tpl jul 7 15

TRANSCRIPT

ABRAHAM [email protected]

2015 issue 12July 7, 2015

Was That an Earthquake? Serious quakes threaten not only growth prospects but also various market performances. What those quakes are, however, are no easy issue either. Is itthe Greek nightmare? The negative result of the Greece vote and how long the Greek population will tolerate the bank holiday and capital controls remainanyone's guess. Does it portend the end of the euro? Is it the boom - bust in China’s equity markets? One cannot easily dismiss China’s stock market asonly an innocuous market gyration. But the government’s direct involvement in pumping the markets up, and its failure to keep it aloft, should haveinvestors concerned about China’s ability to control even more consequential developments. What of developments in Iran and recent patterns incommodity markets? What about the deterioration in Puerto Rico debt? We also continue to highlight the new and tougher geopolitical backdrop. What ofthe U.S. economy heading into a period of monetary tightening. We expect the first Fed rate increase before the end of 2015. We also expect the pace andextent of tightening to be subdued by historical norms, but higher rates will increase debt-servicing costs, and we need to recognize that rates have beenso abnormally low that even a gentle exit from a long period of loose monetary policy could increase financial market and asset price volatility, affectinghousehold wealth and confidence.

EU carmakers warned China ‘cash cow dying’Returns decline due to slowing economy, limits on urban ownership and rising competitionThe Federal Reserve signaled a pickup in

the economy is keeping it on track toraise interest rates this year, thoughsubsequent increases are likely to bemore gradual than anticipated earlier.

Bank of Greece warns of ‘painful’ Grexit

EU agrees to extend Russia sanctionsPersistent violations harden resolve in Brussels and frustrate Moscow’s hopes of a turning point

Both U.S. shale producers and OPEC appear to be relyingfar too heavily on unreliable demand forecasts, whichcould prove a catastrophic misjudgment by 2016

Greek drama – will it waylay Fed?

Looming Puerto Rican default grows nearer

Can monetary easing prevent harsh China slowdown?

Big deals pick up paceSurge in transactions above $5bn sparks valuation worries in a year that is set to be strongest for mergers since crisis

Greece’s plight at odds with public's lack of concern

Global supply glut will keep oil price subdued

Regulators Warn Banks on Loans to Oil, Gas ProducersMove could limit ability of energy companies to obtain financing

Eurozone Into the Unknown

What is going on in Iran?

China's passenger vehicle sales declined for the first time since 2013 as weakeconomic growth weighed on auto demand.Car sales were down 3.2 percent year-on-year to 1.43 million units in June, the China Passenger Car Association reported.

The PunchLine...

2

July 7, 2015

In This Issue

Headlines and data appearing in The Punch Line came from widely available publications including national and international newspapers, trade journals, economic and industrial bulletins and news websites.

• Households… (pg 7)

• U.S. Jobs Update… (pg 8)

• Job Reference Points… (pg 9)

• Dislocation, Dislocation… (pg 10)

• The Likelihood of Unlikely Events... (pg 11)

• Think it Through… (pg 12)

• Credit… (pg 13)

• A New Geography of Business… (pg 14)

• Pumping Iron … (pg 15)

• The DNA of Business… (pg 16)

• Real Estate and Construction… (pg 17)

• Will Life Ever be the Same? (pg 18)

• Was That an Earthquake? …Serious quakes threaten not only growth prospects but also various marketperformances. What those quakes are, however, are no easy issue either. Isit the Greek nightmare? The negative result of the Greece vote and how longthe Greek population will tolerate the bank holiday and capital controls remainanyone's guess. Does it portend the end of the euro? Is it the boom - bust inChina’s equity markets? One cannot easily dismiss China’s stock market asonly an innocuous market gyration. But the government’s direct involvementin pumping the markets up, and its failure to keep it aloft, should haveinvestors concerned about China’s ability to control even more consequentialdevelopments. What of developments in Iran and recent patterns incommodity markets? What about the deterioration in Puerto Rico debt? Wealso continue to highlight the new and tougher geopolitical backdrop. What ofthe U.S. economy heading into a period of monetary tightening. We expectthe first Fed rate increase before the end of 2015. We also expect the paceand extent of tightening to be subdued by historical norms, but higher rateswill increase debt-servicing costs, and we need to recognize that rates havebeen so abnormally low that even a gentle exit from a long period of loosemonetary policy could increase financial market and asset price volatility,affecting household wealth and confidence. (pg 1)

• In This Issue (pg 2)

• The Return to Normal… (pg 3)

• You Can’t Handle the Truth ! (pg 4)

• Market Roar… (pg 5)

• Engines of GrowthConflicting economic signals emanating around the globe have confounded investors andcontributed to intermittent bouts of volatility, even in government bond markets. Despitemassive easing, most of the global economy faces woefully inadequate growth prospectsand difficult policy options. Very obvious financial vulnerabilities, and serious geopoliticalconcerns are aggravating the uncertainty. And let’s not forget that many of thechallenges are not fleeting and cannot be resolved easily … (pg 6)

Contact information:

Abraham Gulkowitz

phone: 917-402-9039 email: [email protected]

The PunchLine...

3

July 7, 2015

The Return to Normal ?

Dollar Strength Saps Many Companies

The pick-up in global economic growth forecasted for2016 reflects a recovery from recession in Brazil andRussia, albeit a weak one; while the structuralslowdown in China continues to weigh on globalgrowth potential. The U.S. Fed will start the globalmonetary tightening cycle with the first rate increasebefore the end of 2015, followed by the Bank ofEngland. However, the pace and extent of thetightening will be subdued by historical norms.

Greece and its membership in Europe's joint currency facedan uncertain future Monday, with the country underpressure to restart bailout talks with creditors as soon aspossible after Greeks resoundingly rejected the notion ofmore austerity in exchange for aid. With Greek banksrunning out of cash and facing the danger of collapsewithin days without new aid, the government in Athens isracing against the clock. In an effort to facilitatenegotiations on a new aid program, Finance Minister YanisVaroufakis, who had clashed with European officials in thebailout talks, announced his resignation Monday. ButGreece and its creditors, who will meet again Tuesday todiscuss how to keep the country in the euro, remain farapart on key issues, particularly the notion of debt relief.

The U.S. trade deficit widenedin May, fueled by a drop inexports that could heightenconcerns over weak overseasdemand and a strong U.S. dollar.

The PunchLine...

4

July 7, 2015

YouCan’t Handle the Truth…Let's Take the “Con” out of Economics

The Federal Open MarketsCommittee announced that they seegrowth expanding moderately, labormarkets picking up and theconsumer sector as moderate. Oneof the conundrums of the USeconomy that will influence theFederal Reserve's timing of aninterest rate rise (currently projectedfor September) is where the savingsfrom low energy prices have gone.Oil prices have dropped sharplysince September 2014, from 97dollars per barrel for West TexasIntermediate in June 2014 to 60dollars per barrel. Yet US personalconsumption expenditures (PCE)only grew by 2.7%, well below therate of growth of personal income,4.1%

Capital control grenade hovers over Greek impasseIf the Tsipras government can’t agree on bailout terms, Europewill soon be able to justify freezing Greek deposits. Athensmight then be scared into a deal, but might also quit the eurozone. EU politicians need to make the threat credible - but theydon’t want to pull the pin.

Standard & Poor's rating agency cut Greece's creditrating further into junk status Monday and said thereis now a 50% chance of Greece leaving the eurozone.

Demand for big‐ticket manufactured goods fellfor the third time in four months, the latest signof caution among businesses. US new ordersfor durable goods—products such as computersand trucks designed to last at least threeyears—decreased a seasonally adjusted 1.8% inMay from a month earlier, the CommerceDepartment said. April durable goods orders fella revised 1.5%, compared with the previouslyreported 1% decrease. Through the first fivemonths of the year, overall orders are down2.2% compared to the same period in 2014.

US crackdowns may impel global 'Dark Web' successorsThe 'Dark Web' has grown in prominenceover the last few years. The term isassociated with a shadowy, anonymousunderworld online where criminals interactto engage in fraud, drug sales, childpornography trading, and weapons sales. Itis also where political activists, dissidents,whistleblowers, police, spies and manyothers operate. While media depictions ofcybercrime are often over-hyped, there issome accuracy in these presentations asthey strike at the core of a problematicphenomenon: Tor-based websites hostingcriminal services.

Amid the acrimonious debate over trade, the U.S. export-import bank is being shuttered after losing Congressional support, threatening the loss of jobs and overseas contracts to rivals such as China. However, large companies like Boeing accounted for more than 30% of the total ExIm support in 2013. Aircraft sales have long been one of the bank’s main business lines

ENERGY SECTOR CREDITS SUBSTANDARD U.S.regulators are sounding the alarm about banks’ exposure to oil-and-gas producers, a move that could limit their ability to lend tocompanies battered by a yearlong slump in prices. The FederalReserve, Office of the Comptroller of the Currency and FederalDeposit Insurance Corp. are telling banks that a large number ofloans they have issued to these companies are substandard, saidpeople familiar with the matter, as they issue preliminary resultsof a joint national examination of major loan portfolios. Thesubstandard designation indicates regulators doubt a borrower’sability to repay or question the value of the assets that back aloan. The designation typically limits banks’ ability to extendadditional credit to the borrowers. The move could add an extraobstacle to companies struggling with high debt loads amid lowerprices for the oil and natural gas they produce. Banks have beenflexible with troubled energy companies to avoid triggering aflood of defaults and bankruptcy filings, but regulatory pressurecould force them to tighten the purse strings.

China’s Bazooka Fails to OverwhelmChina’s stock market bailout probably won’t work. A bigger question is why the country’s leaders felt the need to do it in the first place

Oil Prices Tumble Nearly 8%Oil prices skidded to their biggest single-daydeclines in more than three months, as gyrationsin Chinese stocks and the prospect of more crudefrom the U.S. and Iran revived worries about theglobal supply glut.

Copper prices tumbled to a five-month low Monday,weighed down by sliding oil prices and mounting losses onChinese stock markets.Copper for July delivery, the most actively traded contract, closeddown 3.5% to $2.5380 a pound on the Comex division of the NewYork Mercantile Exchange, its lowest level since Feb. 2. Thepercentage drop was the largest since Jan. 14.

The PunchLine...

5

July 7, 2015

The Market Roar…

The tech-heavy Nasdaq Composite ripped past the all-time high it struck during the Dot-Com bubble amid optimism over a dovish Fed.

It is easy to dismiss China’s stock market as nothing but an innocentmarket gyration. But the magnitude of the boom and bust is breathtaking and government’s direct involvement in pumping it up, and itsfailure to keep it aloft, should have investors concerned about China’sability to control even more consequential markets.

Cliff Diving

China’s Market Rout Is a Double ThreatA failure to halt the sell-off in stocksin the last three weeks has shakenBeijing’s aura of invincibility andimperils the global economy.

Latest = 8286

Latest=8286

The PunchLine...

6

July 7, 2015

Engines of Growth…

U.S. states plan to slow spending growth in fiscal2016, taking a cautious approach to forecastingand budgeting amid only modest increases inrevenue, according to a survey of statespublished on Tuesday. General fund spendingwill rise by 3.1 percent for the fiscal yearbeginning July 1, below the estimated 4.6percent for the current year, according to thesemi‐annual survey by the National Associationof State Budget Officers (NASBO).

China’s Factory Activity Remained Weak in JuneManufacturing reading edges higher but is still below level separating expansion from contraction

A survey by the Confederation of British Industrysuggests that June manufacturing orders in the U.K.weakened to the lowest level since March 2013. Thestrengthening pound and uncertainty caused by thedifficulties in Greece are dampening exports.

Industrial production in Japan contracted by 4 percentin May (y/y), the sharpest fall since June 2013, andsubstantially below expectations. While informationand telecommunications production has been sustained(helped by the weaker yen), other sectors, like transportequipment and chemicals, have been weak.

Japan’s population slide acceleratesBigger drop expected every year until the 2060s, with annual decline already the size of a city

Canada 2015 Capex Intentions -4.9% Vs 2014; Ex Oil & Gas +1.9%--Spending Intentions Decline -4.9%, Largest Drop Since 2009--Mining, Quarrying, Oil & Gas Extraction -18.7%‐‐Private Sector ‐7.0%; Public Sector ‐0.2%Non‐residential capital spending is expected todecline 4.9% this year from 2014, dragged bythe energy sector, Statistics Canada's datashowed Monday. The 4.9% decline was thelargest since 2009, when investment fell 16.1%.

Taiwan's exports declined for the fifth straight month in June at a faster-than-expected pace, preliminary figures from the Ministry of Financeshowed Tuesday. Exports plunged 13.9 percent year-over-year in June,much faster than previous month's 3.8 percent decline. Economists hadexpected a 6.0 percent decrease for the month. The latest decline wasthe sharpest since February 2013, when exports slipped 15.8 percent.Exports of electronic products slid 10.8 percent in June from a year agoand that for basic metals and articles thereof dipped by 17.2 percent.

The PunchLine...

7

July 7, 2015

Households – Brave New World

Lending Tree and hundreds of smallbanks partner up to lend… The moveisn’t without risk: Some observers wonder ifthe community banks are handing acompetitor information on customers andmaking them more likely to go to an onlinefirm rather than a bank branch for mortgagesor other financial needs.

Shale glut turbocharges motoring revivalFord ramps up output as US drivers make use of lower fuel costs

CoreLogic® ... released its May 2015 CoreLogic Home Price Index(HPI®) which shows that home prices nationwide, including distressedsales, increased by 6.3 percent in May 2015 compared with May 2014.This change represents 39 months of consecutive year-over-yearincreases in home prices nationally.

Housing rebound remains inadequate

The PunchLine...

8

July 7, 2015

U.S. Jobs Update: Go Figure… Where Now?

Though some of the decline in labor forceparticipation is tied to the retirement ofbaby boomers, prime-age male workers —between 25 and 54 years old — are alsositting increasingly on the sidelines. Theprime age participation rate for men nowstands at 88.2 percent, compared with 90percent six years ago and 92 percent in2000. Meanwhile, job growth for Apriland May was revised downward by acombined 60,000 positions. With the yearhalf over, the nation is on pace to add 2.5million jobs this year, as opposed to 3.1million in 2014.

Jobs at a Crossroads: Hiring Up, Pay FlatThe U.S. job market sits at a crossroads six years into a fitfuleconomic expansion: Hiring is strong, but weak wagegrowth has failed to pull millions of would-be workers offthe sidelines while prompting others to drop out of the laborforceThe job gains, indicative of a general upswing from a weakfirst quarter, were negatively colored by stagnant wagegrowth and a declining number of Americans participatingin the labor force. The number of Americans consideredmarginally attached to the labor force—not actively lookingbut still available for work—stood at 1.9 million, littlechanged over a year that saw the creation of 2.9 millionjobs.

Changing EU employment spotlights poverty measurementAccording to EU and OECD reports on incomes, employment offers a weakeningguarantee against the risk of deprivation. In-work poverty is closely associated withlow levels of hours worked. Unconventional employment, often involving less-than-full hours, is rising as a share of the total, with greater work-related incomeuncertainty becoming an essential feature of EU job markets. However, cross-countrydata on in-work poverty can be misleading; in the EU, such data typically indicatewage inequality, not absolute poverty.

The PunchLine...

9

July 7, 2015

Job Reference Points…

The PunchLine...

10

July 7, 2015

Dislocation, Dislocation, Dislocation

Copper’s supply glut weighs on pricesThe red metal falls to levels not seen since the financial crisis despite bullish long-term view

Puerto Rico’s governor says island cannot pay back over $70 billion in debt, is near ‘death spiral’

Brazil’s biggest exchange-traded fundtumbled to a one-month low amidspeculation that a possible Greece exit fromthe euro would deepen the largest outflowsamong emerging markets this year.

Puerto Rico's governor, Alejandro Garcia Padilla, announced in a June 29 speech that theisland's current debt load is "not payable". The same day saw the release of a report,authored by former IMF economists, outlining a program of structural reform and sweepingdebt restructuring. Puerto Rico has seen its fiscal situation deteriorate for years, but with aseries of debt repayments due in the next few days and the report, the crisis appears to bereaching a turning point.

Moody's cuts Puerto Rico's bonds further into junk territoryMoody's Investors Service on Wednesdaydowngraded Puerto Rico's generalobligation and guaranteed bonds furtherinto junk territory, citing GovernorAlejandro García Padilla's declaration thatthe commonwealth cannot pay its debt.

The PunchLine...

11

July 7, 2015

The Likelihood of Unlikely EventsFrench economist Thomas Piketty's book'Capital in the 21st century' became abestseller after its publication in Englishearly last year. The book's new account ofthe long-run dynamics of capitalism waslikened to those of Karl Marx and DavidRicardo, and its popular reception returnedthe problem of inequality to the forefrontof policy debate around the world. Sincethen, however, robust critiques haveemerged that cast doubt on Piketty'sfindings, and recommend quite differentpolicies. More Russian infrastructure spending cuts likely

WASHINGTON FEARS LOSING GREECE TO MOSCOW

EU Pressure Points… A recentreport concludes that whether or notGreece is forced out of the singlecurrency, the Eurozone will still facedeep-seated problems that must beresolved by either breaking up or full-blown political integration. When thesingle currency was created in 1999, itsadvocates argued that common economicrules would help its members convergeeconomically, making a single rate ofinterest more and more suitable to all.

Russia-China military ties will deepenChina confirmed yesterday that Russian troops would parade in theSeptember Beijing commemorations marking the end of the Second WorldWar. This follows Chinese troops' participation in Moscow's May VictoryDay event. With Russia's ties with the West currently at their lowest sincethe end of the Cold War as a result of the Ukraine crisis and cooperationwith NATO having suffered, the Kremlin's military relationship with Chinais taking on new significance. This year has seen Moscow and Beijingconduct their first joint Mediterranean Sea drills and further drills areplanned in August. Russia and China now engage in at least one major jointground force and one major bilateral naval exercise annually.

Risks: Declining capital flows to developing countries.If the liftoff were accompanied by a surge in U.S. long-term yields, as happenedduring the taper tantrum, the reduction of capital flows to emerging markets could besubstantial. Changing global financial conditions—especially U.S. yields—drive alarge part of movements in capital flows to emerging markets. Estimates suggest that a100 basis point jump in U.S. long-term yields in response to the liftoff (as occurredduring the taper tantrum) could temporarily reduce capital flows to developingcountries by 0.8–1.8 percentage points of GDP, depending on the degree of pass-through into long-term interest rates in other major advanced economies (Figure 3.D).Stated differently, developing countries would collectively experience an estimated18–40 percent decline in the level of capital flows they received in 2014. While thedecline in capital flows could create policy challenges, they would probably bemanageable for most countries.

Risks with rates... However, the liftoff and

subsequent rate increases carries risks for emergingmarkets. The “taper tantrum” of May‐June 2013 is areminder that even an event anticipated by markets cangenerate spikes in U.S. long‐term yields, significantfinancial market volatility, and shifts in emergingmarket capital flows. Three factors currently heightenthe risk of volatility. First, U.S. term premia are wellbelow their historical average and could correct sharply.Second, market expectations of future interest rates arecurrently below those of members of the U.S. FederalOpen Market Committee. And third, market liquidityconditions are fragile.

Russia's FSB will benefit from instabilityOn June 29, Russia's federal security service, the FSB, detained Crimea's industrialpolicies minister on corruption charges. Four days earlier, Moscow's LefortovoDistrict Court charged a dual Russia-Lithuanian national with treason followingespionage allegations by the FSB. As the Kremlin seeks to intensify Russia's counter-intelligence and counter-terrorism efforts and to tighten its grip on the country's elitesahead of next year's elections, the FSB is taking advantage of the nationalisticallycharged atmosphere to expand its power further.

Capital controls squeeze Greek economyPrice exacted by the extraordinary measures becomes increasingly apparentGreece needs huge aid package

Developing‐country stocks slumped to the lowest level thisyear as Chinese shares continued to tumble. Following thebiggest fall in two years on Monday, the benchmark MSCIEmerging Market index fell 1.4 percent with China’sShanghai Composite Index slipping 1.3 percent amid arecord drop in margin trading. Chinese stocks continued toslide as government measures to stabilize the market failedto stop a sell‐off that has wiped out more than $3.2 trillionin market capitalization. The developing‐country stockgauge has declined 2.7 percent this year, while thedeveloped‐market stock index has gained 0.9 percent.

The PunchLine...

12

July 7, 2015

Think it Through…

The PunchLine...

13

July 7, 2015

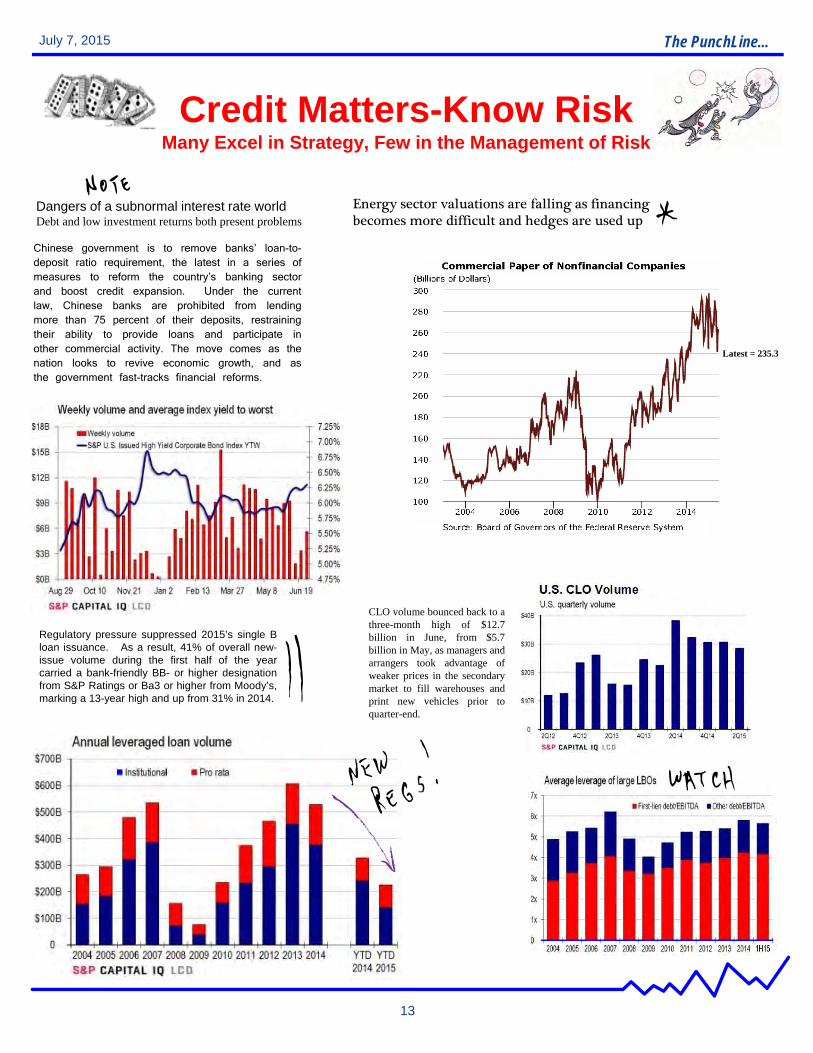

Credit Matters-Know RiskMany Excel in Strategy, Few in the Management of Risk

Dangers of a subnormal interest rate worldDebt and low investment returns both present problems

Energy sector valuations are falling as financing becomes more difficult and hedges are used up

Chinese government is to remove banks’ loan-to-deposit ratio requirement, the latest in a series ofmeasures to reform the country’s banking sectorand boost credit expansion. Under the currentlaw, Chinese banks are prohibited from lendingmore than 75 percent of their deposits, restrainingtheir ability to provide loans and participate inother commercial activity. The move comes as thenation looks to revive economic growth, and asthe government fast-tracks financial reforms.

Regulatory pressure suppressed 2015’s single Bloan issuance. As a result, 41% of overall new-issue volume during the first half of the yearcarried a bank-friendly BB- or higher designationfrom S&P Ratings or Ba3 or higher from Moody’s,marking a 13-year high and up from 31% in 2014.

CLO volume bounced back to athree-month high of $12.7billion in June, from $5.7billion in May, as managers andarrangers took advantage ofweaker prices in the secondarymarket to fill warehouses andprint new vehicles prior toquarter-end.

Latest = 235.3

The PunchLine...

14

July 7, 2015

A New Geography of Business

Hungary plans giant fence to halt migrantsBudapest says plans for barrier on southern border with Serbia already under way

INDIA Prime Minister Narendra Modi's second year ingovernment to May 2016 will be harder than the first. TheGDP rebase and lower oil prices propelled growth to anestimated 7.5% year-on-year in the January-March quarter, butpoor weather and a US interest rate hike loom over economicprospects. The incumbent Bharatiya Janata Party (BJP) sweptimportant state elections last year, but the 'Modi wave' is losingmomentum. The prime minister has been active on foreignpolicy, but now faces pressure to deliver new investment andtrade opportunities for India.

Japanese industry will adapt to South Korean advanceSouth Korea has at last accomplished a national goal it haspursued since the 1960s: catching up with Japan. A cohort ofSouth Korean manufacturing giants has leapt forward, not justcatching up but leaving Japanese rivals behind. Contrary topopular perceptions, however, Japanese industry has notcorrespondingly declined. In some sectors, Japan has retainedor even sharpened its edge, while in others Japanese firmshave taken advantage of South Korea's success.

Indonesia Manufacturing PMIOperating conditions deteriorate for ninth successive month

The Markit PMI for the Turkishmanufacturing sector fell more-than-expected to 49.0 from 50.2 in May.Economists had expected the index tofall to the neutral 50 mark. Both outputand new orders fell at sharper rates inJune as the inconclusive election resulthad undermined confidence. Theheadline figure has been in thecontraction territory five times in thefirst half of 2015, averaging 49.2, whichremained below the long-run average of50.9.

Three‐fifths of Greek voters cast 'No'ballots as recommended by thegovernment in yesterday's referendumon whether Greece should accept itscreditors' latest bailout conditions.Greece's government and voters havedelivered a punishing blow to euro‐areapolicies. However, the underlyingdilemmas remain unchanged: whethercreditors will countenance debt relief,whether the Greek government canproduce credible commitments onreform, and whether euro‐area leaderscan manage their domestic politicalconstraints and divisions.

Philippine borrowers: highly leveragedLower-income households may be at risk of default despite efforts to dampen mortgage demand

German Construction Sector Growth At Five-Month LowGermany's construction sector activity grew at the weakest pace in fivemonths in June as new orders declined, survey data from MarkitEconomics showed Monday. The seasonally adjusted PurchasingManagers' Index, or PMI, for the construction sector, declined to 50.7 inJune from 50.8 in the previous month. Any reading above 50 indicatesexpansion in the sector. Civil engineering building projects contracted ata slower pace in June when compared to the previous month.

Political crisis hits Chile’s economyBusiness confidence undermined by reform programme and political crisis

New Zealand's business confidence dropped to its lowest level in nearly three years in the second quarter on softening demand conditions, the New Zealand Institute of Economic Research's Quarterly Survey of Business Opinion showed Tuesday. The survey showed that the New Zealand economy is losing momentum in the second quarter.

The PunchLine...

15

July 7, 2015

Pumping Iron…The Old Economy Revisited

The top three ocean carriers —Maersk Line, MediterraneanShipping Co. and CMA CGM —have boosted their share of globalcontainer capacity to 38 percentfrom 26 percent over the pastdecade and are continuing to pullahead of their rivals, according toDrewry Maritime Research.

European car sales rose at the slowest pace in six months in May as buyers’ concerns about unemployment and the Greek sovereign debt crisis held back demand at Volkswagen AG and Renault SA.

Policymakers acknowledge that weak investment ratesundermine prospects for long-term growth. Consequently, theyare seeking ways to boost infrastructure spending, includingthrough special funds. New Chinese-backed bilateral andmultilateral funding sources will facilitate this by augmenting, butnot displacing, existing institutions, while bolstering China'sleadership role.

U.S. auto makers’ ability to finance costlytechnology and emissions requirements fromearnings will be tested by a broader group ofcompetitors that for the first time include moreprofitable Indian and Chinese car makers

More than 60 million barrels of oil inventory werestored at a network of storage tanks in the Dutchports of Amsterdam and Rotterdam andBelgium’s Antwerp in June.

Strong demand for sport utilityvehicles and trucks in June helpedGeneral Motors Co and Ford MotorCo offset slowing demand for sedansby allowing them to raise prices ontheir trucks.

Iron ore price fall a sign China's economic might be much weaker

Iron Ore Nose-Dives on Supply SurgeSteelmaking commodity endures its sharpest one-day fall since March, sparking fears of another bear run

El Nino on Radar

U.K. new car registrations increased to the highest half-year total on record in the first half of 2015, the Society ofMotor Manufacturers and Traders, or SMMT, reportedMonday. The number of registered cars increased 7 percentto 1,376,889 units in the first half from 1,287,265 units inthe previous year period. This bettered the previous recordof 1,376,565 units in the same half-year period of 2004.Buyers' appetite for British-built cars increased in the firsthalf, with 13.9 percent choosing a UK-manufacturedvehicle so far this year, which is the highest level in fiveyears. SMMT said low interest rates, attractive financedeals, and new models led consumers to buy new cars.

The PunchLine...

16

July 7, 2015

The DNA of BusinessReconfiguring Industries to Define Growth

AT&T just got hit with a $100 million fine after slowing down its ‘unlimited’ dataThe Federal Communications Commission slapped AT&T with a$100 million fine Wednesday, accusing the country's second-largest cellular carrier of improperly slowing down Internet speedsfor customers who had signed up for "unlimited" data plans.

CVS Pays $1.9 Billion for Target Pharmacy…

Health insurance giant Anthem presses for Cigna takeover at $54 billion

Cheap Energy Poised to Shake Up Pipeline IndustryLow oil-and-gas prices are poised to spur a merger battle among firms that own the key pipelines around the country.

European Grocery Chains to Create U.S. Supermarket GiantEuropean grocery chains Royal Ahold andDelhaize Group have agreed to a merger,creating one of the largest supermarketoperators in the U.S., with a combinedvalue of more than $29 billion.

Russia's Asian gas pivot will progress slowlyLast year, Russia's President Vladimir Putin signed a 30 yeardeal worth 400 billion dollars to sell 38 billion cubic metres(bcm) yearly of natural gas to China, starting in 2018-19.Gazprom will have to build the 4,000 kilometres 'Power ofSiberia' pipeline. The deal is the cornerstone of Russia's pivottowards Asia. Other elements include the East Siberia PacificOil Pipeline, the liberalisation of liquefied natural gas (LNG)exports and the planned second pipeline to China via the AltaiWestern route. However, the past year's events are frustratingMoscow's ambitions. Whether Russia succeeds or not bearsimplications for the global gas industry.

Advertisers fight to measure TV’s declineAs consumers migrate online in increasing numbers, advertisers demand hard numbers on audiences

Ad executives cautious about growth, gear up for contract battleThe reluctance of big companies to spend at a time oflackluster global growth and fewer major sporting eventsthis year are dampening demand for advertising, said thechief executives of two leading ad agencies.

INSURANCE SECTOR Merger mania has sweptacross huge swaths of the corporate landscape in thelast five years. Now the insurance industry, spurred bya $28.3 billion deal, could be about to join that wave.Ace Ltd.’s agreement to buy Chubb, one of the best-known names in the property insurance business,brought talk that more consolidation is in store for thesector. It is being led by Ace’s chief executive, Evan G.Greenberg, scion of a famous insurance family — oneknown for growing through serial deal-making.Wednesday’s transaction was one of the biggest yetannounced this year, a time that has already proved tobe extraordinarily fruitful for mergers in general. It willgive Ace valuable operations from Chubb, perhaps bestknown for insurance covering expensive homes,jewelry and fine art. Together, the two will have netwritten premiums worth over $30 billion and more than31,000 employees around the world. “Thecombination of the two will create greater growth andgreater earning power,” Mr. Greenberg said in aninterview. “I see greater opportunity for the two on aglobal basis, including in the U.S.” Over all, analystssay, the property and casualty insurance market hasbeen primed for consolidation for some time. Lowinterest rates have made it more difficult for thesecompanies to reap satisfactory returns from theircapital. An unusually benign period for naturaldisasters in the last two and a half years, particularlygiven a lack of serious hurricanes making landfall inthe United States, have swelled their coffers withmoney that hasn’t been paid out to fulfill claims.

Aetna buys Humana for $37B amid record number of healthcare dealsHealthcare-insurance firm Aetna announced a $37 billion agreement Friday to acquire smaller rival Humana in a deal that continues the rapid consolidation in the U.S. healthcare industry.

Global supply glut will keep oil price subdued

As More Tech Start‐Ups Stay Private, So Does the MoneyFledgling companies are increasingly delaying initial public offerings of stock, which can keep the risks - and rewards - limited to venture capitalists and hedge funds.

The PunchLine...

17

July 7, 2015

Real Estate and Construction Outlook

Spending on US private construction increased by 0.9 percent to an annual rate of $752.4billion, as spending on residential construction edged up 0.3 to a rate of $359.5 billion andspending on non-residential construction jumped 1.5 percent to a rate of $392.8 billion.The report also said spending on public construction climbed 0.7 percent to an annual rateof $283.4 billion. Spending on state and local construction inched up 0.2 percent to a rateof $260.1 billion, while spending on federal construction surged up 6.3 percent to a rate of$23.3 billion. The Commerce Department noted that total construction spending in Maywas up by 8.2 percent compared to the same month a year ago.With the bigger than expected increase, construction spending rose to its highestannual rate since reaching $1.051 trillion in October of 2008.

Hotels: On Pace for Record Occupancy in 2015, RevPAR up almost 50% from 2009

The PunchLine...

18

July 7, 2015

Will Life Ever Be the Same?

This publication is provided to you for information purposes and is not intended as an offer or solicitation for the purchase or sale of any financialinstrument. The information contained herein has been obtained from sources believed to be reliable but is not necessarily complete and itsaccuracy cannot by guaranteed. The views reflected herein are subject to change without notice. No one connected to this publication accepts anyliability whatsoever for any direct or consequential loss arising from any use of this publication or its contents. This publication may not bereproduced, distributed to any person for any purpose without express permission from TPL Advisory, LLC. Please cite source when quoting. Allrights are reserved.