township-based microlenders: a profile...mfrc – township based microlenders profile eciafrica...

TRANSCRIPT

Prepared by

Maple Place North Momentum Park

145 Western Service Road Woodmead, 2148 Tel: 011 802 0015 Fax: 011 802 1060

Website: www.eciafrica.com

In collaboration with

Tel: 012 663 3251 Fax: 012 663 7026

Township-Based Microlenders:

A Profile

FINAL REPORT

Submitted to:

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training

Table of Contents EXECUTIVE SUMMARY .................................................................................................................................. I 1. INTRODUCTION ....................................................................................................................................... 1 2. RESEARCH APPROACH AND METHODOLOGY .............................................................................. 3 3. OVERVIEW OF LITERATURE............................................................................................................... 5

3.1 INFORMAL FINANCE – AN INTRODUCTION .............................................................................................. 5 3.2 MONEYLENDERS - EXPERIENCES............................................................................................................ 6 3.3 INFORMATION AND TRANSACTION COSTS .............................................................................................. 7

4. TOWNSHIP-BASED MICROLENDERS PROFILE .............................................................................. 8 4.1 DEFINITION ............................................................................................................................................ 8 4.2 LEGAL STATUS ...................................................................................................................................... 8 4.3 MICROLENDING BUSINESS ..................................................................................................................... 9 4.4 HUMAN RESOURCES AND CAPACITY ................................................................................................... 10 4.5 CLIENT’S PROFILE AND TARGET MARKET ........................................................................................... 10 4.6 LOAN SIZE AND LOAN APPLICATION PROCESSES ................................................................................. 13

4.6.1 Loan sizes ....................................................................................................................................... 13 4.6.2 Application Processes..................................................................................................................... 14

4.7 REPAYMENT, PORTFOLIO QUALITY AND COLLECTION ........................................................................ 16 4.8 LOANS BY PURPOSE ............................................................................................................................. 18 4.9 OTHER MICRO-FINANCE PRODUCTS...................................................................................................... 19 4.10 BUSINESS FINANCING AND GROWTH .................................................................................................... 20 4.11 REGULATION AND THE RELATIONSHIP BETWEEN THE LENDERS AND THE MFRC................................. 20

5. DEVELOPMENTAL NEEDS .................................................................................................................. 23 6. COMMUNICATION AND MFRC .......................................................................................................... 23 7. SALIENT ISSUES AND CONCLUDING REMARKS.......................................................................... 24

7.1 INTRODUCTION .................................................................................................................................... 24 7.2 MAIN ISSUES ........................................................................................................................................ 25

7.2.1 Specific profile of the township moneylenders................................................................................ 25 7.2.2 The strategic objectives of the government..................................................................................... 26 7.2.3 The township lenders and new legislation ...................................................................................... 27 7.2.4 Addressing capacity constraints ..................................................................................................... 27 7.2.5 The role of the MFRC (new regulator) ........................................................................................... 28

7.3 CURRENT AND POTENTIAL ROLE OF THE TOWNSHIP BASED MICROLENDERS ........................................ 30 ANNEX A: SURVEY-BASED QUESTIONNAIRE ........................................................................................ 31 ANNEX B: LIST OF STAKEHOLDERS INTERVIEWED .......................................................................... 47 ANNEX C: STAKEHOLDER DISCUSSION GUIDE.................................................................................... 48 ANNEX D: SUMMARY OF STAKEHOLDER INTERVIEWS.................................................................... 51 LIST OF REFERENCES................................................................................................................................... 54

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training

List of Tables Table 1 Detail on sample survey areas and registration status of respondents .......................................3 Table 2 Selection variables .....................................................................................................................4 Table 3 The TOR and the eventual methodological approach followed.................................................4 Table 4 Geographical spread of the registered PDI lenders....................................................................8 Table 5 Reasons for starting microlending business...............................................................................9 Table 6 Staff members of microlenders ................................................................................................10 Table 7 Education levels .......................................................................................................................10 Table 8 Clients’ employment profile ....................................................................................................11 Table 9 Clients’ residential areas ..........................................................................................................11 Table 10 Clients occupations ................................................................................................................12 Table 11 Current numbers of clients.....................................................................................................12 Table 12 Loan products, - periods and - sizes.......................................................................................13 Table 13 Loan size by product period...................................................................................................14 Table 14 Affordability and eligibility checks used by lenders .............................................................15 Table 15 Number of security measures used by lenders.......................................................................16 Table 16 Repayment on time ................................................................................................................17 Table 17 Cases where borrowers did not repay at all ...........................................................................17 Table 18 Ways of collecting on arrears or default payments................................................................18 Table 19 Knowledge of the purpose of the loan ...................................................................................18 Table 20 Loan allocations .....................................................................................................................18 Table 21 MFRC Statistics of Use of Loans, 2003 ................................................................................19 Table 22 Do your clients approach you to deposit money with you (savings)? ...................................19 Table 23 If they do approach you for taking savings, do you assist them? ..........................................19 Table 24 Lenders who provide additional services, such as transmission ............................................19 Table 25 Sources of funding for microlender businesses .....................................................................20 Table 26 Number of Sources of funding for the business.....................................................................20 Table 27 Knowledge of the regulations for microlending ...................................................................21 Table 28 Awareness of the new National Credit Bill ..........................................................................21 Table 29 Specific aspects that could be addressed by the MFRC (New Regulator)............................29

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training i

Executive Summary Background In the recent past, over 300 PDI lenders have registered with the MFRC (now almost equivalent to 1 in 6 registered lenders) with little known about these lenders, and how many similar lenders operate in township areas. ECIAfrica Consulting (Pty) Ltd and RUDO Research and Training were commissioned by the Micro Finance Regulatory Council to undertake research on PDI township-based microlenders. The objective of the study was to construct a profile of the microlenders based and operating in townships. Their relationship/view of the regulatory environment, the constraints and challenges they face as well as the potential role of these lenders were also investigated. Methodology An information gathering methodology was designed that focused more on qualitative information gathering and analysis rather than quantitative data collection to establish statistical representativeness. The research methodology adopted had two main components: (1) stakeholder interviews to get a sense of the perceptions major stakeholders in the financial sector and (2) a detailed questionnaire designed to incorporate quantitative data and open ended questions to explore some crucial issues of PDI micro-lenders. The process followed was to first design a stakeholder discussion guide, used for all the stakeholder interviews conducted. Following these interviews, and a small pilot, a microlender questionnaire (containing both quantitative and qualitative questions) was finalised, and interviews with lenders conducted. The results of both information gathering exercises were then consolidated into a single report. Key findings Contrary to perceptions that these lenders are generally not registered, 20% of the sample of microlenders drawn was in fact registered (implying that they also had a legal status as this is a prerequisite for registration). Including section 21 companies, 307 of the MFRC registered lenders are classified as PDI lenders by the MFRC – almost 1 in 6 of total lenders registered. On average, these lenders have been operating for almost five years, with one being in operation for fifteen years. Given that the element of trust and “knowing your client” is so critical in the loan process for these lenders, the length of operation is an important factor. Some 60% of lenders also operated other businesses, although not necessarily linked to the microlending business. When looking at the unregistered lenders in our sample, the majority were self employed, and only a few had salaried, permanent jobs. The lenders typically employed only a few staff (with one exception, all less than 10), with just over half the lenders not employing any additional staff. Both registered and unregistered lenders indicated that they had significant skill shortages, and further indicated that they would like to receive information from the MFRC on training and skills development. Turning to the typical client of the microlenders profiled, the key factor is that 76% of clients are employed (and can provide a payslip), while another 11% are employed without

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training ii

The “community” money lender in a rural setting Sarah Mohane is a money lender who operates in Mogwase, in a rural village. She has 26 clients and all of them have been clients for many years. Her clients take loans in most months. A small portion of these clients earn salaries or wages, but the bulk are entrepreneurs, a large number receive remittances and pensions (or other grants). She provides loans for small business, for school fees, for funerals, for transport, for housing, for weddings and also for consumption purposes in reaction to the demand from her clients. She also assists with holding savings and often sends money for her clients to Pretoria with her cousin who is a taxi driver. Her last new client joined three years ago, he was the brother of one of her best clients. She knows her clients, their histories and families and trials and tribulations. This is why she is an institution of the community. Her own income is largely a function of the portfolio she has, and thus it is not high – we estimate it to be around a R1000 per month. She has a good spread of loan terms in her portfolio, however the bulk is 30 day loans (except for the small business and housing loans). She visits her clients at home, and quite often she provides the loans and collects the repayments during these visits. Her clients always repay, albeit quite late in some instances. She is not registered with the MFRC. She does not know about the MFRC. She also does not know about competitors, although she is good friends with the woman that is the lender in the neighbouring village.

receiving a payslip. Further, the majority of clients come from the same township or nearby villages. Average loan sizes varied according to term – with loan sizes increasing as the term increased. Most microlenders indicated that their businesses have grown since they started operating, and that they see scope for further growth. Loan application processes are quite simple for the unregistered lenders, with heavy reliance placed on either personal knowledge of the lender, or a strong referral by an existing client. Registered lenders have a fairly formally defined loan application process, which includes looking at affordability. Portfolio quality was generally good – reflecting the closer than usual relationship between the lenders and their clients. Contrary to the formal, registered microloan industry in South Africa, where the majority of loans made are consumption loans, it is clear that a far higher proportion of loans made by this sub set of microlenders is “developmental” in nature, with a lot of lenders making loans for education, business and housing purposes. The research also showed that there is some demand for other services to be provided – particularly savings and transmission services. 10% of lenders said that clients asked to deposit money with them (showing a high degree of trust), while 20% indicated that clients asked for money to be transferred to others on their behalf. Looking at how the lenders funded their businesses, most funding comes from salary or savings, business profits reinvested, and family members. Some also reported receiving funding from friends, and just under 10% indicated the use of retrenchment packages to fund their businesses. None of the microlenders interviewed had any external funding. While the majority of unregistered lenders did not know of the MFRC, they did indicate interest in receiving information on the MFRC. Those that had registered indicated that they did so because they wanted to professionalize their businesses, and they also believed it would help minimise client defaults, because by operating legally, they could take legal steps to recover outstanding amounts. The microlenders also have developmental needs, and all the interviewed microlenders agreed that access to funding and training were two critical areas that, if addressed, could help them expand their businesses. Other than training relating to running their businesses, specific training on relevant acts and regulations was also indicated as important, as was increasing the financial literacy of clients so that they could make better informed financial decisions.

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training iii

The “community” money lender in an urban setting Pascalina Mongane comes from Mogwase. She moved to Mamelodi 20 years ago, and makes her living as a money lender. She has 37 clients. She knows all her clients very well, and the good clients sometimes bring their friends or family members for loans. She knows these other people will repay as she trust her clients who referred them. A larg part of her portfolio is made up of salaried and wage earning clients. Loan sizes provided range from R400 to R800 a loan, but most are the smaller loans. Clients take loans for a variety of things, and one finds loans for small businesses, for funerals, for school fees, for consumption items and more. Her income is slightly higher than her rural counterpart, but she has a problem of people not repaying, however, this is an infrequent event. She runs her business on her own however; sometimes good friends and family members help out. She supplements her lending income with the money that she makes in a small spaza shop she runs from home. Her daughter helps her out in the spaza. She is not really worried about competition, although she sees other lenders in the neighbouring community and they know of each other. One time, she actually borrowed from another lender when she ran low on funds. This is sometimes a problem. She once made a mistake and forgot to remind some of the referred clients, and they did not repay for months.

The hybrid or changing money lender Joe Hlongwane started his money lender business with a group of 10 clients some years ago. He operates his business in Guguletu and also does a bit of business in Salt River. His portfolio (74 clients) exists mostly of salaried and wage earning clients. Now and then he provides a loan to trusted clients for investment in their businesses, or for adding to their houses, but this is only to a select group. Most of his other loans are for 30 days and are used for funerals, school fees, and consumption items. He has expanded his system and makes use of agents that will serve clients in nearby areas. He sees that where he has good agents, he is building his portfolio. However, in one specific factory where he provided a service, he had to stop since another lender took over the service, largely because the person that worked for him was slower than the sales people of the other lender. The bulk of his clients have been on his books for many years, but he does have a portion that fluctuates from month to month. He heard about the MFRC, but his information is sketchy and he is not sure what they do, thus he is afraid that they may hear of him, as the rumour is that they are looking for lenders charging high interest rates.

As noted earlier, 85% of the lenders indicated that they would like to receive information from the MFRC, and indicated a wide choice of communication channels. However, the most popular choice was to receive pamphlets or brochures. In general, the township moneylenders (largely the unregistered lenders) reflects the reality of less asymmetric information problems, and operate their businesses on the basis of a good knowledge of their clients, reflected by the fact that more than 10% of the clients do not receive a salary slip, that about 10% of clients trust them enough to save with

the lenders, and that 20% trusted the lenders to make money transfers for them. This is consistent with other local and international research findings. It is important to consider the strategic objectives of the government while we are looking at the different township microlenders, as well as the concept of market development. On the one hand, the government wants to improve access to financial services (as espoused in their support for the financial sector charter). At the same time, the government wants to ensure that clients are protected from exploitation (as espoused in the objectives of the National Credit Bill). The government also want to protect depositors and motivate savings (Banks Act, Dedicated Banks Bill, Cooperative Banks Bill). If we turn away from the clients to the service providers, the government has a strong transformation agenda, where it wants to ensure that SMMEs face less administrative and bureaucratic hurdles (including less corruption and fraud in the registration and formalisation processes). Through its procurement rules and objectives it also wants to assist SMMEs. The government wants to improve access to funding and access to training, and largely sees the formalisation of SMMEs as the first step in this direction. This is important for the lenders studied, as almost all of them expressed a demand for training and improved access in terms of capitalisation. It may be that we found conflicting objectives, and thus we turn to our specific topic, township lenders and legislation.

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training iv

The registered township moneylender Nthabi (Big Mama) Cele operates her lending business in Tembisa. She has been running this business for four years. She has 300 clients. Almost all her clients are earning a salary or wage, and the majority can show salary slips when they apply for a loan. Most of the loans are used for food, transport, school fees, funerals and some for small business activities. However, the majority of loans are small and for one month. She has a few clients with bigger loans for longer periods, once again clients with excellent track records and good jobs. She is registered with the MFRC and pays R1200 per year for registration. Although she finds it expensive, she feels it is worthwhile as registration gives her clients a sense of security, and many clients are aware of the fact that they have recourse with the MFRC if they have a problem. Her systems are more advanced than the ledger/book system used by the other lenders in the townships. She feels that she competes against the banks and these other lenders. However, she provides a good service and is still building her clientele. Her main constraint is funds to on-lend, and she has to take money from friends from time to time when she wants to expand her business.

It is not clear how regulation will improve the specific situation of the township moneylender as the current and intended regulation in South Africa is largely focused on the protection of the client. As pointed out, the consumer protection angle is less of an issue in the townships due to the relationship between borrower and lender. One may argue that if these entities stay small, continue this relationship and consistent service to a consistent clientele, normal registration may not be necessary for these informal entities. Rather, another form of very basic registration could be considered. On the other hand, we need to state clearly that we have different typologies of township lenders, and that they should be treated differently in terms of the objectives of government. Although it is important to register lenders in some way, the different typologies necessitate a different approach in terms of registration and what each level of registration entails in terms of reporting requirements and registration fees. For example, it is quite clear that the community microlender in rural settings cannot afford to pay the R1200 registration fee. In the same vein, this lender also has such a good relationship with his/her clients that the state’s objective of client protection is not so important in this situation. It follows that we argue for differentiation in registration requirements, reporting requirements and registration fees.

When asked about development needs, the main items mentioned by lenders were access to funding, training for themselves and consumer education. There are also many challenges that will be faced by any intervention to address these issues. Options that can be considered vary widely. In the case of access to funding, the most obvious is to think about linking lenders with larger institutions. We mentioned the example of Bank Rakyat Indonesia, but closer to home we do see a relationship between commercial banks and village banks, and one can think of linkages between lenders and

commercial banks, other bigger lenders, NGOs and more. However, given the importance of the personal relationship between lender and client in this market, there are questions as to how big a business can get without bringing forward other challenges – such as the need for more skilled staff. The MFRC (or the new credit regulator) has a central role, but it should be in close co-operation between the relevant stakeholders. Thus the MFRC can play the role of facilitator to ensure improved services, improved access to finance, sensible approaches in terms of registration and monitoring the progress in the market. The MFRC has a good understanding of the market and has access to government and other stakeholders to ensure that, firstly, the township money lender is on the agenda, and secondly, that appropriate interventions are planned and implemented.

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training v

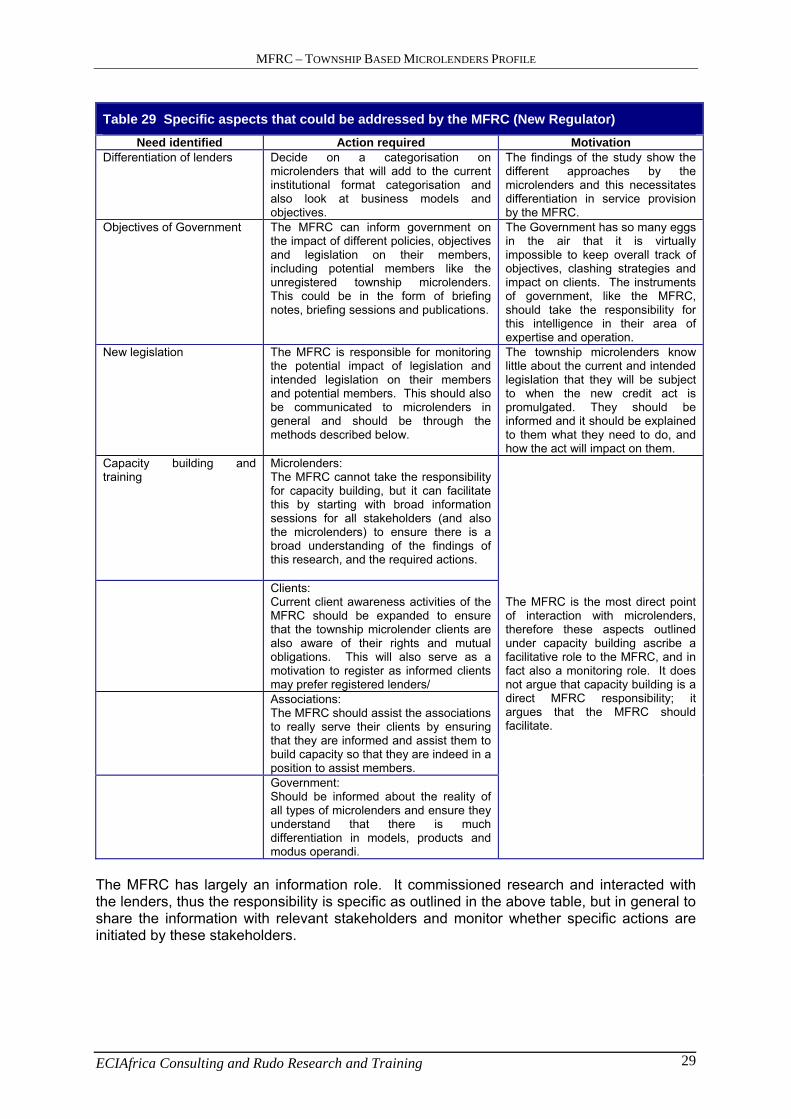

Specific aspects that could be addressed by the MFRC (New Regulator) Need identified Action required Motivation

Differentiation of lenders Decide on a categorisation on money lenders that will add to the current institutional format categorisation and also look at business models and objectives

The findings of the study show the different approaches by the microlenders and this necessitates differentiation in service provision by the MFRC

Objectives of Government The MFRC can inform government on the impact of different policies, objectives and legislation on their members, including potential members like the unregistered township microlenders. This could be in the form of briefing notes, briefing sessions and publications.

The Government has so many eggs in the air that it is virtually impossible to keep overall track of objectives, clashing strategies and impact on clients. The instruments of government, like the MFRC, should take the responsibility for this intelligence in their area of expertise and operation

New legislation The MFRC is responsible for monitoring the potential impact of legislation and intended legislation on their members and potential members. This should also be communicated to microlenders in general and should be through the methods described below

The township moneylenders know little about the current and intended legislation. As they will be subject to the new legislation when the act is promulgated, they should be informed and it should be explained what they need to do, and how the act will impact on them.

Capacity building and training

Microlenders: The MFRC cannot take the responsibility for capacity building, but it can facilitate this by starting with broad information sessions for all stakeholders (and also the microlenders) to ensure there is a broad understanding of the findings of this research, and the required actions.

Clients: Current client awareness activities of the MFRC should be expanded to ensure that the township microlender clients are also aware of their rights and mutual obligations. This will also serve as a motivation to register as informed clients may prefer registered lenders/

Associations: The MFRC should assist the associations to really serve their clients by ensuring that they are informed and assist them to build capacity so that they are indeed in a position to assist members.

Government: Should be informed about the reality of all types of microlenders and ensure they understand that there is much differentiation in models, products and modus operandi.

The MFRC is the most direct point of interaction with microlenders, therefore these aspects outlined under capacity building ascribe a facilitative role to the MFRC, and in fact also a monitoring role. It does not argue that capacity building is a direct MFRC responsibility; it argues that the MFRC should facilitate.

This study addressed a first stab profiling of township microlenders, and also assessed the perceptions and views of lenders and stakeholders on a range of topics. This is a first round study and therefore more detailed case studies of larger township lenders could inform the stakeholders, also an assessment of the regulatory impact of the envisaged Credit Act on the different client categories and potential clients could be worthwhile. In addition, very little is known of the scope and overall size of these lenders, and this could be an area that can also be considered for future research.

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 1

1. Introduction The study was commissioned by the MFRC in light of the fact that over 300 township based lenders (also referred to as previously disadvantaged individuals – PDIs) have registered with the MFRC (almost 1 in 6 of total registrations) with little known about these lenders, and how many similar lenders operate in township areas. Informal finance exists next to and sometimes “within” formal financial markets and service providers. The challenge is to understand the extent of informal financial services, and also in the specific situation of lenders, understand the relationship between lenders and their clients. As such, the objective of the study was to profile the PDI lenders, and gain an insight into the market and how they operate, as well as how they view the regulatory environment. Our research, after discussion with the MFRC, focussed specifically on PDI lenders based and operating in townships1 and more rural settlements. The request for proposals indicated that the research should aim to:

To explore the extent of formal township lenders’ (PDI) involvement in micro lending as well as the size of the market

To construct typical profiles of township lenders including To conduct interviews with the industry participants to determine factors which impact

upon the lenders willingness to be part of the formal and regulated sector To map out the potential role that could be played by the sector in bridging the gap

between South Africa's sophisticated financial sector and the emerging market population

To determine whether township lenders have any specific development needs and whether any other entity can play a role in addressing such needs

To advise the MFRC on the effective communication methods to be embarked upon to engage with this sector.

One change in the approach was the requirement from the MFRC to work more on a case study basis than a representative sample basis during the data gathering for this study. This implied that the questions on the scope of township based lenders would not be answered. To answer questions on overall numbers of township based lenders would require a larger statistically driven study. The report is structured to incorporate the findings of the stakeholder interviews as well as the quantitative and qualitative information drawn from the questionnaires completed during interviews with lenders. By combining the different sources of information, we have endeavoured to construct a holistic profile of these lenders, highlighting when stakeholders’ opinions differed from what lenders reported as well as when they coincided. Section 2 of the report provides an overview of international experience with respect to money lenders. Section 3 provides an overview of the research approach and methodology followed. Section 4 describes the profile of the lenders, both registered and unregistered, following the structure of the lender questionnaire (attached as Annex A) but supplemented and enriched by the information from the stakeholder interviews.

1 The use of the word township refers to urban and peri-urban settlements where mostly black people historically settled, influenced by the spatial requirements of apartheid laws and regulations and concomitant settlement patterns.

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 2

Section 5 describes the developmental needs of the lenders as expressed by themselves as well as the opinion of the stakeholders. Section 6 addresses the issue of communications with the MFRC, looking at what channels have reached the lenders in the past, and what the preferred channels are. Finally, in section 7, we look at the potential role of the sector, particularly considering issues around BEE and the financial services charter.

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 3

2. Research approach and methodology An information gathering methodology was designed to capture all the issues specified in the terms of reference that focused more on qualitative information gathering and analysis rather than quantitative data collection to establish statistical representativeness. The research methodology adopted had two main components: Stakeholder interviews to get a sense of the perceptions major stakeholders in the financial sector had about the micro-lending sub-sector in townships and rural settlements. The stakeholder interviews were conducted as part of phase I of the research project. The sample of interviews included 19 stakeholders (listed in annex B), and they were guided by structured questions that entailed:

The definition and profile of township lenders as perceived by the different stakeholders;

The perceived challenges faced by the township microlenders; Their development needs; The barriers to regulation; Market development processes; and finally The role of the MFRC can play in the sub-sector.

The detailed guide for the stakeholder interview is attached as Annex C A detailed questionnaire was designed incorporating quantitative data and open ended questions to explore some crucial issues in more details from the perspective of PDI microlenders. The target sample included unregistered and registered (with the MFRC) microlenders. The questionnaire explored in details the different aspects of PDI microlenders with particular emphasis in examining processes, rather than raw data. Crucial to the design of the questionnaire was the issue of targeting: the research aims at understanding a particular sub-group of the PDI microlenders, i.e. the ones that operates in township and/or in rural settlements. We understand that there are other PDI microlenders which operate in other economic areas like CBDs, factory floors, suburbs etc. The sample covered 4 townships and 1 rural settlement, and approximately 10 microlenders in each area were interviewed for a total of 50 (including the pilot). It must be noted that this study is not intended to be representative of the sub sets of lenders identified, and is at best indicative and exploratory in nature. The following tables depict the township and sample frames:

Table 1 Detail on sample survey areas and registration status of respondents

Township/Province No. of ML interviewed

Not Registered

Registered with MFRC

Guguletu/ Khayelitsha Western Cape 8 8 0 Umlazi KZN 7 7 0 Soweto/Tembisa Gauteng 10 8 2 Mamelodi Gauteng 10 9 1 Mogwase North West (rural) 7 2 5 Sample size 42 34 8 Pilot sample size 6 Invalid questionnaires 2

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 4

Respondents were recruited based on the basis that they lend money to borrowers and reside in the townships. Given the fact that most unregistered lenders did not want to be identified, recruitment for respondents was conducted with the help of the BMFA as well as community representatives. Based on the residential specifications, the sample is 100% African and the other variables used for recruitment of lenders are illustrated in the table below: Table 2 Selection variables

Unregistered Lenders Registered Lenders • Have to be in the business of lending

money to borrowers • Have to be in the business of lending

money to borrowers • Have to reside in the township or village • Have to reside in the township/village • Male and female • Male and female • South African Citizen • South African Citizen • Not registered with the MFRC • Have to be registered with the MFRC In summary, the methodological approach used relates to the ToR issues as below:

Table 3 The TOR and the eventual methodological approach followed

TOR issues Stakeholder interviews Questionnaire Remarks

To explore the extent of formal township lenders’ (PDI) involvement in micro lending as well as the size of the market.

The research was refocused on gaining a useful insight

into the market rather than

estimating the size of the

market. To construct typical profiles of township lenders ٭ ٭To conduct interviews with the industry participants to determine factors which impact upon the lenders willingness to be part of the formal and regulated sector

٭

To map out the potential role that could be played by the sector in bridging the gap between South Africa's sophisticated financial sector and the emerging market population.

٭

To determine whether township lenders have any specific development needs and whether any other entity can play a role in addressing such needs.

٭ ٭

To advise the MFRC on the effective communication methods to be embarked upon to engage with this sector.

٭

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 5

3. Overview of literature 3.1 Informal finance – an introduction Informal financial activities are common throughout the world. Although the perception exists that informal activities only take place due to the unavailability of formal financial services, informal financial arrangements even exist in formal financial intermediaries - between staff members (Von Pischke, 1991)2. The existence of these activities signals a need by those that take part in them, for types of services not supplied by formal intermediaries. Unavailability of formal intermediaries should be stated in terms of access. There are two motivations for informal finance: Firstly, an autonomous system and secondly, a system operating in moderation in reaction to the formal financial sector. In some instances the formal intermediaries do not serve certain remote areas. In other instances they do serve these areas but access to the formal intermediaries is impossible due to high transaction costs or to an incomplete range of services provided. Furthermore, many poor people perceive formal institutions as inaccessible, mainly due to a lack of information on how these intermediaries operate (DeLancey, 1992). Until the late 70s, research done specifically on informal financial activities was notably absent from rural financial market studies (Adams & Fitchett, 1992). Perceptions on the informal sector were dominated by the concept of usurious moneylenders that exploit poor rural people. Not only is the moneylender but one of the intermediaries in the informal financial sector, but exploitative actions of moneylenders are not the norm. The most puzzling characteristic of the informal sector was however the ability of these arrangements to withstand the circumstances that ruined numerous formal intermediaries (Meyer & Nagarajan, 1991). Another characteristic is the ability to withstand the impact of flows of subsidised credit into financial markets. Although one of the goals of cheap credit programmes was to increase the supply of funds, and thus to decrease the high interest rates charged by moneylenders, the opposite often happened. In areas where cheap credit programmes were implemented, interest rates of moneylenders often rose and the incidence of transactions by the moneylenders increased. This may seem contrary to the laws of supply and demand. However, due to the high transaction costs of formal programmes, the targeting of loans and other maladies of these programmes, the supply of funds to the poor did not really change. In fact, the supply of funds to the rich increased and these cheap credit programmes did not compete with the moneylender, they competed with other formal intermediaries active in the field. The result is that in many ways these programmes decreased both the linking and efficiency of the financial markets and the activities of the formal sector in these areas. The informal financial sector is not without constraints. In most countries fragmented, un-integrated markets have not been positively influenced by informal activities. No significant integration has been achieved, for example. Informal activities are rather characterised by their existence in fairly small isolated geographic areas. Mostly small amounts change hands, whether saved or borrowed. Saving in many instances could be described as money keeping rather than saving, as interest is quite often not part of the transaction. Intermediation, in its definition as the act of serving as a conduit for transactions with concomitant credit creation, is not always applicable in the case of informal intermediaries in rural areas.

2 Such activities between staff members also exist in the Development Bank of Southern Africa. Von Pischke reported on the informal financial activities of staff members of the IMF.

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 6

The rest of this section on informal finance will deal with one of actors in informal markets, the moneylender. We show that there are many similarities between international experience, and the township microlenders in South Africa. 3.2 Moneylenders - experiences The villain in most motivations for cheap credit programmes was often the moneylender. Accounts of high interest rates led to arguments of exploitation. Moneylenders usually lend out of their own sources to a mostly consistent group of borrowers (Timberg & Aiyar, 1984). In some instances moneylenders, once they have reached the ceiling in terms of numbers of borrowers they can accommodate, take on no new borrowers. Timberg and Aiyar (1984) reported the case of a moneylender that never took new borrowers. Moneylenders provide small loans quickly and for short periods. They have comprehensive, almost perfect, information on the creditworthiness of their clients, based on long term relationships they have with them. Those that argue exploitation by moneylenders fail to prove that it is generally the case, and also do not consider the costs to the moneylender in providing a service. Informal lenders do not regularly receive returns that are far beyond their costs, as shown by empirical findings in developed countries (Adams, 1984). Opportunity costs of funds out of non-lending activities are usually high for these informal lenders. Often these lenders are fellow businessmen with surplus funds (savings). They are also exposed to the risks of informal markets (and the vagaries of nature in rural areas) in their enterprises, therefore the high opportunity costs. If all the costs of borrowing are included (i.e. interest rates plus transaction costs) Adams and Nehman (1979) found that cheap formal loans are sometimes even more costly to borrowers than informal high interest loans. Informal lenders have far more information on their clients than formal lenders and this contributes to lowering transaction costs. Also, a continuum of moneylenders exists, ranging from those doing it permanently to those that enter the market from time to time. Most rural people finance themselves out of savings. The majority that borrow money borrow it from friends and family. Moneylenders, therefore, do not play a major role in the provision of credit to the majority of people. They do, however, play an important role in times of covariant risk, but are only involved with those clients whose creditworthiness they can assess. They tend to service specific groups of borrowers (Nagarajan and Meyer, 1991). Contrary to the above scenario, Bolnick (1992) argues that in the case of Malawi the moneylenders do charge exorbitant rates on loans. He contends that the Malawian moneylender does not conform to the neat picture of moneylenders in other countries. This is because of a lack of competition in the market. However, he bases his arguments on interviews with two moneylenders in the urban areas of Malawi and no indications are given on what basis he infers their profiles to that of all moneylenders in that country. The moneylenders he describes do not have close contact with or detailed information on their clients. If we turn to South Africa the most recent research is by Kgowedi et al (2002) and Roth (1999). The only existing estimate of the number of township moneylenders is approximately 30,000 (Du Plessis, 1997). Research by Roth on township moneylenders in the Grahamstown area can be taken as a proxy for the average lender (until this report). This was confirmed by a survey in Limpopo Province (Kgowedi et al, 2002), which found similar statistics. The typical lender has about 15-20 clients with a total outstanding book of about R5,000. Therefore, using this as a proxy, the township lenders account for about 600,000

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 7

clients on a monthly basis with an outstanding book of about R150 million at a given moment. On an annual disbursement basis, this comes to R1.8 billion. 3.3 Information and transaction costs The most telling difference between formal and informal financial activities lies in the area of transaction costs. The most important influence on transaction costs is the level of information that you have on prospective clients. All markets are characterised by external and internal risks. External risks in the informal sector of rural financial markets impact equally on most of the actors in the market. Internal risks are where the real difference lies. Informal financial institutions are able to survive due to the high level of information that the informal institutions have on borrowers (and depositors). How do they obtain this information? Lenders and providers of other financial services in the informal milieu obtain this information because of close proximity to clients and knowledge of their activities and the fact that most of them have a long-term relationship with their clients. Clients therefore have the chance to build a creditworthiness record. They further use specific mechanisms as substitutes for collateral, i.e. peer monitoring and interlinked loan contracts. Therefore, moral hazard and adverse selection problems, which can occur under asymmetric information, are not as prominent in informal as in formal financial markets. Siamwalla et al (1993) state that the application of asymmetric information models in the case of informal markets is misleading. They argue that perfect information models are more applicable in informal markets. The rigid collateral requirements of formal financiers are not applicable in informal markets. Informal financiers adjust to the situations of their clients. They use innovative approaches to substitute for collateral. The group approach is one in which peer monitoring is exercised. In transactions among family and friends, familial and friendship ties are used as collateral. Interlinked contracts are also used. An example of the latter is the custom of pledging the productive value of land as collateral. Thus on default the lender can use the land for a pre-specified period. In this way the land market and the financial market are linked. Another example is where a farmer has to sell his harvest through a lender (obtained credit from a processing firm) (Ladman et al, 1992). In this way the financial market and the market for agricultural produce processing are linked.

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 8

4. Township-Based Microlenders Profile 4.1 Definition In order to profile a typical microlender, whether registered with the MFRC or not, we start by attempting to define who we are talking about. As mentioned before, in this research we collected information and data on PDI microlenders that work in townships and rural settlements. We do acknowledge that this is only a sub-group of the whole population of microlenders, which operate in other economic locations, be these the factory floor, central business districts or other parts of towns/cities. According to some stakeholders, interviewed as part of this research, microlenders can be divided into two groups: (i) township and rural lenders, whose business is based on trust and whose clientele are mostly people from the neighborhood, friends and family. They normally operate from their homes, at work or from their cars; (ii) the semi-formal and formal lenders who normally operate from ‘downtown’. They have little offices that are hidden from the public, and they do basic book and record keeping. They will have a computer and printer half the time, and they take bank cards, pin codes and IDs. They tend to be harsh in cases of defaults (excerpts from interviews with BMFA and DTI). Although there is a perception amongst stakeholders that microlenders in township and rural areas do not register with the MFRC, in the sample for this research, about 20% of the total microlenders interviewed were registered. Data from the MFRC also suggest that about 295 PDI microlenders are registered and this number increases to 307 if section 21 companies are included. The geographical spread of the registered microlenders is as follows:

Table 4 Geographical spread of the registered PDI lenders

Place of operation No. of registered PDIs Percentage Gauteng Province 89 30% North West Province 9 3% Limpopo 60 20% Mpumalanga Province 25 8% Kwa-Zulu Natal 65 22% Eastern Cape Province 11 4% Free State 21 7% Northern Cape 6 2% Western Cape 9 3% Total 295 100%

Source: MFRC 2005. 4.2 Legal Status Industry stakeholders perceived township PDI microlenders as having no legal status, although there is nothing mentioned about the differences between registered and unregistered PDI microlenders. Interviews with a sample of township based microlenders have shown a different picture. Just more than a quarter of the microlenders interviewed had legal status of which two thirds were registered either as Close Corporations (CC’s) or Private Limited Companies (Pty. Ltd)3.

3 Statistical tests showed that there is a linear relationship between having a legal status and being registered with the MFRC. It is noted that having legal status is a prerequisite to register with the MFRC.

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 9

4.3 Microlending Business This section examines some of the characteristics of their modes of operation, the premises from which micro-lending business activities take place, the years of operation, the reason for starting the micro-lending operations and whether the microlenders engage in other businesses. Based on the perceptions expressed by stakeholders (like the BMFA, DTI, Teba Bank and FABCOS) it could be said that microlenders (the unregistered ones) operate within a simple structure, as individuals, and in an environment with a limited level of control to avoid taxation and other ‘administrative processes’ (Consumer Protector). Some work within their local stokvel associations. Because of their very simple structure, there is consensus amongst stakeholders that microlenders in townships and rural settlements do not operate from offices or branches but from their homes, their cars and other more informal premises. These are just few examples of responses from the stakeholders’ interviews: “Most operate from the boot of their cars, under the trees, in their households” (BMFA) and “these schemes (microlenders) are rife in informal settlements, more especially for people receiving pensions. There is a lot of money that circulates within these settlements. You find one person selling meat, the other selling beer and the other lending money for people to buy these commodities. Money rarely leaves these settlements” (DTI) and “they do not have offices. People in the neighborhood tend to know that they have money. Some operate from known premises at specific times” (Capitec) and “they operate in their own neighborhood where they trust and know the surroundings and addresses of their customers” (Teba Bank). These statements are supported by evidence from the interviews with microlenders. Most of them operate from home and from their cars; very few (3 out of 42) had office premises and branches. Regarding the geographic coverage of the operation, most of them (93% of the microlenders interviewed) operate from the township where they are based4. Based on the interviews with microlenders, on average they have been operating for 5 years (4.76 years), with a minimum of 1 year (8 microlenders) and a maximum of 15 years. The longer their years of operation the more knowledge they acquire about their clients and potential clients. The lenders were asked to describe their reasons for starting a microlending business. Both registered and unregistered microlenders stated that they were unemployed and started microlending businesses to earn a living. Others stated that they were employed and started microlending as an additional source of income to complement their salaries. Profit making and helping people who do not have access to credit with formal financial institutions were quoted as the overriding objectives of starting microlending businesses. Table 5 Reasons for starting microlending business Number of Respondents Reasons Given

15 Profit 12 Profit; help people 9 Source of income / earn a living / got retrenched / Compliment income 5 Motivated by a micro lender friend, family member 3 Help people - those who do not qualify with formal financial institutions

4 In the sample used in this project there is no difference in terms of geographical coverage between registered and unregistered micro-lenders.

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 10

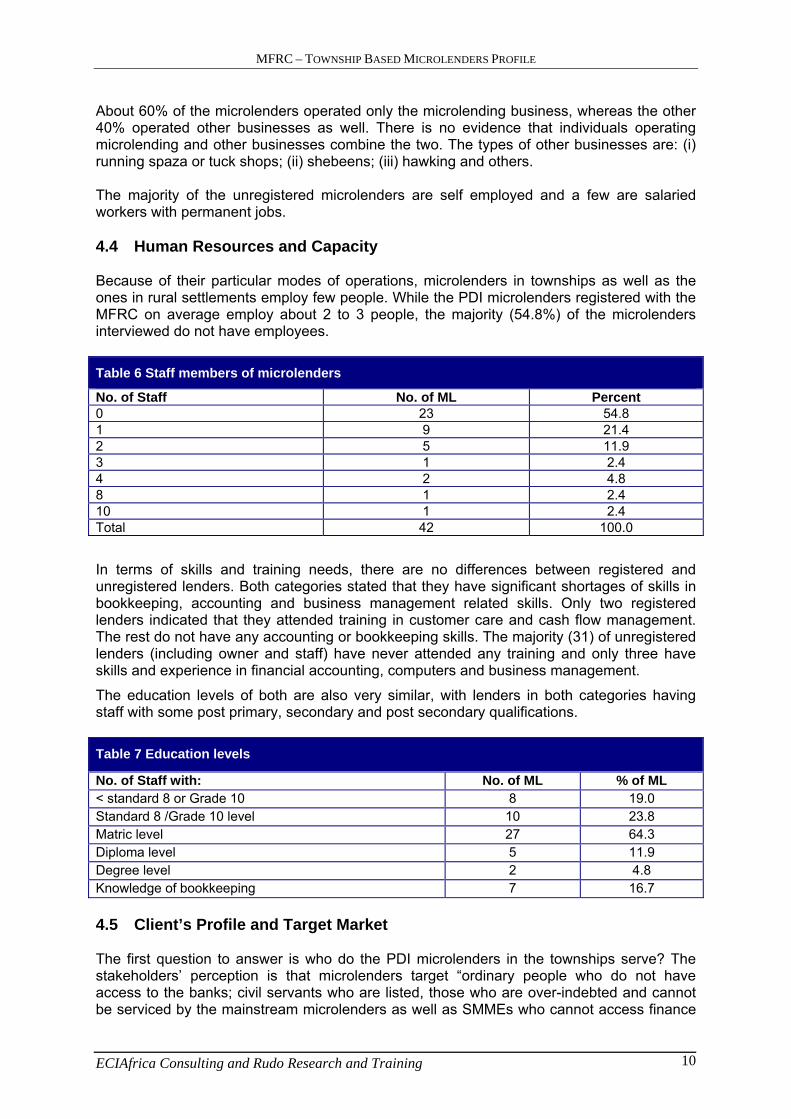

About 60% of the microlenders operated only the microlending business, whereas the other 40% operated other businesses as well. There is no evidence that individuals operating microlending and other businesses combine the two. The types of other businesses are: (i) running spaza or tuck shops; (ii) shebeens; (iii) hawking and others. The majority of the unregistered microlenders are self employed and a few are salaried workers with permanent jobs. 4.4 Human Resources and Capacity Because of their particular modes of operations, microlenders in townships as well as the ones in rural settlements employ few people. While the PDI microlenders registered with the MFRC on average employ about 2 to 3 people, the majority (54.8%) of the microlenders interviewed do not have employees.

Table 6 Staff members of microlenders

No. of Staff No. of ML Percent 0 23 54.8 1 9 21.4 2 5 11.9 3 1 2.4 4 2 4.8 8 1 2.4 10 1 2.4 Total 42 100.0

In terms of skills and training needs, there are no differences between registered and unregistered lenders. Both categories stated that they have significant shortages of skills in bookkeeping, accounting and business management related skills. Only two registered lenders indicated that they attended training in customer care and cash flow management. The rest do not have any accounting or bookkeeping skills. The majority (31) of unregistered lenders (including owner and staff) have never attended any training and only three have skills and experience in financial accounting, computers and business management.

The education levels of both are also very similar, with lenders in both categories having staff with some post primary, secondary and post secondary qualifications.

Table 7 Education levels

No. of Staff with: No. of ML % of ML < standard 8 or Grade 10 8 19.0 Standard 8 /Grade 10 level 10 23.8 Matric level 27 64.3 Diploma level 5 11.9 Degree level 2 4.8 Knowledge of bookkeeping 7 16.7 4.5 Client’s Profile and Target Market The first question to answer is who do the PDI microlenders in the townships serve? The stakeholders’ perception is that microlenders target “ordinary people who do not have access to the banks; civil servants who are listed, those who are over-indebted and cannot be serviced by the mainstream microlenders as well as SMMEs who cannot access finance

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 11

from Khula and the rest” (BMFA). Others felt that “the clientele is wide-ranging – from bankable to un-bankable people” (DTI), perhaps because of the simplicity of their operations and their mechanisms to disburse loans (explained in the next section), their products appeal to a wide range of clients based in the townships. Clients are by and large recruited by word of mouth, and most frequently come from the immediate environment. In particular, existing clients refer new clients to lenders. This referral also forms an important part of screening process used by the lenders. “There are always new people being introduced everyday even though I don’t go out and market myself” - a lender in Tembisa. The use of runners, who have their own networks of clients, was also mentioned by one stakeholder as communication and marketing method employed by lenders. We examine the client’s profile from the interviewed microlenders in more detail below. Firstly, it is interesting to note that, according to the lenders, almost 76% of their clients are formally employed with a payslip as proof of income. Furthermore, another 11% are employed, but without a payslip as proof of income.

Table 8 Clients’ employment profile

% of Total Employed with payslip 75.9 Employed without payslip 10.7 Self-employed 7.8 Unemployed 4.8 Other 0.9 100.0 As was expected the majority of clients are from the township where the lender operates, or from nearby villages. This also confirms the high probability of long terms relationships and good information on clients.

Table 9 Clients’ residential areas

% of Total Townships 45.3 Nearby village 37.4 Other 9.5 Suburbs 6.8 Foreigners 1.1 100.0 Table 8 and Table 9 indicate the occupations and origin of income of the clients of the microlenders. Two points are worth mentioning; the majority of the clients are in formal employment and the majority of the clients come from the same township or nearby village. This is true for both registered and un-registered microlenders. For unemployed borrowers, security is always required. The distinctive difference separating registered and unregistered township micro lenders is that the latter lend money to people they know and trust. For new clients of unregistered microlenders, a compulsory requirement is that they should be referred by existing clients.

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 12

It is also clear that the clients described here mostly work in formal employment, which implies that they borrow from a lender near to their homes, rather than from lenders near to their place of work. It would be interesting to compare the profile of clients of township lenders to the profile of clients of registered lenders outside the township areas. Table 10 shows that almost half of the clients are employed by government and in factories (22.3% and 25.9%), where they would receive payslips. Employment as a domestic worker was the next highest occupation, with 15.7% indicating this as their employment.

Table 10 Clients occupations

% of Tot Factories 25.9 Government 22.3 Domestics 15.7 Township 12.2 Other 10.5 Migrant workers 7.7 Suburbs 4.6 Farms 0.8 Mines 0.5 100.0 As per number of clients per microlender, the results from the questionnaire show that the majority are small operators, as 34 of the microlenders have less than 80 clients each. This also correlates with earlier research in the Eastern Cape (Roth, 1999) that indicated that township based microlenders have small clientele groups with these client/lender relationships spanning many years. Clients are expanded by word of mouth with a trusted and long standing client serving as reference point for new clients.

Table 11 Current numbers of clients

Number of clients No. of ML Percent 1- 20 11 26.1

21 – 40 13 31.0 41 – 80 10 23.9 81 – 120 4 9.5 121 – 250 4 9.5

42 100.0 The microlenders reported that they had on average ten clients when they started their businesses, and 98% have grown their businesses subsequently. While 93% saw opportunities for further growth in the near future, 60% also see an increase in competition. Registered PDI microlenders as per data from the MFRC, shows an average number of clients of 152, which appears to be higher than the selected sample of township microlenders. Competition, faced by 67% of the microlenders interviewed, comes mainly in the form of other lenders, while 20% of respondents also said that the banks were competing in their market.

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 13

Some microlenders interviewed believe that the high unemployment rate forces people to start their own business and micro lending tends to be an easy business to start and is attractive for profit making; this may increase the number of microlenders in the sector and thus result in a possible increase in competition. The majority of unregistered microlenders do not consider competition as a concern. Reasons provided for this argument were:

Banks have entered the micro lending industry but their qualifying requirements are still impossible for the majority of the lower income people. Therefore microlenders are still the most accessible entities. Furthermore, given the way that banks typically operate, they have limited possibilities for getting to know and developing relationships with their clients – a key strength of the township microlender.

Relationships between microlenders and borrowers are very strong and based on trust. As a result, the client retention rate as well as referrals of new clients by old ones is very high. The argument is that it will take a lot of effort and time for new entrants (banks and other microlenders) to build such relationships. In the meantime, those who have been servicing this end of the market have a competitive advantage.

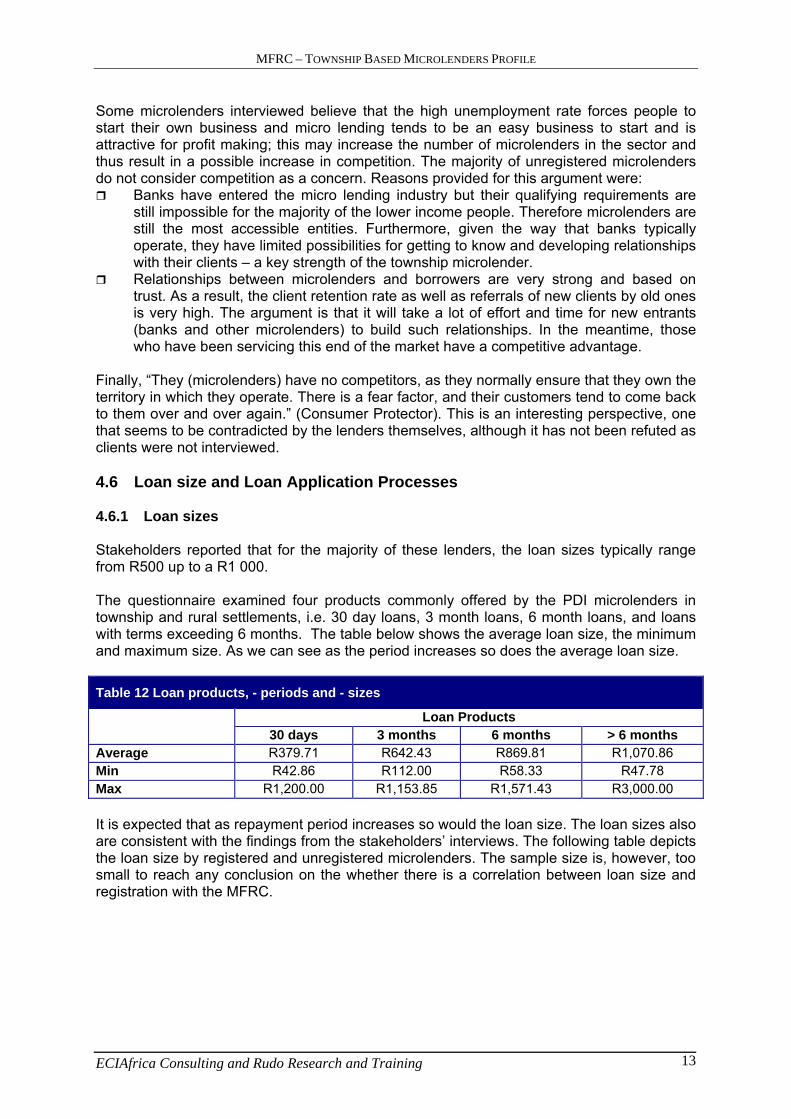

Finally, “They (microlenders) have no competitors, as they normally ensure that they own the territory in which they operate. There is a fear factor, and their customers tend to come back to them over and over again.” (Consumer Protector). This is an interesting perspective, one that seems to be contradicted by the lenders themselves, although it has not been refuted as clients were not interviewed. 4.6 Loan size and Loan Application Processes 4.6.1 Loan sizes Stakeholders reported that for the majority of these lenders, the loan sizes typically range from R500 up to a R1 000. The questionnaire examined four products commonly offered by the PDI microlenders in township and rural settlements, i.e. 30 day loans, 3 month loans, 6 month loans, and loans with terms exceeding 6 months. The table below shows the average loan size, the minimum and maximum size. As we can see as the period increases so does the average loan size. Table 12 Loan products, - periods and - sizes

Loan Products 30 days 3 months 6 months > 6 months

Average R379.71 R642.43 R869.81 R1,070.86 Min R42.86 R112.00 R58.33 R47.78 Max R1,200.00 R1,153.85 R1,571.43 R3,000.00 It is expected that as repayment period increases so would the loan size. The loan sizes also are consistent with the findings from the stakeholders’ interviews. The following table depicts the loan size by registered and unregistered microlenders. The sample size is, however, too small to reach any conclusion on the whether there is a correlation between loan size and registration with the MFRC.

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 14

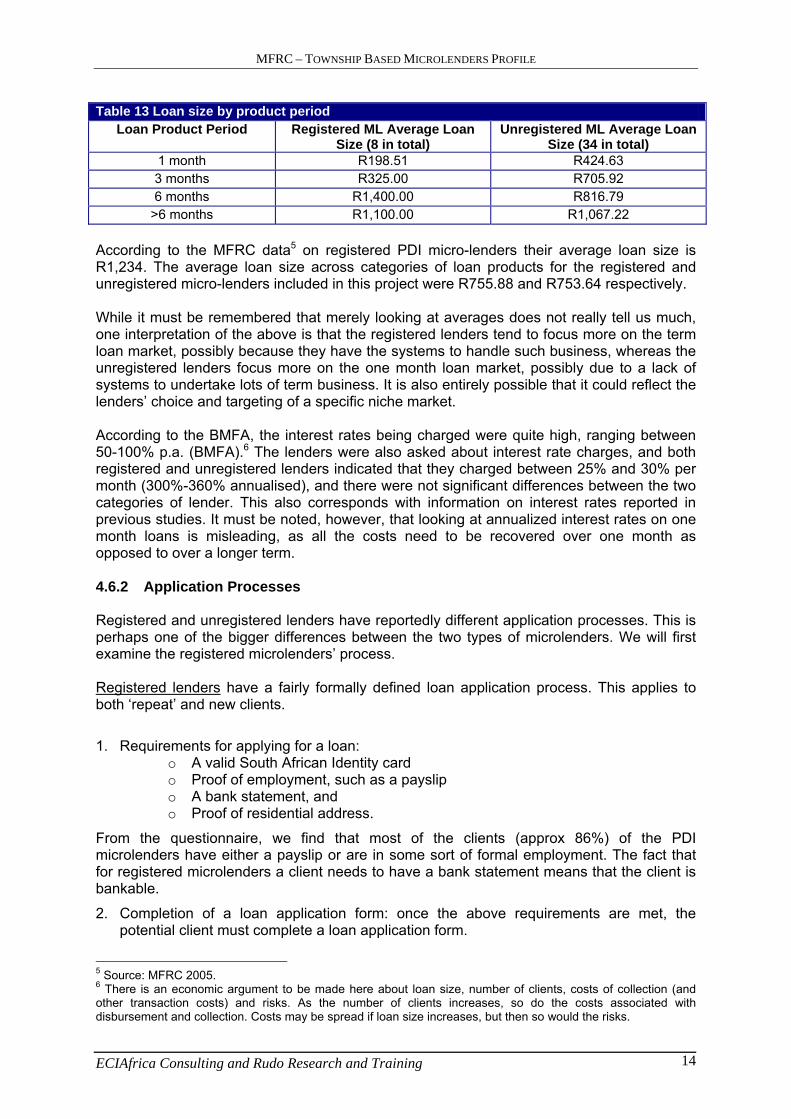

Table 13 Loan size by product period Loan Product Period Registered ML Average Loan

Size (8 in total) Unregistered ML Average Loan

Size (34 in total) 1 month R198.51 R424.63

3 months R325.00 R705.92 6 months R1,400.00 R816.79

>6 months R1,100.00 R1,067.22 According to the MFRC data5 on registered PDI micro-lenders their average loan size is R1,234. The average loan size across categories of loan products for the registered and unregistered micro-lenders included in this project were R755.88 and R753.64 respectively. While it must be remembered that merely looking at averages does not really tell us much, one interpretation of the above is that the registered lenders tend to focus more on the term loan market, possibly because they have the systems to handle such business, whereas the unregistered lenders focus more on the one month loan market, possibly due to a lack of systems to undertake lots of term business. It is also entirely possible that it could reflect the lenders’ choice and targeting of a specific niche market. According to the BMFA, the interest rates being charged were quite high, ranging between 50-100% p.a. (BMFA).6 The lenders were also asked about interest rate charges, and both registered and unregistered lenders indicated that they charged between 25% and 30% per month (300%-360% annualised), and there were not significant differences between the two categories of lender. This also corresponds with information on interest rates reported in previous studies. It must be noted, however, that looking at annualized interest rates on one month loans is misleading, as all the costs need to be recovered over one month as opposed to over a longer term. 4.6.2 Application Processes Registered and unregistered lenders have reportedly different application processes. This is perhaps one of the bigger differences between the two types of microlenders. We will first examine the registered microlenders’ process. Registered lenders have a fairly formally defined loan application process. This applies to both ‘repeat’ and new clients.

1. Requirements for applying for a loan: o A valid South African Identity card o Proof of employment, such as a payslip o A bank statement, and o Proof of residential address.

From the questionnaire, we find that most of the clients (approx 86%) of the PDI microlenders have either a payslip or are in some sort of formal employment. The fact that for registered microlenders a client needs to have a bank statement means that the client is bankable.

2. Completion of a loan application form: once the above requirements are met, the potential client must complete a loan application form.

5 Source: MFRC 2005. 6 There is an economic argument to be made here about loan size, number of clients, costs of collection (and other transaction costs) and risks. As the number of clients increases, so do the costs associated with disbursement and collection. Costs may be spread if loan size increases, but then so would the risks.

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 15

3. The microlender then interviews the potential client to verify information provided in the application form.

4. Affordability check: the microlender then checks the loan amount applied for against the applicants pay slip and bank statement to determine affordability.

5. If everything is in order they both sign the loan agreement, then

6. The loan is disbursed. Unregistered microlenders, on the other hand have two application processes; one for new clients and the other for repeat/existing clients, as follows: First time borrowers The process follows the steps below:

Applicant must be referred and accompanied by an existing client – known and trusted by the lender.

Loan requirements: not all the requirements are necessary. The following are the most common:

o South African identity card o Payslip o Proof of residential address o 2 references o Employer’s address

The survey results indicate that 57% of the lenders require references, 35% require payslips and the rest require credit records, bank statements and other records. It is clear from the table that some lenders require more than one of these information sources before they consider applicants. Some of the lenders reported that they also obtain references from officials of the local authority.

Table 14 Affordability and eligibility checks used by lenders

% of ML References 57.1 Payslip 35.7 Credit records 21.4 Other 14.3 Bank statement 9.5 Those who lend to unemployed people indicated that they require security in the form of jewellery, appliances or any valuables and these are claimed if borrowers default. One unregistered lender indicated “if borrowers do not pay my money back, I confiscate their appliances, furniture or cell phones”. These lenders have also indicated that claiming security is a very risky process as more often borrowers retaliate and the lender has to take security by forceful means. However, the majority of lenders do not require security, as most of the clients are employed and can provide a pay slip as proof of employment.

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 16

Table 15 Number of security measures used by lenders

Number of Security Measures No. of ML % 0 33 78.6 2 5 11.9 4 4 9.5

Total 42 100.0 Out of the ones that ask for security, 14% of microlenders will ask for appliances, and about 12% will ask for furniture, while 7.1% accept jewellery as security and another 7.1% accept other means of security.

If most of the above requirements are met (albeit not all of them), the microlender then interviews the potential borrower to verify the documents and discuss the loan size required - in the presence of the guarantor.

The microlender then explains the loan terms: repayment period, repayment method, interest rates, implications etc.

The borrower signs a book as the lenders do not use application forms. Some go the police station to sign in the presence of a police officer.

Repeat/Existing Clients Repeat clients have a special relationship with the microlenders, mainly based on mutual trust and honesty. This relationship exempts this category of clients from the above process. All that is required from them is to mention the loan amounts they require, sign the books and they get the money. The above descriptions of the loan application processes (particularly for repeat clients) reflects the different modus operandi of the formalised and less formalised lenders, and emphasizes the important role that the lender-client relationship plays in the business of the less formal lenders. 4.7 Repayment, Portfolio Quality and Collection For both types of microlenders, borrowers take monthly instalments to the lender on agreed dates – usually on pay day, and sometimes a microlender collects from borrowers’ homes or work places. Microlenders have also indicated that borrowers always honour the agreement and pay on time minimising the need for formal recovery processes to be put in place. One registered lender mentioned that his customers make their payments by debit orders directly into his bank account. For those whose IDs and bank cards are kept by an unregistered microlender, they accompany the microlender to the ATM to withdraw the payment on the payday. While not confirmed by lenders, one stakeholder stated that ”lenders have runners who work for them. These runners have their own networks which connect them to people who need money. Runners are also the ones who collect repayments, and ensure that their customers pay.”(Consumer Protector) Registered microlenders do not think repayment is a problem. If, for unforeseen circumstances a client will fail to make a repayment on time, he informs the microlender in advance to arrange for an extension. Some unregistered lenders argued that repayment is not a major problem because they only deal with people that they know and trust. However, it may be a problem with new clients. When it does happen that borrowers do not repay, microlenders feel that they do not repay because the borrowers know that microlenders cannot take legal action.

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 17

Results from the questionnaire support these statements7 and indeed the portfolio quality is good, and it does reflect the closer than usual relationship between the microlender and borrower evidenced in this segment of the market. When considering repayment, 31% of lenders said that 10 out of 10 borrowers regularly made repayments on time. Approximately 19% of the microlenders said that 30% of their 1 month loans had not been paid on time and 69% of microlenders said none of their clients were more than three months late. Approximately 36% of microlenders have had experience of some loans not being repaid at all.

Table 16 Repayment on time

Out of ten, how many have repaid on time? No. of ML % .00 1 2.4

2.00 1 2.4 3.00 2 4.8 4.00 4 9.5 5.00 1 2.4 6.00 2 4.8 7.00 8 19.0 7.50 1 2.4 8.00 7 16.7 9.00 1 2.4 9.80 1 2.4 10.00 13 31.0 Total 42 100.0

Payment collection does not seem to be a problem. Microlenders interviewed have two modes of collection - either the clients come to their premises or the microlender owner visits the clients, 22 microlenders would visit the clients, whereas 37 reported that the clients come to them. There is some overlap between the two methods. The collection method of lenders visiting the borrowers also serve as an illustration of the relationship between borrower and lender which are indeed different than in the case of the majority of registered lenders. “There is trust between me and my client”, says a lender in Rustenburg.

Table 17 Cases where borrowers did not repay at all

Out of 10, how many borrowers have not repaid at all? No. of ML Percent 0.00 27 64.3 1.00 9 21.4 1.50 1 2.4 2.00 4 9.5 3.00 1 2.4 Total 42 100.0 Although the majority of the microlenders interviewed do not seem to take action, if the client is delinquent or defaulting, some microlenders will attempt in collecting the payment him/herself.

7 The sample was split unregistered micro-lenders to explore whether the repayments differ amongst the two categories. Correlation tests were carried out and they were not significant. Probably the reason for this is that the sample size is too small to pick up differences.

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 18

Table 18 Ways of collecting on arrears or default payments

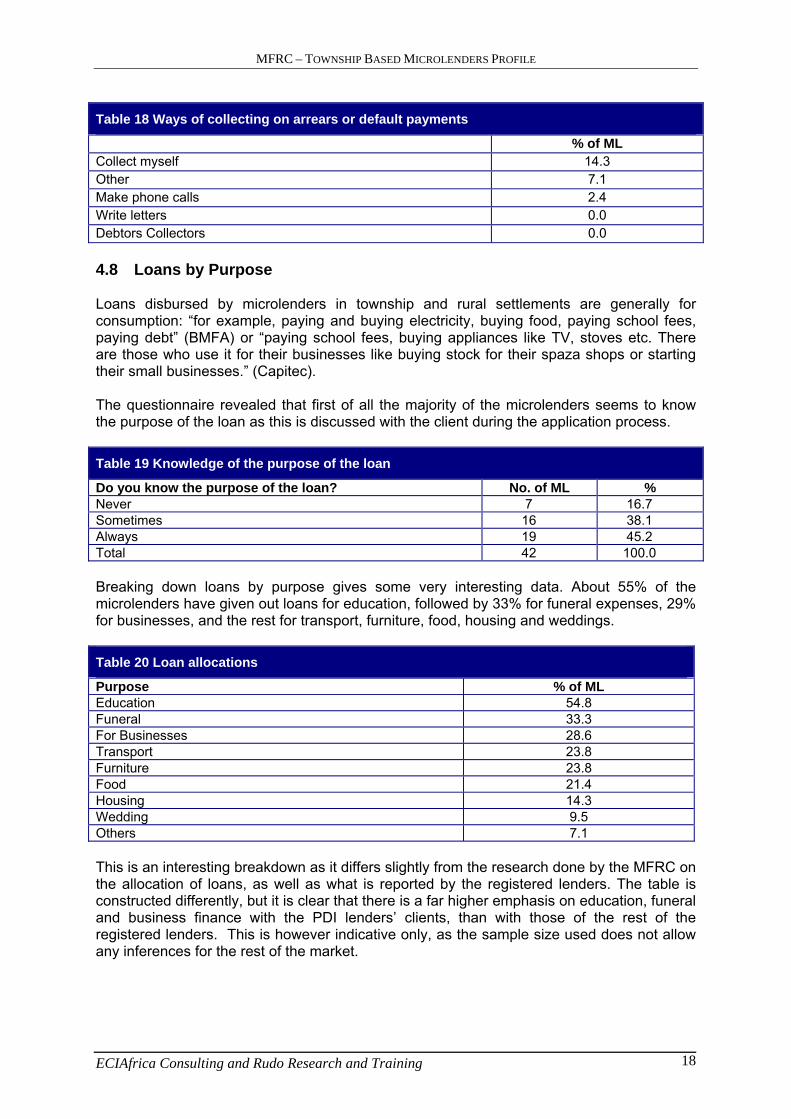

% of ML Collect myself 14.3 Other 7.1 Make phone calls 2.4 Write letters 0.0 Debtors Collectors 0.0 4.8 Loans by Purpose Loans disbursed by microlenders in township and rural settlements are generally for consumption: “for example, paying and buying electricity, buying food, paying school fees, paying debt” (BMFA) or “paying school fees, buying appliances like TV, stoves etc. There are those who use it for their businesses like buying stock for their spaza shops or starting their small businesses.” (Capitec). The questionnaire revealed that first of all the majority of the microlenders seems to know the purpose of the loan as this is discussed with the client during the application process.

Table 19 Knowledge of the purpose of the loan

Do you know the purpose of the loan? No. of ML % Never 7 16.7 Sometimes 16 38.1 Always 19 45.2 Total 42 100.0 Breaking down loans by purpose gives some very interesting data. About 55% of the microlenders have given out loans for education, followed by 33% for funeral expenses, 29% for businesses, and the rest for transport, furniture, food, housing and weddings.

Table 20 Loan allocations

Purpose % of ML Education 54.8 Funeral 33.3 For Businesses 28.6 Transport 23.8 Furniture 23.8 Food 21.4 Housing 14.3 Wedding 9.5 Others 7.1 This is an interesting breakdown as it differs slightly from the research done by the MFRC on the allocation of loans, as well as what is reported by the registered lenders. The table is constructed differently, but it is clear that there is a far higher emphasis on education, funeral and business finance with the PDI lenders’ clients, than with those of the rest of the registered lenders. This is however indicative only, as the sample size used does not allow any inferences for the rest of the market.

MFRC – TOWNSHIP BASED MICROLENDERS PROFILE

ECIAfrica Consulting and Rudo Research and Training 19

Table 21 MFRC Statistics of Use of Loans, 2003