transfer balance cap - ato.gov.au · transfer balance cap exceeded” will be $0.3 million. 17...

TRANSCRIPT

Transfer balance cap

Helping clients who have exceeded their cap

April 2018

Introduction

2

This webinar aims to help you, as tax and super professionals, to:

• understand what transfer balance cap information your clients can see

online:

• that will help them avoid exceeding their transfer balance cap in the

future, or

• what has led them to exceed their cap

• understand the Excess Transfer Balance (ETB) Determination and ETB

Tax Assessment processes and give you some practical insights to take

into consideration when supporting a client issued with one of these

• prepare impacted clients for the changes to Tax Time 18.

Individuals view online - myGov

3

An individual can log on through myGov to:

• view all the events that have been taken into consideration when calculating

the balance of their transfer balance account

• identify if they have exceeded their transfer balance cap

• identify which fund to contact if they disagree with any of the transactions

• download their transfer balance account information and print or email to

their advisor or agent.

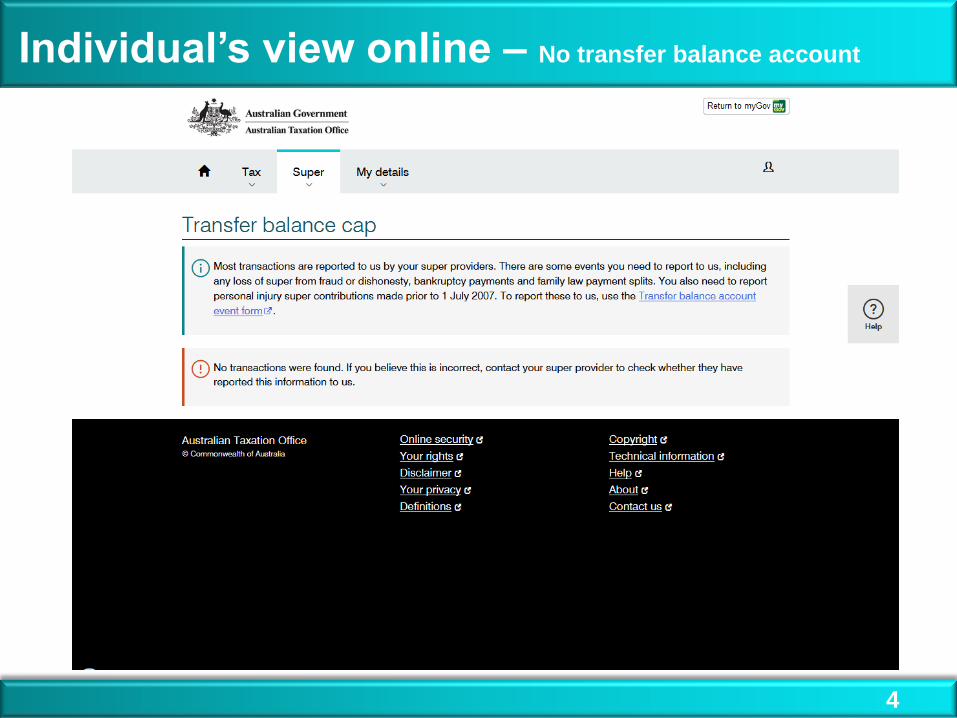

Individual’s view online – No transfer balance account

4

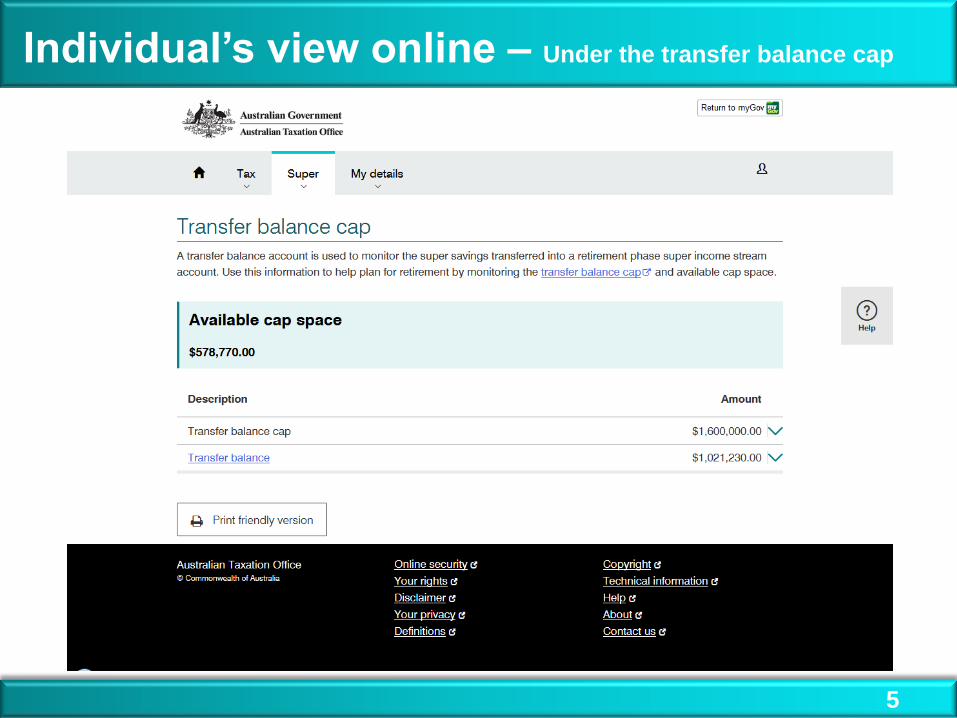

Individual’s view online – Under the transfer balance cap

5

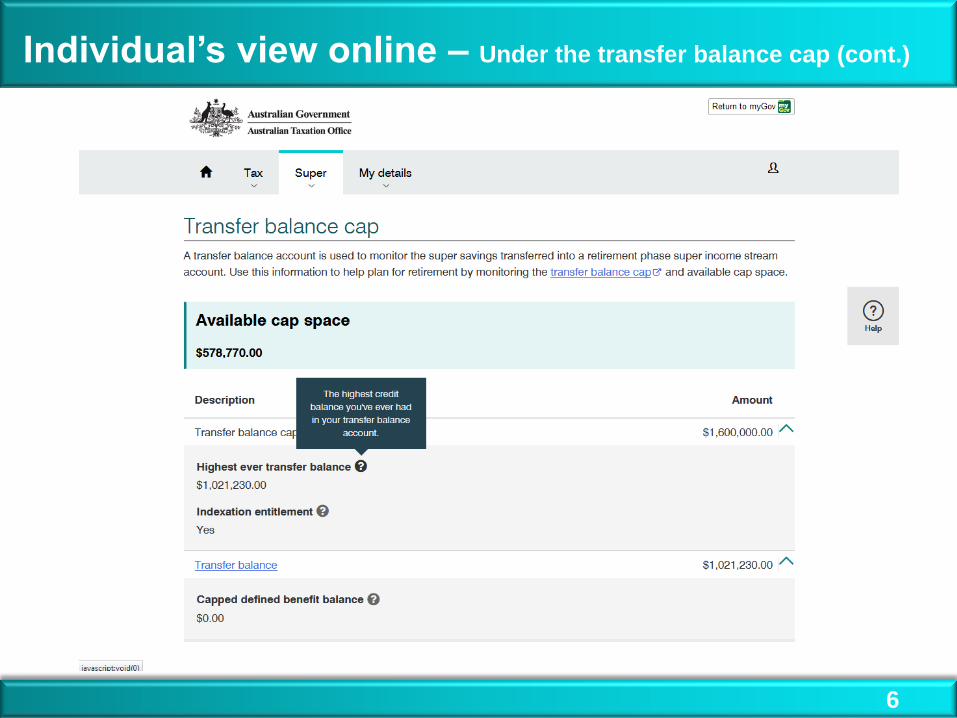

Individual’s view online – Under the transfer balance cap (cont.)

6

Individual’s view online – Transactions listing

7

Download

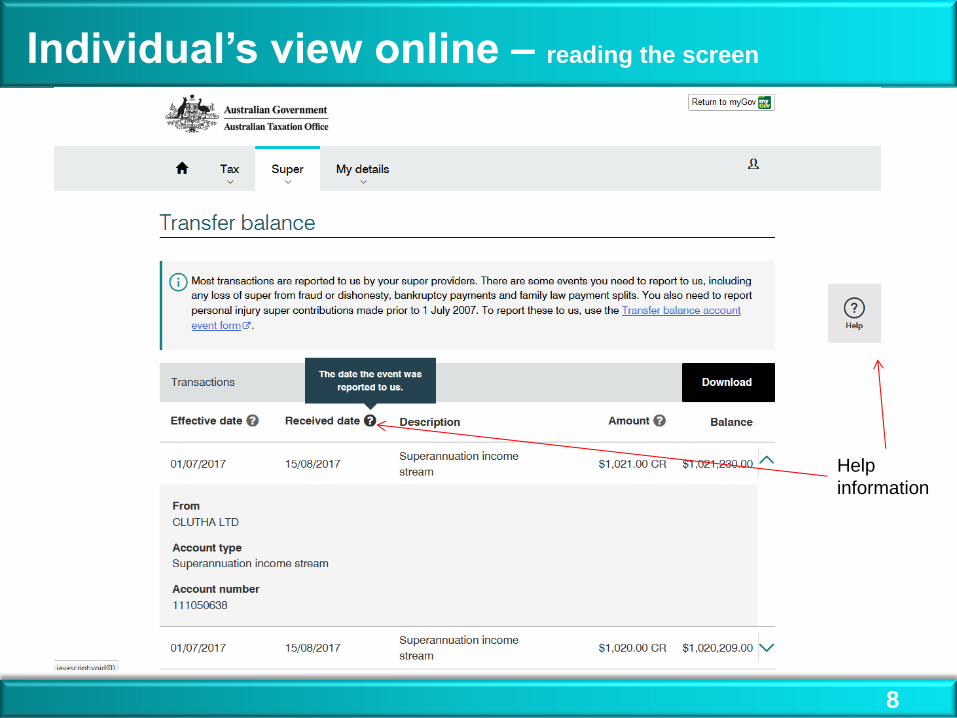

Individual’s view online – reading the screen

8

Help

information

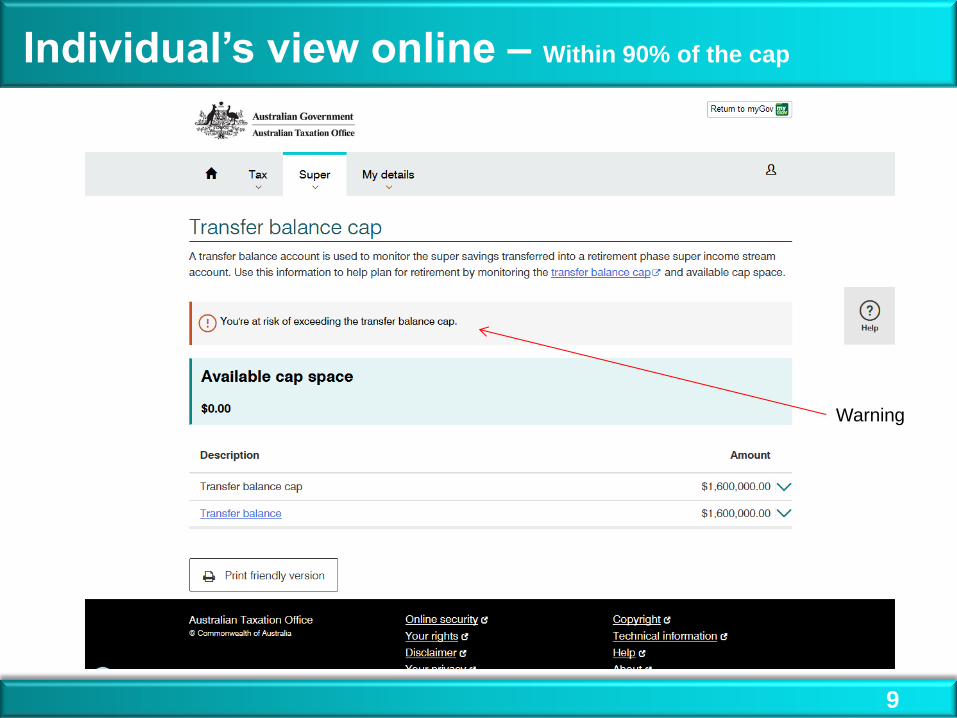

Individual’s view online – Within 90% of the cap

9

Warning

Individual’s view online – ETB Determination

10

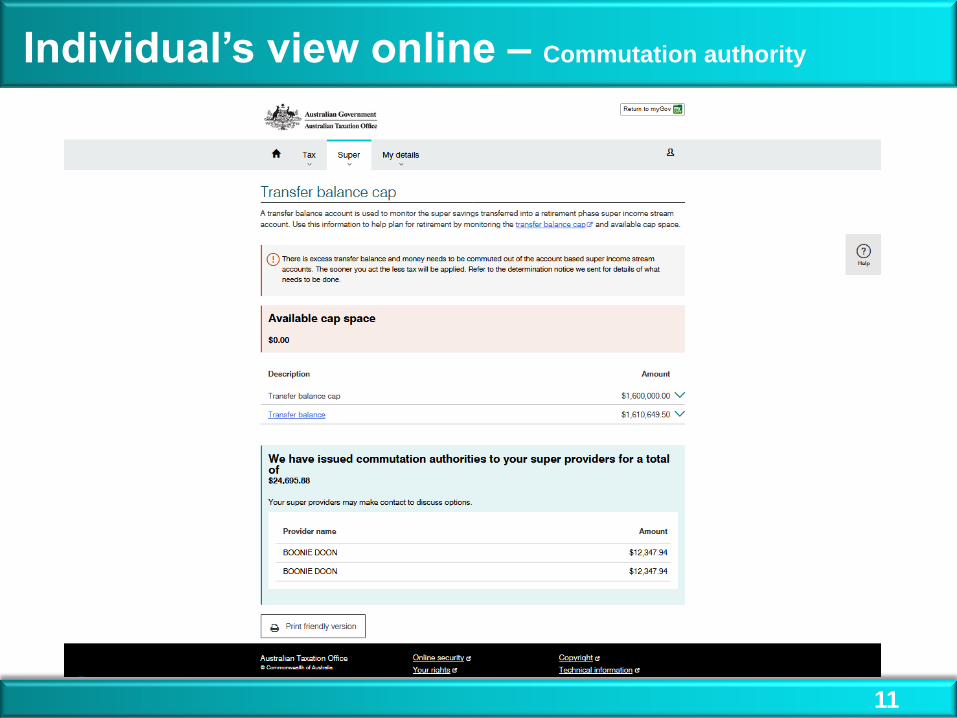

Individual’s view online – Commutation authority

11

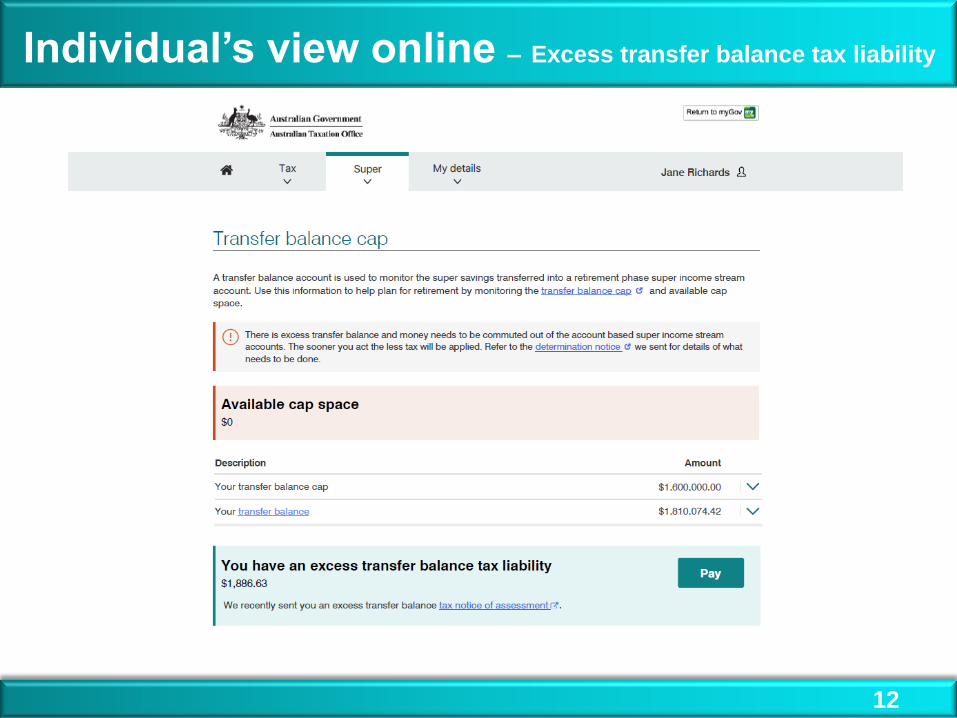

Individual’s view online – Excess transfer balance tax liability

12

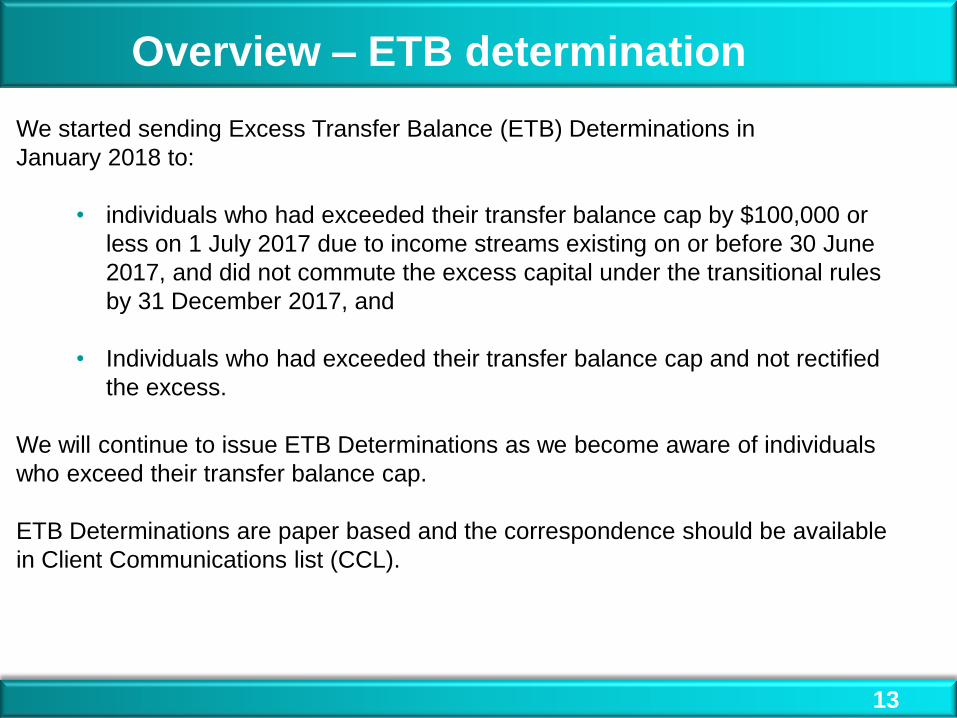

Overview – ETB determination

13

We started sending Excess Transfer Balance (ETB) Determinations in

January 2018 to:

• individuals who had exceeded their transfer balance cap by $100,000 or

less on 1 July 2017 due to income streams existing on or before 30 June

2017, and did not commute the excess capital under the transitional rules

by 31 December 2017, and

• Individuals who had exceeded their transfer balance cap and not rectified

the excess.

We will continue to issue ETB Determinations as we become aware of individuals

who exceed their transfer balance cap.

ETB Determinations are paper based and the correspondence should be available

in Client Communications list (CCL).

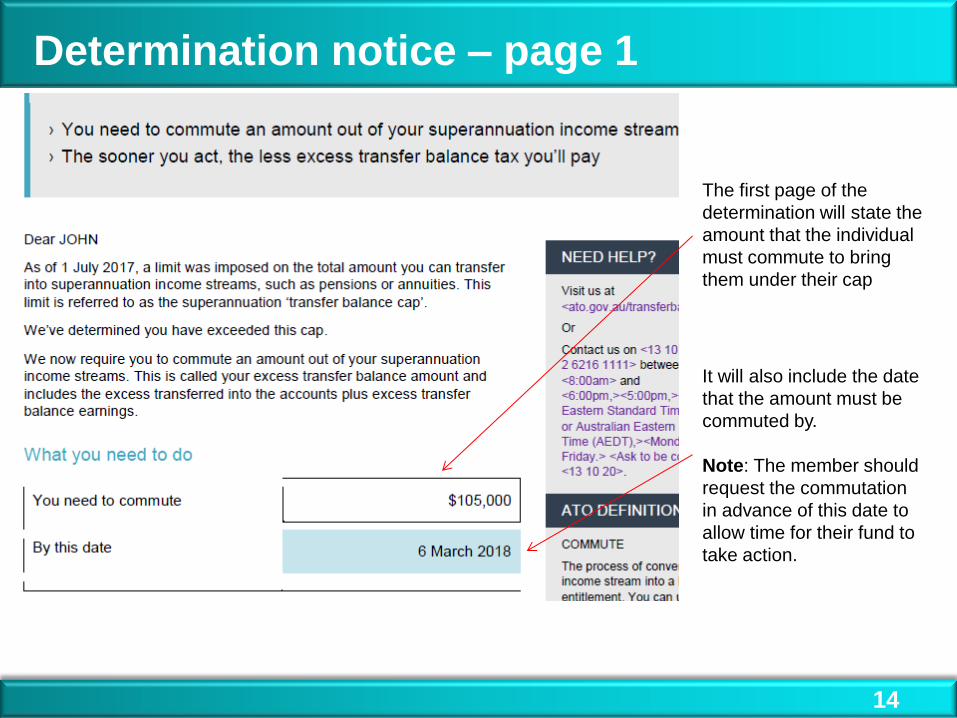

Determination notice – page 1

14

The first page of the

determination will state the

amount that the individual

must commute to bring

them under their cap

It will also include the date

that the amount must be

commuted by.

Note: The member should

request the commutation

in advance of this date to

allow time for their fund to

take action.

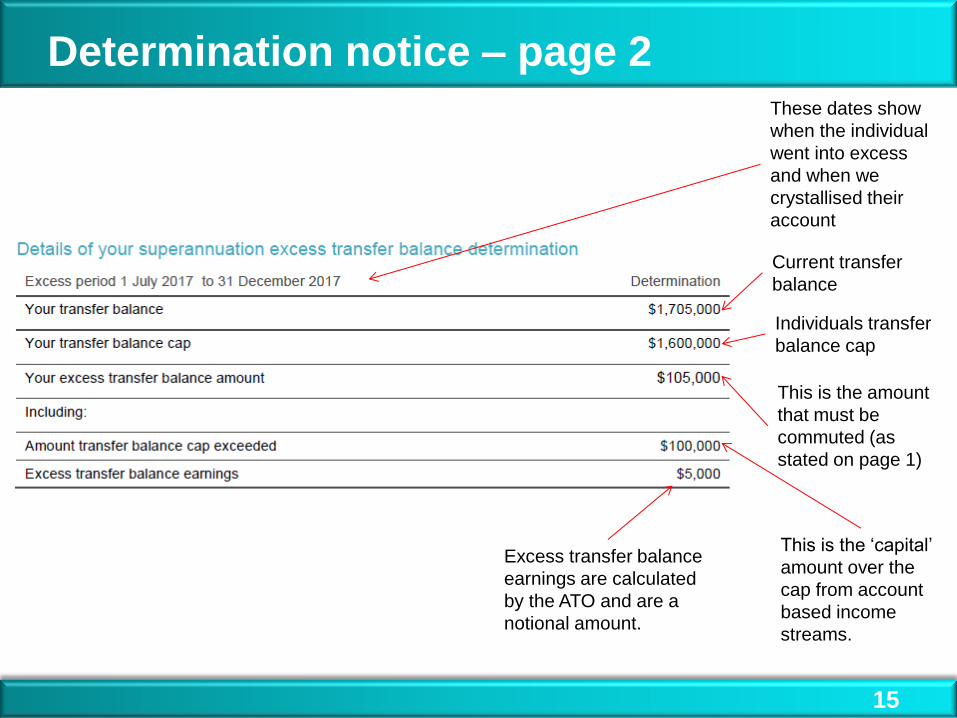

Determination notice – page 2

15

These dates show

when the individual

went into excess

and when we

crystallised their

account

Current transfer

balance

Individuals transfer

balance cap

This is the amount

that must be

commuted (as

stated on page 1)

This is the ‘capital’

amount over the

cap from account

based income

streams.

Excess transfer balance

earnings are calculated

by the ATO and are a

notional amount.

16

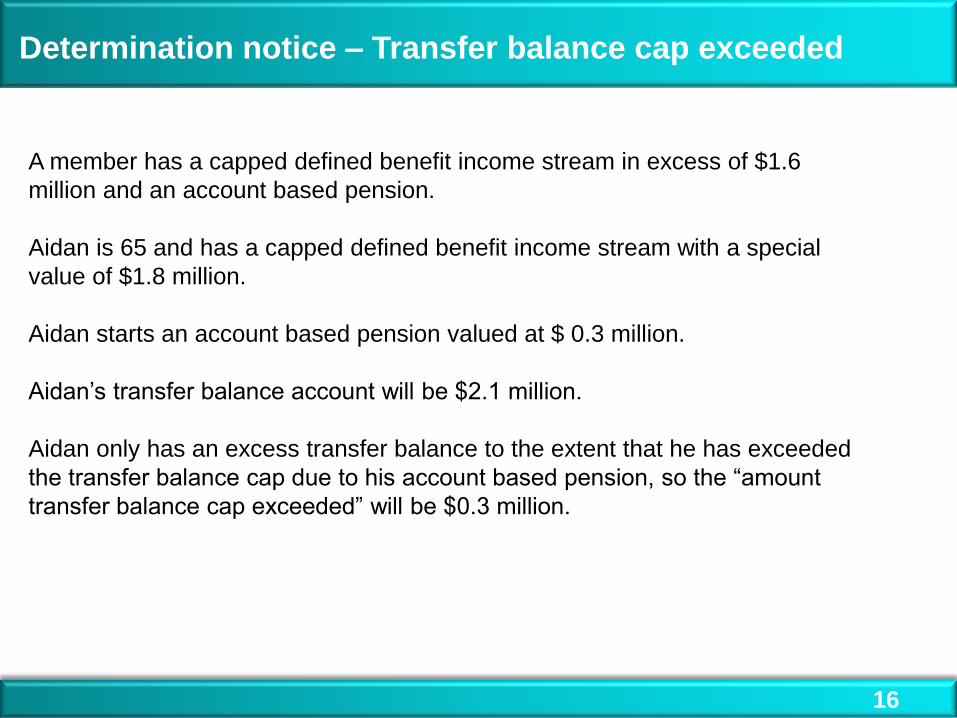

Determination notice – Transfer balance cap exceeded

A member has a capped defined benefit income stream in excess of $1.6

million and an account based pension.

Aidan is 65 and has a capped defined benefit income stream with a special

value of $1.8 million.

Aidan starts an account based pension valued at $ 0.3 million.

Aidan’s transfer balance account will be $2.1 million.

Aidan only has an excess transfer balance to the extent that he has exceeded

the transfer balance cap due to his account based pension, so the “amount

transfer balance cap exceeded” will be $0.3 million.

17

Default Commutation Notice Overview

The default commutation notice sets out who the ATO will send a commutation

authority to, if the individual does not:

• commute the required amount by the due date, or

• make an election by the due date asking us to send a commutation

authority to a different fund (or funds) to that indicated at the top of the

commutation notice.

18

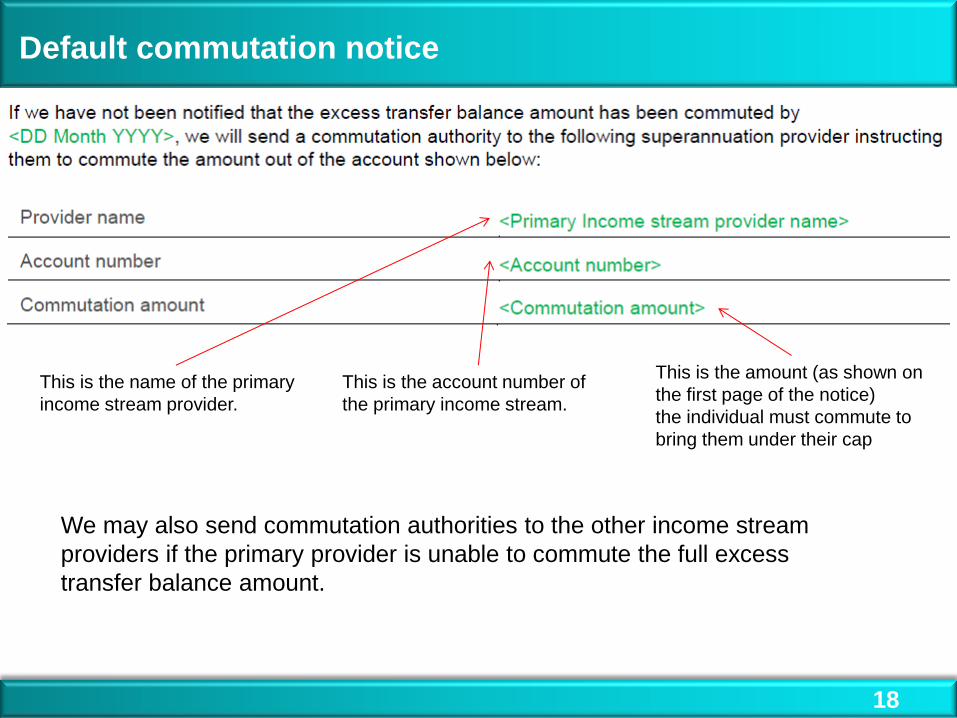

Default commutation notice

This is the amount (as shown on

the first page of the notice)

the individual must commute to

bring them under their cap

We may also send commutation authorities to the other income stream

providers if the primary provider is unable to commute the full excess

transfer balance amount.

This is the name of the primary

income stream provider.

This is the account number of

the primary income stream.

19

Making an excess transfer balance election

An individual can request we send a commutation authority to a fund (or funds) other

than primary income stream provider on the default commutation authority.

We encourage individuals to act for themselves and commute the amount

necessary as:

• even if they make an early election, we cannot send a commutation

authority to a fund until after the due date – so waiting for us to act will

mean they pay more tax

• they can engage with their fund to determine if they want to retain this

amount in super in accumulation phase or cash it out of the system.

20

Excess transfer balance election process

Your client should lodge an excess transfer balance election form by the due date

on the ETB determination when they:

• choose not to commute the amount stated in their excess transfer balance

determination themselves, and

• want the ATO to send a commutation authority to commute the required

amount from one or more different super providers or income streams than

the one specified at the top of their default commutation notice.

They will be able to electronically make their election via myGov soon.

Note: Once an election has been made it is irrevocable and cannot be withdrawn or

amended.

21

The first step is to check their transfer balance account details online through

myGov.

They may lodge an objection, however:

• the Commissioner has no discretion for “special circumstances”

• if the individual is contending that the information we have relied on is

wrong, we will be asking them to talk to their fund. If the information has

been reported incorrectly, it will need to be cancelled and the correct

information reported.

If an individual disagrees with their ETB Determination

22

Broadly there are two main types of reporting errors:

• an error that means the individual was never in excess

• an error that means the individual has always been in excess, and will still

be in excess (for the same period) after the reporting is fixed, just for a

different amount.

The sooner the first type of error is fixed, the sooner we will issue a revoked ETB

Determination.

The sooner the second type of error is fixed, the sooner we will issue an amended

ETB Determination to the individual.

You should be aware that even if the individual may have been in excess for a

lesser amount, it will take them longer to rectify, so they will be in excess for longer.

You should consider whether your client should calculate the earnings on the

anticipated excess and make an early commutation.

Reporting errors: client impact

We will issue a commutation authority when we have not received notification in

response to an ETB Determination that:

• your client has lodged an election form, OR

• your client has voluntarily commuted an amount to rectify the excess.

A commutation authority will detail:

• the amount the provider must commute from a specified income stream

• the issue date and the due date

• the income stream account information.

Commutation Authorities

23

All funds must action the commutation authority and report to the ATO using the

Transfer Balance Account Report (TBAR) within 60 days that:

• they have complied with the commutation authority by:

• commuting the full amount stated in the notice

• commuting as much as possible - even if it is less than the required

amount, or nil

• they have not commuted the amount for one of the following reasons:

• the income stream is a capped defined benefit income stream

• the member is deceased.

Commutation Authorities (cont.)

24

• Your client is liable to pay excess transfer balance (ETB) tax if they have

an excess transfer balance at the end of one or more days.

• If your client is liable for excess transfer balance tax, the ATO will issue

them with an excess transfer balance tax assessment.

• Excess transfer balance tax assessments will commence issuing later in

April.

• Your client’s may NOT have received an ETB Determination but may still

receive a notice of assessment. This is because they have rectified the

excess before they were assessed for a determination, BUT they are still

liable for excess transfer balance tax.

Excess Transfer Balance - Notice of Assessment

25

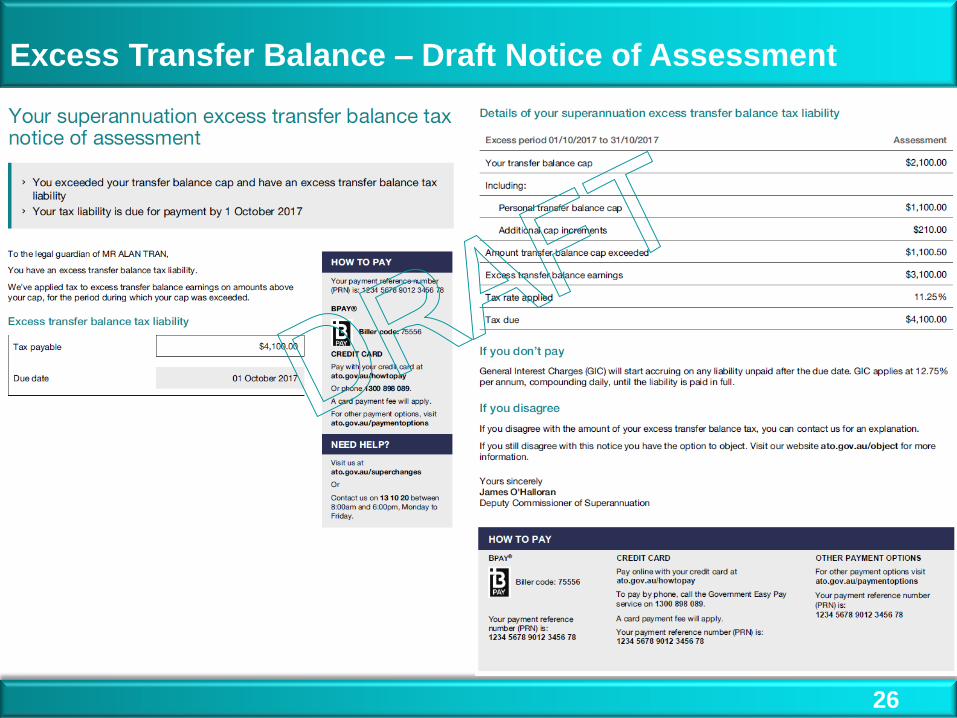

Excess Transfer Balance – Draft Notice of Assessment

26

The transfer balance cap rules apply differently to certain defined benefit

income streams, known as ‘capped defined benefit income streams’. This is

because amounts can't generally be removed from these income streams

(this removal is known as commuting).

Tax Time 18 changes - introduction

27

Capped defined benefit income streams include:

• certain lifetime pensions, regardless of when they start

• certain lifetime annuities that exist prior to 1 July 2017

• certain life expectancy pensions and annuities that exist prior to 1 July

2017

• certain market-linked pensions and annuities that exist prior to 1 July 2017.

If you have a capped defined benefit income stream, you will also have a ‘capped

defined benefit balance’, which usually reflects the credits and debits in your

transfer balance account that relate to your capped defined benefit income

stream(s).

Tax Time 18 changes – introduction (cont.)

28

• If an individual is 60 years old or over (or a death benefit dependant and

the deceased died at 60 years old or over) and their capped defined

benefit income exceeds the defined benefit income cap, they may have

additional tax liabilities.

• Individuals do not need to lodge an Income Tax Return (ITR) just because

they are in this category, but they must take this income into account when

determining if they need to lodge.

• For most people the cap is $100,000 however it may be reduced in some

circumstances.

Tax Time 18 changes – overview

29

• If you are a member of a funded defined benefit scheme (taxed scheme –

this includes taxed element and tax free component), 50% of your annual

income stream amount over your cap will be taxed at your current marginal

rate.

• If you receive an unfunded (untaxed) component of your income stream,

the 10% tax offset will not apply to untaxed-sourced benefits above the

your cap.

• Where you receive a combination of both an untaxed and taxed source

then the taxed-source income is counted first (‘stacked’) before including

your untaxed element in making these calculations.

Tax Time 18 changes – overview (cont.)

30

Frances is 62 years old and retired

In 2017-18 Frances receives $160,000 from a funded capped defined benefit

income stream. It is paid from a funded defined benefit income stream and

contains only a tax free component and a taxed element of the taxable

component.

Frances’ income exceeds the $100,000 cap by $60,000.

Frances will need to include $30,000 (50% of the excess over $100,000) in her

tax return and it will be taxed at her marginal rate.

Tax Time 18 changes – example one

31

Khoi is 68 years old and retired

In 2017-18 Khoi receives $160,000 from a capped defined benefit income

stream. It is paid partially from a taxed source and partially from an untaxed

source and includes the following components:

• $100,000 untaxed element of the taxable component

• $40,000 taxed element of the taxable component

• $20,000 tax-free component

The sum of the taxed element and the tax free component is $60,000. As this is

less than the cap Khoi does not need to include any of this income in his

assessable income.

Khoi includes the untaxed element in his assessable income as usual, but is only

eligible for a $4,000 offset.

Tax Time 18 changes – example two - stacking

32

Your clients defined benefit income cap for an income year will be reduced below

$100,000 in some circumstances, including if they:

• are receiving a capped defined benefit income stream and turn 60 years

old part-way through the year, and therefore begin receiving concessional

tax treatment for that income

• start a capped defined benefit income stream with concessional tax

treatment for the first time part-way through the year

• are in receipt of a reversionary capped defined benefit income stream,

where the individual is less than 60 and the deceased died at 60 years or

older.

Tax Time 18 changes – reduction in the cap

33

Mary is 59 years old and retired.

In 2017-18 Mary receives $150,000 from a fully funded capped defined benefit

income stream. Mary turns 60 on 12 September 2017 and receives 80% of her

benefits ($120,000) after she turns 60.

Her cap is reduced to $80,000 to reflect the period during which her benefits were

subject to concessional tax treatment (that is from when she turned 60 years old).

The income Mary receives after she turned 60 exceeds her reduced defined benefit

income cap by $40,000. She must include $20,000 in her assessable income for

2017–18 (being 50% of the excess).

The rules for the portion of the income Mary receives before she turns 60 have not

changed.

Tax Time 18 changes – reduction in cap example

34

• Your client will receive a PAYG payment summary – superannuation income

stream in relation to their capped defined benefit income stream.

• There is a new reversionary income stream death benefit indicator on the PAYG

payment summary – superannuation income stream.

• Your client will need to take this income into consideration when determining if

they need to lodge an ITR.

• There will be a new label on the income tax return for individuals to report any

income from the sum of the taxed element of the taxable component and the

tax-free component in their assessable income.

• There will be calculators and tools to help you and your client work out:

• what their defined benefit income cap is

• what income is in excess of their cap and will need to be included in their

assessable income

• what their entitlement to an offset is under the new rules.

Tax Time 18 changes – some practicalities

35

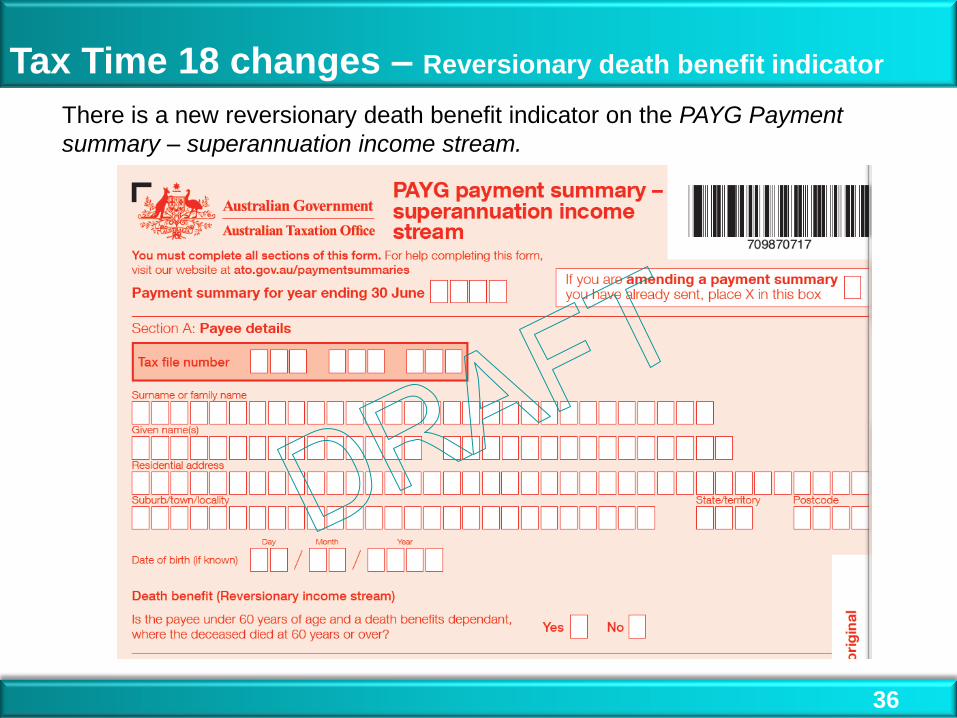

Tax Time 18 changes – Reversionary death benefit indicator

36

There is a new reversionary death benefit indicator on the PAYG Payment

summary – superannuation income stream.

Tax Time 18 changes – Label 7

37

A new item at label 7 will be created to report income from a capped defined

benefit income stream which is treated as assessable income from 1 July 2017.

More information

38

• You may wish to subscribe for ATO Super web content alerts

• Super FAQs (search: QC 51875)

• Guidance Notes for super changes (search: QC 51934).

• What you need to do when you receive a determination (search QC 54355)

• Lodging an objection (search QC 18128)

• Event Based reporting for SMSF’s (search QC 54088)

• Calculate your excess transfer balance earnings and tax (search QC54356)

• Election Form (search QC 54196)

• Transfer Balance Cap (search QC50880)

• Call 13 10 20 to request an extension of time to respond to an ETB Determination

More information

The following Law Companion Rulings have been published:

• LCR 2016/9 Superannuation reform: transfer balance cap

• LCR 2016/8: Superannuation reform: transfer balance cap and transition-to-

retirement reforms: transitional CGT relief for superannuation funds

• LCR 2016/10 Superannuation reform: defined benefit income streams – non-

commutable, lifetime pensions and lifetime annuities

• LCR 2017/1 Superannuation reform: defined benefit income streams – pensions or

annuities paid from non-commutable, life expectancy or market-linked

• LCR 2017/3 Superannuation reform: Superannuation death benefits and the transfer

balance cap

39

Thank you for your participation.

Questions & answers