„transformation of the electricity system: technical ... · uwe leprich • professor at the...

TRANSCRIPT

„Transformation of the electricity system: technical organisational andsystem: technical, organisational and

financial issues

Presentation for the Ann al MeetingPresentation for the Annual Meeting of ABOWind

Uwe LeprichInstitut for Future Energy Systems (IZES)

Weiskirchen, September 28, 2012

Uwe Leprich

• professor at the business school of the University of Applied Sciences in Saarbruecken since 1995Applied Sciences in Saarbruecken since 1995

• at the same time scientific head of the Institute for Future Energy Systems (IZES), a university based research institute focussing on renewable energiesresearch institute focussing on renewable energies, energy efficiency and decentralised power generation

• author and co-author of several books and articles lib li d l i i k f d i l l iliberalised electricity markets, feed-in law regulations and instruments for promoting renewable energies in the heat market.

• expert member of the Enquete commission “Sustainable energy supply” of the 14th German Bundestag

• deputy spokesman of the Renewable Energy Research Association since October 2011

2 [ Leprich, September 28, 2012, ABOWind ]

IZES gGmbH

ManagementD Mi h l B d D F ithj f S

y B

oard Scie

Dr. Michael Brand, Dr. Frithjof Spreer

Scientific DirectorProf Dr Uwe Leprich

perv

isor

y entific AdApplied Research and Development

Prof. Dr. Uwe Leprich

der /

Sup

dvisory B

Energy MarketsProf. Dr. Uwe Leprich

BuildingsProf. Dr. Horst Altgeld

Material Flow ManagementProf. Frank Baur

hare

hold

Board

Solar Power / Test of Social-Scientific

Technology and Scientific Infrastructure

Sh Solar Collectors and Systems (TZSB)Danjana Theis

Technical InnovationsDr. Bodo Groß

Social Scientific Energy Research

Prof. Dr. Petra Schweizer-Ries

3 [ Leprich, September 28, 2012, ABOWind ]

Agenda

S t i bilit d t i bl l b l i1 Sustainability and sustainable global energy scenarios

The German path to a sustainable energy system

12

Resume

34

System design: How to finance the future system

Resume4

4 [ Leprich, September 28, 2012, ABOWind ]

Global Scenarios - Overviewar

ios

mat

e S

cen

IPCC – Climate Change Fourth Assessment Report

Clim

ario

srg

y S

cena

IEA-World Energy Outlook

Ene

Greenpeace, DLR –Energy [R]evolution

Shell – Energy Scenarios to 2050

EIA – International Energy Outlook

5 [ Leprich, September 28, 2012, ABOWind ]

IEA World Energy Outlook 2011

Three scenarios (Current Policies Scenario, New Policies Scenario, 450-Scenario)

One scenario that aims for a maximum of 2°C temperature rise in the long term. => 450 - scenario

4/5 of the energy related CO2-emissions that are permitted

IEA-World Energy Outlook

4/5 of the energy related CO2 emissions, that are permitted within the 450-scenario until 2035, are already determined by the existing facilities (plants, buildings, factories).

Energy efficiency has to develop more than twice as fast thanEnergy efficiency has to develop more than twice as fast than in the past 2 ½ decades (450-scenario).

“Golden Age” for natural gas

f In scenario-450: coal consumption has its maximum before 2020 and declines afterwards

6 [ Leprich, September 28, 2012, ABOWind ]

IEA World Energy Outlook 2011

7 [ Leprich, September 28, 2012, ABOWind ]

EU-Energy Roadmap 2050EU Energy Targets for 2020:

Reduction of the greenhouse gas emissions by 20 % (compared to 1990)

Increase the share of renewables in energy consumption to 20 %

Increase in energy efficiency by 20 %

Range of different EU-scenarios of fuel shares in primary energy consumption

Sourcee: E

C 2011

8 [ Leprich, September 28, 2012, ABOWind ]

As it comes to the EU, it is wind and gas!

9 [ Leprich, September 28, 2012, ABOWind ]

Agenda

S t i bilit d t i bl l b l i1 Sustainability and sustainable global energy scenarios

The German path to a sustainable energy system

12

Resume

34

System design: How to finance the future system

Resume4

10 [ Leprich, September 28, 2012, ABOWind ]

Targets of the Energy Concept 2010SSource: S

chhafhausen 22011

… as cornerstones of the German „Energiewende“

11 [ Leprich, September 28, 2012, ABOWind ]

„ g

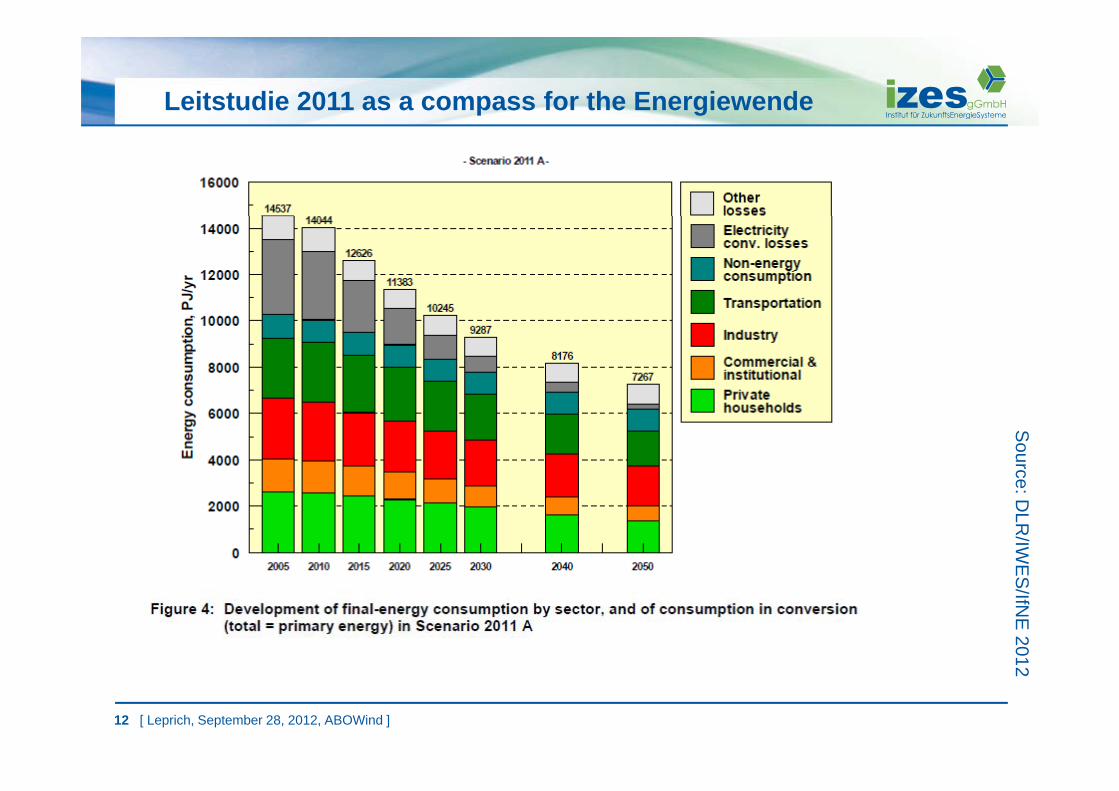

Leitstudie 2011 as a compass for the EnergiewendeS

ourcee: DLR

/IWEES

/IfNE

201

12 [ Leprich, September 28, 2012, ABOWind ]

2

Leitstudie 2011: Gross Electricity GenerationS

ourcee: DLR

/IWEES

/IfNE

201

13 [ Leprich, September 28, 2012, ABOWind ]

2

Leitstudie 2011: Cost AnalysisS

ourcee: DLR

/IWEES

/IfNE

201

14 [ Leprich, September 28, 2012, ABOWind ]

2

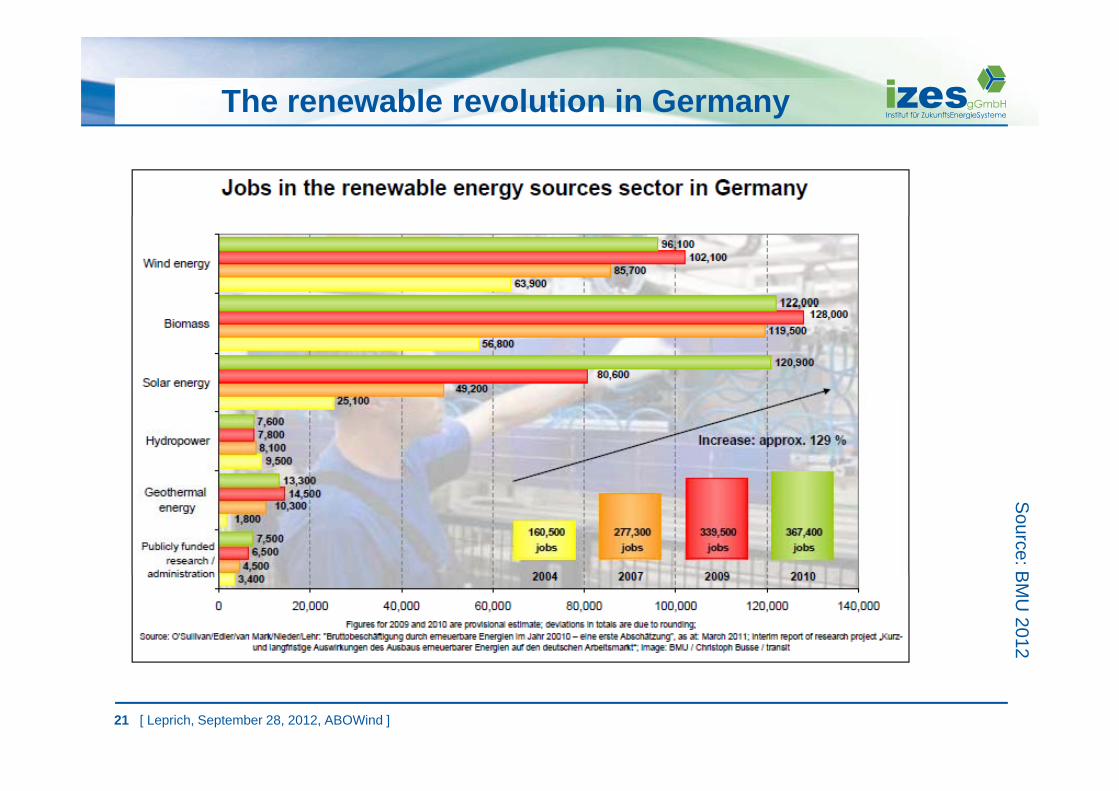

The renewable revolution in GermanyS

ource: BBMU

2012

15 [ Leprich, September 28, 2012, ABOWind ]

The renewable revolution in GermanyS

ource: BBMU

2012

16 [ Leprich, September 28, 2012, ABOWind ]

The renewable revolution in GermanyS

ource: BBMU

2012

17 [ Leprich, September 28, 2012, ABOWind ]

The renewable revolution in GermanyS

ource: BBMU

2012

18 [ Leprich, September 28, 2012, ABOWind ]

The renewable revolution in GermanyS

ource: BBMU

2012

19 [ Leprich, September 28, 2012, ABOWind ]

The renewable revolution in GermanyS

ource: BBMU

2012

20 [ Leprich, September 28, 2012, ABOWind ]

The renewable revolution in GermanyS

ource: BBMU

2012

21 [ Leprich, September 28, 2012, ABOWind ]

Learning curve wind turbinesS

ource: RRenew

s Julii 2010

22 [ Leprich, September 28, 2012, ABOWind ]

Development of costs and feed-in tariffs for PV

Costs and remunerationsremunerations for PV have been cut by more than 50% within 450% within 4 years!

23 [ Leprich, September 28, 2012, ABOWind ]

Expected learning curves for renewables S

ource: WWB

GU

201

24 [ Leprich, September 28, 2012, ABOWind ]

1

Agenda

S t i bilit d t i bl l b l i1 Sustainability and sustainable global energy scenarios

The German path to a sustainable energy system

12

Resume

34

System design: How to finance the future system

Resume4

25 [ Leprich, September 28, 2012, ABOWind ]

The triangle of electricity policyfor 2020o 0 0

35% (39%) Renewables Framework conditionsconditions

• 3 further NPPs off-grid

• no significant storage expansion

• Grid restrictions eliminated?

25% (28%) CHP10% (0%) Reduction

26 [ Leprich, September 28, 2012, ABOWind ]

System Part #1

52 GW PV

The VRE (wind, PV, water) will

Uncertainties

Variablecover up to one half of the total power generation

Will the government hold on to the renewable energy

Renewable

Energies

p g– due to that reason they determine the

targets?

Will the current t iti

gdetermine the rationality of the system

storage capacities be sufficient for that?

Will the grid extension keep up?5-7 GW

Offshore50-70 GW Onshore

27 [ Leprich, September 28, 2012, ABOWind ]

OffshoreOnshore

By the way:

fThe development of wind and PV is increasingly less justified with CO2 reduction targets, but increasingly withwith

• reduction of import dependency

• increase of added domestic value

• job creationjob creation

• stabilization of electricity prices in the long term

• export opportunities of the system

• etc.

28 [ Leprich, September 28, 2012, ABOWind ]

System Part #2

The plant-specific must run-

Investigation requirement

restrictions will gradually be reduced by price

requirement

To what extend can network

Variabley p

signals. related must run-requirements be fulfilled by

Renewable

Energies u ed byrenewables?

g

29 [ Leprich, September 28, 2012, ABOWind ]

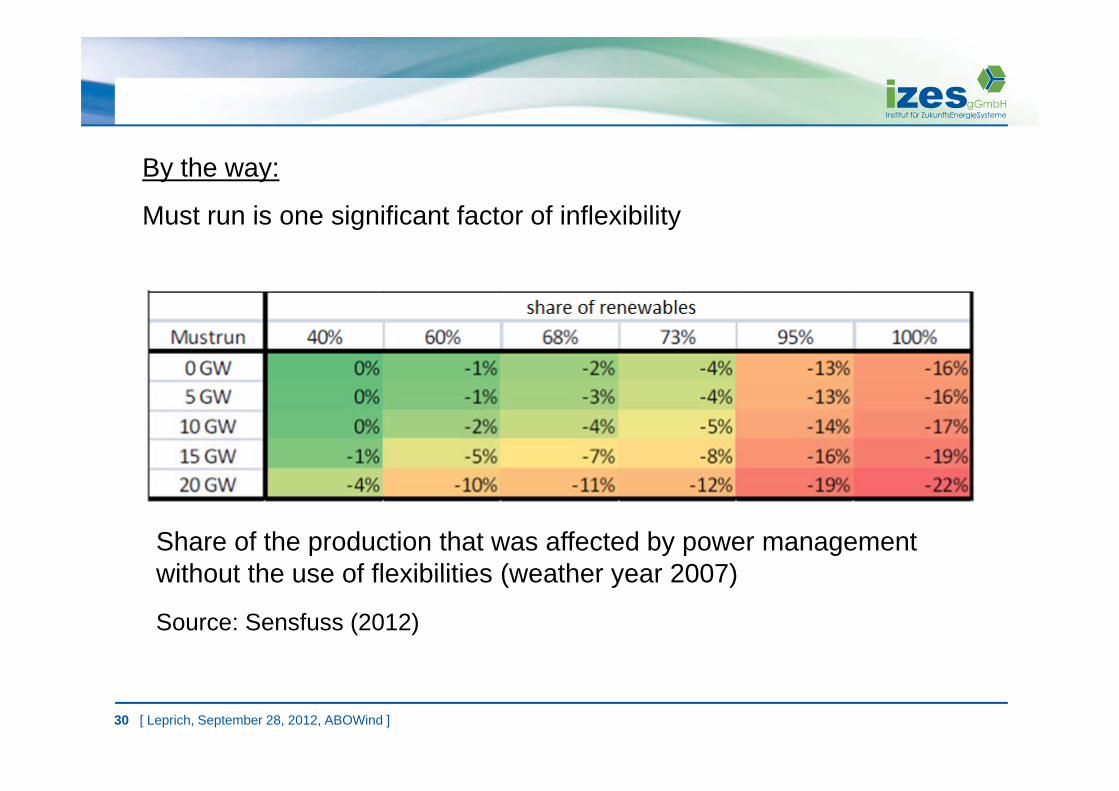

By the way:

Must run is one significant factor of inflexibilityMust run is one significant factor of inflexibility

Share of the production that was affected by power management without the use of flexibilities (weather year 2007)without the use of flexibilities (weather year 2007)

Source: Sensfuss (2012)

30 [ Leprich, September 28, 2012, ABOWind ]

System Part #3

Infrastructure as a system requirementand supplement

31 [ Leprich, September 28, 2012, ABOWind ]

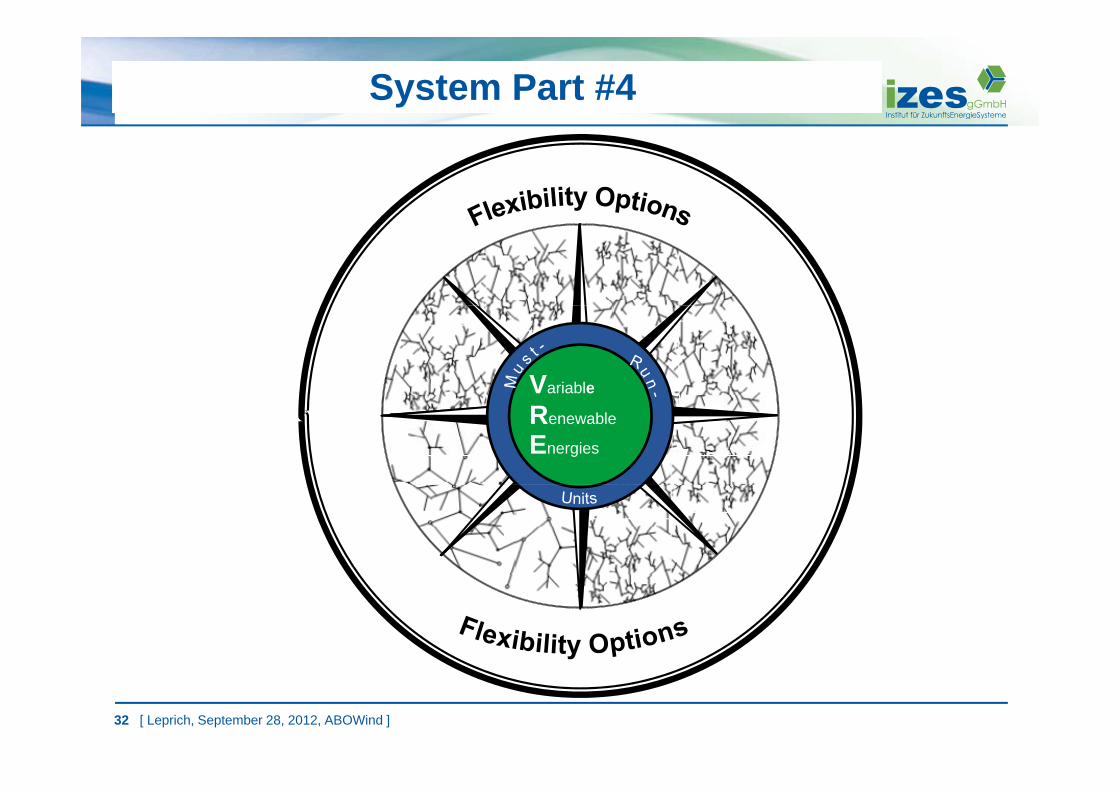

System Part #4

Variable

Renewable

Energies

32 [ Leprich, September 28, 2012, ABOWind ]

The future electricity system

Variable

Renewable

Energies

33 [ Leprich, September 28, 2012, ABOWind ]

Assumption #1

Variable renewable energies will determine the rationality of the future electricity system. All other options in the system will have to adapt to this new rationality and have to be as flexible as possibleadapt to this new rationality and have to be as flexible as possible

Variable

Renewable

Energies

34 [ Leprich, September 28, 2012, ABOWind ]

Assumption #1 (ctd.)A lot of flexibility is needed for the coverage of the residual load!

35 [ Leprich, September 28, 2012, ABOWind ]

Assumption #2

Variable renewable energies with almost zero marginal costs will inevitably drop power exchange prices (“merit oder effect”)

Verhältnis der Stundenmittelwerte der Peak-Stunden zum jährlichen Durchschnittswert des EEX-Spotmarktpreises

von 2007 bis 2012 (April)Decline of the EPEX peak-base ratio due to growing

amounts of PV

50,00 €

52,50 €

55,00 €

150%

160%

170% (from 2007 to april 2012)

42 0 €

45,00 €

47,50 €

120%

130%

140%

in %

37,50 €

40,00 €

42,50 €

100%

110%

120%

35,00 €90%

8‐9h 9‐10h 10‐11h 11‐12h 12‐13h 13‐14h 14‐15h 15‐16h 16‐17h 17‐18h 18‐19h 19‐20h

Tagesstunde2007 2009 2011 Jan ‐ Apr 2012

36 [ Leprich, September 28, 2012, ABOWind ]

Assumption #3

Variable renewable energies with almost zero marginal costs will not be able to recover their capital costs in energy only marketsnot be able to recover their capital costs in energy only markets

for a foreseeable future

l ti M kt t PV d Wi d 08/2010 05/2012

115,00%

120,00%

relative Marktwerte PV und Wind, 08/2010 - 05/2012

100,00%

105,00%

110,00%

90,00%

95,00%

80,00%

85,00%

August 2010 Oktober 2010 Dezember 2010

Februar 2011 April 2011 Juni 2011 August 2011 Oktober 2011 Dezember 2011

Februar 2012 April 2012

MP/Øspot Wind MP/ØSpot PV Linear (MP/Øspot Wind) Linear (MP/ØSpot PV)

Source: IZES 2012, from www.transparency.eex.com

37 [ Leprich, September 28, 2012, ABOWind ]

MP/Øspot - Wind MP/ØSpot - PV Linear (MP/Øspot - Wind) Linear (MP/ØSpot - PV)

Assumption #3

Variable renewable energies with almost zero marginal costs will not be able to recover their capital costs in energy only marketsnot be able to recover their capital costs in energy only markets

for a foreseeable future

Source: MVV 2012, internal calculations

Market Value Wind Onshore: Historical dataMarket Value Wind Onshore: Upper bandMarket Value Wind Onshore: Lower band

38 [ Leprich, September 28, 2012, ABOWind ]

Assumption #3

Variable renewable energies with almost zero marginal costs will not be able to recover their capital costs in energy only marketsnot be able to recover their capital costs in energy only markets

for a foreseeable future

Development of the Phelix Baseload Year Futures 2013

39 [ Leprich, September 28, 2012, ABOWind ]

1st segment of finance

Investigation requirement

How can the EEG be further developed in aVariable developed in a „system-beneficial“ way?

Renewable

EnergiesEnergies

40 [ Leprich, September 28, 2012, ABOWind ]

2nd segment of finance

Hypothesis

Grid related

Investigation requirement

Grid related must run-units cover a total

How can new units be financed via grid-fees in aVariable

capacity of 5-10 GW (maximum)

via grid fees in a concrete way?Renewable

EnergiesEnergies

41 [ Leprich, September 28, 2012, ABOWind ]

3rd segment of finance

HypothesisInvestigation requirement

Generally speaking, dispatch

requirement

How can the harmonization

dispatch markets already work

it ll

of these markets with renewable Variable

quite well energies be improved?

Renewable

EnergiesEnergies

42 [ Leprich, September 28, 2012, ABOWind ]

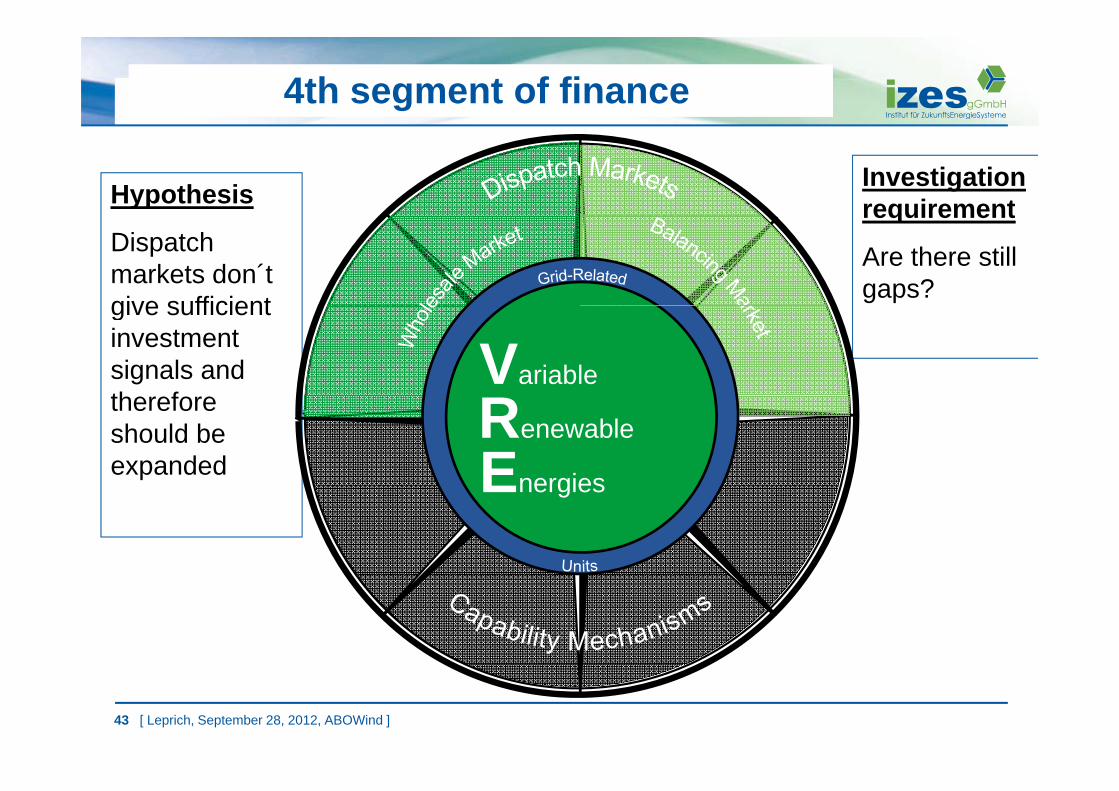

4th segment of finance

Hypothesis Investigation requirement

Dispatch markets don´t give sufficient

requirement

Are there still gaps?give sufficient

investment signals and th f

Variabletherefore should be expanded

Renewable

EnergiesEnergies

43 [ Leprich, September 28, 2012, ABOWind ]

Beyond ceteris paribus …

Variable

Renewable

EnergiesEnergies

44 [ Leprich, September 28, 2012, ABOWind ]

System-design instead of „market-design“

Variable

Renewable

EnergiesEnergies

45 [ Leprich, September 28, 2012, ABOWind ]

Agenda

S t i bilit d t i bl l b l i1 Sustainability and sustainable global energy scenarios

The German path to a sustainable energy system

12

Resume

34

System design: How to finance the future system

Resume4

46 [ Leprich, September 28, 2012, ABOWind ]

Resume

The center of the German Energiewende is the electricity system

The future electricity system will be dominated by variable renewable energies; they will define the g yrationality of the system

To finance the future electricity system one has to o a ce t e utu e e ect c ty syste o e as todifferentiate between four segments; however these segments have interdependencies

The existing system has to be completed by capacity mechanisms which allow for additional capacity related revenues

47 [ Leprich, September 28, 2012, ABOWind ]

Thank you very much for y yyour attention!

Institut für ZukunftsEnergieSysteme (IZES)

Altenkesselerstr. 17, Gebäude A166115 SaarbrückenTel. 0681 – 9762 840Fax 0681 – 9762 850

il l i h@i demail: [email protected] www.izes.de

48 [ Leprich, September 28, 2012, ABOWind ]