(trends in) logistics and supply chain management in...

TRANSCRIPT

(Trends in)

Logistics and Supply Chain Management

in Europe and Germany

Prof. Dr. Tobias Held, University of Applied Sciences Hamburg, Germany

© Heldp. 2

Agenda

1. A Short Overview of Logistics in Europe and Germany

2. Challenges and Trends Impacting Logics and Supply Chain Management

3. Some Current Innovations and Changes in German Logistics

© Heldp. 3

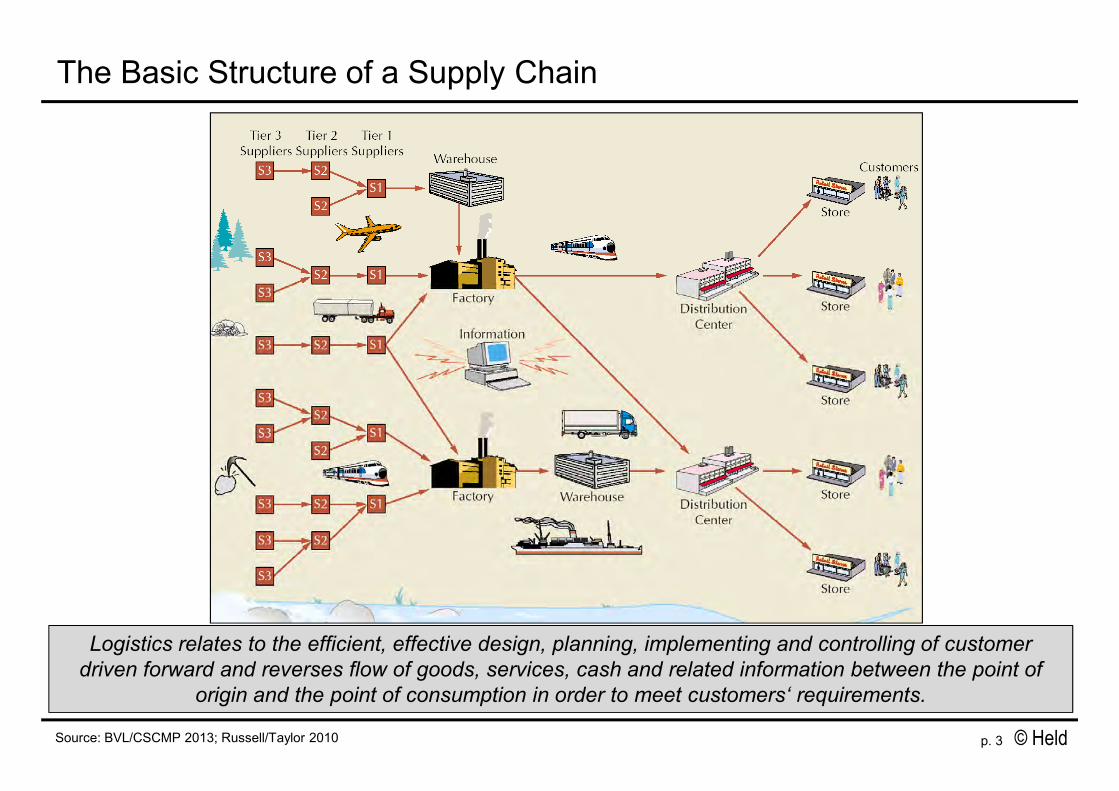

The Basic Structure of a Supply Chain

Source: BVL/CSCMP 2013; Russell/Taylor 2010

Logistics relates to the efficient, effective design, planning, implementing and controlling of customer

driven forward and reverses flow of goods, services, cash and related information between the point of

origin and the point of consumption in order to meet customers‘ requirements.

© Heldp. 4

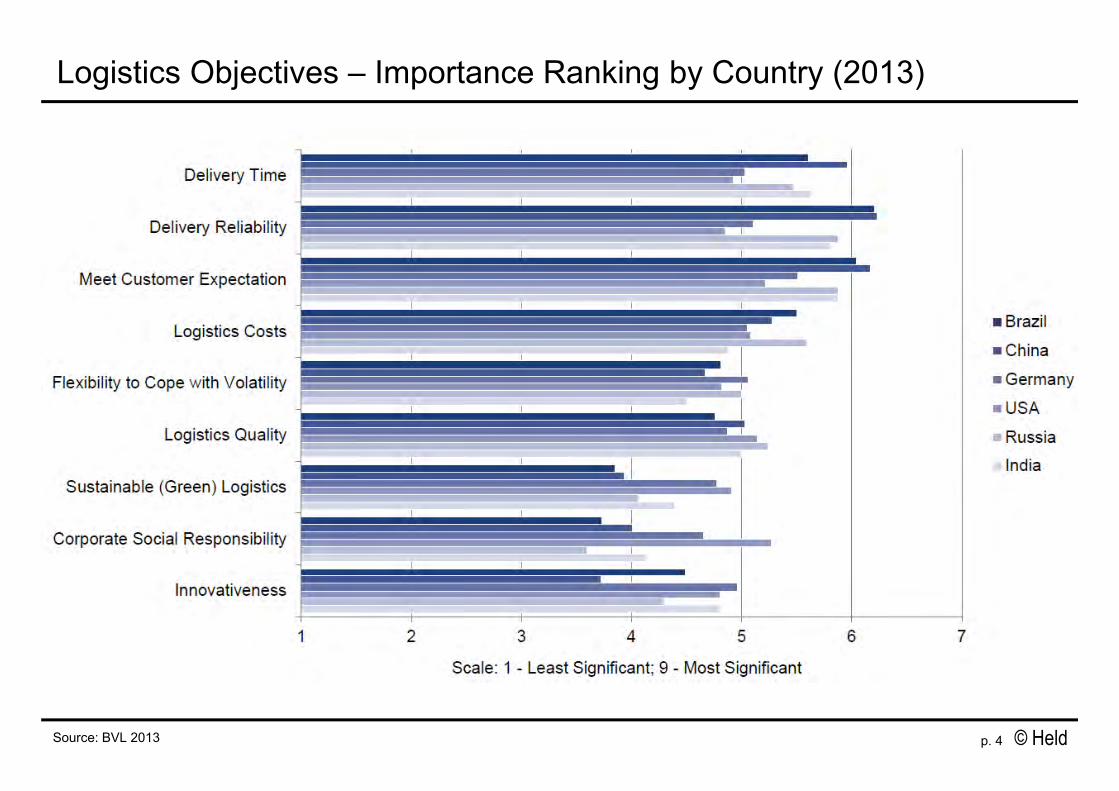

Logistics Objectives – Importance Ranking by Country (2013)

Source: BVL 2013

© Heldp. 5

Agenda

1. A Short Overview of Logistics in Europe and Germany

2. Challenges and Trends Impacting Logics and Supply Chain Management

3. Some Current Innovations and Changes in German Logistics

© Heldp. 6

Market Volume and Tonnages EU29 (2010)

Source: Klaus et al. 2011; Bowersox 2005

Total 930 bn. €

Market Volume Europe

Tonnage in Europe

Inland freight

[million ton kilometers]

Road

Rail

Inland

Waterways

Sea

Pipeline

Air

Transportation

Order Processing

Capital Costs

Warehousing

Administration

Global logistics expenditures equal around 14% of the world´s Gross Domestic Product!

The size of the EU29 logistics market alone is estimated to be € 930 billion!

© Heldp. 7

Market Volume in EU29 by Country (2010)

Source: Klaus et al. 2011

Germany is an important European logistics hub due to the central geographical location

with a market size of more than € 200 billion!

LogisticMarketSize [billion €]

© Heldp. 8

The Logistics Labor Market in Germany

Other sectorsService ProvidersIndustry and Retail

Source: Klaus & Kille 2007

In Million of

Employees

Transport Storage/Transshipping

AdministrativeFunctions

Indirect LogisticsOccupations

0,17 0,430,75 1,13

0,75

0,50

0,25

0

1,00

8%

19%

58%

23%

18%

17%

65%

54%

38%

18%

34%

48%

More than 2.5 million people are working in the logistics market in Germany!

© Heldp. 9

Agenda

1. A Short Overview of Logistics in Europe and Germany

2. Challenges and Trends Impacting Logics and Supply Chain Management

3. Some Current Innovations and Changes in German Logistics

© Heldp. 10

Logistic and Supply Chains are highly impacted by global developments

Global challenges & trends

Logistic / supply chain challenges & trends

Firm level challenges & trends

Source: own

© Heldp. 11

Some Important Global Challenges & Megatrends

• (Asymmetric) population growth and changing age profile: people on earth to 9 billion (2050)

• Radical shifts in global spending power and industrial foot prints

• Increased urbanization: half of the world’s population currently live in urban areas and about 70% will be city dwellers by 2050

• Mega cities: by 2050 there are expected to be more than 27 mega-cities – each with more than 10 million people

• Further globalization: global player companies :17.000 (1990), 75.000 (2009), 170.000 (2020)

• Transport grows faster than world trade and GDP, will double (2025) and grow again 100% until 2060

• Triple sustainability balance: social / economical / environmental

• G

Source: divers

© Heldp. 12

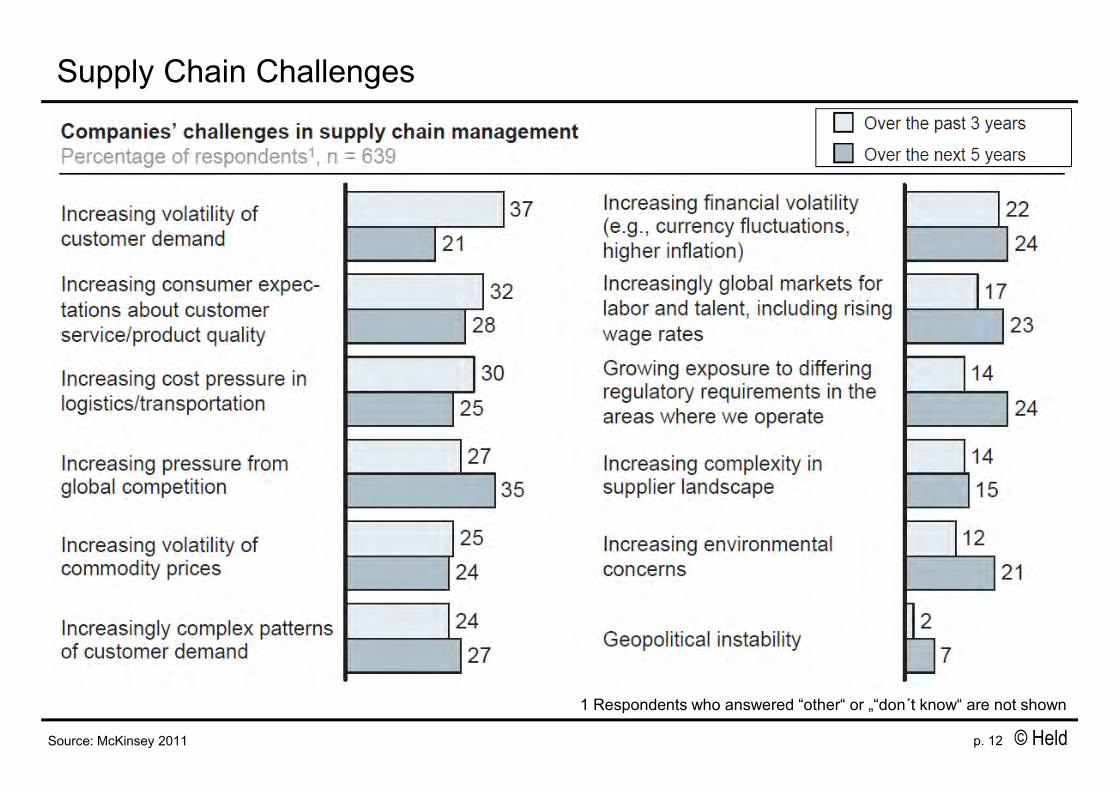

Supply Chain Challenges

Source: McKinsey 2011

1 Respondents who answered “other“ or „“don´t know“ are not shown

© Heldp. 13

Volatility and Logistical Complexity Reduction – Example

There has been a trend in many consumer goods markets towards more and more

harmonized products – in many cases using bigger language clusters

with the same consumer package for several countries!

Source: own, Dr. Oetker KG

Example Product Harmonization: European Dr. Oetker Pizza with 11 countries (7 languages):

© Heldp. 14

Some big challenges facing logistics and supply chain management

Source: Grosse-Ruyken, Jönke, Wagner, and Franklin 2011

© Heldp. 15Source: BBR-Prognose 2010; Statistische Ämter des Bundes / der Länder; Logistik heute 2010; Wildhage & Hector 2007

Demographic Change – Example Germany

Decrease

of the

Young

Increase

of the

Old

Percentage ofpersons under 20

Percentage ofpersons over 60

E.g. approx. 30% of all German truck drivers will retire the next 10 to 15 years!

© Heldp. 16

Types of Talent Shortages Experienced (% of Respondents, 2013)

Source: BVL 2013

© Heldp. 17

The Main Business Regions will Change in the next Decades

Quelle: HDRO; Maddison; Pardee Center for International Futures

Brazil, China and India combined are projected to account for

40% of global output by 2050, up from 10% in 1950!

Share ofglobaloutput

(%)

Projection60

50

40

30

20

10

0

1820 1860 1900 1940 1980 2010 2050

Brasil, China, and India

United States,Germany,

Canada, ItalyFrance, and

United Kingtom

© Heldp. 18

Globalization is highly impacted by Transportation Cost Developments

Source: Baldwin; BVL 2013, n=1,757; *) fugure before 1830 are calculated indirectly; **) Compound average growth rate

Sea freight* Air freight*

CAGR**Percent

Real CostsIndexed, 2004=1

Logistics Costs Trend During 2012Logistics Costs Trend the Last Decades

Increase

Stayconstant

Decrease

Do not know

0% 10% 20% 30% 40% 50%

© Heldp. 19

Logistic Network Consolidation (1/2): Production

P

PP P

P

P

P

P

P

P PPP

PP

P P

PP

P

Example: Production Network of the Henkel Schwarzkopf Personal Care Business Unit

The trend towards fewer but bigger (focused) factories has

led to a more centralized logistic structure in many (European) FMCG-companies!

P

P

Production sitesP

Production sites closed(since 2000)

P

Source: based on Horstmann 2004, own updates. Including former Schwarzkopf & Barnängen sites.

Parma (Italy) Liepvre (France) Raciborz (Poland) Dülken (Germany)Wassertrüdingen (Germany) Maribor (Slovenia)

Yainville (France)Ekerö (Sweden)Frechen/Berlin (3x)/Krefeld (Germany)Dordrecht (Netherlands)Gisors (France)St.Gallen (Switzerland)Castello d’A (Italy)Budapest (Hungary)Kematen/Feldkirchen (Austria)La Coruna (Spain)

© Heldp. 20

D

D

D

D

DC

D

D

D

D

D

D

D

D

D

D

D

D

D

DD

Example: Distribution Structure of the Tesa AG (Consumer Business)

The trend towards fewer but bigger distribution centers / warehouses has

led to a more centralized logistic structure in many (European) FMCG-companies!

Logistic Network Consolidation (2/2): Distribution

D Distribution center

Distribution center closed (since 2000)

D

Central warehouseC

Source: Tesa AG 2006, own updates. All DCs outsourced, exceptions: Copenhagen, Stuttgart and Offenburg.

© Heldp. 21

Sustainability and Environmental Aspects G

Source: BVL 2013

Percentage of Respondents Measuring Different Sustainability Aspects

< are becoming more and more important!

© Heldp. 22

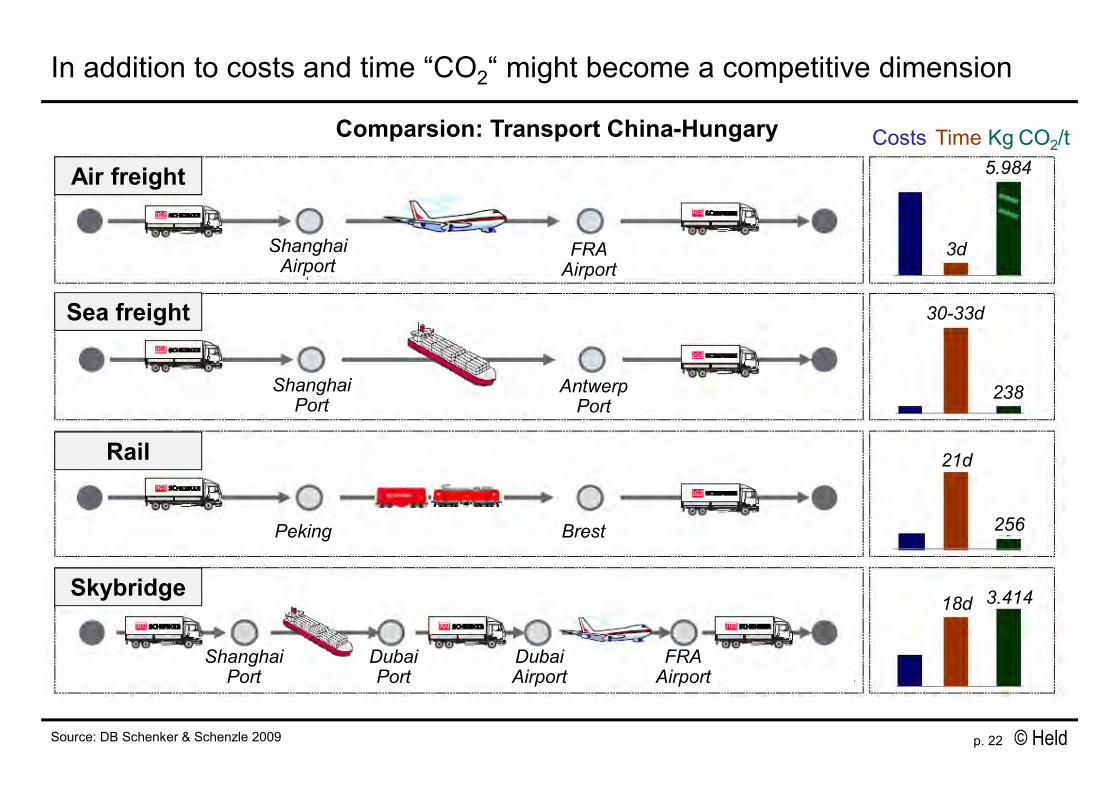

In addition to costs and time “CO2“ might become a competitive dimension

Source: DB Schenker & Schenzle 2009

Comparsion: Transport China-Hungary

Air freight

Sea freight

Rail

Skybridge

Costs Time Kg CO2/t

Peking Brest

ShanghaiAirport

ShanghaiPort

FRAAirport

AntwerpPort

ShanghaiPort

FRAAirport

DubaiAirport

DubaiPort

3d

5.984

30-33d

238

256

21d

18d 3.414

© Heldp. 23

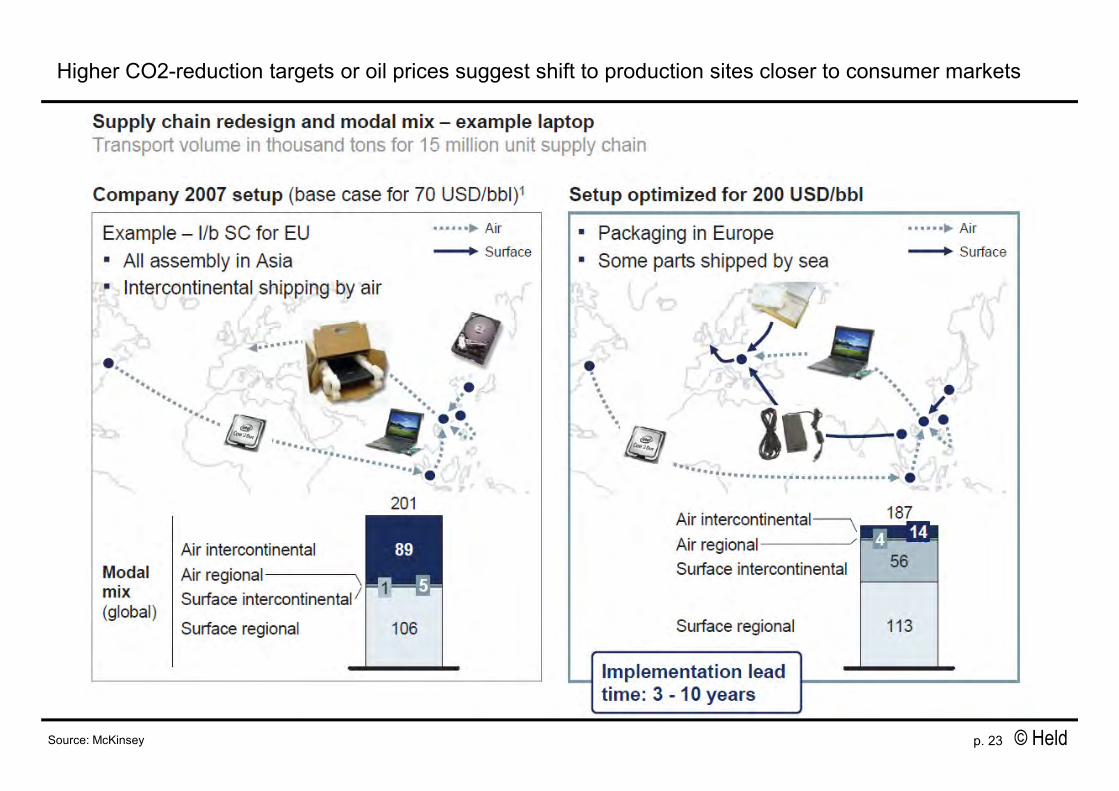

Higher CO2-reduction targets or oil prices suggest shift to production sites closer to consumer markets

Source: McKinsey

© Heldp. 24

The optimal number of storage locations at different Oil-/CO2-PricesG

Source: 4flow 2010; 1) oil price forecast 2030 Energy Information Administration 2010: from 120 und 154 US$/bbl; 1l oil ≈ 3 kg CO2

Variability of the Oil Price 1974 - 2009

Oil PriceForecasts 20301)

+ 10-30 US$/t CO2

Oil price (US$/Barrel)

Optimal number of storeagelocations

0

2

4

6

8

10

12

15 60 105 150 195

Example Industrial Company

Example Trade Company

< has to be calculated individually and an sensitivity-analysis has to be done!

© Heldp. 25

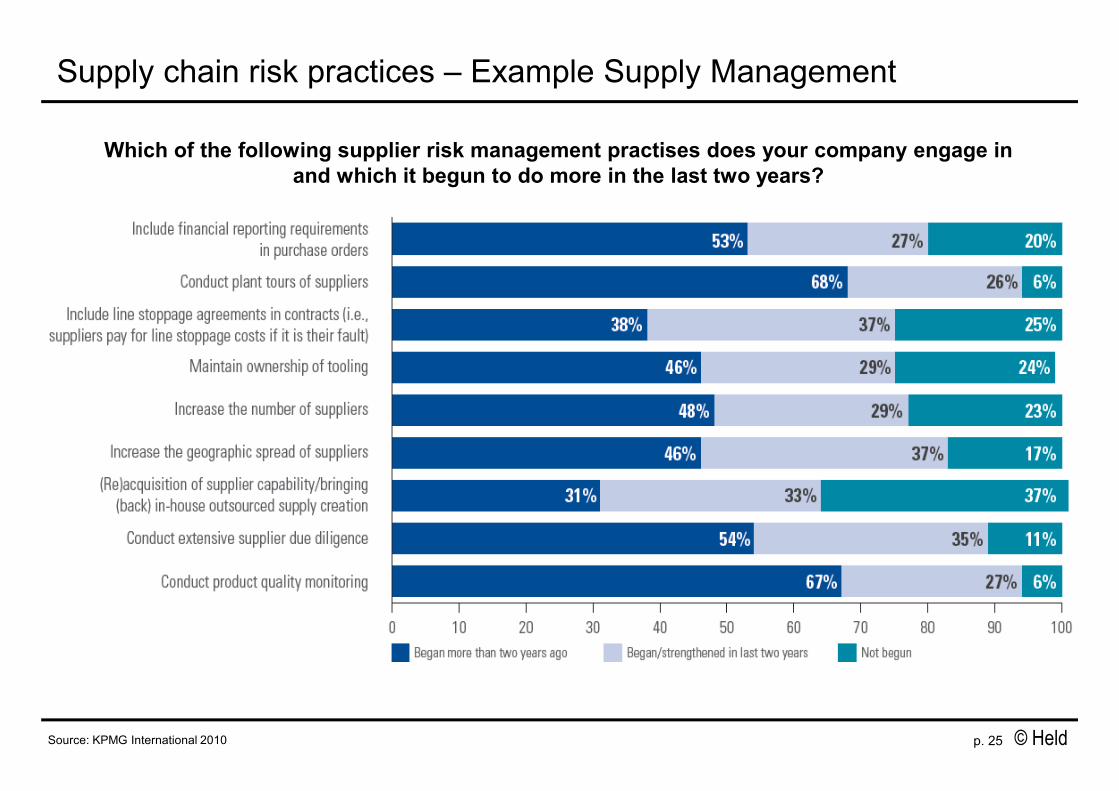

Supply chain risk practices – Example Supply Management

Source: KPMG International 2010

Which of the following supplier risk management practises does your company engage in

and which it begun to do more in the last two years?

© Heldp. 26

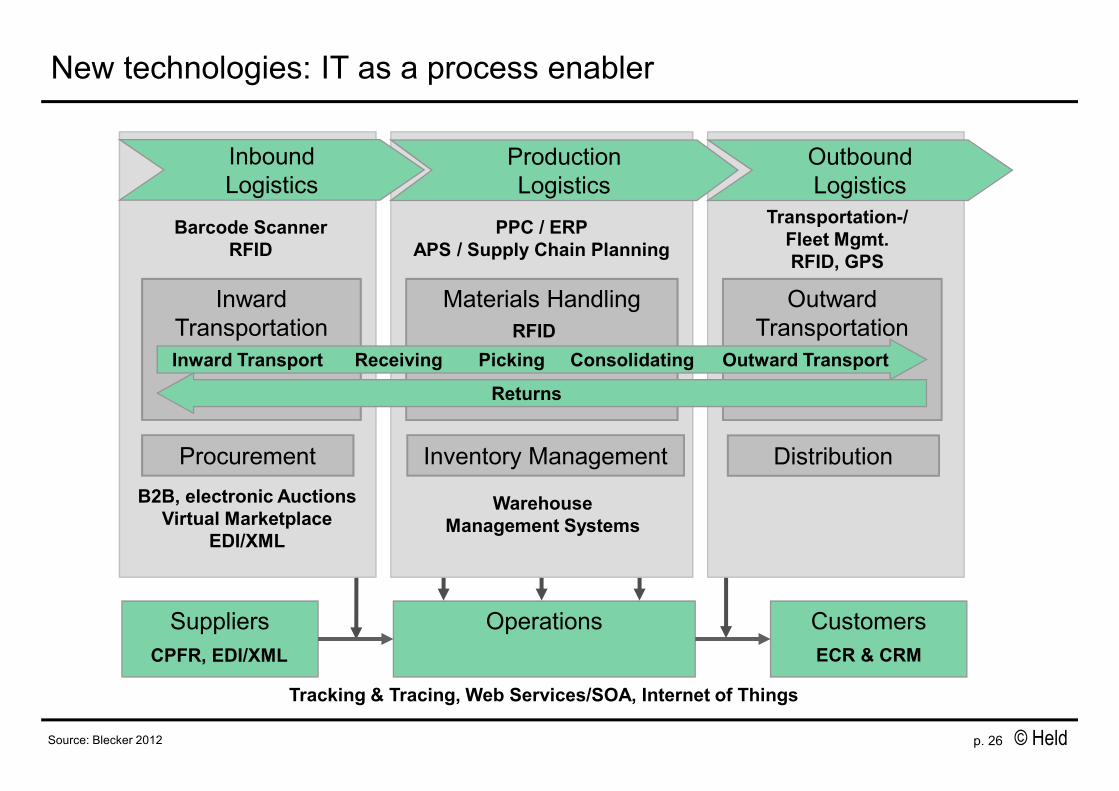

New technologies: IT as a process enabler

Suppliers Operations Customers

OutwardTransportation

Materials HandlingInwardTransportation

Production Logistics

Outbound Logistics

Procurement Inventory Management

Inward Transport Receiving Picking Consolidating Outward Transport

Returns

ECR & CRMCPFR, EDI/XML

RFID

Warehouse

Management Systems

Transportation-/

Fleet Mgmt.

RFID, GPS

PPC / ERP

APS / Supply Chain Planning

B2B, electronic Auctions

Virtual Marketplace

EDI/XML

Barcode Scanner

RFID

Inbound Logistics

Tracking & Tracing, Web Services/SOA, Internet of Things

Distribution

Source: Blecker 2012

© Heldp. 27

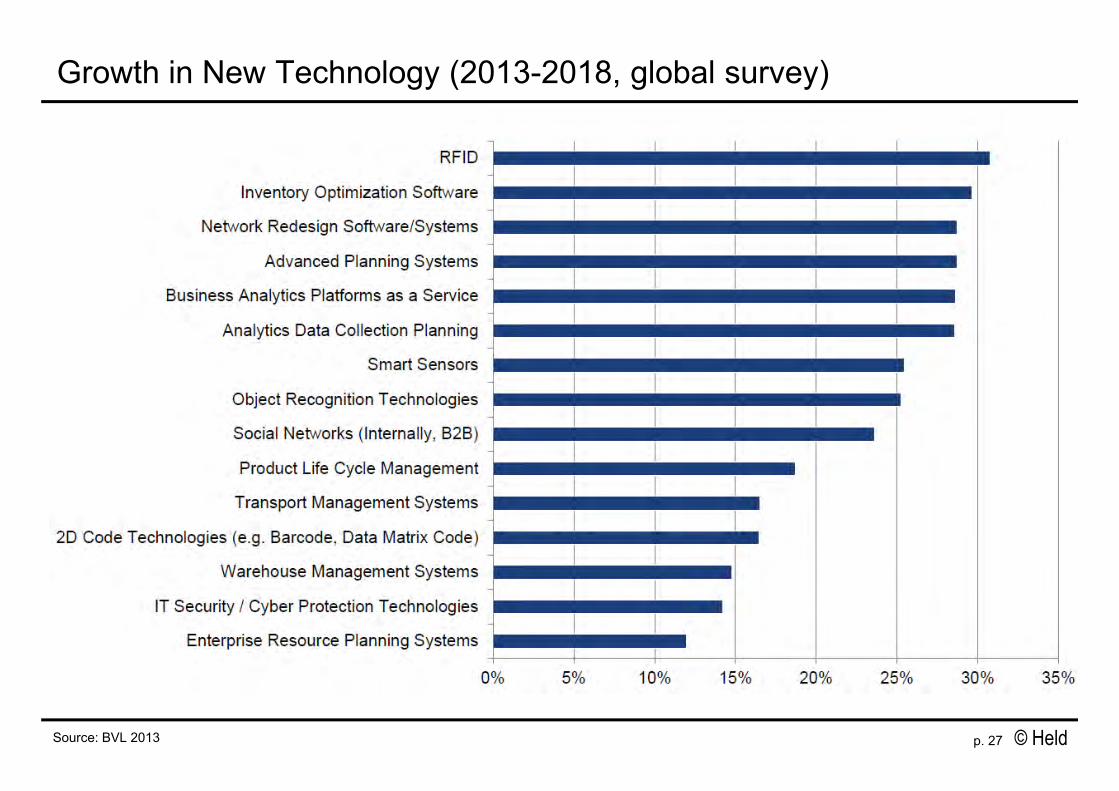

Growth in New Technology (2013-2018, global survey)

Source: BVL 2013

© Heldp. 28

Course Structure

1. A Short Overview Logistics in Europe and Germany

2. Challenges and Trends Impacting Logics

3. Some Current Innovations and Changes in German Logistics

© Heldp. 29

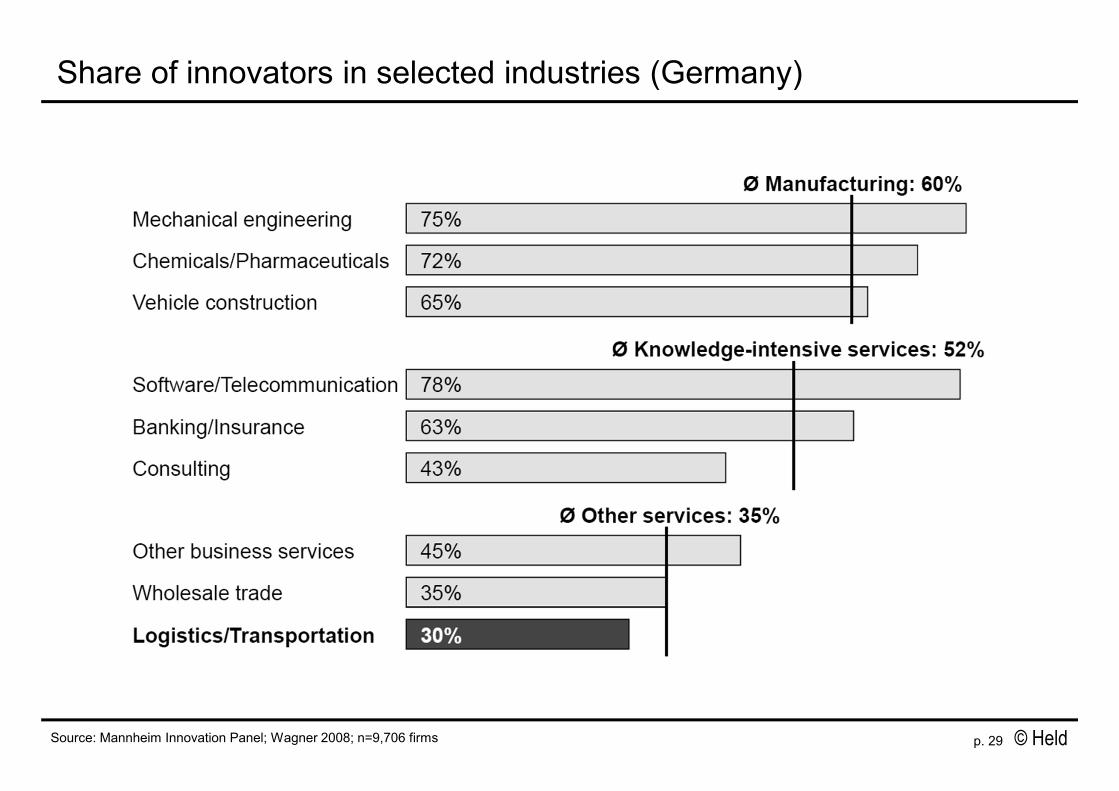

Share of innovators in selected industries (Germany)

Source: Mannheim Innovation Panel; Wagner 2008; n=9,706 firms

© Heldp. 30

Current (technical) logistics research in Germany – two Examples

“Pick by Vision – Augmented Reality“ Data glasses with integrated cameraproviding context specific information

(e.g. which item is in which rack)

“Optimization of pallet checking by mobil devices“

Real time analyzation of pallet qualityusing standard mobil phones

Source: BVL 2013; Fraunhofer 2013

© Heldp. 31

The "Packstation" as new first/last mile product

Source: Deutsche Post 2012; Wagner 2012

© Heldp. 32

Market entrance of long-distance traffic bus companies 2013 (examples)

Source: Wirtschaftswoche 2013

© Heldp. 33Source: Picture: Pascal Crapet; Porter 2013

Many thanks for your attention!

“Co-ordination of complex global networks of company activities is becoming a prime source of competitive advantage. Today’s game of global strategy seems to be

increasingly a game of co-ordination - getting dispersed production facilities, R&D laboratories and market facilities really to work together.”

Michael Porter (Harvard Business School)