trends in dealmaking, fundraising, and partnerships: the ... · • covers announced total deal...

TRANSCRIPT

Trends in Dealmaking, Fundraising, and Partnerships:The Changing Landscape

May 9, 2018

2

Agenda

• Dealmaking 2017 Year-in-Review

• IPO Trends

• Partnering & Preparing for BIO International

• Q&A

Dealmaking 2017

Year-in-Review

Presented by Richard Harrison

This report contains general information only and is based on the experiences and research of Clarivate Analytics practitioners. Clarivate Analytics is not, by means of this report, rendering business, financial, investment, or other professional advice or services. This report is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Clarivate Analytics, its affiliates, and related entities shall not be responsible for any loss sustained by any person who relies on this report.

Disclaimer

5

Overview of all life sciences deals captured by Cortellis in 2017 by percentage

M&A9%

Licenses45%

Asset purchases

4%

Funding19%

Commercial12%

Other10%

Service1%

Total Volume

M&A67%

Licenses20%

Asset Purchases

9%

Total Announced Dollars

4234Total transactions

announced in 2017

$376 BTotal deal dollars

announced in 2017

• Unless otherwise noted, all dollars throughout presentation are USD and are nominal figures (not corrected for inflation).• Transaction types: M&A = 50-100%acquisitions, mergers, reverse mergers; Licenses = licenses, joint ventures, research

collaborations; Asset Purchases = products and business unit acquisitions; Funding = acquisitions of < 50% equity, grants, loans, other funding types; Commercial = distribution, supply, co-promotion agreements; Service = contract services; Other = royalty buyouts, spin-outs, settlements.

Funding 1.6%; Commercial 1.1%, Service 1.2%, Other 0.1%

6

All life sciences deals in 2017 vs. 2016 by number and total deal size $ billion

M&A, 547 M&A, 449

Licenses1749 Licenses

1680

Asset Purch, 250 Asset Purch,

197

Funding866 Funding

889

Commercial514 Commercial

544

Other, 404Other, 435

Service39 Service

40

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2016 2017

Volume

M&A$228

M&A$254

Licenses$88

Licenses$76

Asset Purch, $23

Asset Purch, $32**

**

$0

$50

$100

$150

$200

$250

$300

$350

$400

2016 2017

Announced $ billion

42344369

$376 B

$354 B

** Funding $7.3 (2016), $6.0 (2017); Commercial $4.8, $4.2; Service $0.5, $0.3; Other (royalty buy-out, spin-out, settlement) $2.4, $4.4.

2017 Dealmaking

Year-in-Review

Mergers and Acquisitions (M&A)

8

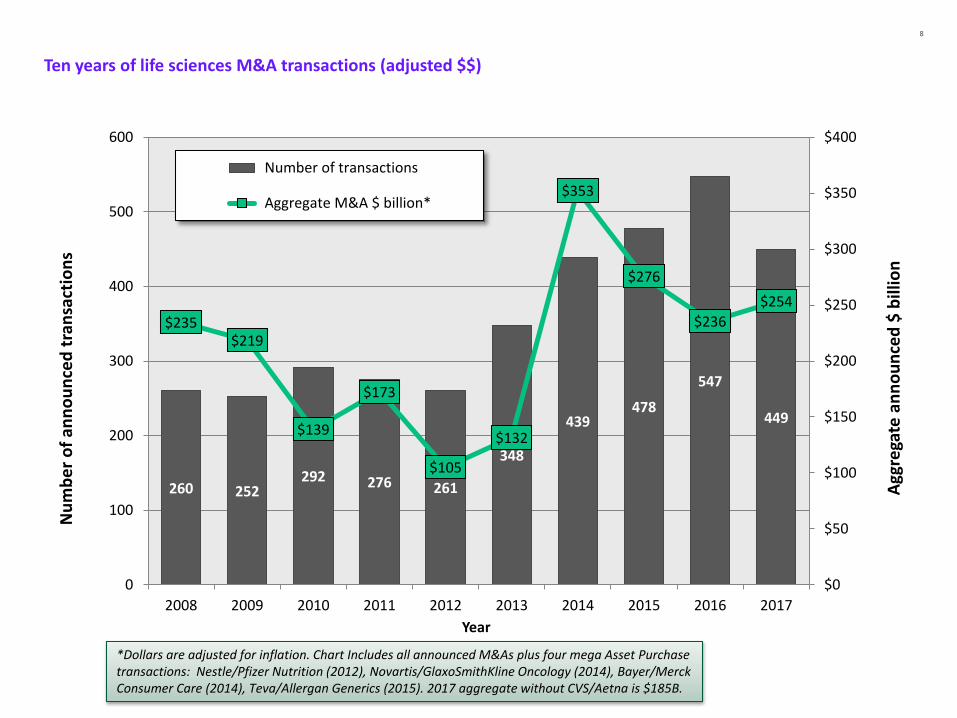

Ten years of life sciences M&A transactions (adjusted $$)

260 252292 276 261

348

439478

547

449

$235$219

$139

$173

$105

$132

$353

$276

$236

$254

$0

$50

$100

$150

$200

$250

$300

$350

$400

0

100

200

300

400

500

600

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Agg

rega

te a

nn

ou

nce

d $

bill

ion

Nu

mb

er

of

ann

ou

nce

d t

ran

sact

ion

s

Year

Number of transactions

Aggregate M&A $ billion*

*Dollars are adjusted for inflation. Chart Includes all announced M&As plus four mega Asset Purchase transactions: Nestle/Pfizer Nutrition (2012), Novartis/GlaxoSmithKline Oncology (2014), Bayer/Merck Consumer Care (2014), Teva/Allergan Generics (2015). 2017 aggregate without CVS/Aetna is $185B.

9

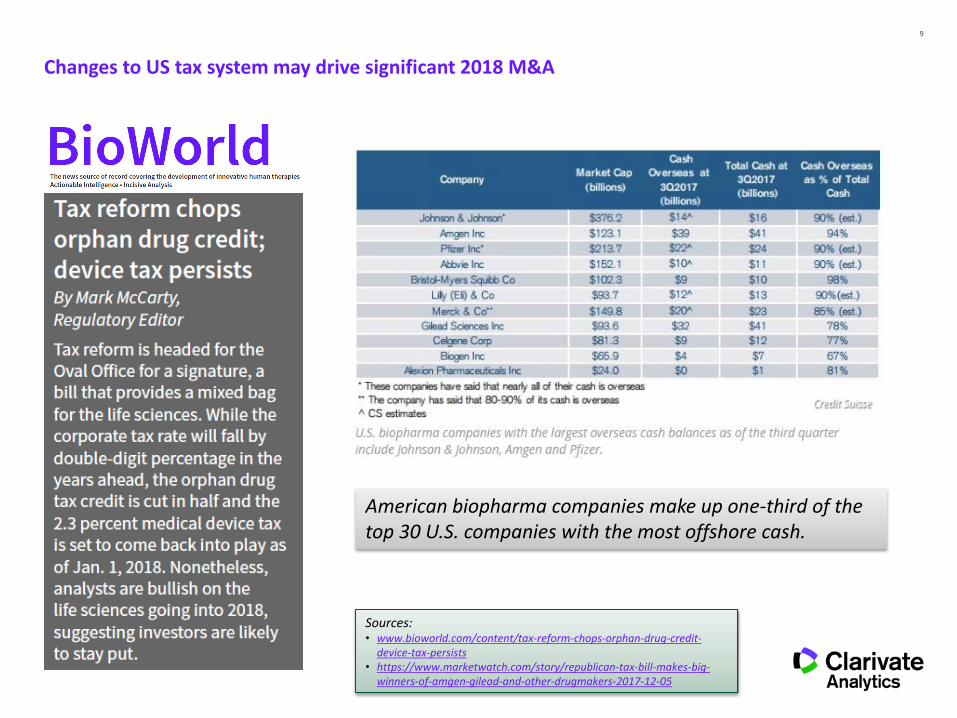

Changes to US tax system may drive significant 2018 M&A

Sources:• www.bioworld.com/content/tax-reform-chops-orphan-drug-credit-

device-tax-persists• https://www.marketwatch.com/story/republican-tax-bill-makes-big-

winners-of-amgen-gilead-and-other-drugmakers-2017-12-05

American biopharma companies make up one-third of the top 30 U.S. companies with the most offshore cash.

10

$2.0

$2.1

$2.3

$2.3

$2.5

$2.8

$3.9

$4.3

$4.6

$4.9

$5.0

$5.2

$6.5

$7.2

$9.1

$11.9

$16.6

$24.2

$30.2

$69.0

$0 $10 $20 $30 $40 $50 $60 $70

Deal size ($ billion)

Top twenty M&As of 2017 by total size

Pharmacies/Insurance

Therapeutics

Medical devices

Nutrition

Therapeutics

Animal health

Services

Medical devices

Therapeutics

Services

Medical devices

Services

Therapeutics

Medical diagnostics

Healthcare data

Medical devices

Therapeutics

Nutrition

Medical devices

Services

Sector

Future milestones

Total at closure $ billion

KEY:

Pending closure

CVS Caremark/Aetna

Johnson & Johnson/Actelion

Reckitt Benckiser/Mead Johnson & Co

Gilead Sciences/Kite Pharma

Thermo Fisher Scientific/Patheon

Avantor Performance Materials/VWR International

Takeda/ARIAD

Pamplona Capital Management/PAREXEL

Unitedhealth Group/DaVita

I N C Research/Inventiv Health Clinical

Fresenius/Akorn

Novartis/Advanced Accelerator Applications

Internet Brands/Webmd Health Corp

Allergan/ZELTIQ Aesthetics

Bristol-Myers Squibb/IFM Therapeutics ($300 M upfront + $2.12 B milestones)

Nestle Health Science/Atrium Innovations

Royal Philips Electronics/The Spectranetics

Fresenius America/NxStage Medical

BD Technologies/CR Bard

M&M Mars/Vca Antech

11

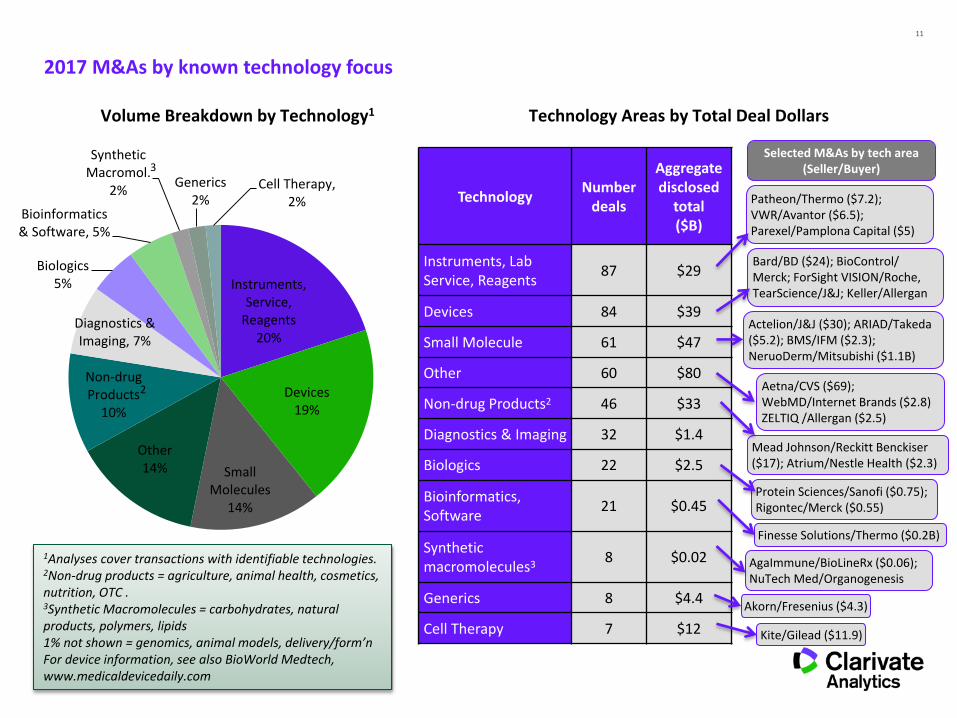

2017 M&As by known technology focus

Volume Breakdown by Technology1 Technology Areas by Total Deal Dollars

Instruments, Service,

Reagents20%

Devices19%

Small Molecules

14%

Other14%

Non-drug Products

10%

Diagnostics & Imaging, 7%

Biologics5%

Bioinformatics & Software, 5%

Synthetic Macromol.

2%Generics

2%Cell Therapy,

2% TechnologyNumber

deals

Aggregatedisclosed

total($B)

Instruments, Lab Service, Reagents

87 $29

Devices 84 $39

Small Molecule 61 $47

Other 60 $80

Non-drug Products2 46 $33

Diagnostics & Imaging 32 $1.4

Biologics 22 $2.5

Bioinformatics, Software

21 $0.45

Syntheticmacromolecules3

8 $0.02

Generics 8 $4.4

Cell Therapy 7 $12

Patheon/Thermo ($7.2);VWR/Avantor ($6.5);Parexel/Pamplona Capital ($5)

Bard/BD ($24); BioControl/ Merck; ForSight VISION/Roche, TearScience/J&J; Keller/Allergan

Aetna/CVS ($69); WebMD/Internet Brands ($2.8) ZELTIQ /Allergan ($2.5)

Actelion/J&J ($30); ARIAD/Takeda ($5.2); BMS/IFM ($2.3); NeruoDerm/Mitsubishi ($1.1B)

Mead Johnson/Reckitt Benckiser ($17); Atrium/Nestle Health ($2.3)

Protein Sciences/Sanofi ($0.75); Rigontec/Merck ($0.55)

Akorn/Fresenius ($4.3)

Kite/Gilead ($11.9)

2

AgaImmune/BioLineRx ($0.06); NuTech Med/Organogenesis

Selected M&As by tech area (Seller/Buyer)

Finesse Solutions/Thermo ($0.2B)

3

1Analyses cover transactions with identifiable technologies.2Non-drug products = agriculture, animal health, cosmetics, nutrition, OTC .3Synthetic Macromolecules = carbohydrates, natural products, polymers, lipids1% not shown = genomics, animal models, delivery/form’nFor device information, see also BioWorld Medtech, www.medicaldevicedaily.com

12

0

10

20

30

40

50

60

Pe

rce

nt

bre

akd

ow

n o

f M

&A

s b

y TA 2016 2017

2016 vs. 2017 M&As by known therapeutic focus

Not shown:

TAs for which there

were ≤5 M&As

announced in 2017:

• Hematology

• Gastroenterology

• Toxicity

• Respiratory

• Endo/Met

Analysis covers M&A transactions with an identifiable core therapeutic focus.

Volume Breakdown by Rx Area 2016 vs. 2017

13

Drug pipeline by therapy area and development stage

Oncology

Immune/ Inflam

Neurology

InfectionGastro-intestinal

Endocrine/ Metabolic

Respiratory

Hematologic

Genito-urinary

Cardio

Derm

Musculo-skeletal

Ophthalm Tox/Intox

Drug pipeline by TA and highest development stageDrug pipeline breakdown by TA

0% 20% 40% 60% 80% 100%

Toxicity/Intox

Ophthalm

Musculoskeletal

Dermatologic

Cardiovascular

Genitourinary

Hematologic

Respiratory

Endo/Metabolic

Gastrointestinal

Infection

Neurology

Immune/Inflam

Oncology

Discovery Phase 1 Phase 2 Phase 3 Launched

Data extracted from Cortellis for Competitive Intelligence and cover all development programs captured as of Dec 31, 2017.

2017 Dealmaking

Year-in-Review

Licenses, Joint Ventures, and Research Collaborations

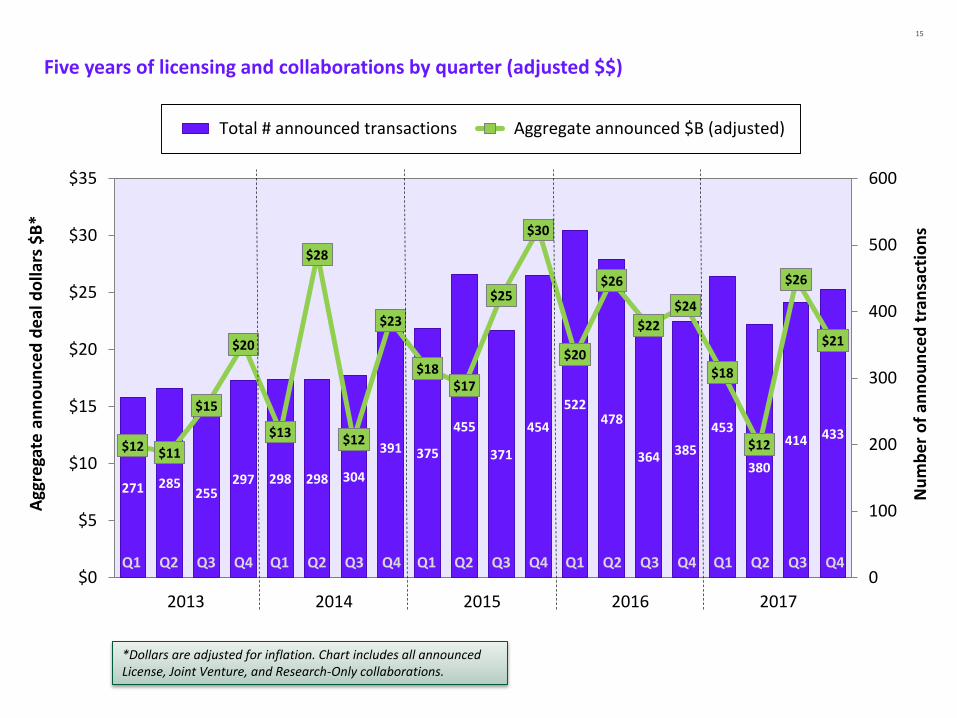

15

Five years of licensing and collaborations by quarter (adjusted $$)

271 285255

297 298 298 304

391 375

455

371

454

522478

364 385

453

380

414 433$12 $11

$15

$20

$13

$28

$12

$23

$18$17

$25

$30

$20

$26

$22

$24

$18

$12

$26

$21

$0

$5

$10

$15

$20

$25

$30

$35

0

100

200

300

400

500

600

Agg

rega

te a

nn

ou

nce

d d

eal

do

llars

$B

*

Nu

mb

er

of

ann

ou

nce

d t

ran

sact

ion

s

Total # announced transactions Aggregate announced $B (adjusted)

2013 2014 2015 2016 2017

Q1 Q2 Q3 Q4Q1 Q2 Q3 Q4Q1 Q2 Q3 Q4Q1 Q2 Q3 Q4Q1 Q2 Q3 Q4

*Dollars are adjusted for inflation. Chart includes all announced License, Joint Venture, and Research-Only collaborations.

16

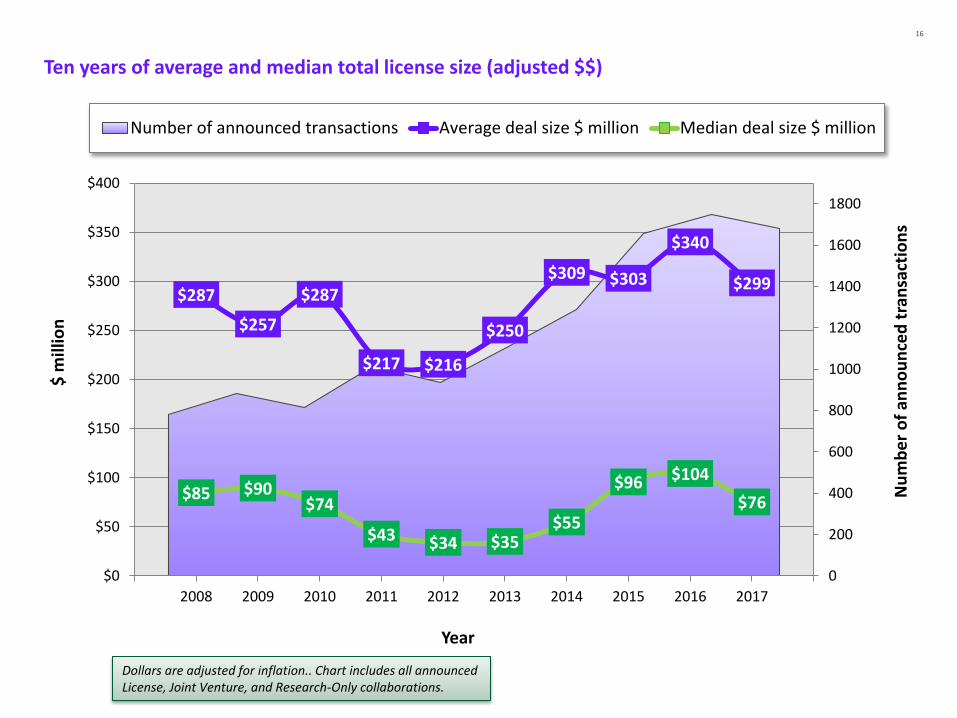

Ten years of average and median total license size (adjusted $$)

$287

$257

$287

$217 $216

$250

$309 $303

$340

$299

$85 $90$74

$43 $34 $35$55

$96 $104

$76

0

200

400

600

800

1000

1200

1400

1600

1800

$0

$50

$100

$150

$200

$250

$300

$350

$400

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Nu

mb

er

of

ann

ou

nce

d t

ran

sact

ion

s

$ m

illio

n

Year

Number of announced transactions Average deal size $ million Median deal size $ million

Dollars are adjusted for inflation.. Chart includes all announced License, Joint Venture, and Research-Only collaborations.

17

$1 billion-plus licensing transactions of 2017

$30

$66

$90

$1,250

$300

$413

$80

$50

$60

$400

$175

$103

$31

$105

$45

$27

$50

$1,600

$1,000

$1,000

$1,030

$1,066

$1,090

$1,110

$1,150

$1,200

$1,260

$1,393

$1,410

$1,452

$1,465

$1,550

$1,655

$1,803

$1,831

$1,865

$2,145

$2,802

$2,830

$8,500

0 1000 2000 3000 4000 5000 6000 7000 8000

Vir/Visterra

Vir/Alnylam

Amgen/Immatics

Merck KGaA/F-Star Delta

Allergan/Editas

Bayer/PeptiDream

Janssen/PeptiDream

Arrys/AskAt

Biogen/Forward

Biogen/BMS

Celgene/BeiGene

Dermira/Roche

Janssen/Zymeworks

Amgen/CytomX

Bayer/Loxo

Novartis/Ionis/Akcea

Eli Lilly/CureVac

Servier/Pieris

BMS/Halozyme

AstraZeneca/Pieris

Sanofi/Ablynx

Allergan/Assembly

Merck/AstraZeneca

Upfront + equity ($M)

Total deal value ($M)

Oncology /Launched

GI/Discovery

Immune-Inflam/Discovery

Respiratory/Discovery

Oncology/Discovery

Oncology/Discovery

Cardio/Phase 2

Oncology /Phase 2 (upfront undisclosed)

Unspecified/Discovery

Derm/Phase 2

Oncology/Launched

Immune-inflam/Launched

Metabolic, Cardio/Discovery (upfront undisclosed)

Diverse/Discovery (upfront undisclosed)

Ophth/Discovery

Oncology/Discovery

Infection/Discovery (upfront undisclosed)

Infection/Phase 2 (upfront undisclosed)

Neuro/Phase 1

Discovery stage alliances

Total announced deal size $ million

Cancer/Drug delivery

Oncology/Discovery

Oncology /Pre-registration

Oncology/Discovery

18

Ten-year trend in upfront cash license payments (adjusted $$)

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

25th percentile Median 75th percentile Average

$ m

illio

n*

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

2017 upfront cash**

25th percentile $3 M

Median $10 M

75th percentile $40 M

Average $35 M

Dollars are adjusted for inflation. Chart includes all announced License, Joint Venture, and Research-Only collaborations that reported an upfront cash payment. **2017 data exclude Merck/AstraZeneca and Biogen/Forward.

19

Top 20 upfront cash payments in 2017 licensing transactions

Rank Licensee Licensor Upfront $M Stage Rx Area

1 Merck & Co AstraZeneca $1,600* Approved Oncology

2 Biogen Forward Pharma $1,250* Approved Autoimm/Inflam

3 Bayer Loxo Oncology $400 Phase 2 Oncology

4 Novartis Ionis $375 Phase 2 Cardiovascular

5 Nanjing Legend Janssen $350 Phase 2 Oncology

6 Biogen Bristol-Myers Squibb $300 Phase 1 Neurology

7 Celgene BeiGene $263 Approved Oncology

8 Merck KGaA Vertex $230 Phase 2 Oncology

9 AbbVie Alector $205 Discovery Neurology

10 Roche Bristol-Myers Squibb $170 Phase 1 Musculoskeletal

11 Incyte MacroGenics $150 Phase 1 Oncology

11 Eli Lilly Nektar $150 Phase 1 Autoimm/Inflam

11 Allergan Lysosomal Therapeutics $150 Discovery Neurology

14 Sanofi AstraZeneca $126 Phase 2 Infection

15 Bristol-Myers Squibb Halozyme $105 Drug delivery Autoimm/Inflam

16 Takeda Oncology TESARO $100 Approved Oncology

17 Allergan Editas Medicine $90 Discovery Ophthalmologic

18 Dermira Roche $80 Phase 2 Dermatologic

19 Jazz ImmunoGen $75 Approved Oncology

20 Pfizer Basilea $72 Discovery Infection

*Calculations on prior slide exclude Merck/AstraZeneca and Biogen/Forward.

20

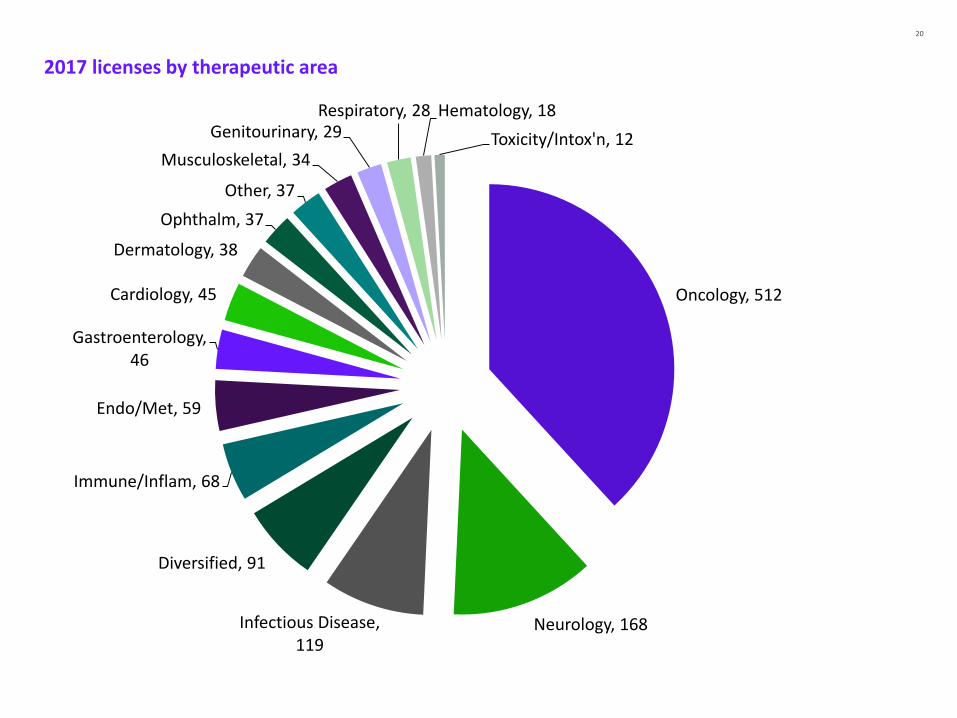

2017 licenses by therapeutic area

Oncology, 512

Neurology, 168Infectious Disease, 119

Diversified, 91

Immune/Inflam, 68

Endo/Met, 59

Gastroenterology, 46

Cardiology, 45

Dermatology, 38

Ophthalm, 37

Other, 37

Musculoskeletal, 34

Genitourinary, 29Respiratory, 28 Hematology, 18

Toxicity/Intox'n, 12

21

2017 license transactions by headquarters of licensor (sellside) party

United States1158

United Kingdom153

Canada108

Japan106

Germany84 China

81

Switzerland; 63

France; 59

Australia; 51

South Korea; 46

Israel; 30Belgium; 29

Denmark; 23

Netherlands; 23

Spain; 23

Sweden; 22

Italy; 18

Ireland; 15

Singapore; 14Finland; 9

India; 9Taiwan; 8Norway; 6

24 other countries < 5 deals each; 40

Other239

By region: North America 1269; Europe 534; Asia 271; Australia/NZ 53; Middle East 32; Central /South America 10; Eastern Europe 7; Africa 2

2017 Dealmaking

Year-in-Review

Top Pharma Dealmakers

23

$0

$10

$20

$30

$40

$50

$60

$70

0

5

10

15

20

25

30

35

40

20

17

to

tal r

eve

nu

es

($ b

illio

n)

Nu

mb

er

of

ann

ou

nce

d t

ran

sact

ion

s

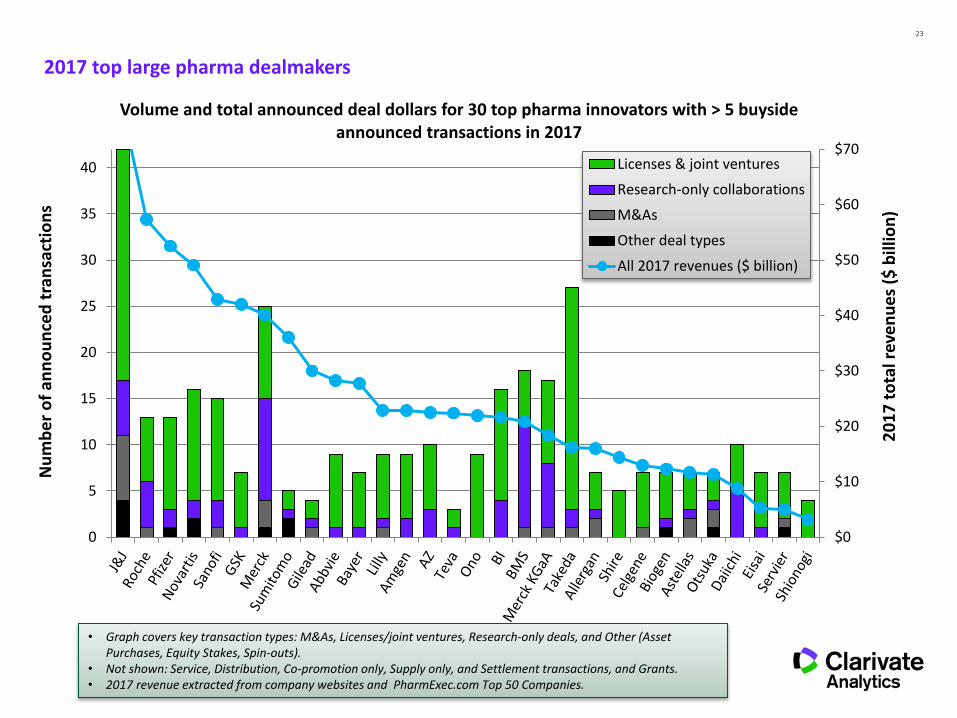

Volume and total announced deal dollars for 30 top pharma innovators with > 5 buyside announced transactions in 2017

Licenses & joint ventures

Research-only collaborations

M&As

Other deal types

All 2017 revenues ($ billion)

2017 top large pharma dealmakers

• Graph covers key transaction types: M&As, Licenses/joint ventures, Research-only deals, and Other (Asset Purchases, Equity Stakes, Spin-outs).

• Not shown: Service, Distribution, Co-promotion only, Supply only, and Settlement transactions, and Grants. • 2017 revenue extracted from company websites and PharmExec.com Top 50 Companies.

24

2017 therapy area focus for top large pharma dealmakers

Oncology

Neuro

Immune/Inflam

Infectious

GI Diversified

Ophthal

Endo/Met

Cardio

Musculoskel

Respiratory

Hematology

Other0

10

20

30

40

50

110

Genitourinary

Volume and total announced deal dollars by therapy area for top pharma dealmakers

• Covers announced total deal size for key transactions types, M&As, Licenses/joint ventures, Research-only deals, and Other (Asset Purchases, Equity Stakes, Spin-outs), with identifiable therapeutic focus areas.

• Not shown: Toxicity, Unknown and Not Applicable therapy areas. • Companies are those among the top 50 pharmaceutical companies who announced 5 or more buyside

transactions in 2017.

Nu

mb

er

of

ann

ou

nce

d t

ran

sact

ion

s w

ith

th

era

py

are

a fo

cus

> $30 billion

$5 - 10 billion

$1 - $5 billion

$0.1 - $0.9 billion

<$100 million or unannounced

Bubble size represents aggregate deal dollars:

Derm

25

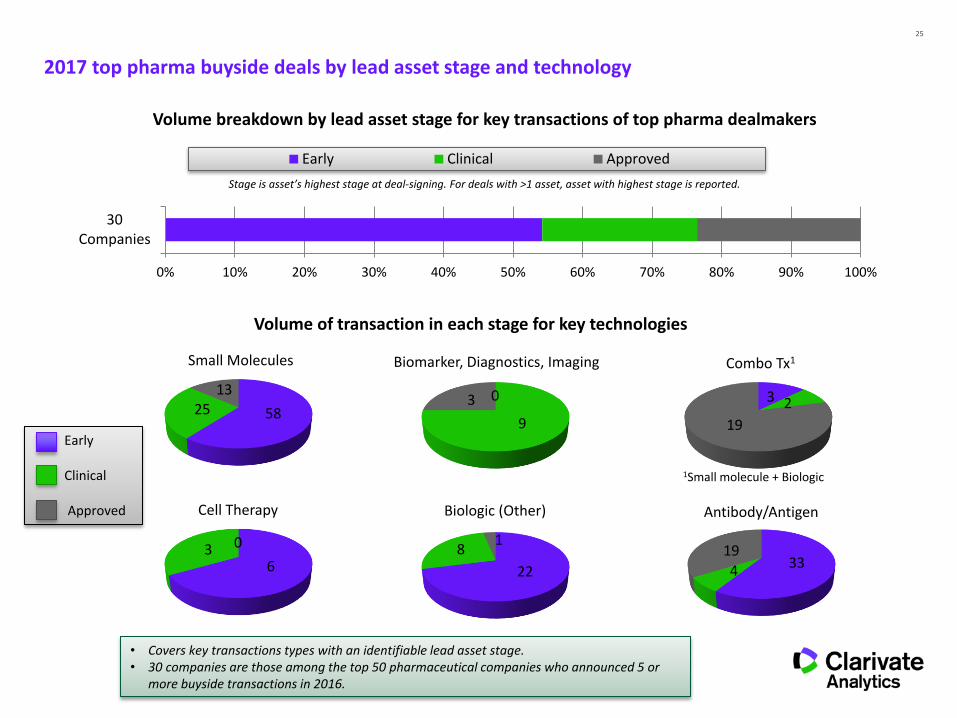

2017 top pharma buyside deals by lead asset stage and technology

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

30Companies

Volume breakdown by lead asset stage for key transactions of top pharma dealmakers

Early Clinical Approved

• Covers key transactions types with an identifiable lead asset stage.• 30 companies are those among the top 50 pharmaceutical companies who announced 5 or

more buyside transactions in 2016.

582513

Small Molecules

334

19

Antibody/Antigen

22

81

Biologic (Other)

63 0

Cell Therapy

3 2

19

Combo Tx1

0

9

3

Biomarker, Diagnostics, Imaging

Stage is asset’s highest stage at deal-signing. For deals with >1 asset, asset with highest stage is reported.

Volume of transaction in each stage for key technologies

1Small molecule + Biologic

Early

Clinical

Approved

26Contributors

Laura Vitez has over 25 years of experience in the life sciences industry. She has held lead or advisory roles at multiple small biotechs, a mid-sized pharma company, and two consulting firms, bringing in over $2B deal dollars. She holds an MS in biochemistry and a BA in mathematics and chemistry

Lisa Christadore has 5+ years consulting with pharmaceutical clients across R&D, clinical, competitive intelligence, and BD. She has interviewed over 100 physicians, scientists, and investors and works closely with Clarivate’s Deals Intelligence team. She is a medical writer, deals enthusiast, and holds a PhD in Biochemistry with a focus on drug discovery.

Helen Dowden is a strategic intelligence professional with more than 20 years pharmaceutical industry experience. She has a PhD in pharmacology, and is currently working as a Consultant within Clarivate’s Life Sciences Professional Services team. Helen has expertise in oncology deals analysis.

Paul D’Souza has over 11 years as a pharmaceutical industry analyst, maintaining and analysing content on various competitive intelligence databases, including Clarivate Analytics’ Cortellis Deals Intelligence module, to support decision making across the pharmaceutical sector. He currently analyses quarterly trends in pharmaceutical mergers & acquisitions and licensing activity and holds an MBA and a BSc in Pharmacology & Physiology.

Jennifer Berbaum is a drug discovery research scientist with over 15 years of experience in all steps of drug discovery. Jen has delivered projects focused on competitive, clinical, and target intelligence, drug device compatibility, breakthrough therapy designation, and R&D outsourcing feasibility. Jen has technical expertise in Cortellis data export and analysis. She has a PhD in Biological Sciences.

IPO Trends

Presented by Peter Winter

28

IPO trends since 2000

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

Biopharma IPO value ($M)

Source: BioWorld

0

10

20

30

40

50

60

70

80

90

Biopharma IPO volume

Source: BioWorld

29

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

IPO value by quarter ($M)

1Q

2Q

3Q

4Q

Source: BioWorld

30

0

5

10

15

20

25

30

35

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

IPO volume by quarter

1Q

2Q

3Q

4Q

Source: BioWorld

31

Notable IPOs 2008-2017

Partnering in 5 Steps

1. Create/update your company’s profile

2. Update your calendar availability

3. Search for potential partners & send tailored meeting requests

4. Actively manage your Message Center

5. BIO will schedule acceptedmeeting requests with mutual availability starting May 14

In & Out-Licensing Intentions (BIO 2018)

Out-Licensing64%

Both

23%

In-Licensing13%

2018 BIO Convention Companies:• Nearly 2/3 are looking

for out-licensing opportunities

• Nearly ¼ are seeking in- and out-licensing

Most Popular Asset Types (BIO 2018)

Most Popular Therapy Areas (BIO 2018)

*Data reflects companies listing a primary or secondary therapeutic area of interest

Investors: Preferred Company Stage (BIO 2018)

2018 BIO Convention Investors slant toward earlier-stage companies

Venture23%

Early stage21%

Growth17%

Seed

16%

Expansion12%

Mezzanine11%

*Investors could designate multiple stages of interest

Investors: Preferred Therapeutic Areas (BIO 2018)

39

Putting It Into Practice

Identifying Target Companies

Segment your search

• Public v. private

• Therapeutic areas of focus

• Last round of funding

• Countries of interest

• In- and out-licensors

• Assets

– Type (cell therapy, protein, small molecule, etc.)

– Development phase

– Clinical indication

– MoA

– Whether asset is partnered

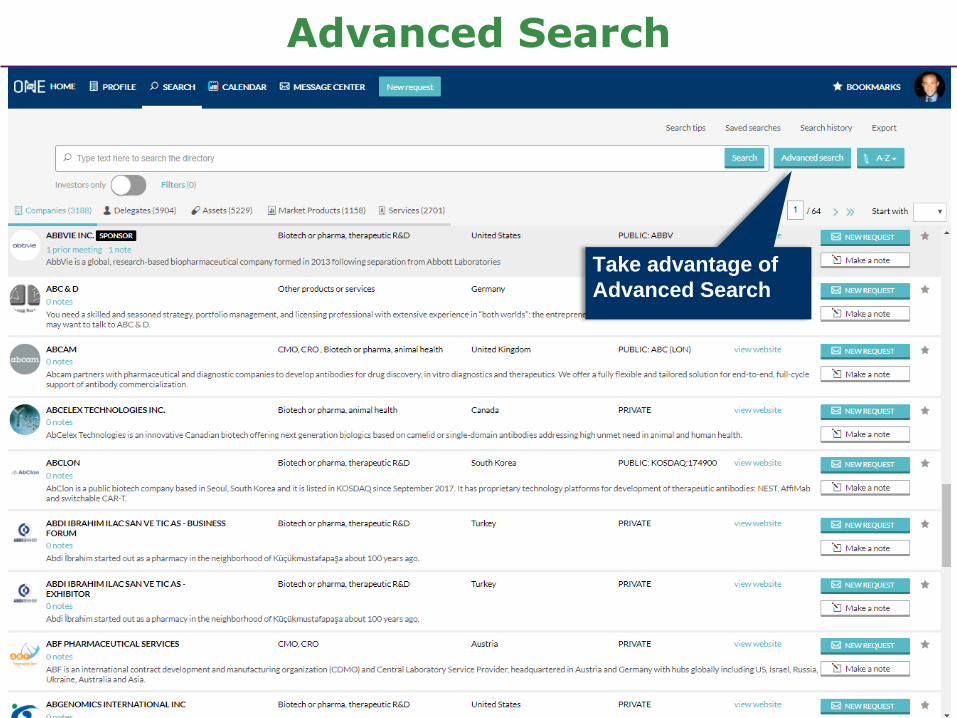

Advanced Search

Take advantage of

Advanced Search

Advanced Search

Combine searches

across tabs

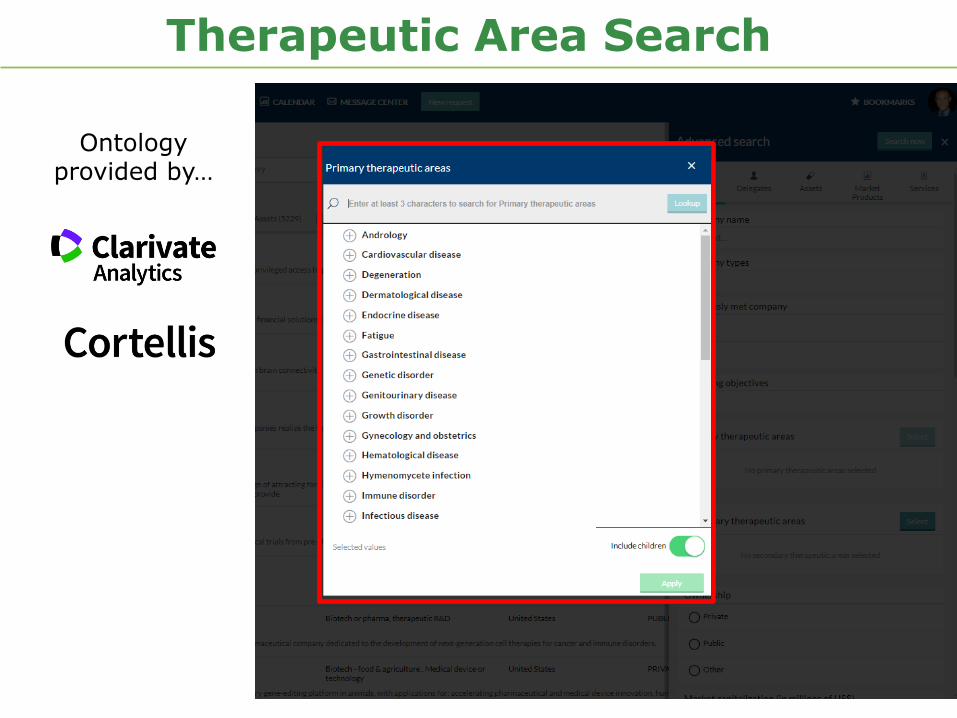

Therapeutic Area Search

Ontology provided by…

Advanced Search

MoA, phase,

technologies,

and more

BIO One-on-One Case StudiesBiotech vs. Biotech. Who secured more meetings?

• Logging in early and checking often for new companies.

• Tailoring the subject of meeting requests.

• Targeting the message body of each meeting request.

• Following up on non-responses (“Requested” meetings) 10 days and 3 days before the Convention.

Participants secured 5X – 7X more meetings by:

Company

Number of

Requests Start Date

Unique

Subject

Lines

Unique

Messages

Scheduled

Meetings

Private Biotech 1 60 4 weeks before 60 60 32

Private Biotech 2 15 1 week before 1 1 6

Public Biotech 1 50 3 weeks before 50 50 35

Public Biotech 2 10 1 week before 2 2 5

5X

7X

Q&A

Thank you!

48

Clarivate Analytics Life Sciences

Clarivate Analytics is the global leader in providing trusted insights and analytics to accelerate the pace of innovation.

Building on a heritage going back more than a century and a half, we have built some of the most trusted brands across the innovation lifecycle, including Web of Science, Cortellis, Derwent, Techstreet, CompuMark, and MarkMonitor.

Today, Clarivate Analytics is a new and independent company on a bold entrepreneurial mission to help our clients radically reduce the time from new ideas to life-changing innovations.

Cortellis Competitive IntelligenceLeading pipeline database for depth and breadth of content

Cortellis Deals IntelligenceRapid insights into critical deal making trends

Cortellis Regulatory IntelligenceMost comprehensive regulatory content and analysis

Cortellis Clinical Trials IntelligenceBroadest source of clinical trials intelligence

MetaCoreProprietary toolbox for discovery of biological pathways

Integrity & Drug Research AdvisorUnique provider of multifaceted drug research content

BioWorld NewsDaily actionable intelligence and incisve analysis