treatment of trusts in divorce (60 minutes) · treatment of trusts in divorce and tips on drafting...

TRANSCRIPT

TREATMENT OF TRUSTS IN DIVORCE

First Run Broadcast: April 7, 2016

1:00 p.m. E.T./12:00 p.m. C.T./11:00 a.m. M.T./10:00 a.m. P.T. (60 minutes)

One of the most fierce – and financially important – disputes in a divorce may be what assets

held in trust are subject to martial division or other claim. Though one of the chief protections of

a trust is shielding assets from claimants, marital or otherwise, there are many exceptions. The

assets of certain trusts may be subject to marital claims but in many others assets are shielded

from a martial claimant but the spouse may make a claim on a distribution interest. Yet, some

distributions are mere “expectancies” and not subject to claim. How a trust is formed – its

specific type and the nature of its distribution provisions – and where it is governed often result

in a very wide range of outcomes. This program will provide you with a practical guide to the

treatment of trusts in divorce and tips on drafting to ensure the integrity of trusts.

Trusts and martial claims – what assets or income may be claimed?

How the type of trust may determine whether its assets are subject to claim or not

Types of interests in trusts – what types of rights are subject to division and which are

not?

Determining when an interest becomes separate and subject to a divorcing spouse’s claim

Understanding the intricacies of valuing a trust in a divorce – what portion of

appreciation is subject to division?

Special issues in multi-generational trusts

Multijurisdictional issues in the division of trust assets

Speaker:

Jeremiah W. Doyle, IV is senior vice president in the Boston office of BNY Mellon Wealth

Management, where he provides integrated wealth management advice to high net worth

individuals on holding, managing and transferring wealth in a tax-efficient manner. He is the

editor and co-author of “Preparing Fiduciary Income Tax Returns,” a contributing author of

Preparing Estate Tax Returns, and a contributing author of “Understanding and Using Trusts,”

all published by Massachusetts Continuing Legal Education. Mr. Doyle received his B.S. from

Providence College, his J.D. form Hamline University Law School, and his LL.M. in banking

from Boston University Law School.

VT Bar Association Continuing Legal Education Registration Form

Please complete all of the requested information, print this application, and fax with credit info or mail it with payment to: Vermont Bar Association, PO Box 100, Montpelier, VT 05601-0100. Fax: (802) 223-1573 PLEASE USE ONE REGISTRATION FORM PER PERSON. First Name ________________________ Middle Initial____Last Name___________________________

Firm/Organization _____________________________________________________________________

Address ______________________________________________________________________________

City _________________________________ State ____________ ZIP Code ______________________

Phone # ____________________________Fax # ______________________

E-Mail Address ________________________________________________________________________

Treatment of Trusts in Divorce Teleseminar April 7, 2016 1:00PM – 2:00PM

1.0 MCLE GENERAL CREDITS

PAYMENT METHOD:

Check enclosed (made payable to Vermont Bar Association) Amount: _________ Credit Card (American Express, Discover, Visa or Mastercard) Credit Card # _______________________________________ Exp. Date _______________ Cardholder: __________________________________________________________________

VBA Members $75 Non-VBA Members $115

NO REFUNDS AFTER March 31, 2016

Vermont Bar Association

CERTIFICATE OF ATTENDANCE

Please note: This form is for your records in the event you are audited Sponsor: Vermont Bar Association Date: April 7, 2016 Seminar Title: Treatment of Trusts in Divorce Location: Teleseminar - LIVE Credits: 1.0 MCLE General Credit Program Minutes: 60 General Luncheon addresses, business meetings, receptions are not to be included in the computation of credit. This form denotes full attendance. If you arrive late or leave prior to the program ending time, it is your responsibility to adjust CLE hours accordingly.

BNY Mellon Wealth Management 1

TRUSTS AND DIVORCE:

SELECTED ISSUES

Jeremiah W. Doyle IV, Esq.

Senior Vice President

BNY Mellon Wealth Management

Boston, MA

BNY Mellon Wealth Management 2

TRUSTS – EXPOSURE TO MARITAL CLAIMS

BNY Mellon Wealth Management 3

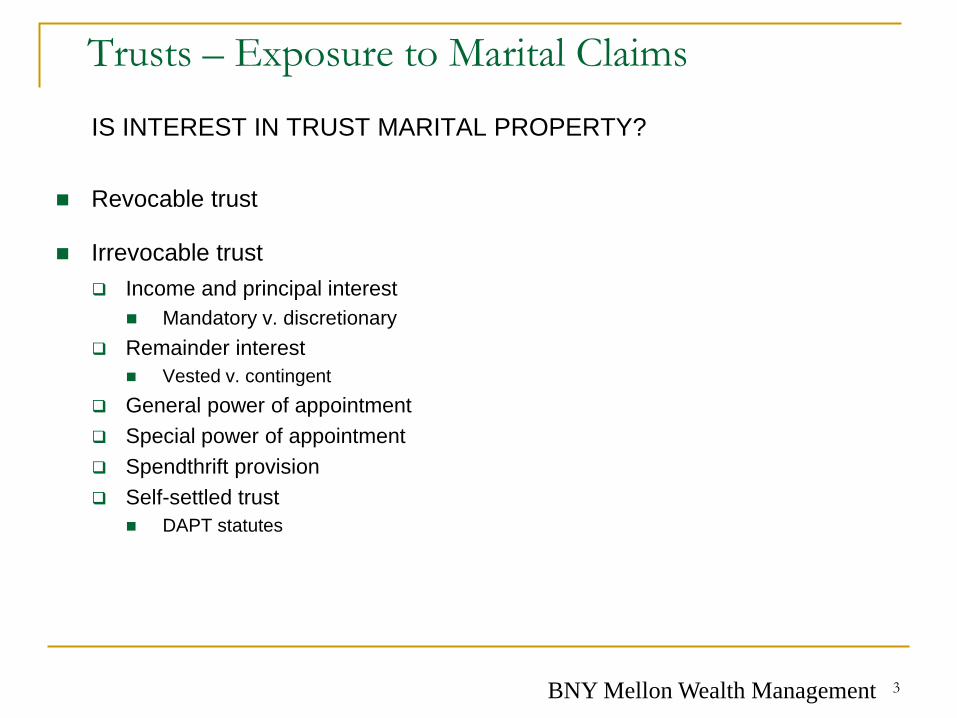

Trusts – Exposure to Marital Claims

IS INTEREST IN TRUST MARITAL PROPERTY?

Revocable trust

Irrevocable trust Income and principal interest

Mandatory v. discretionary

Remainder interest

Vested v. contingent

General power of appointment

Special power of appointment

Spendthrift provision

Self-settled trust

DAPT statutes

BNY Mellon Wealth Management 4

Trusts – Exposure to Marital Claims

REVOCABLE TRUST

As to non-grantor beneficiary, right in revocable trust is a “mere

expectancy”

Non-grantor beneficiary’s interest does not constitute an interest in

property for divorce purposes

Assets treated as owned by grantor

BNY Mellon Wealth Management 5

Trusts – Exposure to Marital Claims

IRREVOCABLE TRUST – DISCRETIONARY INTEREST, INDEPENDENT

TRUSTEE

Discretionary income or principal interest of non-grantor beneficiary

– generally, not interest in property for divorce purposes

Beneficiary has no enforceable rights to distributions

Most effective way of keeping non-grantor beneficiary’s creditors away

from beneficiary’s interest in the trust

Better argument for protection if distributions are in the trustee’s

“absolute”, “sole” or “unfettered” discretion

BNY Mellon Wealth Management 6

Trusts – Exposure to Marital Claims

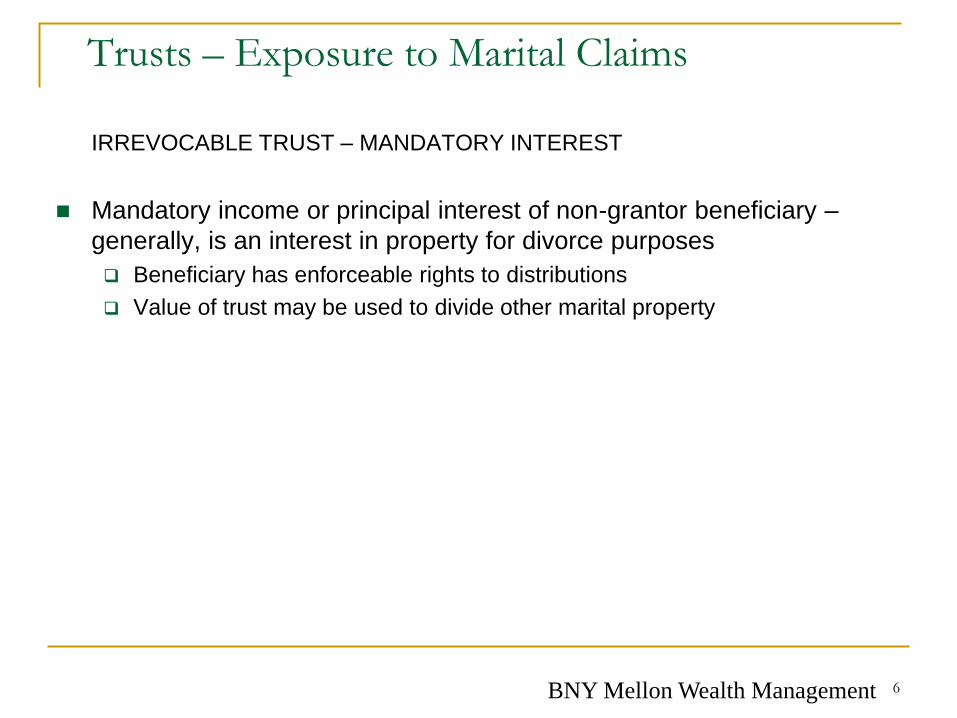

IRREVOCABLE TRUST – MANDATORY INTEREST

Mandatory income or principal interest of non-grantor beneficiary –

generally, is an interest in property for divorce purposes

Beneficiary has enforceable rights to distributions

Value of trust may be used to divide other marital property

BNY Mellon Wealth Management 7

Trusts – Exposure to Marital Claims

IRREVOCABLE TRUST – REMAINDER INTEREST

Traditionally, law focused on whether remainder interest was

vested or contingent

Vested remainder interest – sufficiently certain to constitute an interest

in property

Contingent remainder interest – too speculative to constitute an interest

in property

Massachusetts solution – rejects the mechanical use of the

common law vested/contingent distinction to determine if remainder

interest is property for equitable distribution purposes

Instead, Massachusetts adopts a general test of speculativeness i.e.

whether future acquisition of assets is “fairly certain”

BNY Mellon Wealth Management 8

Trusts – Exposure to Marital Claims

IRREVOCABLE TRUST – GPOA

Common law rule – unexercised GPOA created by person other than the holder of the power, cannot be reached by donee’s creditors

Non-grantor holder of a GPOA cannot be compelled to exercise it

Until the donee exercises the power, he has not accepted control over the appointive assets that gives him the equivalent of ownership of them

If GPOA is exercised, property subject to power is accessible by powerholder’s creditors

Restatement (Third) of Trusts – creditors of non-self settled GPOA can reach the property even if the power is unexercised i.e. it is an ownership equivalent.

UTC in accord with Restatement (Third)

BNY Mellon Wealth Management 9

Trusts – Exposure to Marital Claims

IRREVOCABLE TRUST – SPOA

Common law rule – cannot be reached by powerholder’s creditors

whether or not the power is exercised

BNY Mellon Wealth Management 10

Trusts – Exposure to Marital Claims

IRREVOCABLE TRUST – SPENDTHRIFT PROVISION

Prevents transfer of trust beneficiary’s interest to another

Most courts will respect a spendthrift provision with one exception:

divorce related issues

Historically, Massachusetts enforced spendthrift provisions, even

against former spouses.

Restatement (Third) of Trusts §58 gives spouses, former spouses and

children access to a beneficiary’s equitable interest in a trust despite a

spendthrift provision

BNY Mellon Wealth Management 11

Trusts - Exposure to Marital Claims

IRREVOCABLE TRUST – UNIQUE APPROACH

Trust provisions either limit or deny distributions to beneficiary until

the beneficiary has entered into a pre-nuptial agreement that meet

certain pre-defined parameters

Make the person who created the trust the bad guy

Enforcement is untested

BNY Mellon Wealth Management 12

DOMESTIC ASSET PROTECTION TRUSTS

BNY Mellon Wealth Management 13

Domestic Asset Protection Trusts

IRREVOCABLE TRUST – SELF-SETTLED TRUSTS

Created by party who is also a beneficiary

Common law rule: assets in self-settled trust are subject to donor’s

creditors e.g. spouse for support

Restatement (Third) of Trusts and UTC in accord

BNY Mellon Wealth Management 14

Domestic Asset Protection Trusts IRREVOCABLE TRUST – DAPT

Designed to protect self-settled trusts from creditors

Alaska, Colorado, Delaware, Hawaii, Mississippi, Missouri, Nevada,

New Hampshire, Ohio, Rhode Island, South Dakota, Tennessee,

Utah, Virginia and Wyoming have enacted self-settled trust

legislation

Creditors not permitted to reach assets of trust

In most cases (except Alaska, Nevada, Virginia and Wyoming) spouses

excluded from list of creditors who cannot reach trust assets

In a number of DAPT states the spouse must be married to the grantor

at the time of the transfer to the DAPT to be an exception creditor

Otherwise, spouse has to sue with the S/L claiming a fraudulent

transfer and prove an actual intent to defraud – not easy

UTC has rejected approach taken in DAPT states

BNY Mellon Wealth Management 15

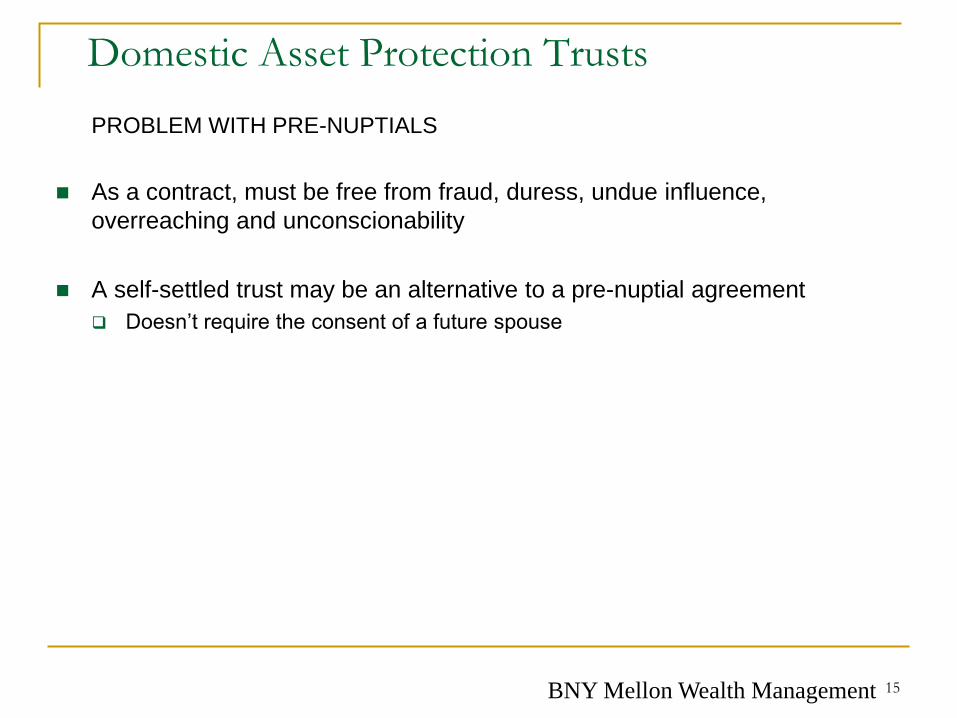

Domestic Asset Protection Trusts

PROBLEM WITH PRE-NUPTIALS

As a contract, must be free from fraud, duress, undue influence,

overreaching and unconscionability

A self-settled trust may be an alternative to a pre-nuptial agreement

Doesn’t require the consent of a future spouse

BNY Mellon Wealth Management 16

Domestic Asset Protection Trusts

SEMINAL CASE – NICHOLS V. EATON (USSC 1875)

USSC says people have the right to dispose of their assets in whatever

manner they wish

There is almost no potential as a creditor for accessing property that is

held in a spendthrift trust

However, there are certain creditors where public policy dictates that

their claims be enforceable even against spendthrift trusts e.g. spouse

and children

These creditors are called exception creditors

The public policy of seeing exception creditors being paid on their claims

outweighs the public policy of enforcing the terms of a spendthrift trust

BNY Mellon Wealth Management 17

Domestic Asset Protection Trusts

BACKGROUND

Historically, self-settled trust have been against public policy

That is the position of Uniform Trust Code. See comment to Section 502 of

the UTC.

Since 1997 in the United States a number of states have enacted

domestic asset protection trust statutes

Currently there are 15 states: AK, CO, DE, HI, MO, MS, NV, NH, OH,

RI, SD, TN, UT, VA and WY. OK also has an ineffective DAPT statute.

BNY Mellon Wealth Management 18

Domestic Asset Protection Trusts

DELAWARE

There are limited circumstances where a creditor will be able to enforce

a claim against the trust property

First situation: There was a fraudulent transfer into the trust

If claim arose after the transfer to the trust, creditor must prove the transfer was

made with actual intent to defraud.

S/L for fraudulent transfer depends on whether the claim arose before or

after the funding of the trust

If claim arose before funding of the trust, S/L is 4 years from the date of the trust

funding or 1 year from the discovery of the funding of the trust

If claim arose after the funding of the trust, S/L is a fixed 4 years from date of trust

funding

BNY Mellon Wealth Management 19

Domestic Asset Protection Trusts

DELAWARE

There are limited circumstances where a creditor will be able to enforce

a claim against the trust property

Second situation: if the creditor is an exception creditor

2 classes of exception creditors: (1) certain tort claims and (2) spousal and child

support claims

However, DE statute defines a spouse or former spouse as persons married to

transferor before the trust was funded.

BNY Mellon Wealth Management 20

Domestic Asset Protection Trusts

DELAWARE

There are limited circumstances where a creditor will be able to enforce

a claim against the trust property

If person funds a DE DAPT and later gets married and then gets divorced,

his spouse or former spouse is not an exception creditor

Spouse would have to proceed against the trust like any other creditor i.e. argue

within the S/L that the transfer was done with intent to defraud

Even if there was an intent to defraud, spouse would have to sue within the 4 year

S/L

If trust was established 4 years before marriage, off the hook

If parties marry before 4 years from the date the trust was established, stay married

for 4 years and you’re off the hook

BNY Mellon Wealth Management 21

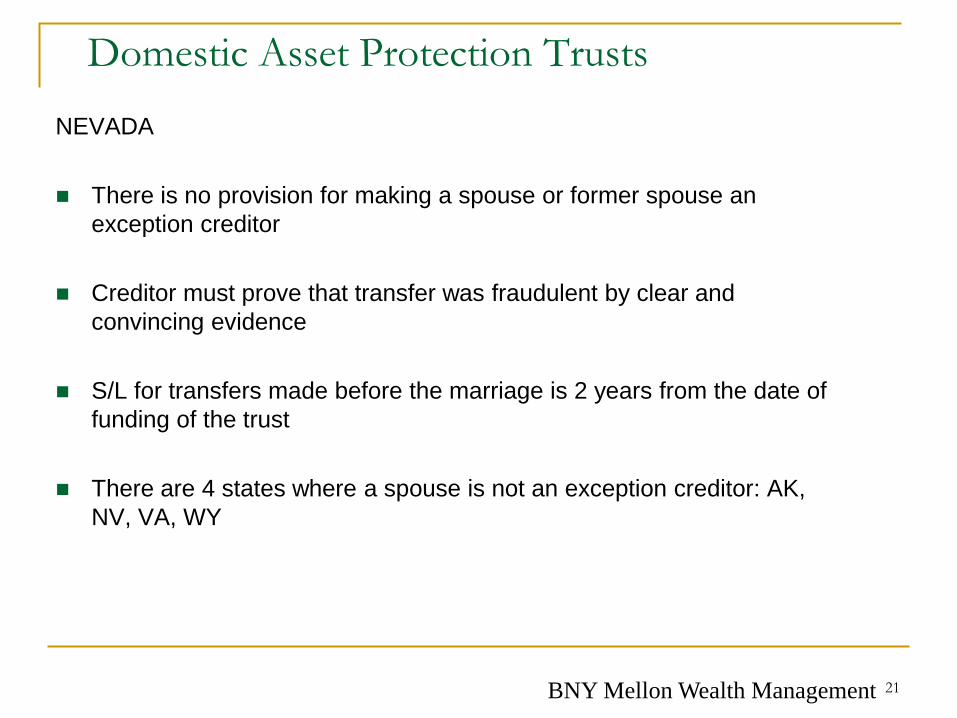

Domestic Asset Protection Trusts

NEVADA

There is no provision for making a spouse or former spouse an

exception creditor

Creditor must prove that transfer was fraudulent by clear and

convincing evidence

S/L for transfers made before the marriage is 2 years from the date of

funding of the trust

There are 4 states where a spouse is not an exception creditor: AK,

NV, VA, WY

BNY Mellon Wealth Management 22

Domestic Asset Protection Trusts

CAN A PERSON ALREADY MARRIED WHO WANTS TO PROTECT

ASSETS GO TO A STATE LIKE AK, NV, VA OR WY AND SET ASIDE

PROEPTY IN A DAPT AND PROTECT IT IN A DIVORCE?

Yes

But better to establish self-settled trust before one gets married in a

DAPT state

BNY Mellon Wealth Management 23

Domestic Asset Protection Trusts

THREE SIGNIFICANT CHALLENGES TO DAPT

Must be separate property – can’t be marital property

Funding was a fraudulent transfer

Conflict of laws issue – can settlor domiciled in one state create a trust

governed by the law in another state?

Restatement 2d of Conflict of Laws Section 273 – validity of trust determined

by law of the state where settlor has manifested an intention that the trust is

to be administered

Scott and Ascher on Trusts – law of the state of administration governs

BNY Mellon Wealth Management 24

Decanting To Protect Trust Assets

Ferri v. Powell-Ferri, 2013 Conn. Supr. NEXIS 1938 (2013)

Court invalidates decanting of trust to take away vested rights over trust

assets and thereby protect trust assets from claims of divorcing spouse

Connecticut case applying Massachusetts law

Trust terms did not grant trustee absolute discretion over trust

distributions

Beneficiary has right to withdraw trust assets upon reaching certain

ages

BNY Mellon Wealth Management 25

Thank You!