transfer inheritance and estate tax - evident title

TRANSCRIPT

Transfer InheritanceAnd Estate Tax

New Jersey Division of TaxationPO Box 249

Trenton, New Jersey 08695-0249

(609) 943-9905 or (609) 943-4108

IT-NRInheritance Tax

Non-Resident Return(2-07)

INTRODUCTIONNEW JERSEY TRANSFER INHERITANCE TAX - ESTATE TAX

GENERALNew Jersey has had a Transfer Inheritance Tax since 1892 when a 5% tax was imposed on property transferred from a decedent

to a beneficiary. Currently, the law imposes a graduated Transfer Inheritance Tax ranging from 11% to 16% on the transfer of real andpersonal property with a value of $500.00 or more to certain beneficiaries. There is no New Jersey Estate Tax for the estates of non-resident decedents.

BENEFICIARY CLASSESThe Transfer Inheritance Tax recognizes five beneficiary classes, asfollows:Class “A” - Father, mother, grandparents, spouse/civil unionpartner (on or after 2/19/07), domestic partner (on or after 7/10/04),child or children of the decedent, adopted child or children of thedecedent, issue of any child or legally adopted child of the decedentand step-child but not step-grandchild of the decedent.Class “B” - Eliminated by statute effective July 1, 1963.Class “C” - Brother or sister of the decedent, including half brotherand half sister, wife/civil union partner (on or after 2/19/07) orwidow/surviving civil union partner (on or after 2/19/07) of a sonof the decedent, or husband/civil union partner (on or after 2/19/07)or widower/surviving civil union partner (on or after 2/19/07) of adaughter of the decedent.Class “D” - Every other transferee, distributee or beneficiary whois not included in Classes “A”, “C” or “E”.Class “E” - The State of New Jersey or any political subdivisionthereof, or any educational institution, church, hospital, orphanasylum, public library or Bible and tract society or to, for the use ofor in trust for religious, charitable, benevolent, scientific, literary oreducational purposes, including any institution instructing the blindin the use of dogs as guides, no part of the net earnings of whichinures to the benefit of any private stockholder or other individualor corporation; provided, that the exemption does not extend totransfers of property to such educational institutions andorganizations of other states, the District of Columbia, territoriesand foreign countries which do not grant an equal, and likeexemption on transfers of property for the benefit of suchinstitutions and organizations of this State.NOTES: If any beneficiary is claimed to be the mutuallyacknowledged child of the decedent, said claim should be set forthin the detailed manner prescribed under N.J.A.C. 18:26-2.6.

For the purposes of the New Jersey Transfer Inheritance Taxan adopted child is accorded the same status as a natural child and,therefore, his relations are treated in the same manner as those of anatural child. (i.e. if the decedent’s adopted son marries/enters intoa civil union, his spouse/civil union partner is “the wife/civil unionpartner of a son of the decedent” and therefore a class “C”beneficiary).

The offspring of a biological parent conceived by the artificialinsemination of that parent who is a partner in a civil union ispresumed to be the child of the non-biological partner. In theMatter of the Parentage of the Child of Kimberly Robinson, 383N.J. Super. 165; 890 A.2d 1036 (Ch. Div. 2005) (Non-biologicalparent of New York registered domestic partnership recognized inNew Jersey, presumed to be the biological parent of childconceived by the other partner through artificial inseminationwhere the non-biological partner has "show[n] indicia ofcommitment to be a spouse and to be a parent to the child.").

A devise of real property to a husband and wife or civil unioncouple as “tenants by the entirety” provides each with a vested lifeestate, the remainder being contingent. See N.J.A.C. 18:26-8.12.

The issue of stepchildren ARE Class “D” (NOT Class “A”)beneficiaries.

The following ARE Class “D” (NOT Class “C”) beneficiaries:stepbrother or stepsister of the decedent, husband/wife/civil unionpartner/domestic partner or widow/widower/surviving civil unionpartner/surviving domestic partner of a step-child or mutuallyacknowledged child of the decedent.

The fact that a beneficiary may be considered “nonprofit” bythe Internal Revenue Service does not necessarily mean that itqualifies for exemption as a Class “E” beneficiary since the criteriaare different.

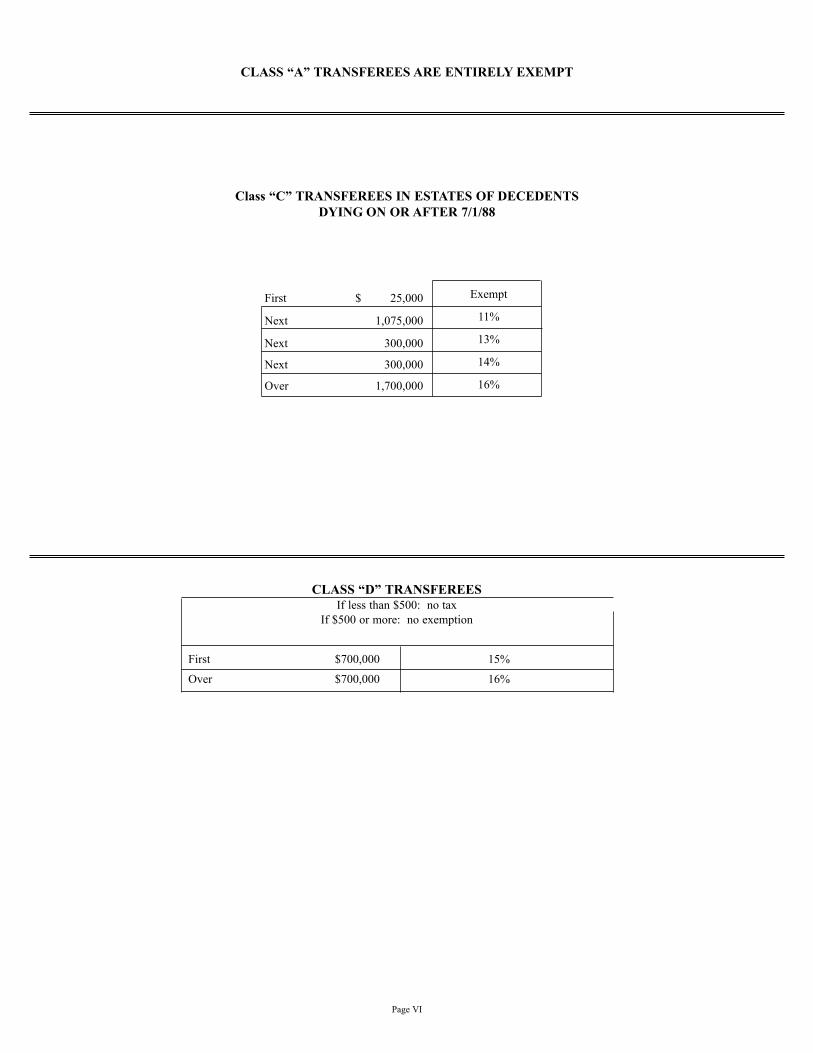

TAX RATESEach class of beneficiary has its own separate tax rate. See the

Rate Schedule on Page VI.EXEMPTIONS

1. The transfer of real property in this State held by a husbandand wife/civil union couple as “tenants by the entirety” to thesurviving spouse/civil union partner is not taxable for NewJersey Inheritance Tax purposes.

2. The transfer of intangible personal property such as stocks,bonds, corporate securities, bank deposits and mortgagesowned by a nonresident decedent is not subject to the NewJersey Inheritance Tax. However, it is used to compute theNew Jersey resident tax on the appropriate worksheet.

3. Any sum recovered under the New Jersey Death Act ascompensation for wrongful death of a decedent is not subjectto the New Jersey Inheritance Tax except as provided below:a. Any sum recovered under the New Jersey Death Act

representing damages sustained by a decedent between thedate of injury and date of death, such as the expenses ofcare, nursing, medical attendance, hospital and othercharges incident to the injury, including loss of earningsand pain and suffering are to be included in the decedent’sestate.

b. Where an action is instituted under the New Jersey DeathAct and terminates through the settlement by a compromisepayment without designating the amount to be paid undereach count, the amount which must be included in theinheritance tax return is an amount, to the extent recovered,which is equal to specific expenses related to the injury.These expenses are similar to those mentioned in section a.above and include funeral expenses, hospitalization andmedical expenses, and other expenses incident to the injury.Any amount which is recovered in excess of these expensesis considered to be exempt from the tax.

4. The proceeds of any contract of insurance insuring the life ofa resident or nonresident decedent paid or payable, by reasonof the death of such decedent, to one or more namedbeneficiaries other than the estate, executor or administrator ofsuch decedent are exempt for New Jersey Inheritance Taxpurposes.

Page I

5. The transfer of property to a beneficiary or beneficiaries of atrust created during the lifetime of a resident or nonresidentdecedent, to the extent such property results from the proceedsof any contract of insurance, insuring the life of such decedentand paid or payable to a trustee or trustees of such by reasonof the death of such decedent, is exempt from the New JerseyInheritance Tax irrespective of whether such beneficiary orbeneficiaries have a present, future, vested, contingent ordefeasible interest in such trust.

6. The transfer of life insurance proceeds insuring the life of aresident or nonresident decedent, paid or payable by reason of the death of such decedent to a trustee or trustees of a trustcreated by such decedent during his lifetime for the benefit ofone or more beneficiaries irrespective of whether suchbeneficiaries have a present, future, vested, contingent ordefeasible interest in such trust, is exempt from the New JerseyInheritance Tax.

7. The transfer, relinquishment, surrender or exercise at any timeor times by a resident or nonresident of this State, of any rightto nominate or change the beneficiary or beneficiaries of anycontract of insurance insuring the life of such resident ornonresident, regardless of when such transfer, relinquishment,surrender or exercise of such right occurred, is exempt fromthe tax.

8. Any amount recovered (under the Federal Liability for Injuriesto Employees Act) for injuries to a decedent by the personalrepresentative for the benefit of the classes of beneficiariesdesignated in that Statute, whether for the pecuniary losssustained by such beneficiaries as a result of the wrongfuldeath of the decedent or for the loss and suffering by thedecedent while he lived, or both is not subject to theInheritance Tax.Any amount recovered by the legal representatives of anydecedent by reason of any war risk insurance certificate orpolicy, either term or converted, or any adjusted servicecertificate issued by the United States, whether receiveddirectly from the United States or through any interveningestate or estates, is exempt from the New Jersey InheritanceTax.This exemption does not entitle any person to a refund of anytax heretofore paid on the transfer of property of the natureaforementioned; and does not extend to that part of the estateof any decedent composed of property, when such propertywas received by the decedent before death.

9. The proceeds of any pension, annuity, retirement allowance,return of contributions or benefit payable by the Governmentof the United States pursuant to the Civil Service RetirementAct, Retired Serviceman’s Family Protection Plan and theSurvivor Benefit Plan to a beneficiary or beneficiaries otherthan the estate or the executor or administrator of a decedentare exempt.

10. All payments at death under the Teachers Pension and AnnuityFund, the Public Employees’ Retirement System for NewJersey, and the Police and Firemen’s Retirement System ofNew Jersey, and such other State, county and municipalsystems as may have a tax exemption clause as broad as that

of the three major State systems aforementioned, whether suchpayments either before or after retirement are made on death tothe employee’s estate or to his specifically designatedbeneficiary, are exempt from the New Jersey Inheritance Tax.The benefit payable under the supplementary annuity plan ofthe State of New Jersey is not considered a benefit of thePublic Employee’s Retirement System and is taxable whetherpaid to a designated beneficiary or to the estate.The death benefits paid by the Social Security Administrationor railroad Retirement Board to the spouse of a decedent arealso exempt. For purposes of filing a return these amountsneed not be reported nor are they to be deducted from theamount claimed as a deduction for funeral expenses.In all other cases the death benefit involved should either bereported as an asset of the estate or deducted from the amountclaimed for funeral expenses.

11. Other pensions. An exemption is provided for payments fromany pension, annuity, retirement allowance or return ofcontributions, which is a direct result of the decedent’semployment under a qualified plan as defined by section401(a), (b), and (c) or 2039(c) of the Internal Revenue Code,which is payable to a surviving spouse or domestic partner.

12. The amount payable by reason of medical expenses incurred asa result of personal injury to the decedent should be reflectedby reducing the amount claimed for medical expenses as aresult of the accident.The amount payable at the death of an income producer as aresult of injuries sustained in an accident, which are paid to theestate of the income producer, is reportable for taxation. In allother instances this amount is exempt.The amount paid at death to any person under the essentialservices benefits section is exempt from taxation.The claim for funeral expense is to be reduced by the amountpaid under the funeral expenses benefits section of the law.

WHERE TO FILEAll returns are to be filed with the Transfer Inheritance and

Estate Tax Branch at the New Jersey Division of Taxation, 50Barrack Street, PO Box 249, Trenton, New Jersey 08695-0249.

WHEN TAX RETURNS ARE DUEA Transfer Inheritance Tax Return must be filed and the tax

paid on the transfer of real and personal property within eightmonths after the death of a nonresident decedent. No tax isimposed on non-resident decedents for real and tangible personalproperty located outside of New Jersey and intangible personalproperty wherever situated. However, even though these items arenot taxed they are used in the formula for computing thenonresident tax (see the “N.J. Resident Tax” line on each taxworksheet).

The tax is a lien on all New Jersey real property for fifteenyears unless paid sooner or secured by an acceptable bond. Interestaccrues on unpaid taxes at the rate of 10% per annum.

Page II

Page III

IMPORTANT REMINDERS• If the decedent died TESTATE you must supply a legible copy of the LAST WILL AND TESTAMENT, all

CODICILS thereto and any SEPARATE WRITINGS.

• A copy of the decedent’s last full year’s FEDERAL INCOME TAX RETURN is required.

• All returns, forms and correspondence must contain the decedent’s SOCIAL SECURITY NUMBER and be signedand notarized.

• PAYMENTS ON ACCOUNT may be made to avoid the accrual of interest. (Form IT-EP is included in thisbooklet.)

• If PAYMENTS are not made by CERTIFIED CHECK the issuance of waivers may be delayed.

• All CHECKS should be made payable to N.J. INHERITANCE TAX and sent to the New Jersey Division ofTaxation, Transfer Inheritance and Estate Tax Branch, 50 Barrack Street, PO Box 249, Trenton, NJ 08695-0249.

AMENDMENTS TO AN ORIGINAL RETURNAny assets and/or liabilities not disclosed in the original return

and all supplemental data requested by the Division is to be filed inaffidavit form and attested to by the duly authorized statutoryrepresentative of the estate, next of kin, or beneficiary certifying indetail a description of the asset, real or personal and/or the liabilityand the reasons for failure to disclose same in the original returnand filed directly with the Transfer Inheritance Tax Branch.

WAIVERSA waiver is required for New Jersey real estate owned by a

decedent dying a resident of another state with the exception of real estate owned by a husband and wife/civil union couple as “tenantsby the entirety”.

A membership certificate or stock in a cooperative housingcorporation is considered intangible personal property and,therefore, is not subject to tax or waiver requirements in the estateof a nonresident decedent.

Waivers are not required for automobiles, bank accounts,stocks, household goods, personal effects, accrued wages ormortgages,but these items must be reported in the return filed.

Page IV

A FLAT TAX MAY BE PAID IN LIEU OF FILING PRESCRIBED DATA

The representatives of the estate may avoid the necessity of a full disclosure of all of the detail called for in the enclosed formsby payment of a flat rate of tax on the fair market value of the decedent’s real estate and goods, wares and merchandise located inthe State of New Jersey. If this procedure is to be followed, submit an affidavit (for which the Division has no printed form) certifyingthe following facts:

1. Name of decedent; date of death; legal domicile as of the date of death.

2. Description and fair market value of the New Jersey goods, wares and merchandise; and describe (by lot and block number,address, municipality and county) the New Jersey real estate and give the assessed and market values thereof for the year ofdecedent’s death. Explain how any fractional ownership in real estate was derived. If any liens or encumbrances wereoutstanding at decedent’s death, state the facts fully. State whether or not there was mortgage insurance and, if there was,the amount thereof.

3. State value of gross estate of decedent both in and outside of New Jersey. Certify whether decedent made any gifts ortransfers in contemplation of death, or to take effect at or after death, or created any trusts in his lifetime. Give names andrelationship to decedent of donees or transferees, and market value of gifts, transfers or trusts. If the decedent at any timeexecuted any deeds of trust or agreements of a similar nature, copies thereof must be submitted. If the decedent had aninterest in either a closely held corporation or partnership submit copies of any stock purchase, option agreement, or mutualpurchase agreement.

4. If decedent died testate, attach a legible copy of the will and give ages as of death of decedent of any life tenants orannuitants. State whether all beneficiaries survived. In those cases where decedent died intestate, state the names of theheirs-at-law and the next-of-kin and their relationship to decedent. Give parentage of heirs and next-of-kin taking deceasedparent’s share.

5. A recital to the effect that all right is waived for a refund of the payment of tax and interest found due. (However, anyoverpayment made in connection with the filing of the flat tax method will be refunded. This recital is meant to precludethe subsequent filing of the full disclosure ratio tax return for the purpose of obtaining a refund of the tax found due underthe flat tax method).

On the basis of the above data, the flat tax will usually approximate the tax payable if the detailed report were filed. Statutoryrates and exemptions are used in the flat rate computations which are illustrated in the attached worksheets.

In addition to the flat tax affidavit, IT-NR Page 1 must be completed and submitted. The numbered line items on the IT-NR Page1 are completed as follows:

1. No entries are made on Lines 1, 2, 3, 4, 6 or 7;

2. Report the gross estate both in and outside of New Jersey, on Line 5;

3. Report any contingent amount included in Line 5, on Line 8;

4. Report the balance of the estate on Line 9 (Line 5 minus Line 8);

5. Complete Lines 10 thru 19.

NOTE: The flat tax affidavit form of return should be utilized for estates where all of the taxable New Jersey property isspecifically devised, jointly owned (joint tenants with the right of survivorship), or transferred to one or moreindividuals within three (3) years of the decedent’s death, or to take effect at or after the decedent’s date of death. Inthese situations, the estate is not subject to the ratio or flat tax computations. Rather, the New Jersey property is taxeddirectly to the devisee, transferee, or surviving joint tenant at the resident rates. Accordingly, no worksheet is required.See the example on page V.

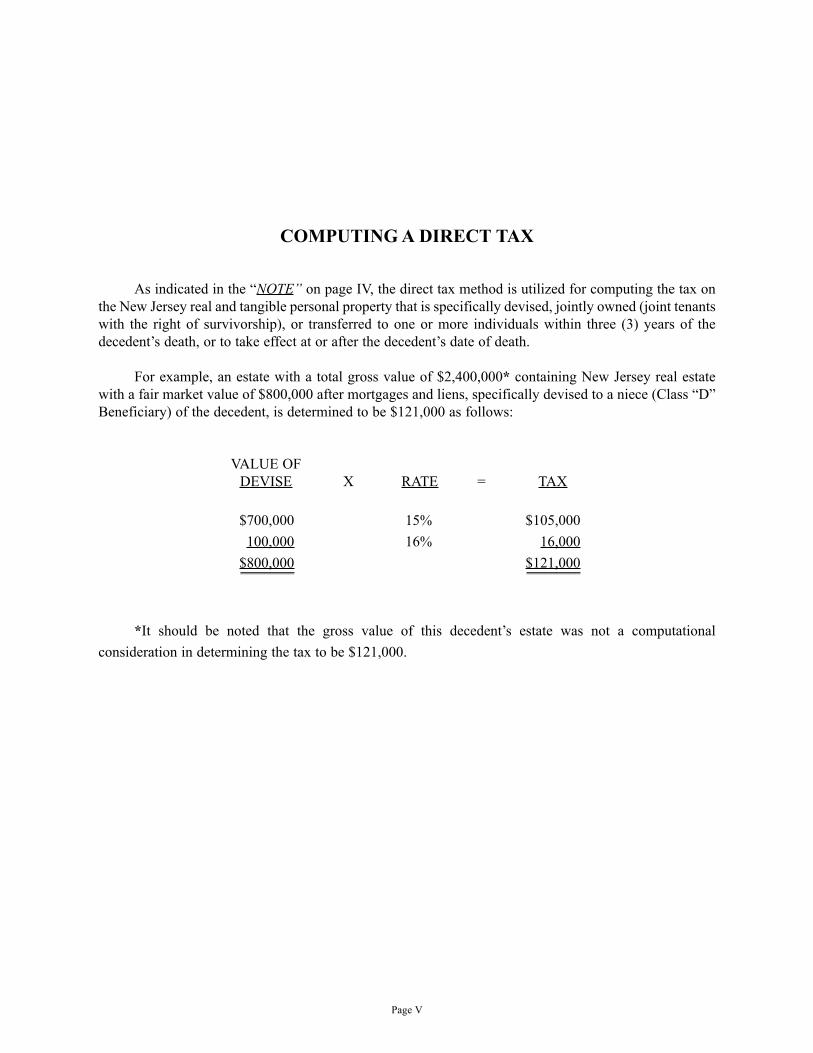

COMPUTING A DIRECT TAX

As indicated in the “NOTE” on page IV, the direct tax method is utilized for computing the tax onthe New Jersey real and tangible personal property that is specifically devised, jointly owned (joint tenantswith the right of survivorship), or transferred to one or more individuals within three (3) years of thedecedent’s death, or to take effect at or after the decedent’s date of death.

For example, an estate with a total gross value of $2,400,000* containing New Jersey real estatewith a fair market value of $800,000 after mortgages and liens, specifically devised to a niece (Class “D”Beneficiary) of the decedent, is determined to be $121,000 as follows:

VALUE OFDEVISE X RATE = TAX

$700,000 15% $105,000100,000 16% 16,000

$800,000 $121,000_________ _________

*It should be noted that the gross value of this decedent’s estate was not a computationalconsideration in determining the tax to be $121,000.

Page V

First $700,000 15%

Over $700,000 16%

CLASS “D” TRANSFEREES If less than $500: no tax

If $500 or more: no exemption

CLASS “A” TRANSFEREES ARE ENTIRELY EXEMPT

Page VI

Exempt

11%

13%

14%

16%

First $ 25,000

Next 1,075,000

Next 300,000

Next 300,000

Over 1,700,000

Class “C” TRANSFEREES IN ESTATES OF DECEDENTS DYING ON OR AFTER 7/1/88

Do you expect to file a Federal Estate Tax Return? . . . . . . . . . . . . . . . . . Yes No

1. Schedule A . . . . . . . . . . . . . . . . . . . . . Real Property . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.

2. Schedule B . . . . . . . . . . . . . . . . . . . . . Closely Held “Businesses” . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.

3. Schedule B(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3.

4. Schedule E . . . . . . . . . . . . . . . . . . . . . . Transfers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4.

5. Total Estate Wherever Situate (Add Lines 1 thru 4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5.

6. Schedule C . . . . . . . . . . . . . . . . . . . . . Deductions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6.

7. Net Estate Wherever Situate (Line 5, minus Line 6) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7.

8. Contingent Amount Included in Line 7 (See instructions on reverse side) . . . . . . . . . . . . . . . . . . . . . . . 8.

9. Balance of Estate (Line 7, minus Line 8) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9.

10. Method Used for Tax Calculation: . . . Flat Tax Ratio Direct Tax . . . . . . . . . . . . . . . . 10.

11. Tax Due Based on Calculation Method (from attached worksheet) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.

12. Compromise Tax Due on Line 8 Amount (See instructions on reverse side) . . . . . . . . . . . . . . . . . . . . . 12.

13. Contingent Tax (See instructions on reverse side) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13.

14. Total Tax Due (Total - Line 11 thru Line 13) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14.

15. Interest Due (If applicable) (See instructions on reverse side) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15.

16. Total Amount Due (Line 14, plus Line 15) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16.

17. Payment on Account (If applicable) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17.

18. If Line 17 (Payments) is LESS THAN Line 16, Enter BALANCE DUE - PAY THIS AMOUNT 18.

19. If Line 17 (Payments) is MORE THAN Line 16 Enter REFUND AMOUNT . . . . . . . . . . . . . . . 19.

Deponent says, under penalty of perjury, “I declare that I have examined this return and all accompanying schedules and to the best of my knowledge and belief, it is true,correct and complete.” I hereby authorize the party(s) set forth above to act as the estate’s representative, to receive confidential information, and to make presentations onbehalf of the estate.

Subscribed and sworn before me

this ___________________________ day of ____________________________, _______.

________________________________________________________________________Official Title (Notarized)

THIS FORM MAY BE REPRODUCEDIT-NR - Page 1

ATTA

CH C

HEC

K F

OR

BAL

ANCE

DU

E H

ERE

STATE OF NEW JERSEYInheritance Tax Return

NON-RESIDENT DECEDENT(Instructions on reverse side)

IT-NR (10/06) (67) For Division Use Only

Transfer Inheritance TaxPO Box 249Trenton, NJ 08695-0249

Decedent’s Name________________________________________________________ Decedent’s S.S. No. ____________/__________/____________(Last) (First) (Middle)

Date of Death (mm/dd/yy) _________/_______/_________ State of Residence _______________________________ Testate Intestate

Name __________________________________________________ Phone ( ) _____________________________

Street _______________________________________________________________________________________________

City ___________________________________________ State ________________ Zip Code ________________________

Mailing Addressto send all

correspondence

_____________________________________________________________________(Executor - Administrator - Heir-at-law)

Address: _____________________________________________________________________

_____________________________________________________________________

____________________________________________________________________

Lines 8, 12 and 13In the case of a transfer or transfers made subject to a

contingency or condition which renders a definite determination ofthe Transfer Inheritance Tax due impossible, the Division willsuggest a compromise of the tax based upon immediate paymentand final disposition of the tax. N.J.A.C. 18:26-2.14, N.J.S.A.54:36-6 AND 54:36-5.

Therefore, enter on Line 8, the amount of the estate that is“Contingent”.

In the event you wish to compute a compromise for theDivision’s review, you should include a rider setting forth fullcomputations and details and enter the proposed amount on Line12. Following this procedure may speed the auditing of thedecedent’s return.

Be advised that where all or any portion of the contingentamount has vested in a beneficiary by reason of the happening ofany contingency event, full details should be set forth on a rider,the tax computed on a rider and entered on Line 13.

Line 15Interest accrues at the rate of 10% per annum on any tax due

or portion thereof not paid within eight months of the decedent’sdeath.

With respect to the payment of the tax due on an executorydevise, or a transfer subject to a contingency or power ofappointment, any payment on such a transfer after the expiration oftwo months from the date the contingency occurs or the propertyvests, shall bear interest at the rate of 10% per annum.

In any case where a contingent remainder vests in beneficialpossession and enjoyment subsequent to the death of the originaldecedent, but prior to the expiration of the statutory interest period,interest on the contingent tax does not start to accrue until eightmonths from the date of death of the original decedent.

Line 17Payments on account may be made at any time to avoid

further accrual of interest on the amount so paid. Any overpaymentwill be promptly refunded upon determination of the actual amountpayable. Make checks payable to “NJ Inheritance Tax”, PO Box249, Trenton, NJ 08695-0249.

ESTIMATED PAYMENT Forms and IT-EP Forms areincluded in this package.

INSTRUCTIONS FOR RECITAL PAGE

Examples of Interest Computations

Date of Death . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5-28-90Interest Date (eight months) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-28-91

Tax Assessed . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $7,120.48Interest @ 10% per annum from 1-28-91 to 9-19-91 ($7,120.48 x 10% x 234/365) . . . . . . . . . . . . . . . . . . . 456.49Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7,576.97Payment on Account (9-19-91) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (7,120.48)Balance Due (plus interest @ 10% per annum from 9-19-91 to date of final payment) . . . . . . . . . . . . . . . . . . 456.49

Date of Death . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8-29-90Interest Date (eight months) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-29-91

Tax Assessed . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $68,389.70Payment on Account (4-19-91) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (16,974.56)Balance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51,415.14Payment on Account (4-28-91) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (31,927.02)Balance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19,488.12Interest @ 10% per annum from 4-29-91 to 5-10-91 ($19,488.12 x 10% x 11/365) . . . . . . . . . . . . . . . . . . . 58.73Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19,546.85Payment on Account (5-10-91) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (27,048.67)Overpayment (to be refunded) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7,501.82

IT-NR Page 2

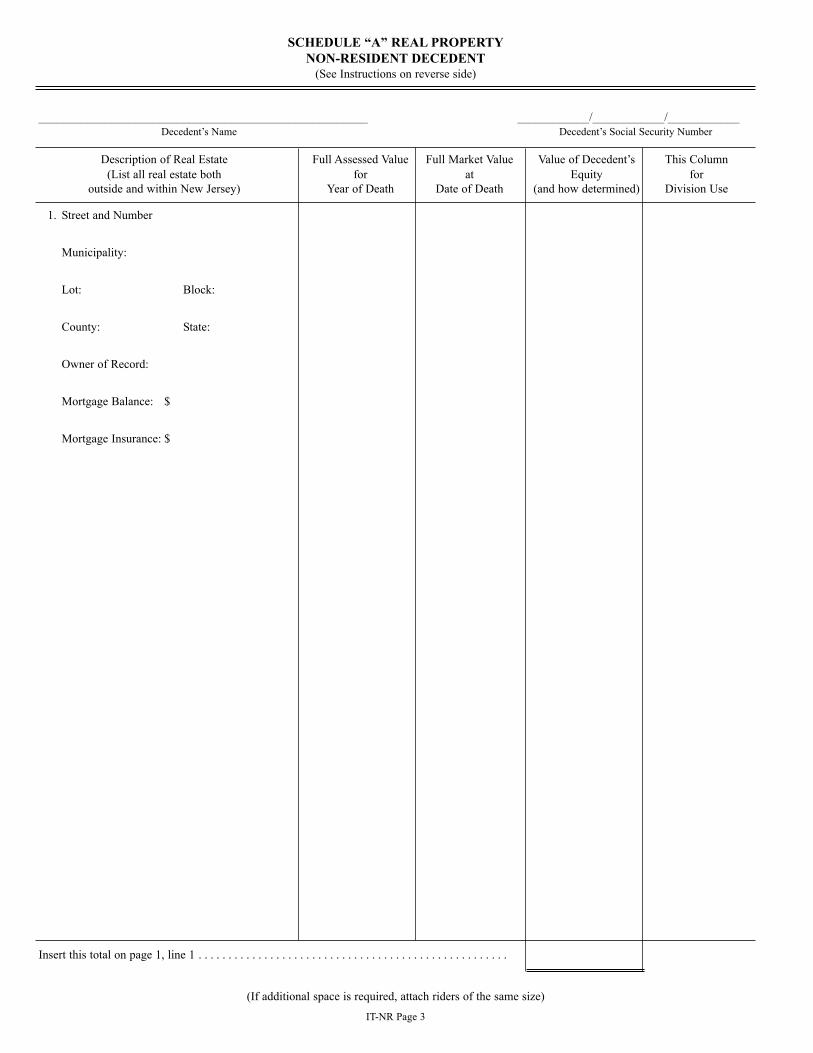

SCHEDULE “A” REAL PROPERTYNON-RESIDENT DECEDENT

(See Instructions on reverse side)

_______________________________________________________ ____________/____________/____________Decedent’s Name Decedent’s Social Security Number

Description of Real Estate Full Assessed Value Full Market Value Value of Decedent’s This Column(List all real estate both for at Equity for

outside and within New Jersey) Year of Death Date of Death (and how determined) Division Use

Insert this total on page 1, line 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(If additional space is required, attach riders of the same size)

IT-NR Page 3

1. Street and Number

Municipality:

Lot: Block:

County: State:

Owner of Record:

Mortgage Balance: $

Mortgage Insurance: $

INSTRUCTIONS FOR SCHEDULE “A”

Real property in New Jersey should be described by the name of the town or city and county wherein saidproperty is located, and by lot and block number and street number, if any.

• Explain how any fractional ownership in realty was derived. Indicate also whether held as tenants incommon, as joint tenants or by entireties.

• Submit verification of the balance at the decedent’s date of death of any mortgage on New Jersey real estate.

• Submit a copy of any appraisal, contract of sale, or closing statement.

IT-NR Page 4

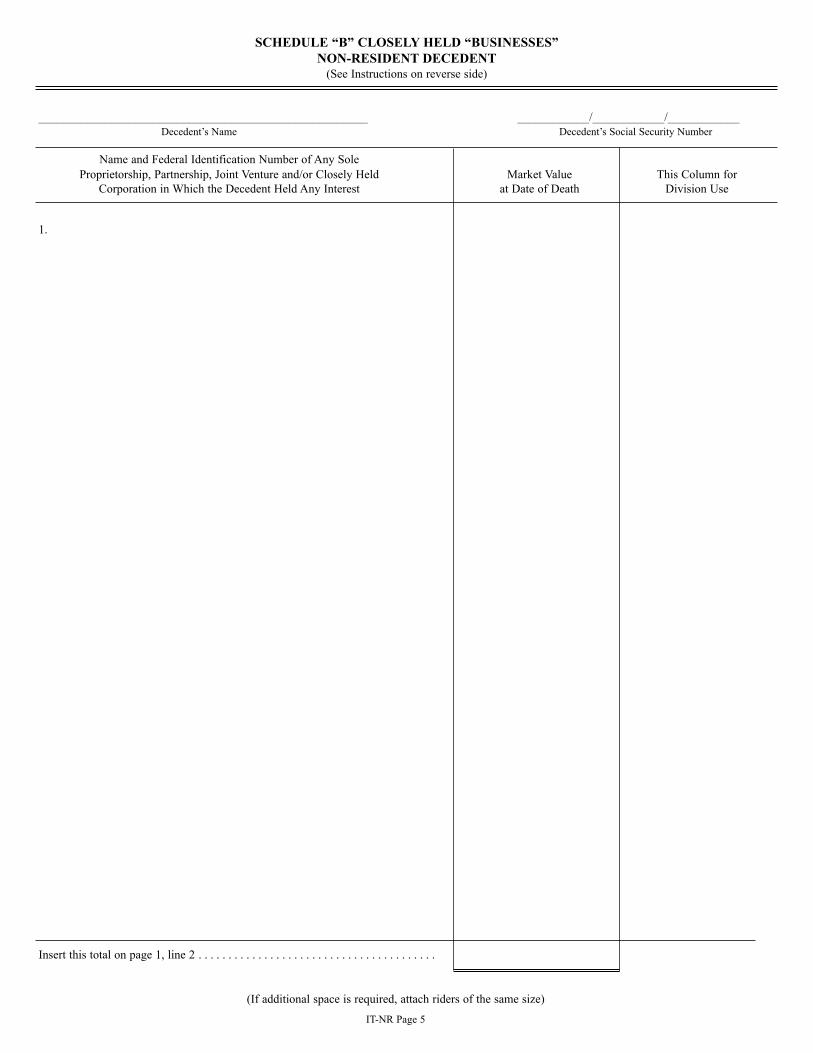

SCHEDULE “B” CLOSELY HELD “BUSINESSES”NON-RESIDENT DECEDENT

(See Instructions on reverse side)

_______________________________________________________ ____________/____________/____________Decedent’s Name Decedent’s Social Security Number

Name and Federal Identification Number of Any SoleProprietorship, Partnership, Joint Venture and/or Closely Held Market Value This Column for

Corporation in Which the Decedent Held Any Interest at Date of Death Division Use

Insert this total on page 1, line 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(If additional space is required, attach riders of the same size)

IT-NR Page 5

1.

INSTRUCTIONS FOR SCHEDULE “B”

GENERALIf the taxpayer had any interest in a closely held corporation, partnership, joint venture or sole proprietorship, the

following information is required (in each instance):1. A detailed balance sheet and profit and loss statement, revised to reflect the market value of the assets thereof as

distinguished from the net book value, as of the decedent’s date of death, or as near thereto as the Director may deemacceptable.

2. For the five year period preceding the decedent’s date of death:A. Detailed balance sheets.B. Detailed profit and loss statements.

3. The nature of the business.4. Describe and state the assessed and market value of any real property.5. Set forth your basis for determining the clear market value as reported.

CLOSELY HELD CORPORATIONSIf the decedent had any interest in a closely held corporation, submit (in addition to the general information required

above):1. For the five year period preceding the decedent’s date of death:

A. A listing of salaries paid to officers.B. A listing of dividends paid, together with the name(s) of the payees.

2. Copy/copies of any stock purchase or option agreement to which the decedent was a party as of the date of death.3. Copy/copies of any insurance policy/policies on the decedent’s life payable to the corporation as beneficiary together

with a statement of the benefits payable thereunder.4. The number of shares of stock of all classes issued and outstanding and the par value thereof.5. List of stockholders setting forth the number of shares held by each.

PARTNERSHIPS OR JOINT VENTURESIf the decedent had any interest in a partnership or joint venture, submit (in addition to the general information required

above):1. Copy of the partnership agreement.2. Copy/copies of any mutual purchase agreement(s) to which the decedent was a party at the date of death.3. Copy/copies of any insurance policy/policies on the decedent’s life payable to the surviving partners as beneficiary

together with a statement of the benefits payable thereunder.

SOLE PROPRIETORSHIPSIf the decedent had any interest in a sole proprietorship, submit (in addition to the general information required above):

1. If any of the sole proprietorship’s assets are listed elsewhere on this return, (i.e. Schedule “A”), make fulldisclosure.

IT-NR Page 6

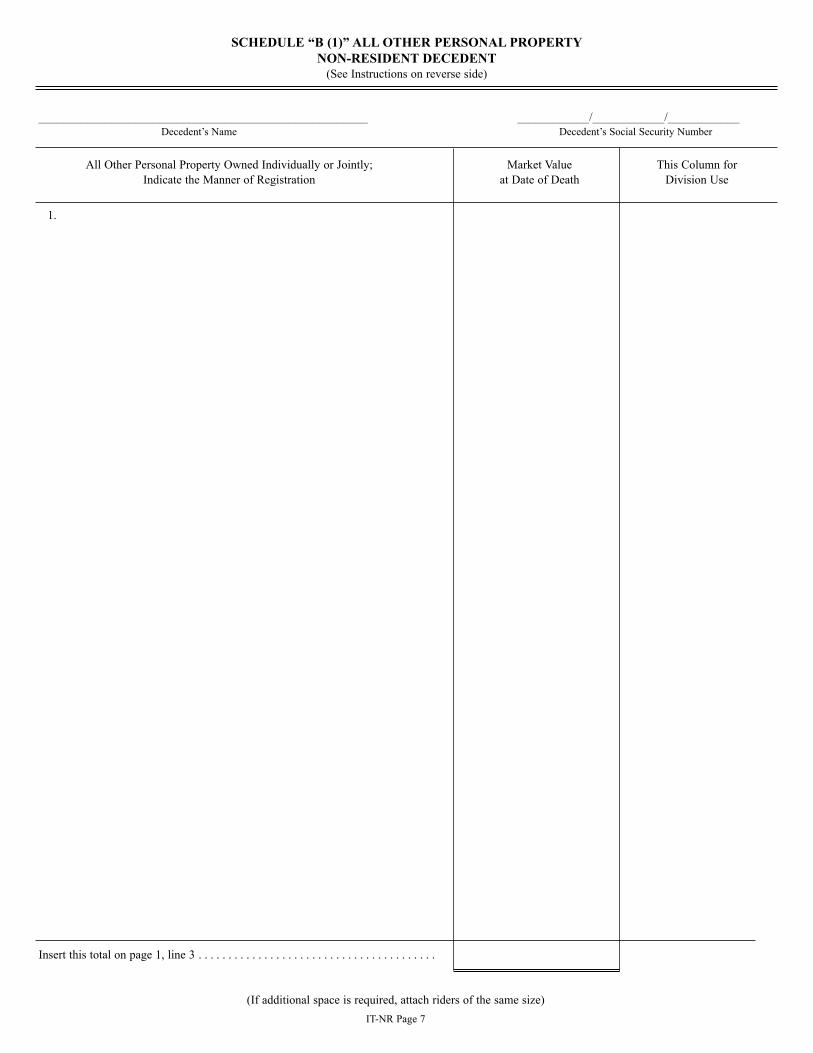

SCHEDULE “B (1)” ALL OTHER PERSONAL PROPERTYNON-RESIDENT DECEDENT

(See Instructions on reverse side)

_______________________________________________________ ____________/____________/____________Decedent’s Name Decedent’s Social Security Number

All Other Personal Property Owned Individually or Jointly; Market Value This Column forIndicate the Manner of Registration at Date of Death Division Use

Insert this total on page 1, line 3 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(If additional space is required, attach riders of the same size)IT-NR Page 7

1.

INSTRUCTIONS FOR SCHEDULE “B (1)”

List all tangible and intangible personal property (excluding that on Schedule B) wherever situated.

This schedule must disclose not only all other personal property owned individually by the decedent but also all otherpersonal property standing in joint names (such as United States Savings Bonds, bank accounts, shares of stock, etc.) whichmay be claimed by another or others as survivors. The deceased joint tenant is deemed to have been the absolute owner ofthe property and the survivor/survivors are presumed to have received a devise or bequest of the whole and not a part of theproperty. This presumption can be rebutted to the extent that the survivor can prove contributions out of funds separate andapart from those that originated in the decedent.

This schedule must list all other intangible personal property such as, but not limited to, United States Savings Bonds;treasury certificates; cash on hand; cash in the bank; deposits in Federal or State Credit Unions; mutual funds; bonds andmortgages; promissory notes; claims; accounts receivables; corporate bonds; corporate stocks; accrued interest; dividends;salaries or wages; insurance payable to the estate or its representatives; interest in any undistributed estate or income fromany property held in trust under the will or agreement of another.

IT-NR Page 8

Name:______________________________________________

Name:______________________________________________

(If more than two, attach a rider of the same size)

Name(s):______________________________________________

______________________________________________

SS# _______________/____________/______________

SS# _______________/____________/______________

Name:_________________________________________

SCHEDULE “C” DEDUCTIONS CLAIMEDNON-RESIDENT DECEDENT(See Instructions on reverse side)

_______________________________________________________ ____________/____________/____________Decedent’s Name Decedent’s Social Security Number

Insert this total on page 1, line 6 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(If additional space is required, attach riders of the same size)

IT-NR Page 9

Debt or Claim of Nature of Same Amount This Column forDivision Use

Estimated Expenses for:Administration . . . . . . . . . . . . . . . . . . .

(Attach an itemized list)

Counsel Fees:Agreed Upon . . . . . . . . . . . . . . . . . . . .Estimated . . . . . . . . . . . . . . . . . . . . . . .

Executor’s or Administrator’s Commissions(Must not be claimed unless reported forIncome Tax purposes.)

SUBTOTAL . . . . . . . . . . . . . . . . . . . . . . .

Funeral . . . . . . . . . . . . . . . . . . . . . . . . . . .

Transfer taxes paid to other states . . . . . .(itemize by state)

Other Deductions (list individually)

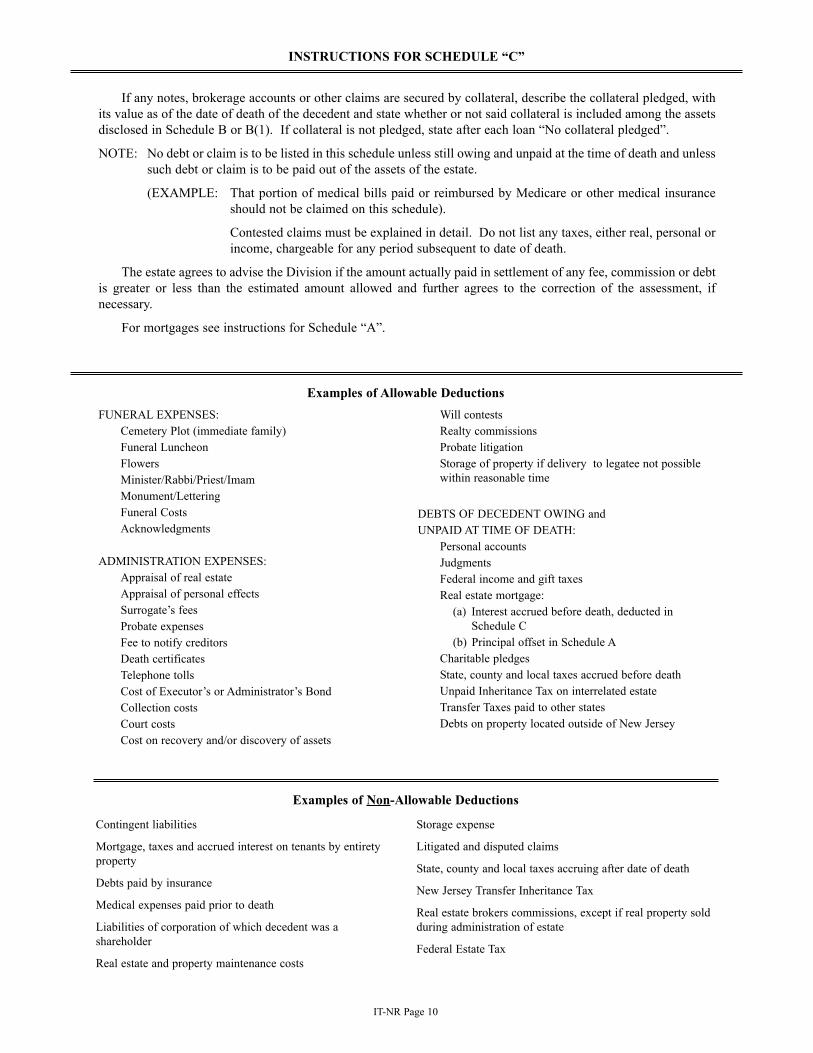

INSTRUCTIONS FOR SCHEDULE “C”

If any notes, brokerage accounts or other claims are secured by collateral, describe the collateral pledged, withits value as of the date of death of the decedent and state whether or not said collateral is included among the assetsdisclosed in Schedule B or B(1). If collateral is not pledged, state after each loan “No collateral pledged”.

NOTE: No debt or claim is to be listed in this schedule unless still owing and unpaid at the time of death and unlesssuch debt or claim is to be paid out of the assets of the estate.

(EXAMPLE: That portion of medical bills paid or reimbursed by Medicare or other medical insuranceshould not be claimed on this schedule).

Contested claims must be explained in detail. Do not list any taxes, either real, personal orincome, chargeable for any period subsequent to date of death.

The estate agrees to advise the Division if the amount actually paid in settlement of any fee, commission or debtis greater or less than the estimated amount allowed and further agrees to the correction of the assessment, ifnecessary.

For mortgages see instructions for Schedule “A”.

FUNERAL EXPENSES:Cemetery Plot (immediate family)Funeral LuncheonFlowersMinister/Rabbi/Priest/ImamMonument/LetteringFuneral CostsAcknowledgments

ADMINISTRATION EXPENSES:Appraisal of real estateAppraisal of personal effectsSurrogate’s feesProbate expensesFee to notify creditorsDeath certificatesTelephone tollsCost of Executor’s or Administrator’s BondCollection costsCourt costsCost on recovery and/or discovery of assets

Will contestsRealty commissionsProbate litigationStorage of property if delivery to legatee not possible within reasonable time

DEBTS OF DECEDENT OWING andUNPAID AT TIME OF DEATH:

Personal accountsJudgmentsFederal income and gift taxesReal estate mortgage:

(a) Interest accrued before death, deducted inSchedule C

(b) Principal offset in Schedule ACharitable pledgesState, county and local taxes accrued before deathUnpaid Inheritance Tax on interrelated estateTransfer Taxes paid to other statesDebts on property located outside of New Jersey

Contingent liabilities

Mortgage, taxes and accrued interest on tenants by entiretyproperty

Debts paid by insurance

Medical expenses paid prior to death

Liabilities of corporation of which decedent was ashareholder

Real estate and property maintenance costs

Storage expense

Litigated and disputed claims

State, county and local taxes accruing after date of death

New Jersey Transfer Inheritance Tax

Real estate brokers commissions, except if real property soldduring administration of estate

Federal Estate Tax

Examples of Allowable Deductions

Examples of Non-Allowable Deductions

IT-NR Page 10

SCHEDULE “D” NON-RESIDENT DECEDENT

_______________________________________________________ ____________/____________/____________Decedent’s Name Decedent’s Social Security Number

Details of Real and Tangible Personal Property subject to the jurisdiction of the State of New Jersey.CONSENTS TO TRANSFER WILL BE GRANTED ONLY ON PROPERTY INCLUDED IN THIS SCHEDULE.

1. List below all New Jersey realty owned by decedent.2. Also list all tangible goods, wares and merchandise in New Jersey.

(Note: Waivers are not required to transfer any intangibles such as bank accounts,mortgages, or bonds and stocks of New Jersey corporations.)

IT-NR Page 11

Market Valueof Decedent’s Equity

This Column forDivision Use

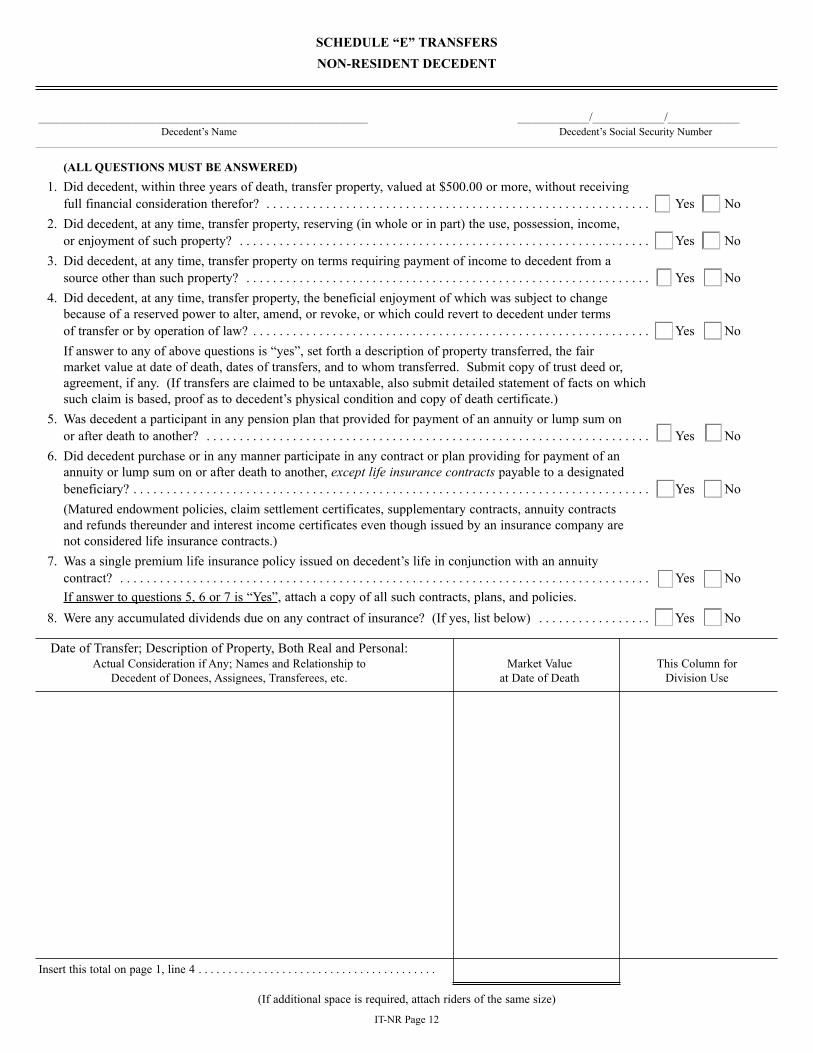

SCHEDULE “E” TRANSFERSNON-RESIDENT DECEDENT

_______________________________________________________ ____________/____________/____________Decedent’s Name Decedent’s Social Security Number

Insert this total on page 1, line 4 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(If additional space is required, attach riders of the same size)

IT-NR Page 12

(ALL QUESTIONS MUST BE ANSWERED)1. Did decedent, within three years of death, transfer property, valued at $500.00 or more, without receiving

full financial consideration therefor? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No2. Did decedent, at any time, transfer property, reserving (in whole or in part) the use, possession, income,

or enjoyment of such property? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No3. Did decedent, at any time, transfer property on terms requiring payment of income to decedent from a

source other than such property? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No4. Did decedent, at any time, transfer property, the beneficial enjoyment of which was subject to change

because of a reserved power to alter, amend, or revoke, or which could revert to decedent under termsof transfer or by operation of law? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes NoIf answer to any of above questions is “yes”, set forth a description of property transferred, the fairmarket value at date of death, dates of transfers, and to whom transferred. Submit copy of trust deed or,agreement, if any. (If transfers are claimed to be untaxable, also submit detailed statement of facts on whichsuch claim is based, proof as to decedent’s physical condition and copy of death certificate.)

5. Was decedent a participant in any pension plan that provided for payment of an annuity or lump sum onor after death to another? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No

6. Did decedent purchase or in any manner participate in any contract or plan providing for payment of anannuity or lump sum on or after death to another, except life insurance contracts payable to a designatedbeneficiary? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No(Matured endowment policies, claim settlement certificates, supplementary contracts, annuity contractsand refunds thereunder and interest income certificates even though issued by an insurance company arenot considered life insurance contracts.)

7. Was a single premium life insurance policy issued on decedent’s life in conjunction with an annuitycontract? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes NoIf answer to questions 5, 6 or 7 is “Yes”, attach a copy of all such contracts, plans, and policies.

8. Were any accumulated dividends due on any contract of insurance? (If yes, list below) . . . . . . . . . . . . . . . . . Yes No

Date of Transfer; Description of Property, Both Real and Personal:Actual Consideration if Any; Names and Relationship to Market Value This Column for

Decedent of Donees, Assignees, Transferees, etc. at Date of Death Division Use

Age AtDeath ofDecedent

NAME DATE OF DEATH DOMICILE AT DEATH

SCHEDULE “F” BENEFICIARIESNON-RESIDENT DECEDENT

ATTACH COPY OF WILL AND CODICILS HERE

_______________________________________________________ ____________/____________/____________Decedent’s Name Decedent’s Social Security Number

In case of intestacy, the parentage of all collateral heirs (such as nieces, nephews, cousins, etc.) must be set forth. The relationship of step-parent,step-child, step-brother or step-sister must be so stated.

BENEFICIARIES AND ADDRESSES(State full names and addresses of all who have aninterest, vested, contingent or otherwise, in estate)

Under authority of Federal law, the Division of Taxation of the Department of the Treasury of the State of New Jersey and the Internal RevenueService have entered into a Federal/State Agreement for the mutual exchange of tax information for purpose of tax administration.

Deponent further says the following schedule contains the names of all beneficiaries who died before or after decedent’s death:

RelationshipInterest of

BeneficiaryIn Estate

SurvivedDecedent

StateYes or No

Class

IT-NR Page 13

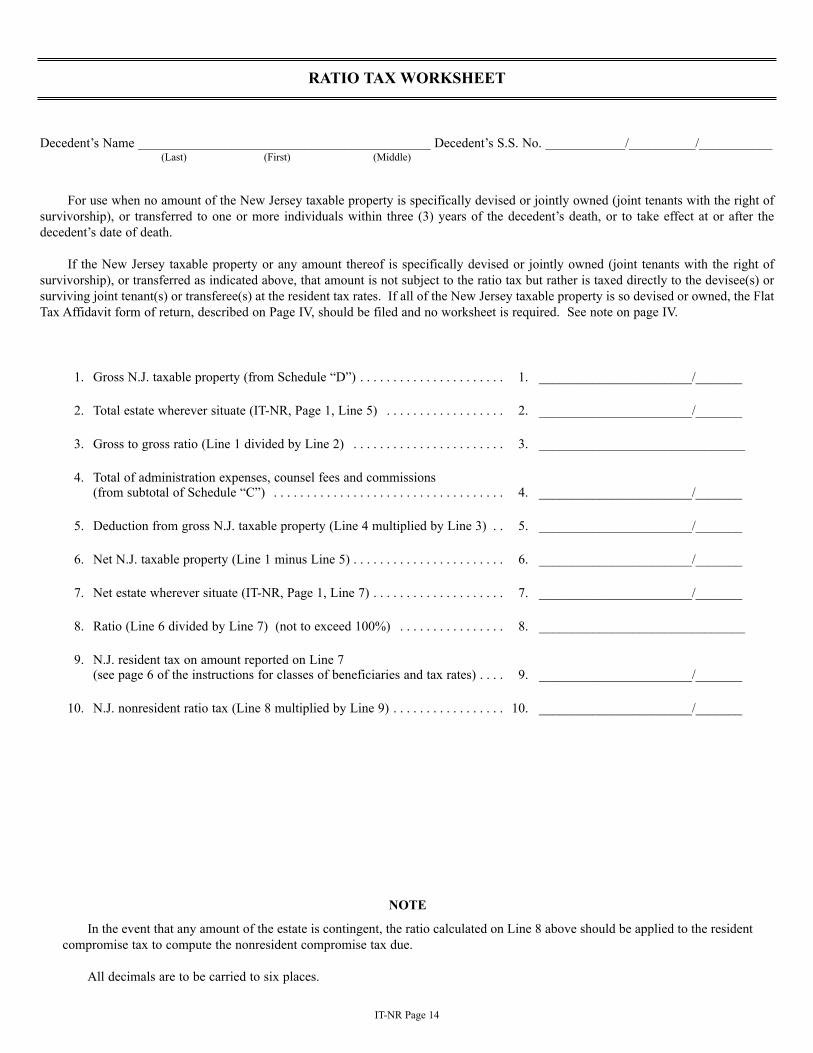

Decedent’s Name ____________________________________________ Decedent’s S.S. No. ____________/__________/___________(Last) (First) (Middle)

For use when no amount of the New Jersey taxable property is specifically devised or jointly owned (joint tenants with the right ofsurvivorship), or transferred to one or more individuals within three (3) years of the decedent’s death, or to take effect at or after thedecedent’s date of death.

If the New Jersey taxable property or any amount thereof is specifically devised or jointly owned (joint tenants with the right ofsurvivorship), or transferred as indicated above, that amount is not subject to the ratio tax but rather is taxed directly to the devisee(s) orsurviving joint tenant(s) or transferee(s) at the resident tax rates. If all of the New Jersey taxable property is so devised or owned, the FlatTax Affidavit form of return, described on Page IV, should be filed and no worksheet is required. See note on page IV.

IT-NR Page 14

RATIO TAX WORKSHEET

1. Gross N.J. taxable property (from Schedule “D”) . . . . . . . . . . . . . . . . . . . . . . 1. _______________________/_______

2. Total estate wherever situate (IT-NR, Page 1, Line 5) . . . . . . . . . . . . . . . . . . 2. _______________________/_______

3. Gross to gross ratio (Line 1 divided by Line 2) . . . . . . . . . . . . . . . . . . . . . . . 3. _______________________________

4. Total of administration expenses, counsel fees and commissions(from subtotal of Schedule “C”) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4. _______________________/_______

5. Deduction from gross N.J. taxable property (Line 4 multiplied by Line 3) . . 5. _______________________/_______

6. Net N.J. taxable property (Line 1 minus Line 5) . . . . . . . . . . . . . . . . . . . . . . . 6. _______________________/_______

7. Net estate wherever situate (IT-NR, Page 1, Line 7) . . . . . . . . . . . . . . . . . . . . 7. _______________________/_______

8. Ratio (Line 6 divided by Line 7) (not to exceed 100%) . . . . . . . . . . . . . . . . 8. _______________________________

9. N.J. resident tax on amount reported on Line 7(see page 6 of the instructions for classes of beneficiaries and tax rates) . . . . 9. _______________________/_______

10. N.J. nonresident ratio tax (Line 8 multiplied by Line 9) . . . . . . . . . . . . . . . . . 10. _______________________/_______

NOTE

In the event that any amount of the estate is contingent, the ratio calculated on Line 8 above should be applied to the residentcompromise tax to compute the nonresident compromise tax due.

All decimals are to be carried to six places.

Decedent’s Name ____________________________________________ Decedent’s S.S. No. ____________/__________/___________(Last) (First) (Middle)

For use when only part of the New Jersey taxable estate is specifically devised or jointly owned (joint tenants with the right ofsurvivorship), or transferred to one or more individuals within three (3) years of the decedent’s death, or to take effect at or after thedecedent’s date of death.

If the New Jersey taxable property or any amount thereof is specifically devised or jointly owned (joint tenants with the right ofsurvivorship), or transferred as indicated above, that amount is not subject to the flat tax but rather is taxed directly to the devisee(s) orsurviving joint tenant(s) or transferee(s) at the resident tax rates. See note on page IV.

IT-NR Page 15

COMBINATION DIRECT TAX AND FLAT TAX WORKSHEET

1. Direct tax on New Jersey taxable property specifically devised, jointlyowned, or transferred as indicated above. See page V. . . . . . . . . . . . . . . . . . 1. ______________________________

2. Value of New Jersey taxable property not specifically devised, jointlyowned, or transferred as indicated above. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2. ______________________________

3. Value of gross estate both in and outside of New Jersey (including theNew Jersey property specifically devised, jointly owned, or transferred asindicated above) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3. ______________________________

4. Flat tax ratio (Line 2 divided by Line 3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4. _______________________________

5. New Jersey resident tax on amount reported on Line 3 above (see page VIof the instructions for classes of beneficiaries and tax rates) . . . . . . . . . . . . . 5. ______________________________

6. Resident tax less direct tax (Line 5 minus Line 1) . . . . . . . . . . . . . . . . . . . . . 6. ______________________________

7. Flat tax (Line 4 multiplied by Line 6) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7. ______________________________

8. Total direct tax and flat tax (Line 1 plus Line 7) . . . . . . . . . . . . . . . . . . . . . . . 8. ______________________________

NOTE

In the event that any amount of the estate is contingent, the ratio calculated on Line 4 above should be applied to the residentcompromise tax to compute the nonresident compromise tax due.

All decimals are to be carried to six places.

Decedent’s Name ____________________________________________ Decedent’s S.S. No. ____________/__________/___________(Last) (First) (Middle)

For use when only part of the New Jersey taxable estate is specifically devised or jointly owned (joint tenants with the right ofsurvivorship), or transferred to one or more individuals within three (3) years of the decedent’s death, or to take effect at or after thedecedent’s date of death.

If the New Jersey taxable property or any amount thereof is specifically devised or jointly owned (joint tenants with the right ofsurvivorship), or transferred as indicated above, that amount is not subject to the ratio tax but rather is taxed directly to the devisee(s) orsurviving joint tenant(s) or transferee(s)at the resident tax rates. If all of the New Jersey taxable property is so devised or owned the FlatTax Affidavit form of return, described on Page IV, should be filed and no worksheet is required. See note on page IV.

IT-NR Page 16

COMBINATION DIRECT TAX AND RATIO TAX WORKSHEET

1. Direct tax on New Jersey taxable property specifically devised, jointlyowned, or transferred as indicated above. See page V. . . . . . . . . . . . . . . . . . 1. _______________________/_______

2. Value of New Jersey taxable property not specifically devised, jointlyowned, or transferred as indicated above. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2. _______________________/_______

3. Total estate wherever situate (IT-NR, Page 1, Line 5) . . . . . . . . . . . . . . . . . . 3. _______________________/_______

4. Gross to gross ratio (Line 2 divided by Line 3) . . . . . . . . . . . . . . . . . . . . . . . 4. _______________________________

5. Total of administration expenses, counsel fees, and commissions(from subtotal of Schedule “C”) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5. _______________________/_______

6. Amount of Line 5 to be deducted from New Jersey taxable property notspecifically devised, jointly owned, or transferred as indicated above.(Line 4 multiplied by Line 5) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6. _______________________/_______

7. Net New Jersey property subject to the ratio tax (Line 2 minus Line 6) . . . . 7. _______________________/_______

8. Net estate wherever situate (IT-NR, Page 1, Line 7) . . . . . . . . . . . . . . . . . . . . 8. _______________________/_______

9. Ratio (Line 7 divided by Line 8) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9. _______________________________

10. New Jersey resident tax on amount reported on Line 8 above(see Page VI of the instructions for classes of beneficiaries and tax rates) . . 10. _______________________/_______

11. Resident tax less direct tax (Line 10 minus Line 1) . . . . . . . . . . . . . . . . . . . . 11. _______________________/_______

12. Ratio tax (Line 9 multiplied by Line 11) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12. _______________________/_______

13. Total direct tax and ratio tax (Line 1 plus Line 12) . . . . . . . . . . . . . . . . . . . . . 13. _______________________/_______

NOTE

In the event that any amount of the estate is contingent, the ratio calculated on Line 9 above should be applied to the residentcompromise tax to compute the nonresident compromise tax due.

All decimals are to be carried to six places.

Decedent’s Name ____________________________________________ Decedent’s S.S. No. ____________/__________/___________(Last) (First) (Middle)

For use when no amount of the New Jersey taxable property is specifically devised or jointly owned (joint tenants with the right ofsurvivorship), or transferred to one or more individuals within three (3) years of the decedent’s death, or to take effect at or after thedecedent’s date of death.

If the New Jersey taxable property or any amount thereof is specifically devised or jointly owned (joint tenants with the right ofsurvivorship), or transferred as indicated above, that amount is not subject to the flat tax but rather is taxed directly to the devisee(s) orsurviving joint tenant(s) or transferee(s) at the resident tax rates. See note on page IV.

IT-NR Page 17

FLAT TAX WORKSHEET

1. Value of New Jersey real property and tangible personal property . . . . . . . . . 1. _______________________/_______

2. Value of gross estate both in and outside of New Jersey . . . . . . . . . . . . . . . . 2. _______________________/_______

3. Flat tax ratio (Line 1 divided by Line 2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3. _______________________________

4. New Jersey resident tax on amount reported on Line 2 above(See Page VI of the instructions for classes of beneficiaries and tax rates) . . 4. _______________________/_______

5. Flat tax (Line 3 multiplied by Line 4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5. _______________________/_______

NOTE

In the event that any amount of the estate is contingent, the ratio calculated on Line 3 above should be applied to the residentcompromise tax to compute the nonresident compromise tax due.

All decimals are to be carried to six places.