treasury centralization at dover corporation€¦ · treasury centralization at dover corporation...

TRANSCRIPT

Treasury Centralization

At Dover Corporation

Garrett Jenks

Risk Manager

Robert Chan

European Treasurer

Agenda

Dover Corporation

Banking Services

Foreign Exchange Procurement

Closing

Presentation Objective

To support this effort, we will focus on two primary topics:

Banking Services Foreign Exchange

Procurement

The objective of today’s presentation is to provide insight into Dover’s experience centralizing core

treasury functions

Dover Corporation

• Diversified global manufacturer with annual revenues greater than $8 billion

• Focused on 4 business segments: – Communication Technologies

– Energy

– Engineered Systems

– Printing and Identification

– Consists of 32 operating companies world-wide

• Strong Financials – Fortune 500 company

– Single A credit rating

• Entrepreneurial business model that encourages, promotes and fosters deep customer engagement and industry-leading product innovation

Treasury Prior to 2012

• Treasury supported investor relations

• Treasury related practices varied by

operating company with decision

making at the local level

• Limited corporate view of bank fees

and expenses

Treasury Organization

• Dover decided to split the Treasury and Investor Relations functions

• In late 2011, Dover hired a new Treasurer

• He expanded the Treasury team to include resources dedicated to operations and risk management

Treasurer

Senior

Analyst

Treasury Manager,

Americas

Treasury

Risk Manager European

Treasurer

Risk

Analyst

Treasury’s Main Priorities

• Ensure funding to facilitate global

growth

• Secure financial services with prices

commensurate for a large MNC

• Managing the financial risk profile of

Dover

• Bank and rating agency relationship

management

Dover Treasury Goals and Behaviors

Improve the Efficiency of Processes Around Cash &

Financial Transactions

Strengthen Internal Controls Around Cash

& Financial Transactions

Manage Dover’s Financial Risk Profile

Lower the Costs of Financial Transactions

Behaviors Operate Ethically

Be Proactive Collaborate

We will not sacrifice one goal

in order to achieve another.

Agenda

Dover Corporation

Banking Services

Foreign Exchange Procurement

Closing

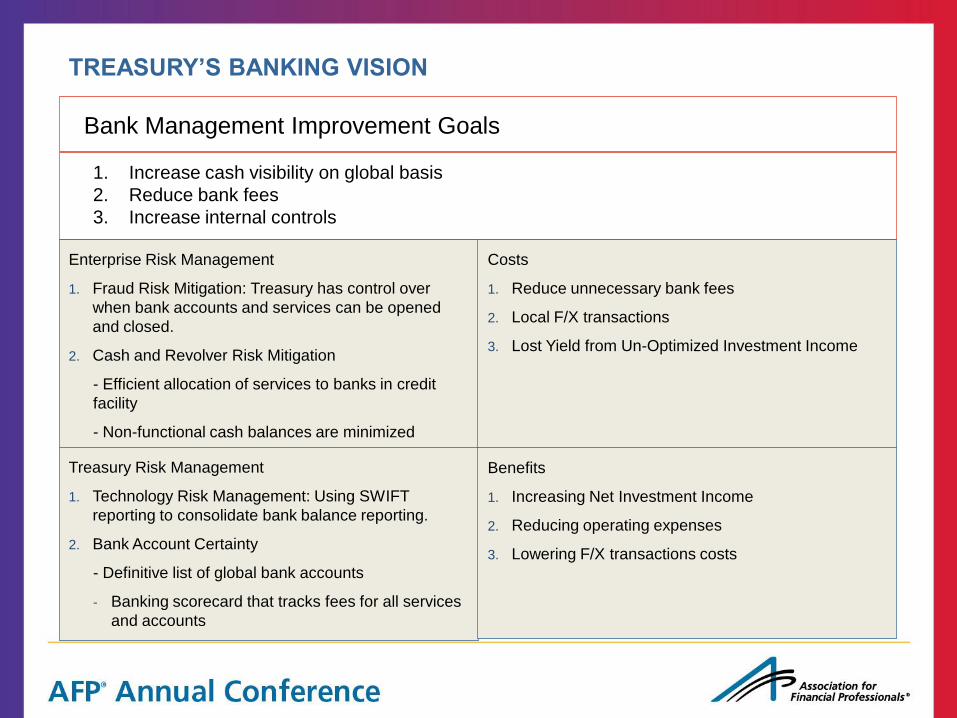

Enterprise Risk Management

1. Fraud Risk Mitigation: Treasury has control over

when bank accounts and services can be opened

and closed.

2. Cash and Revolver Risk Mitigation

- Efficient allocation of services to banks in credit

facility

- Non-functional cash balances are minimized

Costs

1. Reduce unnecessary bank fees

2. Local F/X transactions

3. Lost Yield from Un-Optimized Investment Income

Bank Management Improvement Goals

1. Increase cash visibility on global basis

2. Reduce bank fees

3. Increase internal controls

Treasury Risk Management

1. Technology Risk Management: Using SWIFT

reporting to consolidate bank balance reporting.

2. Bank Account Certainty

- Definitive list of global bank accounts

- Banking scorecard that tracks fees for all services

and accounts

Benefits

1. Increasing Net Investment Income

2. Reducing operating expenses

3. Lowering F/X transactions costs

TREASURY’S BANKING VISION

Cash Efficiency and Credit Risk

• Non-functional cash balances are left in surplus

positions

• Inefficient allocation of cash management business

to relationship banks

Technology Risk

• Heavy reliance on manual data collection and

process

• Key personnel risk: manual processes makes

treasury reliant on personnel with specialized

knowledge of process

IDENTIFYING RISK OF DECENTRALIZED ACCOUNTS

Risk to Enterprise and Treasury

Fraud Risk

Local operating companies have discretion over opening

and closing of bank accounts and cash management

services allowing for potential bank related fraud.

Bank Group Risk

• Control of how local accounts are managed (i.e.

open and closed)

• Potential for fees unknowingly increase

Enterprise Risk Treasury Risk

CALCULATING COSTS OF BANK FEES

Typical approaches for Quantifying Costs of Bank Fees

1. Total Annual Bank Fees Paid

Bank fees could be rising with additional revenues or could be due to industry-wide fee-to-

service trends.

2. Fee-to-volume Ratio

Too granular for senior level attention

3. Fee-to-services Provided Ratio

Too granular for senior level attention

4. Total Fees Compared to Industry Peers

Comparison of fees does not pinpoint where Dover Treasury can take action.

Step 1: Build a compelling business case to engage senior

management.

One-time

• Ensure that senior management is aware of and supports

Treasury’s bank account rationalization efforts

BANK ACCOUNT REVIEW PROCESS

Steps to Control and Manage Bank Accounts

Step 3: Interview Account Owners

Semi-annually

• Interview/email each account owner to confirm list of global

accounts, services and fees paid

• Create master database list of accounts to be confirmed

Step 2: Schedule Information Gathering

Annually

• Schedule time with each operating company

• Frame conversation as supporting the units with necessary cost

reductions

Step 4: Track Accounts and Services

Ongoing

• Compile and consolidate bank account data in Master Database

Step 5: Outline Criteria

Annually

• Determine rules and threshold you will use to screen out fees

that need to be reduced and accounts that need to be eliminated

Step 6: Tier and Communicate Expectations

Annually

• Determine which fees and accounts are Level 1 non-negotiable,

Level 2 Negotiable and Level 3 Strategic

Step 7: Share Best Practices

Quarterly

• Share best practices among operating companies regarding fees

and services that can be eliminated quickly and with little cost to

the business

Step 8: Sustain Senior-Level Support

Quarterly

• Regularly demonstrate benefits of bank management

improvements to senior management

DATA COLLECTION

Tools for Data Collection

1. Banks and bankers

Develop relationship with bankers and ask them for recommendation of accounts and services

2. Bank Analysis

Review bank analysis statements to look for wasted services and fees

3. Develop survey to discuss with operating companies

Use a survey or interviews to understand business needs and service requirements

Important! Listen to your customers

4. Peers and Network

Speak with your peers and others in your network to share best practices

Accounts

1. How many bank accounts does your entity control?

2. How many bank relationships do you have?

3. Which banks do you have these accounts with?

4. How are these accounts utilized? What is their

purpose?

Learning

Don’t attempt to understand the reasoning behind their

account structure

1. Why did you open these accounts?

2. What were you planning to do with these accounts?

3. Why didn’t you open “XYZ” type of account?

METHOD FOR COLLECTING DATA

Interviewing process

Services

1. What cash management services do you have?

2. How much in cash management fees did you pay in

2012?

3. How much have these fees increased or decreased

over the past one, two, and three years?

Educating

Don’t attempt to change their perspective on their

account current fee or account structure (yet)

1. How can Treasury help you manage your accounts

and services better?

Things to ask What not to ask

TRACKING BANK DATA

Level 1 Level 2 Level 3

Based on March 2012 fees. Seg A $8,313 $8,976 $10,736

These are 1 month fees only. Seg B $8,464 $7,917 $1,244

Seg C $4,962 $1,496 $0

Seg D $1,198 $2,460 $1,679

CORP $3,189 $1,874 $525

$26,125 $22,723 $14,184

Level 1 Level 2 Level 3 Seg $313,499 $272,675 $170,208

Bank

A 2,346.04 1,541.00 CORP

B 31.00 A

C 259.00 430.88 677.00 B

D 60.00 180.11 C

E 534.68 D

F 191.00 30.00 A

G 143.00 177.36 302.00 B

H 2,111.00 162.72 C

I 22.41 D

J 264.50 123.00 525.43 A

K 290.00 558.93 1,244.00 B

L 455.00 1,179.38 352.58 C

Monthly

Annual

TRACKING BANK DATA

Criteria for accounts and services

Level 1

Level 2

Level 3

Questions to

consider

1. Is there a low-cost

alternative to this

service or account?

2. Can local operating

companies eliminate

these services without

disrupting business

operations?

3. Have costs for this

kind of account or

service risen over past

years?

Questions to

consider

1. Is there a valid business

case for keeping these

accounts or services?

2. Are these accounts or

services necessary for

local operations?

3. Are these local specific

regulatory issues that

require these accounts?

4. Are there tax implications

for eliminating or

restructuring these

accounts?

Questions to

consider

1. Can Treasury add

value to the enterprise

by performing these

cash functions

centrally?

2. Can Treasury utilize

its scale to have a

better negotiating

position?

3. Can the operating

company change its

process strategically

to create savings

opportunities?

Non-negotiable Negotiable Strategic

Criteria for accounts and services

Level 1

Level 2

Level 3

Example

s 1. Paper statements

2. CD-ROM for lockbox and

disbursements

3. Paper/fax confirmations

4. Dual sided scanning of

lockbox items

5. Weekend lockbox

processing

6. Dormant accounts

Example

s 1. Local banking relationships

2. Lockboxes for low volume

accounts

3. Accounts that may be

commingled

4. Services that allow for

efficiencies

Example

s 1. Globally integrated banking

platform

2. Low-cost F/X transactions

3. Policy requiring all new

accounts and services

routed through Treasury

4. Shared Service Center

Non-negotiable Negotiable Strategic

IMPLEMENTATION / ONGOING MANAGEMENT

Implementation / Continued ongoing management

1. Develop training manual and establish backups

2. Insured proper segregations of duties and internal controls in place

3. Have routine meetings with bankers to go over structure and fees

4. Establish practice with bankers to notify Treasury anytime there are requests from the field

5. Regularly review account analysis statements

6. Create a scorecard of key initiatives to be tracked and measured

Agenda

Dover Corporation

Banking Services

Foreign Exchange Procurement

Closing

Foreign Exchange Procurement

• Dover has extremely large intercompany trade flows between operating companies in different countries – These flows require currency conversion

• Dover Treasury helps its operating companies get the best price for foreign currencies

Foreign Exchange Procurement

• F/X can generate hidden costs – F/X rates get buried in operating company sales and

COGS

– Banks often try to charge above-market F/X rates to earn more money

– This can lead to additional costs that you might not see

• How can Treasury help operating companies? – By having banks compete for F/X trades, we source the

cheapest rates, which has a positive impact on margins

Foreign Exchange Procurement

• Dover Treasury discovered in 2012 that its cash management banks were charging very high spreads on F/X transactions – Alerted by an Operating Company CFO, who saw a

large F/X disparity between EUR/USD rate in WSJ and quote from bank

• Treasury initiated a process to identify an electronic F/X dealing platform

• Initiated negotiations with cash management banks to negotiate F/X spreads

Foreign Exchange Procurement

2 They provide the quotes

Foreign Exchange Procurement Dover initiated a pilot F/X procurement program with an operating company.

Amount bought: $1.5 million of EUR and THB

Time period: July 13 to August 16

Total number of trades: 8

Total savings ($): Over $40,000

Total savings (%): Over 2.6%

Based on the pilot program’s results, Dover moved forward with a larger scale program to procure F/X for its operating companies.

Foreign Exchange Procurement

• Make Sourcing F/X from Treasury easy: – Operating company

emails Treasury F/X inbox to request set-up

– Treasury will provide a simple form to fill out and email with F/X requests

– Going forward, operating company sends email requests to the Treasury F/X inbox and transactions will be processed

Agenda

Dover Corporation

Banking Services

Foreign Exchange Procurement

Closing

Lessons Learned

• Strive to understand your business’ service needs

• Be proactive, not reactive

• Be a collaborative partner – strive to present “opportunities” for real cost savings or process improvements

• Be mindful of treasury’s brand within the organization

• Continually evaluate bank fees and services

• Be aware of “hidden costs” (e.g., foreign exchange spread)

• Continually evaluate how to better serve your organization in the future

Questions?