transfer balance cap completing a transfer balance … · structured settlement contributions...

TRANSCRIPT

Transfer balance cap

Completing a Transfer Balance Account Report (TBAR)

December 2017

Transfer balance account report (TBAR)

The TBAR has been developed to capture the information income stream

providers need to provide to the ATO

All superannuation providers paying a superannuation income stream to an

individual will need to complete and lodge this form

There will be three lodgment channels available Bulk data exchangetransfer

via the business portal (BDE) Online lodgment (available from January 2018)

and Paper form

Any provider can use any channel however BDE is likely to best suit larger

providers

The TBAR has two purposes

1 Reporting transfer balance cap events

2 Reporting information for a memberrsquos total super balance

Transfer balance account report

2

Transfer balance account report

3

What lodgement channel are you most likely to use

A Paper form

B Online form that will be available in January

C Bulk data transfer via the business portal

D Unsure

Audience poll

What income stream providers need to report to us

4

Common events

lsquopre-existingrsquo superannuation income streams in the retirement phase

New income streams in the retirement phase on or after 1 July 2017 including

reversionary income streams

You only need to report a TRIS when it starts to be in the retirement phase

The date and value of amounts commuted from a members income stream

Less common events

Certain limited recourse borrowing arrangement repayments

Personal injury (structured settlement) contributions

Child death benefit income streams (including reversionary death benefit income

streams)

Certain information about income streams that stop being in retirement phase

Commissionerrsquos commutation authority (CCA) actions ndash including commuted in full and

unable to commute

There is some information that income stream providers will not need to report to us via the

TBAR this includes

Pension draw downs These are not debits in the transfer balance account

Investment earnings or losses

When assets supporting an income stream are exhausted

Death of a member

There is some information that income stream providers will not need to report to us

because it is the responsibility of the individual this includes

Structured settlement contributions received by the fund prior to 1 July 2007

Debits that arise as a result of fraud or bankruptcy

5

What income stream providers do not need to report to us

Transfer balance account report

6

Who are you lodging on behalf of

A Income stream providers (super funds) for example you are a fund

administrator

B Your own SMSF members

C Your clients for example you are a tax agent

D Other

Audience poll

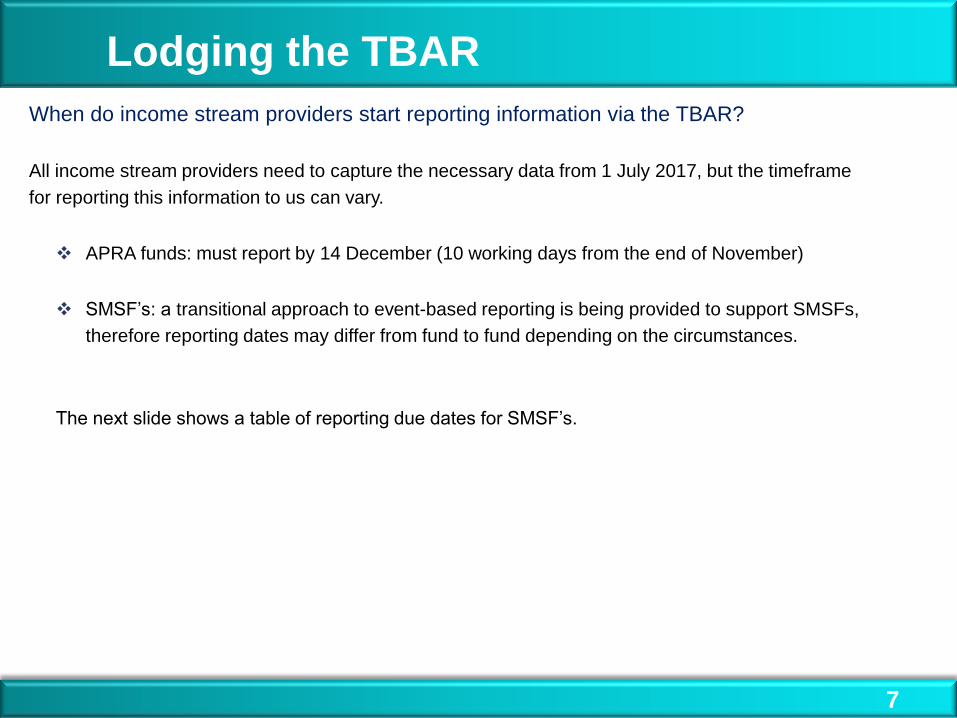

When do income stream providers start reporting information via the TBAR

All income stream providers need to capture the necessary data from 1 July 2017 but the timeframe

for reporting this information to us can vary

APRA funds must report by 14 December (10 working days from the end of November)

SMSFrsquos a transitional approach to event-based reporting is being provided to support SMSFs

therefore reporting dates may differ from fund to fund depending on the circumstances

The next slide shows a table of reporting due dates for SMSFrsquos

Lodging the TBAR

7

Frequency of reporting SMSF Transfer Balance Account reporting due date

Determined at 30 June immediately before each year the first member of the fund starts their first

retirement phase income stream in that SMSF Event type At least one member of

the fund has an income

stream just before 1 July

2017 AND

All members of the

SMSF have a total super

balance of less than

$1 million as at 30 June

2017

At least one member of

the fund has an income

stream just before 1

July 2017 AND At least

one member of a SMSF

has a total super

balance of $1 million or

more as at 30 June

2017

A member of a SMSF

starts an income stream

on or after 1 July 2017

AND as at 30 June in the

income year immediately

prior to the member

starting the income

stream all members of

the SMSF have a total

super balance of less

than $1 million

A member of a SMSF

starts an income stream

on or after 1 July 2017

AND as at 30 June in the

income year immediately

prior to the member

starting the income

stream at least one

member of the SMSF has

a total super balance $1

million or more An income stream payable to a member

just before 1 July 2017 that continues to

be paid to the member on or after 1 July

2017

On or before 1 July 2018 On or before 1 July

2018 NA NA

Any other event that is NOT

A commutation of an income stream in

response to an Excess Transfer Balance

(ETB) Determination issued to a member

of your fund by the ATO because they

have exceeded their transfer balance cap

OR

Responding to a Commutation Authority

issued to you because a member has

exceeded their transfer balance cap

No later than the due

date for lodging your

annual return

(for funds with an agent

and no outstanding

lodgements generally 15 May each year)

The later of

bull 28 October 2018 or

bull 28 days after the end

of the quarter in which

the event occurred

No later than the due

date for lodging your

annual return

(for funds with an agent

and no outstanding

lodgements generally 15 May each year)

The later of

bull 28 October 2018 or

bull 28 days after the end of

the quarter in which the

event occurred

A commutation of an income stream in

response to an ETB Determination issued

to a member of your fund by the ATO

10 business days after the end of the month in which the commutation occurs

Commutation Authority- compliance or

reasons for non-compliance Legislated due date (as stated on Authority) ie within 60 days of the date of issue of the Commutation

Authority

Lodged in error

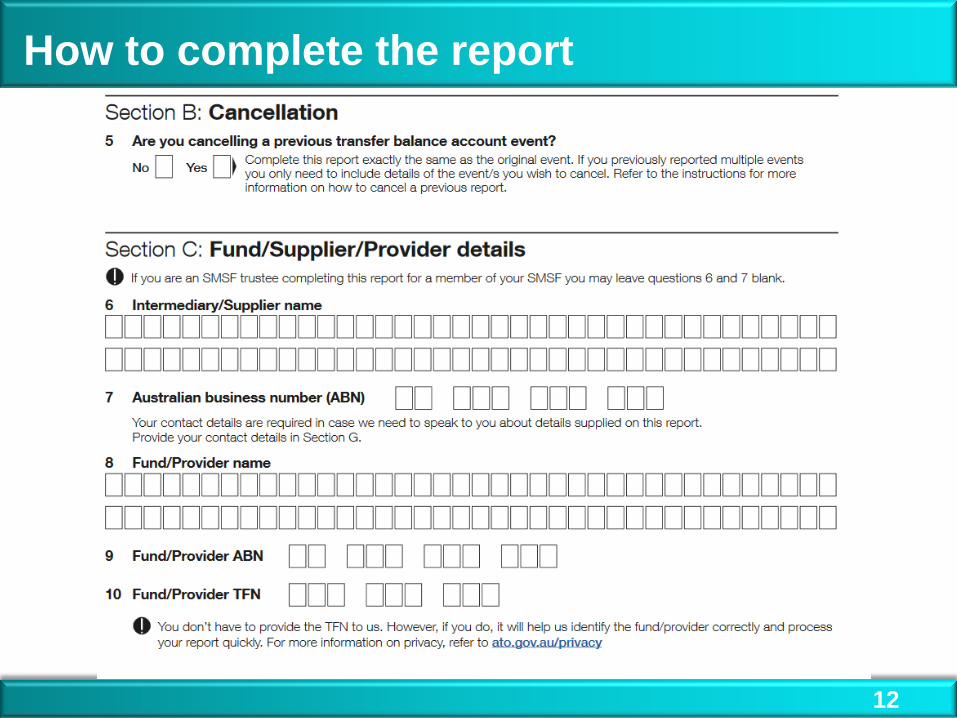

To cancel or update information already reported to us income stream providers must

cancel the original report then

lodge a new report with the correct information

Lodging the TBAR

9

TBAR instructions can be found here atogovautbar-instructions

You can reach the form and instructions on atogovau by navigating to the Administering and

reporting page under self-managed super funds Alternatively you can also use quick search or key

words TBAR QC53363 QC53364 Transfer balance account report

In most instances the TBAR allows you to report up to four events per member You must complete

separate reports for each member If you have more than four events to report for a member you

need to lodge multiple reports

If you are reporting a child death benefit income stream or child reversionary income stream you can

only report that one event on the TBAR Any other events must be reported in a separate TBAR

In the next slides we are going to give an overview of each section of the report We will then work

through some detailed examples

TBAR instructions

10

How to complete the report

11

UNCLASSIFIED SMSF professionals webinar - July 2016 update

How to complete the report

12

How to complete the report

13

UNCLASSIFIED SMSF professionals webinar - July 2016 update 14 UNCLASSIFIED SMSF professionals webinar - July 2016 update 14 UNCLASSIFIED SMSF professionals webinar - July 2016 update 14

How to complete the report

14

How to complete the report

15

How to complete the report

16

How to complete the report

17

How to complete the report

18

Examples of how to complete the report

19

We will now work through the following examples reporting

1 a pre-existing income stream (pre 1 July 2017)

2 a new income stream (post 1 July 2017) and member commutation (multiple events)

3 a pre-existing income stream (pre 1 July 2017) where an election to use the Practical Compliance

Guideline 20175 applies

4 a capped defined benefit income stream

5 a TRIS that moves into retirement phase

6 a commutation in response to a commutation authority

7 a child reversionary income stream

Example 1 ndash Pre existing income stream

20

Example 1

You are the trustee of the Snowflake super fund

Your member Bill was receiving a retirement income stream on 30 June 2017 valued at $1200000

The income stream is an account based pension

You lodge a TBAR to notify us about Billrsquos income stream You complete the TBAR as followshellip

Example 1 ndash Pre existing income stream

21

As Billrsquos income stream

existed before 1 July

2017 select this event

and go to question 13

Bill is receiving a

retirement phase

income stream that is

not a reversionary

income stream Select

super income stream

and go to event details

Example 1 ndash Pre existing income stream

22

As Billrsquos income stream

existed before 1 July

2017 the effective date

is 30 June 2017 The

value at 30 June 2017

was $120000000

Bill is receiving an

account based income

stream

At the time of the event

Billrsquos account is open he

does not have a USI or

member client identifier

and his member account

number is 1

23 2

3

Example 2 ndash New income stream and member commutation

Example 2

You are the trustee of the Tamborine super fund

Your member Sally commences a retirement income stream on 19 October 2018 valued at $600000

Sally commutes $100000 back to accumulation account on 15 February 2019

The income stream is an account based pension

Your tax agent lodges a TBAR to notify us of Sallyrsquos new income stream and member commutation Your

agent completes the TBAR as followshellip

23

24 2

4

Example 2 ndash New income stream and member commutation

24

Example 2 ndash New income stream and member commutation

25

As Sallyrsquos income

stream commenced

after 1 July 2017 select

this event and go to

question 13

Sally commenced a

retirement phase income

stream that is not a

reversionary income

stream Select super

income stream and go to

event details

Example 2 ndash New income stream and member commutation

26

Sallyrsquos income stream

commenced on 19

October 2018 The

value at 19 October

2018 was $60000000

Sally is receiving an

account based income

stream

Sallyrsquos account is

open she does not

have a USI or member

client identifier and her

member account

number is 1

Example 2 ndash New income stream and member commutation

27

Sally made a member

commutation select this

event and go to

question 14

Select member

commutation and go

to event details

Example 2 ndash New income stream and member commutation

28

On 15 February 2019

Sally commuted

$10000000

Sally commuted from

her account based

pension

Sallyrsquos account is open

she does not have a USI

or member client identifier

and her member account

number is 1

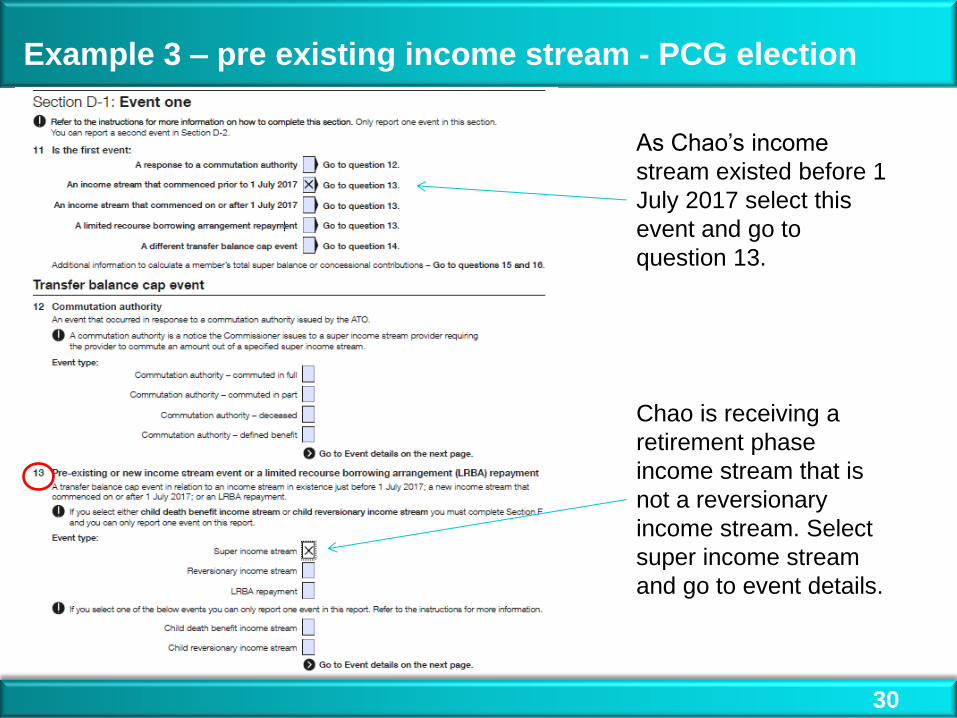

Example 3 ndash pre existing income stream - PCG election

29

Example 3

You are the trustee of the Shooting star super fund

Your member Chao has pre 1 July 2017 income stream and was uncertain of the actual value of the

income stream prior to 1 July 2017

Chao makes a request as per PCG 20175 which is subsequently accepted by you (the trustee of the

SMSF) to commute his superannuation income stream(s) by the amount that the value of the

superannuation interests that support their superannuation income streams exceeds $16 million

The income stream is an account based pension

You lodge a TBAR to notify us about Chaorsquos pre-existing income stream and value just before 1 July 2017

You complete the TBAR as followshellip

30

Example 3 ndash pre existing income stream - PCG election

As Chaorsquos income

stream existed before 1

July 2017 select this

event and go to

question 13

Chao is receiving a

retirement phase

income stream that is

not a reversionary

income stream Select

super income stream

and go to event details

30

Example 3 ndash pre existing income stream - PCG election

31

Chaorsquos income stream

existed before 1 July 2017

and therefore the effective

date is 30 June 2017 As

Chao has elected to use

the PCG the value of the

income stream is

$16million

Chao is receiving an

account based income

stream

Chaorsquos account is open he

has a USI but not a member

client identifier Chaorsquos

account number is 2

Example 4 ndash Capped defined benefit income stream

32

Example 4

You are the trustee of the Flake super fund

Your member Shannon has pre 1 July 2017 income stream

The income stream is a market linked pension and therefore a capped defined benefit income stream

You lodge a TBAR to notify us about Shannonrsquos pre-existing income stream

You complete the TBAR as followshellip

Example 4 ndash Capped defined benefit income stream

33

As Shannonrsquos income

stream existed before 1

July 2017 select this

event and go to

question 13

Shannon is receiving a

retirement phase

income stream that is

not a reversionary

income stream Select

super income stream

and go to event details

Example 4 ndash Market linked CDBI

34

Shannonrsquos income stream

existed before 1 July 2017

Therefore the effective date

is 30 June 2017 Shannonrsquos

capped defined benefit

income stream lsquospecial

valuersquo on 30 June 2017 is

$2160000

Shannon is receiving a

market linked capped

defined benefit income

stream

Shannonrsquos account is open

she does not have a USI or

member client identifier

Shannonrsquos account number

is 532

Example 5 ndash TRIS moves to retirement phase

35

Example 5

You are the trustee of the Octopus super fund

Your member Keith has been receiving a transition to retirement income stream (TRIS)

On 24 October 2019 Keith turns 65 years old and his TRIS moves into retirement phase

You lodge a TBAR to the ATO to notify them about Keiths new retirement income stream

You complete the TBAR as followshellip

Example 5 ndash TRIS moves to retirement phase

36

Keithrsquos TRIS moves to

retirement phase on his

65th birthday 24

October 2019 select

this event and go to

question 13

Keith is receiving a

retirement phase

income stream that is

not a reversionary

income stream Select

super income stream

and go to event details

Example 5 ndash TRIS moves to retirement phase

37

Keiths income stream

moved to retirement phase

on 24 October 2019 and is

valued at $1150000

Keith is receiving an

account based income

stream

Keithrsquos account is open he

does not have a USI or

member client identifier

Keithrsquos account number is 3

Example 6 ndash Response to a commutation authority

38

Example 6

You are the trustee of the Circus super fund

Your member Alex has exceeded their transfer balance cap and did not respond to their determination

within the required timeframe

As the trustee you have received a Commissioners commutation authority from the ATO The

commutation authority requires you to commute $125000

You commute the amount stated in the commutation within 60 days

You lodge a TBAR within 60 days of the notice to notify us of your compliance with the commutation

authority You complete the TBAR as followshellip

Example 6 ndash Response to a commutation authority

39

You are responding to a

commutation authority

select this event and go

to question 12

You commute the full

amount stated in the

commutation authority

You also ensure the

minimum pension

payment requirements

have been met before

commuting

Example 6 ndash Response to a commutation authority

40

You commuted $125000

from Alexs income stream

on 6 July 2018

Alex chose to keep the

lump sum in an

accumulation account

Alex is receiving an

account based income

stream

Alexrsquos account is open he

does not have a USI or

member client identifier and

the account number is 1

Example 7 ndash Reporting a child reversionary income stream

41

Example 7

You are the trustee of the Capital super fund

Your member Amy started to receive a child reversionary income stream on 15 June 2018

You lodge a TBAR to notify us of Amyrsquos child reversionary income stream

You complete the TBAR as followshellip

Example 7 ndash Reporting a child reversionary income stream

42

You are reporting an

income stream that

commenced after 1 July

2017 therefore select this

event and go to question

13

You are reporting a child

reversionary income

stream select this and go

to event details Note that

your cannot report any

further events in the

report

Example 7 ndash Reporting a child reversionary income stream

43

Amyrsquos child reversionary

income stream

commenced on 15 June

2018 and was valued at

$980000

Amyrsquos income stream is an

account based pension

Amyrsquos account is open and

she does not have a USI or

member client identifier and

her account number is 1

More information

There are a number of resources available to help a fund understand their options

ATO Web Content for APRA funds (search QC 50730)

ATO Web content for SMSFs (search QC 50731)

You may wish to subscribe for ATO Super web content alerts

Super FAQs (search QC 51875)

Guidance Notes for super changes (search QC 51934)

44

More information

The following Law Companion Guides have been published

LCG 20169 Superannuation reform transfer balance cap

LCG 20168 Superannuation reform transfer balance cap and transition-to-retirement

reforms transitional CGT relief for superannuation funds

LCG 201610 Superannuation reform defined benefit income streams ndash non-commutable

lifetime pensions and lifetime annuities

LCG 20171 Superannuation reform defined benefit income streams ndash pensions or

annuities paid from non-commutable life expectancy or market-linked

LCG 20173 Superannuation reform Superannuation death benefits and the transfer

balance cap

Practical Compliance Guideline 20175 Superannuation reform commutation requests

made before 1 July 2017 to avoid exceeding the $16 million transfer balance cap

45

Thank you for your participation

Questions amp answers

Transfer balance account report (TBAR)

The TBAR has been developed to capture the information income stream

providers need to provide to the ATO

All superannuation providers paying a superannuation income stream to an

individual will need to complete and lodge this form

There will be three lodgment channels available Bulk data exchangetransfer

via the business portal (BDE) Online lodgment (available from January 2018)

and Paper form

Any provider can use any channel however BDE is likely to best suit larger

providers

The TBAR has two purposes

1 Reporting transfer balance cap events

2 Reporting information for a memberrsquos total super balance

Transfer balance account report

2

Transfer balance account report

3

What lodgement channel are you most likely to use

A Paper form

B Online form that will be available in January

C Bulk data transfer via the business portal

D Unsure

Audience poll

What income stream providers need to report to us

4

Common events

lsquopre-existingrsquo superannuation income streams in the retirement phase

New income streams in the retirement phase on or after 1 July 2017 including

reversionary income streams

You only need to report a TRIS when it starts to be in the retirement phase

The date and value of amounts commuted from a members income stream

Less common events

Certain limited recourse borrowing arrangement repayments

Personal injury (structured settlement) contributions

Child death benefit income streams (including reversionary death benefit income

streams)

Certain information about income streams that stop being in retirement phase

Commissionerrsquos commutation authority (CCA) actions ndash including commuted in full and

unable to commute

There is some information that income stream providers will not need to report to us via the

TBAR this includes

Pension draw downs These are not debits in the transfer balance account

Investment earnings or losses

When assets supporting an income stream are exhausted

Death of a member

There is some information that income stream providers will not need to report to us

because it is the responsibility of the individual this includes

Structured settlement contributions received by the fund prior to 1 July 2007

Debits that arise as a result of fraud or bankruptcy

5

What income stream providers do not need to report to us

Transfer balance account report

6

Who are you lodging on behalf of

A Income stream providers (super funds) for example you are a fund

administrator

B Your own SMSF members

C Your clients for example you are a tax agent

D Other

Audience poll

When do income stream providers start reporting information via the TBAR

All income stream providers need to capture the necessary data from 1 July 2017 but the timeframe

for reporting this information to us can vary

APRA funds must report by 14 December (10 working days from the end of November)

SMSFrsquos a transitional approach to event-based reporting is being provided to support SMSFs

therefore reporting dates may differ from fund to fund depending on the circumstances

The next slide shows a table of reporting due dates for SMSFrsquos

Lodging the TBAR

7

Frequency of reporting SMSF Transfer Balance Account reporting due date

Determined at 30 June immediately before each year the first member of the fund starts their first

retirement phase income stream in that SMSF Event type At least one member of

the fund has an income

stream just before 1 July

2017 AND

All members of the

SMSF have a total super

balance of less than

$1 million as at 30 June

2017

At least one member of

the fund has an income

stream just before 1

July 2017 AND At least

one member of a SMSF

has a total super

balance of $1 million or

more as at 30 June

2017

A member of a SMSF

starts an income stream

on or after 1 July 2017

AND as at 30 June in the

income year immediately

prior to the member

starting the income

stream all members of

the SMSF have a total

super balance of less

than $1 million

A member of a SMSF

starts an income stream

on or after 1 July 2017

AND as at 30 June in the

income year immediately

prior to the member

starting the income

stream at least one

member of the SMSF has

a total super balance $1

million or more An income stream payable to a member

just before 1 July 2017 that continues to

be paid to the member on or after 1 July

2017

On or before 1 July 2018 On or before 1 July

2018 NA NA

Any other event that is NOT

A commutation of an income stream in

response to an Excess Transfer Balance

(ETB) Determination issued to a member

of your fund by the ATO because they

have exceeded their transfer balance cap

OR

Responding to a Commutation Authority

issued to you because a member has

exceeded their transfer balance cap

No later than the due

date for lodging your

annual return

(for funds with an agent

and no outstanding

lodgements generally 15 May each year)

The later of

bull 28 October 2018 or

bull 28 days after the end

of the quarter in which

the event occurred

No later than the due

date for lodging your

annual return

(for funds with an agent

and no outstanding

lodgements generally 15 May each year)

The later of

bull 28 October 2018 or

bull 28 days after the end of

the quarter in which the

event occurred

A commutation of an income stream in

response to an ETB Determination issued

to a member of your fund by the ATO

10 business days after the end of the month in which the commutation occurs

Commutation Authority- compliance or

reasons for non-compliance Legislated due date (as stated on Authority) ie within 60 days of the date of issue of the Commutation

Authority

Lodged in error

To cancel or update information already reported to us income stream providers must

cancel the original report then

lodge a new report with the correct information

Lodging the TBAR

9

TBAR instructions can be found here atogovautbar-instructions

You can reach the form and instructions on atogovau by navigating to the Administering and

reporting page under self-managed super funds Alternatively you can also use quick search or key

words TBAR QC53363 QC53364 Transfer balance account report

In most instances the TBAR allows you to report up to four events per member You must complete

separate reports for each member If you have more than four events to report for a member you

need to lodge multiple reports

If you are reporting a child death benefit income stream or child reversionary income stream you can

only report that one event on the TBAR Any other events must be reported in a separate TBAR

In the next slides we are going to give an overview of each section of the report We will then work

through some detailed examples

TBAR instructions

10

How to complete the report

11

UNCLASSIFIED SMSF professionals webinar - July 2016 update

How to complete the report

12

How to complete the report

13

UNCLASSIFIED SMSF professionals webinar - July 2016 update 14 UNCLASSIFIED SMSF professionals webinar - July 2016 update 14 UNCLASSIFIED SMSF professionals webinar - July 2016 update 14

How to complete the report

14

How to complete the report

15

How to complete the report

16

How to complete the report

17

How to complete the report

18

Examples of how to complete the report

19

We will now work through the following examples reporting

1 a pre-existing income stream (pre 1 July 2017)

2 a new income stream (post 1 July 2017) and member commutation (multiple events)

3 a pre-existing income stream (pre 1 July 2017) where an election to use the Practical Compliance

Guideline 20175 applies

4 a capped defined benefit income stream

5 a TRIS that moves into retirement phase

6 a commutation in response to a commutation authority

7 a child reversionary income stream

Example 1 ndash Pre existing income stream

20

Example 1

You are the trustee of the Snowflake super fund

Your member Bill was receiving a retirement income stream on 30 June 2017 valued at $1200000

The income stream is an account based pension

You lodge a TBAR to notify us about Billrsquos income stream You complete the TBAR as followshellip

Example 1 ndash Pre existing income stream

21

As Billrsquos income stream

existed before 1 July

2017 select this event

and go to question 13

Bill is receiving a

retirement phase

income stream that is

not a reversionary

income stream Select

super income stream

and go to event details

Example 1 ndash Pre existing income stream

22

As Billrsquos income stream

existed before 1 July

2017 the effective date

is 30 June 2017 The

value at 30 June 2017

was $120000000

Bill is receiving an

account based income

stream

At the time of the event

Billrsquos account is open he

does not have a USI or

member client identifier

and his member account

number is 1

23 2

3

Example 2 ndash New income stream and member commutation

Example 2

You are the trustee of the Tamborine super fund

Your member Sally commences a retirement income stream on 19 October 2018 valued at $600000

Sally commutes $100000 back to accumulation account on 15 February 2019

The income stream is an account based pension

Your tax agent lodges a TBAR to notify us of Sallyrsquos new income stream and member commutation Your

agent completes the TBAR as followshellip

23

24 2

4

Example 2 ndash New income stream and member commutation

24

Example 2 ndash New income stream and member commutation

25

As Sallyrsquos income

stream commenced

after 1 July 2017 select

this event and go to

question 13

Sally commenced a

retirement phase income

stream that is not a

reversionary income

stream Select super

income stream and go to

event details

Example 2 ndash New income stream and member commutation

26

Sallyrsquos income stream

commenced on 19

October 2018 The

value at 19 October

2018 was $60000000

Sally is receiving an

account based income

stream

Sallyrsquos account is

open she does not

have a USI or member

client identifier and her

member account

number is 1

Example 2 ndash New income stream and member commutation

27

Sally made a member

commutation select this

event and go to

question 14

Select member

commutation and go

to event details

Example 2 ndash New income stream and member commutation

28

On 15 February 2019

Sally commuted

$10000000

Sally commuted from

her account based

pension

Sallyrsquos account is open

she does not have a USI

or member client identifier

and her member account

number is 1

Example 3 ndash pre existing income stream - PCG election

29

Example 3

You are the trustee of the Shooting star super fund

Your member Chao has pre 1 July 2017 income stream and was uncertain of the actual value of the

income stream prior to 1 July 2017

Chao makes a request as per PCG 20175 which is subsequently accepted by you (the trustee of the

SMSF) to commute his superannuation income stream(s) by the amount that the value of the

superannuation interests that support their superannuation income streams exceeds $16 million

The income stream is an account based pension

You lodge a TBAR to notify us about Chaorsquos pre-existing income stream and value just before 1 July 2017

You complete the TBAR as followshellip

30

Example 3 ndash pre existing income stream - PCG election

As Chaorsquos income

stream existed before 1

July 2017 select this

event and go to

question 13

Chao is receiving a

retirement phase

income stream that is

not a reversionary

income stream Select

super income stream

and go to event details

30

Example 3 ndash pre existing income stream - PCG election

31

Chaorsquos income stream

existed before 1 July 2017

and therefore the effective

date is 30 June 2017 As

Chao has elected to use

the PCG the value of the

income stream is

$16million

Chao is receiving an

account based income

stream

Chaorsquos account is open he

has a USI but not a member

client identifier Chaorsquos

account number is 2

Example 4 ndash Capped defined benefit income stream

32

Example 4

You are the trustee of the Flake super fund

Your member Shannon has pre 1 July 2017 income stream

The income stream is a market linked pension and therefore a capped defined benefit income stream

You lodge a TBAR to notify us about Shannonrsquos pre-existing income stream

You complete the TBAR as followshellip

Example 4 ndash Capped defined benefit income stream

33

As Shannonrsquos income

stream existed before 1

July 2017 select this

event and go to

question 13

Shannon is receiving a

retirement phase

income stream that is

not a reversionary

income stream Select

super income stream

and go to event details

Example 4 ndash Market linked CDBI

34

Shannonrsquos income stream

existed before 1 July 2017

Therefore the effective date

is 30 June 2017 Shannonrsquos

capped defined benefit

income stream lsquospecial

valuersquo on 30 June 2017 is

$2160000

Shannon is receiving a

market linked capped

defined benefit income

stream

Shannonrsquos account is open

she does not have a USI or

member client identifier

Shannonrsquos account number

is 532

Example 5 ndash TRIS moves to retirement phase

35

Example 5

You are the trustee of the Octopus super fund

Your member Keith has been receiving a transition to retirement income stream (TRIS)

On 24 October 2019 Keith turns 65 years old and his TRIS moves into retirement phase

You lodge a TBAR to the ATO to notify them about Keiths new retirement income stream

You complete the TBAR as followshellip

Example 5 ndash TRIS moves to retirement phase

36

Keithrsquos TRIS moves to

retirement phase on his

65th birthday 24

October 2019 select

this event and go to

question 13

Keith is receiving a

retirement phase

income stream that is

not a reversionary

income stream Select

super income stream

and go to event details

Example 5 ndash TRIS moves to retirement phase

37

Keiths income stream

moved to retirement phase

on 24 October 2019 and is

valued at $1150000

Keith is receiving an

account based income

stream

Keithrsquos account is open he

does not have a USI or

member client identifier

Keithrsquos account number is 3

Example 6 ndash Response to a commutation authority

38

Example 6

You are the trustee of the Circus super fund

Your member Alex has exceeded their transfer balance cap and did not respond to their determination

within the required timeframe

As the trustee you have received a Commissioners commutation authority from the ATO The

commutation authority requires you to commute $125000

You commute the amount stated in the commutation within 60 days

You lodge a TBAR within 60 days of the notice to notify us of your compliance with the commutation

authority You complete the TBAR as followshellip

Example 6 ndash Response to a commutation authority

39

You are responding to a

commutation authority

select this event and go

to question 12

You commute the full

amount stated in the

commutation authority

You also ensure the

minimum pension

payment requirements

have been met before

commuting

Example 6 ndash Response to a commutation authority

40

You commuted $125000

from Alexs income stream

on 6 July 2018

Alex chose to keep the

lump sum in an

accumulation account

Alex is receiving an

account based income

stream

Alexrsquos account is open he

does not have a USI or

member client identifier and

the account number is 1

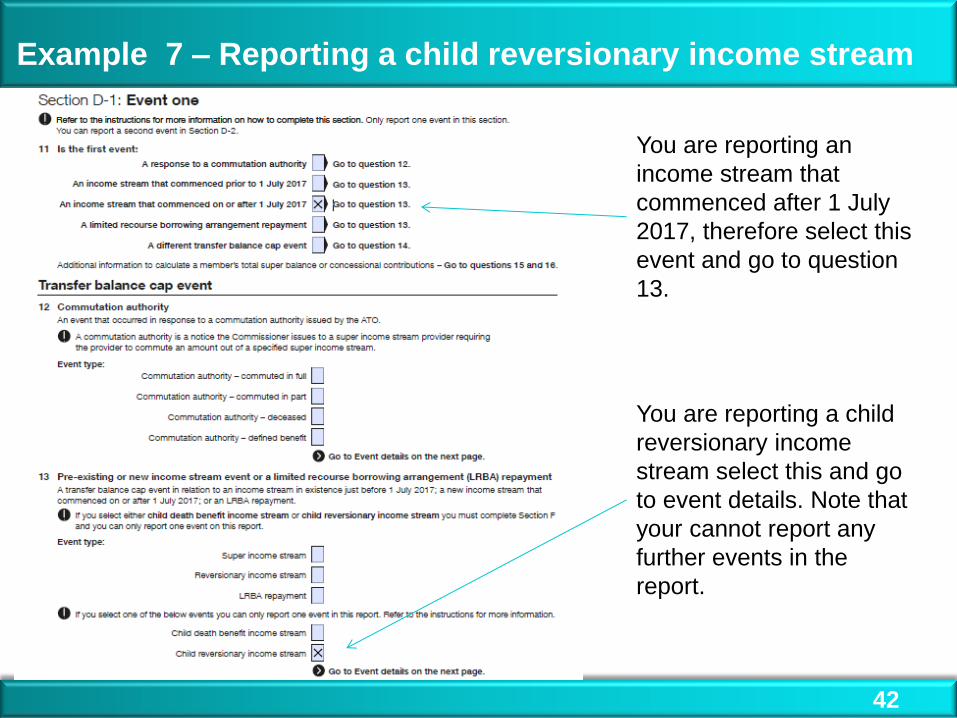

Example 7 ndash Reporting a child reversionary income stream

41

Example 7

You are the trustee of the Capital super fund

Your member Amy started to receive a child reversionary income stream on 15 June 2018

You lodge a TBAR to notify us of Amyrsquos child reversionary income stream

You complete the TBAR as followshellip

Example 7 ndash Reporting a child reversionary income stream

42

You are reporting an

income stream that

commenced after 1 July

2017 therefore select this

event and go to question

13

You are reporting a child

reversionary income

stream select this and go

to event details Note that

your cannot report any

further events in the

report

Example 7 ndash Reporting a child reversionary income stream

43

Amyrsquos child reversionary

income stream

commenced on 15 June

2018 and was valued at

$980000

Amyrsquos income stream is an

account based pension

Amyrsquos account is open and

she does not have a USI or

member client identifier and

her account number is 1

More information

There are a number of resources available to help a fund understand their options

ATO Web Content for APRA funds (search QC 50730)

ATO Web content for SMSFs (search QC 50731)

You may wish to subscribe for ATO Super web content alerts

Super FAQs (search QC 51875)

Guidance Notes for super changes (search QC 51934)

44

More information

The following Law Companion Guides have been published

LCG 20169 Superannuation reform transfer balance cap

LCG 20168 Superannuation reform transfer balance cap and transition-to-retirement

reforms transitional CGT relief for superannuation funds

LCG 201610 Superannuation reform defined benefit income streams ndash non-commutable

lifetime pensions and lifetime annuities

LCG 20171 Superannuation reform defined benefit income streams ndash pensions or

annuities paid from non-commutable life expectancy or market-linked

LCG 20173 Superannuation reform Superannuation death benefits and the transfer

balance cap

Practical Compliance Guideline 20175 Superannuation reform commutation requests

made before 1 July 2017 to avoid exceeding the $16 million transfer balance cap

45

Thank you for your participation

Questions amp answers

Transfer balance account report

3

What lodgement channel are you most likely to use

A Paper form

B Online form that will be available in January

C Bulk data transfer via the business portal

D Unsure

Audience poll

What income stream providers need to report to us

4

Common events

lsquopre-existingrsquo superannuation income streams in the retirement phase

New income streams in the retirement phase on or after 1 July 2017 including

reversionary income streams

You only need to report a TRIS when it starts to be in the retirement phase

The date and value of amounts commuted from a members income stream

Less common events

Certain limited recourse borrowing arrangement repayments

Personal injury (structured settlement) contributions

Child death benefit income streams (including reversionary death benefit income

streams)

Certain information about income streams that stop being in retirement phase

Commissionerrsquos commutation authority (CCA) actions ndash including commuted in full and

unable to commute

There is some information that income stream providers will not need to report to us via the

TBAR this includes

Pension draw downs These are not debits in the transfer balance account

Investment earnings or losses

When assets supporting an income stream are exhausted

Death of a member

There is some information that income stream providers will not need to report to us

because it is the responsibility of the individual this includes

Structured settlement contributions received by the fund prior to 1 July 2007

Debits that arise as a result of fraud or bankruptcy

5

What income stream providers do not need to report to us

Transfer balance account report

6

Who are you lodging on behalf of

A Income stream providers (super funds) for example you are a fund

administrator

B Your own SMSF members

C Your clients for example you are a tax agent

D Other

Audience poll

When do income stream providers start reporting information via the TBAR

All income stream providers need to capture the necessary data from 1 July 2017 but the timeframe

for reporting this information to us can vary

APRA funds must report by 14 December (10 working days from the end of November)

SMSFrsquos a transitional approach to event-based reporting is being provided to support SMSFs

therefore reporting dates may differ from fund to fund depending on the circumstances

The next slide shows a table of reporting due dates for SMSFrsquos

Lodging the TBAR

7

Frequency of reporting SMSF Transfer Balance Account reporting due date

Determined at 30 June immediately before each year the first member of the fund starts their first

retirement phase income stream in that SMSF Event type At least one member of

the fund has an income

stream just before 1 July

2017 AND

All members of the

SMSF have a total super

balance of less than

$1 million as at 30 June

2017

At least one member of

the fund has an income

stream just before 1

July 2017 AND At least

one member of a SMSF

has a total super

balance of $1 million or

more as at 30 June

2017

A member of a SMSF

starts an income stream

on or after 1 July 2017

AND as at 30 June in the

income year immediately

prior to the member

starting the income

stream all members of

the SMSF have a total

super balance of less

than $1 million

A member of a SMSF

starts an income stream

on or after 1 July 2017

AND as at 30 June in the

income year immediately

prior to the member

starting the income

stream at least one

member of the SMSF has

a total super balance $1

million or more An income stream payable to a member

just before 1 July 2017 that continues to

be paid to the member on or after 1 July

2017

On or before 1 July 2018 On or before 1 July

2018 NA NA

Any other event that is NOT

A commutation of an income stream in

response to an Excess Transfer Balance

(ETB) Determination issued to a member

of your fund by the ATO because they

have exceeded their transfer balance cap

OR

Responding to a Commutation Authority

issued to you because a member has

exceeded their transfer balance cap

No later than the due

date for lodging your

annual return

(for funds with an agent

and no outstanding

lodgements generally 15 May each year)

The later of

bull 28 October 2018 or

bull 28 days after the end

of the quarter in which

the event occurred

No later than the due

date for lodging your

annual return

(for funds with an agent

and no outstanding

lodgements generally 15 May each year)

The later of

bull 28 October 2018 or

bull 28 days after the end of

the quarter in which the

event occurred

A commutation of an income stream in

response to an ETB Determination issued

to a member of your fund by the ATO

10 business days after the end of the month in which the commutation occurs

Commutation Authority- compliance or

reasons for non-compliance Legislated due date (as stated on Authority) ie within 60 days of the date of issue of the Commutation

Authority

Lodged in error

To cancel or update information already reported to us income stream providers must

cancel the original report then

lodge a new report with the correct information

Lodging the TBAR

9

TBAR instructions can be found here atogovautbar-instructions

You can reach the form and instructions on atogovau by navigating to the Administering and

reporting page under self-managed super funds Alternatively you can also use quick search or key

words TBAR QC53363 QC53364 Transfer balance account report

In most instances the TBAR allows you to report up to four events per member You must complete

separate reports for each member If you have more than four events to report for a member you

need to lodge multiple reports

If you are reporting a child death benefit income stream or child reversionary income stream you can

only report that one event on the TBAR Any other events must be reported in a separate TBAR

In the next slides we are going to give an overview of each section of the report We will then work

through some detailed examples

TBAR instructions

10

How to complete the report

11

UNCLASSIFIED SMSF professionals webinar - July 2016 update

How to complete the report

12

How to complete the report

13

UNCLASSIFIED SMSF professionals webinar - July 2016 update 14 UNCLASSIFIED SMSF professionals webinar - July 2016 update 14 UNCLASSIFIED SMSF professionals webinar - July 2016 update 14

How to complete the report

14

How to complete the report

15

How to complete the report

16

How to complete the report

17

How to complete the report

18

Examples of how to complete the report

19

We will now work through the following examples reporting

1 a pre-existing income stream (pre 1 July 2017)

2 a new income stream (post 1 July 2017) and member commutation (multiple events)

3 a pre-existing income stream (pre 1 July 2017) where an election to use the Practical Compliance

Guideline 20175 applies

4 a capped defined benefit income stream

5 a TRIS that moves into retirement phase

6 a commutation in response to a commutation authority

7 a child reversionary income stream

Example 1 ndash Pre existing income stream

20

Example 1

You are the trustee of the Snowflake super fund

Your member Bill was receiving a retirement income stream on 30 June 2017 valued at $1200000

The income stream is an account based pension

You lodge a TBAR to notify us about Billrsquos income stream You complete the TBAR as followshellip

Example 1 ndash Pre existing income stream

21

As Billrsquos income stream

existed before 1 July

2017 select this event

and go to question 13

Bill is receiving a

retirement phase

income stream that is

not a reversionary

income stream Select

super income stream

and go to event details

Example 1 ndash Pre existing income stream

22

As Billrsquos income stream

existed before 1 July

2017 the effective date

is 30 June 2017 The

value at 30 June 2017

was $120000000

Bill is receiving an

account based income

stream

At the time of the event

Billrsquos account is open he

does not have a USI or

member client identifier

and his member account

number is 1

23 2

3

Example 2 ndash New income stream and member commutation

Example 2

You are the trustee of the Tamborine super fund

Your member Sally commences a retirement income stream on 19 October 2018 valued at $600000

Sally commutes $100000 back to accumulation account on 15 February 2019

The income stream is an account based pension

Your tax agent lodges a TBAR to notify us of Sallyrsquos new income stream and member commutation Your

agent completes the TBAR as followshellip

23

24 2

4

Example 2 ndash New income stream and member commutation

24

Example 2 ndash New income stream and member commutation

25

As Sallyrsquos income

stream commenced

after 1 July 2017 select

this event and go to

question 13

Sally commenced a

retirement phase income

stream that is not a

reversionary income

stream Select super

income stream and go to

event details

Example 2 ndash New income stream and member commutation

26

Sallyrsquos income stream

commenced on 19

October 2018 The

value at 19 October

2018 was $60000000

Sally is receiving an

account based income

stream

Sallyrsquos account is

open she does not

have a USI or member

client identifier and her

member account

number is 1

Example 2 ndash New income stream and member commutation

27

Sally made a member

commutation select this

event and go to

question 14

Select member

commutation and go

to event details

Example 2 ndash New income stream and member commutation

28

On 15 February 2019

Sally commuted

$10000000

Sally commuted from

her account based

pension

Sallyrsquos account is open

she does not have a USI

or member client identifier

and her member account

number is 1

Example 3 ndash pre existing income stream - PCG election

29

Example 3

You are the trustee of the Shooting star super fund

Your member Chao has pre 1 July 2017 income stream and was uncertain of the actual value of the

income stream prior to 1 July 2017

Chao makes a request as per PCG 20175 which is subsequently accepted by you (the trustee of the

SMSF) to commute his superannuation income stream(s) by the amount that the value of the

superannuation interests that support their superannuation income streams exceeds $16 million

The income stream is an account based pension

You lodge a TBAR to notify us about Chaorsquos pre-existing income stream and value just before 1 July 2017

You complete the TBAR as followshellip

30

Example 3 ndash pre existing income stream - PCG election

As Chaorsquos income

stream existed before 1

July 2017 select this

event and go to

question 13

Chao is receiving a

retirement phase

income stream that is

not a reversionary

income stream Select

super income stream

and go to event details

30

Example 3 ndash pre existing income stream - PCG election

31

Chaorsquos income stream

existed before 1 July 2017

and therefore the effective

date is 30 June 2017 As

Chao has elected to use

the PCG the value of the

income stream is

$16million

Chao is receiving an

account based income

stream

Chaorsquos account is open he

has a USI but not a member

client identifier Chaorsquos

account number is 2

Example 4 ndash Capped defined benefit income stream

32

Example 4

You are the trustee of the Flake super fund

Your member Shannon has pre 1 July 2017 income stream

The income stream is a market linked pension and therefore a capped defined benefit income stream

You lodge a TBAR to notify us about Shannonrsquos pre-existing income stream

You complete the TBAR as followshellip

Example 4 ndash Capped defined benefit income stream

33

As Shannonrsquos income

stream existed before 1

July 2017 select this

event and go to

question 13

Shannon is receiving a

retirement phase

income stream that is

not a reversionary

income stream Select

super income stream

and go to event details

Example 4 ndash Market linked CDBI

34

Shannonrsquos income stream

existed before 1 July 2017

Therefore the effective date

is 30 June 2017 Shannonrsquos

capped defined benefit

income stream lsquospecial

valuersquo on 30 June 2017 is

$2160000

Shannon is receiving a

market linked capped

defined benefit income

stream

Shannonrsquos account is open

she does not have a USI or

member client identifier

Shannonrsquos account number

is 532

Example 5 ndash TRIS moves to retirement phase

35

Example 5

You are the trustee of the Octopus super fund

Your member Keith has been receiving a transition to retirement income stream (TRIS)

On 24 October 2019 Keith turns 65 years old and his TRIS moves into retirement phase

You lodge a TBAR to the ATO to notify them about Keiths new retirement income stream

You complete the TBAR as followshellip

Example 5 ndash TRIS moves to retirement phase

36

Keithrsquos TRIS moves to

retirement phase on his

65th birthday 24

October 2019 select

this event and go to

question 13

Keith is receiving a

retirement phase

income stream that is

not a reversionary

income stream Select

super income stream

and go to event details

Example 5 ndash TRIS moves to retirement phase

37

Keiths income stream

moved to retirement phase

on 24 October 2019 and is

valued at $1150000

Keith is receiving an

account based income

stream

Keithrsquos account is open he

does not have a USI or

member client identifier

Keithrsquos account number is 3

Example 6 ndash Response to a commutation authority

38

Example 6

You are the trustee of the Circus super fund

Your member Alex has exceeded their transfer balance cap and did not respond to their determination

within the required timeframe

As the trustee you have received a Commissioners commutation authority from the ATO The

commutation authority requires you to commute $125000

You commute the amount stated in the commutation within 60 days

You lodge a TBAR within 60 days of the notice to notify us of your compliance with the commutation

authority You complete the TBAR as followshellip

Example 6 ndash Response to a commutation authority

39

You are responding to a

commutation authority

select this event and go

to question 12

You commute the full

amount stated in the

commutation authority

You also ensure the

minimum pension

payment requirements

have been met before

commuting

Example 6 ndash Response to a commutation authority

40

You commuted $125000

from Alexs income stream

on 6 July 2018

Alex chose to keep the

lump sum in an

accumulation account

Alex is receiving an

account based income

stream

Alexrsquos account is open he

does not have a USI or

member client identifier and

the account number is 1

Example 7 ndash Reporting a child reversionary income stream

41

Example 7

You are the trustee of the Capital super fund

Your member Amy started to receive a child reversionary income stream on 15 June 2018

You lodge a TBAR to notify us of Amyrsquos child reversionary income stream

You complete the TBAR as followshellip

Example 7 ndash Reporting a child reversionary income stream

42

You are reporting an

income stream that

commenced after 1 July

2017 therefore select this

event and go to question

13

You are reporting a child

reversionary income

stream select this and go

to event details Note that

your cannot report any

further events in the

report

Example 7 ndash Reporting a child reversionary income stream

43

Amyrsquos child reversionary

income stream

commenced on 15 June

2018 and was valued at

$980000

Amyrsquos income stream is an

account based pension

Amyrsquos account is open and

she does not have a USI or

member client identifier and

her account number is 1

More information

There are a number of resources available to help a fund understand their options

ATO Web Content for APRA funds (search QC 50730)

ATO Web content for SMSFs (search QC 50731)

You may wish to subscribe for ATO Super web content alerts

Super FAQs (search QC 51875)

Guidance Notes for super changes (search QC 51934)

44

More information

The following Law Companion Guides have been published

LCG 20169 Superannuation reform transfer balance cap

LCG 20168 Superannuation reform transfer balance cap and transition-to-retirement

reforms transitional CGT relief for superannuation funds

LCG 201610 Superannuation reform defined benefit income streams ndash non-commutable

lifetime pensions and lifetime annuities

LCG 20171 Superannuation reform defined benefit income streams ndash pensions or

annuities paid from non-commutable life expectancy or market-linked

LCG 20173 Superannuation reform Superannuation death benefits and the transfer

balance cap

Practical Compliance Guideline 20175 Superannuation reform commutation requests

made before 1 July 2017 to avoid exceeding the $16 million transfer balance cap

45

Thank you for your participation

Questions amp answers

What income stream providers need to report to us

4

Common events

lsquopre-existingrsquo superannuation income streams in the retirement phase

New income streams in the retirement phase on or after 1 July 2017 including

reversionary income streams

You only need to report a TRIS when it starts to be in the retirement phase

The date and value of amounts commuted from a members income stream

Less common events

Certain limited recourse borrowing arrangement repayments

Personal injury (structured settlement) contributions

Child death benefit income streams (including reversionary death benefit income

streams)

Certain information about income streams that stop being in retirement phase

Commissionerrsquos commutation authority (CCA) actions ndash including commuted in full and

unable to commute

There is some information that income stream providers will not need to report to us via the

TBAR this includes

Pension draw downs These are not debits in the transfer balance account

Investment earnings or losses

When assets supporting an income stream are exhausted

Death of a member

There is some information that income stream providers will not need to report to us

because it is the responsibility of the individual this includes

Structured settlement contributions received by the fund prior to 1 July 2007

Debits that arise as a result of fraud or bankruptcy

5

What income stream providers do not need to report to us

Transfer balance account report

6

Who are you lodging on behalf of

A Income stream providers (super funds) for example you are a fund

administrator

B Your own SMSF members

C Your clients for example you are a tax agent

D Other

Audience poll

When do income stream providers start reporting information via the TBAR

All income stream providers need to capture the necessary data from 1 July 2017 but the timeframe

for reporting this information to us can vary

APRA funds must report by 14 December (10 working days from the end of November)

SMSFrsquos a transitional approach to event-based reporting is being provided to support SMSFs

therefore reporting dates may differ from fund to fund depending on the circumstances

The next slide shows a table of reporting due dates for SMSFrsquos

Lodging the TBAR

7

Frequency of reporting SMSF Transfer Balance Account reporting due date

Determined at 30 June immediately before each year the first member of the fund starts their first

retirement phase income stream in that SMSF Event type At least one member of

the fund has an income

stream just before 1 July

2017 AND

All members of the

SMSF have a total super

balance of less than

$1 million as at 30 June

2017

At least one member of

the fund has an income

stream just before 1

July 2017 AND At least

one member of a SMSF

has a total super

balance of $1 million or

more as at 30 June

2017

A member of a SMSF

starts an income stream

on or after 1 July 2017

AND as at 30 June in the

income year immediately

prior to the member

starting the income

stream all members of

the SMSF have a total

super balance of less

than $1 million

A member of a SMSF

starts an income stream

on or after 1 July 2017

AND as at 30 June in the

income year immediately

prior to the member

starting the income

stream at least one

member of the SMSF has

a total super balance $1

million or more An income stream payable to a member

just before 1 July 2017 that continues to

be paid to the member on or after 1 July

2017

On or before 1 July 2018 On or before 1 July

2018 NA NA

Any other event that is NOT

A commutation of an income stream in

response to an Excess Transfer Balance

(ETB) Determination issued to a member

of your fund by the ATO because they

have exceeded their transfer balance cap

OR

Responding to a Commutation Authority

issued to you because a member has

exceeded their transfer balance cap

No later than the due

date for lodging your

annual return

(for funds with an agent

and no outstanding

lodgements generally 15 May each year)

The later of

bull 28 October 2018 or

bull 28 days after the end

of the quarter in which

the event occurred

No later than the due

date for lodging your

annual return

(for funds with an agent

and no outstanding

lodgements generally 15 May each year)

The later of

bull 28 October 2018 or

bull 28 days after the end of

the quarter in which the

event occurred

A commutation of an income stream in

response to an ETB Determination issued

to a member of your fund by the ATO

10 business days after the end of the month in which the commutation occurs

Commutation Authority- compliance or

reasons for non-compliance Legislated due date (as stated on Authority) ie within 60 days of the date of issue of the Commutation

Authority

Lodged in error

To cancel or update information already reported to us income stream providers must

cancel the original report then

lodge a new report with the correct information

Lodging the TBAR

9

TBAR instructions can be found here atogovautbar-instructions

You can reach the form and instructions on atogovau by navigating to the Administering and

reporting page under self-managed super funds Alternatively you can also use quick search or key

words TBAR QC53363 QC53364 Transfer balance account report

In most instances the TBAR allows you to report up to four events per member You must complete

separate reports for each member If you have more than four events to report for a member you

need to lodge multiple reports

If you are reporting a child death benefit income stream or child reversionary income stream you can

only report that one event on the TBAR Any other events must be reported in a separate TBAR

In the next slides we are going to give an overview of each section of the report We will then work

through some detailed examples

TBAR instructions

10

How to complete the report

11

UNCLASSIFIED SMSF professionals webinar - July 2016 update

How to complete the report

12

How to complete the report

13

UNCLASSIFIED SMSF professionals webinar - July 2016 update 14 UNCLASSIFIED SMSF professionals webinar - July 2016 update 14 UNCLASSIFIED SMSF professionals webinar - July 2016 update 14

How to complete the report

14

How to complete the report

15

How to complete the report

16

How to complete the report

17

How to complete the report

18

Examples of how to complete the report

19

We will now work through the following examples reporting

1 a pre-existing income stream (pre 1 July 2017)

2 a new income stream (post 1 July 2017) and member commutation (multiple events)

3 a pre-existing income stream (pre 1 July 2017) where an election to use the Practical Compliance

Guideline 20175 applies

4 a capped defined benefit income stream

5 a TRIS that moves into retirement phase

6 a commutation in response to a commutation authority

7 a child reversionary income stream

Example 1 ndash Pre existing income stream

20

Example 1

You are the trustee of the Snowflake super fund

Your member Bill was receiving a retirement income stream on 30 June 2017 valued at $1200000

The income stream is an account based pension

You lodge a TBAR to notify us about Billrsquos income stream You complete the TBAR as followshellip

Example 1 ndash Pre existing income stream

21

As Billrsquos income stream

existed before 1 July

2017 select this event

and go to question 13

Bill is receiving a

retirement phase

income stream that is

not a reversionary

income stream Select

super income stream

and go to event details

Example 1 ndash Pre existing income stream

22

As Billrsquos income stream

existed before 1 July

2017 the effective date

is 30 June 2017 The

value at 30 June 2017

was $120000000

Bill is receiving an

account based income

stream

At the time of the event

Billrsquos account is open he

does not have a USI or

member client identifier

and his member account

number is 1

23 2

3

Example 2 ndash New income stream and member commutation

Example 2

You are the trustee of the Tamborine super fund

Your member Sally commences a retirement income stream on 19 October 2018 valued at $600000

Sally commutes $100000 back to accumulation account on 15 February 2019

The income stream is an account based pension

Your tax agent lodges a TBAR to notify us of Sallyrsquos new income stream and member commutation Your

agent completes the TBAR as followshellip

23

24 2

4

Example 2 ndash New income stream and member commutation

24

Example 2 ndash New income stream and member commutation

25

As Sallyrsquos income

stream commenced

after 1 July 2017 select

this event and go to

question 13

Sally commenced a

retirement phase income

stream that is not a

reversionary income

stream Select super

income stream and go to

event details

Example 2 ndash New income stream and member commutation

26

Sallyrsquos income stream

commenced on 19

October 2018 The

value at 19 October

2018 was $60000000

Sally is receiving an

account based income

stream

Sallyrsquos account is

open she does not

have a USI or member

client identifier and her

member account

number is 1

Example 2 ndash New income stream and member commutation

27

Sally made a member

commutation select this

event and go to

question 14

Select member

commutation and go

to event details

Example 2 ndash New income stream and member commutation

28

On 15 February 2019

Sally commuted

$10000000

Sally commuted from

her account based

pension

Sallyrsquos account is open

she does not have a USI

or member client identifier

and her member account

number is 1

Example 3 ndash pre existing income stream - PCG election

29

Example 3

You are the trustee of the Shooting star super fund

Your member Chao has pre 1 July 2017 income stream and was uncertain of the actual value of the

income stream prior to 1 July 2017

Chao makes a request as per PCG 20175 which is subsequently accepted by you (the trustee of the

SMSF) to commute his superannuation income stream(s) by the amount that the value of the

superannuation interests that support their superannuation income streams exceeds $16 million

The income stream is an account based pension

You lodge a TBAR to notify us about Chaorsquos pre-existing income stream and value just before 1 July 2017

You complete the TBAR as followshellip

30

Example 3 ndash pre existing income stream - PCG election

As Chaorsquos income

stream existed before 1

July 2017 select this

event and go to

question 13

Chao is receiving a

retirement phase

income stream that is

not a reversionary

income stream Select

super income stream

and go to event details

30

Example 3 ndash pre existing income stream - PCG election

31

Chaorsquos income stream

existed before 1 July 2017

and therefore the effective

date is 30 June 2017 As

Chao has elected to use

the PCG the value of the

income stream is

$16million

Chao is receiving an

account based income

stream

Chaorsquos account is open he

has a USI but not a member

client identifier Chaorsquos

account number is 2

Example 4 ndash Capped defined benefit income stream

32

Example 4

You are the trustee of the Flake super fund

Your member Shannon has pre 1 July 2017 income stream

The income stream is a market linked pension and therefore a capped defined benefit income stream

You lodge a TBAR to notify us about Shannonrsquos pre-existing income stream

You complete the TBAR as followshellip

Example 4 ndash Capped defined benefit income stream

33

As Shannonrsquos income

stream existed before 1

July 2017 select this

event and go to

question 13

Shannon is receiving a

retirement phase

income stream that is

not a reversionary

income stream Select

super income stream

and go to event details

Example 4 ndash Market linked CDBI

34

Shannonrsquos income stream

existed before 1 July 2017

Therefore the effective date

is 30 June 2017 Shannonrsquos

capped defined benefit

income stream lsquospecial

valuersquo on 30 June 2017 is

$2160000

Shannon is receiving a

market linked capped

defined benefit income

stream

Shannonrsquos account is open

she does not have a USI or

member client identifier

Shannonrsquos account number

is 532

Example 5 ndash TRIS moves to retirement phase

35

Example 5

You are the trustee of the Octopus super fund

Your member Keith has been receiving a transition to retirement income stream (TRIS)

On 24 October 2019 Keith turns 65 years old and his TRIS moves into retirement phase

You lodge a TBAR to the ATO to notify them about Keiths new retirement income stream

You complete the TBAR as followshellip

Example 5 ndash TRIS moves to retirement phase

36

Keithrsquos TRIS moves to

retirement phase on his

65th birthday 24

October 2019 select

this event and go to

question 13

Keith is receiving a

retirement phase

income stream that is

not a reversionary

income stream Select

super income stream

and go to event details

Example 5 ndash TRIS moves to retirement phase

37

Keiths income stream

moved to retirement phase

on 24 October 2019 and is

valued at $1150000

Keith is receiving an

account based income

stream

Keithrsquos account is open he

does not have a USI or

member client identifier

Keithrsquos account number is 3

Example 6 ndash Response to a commutation authority

38

Example 6

You are the trustee of the Circus super fund

Your member Alex has exceeded their transfer balance cap and did not respond to their determination

within the required timeframe

As the trustee you have received a Commissioners commutation authority from the ATO The

commutation authority requires you to commute $125000

You commute the amount stated in the commutation within 60 days

You lodge a TBAR within 60 days of the notice to notify us of your compliance with the commutation

authority You complete the TBAR as followshellip

Example 6 ndash Response to a commutation authority

39

You are responding to a

commutation authority

select this event and go

to question 12

You commute the full

amount stated in the

commutation authority

You also ensure the

minimum pension

payment requirements

have been met before

commuting

Example 6 ndash Response to a commutation authority

40

You commuted $125000

from Alexs income stream

on 6 July 2018

Alex chose to keep the

lump sum in an

accumulation account

Alex is receiving an

account based income

stream

Alexrsquos account is open he

does not have a USI or

member client identifier and

the account number is 1

Example 7 ndash Reporting a child reversionary income stream

41

Example 7

You are the trustee of the Capital super fund

Your member Amy started to receive a child reversionary income stream on 15 June 2018

You lodge a TBAR to notify us of Amyrsquos child reversionary income stream

You complete the TBAR as followshellip

Example 7 ndash Reporting a child reversionary income stream

42

You are reporting an

income stream that

commenced after 1 July

2017 therefore select this

event and go to question

13

You are reporting a child

reversionary income

stream select this and go

to event details Note that

your cannot report any

further events in the

report

Example 7 ndash Reporting a child reversionary income stream

43

Amyrsquos child reversionary

income stream

commenced on 15 June

2018 and was valued at

$980000

Amyrsquos income stream is an

account based pension

Amyrsquos account is open and

she does not have a USI or

member client identifier and

her account number is 1

More information

There are a number of resources available to help a fund understand their options

ATO Web Content for APRA funds (search QC 50730)

ATO Web content for SMSFs (search QC 50731)

You may wish to subscribe for ATO Super web content alerts

Super FAQs (search QC 51875)

Guidance Notes for super changes (search QC 51934)

44

More information

The following Law Companion Guides have been published

LCG 20169 Superannuation reform transfer balance cap