and the Statement of Activities report information about theTown as a whole and about its activities in a way that helps answer this question.These statements include all assets and liabilities using the accrual basis ofaccounting, which is similar to the accounting used by most private-sectorcompanies. All of the current year's revenues and expenses are taken into accountregardless of when cash is received or paid.

These two statements report the Town's net assets and changes in them. The Town's netassets, the difference between assets and liabilities, are one way to measure theTown's financial health, or financial position. Over time, increases or decreases inthe Town's net assets are one indicator of whether its financial health is improvingor deteriorating. You will need to consider other non-financial factors, however,such as changes in the Town's taxpayer base and the condition of the Town's roads toassess the overall health of the Town.

In the Statement of Net Assets and the Statement of Activities, we divide the Towninto two kinds of activities:

• Governmental activities - Most of the Town's basic services are reported hereincluding police, fire, streets and highways, parks and recreation, economicdevelopment, and general administration. Sales and property taxes, franchisefees, and state and federal grants finance most of these activities.

• Business-type activities - The Town charges a fee to customers to help itcover all or most of the cost of certain services it provides. The Town'sutility system is reported here.

Reporting the Town's Most Significant Funds

The fund financial statements provide detailed information about the mostsignificant funds - not the Town as a whole. Some funds are required to beestablished by State law and bond covenants. However, the Town Council establishesmany other funds to help it control and manage money for particular purposes or toshow that it is meeting legal responsibilities for using certain taxes, grants, andother money. The Town's two types of funds, governmental and proprietary, usedifferent accounting approaches.

• Governmental funds - Most of the Town's basic services are reported ingovernmental funds, which focus on how money flows into and out of thosefunds and the balances left at year end that are available for spending.These funds are reported using an accounting method called modified accrualaccounting, which measures cash and all other financial assets that canreadily be converted to cash. The governmental fund statements provide adetailed short-term view of the Town's general government operations and thebasic services it provides. Governmental fund information helps youdetermine whether there are more or fewer financial resources that can bespent in the near future to finance the Town's programs. We describe therelationship (or differences) between governmental activities (reported inthe Statement of Net Assets and the Statement of Activities) and governmentalfunds in reconciliation at the bottom of the fund financial statements.

Proprietary funds - When the Town charges customers for the services itprovides, these services are generally reported in the same way that allactivities are reported in the Statement of Net Assets and the Statement ofActivities. In fact, the Town's enterprise fund is the same as the business-type activities we report in the government-wide statements but provide moredetail and additional information, such as cash flows.

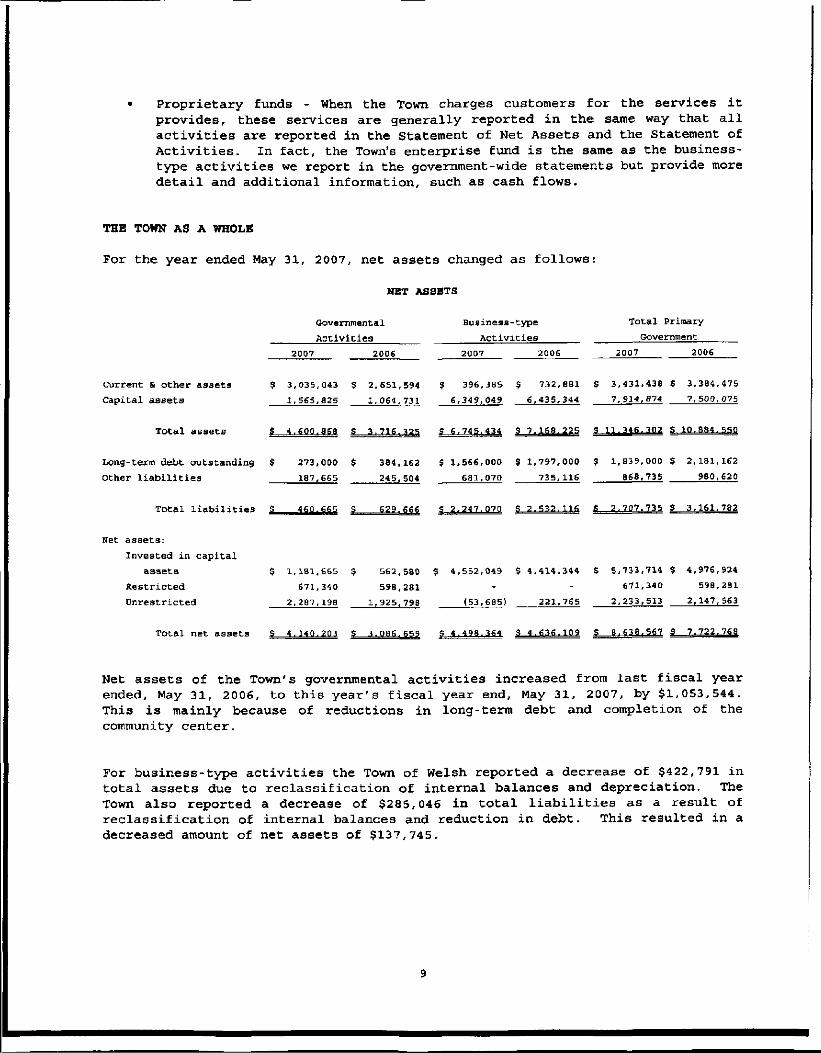

THE TOWN AS A WHOLE

For the year ended May 31, 2007, net assets changed as follows:

NET ASSETS

Current 6 other assets

Capital assets

Total assets

Governmental

Activities

2007 2006

Business-type

Activities

2007

Total Primary

Government

2007 2006

S 3,035,043 $ 2,651,594 $ 396,385 $ 732,881 $ 3,431,438 $ 3,384,475

1,565.825 1,064.731 6,349,049 6,435,344 7,914,874 7.500,075

S 4.600.868 S 3.716.325 S 6.745.434 S 10.884.550

Long-term debt outstanding $ 273,000 $ 384,162 $ 1,566,000 $ 1,797,000 $ 1,839,000 $ 2,181,162

Other liabilities 187.665 245.504 681.070 735,116 868,735 980,620

Total liabilities S 460.665 5 2.247.070 S 2.532.116 S 3.161.782

Net assets:

Invested in capital

assets $ 1,181,665 $ 562,580 $ 4,552,049 S 4,414,344 $ 5,733,714 $ 4,976,924

Restricted 671,340 598,281 - - 671,340 598,281

Unrestricted 2,287.198 1.925.798 (53,685) 221.765 2,233,513 2.147,563

Total net assets S 4.140.203 S 4.498.364 S 4.636.109

Net assets of the Town's governmental activities increased from last fiscal yearended, May 31, 2006, to this year's fiscal year end. May 31, 2007, by $1,053,544.This is mainly because of reductions in long-term debt and completion of thecommunity center.

For business-type activities the Town of Welsh reported a decrease of $422,791 intotal assets due to reclassification of internal balances and depreciation. TheTown also reported a decrease of $285,046 in total liabilities as a result ofreclassification of internal balances and reduction in debt. This resulted in adecreased amount of net assets of $137,745.

The following table provides a summary of the Town's changes in net assets:

CHANGES IN NET ASSETS

Governmental

Activities

2007 2006

Business-typeActivities

2007 2006

Total Primary

Government

2007 2006

Program revenues:

Charges for services $ 929,932

Operating grants 64,592

Capital grants 610,241

General revenues;

Property taxes 80,189

Other taxes 784,263

Other general revenues 278,812

Total revenues 2,748.029

Program expenses)

General government 399,645Public safety 1,008,027Highways and streets 252,355Culture and recreation 165,288

Sanitation 134,170

Electric, water and

sewer -

Total expenses 1,959,485

Excess (deficiency)

before transfers 788,544

Transfers in (out) 265,OOP

increase (decrease)

in net assets

854,966

585,417

182,376

80,079

752,589

178,540

2,633,967

349,906

1.026,043

624,130

96,553

181,534

2,278,166

355,801

252,282

$ 3,743,851 $ 3,873,656

349,635

67,434

3,811,285

(137.745)

54,699

4,277,990

3.684,030 3.985,652

3,684,030 3.985,652

$ 4,673,783 $ 4,728,622

64,592 935,052

610,241 182,376

6,

1,

3,

5,

80,

784,

346,

559,

399,

008,

252,

165,

134,

684,

613,

189

263

426

494

645

027

355

238

170

030

515

80,

752,

233,

6,911,

349,

1,026,

624,

96,

181,

3,985,

6,263,

079

589

239

957

906

043

130

553

534

652

818

127,255 292,338

(265,000) (252.282)

915,979

(180)

648,139

915.799 £_ 64B.139

Governmental Activities

Revenue from governmental activities increased approximately $114,242. The increasewas due primarily to increased garbage fees and increased distributions from JeffDavis Landfill. Also, the increase in revenue received from the LCDBG grant offsetthe decrease in revenue received from FEMA compared to 2006. Expenses fromgovernmental activities decreased $(318,681). This was due to a decrease in stormrepairs and debris removal.

10

To aid in the understanding of the Statement of Activities some additionalexplanation is given. Of particular interest is the format that is significantlydifferent than a typical Statement of Revenues, Expenses, and Changes in FundBalance. You will notice that expenses are listed in the first column with revenuesfrom that particular program reported to the right. The result is a Net(Expense) /Revenue. The reason for this type of format is to highlight the relativefinancial burden of each of the functions on the Town's taxpayers. It alsoidentifies how much each function draws from the general revenues or it is self-financing through fees.

All other governmental revenues are reported as general. It is important to notethat all taxes are classified as general revenue even if restricted for a specificpurpose.

This table presents the cost of each of the Town's programs, including the net costs(i.e., total cost less revenues generated by the activities). The net costsillustrate the financial burden that was placed on the Town's taxpayers by each ofthese functions.

General governmentPublic safetyHighway and streetsSanitationCulture and recreation

Total

Total Costof Services

2007 2006

$ 399,645 $1,008,027 1,252,355134,170165,288

349,026,624,

181,96,

906043130534553

$ 1.959.485 $ 2.278.166

Total Costof Services

2007 2006

$

$

(335,816) $454,819249,839(151,647)137,525

354.720 S

36,740333,774188,28649,00747,600

655.407

Business-type Activities

The total revenues of the Town's business-type activities (see table 2) decreased by$(466,705) and total expenses decreased by $(301,622) from the prior year. Thisresulted in income before transfers of $127,255 in the current year as compared tolast year's income of $292,388. Net assets of the Town's business-type activitiesdecreased approximately $(137,745) from the prior year. The factors driving theseresults include:

• Increased charges for electricity due to fuel adjustments

• Increased costs to purchase and distribute electricity

• Costs related to storm recovery

11

THE TOWN'S FUNDS

Governmental funds

The focus of the Town's governmental funds is to provide information on near-terrainflows, outflows, and balances of spendable resources. Such information is usefulin assessing the Town's financing requirements. In particular, unreserved fundbalance may serve as a useful measure of a government's net resources available forspending at the end of the fiscal year.

As the Town completed the year, its governmental funds reported a combined fundbalance of $2,958,537, compared to last year's total of $2,524,079, an increase of$434,458.

Proprietary fund

The Town's proprietary fund statements provided the same type of information found inthe government-wide financial statements, but in more detail. Analysis of theproprietary fund consists of the same information provided in the business-typeactivities section commented on above.

BUDGETARY HIGHLIGHTS

The General Fund - The Town amended the budget twice during the year. The firstamendment was to increase projected revenues from police fines and projectedexpenditures for the police department. The second amendment was to reflect stormrelated grants and expenditures in the fire and street departments,

CAPITAL ASSETS

The Town's investment in capital assets, net of accumulated depreciation, forgovernmental and business-type activities as of May 31, 2007 was $1,565,825 and$6,349,049 respectively. The following table provides a summary of capital assetactivity.

BuildingsUtility systemLandFurniture and

equipmentConstruction in

progressVehicles

Totals

Capital Assets

GovernmentalActivities

Business-typeActivities

2007 2006 2007 2006Totals

2007 2006

$ 947,961 $ 164,870 $ $ $ 947,961 $ 164,8706,220,844 6,307,139 6,220,844 6,307,139

67,599 67,599 128,205 128,205 195,804 195,804

178,342

371,923

193,542

240,853397,867

S 1.565.825 S 1.064.731 S 6 . 3 4 9 . Q 4 9 S 6 . 4 3 5 . 3 4 4

178,342

371,923

7.914.874

193,542

240,853397.867

7 . S O D . 0 7 5

12

Major Capital Asset Additions:

Item 1 - Additional construction in progress related to the Community Center.

Item 2 - Improvements to the utility system.

Item 3 - Purchased five police vehicles and one excavator.

See Note 6 for additional information.

LONG-TERM DEBT

At the end of the fiscal year, the Town had total bonded debt outstanding of$2,181,159, a decrease of $341,992 from last year as follows:

Certificate of

indebtednessGeneral obligation

bonds

Revenue bonds

Capital lease

obligations

Totals

OUTSTANDING DEBT

Governmental

Activities

Business-type

Activities Totals

2007 2006 2007 2006 2007 2006

$ $ 6,400 $ 164,000 $ 185,000 $ 164,000 $ 191,400

356,000 438,0001,633,000 1,836,000

356,000 438,000

1,633,000 1,836,000

28,160 57,751 28,160 57,751

S 2.523.151

Additional detail is provided in the financial statements and notes (Note 8).

ECONOMIC FACTORS AFFECTING THE TOWN

Since the primary revenue stream for the Town is sales taxes, the Town's sales taxrevenues are subject to changes in the economy. Since sales are considered an"elastic" revenue stream, tax collections are higher in a flourishing economy andlower in a depressed economy. During the fiseal year ending May 31, 2007, weexperienced a good year of sales tax revenue. For the end of 2007, the Town is notexpecting much change in sales tax.

13

CONTACTING THE TOWN'S FINANCIAL MANAGEMENT

This financial report is designed to provide a general overview of the Town'sfinances, comply with finance-related laws and regulations, and demonstrate theTown's commitment to public accountability. If you have any questions about thisreport or would like to request additional information/ contact the Town's Clerk,Linda LeBlanc, P.O. Box 786, Welsh, LA 70591.

Linda LeBlancTown ClerkTown of Welsh

14

GOVERNMENT-WIDE FINANCIAL STATEMENTS

15

TOWN OF WELSH, LOUISIANA

GOVERNMENT-WIDESTATEMENT OF NET ASSETS

May 31, 2007

ASSETS

Cash and cash equivalentsInvestmentsReceivables (net, where applicable, of

allowance for uncollectibles) :AccountsUnbilled accountsAccrued interestTaxesGrants

InventoryPrepaid expensesInternal balancesOther current assetsRestricted assets:

Cash and cash equivalentsInvestments

Capital assets:Land improvements and construction

in progressBuildings, furniture and equipment,

net of depreciationOther assets:

Bond issue cost, netTotal assets

LIABILITIES

Accounts payableAccrued liabilitiesCash overdraftNoncurrent liabilities:

Due within one yearDue in more than one year

Payable from restricted assetsTotal liabilities

GovernmentalActivities

$ 211,682724,954

57,116--

1,80446,302

--

993,056129

_

1,000,000

67,599

1,498,226

-4, 600,868

57,684-

18,821

111,160273,000

-460,665

BusinessType

Activities

$ 110,518 $60,724

282,56076,0002,284

--

139,8886,761

(993,056)637

115,725584,647

128,205

6,220,844

9,6976,745,434

387,28820,447

-

231,0001,566,000

42,3352,247,070

Total

322,200785,678

339,67676,0002,2841,80446,302139,8886,761

•766

115,7251,584,647

195,804

7,719,070

9,69711,346,302

444,97220,44718,821

342,1601,839,000

42,3352,707,735

(continued on next page)

16

NET ASSETS

TOWN OF WELSH, LOUISIANA

GOVERNMENT-WIDESTATEMENT OF NET ASSETS

May 31, 2007

GovernmentalActivities

Investment in capital assets, net ofrelated debt

Restricted for:Debt serviceVarious purposes-sales tax

Unrestricted

Total net assets

1,181,665

BusinessType

Activities

4,552,049

Total

5,733,714

$

397,890273,450

2,287,198

4,140,203

' --

(53,685)

S 4,498,364 $

397,890273,450

2,233,513

8,638,567

See accompanying notes to financial statements

17

TOWN OF WELSH, LOUISIANA

GOVERNMENT-WIDESTATEMENT OF ACTIVITIESYear Ended May 31, 2007

Functions/Programs

Government activities:General governmentPublic safetyHighway and streetsSanitationCulture and recreation

Total governmentalactivities

Business-type activities:Water utilitySewer utilityElectric utility

Total business-typeactivities

Total government

Program Revenues

Expenses

Fees, Finesand Operating Capital

Charges for Grants and Grants andServices Contributions Contributions

$ 399,645 $ 125,220 $1,008,027 488,616252,355134,170

610,24164,592

165,288

1,959,485

251,751333,142

3,099,137

3,684,030

2,516285,81727,763

929,932 64,592

305,641253,893

3,184,317

3,743,851

610,241

$ 5.643.515 5 4.673.783 £_ 64.592 610.241

General revenues:Ad valorem taxesSales taxesFranchise taxesGaming taxesOther taxesInterest earnedMiscellaneous

TransfersTotal general revenues

and transfers

Change in net assets

Net assets at beginning of year

Net assets at end of year

See accompanying notes to financial statements

18

Net (Expenses) Revenue andChanges in Net Assets

BusinessGovernmental TypeActivities Activities Total

335,816 $ $ 335,816(454,819) - (454,819)(249,839) - (249,839)151,647 - 151,647(137,525) -_ (137,525)

(354,720) - (354,720)

53,890 53,890(79,249) (79,249)85,180 85,180

59,821 59,821

(354,720) 59,821 (294,899)

80,189 - 80,189701,896 - 701,89637,645 - 37,54533,387 - 33,38711,335 - 11,33582,836 39,011 121,847195,976 28,423 224,399265,000 (265,000) -_

1,408,264 (197,566) 1,210,698

1,053,544 (137,745) 915,799

3,086,659 4,636,109 7,722,768

$ 4.140,203 $ 4.498.364 S 8.638.567

19

FUND FINANCIAL STATEMENTS

20

TOWN OP WELSH, LOUISIANA

BALANCE SHEET - GOVERNMENTAL FUNDSMay 31, 2007

ASSETS

CashCash - sinkingInvestmentsReceivables:

TaxesAccountsGrants

Due from other fundsRestricted assets:

Investments

Total assets

LIABILITIES AND FUND BALANCE

Liabilities:Cash overdraftAccounts payableAccrued liabilitiesDue to other funds

Total liabilities

Fund balances:ReservedUnreserved

Total fund balances

Total liabilities and fund balances

General

$ 59,128

527,940

1,80457,116

1,012,824

1,000,000

$ 2.658,812

DebtServiceSales Tax1996

$ 85,205

120,231

SpecialRevenueSales Tax

1996

$ 46,555

59,658

174,405

S 379.841

86,539

$ 192.752

$57,517

(129)290,096

$

347,484

1,000,0001,311,3292,311,329

379,841379,841

$ 2.658.813 $ 379.841

192,752192,752

$ 192.752

Amounts reported for governmental activities in the statementof net assets are different because:Total fund balance - total governmental fundsCapital assets used in governmental activities are not financial

resources and, therefore, are not reported in the fundsLong-term liabilities, including bonds payable, are not due and

payable in the current period and, therefore, are not reportedin the funds

See accompanying notes to financial statements

21

Non-Major Total

Governmental Governmental

Grant Funds Funds

$ 12,374 $ 8,283 $ 211,545

137 137

7f125 10,000 724,954

1,804

57,116

46,302 - 46,302

80,685 1,354,453

- - 1,000,000

65.801 3 99,105 $ 3,396.311

$ 18,821

167

-

190

19,178

79,926

79,926

$ 18,821

57,684

(129)

361,396

437,772

1,000,000

1,958,537

2,958,537

71,110

71,110

(5,311)

(5,311)

65,799 $ 99.104 $ 3.396.309

$ 2,958,537

1,565,826

(384,160)

S 4.140.203

22

TOWN OF WELSH, LOUISIANA

STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCESGOVERNMENTAL FUNDS

Year Ended May 31, 2007

General

DebtServiceSales Tax1996

SpecialRevenueSales Tax

1996

Revenues:TaxesLicenses and permitsIntergovernmentalCharges for servicesFines and forfeitsInterest incomeVending machine commissionJeff Davis Sanitary LandfillGrantsAssessmentsMiscellaneous

Total revenues

Expenditures:Current:

General governmentPoliceFireStreetSanitationRecreationCemeteriesAirportHealth and welfarePaving/streetsEconomic development

Debt Service:Bond principalBond interest

Total expenditures

Excess (deficiency) of revenuesover expenditures

122,755111,41617,135456,718359,28267,12533,387122,18364,592

63,0701,417,663

297,833887,92390,76967,359144,651144,2598,0334,3725,538

43,939

29,5901,737

1,726,003

(308,340)

$ 350,948

12,481

363,429

184,390

82,00014,79596,795

(96,795)

184,390

179,039

23

Grant

Non-MajorGovernmental

Funds

TotalGovernmental

Funds

350,948

2,404

610,241

612,645

826

2,516

824,651111,41617,135456,718359,28282,83633,387122,183674,8332,51663,070

354,290 2,748,027

557,157 7,472 862,462887,92390,76967,359144,651144,2598,0334,3725,538

184,39043,939

6,400352

557,157 14,224

117,99016,684

2,578,569

55,488 340,066 169,458

(continued on next page)

24

TOWN OF WELSH, LOUISIANA

STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCESGOVERNMENTAL FUNDS

Year Ended May 31, 2007

Other financing sources (uses):Operating transfers inOperating transfers out

Total other financing sources (uses)

Excess (deficiency) of revenues andother sources over expendituresand other uses

Fund balance at beginning of year

Fund balance at end of year

General

614,316

(111)614,205

305,865

2,005,464

5 2.311.329

DebtServiceSales Tax

1996

175,864

175,864

79,069

300,772

SpecialRevenueSales Tax

1996

(181,069)(181,069)

(2,030)

194,782

379.841 $ 192.752

See accompanying notes to financial statements

25

Non-Major TotalGovernmental Governmental

Grant Funds Funds

790,180(344,000) (525,180)(344,000) (265,000)

55,488 (3,934) 434,458

(60,799) 83,860 2,524,079

$ (5.311) £ 79.926 $ 2.958.537

26

TOWN OF WELSH, LOUISIANA

RECONCILIATION OF STATEMENT OF REVENUES, EXPENDITURES ANDCHANGES IN FUND BALANCES OF GOVERNMENTAL FUNDS

TO THE STATEMENT OF ACTIVITIESYear Ended May 31, 2007

Amounts reported for governmental activities in thestatement of activities different because:

Net change in fund balance - total governmental funds $ 434,458

Governmental funds report capital outlays as expenditures.However, in the statement of activities the costs ofthose assets is allocated over their estimated usefullives and reported as depreciation expense. This isthe amount by which capital outlays exceeded depreciationin the current period. 501,096

Principal payments of long-term debt 117, 990

Change in net assets of governmental activities $ 1,053,544

See accompanying notes to financial statements

27

TOWN OF WELSH, LOUISIANAGENERAL FUND

STATEMENT OF REVENUE, EXPENDITURES AND CHANGES IN FUND BALANCEBUDGET AND ACTUAL

Year Ended May 31, 2007

Revenues:TaxesLicenses and permitsIntergovernmentalCharges for servicesFines and forfeitsInterest incomeVending machine incomeGrantsLandfillMi see1laneous

Total revenues

Expenditures:Current:

General governmentPoliceFireStreetSanitationRecreationCemeteriesAirportHealth and welfareEconomic development

Total expenditures

Excess (deficiency)of revenues overexpenditures

Other financing sources (uses):Operating transfers inOperating transfers out

Total other financingsources (uses)

^Budgeted Amounts^

Variance WithFinal BudgetPositive

Original

$ 118,20097,00075,700262,100358,00050,00032,200

-

45,0006,000

1,044,200

Final

$ 122,

111,16,

452,

356,

67,

32,

64,

122,

63,

1,407,

Actual (Unfavorable)

200000700100800000200

000

000

000000

$ 122,

111,

17,

456,

359,

67,

33,

64,

122,

63,

1,417,

755 $

416

135

718

282

125

387

592

183

251

844

555

416

435

4,6182,482125

1,187592

183

251

10, 844

376

950

98

78

194

136

12

12

5

16

1,881

,043,971,470,330

,455,133,950,350,800,250,752

298,914,98,

68,

176,144,

8,

6,

5,

44,

1,766,

043

971

470

330

455

133

950

718

800

250

120

297,

887,

90,

67,

175,

144,

8,

4,

5,

43,

1,726,

833

923

769

359

978

259

033

372

538

939

003

210

27,0487,701971

477

(126)917

2,346262

311

40, 117

(837,552) (359,120) (308,159)

593,000

593,000

593,000

593,000

614,136

(111)

614,025

50,961

21,136

(111)

21,025

(continued on next page)

28

TOWN OF WELSH, LOUISIANAGENERAL FUND

STATEMENT OF REVENUE, EXPENDITURES AND CHANGES IN FUND BALANCE

BUDGET AND ACTUALYear Ended May 31, 2007

Excess (deficiency) ofrevenue and otherfinancing sources

over expendituresand other uses

Fund balance at beginning of year

Fund balance at end of year

Budgeted AmountsOriginal Final Actual

Variance WithFinal BudgetPositive

(Unfavorable)

(244,552) 233,880 305,866

2,005,464 2,005,464 2,005,464

1.760.912 S 2,239.344 S 2.311.330

71,986

71.986

See accompanying notes to financial statements

TOWN OF WELSH, LOUISIANA

SALES TAX 1996

STATEMENT OF REVENUE, EXPENDITURES AND CHANGES IN FUND BALANCE

BUDGET AND ACTUAL

Year Ended May 31, 2007

Revenues:Taxes

Interest incomeTotal revenues

Expenditures:

Current:Paving/streets

Excess (deficiency)

of revenues over

expenditures

Other financing sources (uses):

Operating transfers out

Excess (deficiency) of

revenue and other

financing sourcesover expendituresand other uses

Fund balance at beginning of year

Fund balance at end of year

Budgeted Amounts

Original Final

Variance With

Final Budget

_____ PositiveActual (Unfavorable)

$ 301,000 $ 340,636 $ 350,948 $ 10,31210,000 10,000 12,481 2,481

311,000

499,510

(188,510)

350,636

309,908

363,429

184,390

40,728 179,039

(181,000? (181,069)

12,793

125,518

138,311

(69)

(188,510) (140,272) (2,030) 138,242

194,782 194,782 194,782 ___

6 .272 5 54.510 S 192.752 138.242

See accompanying notes to financial statements

30

TOWN OF WELSH, LOUISIANAPROPRIETARY FUND - UTILITY ENTERPRISE FUND

STATEMENT OF NET ASSETSMay 31, 2007

ASSETS

Cash and cash equivalents $ 110,518

Investments eo *724

Receivables:Accounts 361,079

Estimated uncollectibles and allowances (78,519)Unbilled accounts 76,000Accrued interest 2,284

Inventory 139,888Prepaid expenses 6,761

Other current assets 637

Due from other funds (993,056)

Restricted assets:Cash and cash equivalents 115,725Investments 584,647

Capital assets:Land, improvements and construction in progress 128,205Buildings, furniture and equipment, net of depreciation 6,220,844

Other assets:Bond issue cost, net 9,697

Total assets $ 6.745.434

LIABILITIES

Accounts payable $ 387,288Accrued liabilities 20,447

Noncurrent liabilities:Current portion of long-term debt 231,000Due in more than one year 1,566,000

Payable from restricted assets 42> 335

Total liabilities 5 2.247.070

NET ASSETS

investment in capital assets, net of related debt $ 4,552,049Unrestricted (53,685)

Total net assets S 4.498.364

See accompanying notes to financial statements

31

TOWN OF WELSH, LOUISIANAPROPRIETARY FUND - UTILITY ENTERPRISE FUND

STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN NET ASSETSYear Ended May 31, 2007

Operating revenues;Charges for services $ 3,740,851Tap fees 3,000Miscellaneous 28 > 423

Total operating revenues 3,772,274

Operating expenses:Public utility 3,418,701Depreciation 201,711Amortization 3 , 544

Total operating expenses 3,623,956

Operating (loss) 148,318

Nonoperating revenues (expenses):Interest income 39,011Interest expenses (60,074)

Total nonoperating expenses (21, 063)

Income before operating transfers 127,255

Operating transfers (265f OOP)

Change in net assets (137,745)

Net assets at beginning of year 4,636,109

Net assets at end of year $ 4.498,364

See accompanying notes to financial statements

32

TOWN OF WELSH, LOUISIANAPROPRIETARY FUND - UTILITY ENTERPRISE FUND

STATEMENT OF CASH FLOWSYear Ended May 31, 2007

CASH FLOWS FROM OPERATING ACTIVITIESOperating income $ 148,318Adjustments to reconcile operating income to net

cash provided by operating activities:Depreciation 199,955Amortization 5,300Changes in assets and liabilities:

(Increase) in investments (42,482)Decrease in receivables and accruals 384,585(Increase) in inventories (32,679)(Increase) in prepaid expenses (2)(Decrease) in accounts payable and accruals (61,746)Increase in liabilities payable from restricted assets 700

Net cash provided by operating activities 601,949

CASH FLOWS FROM NONCAPITAL FINANCING ACTIVITIESIncrease in amounts due from other funds 35,256Operating transfers out (265,OOP)

Net cash (used in) noncapital financing activities (229,744)

CASH FLOWS FROM CAPITAL AND RELATED FINANCING ACTIVITIESAcquisition and construction of fixed assets (113,660)Principal paid on bonds (224,000)Interest paid on bonds and capital lease obligations (60,074)

Net cash (used in) capital and relatedfinancing activities (397,734)

CASH FLOWS FROM INVESTING ACTIVITIESInterest income 39, Oil

Net increase in cash and cash equivalents 13,482

Cash and cash equivalents:Beginning of year 212,761

End of year $ 226,243

Cash and cash equivalents at end of year consisted of:Restricted cash $ 110,518Unrestricted cash 115,725

S 226.243

See accompanying notes to financial statements

33

TOWN OF WELSH, LOUISIANA

NOTES TO BASIC FINANCIAL STATEMENTSMay 31, 2007

Note 1. Summary of Significant Accounting Policies

The Town of Welsh, Louisiana was incorporated September 4, 1951, under theprovisions of the Lawrason Act. The Town operates under a Mayor-TownCouncil form of government.

The accounting and reporting policies of the Town of Welsh, Louisianaconform to accounting principles generally accepted in the United States ofAmerica as applicable to governments. Such accounting and reportingprocedures also conform to the requirements of Louisiana Revised Statutes24:517 and to the guidance set forth in the Louisiana Municipal Audit andAccounting Guide, and to the industry audit guide, Audits of State andLocal Governmental Units.

The following is a summary of certain significant accounting policies.

A. Financial Reporting Entity

The accompanying financial statements include the various departments,activities, and organizational units that are within the control andauthor i ty of the Mayor and Town Counc i 1 of the Town of We 1 sh,Louisiana. The decision to include a potential component unit in thereporting entity was made by applying the criteria set forth inStatement No. 14 of the Governmental Accounting Standards Board. Thisstatement defines the reporting entity as the primary government andthose component units for which the primary government is financiallyaccountable. Financial accountability is defined as appointment of avoting majority of the component unit' s board, and either a) theability to impose will by the primary government, or b) the possibilitythat the component unit will provide a financial benefit to or impose afinancial burden on the primary government.

B. Change in Accounting Principles

The Town of Welsh, Louisiana adopted the provisions of GASB Statement34, Basic Financial Statements - and Management's Discussion andAnalysis - for State and Local Governments (Statement 34) and GASBStatement 33, Accounting and Financial Reporting for NonexchangeTransactions (Statement 33) for the year ended May 31, 2005. Statement

34

34 establishes financial reporting standards for all state and localgovernments and related entities. Statement 34 primarily relates topresentation and disclosure requirements. This had an impact on capitalassets, the presentation of net assets and the inclusion ofmanagement's discussion and analysis. Concurrent with theimplementation of Statement 34, the following additional standards havebeen adopted. GASB Statement 37, Basic Financial Statements-andManagement's Discussion and Analysis-for State and Local Governments.-Omnibus. This Statement amends Statement 34 to either (1) clarifycertain provisions or (2) modify other provisions that the GASBbelieves may have unintended consequences in some circumstances. GASBStatement 38, Certain Financial Statement Note Disclosures. ThisStatement modifies, establishes and rescinds certain financialstatement disclosure requirements.

For the year ended May 31, 2006, the Town adopted GASB Statement 40,Deposit and Investment Risk Disclosures.

C. Basis of Presentation

GOVERNMENT-WIDE FINANCIAL STATEMENTS

The government-wide financial statements (i.e., the Statement of NetAssets and the Statement of Activities) report information on all ofthe activities of the primary government.

The Statement of Net Assets and the Statement of Activities reportfinancial information for the Town as a whole so that individual fundsare not displayed. However, the Statement of Activities reports theexpense of a given function offset by program revenues directlyconnected with the functional program. A function is an assembly ofsimilar activities and may include portions of a fund or summarize morethan one fund to capture the expenses and program revenues associatedwith a distinct functional activity. Program revenues include: (1)charges to customers or applicants who purchase, use, or directlybenefit from goods, services, or privileges provided by a given programand {2} operating or capital grants and contributions that arerestricted to meeting the operational or capital requirements of aparticular program. Taxes and other revenue sources not properlyincluded with program revenues are reported as general revenues.

35

FUND FINANCIAL STATEMENTS

The Town segregates transactions related to certain functions oractivities in separate funds in order to aid financial management andto demonstrate legal compliance. Separate statements are presented forgovernmental and proprietary activities. These statements present eachmajor fund as a separate column on the fund financial statements; allnon-major funds are aggregated and presented in a single column.

Governmental funds are those funds through which most governmentalfunctions typically are financed. The measurement focus ofgovernmental funds is on the sources, uses and balance of currentfinancial resources. The various funds are grouped, in the financialstatements in this report, into three broad fund categories as follows:

GOVERNMENTAL FUNDS

General Fund - The General Fund is the general operating fund of theTown. It is used to account for all financial resources except thoserequired to be accounted for in another fund.

Special Revenue Funds - Special Revenue Funds are used to account forthe proceeds of specific revenue sources (other than specialassessments, expendable trusts, or major capital projects) that arelegally restricted to expenditures for specified purposes.

Capital Proj ects Funds - These funds account for all financialresources segregated for the acquisition or construction of majorgeneral government capital projects.

Debt Service Funds - Debt Service Funds are used to account for theaccumulation of resources for, and the payment of, general long-termdebt principal, interest and related costs.

PROPRIETARY FUNDS

Enterprise Funds - Enterprise Funds are used to account for operations(a) that are financed and operated in a manner similar to privatebusiness enterprises - where the intent of the governing body is thatthe costs (expenses, including depreciation) of providing goods orservices to the general public on a continuing basis be financed orrecovered primarily through user charges; or (b) where the governingbody has decided periodic determination of revenues earned, expensesincurred, and/or net income is appropriate for capital maintenance,public policy, management control, accountability, or other purposes.

36

D. Measurement Focus and Basis of Accounting

Measurement focus refers to which transactions are recorded withinvarious financial statements. Basis of accounting refers to whenrevenues and expenditures (or expenses) are recognized in the accountsand reported in the financial statements. Basis of accounting relatesto the timing of the measurement made/ regardless of the measurementfocus applied.

The government-wide statements are prepared using the economicresources measurement focus and the accrual basis of accounting.Revenues are recorded when earned and expenses are recorded when aliability is incurred, regardless of the timing of related cash flows.Therefore, governmental fund financial statements includereconciliations with brief explanations to better identify therelationship between the government-wide statements and the statementsfor government funds. The primary effect of internal activity (betweenor within funds) has been eliminated from the government-wide financialstatements.

In the fund financial statements, governmental funds are accounted forusing a financial resources measurement focus whereby only currentassets and current liabilities generally are included on the balancesheet and increases or decreases in net current assets are presented inthe operating statements. These funds utilize the modified accrualbasis of accounting. Revenues are recognized when they become both:measurable and available to finance expenditures of the current period.Certain revenues such as sales tax, property tax, and charges forservices are assessed and collected in such a manner that they can beaccrued appropriately. Expenditures are recognized in the accountingperiod in which the liability is incurred, if measurable, except forprincipal and interest on general long-term debt which are recognizedwhen due. Also, expenditures for accrued compensated absences are notrecognized until they are payable from current available financialresources.

The proprietary fund, also in the fund financial statements, isaccounted for and reported using a flow of economic resourcesmeasurement focus. This means that all assets and liabilitiesassociated with the operation of these funds are included on thebalance sheet and fund equity consists of contributed capital andretained earnings. The operating statements for the proprietary fundpresent increases or decreases in net total assets.

37

The preparation of financial statements in conformity with accountingprinciples generally accepted in the United States of America requiresmanagement to make estimates and assumptions that affect the reportedamounts of assets and liabilities and disclosure of contingent assetsand liabilities at the date of the financial statements and thereported amounts of revenues and expenses during the reporting period.Actual results could differ from those estimates.

E. Budgets and Budgetary Accounting

The Town follows these procedures in establishing the budgetary datareflected in the financial statements:

1. Prior to May 15, the Town Clerk submits to the Mayor and TownCouncil a proposed operating budget for the fiscal year commencingthe following June 1. The operating budget includes proposedexpenditures and the means of financing them.

2 . Public hearings are conducted at Town Hall to obtain comments fromthe public.

3. Prior to May 31, the budget is legally enacted through passage ofan ordinance.

4. Amendments to the budget are approved by the Town Council by aformal adoption of an ordinance.

5. Formal budgetary integration is employed as a management controldevice during the year for the General and Special Revenue and DebtService Funds. The capital budget ordinances which encompass theCapital Project Funds present cumulative as opposed to annualbudget amounts and thus budget and actual comparisons are notreported in the accompanying financial report for these funds.

6. Any revisions that alter total expenditures of any fund must beapproved by the Councilmen. Expenditures cannot legally exceedappropriations on a fund level.

7. The Town does not utilize encumbrance accounting.

8. Budget appropriations lapse at year end.

38

F. Cash, Cash Equivalents and Investments

Cash and cash equivalents include amounts in demand deposits andcertificates of deposit. The Town considers all highly liquid debtinstruments purchased with a maturity of three months or less to becash equivalents. Certificates of deposit are stated at cost.

Louisiana State Statutes, as stipulated in R.S. 39:1271, authorize theTown to invest in United States bonds, treasury notes, or certificates,or time certificates of deposit of state banks organized under the lawsof Louisiana and national banks having the principal office in theState of Louisiana. In addition, local governments in Louisiana areauthorized to invest in the Louisiana Asset Management Pool, Inc.(LAMP), a nonprofit corporation formed by an initiative of the StateTreasurer and organized under the laws of the State of Louisiana, whichoperates a local government investment pool. Investments are stated atcost.

G. Estimated Uncollectibles and Contractual Allowances

Uncollectible amounts due from customers' utility receivables, hospitaland extended care receivables are recognized as bad debts andcontractual allowances expense through the establishment of anallowance account at the time information becomes available, whichwould indicate the uncollectibility of the particular receivable.

H. Interfund Activity

Interfund activity is reported as either loans, reimbursements ortransfers. Loans are reported as interfund receivables and payables asappropriate and are subject to elimination upon consolidation.Reimbursements are when one fund incurs a cost, charges the appropriatebenefiting fund and reduces its related cost as a reimbursement. Allother interfund transactions are treated as transfers. Transfersbetween governmental or proprietary funds are netted as part of thereconciliation to the government-wide financial statements.

I. Capital Assets and Depreciation

The accounting and reporting treatment applied to capital assetsassociated with a fund are determined by their measurement focus.General capital assets are recorded as expenditures in the governmentalfunds and capitalized. The valuation basis for general capital assetsare historical cost, or where historical cost is not available,estimated historical cost based on replacement cost. The minimumcapitalization threshold is any individual item with a total costgreater than $1,500.

39

Depreciation of capital assets is computed and recorded by thestraight-line method. Estimated useful lives of the various classes ofdepreciable capital assets are as follows:

Plant 10 to 33 yearsMachinery and equipment 5 to 10 yearsFurniture and fixtures 5 to 10 years

J. Accumulated Unpaid Sick Pay

Accumulated unpaid sick pay was not considered material at May 31, 2007and is not reflected in these financial statements.

K. Property Taxes

Property taxes levied in any one year are recognized as revenues ofthat year.

L. Inventories

Inventories held by the Enterprise Funds are priced at the lower ofcost (first-in, first-out) or market.

M. Revenue Recognition - Property Taxes

Property taxes are levied on June 1, billed on November 1, and payableby December 31.

Property tax revenues are recognized when they become available.Available includes those property tax receivables expected to becollected within sixty days after year end.

The total millage of 7.47 for the year ended May 31, 2007 was composedof the following:

Description Millage Tax Revenue

General property tax 7.47 $ 80,189

N. Compensated Absences

The Town accrued a liability for compensated absences which meet thefollowing criteria:

40

1. The Town's obligation relating to employees' rights to receivecompensation for future absences is attributable to employees'services already rendered.

2. The obligation relates to rights that vest or accumulate.

3. Payment of the compensation is probable.

4. The amount can be reasonably estimated.

In accordance with the above criteria the Town has accrued a liabilityfor vacation pay that has been earned but not taken by Town employees.For governmental funds the liability for compensated absences is in thegeneral fund since it is anticipated that the liability will beliquidated with expendable available financial resources. Theliability for compensated absences is recorded in proprietary fundtypes as an accrued liability in accordance with FASB Statement 43.

0. Interest Expense

Interest expense that relates to the cost of acquiring or constructingfixed assets in the Enterprise Funds is capitalized. Interest expenseincurred in connection with construction of capital assets has beenreduced by interest earned on the investment of funds borrowed forconstruction in accordance with Financial Accounting Standards Board(FASB) Statement No. 62 - Capitalization of Interest Cost in SituationsInvolving Certain Tax Exempt Borrowings and Certain Gifts and Grants.

Note 2. Cash, Cash Equivalents and Investments

Custodial credit risk - deposits. Custodial credit risk is the risk thatin the event of a bank failure, the government's deposits may not bereturned to it.

In accordance with a fiscal agency agreement that is approved by the Boardof Aldermen, the Town of Welsh maintains demand and time deposits throughlocal depository banks that are members of the Federal Reserve System.

Deposits in excess of federally insured amounts are required by Louisianastate statute to be protected by collateral of equal market value.Authorized collateral includes general obligations of the U.S. government,obligations issued or guaranteed by an agency established by the U.S.government, general obligation bonds of any state of the U.S., or of anyLouisiana parish, municipality, or school district.

41

The Town's bank demand and time deposits at year end of $3,023,163 (bankbalances) were entirely covered by federal depository insurance or bypledge of securities owned by the financial institution in the Town's name.

Investments held at May 31, 2007, consist of $670,156 in the LouisianaAsset Management Pool, inc. (LAMP), a local government investment pool (seeSummary of S igni f i cant Account ing Polic ie s). In accordance with GASBCodification Section 150.165, the investment in LAMP at May 31, 2007, isnot categorized in the three risk categories provided by GASB CodificationSection 150.164 because the investment is in the pool of funds andtherefore not evidenced by securities that exist in physical or book entryform. LAMP is administered by LAMP Inc., a non-profit corporationorganized under the laws of the State of Louisiana, which was formed by aninitiative of the State Treasurer in 1993. The corporation is governed bya board of directors comprising the State Treasurer, representatives fromvarious organizations of local government, the Government Finance OfficersAssociation of Louisiana, and the Society of Louisiana CPA's. Only localgovernments having contracted to participate in LAMP have an investmentinterest in its pool of assets. The primary objective of LAMP is toprovide a safe environment for the placement of public funds in short-termhigh-quality investments. The LAMP portfolio includes only securities andother obligations in which local governments in Louisiana are authorized toinvest. Accordingly, LAMP investments are restricted to securities issued,guaranteed, or backed by the U.S. Treasury, the U.S. Government, or one ofits agencies, enterprises, or instrumentalities, as well as repurchaseagreements collateralized by those securities. The dollar weighted averageportfolio maturity of LAMP assets is restricted to not more than 90 days,and consists of no securities with a maturity in excess of 397 days. LAMPis designed to be highly liquid to give its participants immediate accessto their account balances.

Interest rate risk. The Town does not have a formal investment policy thatlimits investment maturities as a means of managing its exposure to fairvalue losses arising from increasing interest rates.

Credit risk. State law limits investments to United States bonds, treasurynotes, or certificates, or time certificates of deposit of state banksorganized under the laws of Louisiana and national banks having a principaloffice in the State of Louisiana. Local governments in Louisiana areauthorized to invest in LAMP. The Town has no investment policy that wouldfurther limit its investment choices. As of December 31, 2007, the Town'sinvestment in LAMP was rated AAAm by Standard & Poor's.

Concentration of credit risk. The Town places no limit on the amount theTown may invest in any one issuer. All of the Town's investments are inLAMP.

42

Note 3. Individual Fund Transactions

Individual fund interfund receivables and payables are as follows:

Receivables Payables

General FundSales Tax FundLocal Government AssistanceEnterprise FundFederal Revenue SharingCapital Project - GrantSpecial Revenue - Sales Tax 1996Debt Service - Sales Tax 1996

$ 1,012,823 $ 290,09675,6265,059

86,539174,405

993,056190

71,110

5 1.354.452 S 1,354,452

Note 4. Dedication of Proceeds and Flow of Funds - 2.0% Sales and Use Tax

Proceeds of a 1% sales and use tax levied by the Town of Welsh, Louisiana(2007 collections $350,948; 2006 $331,381) are dedicated to the followingpurposes:

1. Used for any legal purpose as approved by Mayor and Board of Aldermen.Proceeds of a 1% sales and use tax levied by the Town of Welsh,Louisiana approved by voters May, 1996 to expire April 2006 (2007collections $350,948; 2006 $331,381) are dedicated to the followingpurposes:

A. 100% of collections to be used for street maintenance,construction and bonded debt repayment.

Note 5. Restricted Assets

Assets were restricted for the following purposes as of May 31, 2007:

Public utility:Customer depositSewer and water system construction in progressRevenue bond sinking fund, 1988 seriesRevenue bond reserve fund, 1988 seriesRevenue bond sinking fund, 1994 seriesRevenue bond reserve fund, 1994 seriesWater sinking and construction fund, 2003 series

Total - all proprietary fund types

General fund:Emergency cash reserve

$

$

42,33593,495182,255224,69948,32561,07348,190

700,372

S 1.000.OOP

43

Note S. Changes in Capital Assets

Capital asset activity for the year ended May 31, 2007, was as

Beginningof Year Additions Deletions

follows:

End ofYear

Governmental activities:Capital assets not being

depreciated:Land $ 67,599Construction in progress 240,853

Total capital assetsnot being depreciated 308,452

Capital assets beingdepreciated:Buildings 1,101,201Furniture and equipment 431,942vehicles 879,004

Total capital assetsbeing depreciated 2,412,147

Less accumulated depreciation for:Buildings 936,331Furniture and equipment 238,400Vehicles 481,137

Total accumulateddepreciation 1,655,868

Government activities capitalassets, net 5 1.064.731

(240,853)

(240,853)

822,39038,62553,464

914.479

39,29953,82579.409

172,533

741.946

67,599

67,599

1,923,591470,567932,468

3,326,626

975,630292,225560,546

1,828,401

S 1.565.824

Business-type activities:Capital assets not being

depreciated:Land $ 128,205 $

Capital assets being depreciated:Plant and equipment-sewer 6,009,319Plant and equipment-water 2,030,310Plant and equipment-electric 2,310,431 _

Total capital assetsbeing depreciated 10,350,060 _

Less accumulated depreciation for:Plant and equipment-sewer 1,483,627Plant and equipment-water 1,153,572Plant and equipment-electric 1,405,722

Total accumulateddepreciation

Business-type activities capitalassets, net

4,042,921

3,54649,36560,748

113,659

114,54541,55943.851

199,955

128,205

6,012,3652 ,079 ,6752,371,179

10.463.719

1,598,1721,195,1311,449,573

4 , 2 4 2 , 8 7 6

44

Depreciation expense was charged to governmental activities as follows:

General government $ 28,323Public safety 105,922Highway and streets 15,756Sanitation 18,900Culture and recreation 3, 632

Total depreciation S 172.533

Note 7. Bond Issue Cost

Bond issue costs are being amortized on the straight-line method over thelife of the bonds. The following is a summary of net bond issue cost atMay 31, 2007:

Cost $ 79,655Less accumulated amortization 69,958

S 9.697

Note 8. Long-Term Debt

The following is a summary of bonds payable of the Town for the year endedMay 31, 2007:

Balance Balance5-31-06 Additions Reductions 5-31-07

Business-type activities:Revenue bonds S 2.021.000 $ i_ S (224,000) $ 1.797.000

Governmental activities:Revenue bonds $ 502.151 & $ (117.991) S 384.160

Bonds payable are comprised of the following:

Enterprise fund debt:Refunding bonds-Series 2004, maturing serially

and become due November 1 of each year untilfinal retirement November 1, 2014, interestrate ranging from 2.45% to 4.60% $ 553,000

Refunding bonds-Series 1995, maturing seriallyand become due September 1 of each year untilfinal retirement September 1, 2008, interestRate at 4.48% 175,000

45

DEQ loan dated October 25, 1996 in the originalamount of $1,500,000, 1.95% interest plus .5%fee maturing September 1, 2017 payableannually in amortization payments

$225,000 of Certificate of Indebtedness, Series2003, maturing November 1, 2013, net interestrate of 4.04%, interest payable semi-annuallywith principal payments made annually

Total enterprise fund debt

905,000

164,000

5 1.797.000

General obligation debt:$1,500,000 Public Improvement Sales Tax Bonds

Series ST-1996 maturing May 1, 2011, principalpayable annually, interest payable semi-annuallyuntil final retirement, interest rate 8.00%through May 1, 2001 and increases annually from4,9% at May 1, 2003 to 5.5% at maturity

Capital lease obligation as described in Note 9

Total long-term debt

356,000

28,160

384.160

The annual requirements to amortize all bonded debts outstanding as of May31, 2007 follow:

Enterprise Fund Bonds:

Year EndingMay 31,

20082009201020112012

2013-2015

FMHA Water Revenue BondsPrincipal Interest

62,00065,00068,00070,000228,000

18,45916,33013,95111,32815,415

Total

60,000 $ 20,381 $ 80,38181,45981,33081,95181,328243,415

$ 553.000 5 95.864 $ 648.864

Year EndingMay 31,

20082009

Utility Revenue Bonds-Series 1995Principal Interest Total

85,00090,000

175.000

5,9362,016

90,93692,016

7.952 $ 182.952

46

Year EndingMay 31,

20082009201020112012

2013-20162017-2018

DEQ LoanPrincipal Interest

$ 65,70,

75,75,80,

345,195,

000 $000000000000000000

21,

19,17,

16,14,36,4,

376 $723946109210444839

Total

86,89,92,91,94,

381,199,

376723946109210444839

905.000 $ 130.647 & 1.035.647

Year EndingMay 31,

20082009201020112012

2013-2015

Certificate of Indebtedness-Series 2003Principal

$ 21,00022,00022,00024,00024,00051, 000

$ 164,000

Interest

$ 6,3515,8105,0654,0813,0002,485

$ 26.792

Total

$ 27,35127,81027,06528,08127,00053,485

S 190,792

General Long-Term Debt:

Year EndingMay 31,

20082009201020112012

Public Improvement Bonds-ST-1996Principal Interest Total

$ 83,000 $88,00089,00096,000

12,704 $10,2137,1783,840

95,70498,21396,17899,840

$ 356.000 33.935 S 389.935

The Utilities Revenue Bond, Series 1988 was refunded during the fiscal yearended May 31, 1997, which will produce an ultimate savings of $351,316 overthe life of the issue, which will be fully paid on September 1, 2008. Anew bond issue in the amount of $700,000 was combined with funds of theTown to retire the 1988 issue on September 1, 1998. The Series 1988 issuehad an interest rate of above 8% while the refunding bonds have an interestrate of 5.75%.

47

All issuance costs of the transaction ($105,977) were paid with variousrestricted funds remaining from the Series 1988 issue. The net proceedswere used to purchase U.S. Government securities yielding 5 percent. Thesefunds were deposited with the escrow agent to provide for debt service atSeptember 1, 2008. These costs will be amortized over the life of the oldissue (three years) beginning June I/ 1997.

The 1988 Public Utility Fund Revenue Bond Indenture requires, among otherthings, that the Town establish and maintain utility rates so thatoperating income before depreciation is at least equal to 140% of thelargest amount of principal and interest maturing in any future fiscal year($161,280). This bond indenture also requires the establishment andmaintenance of various cash funds. As of May 31, 2007, the Town remains insubstantial compliance with these requirements as well as numerous otherlimitations and restrictions contained in this indenture.

The 1994 FMHA Utility Revenue Bond Indenture requires, among other things,that the Town adopt the utility rates as outlined on the bond indenture.This bond also requires the establishment and maintenance of various cashfunds. As of May 31, 2007, the Town is in substantial compliance withthese requirements, as well as numerous other limitations and restrictionscontained in this indenture.

On March 11, 2002, the Town consummated an interest rate reduction on theoutstanding Utilities Revenue Refunding Bonds, Series 195, of the Town ofWelsh, State of Louisiana, from 2.45 percent to 1.95 percent. The Towncompleted this interest rate reduction to reduce its total debt servicepayments over the next 15 years by $22,384 and to obtain an economic gain(difference between the present values of the debt service payments on theold and new debt) of $19,633.

On August 5, 2004, the Town issued Refunding Bonds, Series 2004 in theamount of $678,000 to retire the Water Revenue Bonds, Series 1994. TheTown completed this refinancing in order to reduce its total debt servicepayments over the next 10 years by $19,623 and to obtain an economic gain(difference between the present values of the debt service payments on theold and new debt) of $28,387. This refinancing reduces the interest rateon the bonds from 5.125% to a range between 2.45% and 4.60%.

48

Note 9. Capital Lease

The present value of capital leases are:

Capital LeasesGeneralLong-TermDebt (1)

2008 $ 28,715Less amount representing interest

(0.525% to 0.650%) 555

Present value of future minimumlease payments $ 28,160

(1) These leases, primarily payable from the General Fund, are reportedas an expenditure and other financing source in the year ofacquisition.

Note 10. Deficit Fund Balance or Retained Earnings

As of May 31, 2007, there were deficits of $ (18,821) in the PavingCertificate Capital Project Fund and $(5,311) in the Grants Capital ProjectFund. There was also a deficit of $(190) in the Federal Revenue SharingFund.

Note 11. Litigation

The Town has had various claims and lawsuits lodged against it. All arewithin the normal course of business and have been evaluated by the Town'sattorney and management. It is the opinion of legal counsel that theseclaims are adequately covered by insurance.

Note 12. Landfill Joint Venture

The Town is a participant in a joint venture referred to as the JeffersonDavis Parish Sanitary Landfill Commission. This entity was chartered onFebruary 17, 1984. The Commission1s purpose is the establishment of along-term plant for the disposal of solid wastes in Jefferson Davis Parish.According to the charter, each participant in the Commission is responsiblefor a pro rata share of any operating deficits. Likewise, anydistributions of surpluses are also shared on a pro rata basis. Eachparticipant's pro rata share is based on the number of households withineach participant's unit to the total number of households within allparticipating units. These proportions were determined using the 1980 U.S.Census as follows:

49

Locality

JenningsWelshLake ArthurParish {excluding Jennings, Welsh,

Lake Arthur and Elton)

Number ofHouseholds

4,1611,1671,212

3,339

9.879

Percentages

.421196

.118129

.122684

.337991

1.000000

The Commission consists of six commissioners as follows: two residents ofJennings, one resident of Welsh, one resident of Lake Arthur, and tworesidents of Jefferson Davis Parish living outside the city limits ofJennings, Welsh, Lake Arthur and Elton. The Commission members are to beappointed by the governing body of their place of residence.

The Commission has the power and authority to employ personnel, adopt itsown budget and enter into agreements necessary for the operation of thelandfill. In certain instances, some agreements must be consented to byall six members of the Commission.

Condensed financial information for the Jefferson Davis Parish SanitaryLandfill as of December 31, 2006 (the latest available audited financialstatements) was as follows:

Total assetsTotal liabilitiesTotal net assetsTotal liabilities and net assetsTotal revenuesTotal expendituresNet increase in net assets

Total

$ 5,690,87620,372

5,670,5045,690,876987,356

1,408,149(420,793)

Welsh(11.8129%)

672,2572,407

669,851672,257116,635166,343(49,708)

As of December 31, 2006, the Commission had no long-term debt outstanding.

50

The Landfill Commission as owner of a sanitary landfill is subject torecent Environmental Protection Agency (EPA) regulations that requiremonitoring the landfill site for 30 years following closure of the site inaddition to other closure requirements. These regulations also mandatethat landfill owners provide financial assurances that they will have theresources available to satisfy the post closure standards. Theseguarantees can be third-party trusts, surety bonds, letters of credit,insurance, or state sponsored plans. According to the Commission'scontract with the site operator, "...the contractor shall be responsiblefor closure in accordance with the permit..". Additionally, "...thecontractor's post-closure care, maintenance and monitoring responsibilityshall be three (3) years, or as required by law...". In the event theoperator is for whatever reason unwilling or unable to fulfill thisrequirement, the responsibility for closure and post closure monitoringwill revert back to the Commission.

Additionally, because of the industry the Commission participates in,certain potential liabilities are always present. These include, but arenot limited to, environmental cleanup costs and EPA penalties for violationof its regulations. The EPA is empowered by law (through the Superfundlegislation) to seek recovery from anyone who ever owned or operated aparticular contaminated site, or anyone who ever generated or transportedhazardous materials to a site (these parties are commonly referred to aspotentially responsible parties, or PRPs). Potentially, the liability canextend to subsequent owners or to the parent company of a PRP.

While there are no asserted or unasserted potential costs or penalties atthe date of this report that the Commission is aware of, the potential ispresent.

Note 13. Pension Plan

Municipal Employee's Retirement System:

Plan description:

The Town of Welsh contributes to the Municipal Employees' RetirementSystem of Louisiana, a cost-sharing multiple-employer planadministered by the Municipal Employee's Retirement System, State ofLouisiana. The Municipal Employees' Retirement System of Louisiana wasestablished by Act 356 of the 1954 regular session of the Legislatureof the State of Louisiana to provide retirement benefits to employeesof all incorporated villages, towns and cities within the State, whichdid not have their own retirement systems and which elected to becomemembers of the System. The System is administered by a Board ofTrustees composed of nine members, six of whom shall be active andcontributing members of the System with at least ten years creditableservice, elected by the members of the System; one of whom shall be

51

the president of the Louisiana Municipal Association who shall serveas an ex-officio member during his tenure; one of whom shall be theChairman of the Senate Retirement Committee; one of whom shall be theChairman of the House Retirement Committee of the Legislature ofLouisiana. Act #569 of the year 1968 established by the Legislatureof the State of Louisiana provides an optional method formunicipalities to cancel Social Security and come under supplementarybenefits in the Municipal Employees' Retirement System, effective onand after June 30, 1970. Effective October 1, 1978, under Act #788,the "regular plan" and the "supplemental plan" were replaced, and arenow known as Plan "A" and Plan "B". Plan "A" combines the original planand the supplemental plan for those municipalities participating inboth plans, while Plan "B" participates in only the original plan. TheTown of Welsh is a member of plan "B" of the retirement system.Historical trend information for this plan is included in theseparately issued report for the Municipal Employee's Retirement Systemfor the period ended June 30, 2006.

Funding policy:

Plan members are required to contribute 5.00% of their annual coveredsalary and the Town of Welsh is required to contribute at astatutorily determined rate. The current rate is 9.75% of annualcovered payroll. The contribution requirements of plan members andthe Town of Welsh are established and may be amended by the Board ofTrustees. The Town of Welsh's contributions to the Municipal Employees'Retirement System of Louisiana for the years ending May 31, 2007, 2006and 2005 were $46,929, $45,201, and $38,596, respectively, equal tothe required contributions for each year.

Municipal Police Employees Retirement System:

Plan description: