transformation report 2018 - sustainability.standardbank.com · supporting social and economic...

TRANSCRIPT

THE STANDARD BANK OF SOUTH AFRICA

TransformationReport 2018

B

Contents2 Introduction

3 A letter from SBSA CE: Lungisa Fuzile

4 Standard Bank’s BEE Scorecard

5 Ownership

7 Management control

10 Skills development

12 Preferential procurement

14 Socioeconomic development and consumer education

20 Empowerment financing and enterprise and supplier development

23 Access to financial services

24 Where to find more information

Introduction This section of our reporting suite looks at how The Standard Bank of South Africa (SBSA) is enabling the transformation of South Africa’s economy through our broad-based black economic empowerment programmes. The report is structured according to the elements of the Financial Sector Code and covers the initiatives, projects, and strategies that are in place to drive transformation.

Our transformation efforts are guided by the SBSA political economy, transformation and black economic empowerment committee (PETBEE) which is chaired by our SBSA chief executive, Lungisa Fuzile. The Standard Bank Group’s social and ethics committee has oversight of this work and monitors progress in achieving transformation targets.

Enabling the transformation of South Africa’s economy aligns with our group social, economic and environmental (SEE) value driver which seeks to generate social, economic and environmental value for our stakeholders and society through our core business activities.

RTS For more information about SEE, please refer to Standard Bank Group’s Reporting to Society.

ESG For more information please refer to our Environmental, Social and Governance (ESG) report.

As the Standard Bank Group, including SBSA, we are striving to impact positively on financial inclusion, job creation, enterprise development and infrastructure development, the facilitation of Africa trade and investment, and education and skills development. These impacts support economic transformation and broad-based black economic empowerment.

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

2

A letter from our SBSA CE: Lungisa FuzileStandard Bank’s purpose is ‘Africa is our home, we drive her growth.’ Driving growth means an economy in which every South African, regardless of their race or gender or the social context, can access basic necessities; and an economy in which success and prosperity are the result of hard work and talent, rather than inherited privilege or personal connections. As a corporate citizen with a social responsibility, we are committed to supporting economic growth.

The pace of transformation in the financial sector has been in sharp focus over the past two years. Standard Bank is committed to supporting social and economic transformation, and the expansion of economically sustainable businesses as the foundation for inclusive growth and profitability. With this, there is a deliberate focus on black and women-owned businesses. We recognise broad-based black economic empowerment (BBBEE) as a moral and commercial imperative, crucial to secure a more sustainable growth path for South Africa.

Standard Bank was recently certified as a Level 1 (BBBEE) Company, under the revised Financial Sector Code. Whilst the Financial Sector Code Scorecard is an important tool to measure our outcomes, it is not the primary way in which we drive transformation activities. We remain focused on ensuring that we play our role in contributing to the creation of a more just and equitable society.

Internally, we continuously work to identify opportunities within the Standard Bank ecosystem to accelerate transformation, leveraging our skills, expertise and access to various stakeholders in the economy. Progress is overseen by the political economy, transformation and BBBEE (PETBEE)committee, and by the group social and ethics committee of the board. Some of the measures that have been implemented include the following:

•• Implementation of clearly defined employment equity (EE) targets, for all business units and corporate functions. Targets are monitored by the PETBEE committee, and by the group social and ethics committee. The heads of our business units and corporate functions account for progress against targets on a regular basis

•• Targeted development of high potential and high performing black and women employees, to position them for senior roles

•• Continual development of a company culture that accommodates and encourages diversity and inclusion. This includes transparent engagement across our business, from board members to general staff, on issues that impact on our ability to accelerate transformation. We have a diversity and inclusion forum, whose mandate includes monitoring EE targets and holding executive and senior management to account on all diversity and inclusion matters

•• Ensuring that our core business makes a substantial contribution to enabling economic activity and driving economic transformation

•• Partnering with third parties to develop black-owned businesses, some of whom are suppliers to Standard Bank.

As a corporate citizen who is responsible for contributing to economic growth, Standard Bank has a moral and social obligation to participate in industry initiatives to accelerate transformation.

Representatives from business, government, the Department of Labour and other stakeholders have been engaging through the National Economic Development and Labour Council (Nedlac) to identify mechanisms to accelerate transformation in the financial sector. Standard Bank has dedicated considerable time to participating in this important dialogue. We are also participating in the Banking Association South Africa (BASA) engagement to develop sector-level commitments, and coordinate detailed action plans for collaborative initiatives, while individual institutions are also developing internal plans.

Standard Bank is committed to engaging with our stakeholders about your expectations of our role in relation to transformation. We welcome your feedback in this regard.

Lungisa Fuzile, Chief executive, The Standard Bank of South Africa

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

3

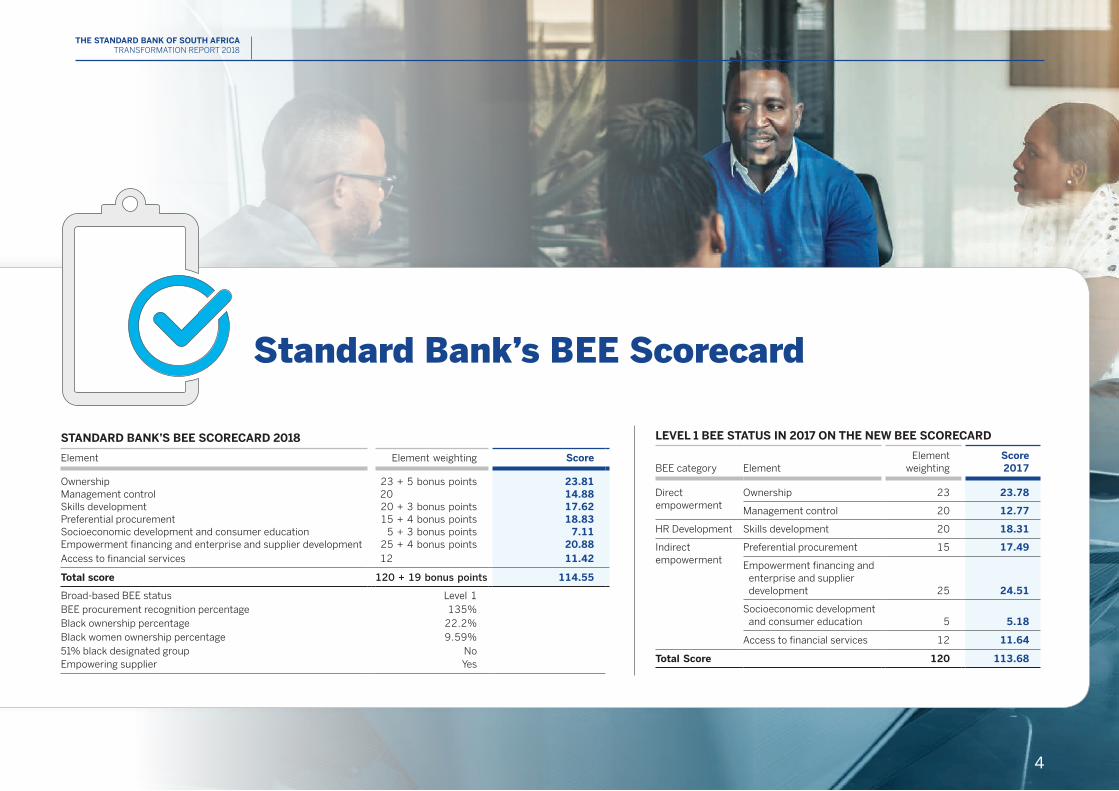

Standard Bank’s BEE Scorecard

STANDARD BANK’S BEE SCORECARD 2018

Element Element weighting Score

Ownership 23 + 5 bonus points 23.81Management control 20 14.88Skills development 20 + 3 bonus points 17.62Preferential procurement 15 + 4 bonus points 18.83Socioeconomic development and consumer education 5 + 3 bonus points 7.11Empowerment financing and enterprise and supplier development 25 + 4 bonus points 20.88Access to financial services 12 11.42

Total score 120 + 19 bonus points 114.55

Broad-based BEE status Level 1BEE procurement recognition percentage 135%Black ownership percentage 22.2%Black women ownership percentage 9.59%51% black designated group NoEmpowering supplier Yes

LEVEL 1 BEE STATUS IN 2017 ON THE NEW BEE SCORECARD

BEE category ElementElement

weightingScore2017

Directempowerment

Ownership 23 23.78

Management control 20 12.77

HR Development Skills development 20 18.31

Indirect empowerment

Preferential procurement 15 17.49

Empowerment financing and enterprise and supplier development 25 24.51

Socioeconomic development and consumer education 5 5.18

Access to financial services 12 11.64

Total Score 120 113.68

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

4

Ownership We scored 23.81 out of 28 points against the ownership element of the revised Financial Sector Code scorecard. This is an improvement against our score of 23.78 out of 28 points in 2017.

Who owns Standard Bank?Standard Bank’s shareholding is characterised by significant global and institutional ownership, reflecting our status as Africa’s largest financial services provider. Our shares are publicly traded on the Johannesburg Stock Exchange. Many of our shareholders are ordinary South Africans who own a stake in Standard Bank through their pension funds and unit trusts. Many of our employees are also shareholders. We allocate shares to senior employees as part of their remuneration package, helping to ensure that they have a vested interest in the long-term success of the company.

1 Beneficial holdings determined from the share register and investigations conducted on our behalf in terms of section 56 of the Companies Act.

Standard Bank’s largest shareholder is the Industrial and Commercial Bank of China (ICBC), the world’s largest bank, with a 20.1% stake.

RTS Read more about our 10-year anniversary with ICBC and our strategic partnership in our Reporting to Society.

The second largest shareholder is the South African Government Employee Pension Fund with 12.3%. There are other institutional investors in Standard Bank who are the custodians of the savings and investments of many ordinary South Africans.

TEN MAJOR SHAREHOLDERS1

Indicator description2018 number of shares (million)

%holding

2017 number of shares (million)

%holding

Industrial and Commercial Bank of China 325.0 20.1 325.0 20.1Government Employees Pension Fund (PIC) 199.7 12.3 199.6 12.3Allan Gray Balanced Fund 29.7 1.8 27.8 1.7Alexander Forbes Investments (prev. Investment Solutions) 25.8 1.6 28.3 1.8Old Mutual Life Assurance Company 23.8 1.5 19.7 1.2Vanguard Emerging Markets Stock Index Fund 22.1 1.4 23.8 1.5GIC Asset Management 21.0 1.3 18.3 1.1Vanguard Total International Stock Index Fund 19.4 1.2 16.5 1.0Dimensional Emerging Markets Value Fund 16.8 1.0 17.1 1.1Government of Norway 14.8 0.9 9.6 0.6

698.1 43.1 685.7 42.4

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

5

GEOGRAPHIC SPREAD OF SHAREHOLDERS

Indicator description2018 number of shares (million)

%holding

2017 number of shares (million)

%holding

South Africa 785.1 48.5 759.6 46.9Foreign shareholders 833.4 51.5 859.7 53.1

China 325.9 20.1 325.2 20.1United States of America 240.3 14.8 252.9 15.6United Kingdom 39.0 2.4 63.7 3.9Singapore 24.0 1.5 22.8 1.4Namibia 19.6 1.2 22.5 1.4Netherlands 15.6 1.0 15.0 0.9Norway 15.4 1.0 10.3 0.6Japan 15.0 0.9 13.7 0.8Ireland 13.3 0.8 20.9 1.3United Arab Emirates 12.2 0.8 7.8 0.5Hong Kong 12.0 0.7 10.8 0.7Canada 11.0 0.7 10.5 0.6Saudi Arabia 10.4 0.6 8.4 0.5Luxembourg 10.3 0.6 11.0 0.7Other 69.4 4.4 64.2 4.1

1 618.5 100.0 1 619.3 100.0

The Standard Bank Group black ownership initiative, Tutuwa, has delivered significant value for a broad base of stakeholders, including its beneficiaries and government, since the scheme unlocked at the beginning of 2015. Communities have also benefited directly from the scheme, particularly since 2016, through the Standard Bank Tutuwa Community Foundation. This non-profit foundation aims to help our young people achieve their full potential, by supporting their educational foundations, schooling development and their transition to the world of work, by creating innovative partnerships in these domains.

RTS For more information on the foundation, see page 64 to 65 of Standard Bank’s Reporting to Society.

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

6

OWNERSHIP

Management control

South Africa (SA) executive committee

Standard Bank scored 14.88 out of 20 for this element of the Financial Code in 2018. This is an improvement against our score of 12.77 out of 20 in 2017. Our score is calculated based on the membership of the SBSA board and South Africa executive committee, including Standard Bank Group executive committee members employed in SBSA. The score also measures the representation of black people, black women and African people across occupational levels.

LUNGISA FUZILEChief executive, SBSA

LIBBY KINGChief financial officer,

SBSA and head, finance operations

RENÉ DU PREEZGroup general counsel

JÖRG FISCHERGroup head of shared

services and real estate services

PEGGY-SUE KHUMALOChief executive,

Wealth, SA

ISABEL LAWRENCEGroup chief compliance

and data officer

DISEBO MOEPHULIChief executive, CIB SA

FUNEKA MONTJANE Chief executive, PBB SA

MYEN MOODLEY Head of human capital, SA

MIKE MURPHYChief information

officer, SA

THULANI SIBEKOGroup head marketing

and communication

NEIL SURGEYGroup chief risk officer and group ethics officer

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

7

The SBSA BoardEXECUTIVE DIRECTORS

13MEN

4WOMEN

LUNGISA FUZILE Chief executive, SBSA

SIM TSHABALALAChief executive, SBG

ARNO DAEHNKEChief financial officer,

SBG

THULANI GCABASHEChairman and independent

non-executive director

GERALDINE FRASER-MOLEKETI

Independent non-executive

director

HAO HUNon-executive

director

TRIX KENNEALY Independent

non-executive director

JACKO MAREENon-executive

director

NOMGANDO MATYUMZAIndependent

non-executive director

KGOMOTSO MOROKA

Non-executive director

MARTIN ODUOR-OTIENO

Independent non-executive

director

NON-EXECUTIVE DIRECTORS

ANDRÉ PARKER Independent

non-executive director

ATEDO PETERSIDE Independent

non-executive director

MYLES RUCK Independent

non-executive director

PETER SULLIVAN Independent

non-executive director

JOHN VICE Independent

non-executive director

LUBIN WANG Non-executive director

In 2018, our SBG CE Sim Tshabalala was awarded CEO of the decade by the Association of Black Securities and Investment Professionals (ABSIP), while The Standard Bank of South Africa won the award for the most transformed bank.

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

8

MANAGEMENT CONTROL

Top management

Senior management

Middlemanagement

Juniormanagement

We achieved our 2018 targets for the representation of black people and black women in senior, middle and junior management. Black people constituted the majority of promotions into all grades. However, African people are still under-represented in promotions into senior management and executive positions and progress in achieving equitable African representation at senior and middle management levels has been slower than we would like. The percentage of African people appointed into senior management roles (34%) decreased slightly in comparison to 2017 (37%). The proportion of black women appointed into senior management increased to 34%, from 22% in 2017.

SBSA – Black employees (South African citizens)

2016

2018

2017

88

%

71%

46

%ü

42

%ü

88

%

70%

43

%

34

%

87%

68

%

41%

22

%

Gender As part of our group-wide efforts to promote gender equity, we have set a target to increase the representation of women in executive

positions in Standard Bank South Africa from 32% in 2018 to 40% by 2021. See the skills

development chapter for more information about how we’re investing in developing women leaders.

Women in executive management positions (%) 32.2

Women in senior management positions (%) 39.4

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

MANAGEMENT CONTROL

9

Skills developmentSBSA scored 17.62 on the skills development element of the scorecard. This is slightly lower than the score of 18.31 we achieved in 2017, primarily due to spending on the training of unemployed black people being included under CSI rather than skills development, and a delayed start to some of our learnerships.

In 2018, we spent approximately 82% of our total skills development budget on the development of black employees across all levels of the organisation. Approximately 15% was spent at senior and executive management levels.

Standard Bank is committed to the development of leadership skills across the bank. In 2018, 4 920 SBSA employees attended leadership and management development programmes. Almost 75% of these employees were black, and 41% were black African.

We encourage our employees to stay up to date with developments in their various fields of work, to develop their professional skills and where appropriate to pursue additional formal qualifications. The bank offers bursaries to all employees who meet set criteria. We have implemented an online system to facilitate the application process. In many instances our employees pursue specialist qualifications, but we have also seen a significant uptake in post-graduate qualifications, and MBAs in particular. We awarded 1 555 staff bursaries in 2018, valued at approximately R38.1 million.

Standard Bank’s graduate programme provides an entry-point to the corporate world for university graduates. 194 graduates joined the programme in 2018, of whom 91% were black.

We offer learnerships for matriculants and graduates, which provide young people from disadvantaged backgrounds with an opportunity to work in the bank and learn about different aspects of our business. Each learner is assigned a coach, mentor and line manager who are there to provide ongoing support and give the learner as much opportunity as possible to succeed. On completion of the programme (12 to 18 months), participants receive a nationally recognised qualification and where possible, are absorbed into the organisation. In 2018, 815 unemployed people started a learnership or internship programme with the bank, 99% of whom were black, and 87% of whom were black African. At the end of 2018, 64% of learners who completed their learnership were offered additional work opportunities, be it on an internship, fixed-term contract or in a permanent role.

From 2019, SBSA is participating in the YES initiative, a joint programme between government and business that aims to place unemployed young people in training programmes, learnerships and jobs, to support sustainable work readiness and skills development. We have adapted some of our existing learnership programmes to accommodate YES participants.

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

10

201891%

201789%

2018 2017 2016

Leadership training and graduate programmes

SBSA leadership training – total number of employees 4 920 3 543 2 460

SBSA leadership training – % of black attendees 74.8ü 67.5 67.0

SBSA leadership training – % of black African attendees 41.0 34.8 na

SBSA learnership/graduate programmes – total number of employees 1 009 924 1 037

SBSA graduate programmes – % of black attendees 91 89 81

SBSA graduate programmes – % of black African attendees 75 40 na

SBSA Leadership Training

% of black attendees

201874.8%ü

201767.5%

SBSA graduate programmes

% of black attendees

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

11

SKILLS DEVELOPMENT

Preferential procurement

We are committed to advancing job creation and economic transformation by opening opportunities in our supply chain to black-owned suppliers and small enterprises. We have revised our preferential procurement and supplier development policy to better support transformation and inclusion within our supply chain. We work with potential and current suppliers to identify appropriate opportunities, and we provide successful candidates with business development support. We also provide suppliers who meet specific criteria with access to finance where needed.

In 2018 SBSA achieved 14.94 out of 15 points for procurement, with 3.90 out of 4 bonus points. We exceeded our internal minimum targets and FSC targets, with the exception of the qualifying small enterprise (QSE) category. Spend with black-owned suppliers has increased over the past three years, from R3.4 billion in 2016, to R4.1 billion in 2017, and R5.1 billion in 2018, in actual rand terms and spend. We have exceeded our target for procurement spend with BBBEE compliant companies. 35% of our procurement spend is with black-owned companies and 22% directed to black women-owned companies. The percentages on the different spend categories is based on weighted spend on the bank’s preferential procurement scorecard.

We scored 18.83 out of 19 for preferential procurement. This is a significant improvement against our score of 17.49 out of 19 in 2017 and reflects the bank’s increased investment in procuring from black and black women-owned qualifying suppliers.

We are working with suppliers to improve their BBBEE status. We’re in the process of engaging with all our non-BBEEE-compliant suppliers, asking them to provide us with their BBBEE Improvement Plans, detailing their plans to transform their businesses. This consultation is yielding positive results. We’ve also developed a strategy to identify opportunities where procurement spending can be shifted from non-compliant suppliers, who currently constitute 48% of Total Measured Procurement Spend, to black-owned small and medium enterprises (SMEs).

Our efforts to diversify our supply chain include a specific focus on black-owned small and medium enterprises. In 2018, 17% of Total Measured Procurement Spend (TMPS) for preferential procurement initiatives was with black-owned SMEs, and 8% with black women-owned SMEs.

We have pioneered a supplier development programme that aims to improve economic participation of black-owned SMEs into our supply chain, by providing them with business development support services together with tailored financial solutions. The business development support available to participants ranges from coaching and mentoring to technical training. During 2018, 109 suppliers participated in our supplier development programme. 65 of these suppliers received procurement opportunities worth almost R198 million.

The Standard Insurance Limited (SIL) team, which provides a wide range of short-term insurance solutions, is committed to using locally based, black-owned enterprises to service customer claims. We’re growing our stable of black-owned small businesses, from panel beaters and electricians to plumbers and builders, and bringing these small enterprises into our formal supply chains.

We have exceeded our target for procurement from BBBEE-compliant insurance service providers. During 2018, SIL and supplier development engaged with suppliers through supplier roadshows across the country. We also onboarded 400 service providers to our digital platform. The aim of these engagements was to raise awareness among the suppliers on our SIL panel of supplier development opportunities, and to hear directly from them about the kinds of support and information they need from us. One recent success story is that of a small black-owned supplier who manufactures and distributes electric geysers, who is now part of Standard Bank’s supplier database. From November 2018, this business will supply about 30% of SIL’s electric geyser requirements to the customer base. SIL’s leadership team worked closely with group procurement to ensure the successful fulfilment of this partnership and continues to work on developing similar partnerships.

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

12

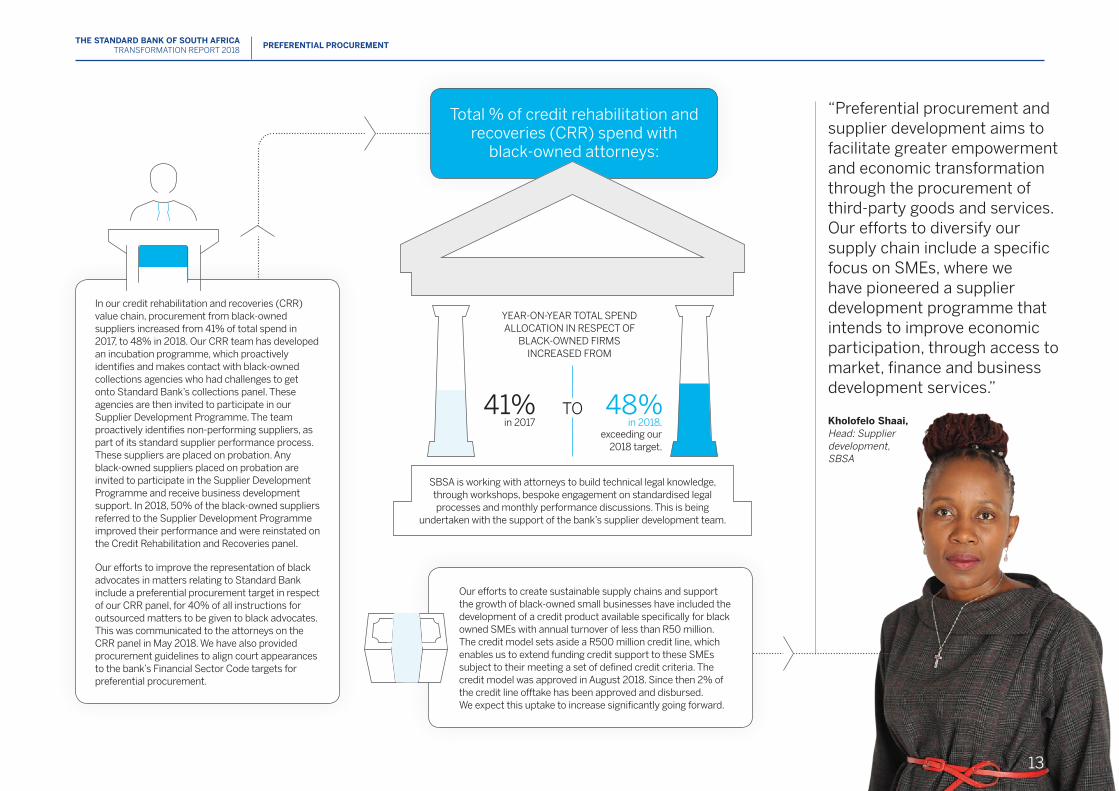

Total % of credit rehabilitation and recoveries (CRR) spend with

black-owned attorneys:

41%

SBSA is working with attorneys to build technical legal knowledge, through workshops, bespoke engagement on standardised legal processes and monthly performance discussions. This is being

undertaken with the support of the bank’s supplier development team.

YEAR-ON-YEAR TOTAL SPEND ALLOCATION IN RESPECT OF

BLACK-OWNED FIRMS INCREASED FROM

in 2017TO 48%

in 2018,exceeding our

2018 target.

In our credit rehabilitation and recoveries (CRR)value chain, procurement from black-owned suppliers increased from 41% of total spend in 2017, to 48% in 2018. Our CRR team has developed an incubation programme, which proactively identifies and makes contact with black-owned collections agencies who had challenges to get onto Standard Bank’s collections panel. These agencies are then invited to participate in our Supplier Development Programme. The team proactively identifies non-performing suppliers, as part of its standard supplier performance process. These suppliers are placed on probation. Any black-owned suppliers placed on probation are invited to participate in the Supplier Development Programme and receive business development support. In 2018, 50% of the black-owned suppliers referred to the Supplier Development Programme improved their performance and were reinstated on the Credit Rehabilitation and Recoveries panel.

Our efforts to improve the representation of black advocates in matters relating to Standard Bank include a preferential procurement target in respect of our CRR panel, for 40% of all instructions for outsourced matters to be given to black advocates. This was communicated to the attorneys on the CRR panel in May 2018. We have also provided procurement guidelines to align court appearances to the bank’s Financial Sector Code targets for preferential procurement.

Our efforts to create sustainable supply chains and support the growth of black-owned small businesses have included the development of a credit product available specifically for black owned SMEs with annual turnover of less than R50 million. The credit model sets aside a R500 million credit line, which enables us to extend funding credit support to these SMEs subject to their meeting a set of defined credit criteria. The credit model was approved in August 2018. Since then 2% of the credit line offtake has been approved and disbursed. We expect this uptake to increase significantly going forward.

“Preferential procurement and supplier development aims to facilitate greater empowerment and economic transformation through the procurement of third-party goods and services. Our efforts to diversify our supply chain include a specific focus on SMEs, where we have pioneered a supplier development programme that intends to improve economic participation, through access to market, finance and business development services.”

Kholofelo Shaai, Head: Supplier development, SBSA

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

13

PREFERENTIAL PROCUREMENT

Socioeconomic developmentStandard Bank focuses our socioeconomic development investment in education, with the objective of enhancing access to quality education for all, from early childhood development to higher education, and improving educational outcomes. We also invest in arts, culture and sports development. In 2018, our total investment in socioeconomic development initiatives (our corporate social investment spending) amounted to R141.2 million. Of this amount, education spend accounted for just under R96.6 million, or about 68% of the total.

Early childhood developmentExtensive empirical research has demonstrated that developmental stimulation during the earliest years of childhood are critical to future intellectual, emotional and physical wellbeing. In South Africa, Standard Bank supports early childhood development (ECD) through a number of targeted initiatives that upskill ECD practitioners to a level at which they can achieve a certified qualification, which enables them to register their ECD centres with the Department of Social Development.

A

BC

Socioeconomic development and consumer educationWe scored 7.11 out of 8 for the socioeconomic development and consumer education pillar. This is a significant improvement in comparison to 5.18 out of 8 points in 2017. This element measures the annual value of the bank’s qualifying socioeconomic development contributions as a percentage of net profit after tax (NPAT), together with the annual value of all qualifying consumer education contributions as a percentage of NPAT of our retail business (PBB SA). The Financial Sector Code requires us to spend 0.6% of NPAT on socioeconomic development, and 0.4% of retail (personal and business banking) NPAT on consumer education. In 2018, Standard Bank’s total spend on socioeconomic development was 0.88% of NPAT and spend on consumer education was 0.42% of retail NPAT.

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

14

Participation of 50 learners from six schools in three provinces in the Wits University Targeting Talent Programme, which engages with learners from Grade 10 through to 12 to support university readiness.

Ongoing participation in the National Education Collaboration Trust, a collaboration between businesses, labour, civil society and government to influence and support the implementation of government’s education reform agenda in primary and secondary schools.

Foundation skillsWithout a solid grounding in numeracy, literacy and life-skills in the foundation phase of schooling, children will struggle to perform to their full potential in further schooling and higher education. Standard Bank corporate social investment (CSI) works in partnership with a range of organisations across seven provinces to improve the teaching of foundation skills through a focus on upskilling teachers in numeracy, literacy and life-skills teaching, largely though in-classroom mentoring by skilled and experienced retired educators. In some instances, the mentoring is supplemented with workshops, the provision of learner workbooks and literacy workshops for parents.

School level education Our focus is primarily on supporting the teaching of mathematics and science through teacher upskilling, Saturday school programmes and other programmes which aim to prepare high-school learners for tertiary education through a focus on academic support together with leadership skills, self-mastery and study skills. In 2018, we invested in:

We also fund the Little African Scientist Project, which forms part of the teacher development programme run by the Faculty of Education at North West University. It aims to support foundation phase teachers in mathematics and science education.

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

15

SOCIOECONOMIC DEVELOPMENT AND CONSUMER EDUCATION

Funding higher educationStandard Bank aims to improve access to student funding for tertiary education. Initiatives in this area include our crowdfunding Feenix platform, together with direct funding through Standard Bank bursaries and scholarships.

We launched the Feenix Trust, an NPO, in June 2017. It is an initiative that allows individuals and enterprises to donate money directly to students to help them complete their studies. Crowdfunding platforms like Feenix allow ordinary citizens to take meaningful action to solve social problems, with 75% of the fund allocated to black recipients, and 50% to women. Standard Bank is a funder, enabler and partner of the trust, which retains and manages funds from donors. The trust allows individuals and enterprises to donate money to universities on behalf of selected students.

We covered the set-up costs and will cover any shortfall between the total operating costs and the income received from the admin fee charged to funders. We have a three year commitment to the project, which we expect to become self-sustaining. Feenix has raised R22 million thus far, providing support for 800 tertiary students, funding 650ü students in 2018. Standard Bank employees have contributed R850 000 of this amount. The Feenix Trust owns the Feenix.org domain, ensuring professional and accountable handling of all funds raised and disbursed. Feenix won the Public Intellectual Influencer Brand Award at the 2018 Brand Summit South Africa and was recognised by Next Generation in their 2018 Innovation and Impact Research Report as a leader of the pack.

Our bursary programmes support deserving students to obtain degrees in critical skills areas. In 2018, we funded 296 bursaries for students at South African universities, to the value of R35.7 million. Standard Bank directly awarded and managed 130 of these bursaries and 166 were funded through the Ikusasa Financial Aid Programme (ISFAP). ISFAP is a public-private partnership between government and corporates, aimed specifically at addressing the funding gap for the so-called ‘missing middle’.

In 2018, 12 of our bursary recipients who graduated in 2017 were employed by Standard Bank.

RTS To read more about a few of these individuals, see our Reporting to Society, page 62.

Standard Bank and the University of Johannesburg have partnered to support ten exceptional students through their undergraduate and post-graduate studies, through the Actuationist programme. Two of these students started their careers at Standard Bank in 2019.

Feenix crowdfunding platform

enables individuals and companies to donate money directly to universities

on behalf of selected students.

Standard Bank covered set-up and operating cost shortfalls.

TM

THE SOLUTION

Raised over R22 million

650 studentsfunded in 2018Student access

to funding.

THE CHALLENGE

THE IMPACT

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

SOCIOECONOMIC DEVELOPMENT AND CONSUMER EDUCATION

16

Standard Bank provides funding to support the development of cricket in South Africa. In 2018, we provided R9.3 million in support of cricket development (rights and leverage costs). We partner with Cricket South Africa to support the development of young cricketers at school level. We recognise that to support integration, and transform the sport at national team level, we need to address inequalities in the foundation feeder system.

Sports sponsorship

In 2018, we sponsored 12 regional performance centres (RPC) across the country, all in previously disadvantaged areas, to grow the pipeline of future stars. The RPC programme focuses on players aged between 13 and 18. To date 144 talented young cricketers from all over South Africa have benefited.

We also sponsor the Ironman programme, and invested R250 000 to support Siyaphambili, a triathlon development participation programme.

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

17

SOCIOECONOMIC DEVELOPMENT AND CONSUMER EDUCATION

In 2018 we celebrated 20 years of our sponsorship of the Standard Bank Joy of Jazz which was held in Johannesburg. The sponsorship investment of R17 million includes hospitality for the artists, marketing, production expenses, payment to the artists, and funding for development projects. Our production partner for the event, T Musicman CC, is 100% black owned and other beneficiaries of the funding are 90% black. The festival contributes over R80 million to Gauteng’s GDP and approximately 3 119 jobs were created.

Arts sponsorship Standard Bank supports a range of initiatives to nurture young talent and showcase the rich diversity of our creative arts. We’re proud to provide ongoing support for a variety of major arts events, which have become highlights of South Africa’s cultural calendar.

In 2018, we sponsored the National Arts Festival to the value of R11.1 million. The festival contributes around R377 million to the Eastern Cape’s GDP, and R94 million to the GDP of Makhanda, previously the city of Grahamstown. Our sponsorship included funding for:

The Standard Bank Young Artist Award programme – four of the six winners were black artists

The Creativate Digital Arts Festival – five of 33 events (15%) involved black artists/exhibitors/lecturers

The Standard Bank Ovation Awards – 19 of the 34 winning productions (56%) were produced or performed by black artists

Standard Bank Village Green project (craft market) – 62% of the 329 stall-holders were black, and 20% came from rural areas

The Children’s Arts Festival – our funding enabled 84 children to participate in the programme. 80% of the participating children were black, as were 76% of the children who participated in the boarding programme

The Standard Bank Jazz Festival in Makhanda, including one of the biggest jazz development programmes in South Africa, the Standard Bank National Youth Jazz Festival. 319 students participated in the youth programme, of whom 47% were black beneficiaries. 77% of the 94 musicians that participated in the festival were black.

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

SOCIOECONOMIC DEVELOPMENT AND CONSUMER EDUCATION

18

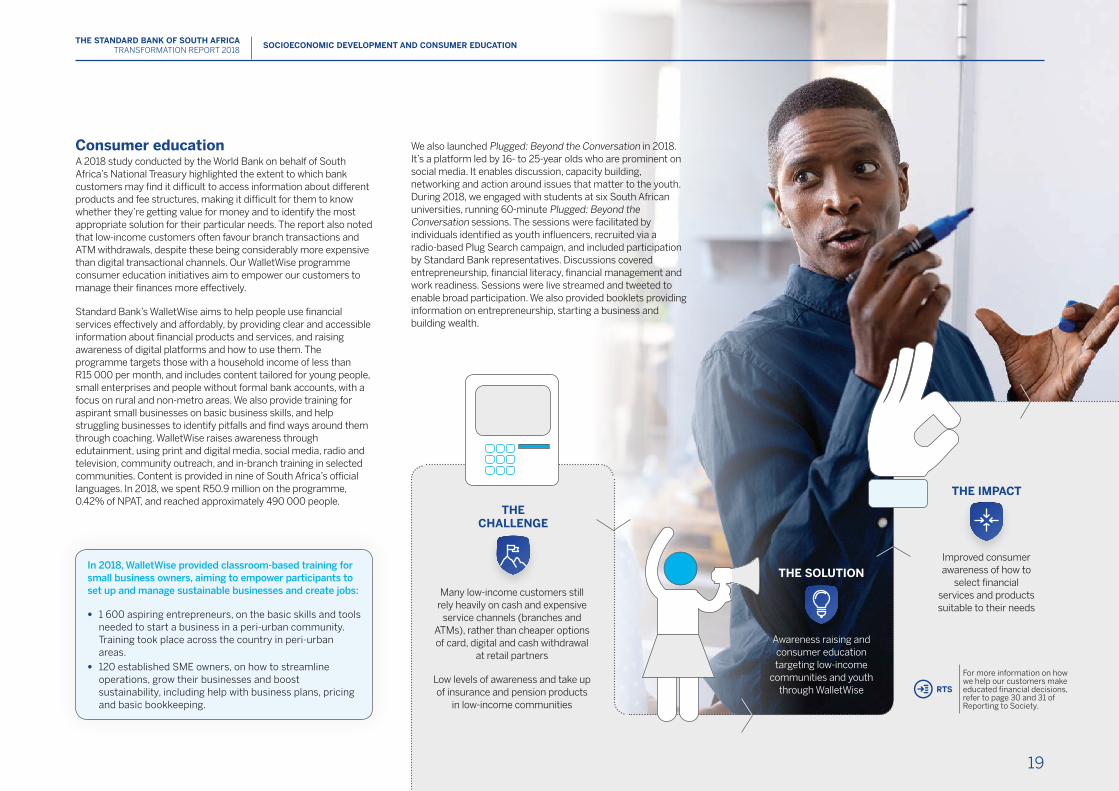

Consumer education A 2018 study conducted by the World Bank on behalf of South Africa’s National Treasury highlighted the extent to which bank customers may find it difficult to access information about different products and fee structures, making it difficult for them to know whether they’re getting value for money and to identify the most appropriate solution for their particular needs. The report also noted that low-income customers often favour branch transactions and ATM withdrawals, despite these being considerably more expensive than digital transactional channels. Our WalletWise programme consumer education initiatives aim to empower our customers to manage their finances more effectively.

Standard Bank’s WalletWise aims to help people use financial services effectively and affordably, by providing clear and accessible information about financial products and services, and raising awareness of digital platforms and how to use them. The programme targets those with a household income of less than R15 000 per month, and includes content tailored for young people, small enterprises and people without formal bank accounts, with a focus on rural and non-metro areas. We also provide training for aspirant small businesses on basic business skills, and help struggling businesses to identify pitfalls and find ways around them through coaching. WalletWise raises awareness through edutainment, using print and digital media, social media, radio and television, community outreach, and in-branch training in selected communities. Content is provided in nine of South Africa’s official languages. In 2018, we spent R50.9 million on the programme, 0.42% of NPAT, and reached approximately 490 000 people.

Improved consumer awareness of how to

select financial services and products suitable to their needs

THE SOLUTION

THE IMPACT

Many low-income customers still rely heavily on cash and expensive

service channels (branches and ATMs), rather than cheaper options of card, digital and cash withdrawal

at retail partners

Low levels of awareness and take up of insurance and pension products

in low-income communities

Awareness raising and consumer education targeting low-income

communities and youth through WalletWise

THE CHALLENGE

In 2018, WalletWise provided classroom-based training for small business owners, aiming to empower participants to set up and manage sustainable businesses and create jobs:

•• 1 600 aspiring entrepreneurs, on the basic skills and tools needed to start a business in a peri-urban community. Training took place across the country in peri-urban areas.

•• 120 established SME owners, on how to streamline operations, grow their businesses and boost sustainability, including help with business plans, pricing and basic bookkeeping.

We also launched Plugged: Beyond the Conversation in 2018. It’s a platform led by 16- to 25-year olds who are prominent on social media. It enables discussion, capacity building, networking and action around issues that matter to the youth. During 2018, we engaged with students at six South African universities, running 60-minute Plugged: Beyond the Conversation sessions. The sessions were facilitated by individuals identified as youth influencers, recruited via a radio-based Plug Search campaign, and included participation by Standard Bank representatives. Discussions covered entrepreneurship, financial literacy, financial management and work readiness. Sessions were live streamed and tweeted to enable broad participation. We also provided booklets providing information on entrepreneurship, starting a business and building wealth.

RTS

For more information on how we help our customers make educated financial decisions, refer to page 30 and 31 of Reporting to Society.

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

19

SOCIOECONOMIC DEVELOPMENT AND CONSUMER EDUCATION

Empowerment financing and enterprise and supplier development Businesses, large and small, require access to finance to expand their operations and improve productivity. Accessing finance enables them to access supply chains and equipment and as well as access new markets, creating jobs but also boosting profitability. We scored 20.88 out of 25 for the empowerment financing and enterprise development element. This is below our score of 24.51 out of 29 in 2017. New targets for empowerment financing have been agreed at the Banking Association of South Africa (BASA). The Financial Sector Transformation Council (FSTC) is expected to issue an updated guidance note that reflects these targets.

Empowerment financing Standard Bank continues to drive economic transformation through empowerment financing. We have been involved in several major transactions over the past year, which have increased economic participation by black people and led to the creation of new companies and jobs. We have also contributed significantly in the funding of critical infrastructure required for driving economic growth. Transactions include:

•• The financing of several renewable energy projects under the fourth round of South Africa’s renewable energy independent power producers programme (REIPPP), lending to municipalities, and lending to state owned enterprises responsible for economic infrastructure. (See our Reporting to Society for details.)

•• Advised on, structured and part-financed a major black economic empowerment deal for the South African National Taxi Council (SANTACO). The R1.7 billion deal enabled Santaco to acquire a 25% stake in SA Taxi, a subsidiary of Transaction Capital that specialises in sales, financing and insurance of minibus taxis. The deal will benefit thousands of taxi operations and drivers, enabling SANTACO to expand into higher margin upstream sectors, including vehicle sales, finance, and insurance.

•• Financed Seriti Resources’ acquisition of Anglo American’s Eskom-supplying coal assets. Seriti is a 91% black owned and controlled South African mining company. The acquisition makes Seriti Eskom’s largest black-controlled coal supplier.

•• Facilitated the merger of Peregrine Securities and Legae Securities (South Africa’s oldest stockbroker), resulting in the formation of Legae Peresec and creating the largest stockbroker on the JSE.

•• Facilitated Afropulse Group’s subscription of 25% of the share capital in Imperial Logistics Advance, making Imperial Logistics Advance the only 100% black-women owned company in the logistics industry.

•• Provided funding for AdaptIT for a pipeline of acquisitions.

•• Structured an acquisition finance facility for the African Pioneering Group (APG), enabled it to acquire the remaining shares in Pioneer Fishing.

Enterprise development Entrepreneurs and start-ups struggle to access finance to get off the ground. Many start-ups fail within the first two years, making them a risky proposition for credit providers. We’re working with our small enterprise clients to develop financial and business support solutions in ways that meet their needs and support growth in this crucial sector while minimising risk to the bank.

During 2018, we invested R38.6 million on enterprise development projects and a rand equivalent of R87.2 million on supplier development. We also worked to create better coordination of our combined enterprise and supplier development programmes.

For example, we’ve signed a cooperation agreement with the Limpopo Provincial Treasury in South Africa to provide access to funding for SMEs who have secured government contracts but lack the finance to execute such projects. We have committed R300 million ($21.4 million) over three years to this initiative. Funding includes a short-term/once off revolving facility, for suppliers undertaking work valued below R500 000; and short, medium-term and asset finance for contracts above R500 000.

SBSA’s Tshwaranang Trust, established in 2016 as a means to provide collateral against which to extend loans to small businesses, experienced a rising default rate during 2018. Concerns were also raised by the relevant regulator regarding the use of a trust mechanism as a means of disbursing enterprise development funds. We have undertaken an extensive review of the model, drawing on the lessons learned to develop better ways of enabling access to finance for SMEs that lack collateral or surety.

Standard Bank’s agribusiness transformation programme develops black commercial farmers and black owned agribusinesses to contribute to the transformation and economic viability of the agricultural sector in the Free State, support job creation and improve food security. Objectives include developing black sustainable commercial farmers, developing sustainable secondary agribusinesses, cultivating mutually beneficial relationships amongst stakeholders, strengthening agricultural training and development networks in Africa, improving academic programme and graduate employability. We aim to develop a model replicable across South Africa and potentially in other African countries.

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

20

Since 2013 we have helped over

189 000 historically disadvantaged

customers register R108 billion in home loans

In 2018 we registered

R20.5 billion in loans for historically

disadvantaged customers, a 16% increase on the prior year

Enabling home ownership to improve financial inclusionHelping people buy a home is one of the most important roles we play in society. A home provides shelter and dignity for families and provides an opportunity to build inter-generational wealth. Standard Bank is a major provider of home loans in South Africa, with a 34% market share.

Since 2013, we have helped over 103 000 women register R73.2 billion in home loans,

of which R13 billion were registered in 2018, an 11% increase on the prior year

Affordable housingThe Financial Sector Coderequires banks to provide funding/loans for affordable housing for consumers that earn a gross income between R3 500 and R23 300. Standard Bank’s Affordable Housing book is valued at around R25 billion. As the largest lender in the affordable housing sector, we have assisted 96 359 customers to purchase a new home since 2008. We work closely with the Department of Human Settlements to enable access to finance, and access to information to support responsible debt management. In 2018, we helped 4 958 South African affordable housing customers purchase a home.

We offer our affordable housing mortgage customers online or classroom-based training to help manage their home ownership obligations. Training is provided by external service providers and funded by the bank. In 2018, 726 customers participated in the programme.

Despite South Africa’s tough economic conditions, 88% of our affordable housing customers are keeping up with their repayments. We’re working with 7% of our customers who are showing signs of struggling to service their home loan to get back on track, providing them with alternative options that include a pause on their loan, an extension on the loan terms or a reduced repayment. In 2018, 2 054ü home loans were restructured to keep families in their homes.

Total number of home loans on our books: 538 195

accounts to the value of

R306 billion

In 2018, 2 054 home loans were restructured to keep families in their homes

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

21

EMPOWERMENT FINANCING AND ENTERPRISE AND SUPPLIER DEVELOPMENT

We do everything we can to help our customers stay in their homes. However, in 2018, we regrettably had to enter legal processes with 5% of our customers who were in default, after all alternative arrangements had been exhausted. Over the past two years, we have undertaken a wide range of engagements with government officials, members of parliament, and civil society groups to gain a better understanding of what we as a bank can do to try to prevent mortgage defaults. Our group social and ethics committee has mandated various areas within the bank to communicate more proactively with stakeholders regarding the processes followed in cases of default, and the various options available to customers, including loan restructuring and assisted sales. We have also increased our focus on ensuring the courts have the relevant information on steps taken to try to assist clients in distress prior to taking the matter to court. We continue to work with National Treasury, Lungelo Lethu Human Rights Foundation and other relevant stakeholders to try to develop practical and sustainable solutions. We recognise the need to provide more regular, user-friendly communication to customers, to better support understanding of their rights and responsibilities, and how they can access assistance when payments first fall behind. We’re working with Lungelo Lethu to improve our communication in this regard.

KEEPING PEOPLE IN THEIR HOMES: THE LEGAL PROCESS WE FOLLOW WHEN CLIENTS FALL BEHIND ON THEIR MORTGAGES

Sale cancelled

Property sold to third party

Bank buy-in property in possession (PIP)

a. A Section 129 notice is the first step in the legal process when one has defaulted on a loan repayment. It is the notice issued in terms of Section 129 of the National Credit Act (NCA), advising a consumer that they are in arrears of a certain amount in unpaid instalment(s) at a given date. A credit provider, or an attorney appointed by the credit provider, may issue notice according to Section 129 of the NCA at any time after the client has been in arrears for more than 20 business days. The credit provider may not proceed with any legal action without having fully complied with NCA requirements as contemplated in Sections 129 and 130.

b. An order to appear before a judge or magistrate. c. Decision by the court. d. The transfer of the property to the creditor or the sale of such property to recover outstanding debt.

Throughout the collections and legal action processes, banks allow consumers to make use of rehabilitation options and/or assisted sales to prevent the occurrence of a sale in execution (SIE). These options slow the typical SIE process down from – on average – 16 months to 29 months.

29MONTHS

Shortfall

Debt review

Early stage

Late stage

S129 noticea

Collections

3MONTHS

6MONTHS

7MONTHS

Summonsb

Judgementc

Attachmentd

9MONTHS

12MONTHS

16MONTHSLegal

action

Sale in execution(SIE)

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

22

EMPOWERMENT FINANCING AND ENTERPRISE AND SUPPLIER DEVELOPMENT

Digital solutions to expand financial access Standard Bank is committed to finding new ways to extend access to financial services to the most under-served and unbanked individuals, entrepreneurs, and small enterprises. We aim to provide banking products and services that deliver what really matters to these customers: safety and security, convenience and affordability.

Standard Bank’s digital wallets and apps, including Instant Money and SnapScan, enable our customers to transact efficiently, safely and conveniently.

•• Instant Money is a safe, affordable and reliable way to send money, even if neither the sender nor receiver have a bank account. Money can be sent instantly from an ATM, via the banking app, online banking, cellphone banking or through our retail partners, and is delivered instantly. Instant Money currently has over 4.9 million users in South Africa, of whom over 3.2 million are Standard Bank customers.

•• Instant Money Wallet provides a pay as you go transactional option, and allows users to receive, store and send money and to make purchases. There is no cost for sending money between wallets, making it convenient and cost effective for customers to transact with one other. Users of the service can also buy electricity and airtime on their phones.

•• Instant Money Bulk Payments enables businesses to transact efficiently and conveniently, eliminating the need to deal in cash and thereby reducing security risks. Businesses can make digital payments to employees, even if employees don’t have bank accounts. It also provides a convenient payment mechanism for small businesses to make payments to suppliers and service providers who may not have formal bank accounts.

Access to financial servicesFinancial inclusion is related to economic growth, efficiency, dignity and welfare. Low levels of financial inclusion undermine the integrity of the financial system and pose a risk to socioeconomic development. South Africa’s government has taken many steps to adjust the regulatory framework in a way that supports greater financial inclusion. This has included making the National Payments System accessible to a broader range of players, including non-bank payment providers. Recent proposals for regulatory reform in the insurance sector include measures that are aimed at facilitating new entrants, as well as new insurance products for lower income customers.

The revised Financial Sector Code continues to score access according to ‘service points’ and ‘transaction points’, in addition to ‘sales points’ and ‘electronic access’. Standard Bank is under target on the first two measures, and well over target on the electronic access measure. This is indicative of behaviour shifts by increasing numbers of South Africans, who are choosing digital channels over face to face options to conduct their financial transactions. During 2018, for example, Standard Bank customer’s digital transactions volumes (including online and mobile banking) increased by 34%, while teller-based transactions declined by 14%. The measures contained within the FSC Code do not yet reflect this shift.

We scored

11.42 out of 12

for access to financial services.

This is much

the same as last

year’s score, of

11.64 out of 12.

THE STANDARD BANK OF SOUTH AFRICA TRANSFORMATION REPORT 2018

23

standardbank.com

Where to find more information For more information about the ways in which Standard Bank is impacting on the

economies and societies in which we operate, please visit our Report to Society website. For detailed information on our material issues, and our performance against our five value drivers, please refer to the Standard Bank Group’s Annual Integrated Report.