treasurytoday © august 008

TRANSCRIPT

� | treasurytoday © August �008

Anzeige – Treasury Today (Global) – SEPA 2008/Red Carpet – 210 x 297 mm, 10.1. 2008, 18:10 Uhr

Deutsche Bank Securities Inc., a subsidiary of Deutsche Bank AG, conducts investment banking and securities activities in the United States. Private & Business Clients services are not offered in the United States. Deutsche Bank Securities Inc. is a member of NYSE, FINRA and SIPC. This advertisement has been approved and/or communicated by Deutsche Bank AG and by each region with appropriate local regulation. The services described in this advertisement are provided by Deutsche Bank AG or by its subsidiaries and/or affi liates in accordance with appropriate local legislation and regulation. © Copyright Deutsche Bank 2007.

Are you ready to take advantage of the Single Euro Payments Area? Deutsche Bank makes SEPA’s medium-term advantages today’s reality. Talk to us now and change the way you look at Euro payments.

SEPArate from the crowd: www.db.com/gtb/sepa

+++ SEPA is here +++ Deutsche Bank offers immediate fi nancial benefi ts to corporate clients +++

GLOBAL TRANSACTION BANKING I CASH MANAGEMENT

210x297_SEPA08_TreasTod.indd 1 11.01.2008 9:54:06 Uhr

treasurytoday © August �008 | �

Adam Smith Awards Supplement • August �008

www.treasurytoday.com

PublisherAngela Berry

Managing DirectorRichard Parkinson

Editorial ManagerRebecca Brace

Senior Editorial ResearcherMichael Klein

Editorial ResearcherKathryn Terry

Editorial AssistantEleanor Hill

Senior Relationship Manager John Nicholas

Relationship ManagerTeri Richardson

Operations ManagerLisa Bigley

Senior Design and Production Controller

Sion Smith

Design and Production ControllerNadia Ouertani

Circulation ManagerCarrie White

Circulation AssistantSamantha Scott

Switchboard +44 (0)�3 046� 9000 Publisher +44 (0)�3 046� 90�� Subscriptions +44 (0)�3 046� 900� Advertising +44 (0)�3 046� 90�8 Editorial +44 (0)�3 046� 9006 Production +44 (0)�3 046� 9007 Fax +44 (0)�3 046� 90�0

Annual Subscription Rates UK/Europe £�75/€430 Rest of world £340/€530

© Treasury Today ISSN �466-4��4

treasurytoday is published monthly (�0 issues) by Treasury Today Limited • Courtyard Offices

Harnet Street • Sandwich • CT�3 9ES • UK

The entire content of this publication is protected by copyright. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means mechanical, electronic, photocopying, recording or otherwise, without the prior written consent of the copyright holders. Every effort has been made to ensure the accuracy of the information contained in this publication, Treasury Today Limited cannot accept liability for inaccuracies that may occur. No statement is to be considered as a recommendation or solicitation to buy or sell securities or other instruments, or to provide investment, tax or legal advice. Readers should be aware that this publication is not intended to replace the need to obtain professional advice in relation to any topic discussed.

Treasury Today (USPS 023-387) is published monthly except August and December by Treasury Today Limited, Courtyard Offices, Harnet Street, Sandwich, CT13 9ES, United Kingdom. The 2008 US annual subscription price is $588. Airfreight and mailing in the USA by Agent named Air Business, c/o Worldnet Shipping USA Inc., 149-35 177th Street, Jamaica, New York, NY11434. Periodical postage paid at Jamaica NY 11431. US Postmaster: Send address changes to Treasury Today, Air Business c/o Worldnet Shipping USA Inc., 149-35 177th Street, Jamaica, New York, NY11434. Subscription records are maintained at Treasury Today Limited, Courtyard Offices, Harnet Street, Sandwich, CT13 9ES, United Kingdom.

Air Business is acting as our mailing agent.

treasurytoday

Audited member of BPA Worldwide

Welcome 3

Award details 4-7

Case studies 8-28

Photo gallery 29

AWARD CATEGORIES

Bank Relationship ManagementThe first category covered any aspect of the client/bank relationship, including the RFP/bank selection process, credit, bank charges, account analysis, managing mandates and the use of digital signatures, use of other new software, the outsourcing of tasks to the bank and client service delivery.

Global Liquidity ManagementThis Award was open to projects incorporating any aspect of the management of the company’s cash and liquidity. Eligible projects ranged from simple cash reporting processes to complex multi-currency cash pooling solutions, special purpose vehicles and in-house banks.

Working Capital/Financial Supply Chain/Payable and/or Receivable SolutionsThis area is now regarded as the combination of the customer-to-cash, purchase-to-pay and forecast-to-fulfilment processes within any business. This Award was open to projects such as A/P and A/R solutions, the establishment of payment factories or shared service centres and the use of SWIFT’s new corporate access models.

Outstanding Insourcing/OutsourcingEvery treasury needs to strive for continuous improvement. This often results in a review of processes that can be automated, insourced and/or outsourced. This Award was open to companies demonstrating success and innovation in their in/outsourcing of any activity within the corporate treasury arena.

The Best SEPA SolutionReflecting innovation and/or best practice demonstrated as a result of the introduction of SEPA in 2008, this Award was open to companies that had changed their processes, systems or service provider(s) to respond to the new SEPA environment.

Leveraging Corporate Debt SolutionsFocusing on how companies raise debt and use short, medium and/or long term facilities, this category covered projects such as issuing commercial paper, bonds, bank finance, IPO or other instruments. It included both single transactions and projects that formed part of a company’s overall debt strategy.

Effective Enterprise Risk Management The winning project in this category needed to demonstrate excellence in any aspect of risk within the corporate treasury arena, such as foreign exchange risk, interest rate risk, systemic risk, country risk, commodity risk, counterparty risk, operational risk or weather risk.

Mid-market TreasuryRecognising that a company does not have to be a major multinational to be considered for an Award, this category was specifically aimed at SME/MMEs. The Award was open to companies demonstrating best practice and/or innovation in any aspect of the treasury/cash management arena.

Harnessing the power of technologyThis category covered any solution evidencing best practice and/or innovation where technology was the primary driver, such as a new TMS or ERP system, supply chain solutions or the use of technology to support cash management processes.

Bright SOX award for good corporate governanceThe sometimes difficult areas of compliance, governance and the impact of regulatory considerations on the treasury environment were covered by this category. Nominations were accepted from accounting firms as well as companies that had found cost-effective ways to tackle these issues.

Treasury Today’s Top Treasury Team – awarded for overall excellenceThis category was open to any corporate team (either the treasury team itself or a broader team effort involving different disciplines within a company) which has made an outstanding contribution to its organisation – or a supplier which has made an outstanding contribution to the industry and made the world of corporate treasury that much better.

CONTENTS

treasurytoday © August �008 | 3

WelcomeThe last year will never be forgotten by those that work in the financial markets. But that has not stopped treasurers getting on with projects that have added significant value to their companies while demonstrating best practice. Treasury Today’s Adam Smith Awards recognise some of the very best examples as we celebrate winners who have really achieved something for their companies.

Often heralded as the father of economics, we felt Adam Smith would be the perfect representative for our Awards. His resounding influence can be felt as much today as at any other time in history, with his writings and analysis on changing the face of the economy providing a stable platform for the modern economic era.

The Awards recognise the achievements of those companies that have forged strong and efficient relationships; ties that have enabled the successful overhaul of cash management structures, the implementation of SEPA-compliant systems, innovative technological advances and much more. These Awards are a celebration of those relationships, and we believe the achievements of the successful treasury teams should be commended.

The many who were nominated and did not receive an Award should also take pride in the ingenuity and effectiveness of their solutions: solutions that have shown that even in the recent periods of ‘turmoil’ and ‘crisis’, successful management will continue to drive the industry forward.

In closing, I would like to take this opportunity to remind you that these Awards will be an annual event. Nominations for the Adam Smith Awards for Best Practice and Innovation 2009 will open in February.

Richard Parkinson Managing Director

Treasury Today

4 | treasurytoday © August �008

Treasury Today would like to thank the judging panel and all those who submitted nominations for this year’s Awards. We made Awards as described on the following pages:

Bank Relationship Management 8

WinnerBen FletcherThe Procter & Gamble CompanyIn partnership with ABN AMRO, Procter & Gamble initiated an innovative Joint Internship Scheme. This scheme placed Procter & Gamble employees in the bank and vice versa, allowing both organisations to learn from one another and drive their relationship forward. This is easier to say than do with restricted confidential and commercial information on both sides that had to be inaccessible to the interns. The overall result is much lower error rates and vastly improved customer service at all levels.

Highly CommendedPaul Burstein/Dennis SweeneyGE/TWIST General Electric and TWIST worked together to initiate the global standardisation of e-billing and the writing of the new international standard, the Bank Services Billing (BSB) standard. This standard, which is apparently being adopted somewhat reluctantly by other banks, dramatically improves a customer’s ability to get detail of all commission charges in a standardised form. Danske Bank say it has won business by offering to provide information on charges using the standard and GE/TWIST say several more banks are about to join Danske and Barclays, the forerunners, in offering information in this way. The BSB is already the billing standard of choice for many corporates but it looks like it is going to be several more years before it is universally available. Nonetheless the judging panel felt the initiative should be recognised.

Global Liquidity Management ��

Winner Pauline HaggertyMarsh & McLennanMarsh & McLennan Companies worked alongside Citi to create a highly-automated, multi-currency notional pooling system. This type of pooling is not easy to establish as multiple regulatory and legal issues have to be resolved. The new arrangement provides automated interest allocation and settlement. As a result, administration activities were reduced significantly while cash and debt management was eased through the accessibility of available funds on a global scale. The savings achieved have been very significant.

Highly Commended Ouisem SamoudSkandia Insurance Co. LtdLiquidity management for Skandia had become hampered by the decentralised structure of its operations. In joining with Deutsche Bank, a multi-currency account platform was established that eased the initiation of domestic and cross-border payments and significantly reduced the number of banking platforms used.

Working Capital �3

Winner Giovanni CraveroTelecom ItaliaWorking in conjunction with JPMorgan, Telecom Italia set up a SWIFT connection to streamline its cross-border payments. All three of the available SWIFT corporate access models were used – Treasury Counterparty, MA-CUG (Member Administered Closed User Group) and SCORE (Standard CORporate Environment). Control of the data is automated by the bank’s back office and funds reach the beneficiary within minutes. Furthermore, any SWIFT message is stored and electronically available for the 10 years required by Italian law, as well as for internal and external auditing. Subsequently, Telecom Italia has benefitted from the sending of messages in a standard format as well as enhanced levels of traceability. Telecom Italia is the overall winner in this category.

treasurytoday © August �008 | 5

Financial Supply Chain �4

Highly Commended Knorr-Bremse AGThe effect on a company’s working capital of days sales outstanding exceeding days payable outstanding can be significant – especially as the company expands and sales grow. Knorr-Bremse made the decision to implement Deutsche Bank’s Supplier Finance programme to address this issue. This solution enabled each party to benefit: Knorr-Bremse had a better chance of agreeing longer payment terms with its suppliers, who then enjoyed access to additional funding at better rates, while Deutsche Bank gained transaction and factoring business from a well-rated company. The ability to customise the solution was also a big advantage for Knorr-Bremse.

Outstanding Insourcing/Outsourcing �5

Winner Rebecca WilsonKimberly-Clark CorporationOutsourcing may sometimes no longer be appropriate and Kimberly-Clark’s innovative insourcing of an in-house bank is a good example of this. The project involved the formation of an entirely new legal structure, bank account structure and the use of a treasury management system that would improve processes and efficiency. Working with their partner bank, Citi, the project was completed in less than a year.

Highly Commended Jonathan ReynoldsStandard Bank Offshore GroupSBOG was looking for a means to improve its efficiency and STP rates, at the same time reducing operational risks and eliminating manual processes. HSBC was able to initiate a solution to meet its requirements through a combination of banking services and third party suppliers. Combining the use of a SWIFT service bureau with the outsourcing of activities, Standard Bank has seen a significant reduction in manual processes that have driven increased levels of efficiency within the company. This sort of outsourcing from one financial institution to another is becoming more common and we are beginning to see even big banks outsourcing some aspects of their back office processes. This is a particularly good example of this trend.

Leveraging Corporate Debt Solutions �7

Winner Mark WyllieCentral European Media EnterprisesCME’s in-house treasury devised an innovative call spread and convertible offering that successfully raised a total of $475m – a figure achieved through the use of four different banks. This was particularly impressive at a time when credit conditions were in such a volatile state and financing was difficult to come by. They are the outright winner in this category.

The judging panel did not make an Award in the Highly Commended category.

6 | treasurytoday © August �008

The Best SEPA Solution �8

Winner Martin SchlageterRocheBy addressing the impact of SEPA early, Roche was also well ahead of the pack and able to reap the benefits of SEPA’s launch from day one. Roche is one of the few companies that, thanks to its co-operation with Deutsche Bank, has been seamlessly using SEPA Credit Transfers for all its entities across Europe from day one. Roche is the winner of the Adam Smith Award for The Best SEPA Solution.

Highly Commended Martin WilsonVocaLinkThe January launch of the Single Euro Payments Area has been one of the largest developments in the payments arena for some time. One company that is ahead of the pack in achieving SEPA compliance is VocaLink. The creation of their euro Clearing and Settlement Mechanism was Europe’s first independent pan-European clearing payment service and has the versatility to allow banks, no matter what size, to benefit from a fully compliant, ready-made solution. VocaLink is the winner of the Highly Commended Award for The Best SEPA Solution.

Effective Enterprise Risk Management ��

Winner Jesus Angel Garcia-QuilezAbengoaIn looking to develop its operations on a global scale, Abengoa devised a solution that covered credit risk, liquidity risk, exchange rate risk and interest risk. They created a consolidated risk management process that provides a secure financial position and demonstrably enhances business results.

Highly Commended Friedrich FlotoNovelis AGNovelis currently has operations in 11 countries and wanted to manage its cash and risk management activities on a central basis. However, a number of obstacles had to be overcome, including the conditions of the company’s syndicated loan. Working with Commerzbank, Novelis overcame these to set up euro cash pooling and centralise its risk management activities.

Mid-market Treasury �3

Winner Michael McAdamsRobbins & Myers Inc.By working alongside JPMorgan, the company implemented a less fragmented treasury structure capable of meeting the company’s needs as it continued its European expansion. In reducing the number of banking relationships, achieving economies of scale and minimising the level of manually intensive tasks, Robbins & Myers was able to meet its requirements and establish a centralised treasury that had enhanced levels of control over its financial operations. In the process, they have established a structure as good as, or better than, many much larger companies, thus demonstrating what can be achieved if you work hard at getting the basics right.

The judging panel did not make an Award in the Highly Commended category.

treasurytoday © August �008 | 7

Harnessing the power of technology �4

Winner Ian JohnsonMerck & Co., Inc.Despite the competition from Volkswagen, the overall award goes to Merck. In conjunction with Wall Street Systems, Merck was able to reduce the number of banking relationships it maintained from 100 to three after upgrading to the treasury management system, Wallstreet Suite 7.1. This was a complex project but the rewards have been significant.

Highly Commended Thorsten BrandVolkswagenWorld-renowned automobile manufacturer Volkswagen is the recipient of the Highly Commended title for Harnessing the power of technology. Technology consulting company BearingPoint took up the challenge of replacing Volkswagen’s diverse network of legacy systems, many of which were restricting the efficient operations of the company, in a process involving a combination of its ProvenCourse® methodology with Volkswagen’s SEP-SAPSM implementation technology. This was another complex project with impressive results.

Bright SOX award for good corporate governance �6

Highly Commended Dharmendra VarmaRevalSOX compliance demands that as well as ensuring that your own company is compliant, companies are also responsible for ensuring that their third party software providers comply with their controls. Reval has become Type II SAS70 compliant, the more stringent type of certification, making SOX compliance much easier for its clients. Previously each company auditor had to review individually Reval’s processes for SOX compliance.

The judging panel did not make an overall winner Award in this category.

Treasury Today’s Top Treasury Team �7Our final Awards are presented to those treasury teams we feel deserve the greatest level of recognition. Both of the teams receiving an Award in this category have demonstrated high levels of innovation, ingenuity and efficiency in the management and operation of their treasury departments.

Winner Olivier BouillaudAntalisThe overall winner is Antalis and Olivier Bouillaud led the team. The need to raise enough funds to strengthen its financial position and purchase Map Merchant was an unenviable task for Antalis, yet the required level of finance was raised with the support of some of Europe’s leading banks and the dedication of its entire treasury team. In addition to the case study we will be carrying an interview with Olivier in the September edition of Treasury Today. This was an impressive team effort and the Antalis treasury team won Treasury Today’s Top Treasury Team Award.

Highly Commended Jörg WiemerSAP AGSAP created an automated statement collection solution for its worldwide bank accounts and improved the visibility of its cash positions across all 27 currencies. A reduction of workload and process complexity for staff, improved efficiency, cost savings and security enhancements are just some of the benefits they now enjoy.

8 | treasurytoday © August �008

Winner – Bank Relationship Management

TheProcter&GambleCompanyBenFletcher:EMEATreasuryBankingManager

Procter & Gamble first appointed ABN AMRO to manage its European collection business in 2004, as part of an initiative to consolidate its banking relationships. In order to maximise this relationship for both parties and ensure that shared objectives were met, a Joint Business Plan was set up.

During this process an idea was developed for a new model of bank relationship management based on an approach Procter & Gamble had sometimes used with retailers. “Our mindset was to create a model that set a new standard of best practice in the field of relationship management,” says Ben Fletcher, EMEA Treasury Banking Manager at Procter & Gamble.

“To achieve that aim we created a Joint Internship Scheme, which places employees of Procter & Gamble into the bank for a period of time and vice versa. This allows us to really penetrate the issues/systems and solutions of both companies in order to find solutions that change the game.”

Each internship, lasting around 10 days, was set up to focus on a specific issue with all outcomes rigorously reviewed and tracked. Quarterly assessments were also put in place to ensure the scheme delivers benefits to both the bank and Procter & Gamble. Security of data was of course a top priority for both parties, and six months were spent ensuring that the project met legal and tax requirements and that only data relating to the two companies would be shared.

Following the launch of the project in July 2006, Procter & Gamble has seen the handling time for bank accounts cut from 10 weeks to two days by leveraging new tools provided by the bank. It has also seen its fees budget reduced by nearly a quarter, despite business growth of

almost 40%. The bank, meanwhile, has gained an insight into the working of a large corporate and Procter & Gamble now acts as a lead partner in testing new products for the bank. They have also looked at broader areas important to both companies such as change management and the use of Six Sigma.

“The stand-apart feature of the solution,” says Fletcher, “is the degree of transparency and engagement between a corporate and one of their key banking partners. Being able to place employees into each other’s organisation is a mindset change on both sides that opened up significant benefits.”

The programme looks set to continue benefiting both parties well into the future and Procter & Gamble is planning to arrange future internships in order to address its end-to-end cash management process.

Fletcher hopes to extend this approach to additional bank relationships in time and would recommend it to other corporates, although he points out that such a project should be undertaken to further an existing strong relationship rather than at the outset of a new one.

He concludes, “We believe there is nothing similar in the industry and that has been possible because of the willingness of our banking partner to find ways to give us access to their back office whilst protecting the integrity of their data and systems.”

From left: Ben Fletcher, Richard Parkinson

Our mindset was to create a model that set a new standard of

best practice in the field of relationship management.

”“

The Procter & Gamble Company retails

such iconic brands as Pantene, Pampers,

Olay, Ariel and Gillette to consumers in over

180 countries. In 2007 the company posted sales figures of more

than $76 billion.

treasurytoday © August �008 | 9

Highly Commended – Bank Relationship Management

GE/TWISTPaulBurstein,formerlyManagingDirector,GETreasuryStrategicInitiatives

DennisSweeney,DeputyTreasurer,GeneralElectricCompany

Large corporations have long struggled to manage banking costs, as paper statements showing bank charges provided by banks are often incomplete and those providing billing data through spreadsheets only allow for limited levels of analysis. A further drawback is the inability to get comprehensive detail of all the cash management fees.

In the US, there is a solution: billing data is available in the AFP/ANSI 822 data standard adopted by over 90 major US cash management banks and used by over 500 corporations. Commercially available software used by corporations can identify billing errors and areas requiring optimisation of bank services and assist in managing banking relationships. The problem lies in the lack of a solution on an international scale, particularly addressing taxes on bank fees and the use of multiple currencies.

In order to address this apparent shortfall, General Electric (GE) approached TWIST and organised 35 global companies and banks into forming the International Bank Compensation Group, aiming to push for the international standardisation of e-billing for bank cash management charges. The move led to the writing of the new international standard, the Bank Services Billing (BSB), published by TWIST and available from their website.

General Electric then took the next step of working with many banks to implement the standard. This process would require different measures from each individual bank. For example, for some it was necessary only to modify their bank billing system to produce a new output format – the TWIST BSB file. For others, the task was much larger, requiring modification of a number of core systems to aggregate the service charges. At present, Danske Bank and Barclays are live and sending out TWIST BSB files to corporate customers,

with 14 other banks either actively developing the BSB or committed to providing BSB in the near future.

By developing a recognised and accepted standard for presenting bank invoices for cash management services, TWIST has significantly increased the visibility and effectiveness associated with managing banking costs. Once the new standard is in place, corporates can more easily check all bank calculations; examine expected balances, volumes and service prices; allocate bank charges automatically; perform bank comparisons and more.

It remains to be seen whether the standard is adopted by all the major international cash management banks but GE is pleased by progress to date. Paul Burstein says, “The development of the BSB standard is clear evidence of a new spirit in banking, working together to create and implement international standards to meet their customers’ business needs.”

Dennis Sweeney adds, “Finally we will have the same level of information needed to manage our relationships internationally that we have long enjoyed in the US. We will know which business units are using what services. We will be able to analyse which business units will benefit by migrating from basic to more advanced, value added services, and which should outsource altogether. We can identify opportunities to eliminate manual processing in our back office as well as the bank’s back office. It is a real win-win for both corporates and banks.”

Peter Storgaard from Danske Bank, who has been working in partnership with GE and TWIST on this project, agrees. “We are winning business as a direct result of introducing the new billing standard and are delighted to be one of the first banks to offer the facility.”

The development of the BSB standard is clear evidence of a new spirit in banking, working together to

create and implement international standards to meet their customers’

business needs.

“”

The not-for-profit industry group TWIST – the Transaction Workflow Innovation Standards Team – comprises a number of major corporates, fund managers, banks, system suppliers and others in an organisation responsible for the development and rationalisation of financial industry standards. GE has been the major sponsor behind the development of TWIST’s Bank Services Billing standard.

Paul Burstein Dennis Sweeney

�0 | treasurytoday © August �008

Monitor your banking fees - with a TWIST

Would you like to track and monitor the fees you pay for your banking services? We are the first bank to deliver this information in a structured and standardised TWIST BSB format to our customers in several European countries.

Together with our customers, we are constantly working on creating solutions for easier admi-nistration and review. We have therefore been awarded a prize for best practice and innovation within the category of Bank Relationship Manage-ment.

For further information, please contact us at www.danskebank.com/cashmanagement.

treasurytoday © August �008 | ��

Winner – Global Liquidity Management

Marsh&McLennanPaulineHaggerty:EMEATreasurer

Due to its wide-reaching presence around the world across multiple business lines, MMC’s businesses generate cash flows in a variety of currencies. Consequently, one of the core objectives of its treasury is to improve cash utilisation, increase transparency and enhance balance sheet management. To that end, several single currency cash pools had been managed for several years. However, surplus cash could not be easily utilised for interest or balance sheet purposes without restricting local access to those funds.

Such a position left the company with borrowings in one currency and surpluses in another, and where inter-company loans were established to balance out these surpluses and deficits, significant internal administration was required. It became clear that a more innovative solution was required that would not only meet treasury objectives but also deliver an automated, scaleable, cost-efficient approach to common liquidity processes without stifling the creativity and energy of in-country teams at the sharp end of the business.

After establishing that cross-border, multi-currency notional pooling would deliver the required benefits, MMC set about assessing the pooling offerings available from various banks. Following a period of deliberation, Citi was selected due to the quality of its solution, plus its proven track record in client delivery to MMC.

The innovative and highly-automated solution offered by Citi enabled MMC to establish a notional multi-currency cross-border pool of corporate liquidity. Local entities’ accounts with either Citi or third-party banks are automatically swept into a central pool, but – being notional – funds remain in the entities’ names. With pool account balances offsetting and credit and debit interest rates closely replicating swaps through interest rate parity, pooled funds can be utilised

in any constituent currency without the use of derivatives. Additionally, automated interest allocation and settlement of allocated interest to pool participants accounts each month significantly reduces administration.

Improved intraday visibility and access to funds is achieved through electronic banking reporting. Entities access their own account position and interest income, while customised reporting enables treasury dealers to deploy or invest consolidated liquidity more effectively.

Implementation of the initial solution was achieved in just three weeks, thanks to a dedicated Citigroup/MMC project team. By the end of 2007, the pool consisted of 80 accounts in 13 currencies across 60 legal entities, with further significant growth anticipated. Its success has meant that MMC has been able to reduce local cash floats, increasing the proportion of funds invested and the yield earned thereon. Additionally, due to the multi-currency nature of the pool, greater access to funds is available across different geographies, enabling cash and debt to be managed more effectively.

The success of the pool has far exceeded the original objectives set by MMC and demonstrates the value of leveraging an established banking relationship with a market leading, highly automated solution.

Pauline Haggerty, EMEA Treasurer of MMC, commented, “Funds that were domiciled and managed by local finance teams across Europe, Canada, Asia and Pacific regions are now concentrated in London for central management. By the end of 2008, we expect the pool to increase to around 150 accounts across 80 entities. The financial and control associated benefits to MMC are very significant and will increase further as the pool continues to expand.”

Funds that were domiciled and managed by local finance teams across Europe, Canada, Asia and Pacific regions are

now concentrated in London for central management. By the end of 2008, we

expect the pool to increase to around 150 accounts across 80 entities.

“”

in partnership with

Marsh & McLennan Companies (MMC) are among the premier global providers of advice and solutions in risk, strategy and human capital. With more than 55,000 employees worldwide and a customer base across 100 countries, annual revenue for the company exceeds $11 billion. Companies in the group include Marsh, Guy Carpenter, Mercer, Oliver Wyman and Kroll.

From left: David Li (Citi), Elias Xilas (Citi), Pauline Haggerty and Richard Parkinson

�� | treasurytoday © August �008

Highly Commended – Global Liquidity Management

SkandiaInsuranceCo.LtdOuisemSamoud:CashManager

Historically, Skandia’s decentralised structure has made it difficult to achieve the co-operation needed for cash pool solutions. This has presented the treasury with a number of challenges, including a lack of visibility over group bank balances, no access to group liquidity, no cross-border cash pooling, and a multi-bank structure which comes with high transaction costs and limits negotiation power with banks. What is more, the added hindrances of legislation in the insurance industry and restrictive rules over the co-mingling of funds between companies – and between policy holders and shareholders – meant that there was a pressing need for Skandia’s treasury to develop a unique solution.

“In 2007 we asked seven banks to support us in developing an overlay, multi-currency cash pool without inter-company loans/guarantees and no co-mingling of funds,” explains Ouisem Samoud, Cash Manager in Skandia. The chosen solution had to fulfil several key criteria: improved management of liquidity and capital at a group level, increased interest on bank holdings for the subsidiaries, support for straight through processing solutions for internal financial flows and efficient and low-cost transactions. In addition, real-time access to account information was required on a group level.

The chosen solution provided by Deutsche Bank comprised a multi-currency account platform that could include all participating entities of Skandia Group. An industry-specific interest optimisation scheme was implemented to pool the entities’ cash without co-mingling funds in order to comply with regulations. This was achieved using an accounting set-up that clearly separates the different types of cash. The solution also offered enhanced interest rates on overdraft and deposit positions, as well as flexible investment options into higher yielding investments and optimised transaction handling. Supported

by the bank’s multi-bank electronic banking system, the structure is able to provide Skandia with access to account information and liquidity reports, as well as the ability to initiate all forms of domestic and cross-border transactions.

With the new system in place, Skandia sees the possibility of decreasing the costs associated with maintaining multiple banking platforms and separate credit facilities previously required. As more subsidiaries join the platform, the group will also benefit from decreasing bank spreads by netting their FX requirements. The new structure also brings the company a step closer to being able to make high value settlements and bulk settlements via a payment factory.

As a result of solid planning, clearly defined roles and a strong relationship between Skandia and Deutsche Bank, the solution was implemented in an efficient manner. In fact, by tightly monitoring the budget, the return on the investment looks set to be positive in less than a year.

“This solution has from the start been about challenging Deutsche Bank with Skandia’s Cash Management vision – the challenge of being creative, bold and in the frontier, but at the same time building a sustainable solution that will bring the group liquidity and payment processes together despite insurance legislation,” Samoud concludes. “This result will lead the way for more insurers across Europe to develop cross-border, multi-currency, multi-entity cash pool solutions.”

This result will lead the way for more insurers across Europe

to develop cross-border, multi-currency, multi-entity

cash pool solutions.“

”

Skandia is a provider of long-term savings and

investment products operating in over 20

countries. Owned by Old Mutual since 2006,

Skandia’s core business is in Europe.

in partnership with

From left: Claus Pahlke (Deutsche Bank), Ouisem Samoud and Richard Parkinson

treasurytoday © August �008 | �3

Winner – Working Capital

TelecomItaliaGiovanniCravero:HeadofFinance,OperationsandCashManagement

Telecom Italia provides services to customers throughout Europe and Latin America. However, while CBI, the Italian corporate banking standard, acts as a robust solution for domestic low value bulk payments, there was no such solution in place for cross-border payments. The level of manual and back office processes involved was increasingly unwieldy, bringing the risk that any mistake in settlement could result in heavy claims and disruption of the intraday credit lines or cash needs.

“Both the Milan and the Luxembourg treasuries of the group, had several procedures for each bank and different devices, including fax, call back, internet banking and ftp,” says Giovanni Cravero, Head of Finance, Operations and Cash Management of Telecom Italia. “The company therefore had lack of traceability, low security and little control over the content of the message or the status of the processing.

“We were looking for a way to implement a single payment channel, communicate with a wide variety of financial institutions, handle transactions from large individual treasury payments to large volume low value transactions. We also hoped to anticipate the arrival of SEPA and achieve financial gains by improving our working capital through a better understanding and mastering of the overall payment flows.”

The decision was taken to set up a SWIFT connection using all three of the available models: Treasury Counterparty, MA-CUG (Member Administered Closed User Group) and SCORE (Standard Corporate Environment). This was achieved using a service bureau, meaning that no hardware or software had to be installed in-house. The SWIFT connection provided Telecom Italia treasuries with three different Business Entity Identifiers that identify the company on the network, with employees able

to access the channel using the user-friendly SWIFT Alliance Messenger web interface.

As a result of the implementation, Telecom Italia has seen many benefits. “With SWIFT it is possible to send payments (Message Type FIN MT101) in a standard way with any of our transaction banking counterparties. The payment is fully electronic, and it is possible to track the full cycle of the message,” says Cravero.

Control of the data is automated by the bank’s back office and funds reach the beneficiary within minutes. Furthermore, any SWIFT message is stored and electronically available for the 10 years required by Italian law, also providing Telecom Italia with full traceability for daily operations purposes as well as for internal and external auditing.

JPMorgan was the first bank to set up a MA-CUG with Telecom Italia and was instrumental in implementing the solution, contributing technical expertise, testing and project management. JPMorgan was also the first bank to process Telecom Italia’s bulk payments via FileAct, providing Telecom Italia with a back-up network for its domestic CBI transactions.

By allowing the company to receive intraday statements of account and confirmation of payments and credits, the SWIFT connection enables Telecom Italia to observe real-time data and act on any exceptions or failures with immediacy.

To that end, SWIFT has also significantly improved the overall monitoring of daily cash flows. “SWIFT has been a qualitative tool to better understand and follow financial, supply and operations daily cash-flows, and thus to better master the cycles that impact on our working capital,” concludes Cravero.

SWIFT has been a qualitative tool to better understand and follow

financial, supply and operations daily cash-flows, and thus to better master

the cycles that impact on our working capital.

“”

Telecom Italia Group, which employs over 83,000 workers, reported revenues of €31.3 billion in 2007. The company currently provides 7.7 million broadband connections and 36 million mobile lines in Italy alone.

in partnership with

From left: Neil Gray (SWIFT), Tancrede Carpenter (JPMorgan), Roberto Rossetti (Telecom Italia) and Ernesto Simonetta (Telecom Italia)

�4 | treasurytoday © August �008

Winner – Outstanding Insourcing/OutsourcingHighly Commended – Financial Supply Chain

Knorr-BremseAG

For many companies, their days sales outstanding (DSO) far exceed days payable outstanding (DPO), a fact that has an adverse effect on the working capital of the organisation. In order to address this issue, Knorr-Bremse made the decision to adopt a solution whereby suppliers would get access to financing at better rates in order to support their ability to accept the longer payment terms Knorr-Bremse wanted to take.

In selecting a solution, the highest priority was increasing the volume of funds at the disposal of the supplier while improving the financing conditions currently available to the supplier in financing its accounts receivable. The solution chosen to address these issues was Deutsche Bank’s Supplier Finance programme. One of the main reasons for this decision was the underlying software that was developed by Deutsche Bank and is its ‘property’ in the best sense of the word. Essentially this means it can easily and quickly be adjusted to special requirements, if any, by Deutsche Bank themselves and exactly meets the requirements suppliers and customers have in connection with the programme.

In the first step of the process, Knorr-Bremse appointed Deutsche Bank as payment agent for selected suppliers using Deutsche Bank’s db-eBills platform. Knorr-Bremse was then responsible for sending the relevant supplier’s invoice data to Deutsche Bank’s platform, along with confirmation that Knorr-Bremse would pay the full amount to the supplier via Deutsche Bank on the due date.

Suppliers, meanwhile, were able to obtain consent from Knorr-Bremse to sell their accounts receivable to Deutsche Bank. The bank would then arrange its own factoring contract with the relevant supplier, independent from Knorr-Bremse.

This process enables the bank to buy the accounts receivable from the supplier without withholding security amounts and at rates favourable to the supplier. Via internet access to the platform, the supplier can easily recognise all invoices released for payment by Knorr-Bremse and can select the invoices to be sold on a case-by-case basis.

With the new system in place, each party stands to benefit:

n Knorr-Bremse can enjoy a better chance of agreeing longer payment terms with its suppliers.

n Suppliers can enjoy access to additional funds at better rates than they could obtain individually, as well as greater visibility over cash flows.

n The bank can benefit from additional transaction and factoring business with a well rated company like Knorr-Bremse.

The programme is unique because it combines traditional factoring with innovative elements and a new financing scheme. Well rated companies can make available their creditworthiness to their suppliers, helping them therewith to obtain a favourable financing and themselves to improve the DPO. Since the execution of the program was started in February 2008, more than 20 suppliers, with a purchase volume of approximately €100m, have joined. A lot more are still interested and in discussion. Unlike other factoring programmes, the participants get 100% of the invoice amount paid out immediately, no extra fees occur and each and every invoice can be factored separately – this is easily done using internet access and the click of a mouse. The programme therefore combines innovation with a triple win situation, for the customer, the supplier and the bank.

Since the execution of the program was started in February 2008, more than 20 suppliers, with a purchase volume of approximately €100m,

have joined.“

”The world’s leading

manufacturer of braking systems for rail and

commercial vehicles, Knorr-Bremse AG has

been a pioneer in the field for over 100 years. Now

operating with almost 14,000 employees, the company’s worldwide sales in 2007 reached

€3.25 billion.

in partnership with

From left: Fritz Philipps (Deutsche Bank), Sigurd Dahrendorf (Knorr-Bremse)

treasurytoday © August �008 | �5

Winner – Outstanding Insourcing/Outsourcing

Kimberly-ClarkCorporationRebeccaWilson:TreasuryManagerEurope

Since 1998, Kimberly-Clark had been operating a global in-house bank through an outsource provider, which offered Kimberly-Clark and its global affiliates a number of services such as cash management, intercompany payments and receipts netting, intercompany investing and borrowing, foreign currency payments and receipts processing, and foreign currency exposure management. However, over the years the increased levels of outsourcing resulted in activity at the in-house bank increasing ten-fold, with the number of supported affiliates rising to 115, foreign exchange transactions exceeding $20 billion and intercompany loans and deposits valued at more than $1 billion each.

Consequently, the outsource provider’s systems, processes and resources were no longer sufficient to ensure reliable and consistent operation. In 2005, the provider took steps to cap its liability for any losses resulting from operational errors, with Kimberly-Clark assuming most of the risk of execution. Combined with the scale and complexity of the operation, the risk associated with such a move prompted Kimberly-Clark to bring the operation back in-house.

However, the insourcing of an in-house bank was not a simple ‘lift and shift’ from the outsourcer back to Kimberly-Clark. New and improved processes were put in place, a new legal structure and bank account structure were initiated, a new treasury management system installed, and a new team was put together as there was no retained experience within Kimberly-Clark.

As Kimberly-Clark’s core regional relationship bank, Citi had a pivotal role to play in ensuring the timely and efficient execution of the project’s cash management requirements. Rebecca Wilson, Treasury Manager Europe at Kimberly-Clark, explains: “As a result of Kimberly-Clark’s revised legal entity structure, this involved not

only the opening of 16 new accounts in various jurisdictions throughout Western and Eastern Europe, but also the redesign of a cross-border target balance structure together with the implementation of file-based connectivity. Working to a rigid timetable, the seamless completion of these fundamental components was key to the establishment of a working financial model.”

Configuration and testing of the new system began in early 2007, with user acceptance testing occurring in the second quarter. July saw the transfer of operations to the UK. The new currency system avoids the need for each affiliate to maintain separate internal or external bank accounts for each of the currencies in which it makes or receives foreign currency payments. As a result, Kimberly-Clark now has only approximately 50 bank accounts supporting its in-house bank structure, whereas other comparable companies typically have hundreds.

As Wilson says, “The insourcing of the in-house bank to Kimberly-Clark has provided improved efficiency and control by eliminating manual processes and enhancing decision support capabilities through improved access and visibility of information. The project also transformed Kimberly-Clark’s in-house bank from an administrative processing centre to a strategic arm of the corporate treasury function.”

Despite the substantial changes that needed to be made in terms of systems, structure and staff, the project took less than a year to complete. Wilson concludes, “I believe the reason for the success of the project rests with the diversity of the team. Due to an abundance of theoretical rather than practical knowledge, the boundaries were pushed as we were expecting to get more out of the system and the process than had previously been seen.”

Despite the substantial changes that needed to be made in terms of systems,

structure and staff, the project took less than a year to complete.“

”Kimberly-Clark is one of the world’s leading health and hygiene companies, with its range of brands, including Kleenex, Scott, Andrex and Huggies, sold globally to more than 150 countries. Employing more than 55,000 staff in 37 countries, the company’s customer base exceeds one billion people, with sales of $18.3 billion reported in 2007.

in partnership with

From left: Julian Giliberti (Citi), Rebecca Wilson and Richard Parkinson

�6 | treasurytoday © August �008

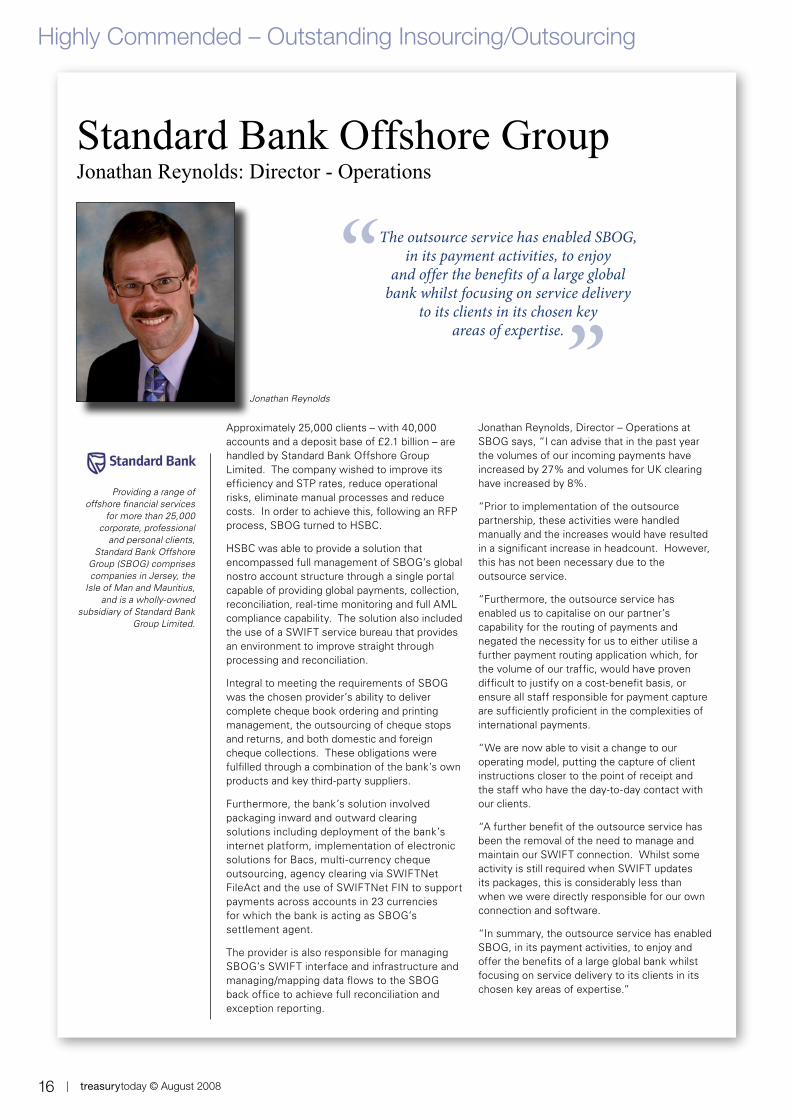

Highly Commended – Outstanding Insourcing/Outsourcing

StandardBankOffshoreGroupJonathanReynolds:Director-Operations

Approximately 25,000 clients – with 40,000 accounts and a deposit base of £2.1 billion – are handled by Standard Bank Offshore Group Limited. The company wished to improve its efficiency and STP rates, reduce operational risks, eliminate manual processes and reduce costs. In order to achieve this, following an RFP process, SBOG turned to HSBC.

HSBC was able to provide a solution that encompassed full management of SBOG’s global nostro account structure through a single portal capable of providing global payments, collection, reconciliation, real-time monitoring and full AML compliance capability. The solution also included the use of a SWIFT service bureau that provides an environment to improve straight through processing and reconciliation.

Integral to meeting the requirements of SBOG was the chosen provider’s ability to deliver complete cheque book ordering and printing management, the outsourcing of cheque stops and returns, and both domestic and foreign cheque collections. These obligations were fulfilled through a combination of the bank’s own products and key third-party suppliers.

Furthermore, the bank’s solution involved packaging inward and outward clearing solutions including deployment of the bank’s internet platform, implementation of electronic solutions for Bacs, multi-currency cheque outsourcing, agency clearing via SWIFTNet FileAct and the use of SWIFTNet FIN to support payments across accounts in 23 currencies for which the bank is acting as SBOG’s settlement agent.

The provider is also responsible for managing SBOG’s SWIFT interface and infrastructure and managing/mapping data flows to the SBOG back office to achieve full reconciliation and exception reporting.

Jonathan Reynolds, Director – Operations at SBOG says, “I can advise that in the past year the volumes of our incoming payments have increased by 27% and volumes for UK clearing have increased by 8%.

“Prior to implementation of the outsource partnership, these activities were handled manually and the increases would have resulted in a significant increase in headcount. However, this has not been necessary due to the outsource service.

“Furthermore, the outsource service has enabled us to capitalise on our partner’s capability for the routing of payments and negated the necessity for us to either utilise a further payment routing application which, for the volume of our traffic, would have proven difficult to justify on a cost-benefit basis, or ensure all staff responsible for payment capture are sufficiently proficient in the complexities of international payments.

“We are now able to visit a change to our operating model, putting the capture of client instructions closer to the point of receipt and the staff who have the day-to-day contact with our clients.

“A further benefit of the outsource service has been the removal of the need to manage and maintain our SWIFT connection. Whilst some activity is still required when SWIFT updates its packages, this is considerably less than when we were directly responsible for our own connection and software.

“In summary, the outsource service has enabled SBOG, in its payment activities, to enjoy and offer the benefits of a large global bank whilst focusing on service delivery to its clients in its chosen key areas of expertise.”

The outsource service has enabled SBOG, in its payment activities, to enjoy

and offer the benefits of a large global bank whilst focusing on service delivery

to its clients in its chosen key areas of expertise.

“”

Providing a range of offshore financial services

for more than 25,000 corporate, professional

and personal clients, Standard Bank Offshore

Group (SBOG) comprises companies in Jersey, the

Isle of Man and Mauritius, and is a wholly-owned

subsidiary of Standard Bank Group Limited.

Jonathan Reynolds

treasurytoday © August �008 | �7

Winner – Leveraging Corporate Debt Solutions

CentralEuropeanMediaEnterprisesMarkWyllie:VicePresidentCorporateFinance

Earlier this year, CME embarked upon a project to acquire the remaining 40% minority interest in its Ukrainian TV station Studio 1+1. The treasury team at CME was tasked with the objective of raising $400m in order to ensure the deal could close while remaining flexible in terms of future funding. However, high yield markets were closed, equity markets were volatile and the bank markets quoted unacceptable terms.

In addition, two of the major ratings agencies were expressing some general liquidity concerns over the prospect of CME utilising most or all of its credit lines in funding the Studio 1+1 transaction. The ratings agencies were not convinced that these lines would be easily replaced in the current climate and wanted CME to ensure it had sufficient liquidity.

In short, cash was required quickly at a time when the credit markets were very difficult. As Mark Wyllie states, “The deal was announced on March 3rd and priced on March 4th, closing March 10th which you will remember was a particularly difficult period – you may recall Bear Stearns collapsed five days later.”

The in-house treasury team devised an innovative call spread and convertible offering

which successfully raised a total of $475m, $401m net of call spread at an effective rate of 7.2%, lower than CME’s prevailing financing costs, with an 85% premium to the current share price.

By using four different banks and a competitive bidding process to provide the derivative instrument (call spread) that CME used, its likelihood of dilutive conversion was reduced.

“The process was run by issuing bid sheets to the banks in advance, then collecting in the best prices on the day before announcement, then negotiating the pricing to give CME the lowest possible price without ending up with a single counterparty,” explains Wyllie.

Robert Janta-Lipinski, Group Treasurer at CME, summarises: “Over the last few years, CME has successfully accessed the capital markets to help fund the Group’s expansion. We were recently able to turn market volatility to our advantage and issued a $475m convertible bond at a time of significant instability and uncertainty in the debt markets, which were effectively closed to high yield issuers.

“The volatility in CME’s stock is very attractive to convertible investors which meant the issue was well over-subscribed. By combining this convertible bond with a tightly negotiated ‘call-spread’ we also made the offering positive from our shareholder’s perspective, by providing significant protection against dilution for an all-in cost approximating that of a straightforward debt issue, but in reality those markets were closed as well.

“We are particularly pleased with our banking partners, who worked with us to quickly execute an innovative structure in a very difficult environment, giving us significant financial flexibility.”

We are particularly pleased with our banking partners,

who worked with us to quickly execute an innovative structure in a very difficult environment,

giving us significant financial flexibility.

“”

Central European Media Enterprises (CME) was founded by Ronald Lauder in 1994. CME is the leading television broadcaster in Central and Eastern Europe, with 17 networks in six countries, Croatia, the Czech Republic, Romania, the Slovak Republic, Slovenia and Ukraine. In 2008 revenues are expected to exceed $1 billion.

Mark Wyllie

We were recently able to turn market volatility to our advantage and issued a $475m convertible bond at a time of significant instability and uncertainty

in the debt markets, which were effectively closed to high yield issuers.

“”

�8 | treasurytoday © August �008

Winner – The Best SEPA Solution

RocheMartinSchlageter:HeadofTreasuryOperations

“When Swiss pharmaceutical giant Roche redesigned its Western European cash management set-up in 2005, shaping a powerful SEPA solution was already a key project objective,” says Martin Schlageter, Head of Treasury Operations.

With this in mind, measures were taken to change the company’s cash management solution by significantly reducing complexity in terms of its order-to-cash and purchase-to-pay processes, as well as simplifying liquidity and treasury management. There was also the need for Roche to maintain cash management on a local basis, a requirement that called for regular local input during the selection process.

The first stages of the process were the introduction of standardised and fully-integrated payment and collection processes in SAP on a regional level. Roche’s Western European entities were then able to migrate to the new standards by achieving straight through processing in terms of the authorisation and reconciliation of payments and collection files.

In addition, the centralised transfer of transaction and reporting files based on SAP format standards was established with Deutsche Bank, which offered a streamlined and centralised cash management structure that anticipated a seamless transition to SEPA.

Addressing the impact of SEPA early, Roche had been collecting IBANs and BICs while keeping master data up-to-date in SAP in preparation for its launch. Roche was also keen to utilise SEPA benefits fully from day one, while avoiding any additional investments and maintenance costs associated with the new platform.

In order to achieve this, the new cash management set-up was always benchmarked in terms of SEPA interoperability and scalability, well before the introduction of SEPA. This made it possible for the company to use both SEPA and non-SEPA payments and collections simultaneously during the migration period.

The complete implementation of Roche’s cash management solution took approximately 18 months. As a result of the extensive preparations, the company has been compliant since the launch of SEPA in January 2008. As such, Roche has been seamlessly using SEPA Credit Transfers for all of its entities across Western Europe.

The company is also preparing for the SEPA Direct Debit scheme based on existing standards that significantly reduce efforts and investments for this new transaction type. Once again, Deutsche Bank will be integral to the success of the migration.

To date, Roche has achieved great success in its centralisation and standardisation of its cash management structure. However, Schlageter is already looking to build upon the success of the processes already in place.

“In order to increase further the level of efficiency in Roche’s Cash Management set-up, more and more external payments and collections will be routed via the internal in-house bank set-up while external account structures will be streamlined as well through this new Payment Factory set-up,” Schlageter explains. “Neither of these initiatives will change the overall cash management architecture, but rather build on the standardised processes established in 2005.”

As a result of the extensive preparations, the company has been compliant since the launch of SEPA

in January 2008. As such, Roche has been seamlessly using SEPA Credit

Transfers for all of its entities across Western Europe.

“”

Swiss pharmaceutical company Roche develops, manufactures and markets

medical solutions on a global scale. Financial

figures for 2007 saw sales grow 10% to 46.1 billion

Swiss francs. The company currently operates with over

78,000 employees.

From left: Martin Runow (Deutsche Bank), Martin Schlageter and Richard Parkinson

in partnership with

Real-time payments. Detail delivered instantly

VocaLink. We’ve been accelerating payments for over 40 years. Our Real-Time Platform takes payments to a new level. For banks, real-time payments offer a fast and effective payment method that requires no intervention. For business, it improves cash flow and simplifies the detail of reconciliation. For consumers, it will become a new way to pay, as convenient as cash but far more secure.

The VocaLink Real-Time Platform is the processing power behind the UK Faster Payments programme. It allows banks to become more efficient as less time is spent sorting out the detail of failed payments. Customers get a better, faster service that suits their lifestyles, and everyone gets paid on time, all the time.

To find out how real-time payments can help your bank and to reveal the identity of our image, visit www.becausedetailmatters.com

�0 | treasurytoday © August �008

Highly Commended – The Best SEPA Solution

VocaLinkMartinWilson:ChiefCommercialOfficer

With the launch of the Single Euro Payments Area (SEPA) in January 2008, VocaLink has responded to the challenge of enabling European banks of all sizes to become SEPA compliant.

Martin Wilson at VocaLink, explains, “We believe that the European vision of a truly single market can only be realised by implementing the right commercial framework to enable banks of all sizes to participate.”

“A successful payments infrastructure is the backbone of any modern economy, but the provision of low-cost payments requires substantial economies of scale and continual investment. VocaLink has adopted an innovative approach to SEPA and has invested heavily to meet the collective needs of European banking.”

These banking needs included the requirement for fast SEPA compliance, lower transaction costs, and value-added banking services. In addition, for SEPA to be wholly successful, banks throughout Europe would need to operate with improved levels of co-operation, in particular collaborating to achieve reach throughout the region and for payments volume to be aggregated to achieve the economies of scale necessary to reduce transaction costs. The solution devised by VocaLink is their Euro Clearing and Settlement Mechanism (Euro CSM).

“The VocaLink Euro CSM is Europe’s first independent pan-European clearing payment service,” continues Martin. “Participating banks of all sizes benefit from the scale of the VocaLink processing operation and enjoy some of the lowest transaction charges in Europe. VocaLink is also working with the Euro CSM’s founder banks to develop a range of value-added services that will help banks meet their emerging customer needs.”

Among the needs of the customer lies the requirement for high straight-through processing rates, end-to-end analysis of the payment value chain, improved liquidity management and a shorter time to market for new products.

Implementation of the Euro CSM allows banks to benefit from a SEPA-compliant, ready-made solution, designed to ensure that the same benefits are available for banks of all sizes. The highly flexible format supports existing bilateral clearing relationships, and has been created to be interoperable with all other CSMs – such as EBA STEP2 – to adapt to the evolving nature of SEPA. Plus, all conceivable data formats are supported for input or output, thereby eliminating the need for changes to legacy formats and systems.

VocaLink, aware that payments are only one element of transaction processes, has taken its solution one step further, a move that acknowledges a bank’s need to offer business customers a range of services. To achieve this, VocaLink developed a suite of service components, including payments capture, payments authorisation and mandate management. These modular service components can be offered in any combination and are offered as managed services to control costs and mitigate risk.

The approach taken by VocaLink attempts to think “beyond SEPA”. In designing a technical infrastructure appealing to banks of all sizes, they have matched the European Commission’s aim of seeking to increase European prosperity through competition.

Since its launch on 28 January 2008, the VocaLink Euro CSM has successfully been providing a European service that may be beginning to change the way banks view the processing market.

The VocaLink Euro CSM is Europe’s first independent pan-European clearing

payment service. Participating banks of all sizes benefit from the scale of the

VocaLink processing operation and enjoy some of the lowest transaction

charges in Europe.

“”

Created through a merger of Voca and LINK Network

Interchange in July 2007, VocaLink is well

established in the field of electronic payments, with

its automated payment platform carrying out

over 90m transactions per day. VocaLink is also the innovator behind the

new UK Faster Payments service launched in May

2008, which has introduced features other clearing

systems are expected to adopt in the next few years.

From left: Martin Wilson, Richard Parkinson

treasurytoday © August �008 | ��

Winner – Effective Enterprise Risk Management

AbengoaJesusAngelGarcia-Quilez:HeadofCorporateFinance

Currently operating in 70 countries, Abengoa was looking to develop its operations further in the global marketplace. In particular, the company was aiming to reduce, mitigate and cover all of the financial risks to which it was exposed as a result of its activities – notably credit risk, liquidity risk, currency risk and interest rate risk.

As Jesus Angel Garcia-Quilez, Abengoa’s Head of Corporate Finance, explains: “The main purpose of implementing an ERM (Enterprise Risk Management) programme is to be covered from any of the different financial risks you are exposed to in the ordinary course of your activities, optimising business results and the success of your projects.”

In a move to address these risks, Abengoa began designing and implementing a solution that would comply with corporate guidelines, totally updating policies for the management of risk exposure that were originally formulated some 15 years ago.

Abengoa’s risk management policy demands that all types of financial risk are covered as soon as they are generated. Essentially this means that risks must be addressed as soon as a particular contract is negotiated with the client.

Working in conjunction with leading financial institutions, Abengoa was able to design a range of financial products to cover each type of risk:

n Credit risk was covered by previously negotiated financial lines of discount without recourse.

n Liquidity risk was covered by the same financial lines without recourse, combined with facility lines for payments to suppliers. At the same time, this coverage is complemented by Abengoa’s financial and credit

lines, which are necessary for investments and operations defined in the financial strategy of the company – all with a minimum availability of five years.

n The exchange rate risk faced by the company was mainly covered through conveyance contracts for all payments and receivables in different currencies.

n Interest risk, meanwhile, was resolved through the individual coverage of interest rates for each project that had a determined debt, combined with a general coverage of interest rates for all the lines of working capital present in the group. Coverage involved the use of both futures and derivative contracts, allowing the company to keep a secured and controlled position in terms of interest risk and the effect that this risk has on the company’s balance sheet.

By designing and implementing an ERM programme with the capability of mitigating, controlling and covering the various types of financial risk associated with the day-to-day activities of operation, Abengoa has created an increasingly secure financial position, optimising business results which are now only exposed to the company’s performance.

As well as mitigating the risks themselves, a number of other benefits have arisen from the project. These include improvements in the company’s credit rating, working capital ratios and process efficiencies. “Once you are able to put in place a global and universal risk management policy in an efficient manner, you really get a competitive advantage, and that creates value for the company,” says Garcia-Quilez.

Once you are able to put in place a global and universal risk management

policy in an efficient manner, you really get a competitive advantage, and

that creates value for the company.“

”Abengoa is a technology company which applies innovative solutions for sustainable development in the environment and energy sectors. With over 20,000 members of staff and a presence through subsidiaries in more than 70 countries, Abengoa’s revenues in 2007 exceeded €3 billion.

From left: Jesus Angel Garcia-Quilez, Richard Parkinson

�� | treasurytoday © August �008

Highly Commended – Effective Enterprise Risk Management

NovelisAGFriedrichFloto:EuropeanTreasurer

“Novelis’ treasury in Europe comprises mainly FX and interest management, metal management and cash management,” says Friedrich Floto, European Treasurer of Novelis. “We also control the insurance programmes and are responsible for credit management in terms of customer credit.”

Novelis was aiming to centralise all of these activities into its treasury centre based in Zurich in order to increase efficiencies and improve risk management, particularly relating to liquidity risk.

However, in order to achieve this, a number of obstacles had to be overcome. One of these related to the conditions of Novelis’ complex syndicated loan, which needed to be taken into account.

“The pledge of assets to the bank syndicate and a very tight covenant package meant a difficult starting basis for the implementation of the European cash management,” Floto explains.

“In addition to the purely technical aspects, it was in particular the special legal features, the fixing of the judicial locations and the complexity of the agreements which were a true challenge, on account of the differing state-law provisions.”

Novelis chose Commerzbank to manage the cash pooling, initially because the bank was part of a lender group that granted Novelis two syndicated loans of currently $1,760m in total. Working with Commerzbank, Novelis set up a euro cash pool at the beginning of February 2007.

Consisting of several automated domestic zero balance cash pooling and cross-border cash pooling agreements that regulate the payment flows of Novelis’ companies in Luxembourg, Italy, England, France, Switzerland and Germany,

the accounts are then pooled on the master account of Novelis AG in Berlin.

As a result of this, the treasury now operates with greater efficiency and allows for optimised cash and FX flow, with significant cost savings and optimisations. Meanwhile, all of the company’s hedging activities, ranging from FX to commodity hedging, are handled on a centralised basis.

“The sheer complexity of bringing together various companies in different countries with underlying divergent legal jurisdictions and diverse currency accounts into a functioning cash pool was implemented professionally in a relatively short period of time, creating a highly professional treasury management structure,” says Floto.

“All decentralised activities with regard to working capital as well as risk management have been absorbed by the new set-up.”

In addition to the purely technical aspects, it was in

particular the special legal features, the fixing of the judicial locations

and the complexity of the agreements which

were a true challenge, on account of the differing

state-law provisions.

“”

Novelis is the world’s leading producer of

aluminium rolling products. Operating in 11 countries with

approximately 12,900 employees, the company

reported net sales of $11.2 billion in 2007.

Novelis was acquired by Hindalco Industries

Limited, part of the India-based Aditya Birla

Group, in 2007.

From left: Ulf Gedamke (Commerzbank), Friedrich Floto and Richard Parkinson

treasurytoday © August �008 | �3

Winner – Mid-market Treasury

Robbins&MyersInc.MichaelMcAdams:Treasurer

Although its headquarters are based in the US, in recent years Robbins & Myers has expanded throughout Europe, both organically and through a number of acquisitions. As a result, individual entities operated a variety of accounting and banking systems, with the company headquarters maintaining visibility over only 60% of its numerous bank accounts.

The company’s multiple banking relationships, meanwhile, resulted in high banking costs, manually intensive and costly cash concentration, and no economies of scale. Furthermore, the company had no consolidated liquidity position, individual entities found themselves borrowing locally at high cost, and only 25% of the available credit lines were being utilised.

With such a fragmented structure, Michael McAdams, Treasurer of Robbins & Myers, developed the following goals: rationalise bank relationships, improve visibility over accounts, increase yields on balances, improve process efficiencies and further strengthen internal controls. The company’s new senior management team provided the support necessary to initiate a project to achieve these ambitious goals.

Having reduced its European banking structure from 22 banks to just nine, Robbins & Myers conducted a rigorous evaluation process in 2007 to select a bank to lead its pan-European cash management project, choosing JPMorgan because of its demonstrated success in offering similar, seamless solutions.

Automated cash concentration structures were established for the major currencies (sterling, dollars and euro), and standalone accounts were opened for Swiss francs. In-country accounts were subsequently set up in the UK, Germany, Switzerland, Italy, Belgium and Spain for local payments and receipts.

Robbins & Myers’ treasury team drove the project from the Dayton headquarters, working closely with local finance managers and relying on JPMorgan Chase expertise for implementation assistance. One of the key elements of the solution was the creation of a SOX-compliant structure with the required levels of security, visibility and control from account opening and operation to account visibility and payment approvals.

“This complex liquidity and technology solution was implemented across seven countries in just four months, ready to be SOX audited and to go live within the financial calendar year,” says McAdams.

In implementing the solution, Robbins & Myers has achieved the targets it set out to meet. The strategy of centralising selected functions to comply with SOX requirements has eliminated local bilateral credit lines, consolidated credit to a single in-house bank, improved interest yields on account balances and improved processes for trade finance requests. Economies of scale have been achieved in transactional pricing and bank costs have been reduced by over $200,000 per year.

According to McAdams, the success of this far-reaching project can be attributed to a number of factors, including support from local finance managers, the setting of ambitious but achievable goals and a gradual approach to treasury centralisation supported by a dedicated team.

As a result, McAdams concludes, “Robbins & Myers has developed a world-class, highly-effective treasury function which demonstrates how an efficient cash management structure can provide quantifiable benefits – achievable within an aggressive timeline and with a relatively small, previously decentralised, treasury and finance structure.”

This complex liquidity and technology solution was implemented across seven countries in just four months, ready to be SOX audited and to go live within

the financial calendar year.“

”Robbins & Myers is a leading supplier of highly engineered equipment and systems for the global energy, industrial, chemical and pharmaceutical markets. Headquartered in Dayton, Ohio in the US, the company’s sales were $695m in 2007.

in partnership with

Michael McAdams