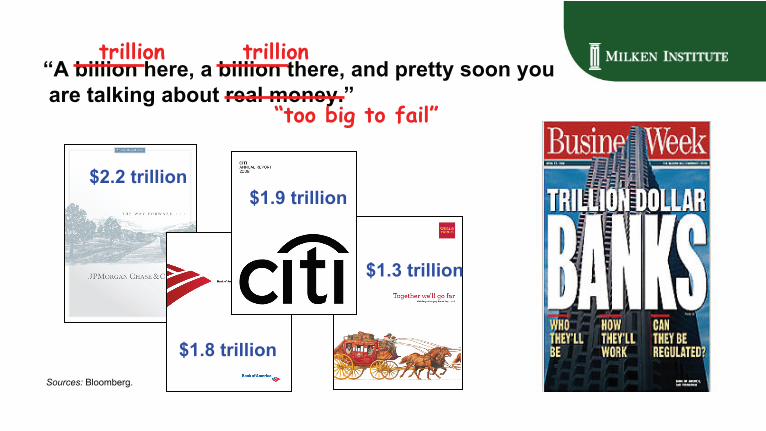

trillion “a billion here, a billion there, and pretty soon...

TRANSCRIPT

“A billion here, a billion there, and pretty soon you

are talking about real money.”

Sources: Bloomberg.

trillion

trillion

“too big to fail”

$2.2 trillion

$1.8 trillion

$1.9 trillion

$1.3 trillion

Subprime write-downs

Source:

Bloomberg.

US$ billions, as of April 10, 2009 Loss CapitalWachovia, United States 101.9 11Citigroup, United States 88.3 109.3AIG, United States 87.3 91.7Freddie Mac, United States 81.6 51.6Fannie Mae, United States 71.3 30.8Merrill Lynch, United States 55.9 29.9UBS, Switzerland 50.6 32.1Washington Mutual, United States 45.3 12.1Bank of America, United States 42.7 78.5HSBC, United Kingdom 42.2 23.7Others 621 633.2Grand total 1,288.1 1,103.9

Number of unprofitable financial institutions

on the rise

Annual, 1982-2008

0

5

10

15

20

25

30

35

1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Percent

Commercial banks: 21.9% in 2008

Savings institutions: 32.1% in 2008

Sources: Moody’s Economy.com, FDIC, Milken Institute.

The rise and fall of private-label securitizers

Sources:

Federal Reserve, Milken Institute.

Private-label

1985

total = $110 B2001

total = $1.3 T2006

total = $2.0 T2008

total = $1.2 T

New securities issuance

Fannie Mae, Freddie Mac, Ginnie Mae

2%

98%

20%

80%

56%

44%

4%

96%

Rising risk: The credit default swap market nearly doubled each year from June 2001

through October 2008

0.6 0.9 1.6 2.2 2.7 3.8 5.4 8.412.4

17.126.0

34.4

45.5

62.254.6

47.0

0

10

20

30

40

50

60

70

June2001

Dec.2001

June2002

Dec.2002

June2003

Dec.2003

June2004

Dec.2004

June2005

Dec.2005

June2006

Dec.2006

June2007

Dec.2007

June2008

Oct.2008

Notional amount of credit default swaps outstanding, US$ trillions

Source: International Swaps and Derivatives Association.

AIG received AA rating despite large

exposure in credit default swaps

$1,058 $1,167$883

$218$224

$194

$180$179

$132

$484$562

$306

0

500

1,000

1,500

2,000

2,500

2006 2007 2008

Credit default swaps

Swaptions, equityand commodityswapsCurrency swaps

Interest rate swaps

US$ billionsIssuer rating for AIG,

2005-2008

S&P AA

Moody’s Aa2

Fitch AA

Sources: AIG, Bloomberg.

Note: Credit default swaps exposure not released in 10K before 2006.

Market for liquidity freezes Spread between 1-month LIBOR and OIS

Note: LIBOR:

London Interbank

Offered Rate; OIS: Overnight indexed swap.Sources: Bloomberg, Milken Institute.

0

100

200

300

400

January-07 July-07 January-08 July-08 January-09

1-month LIBOR-OIS spread, basis points

Bear Stearns IndyMac

FannieMae/Freddie Mac

Lehman Brothers

Wachovia

Washington Mutual AIG

CPP + TLGPEESA passed

Beginning of credit crisis

EESA: Emergency Economic Stabilization Act.

CPP: Capital Purchase Program

TLGP: Temporary Liquidity Guarantee Program

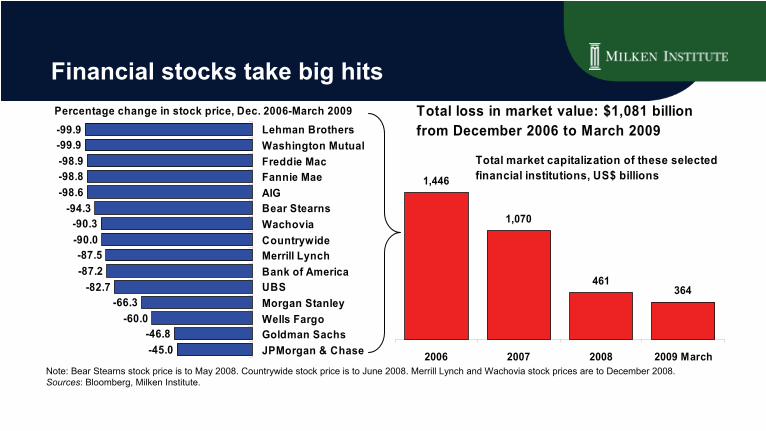

Financial stocks take big hits

Note: Bear Stearns stock price is to May 2008. Countrywide stock

price is to June 2008. Merrill Lynch and Wachovia stock prices are to December 2008.Sources: Bloomberg, Milken Institute.

-99.9-99.9-98.9-98.8-98.6

-94.3-90.3-90.0-87.5-87.2

-82.7-66.3

-60.0-46.8-45.0

Lehman BrothersWashington MutualFreddie MacFannie MaeAIGBear StearnsWachoviaCountrywideMerrill LynchBank of AmericaUBSMorgan StanleyWells FargoGoldman SachsJPMorgan & Chase

Percentage change in stock price, Dec. 2006-March 2009

1,446

1,070

461364

2006 2007 2008 2009 March

Total loss in market value: $1,081 billion from December 2006 to March 2009

Total market capitalization of these selectedfinancial institutions, US$ billions

Estimated U.S. total bailout costs (US$ billions)

The government has extended the bailouts to nearly $US10 trillion

Source:

The Milken Institute.

Federal Reserve, Treasury, FDIC:

$362

FDIC: $926

Treasury: $2,466Federal Reserve:

$6,139

Estimated U.S. total bailout costs as of March 2009 (including guarantees and all commitments):

US$9.9 trillion

TARP: Troubled Asset Relief Program

Status of TARP

funds (US$ billions) as of March 27, 2009

Source: Wall Street Journal. US$ billions

40

24.5

238.9

0 100 200 300 400 500 600

Already disbursed

Maximum announced funding level

15

Banking system

AIG

Auto companies and suppliers

Small business

Life insurers (estimated)

522.5

70

29.9

25

U.S. Treasury Department TARP funds

As of April 15, 2009

Company US$ billionsCitigroup 50.0Bank of America/Merrill Lynch 45.0JPMorgan Chase 25.0Wells Fargo 27.9Goldman Sachs 10.0Morgan Stanley 10.0PNC Financial Services 7.6U.S. Bancorp 6.6Other 161.0Total 343.1

Source: U.S. Treasury Department.

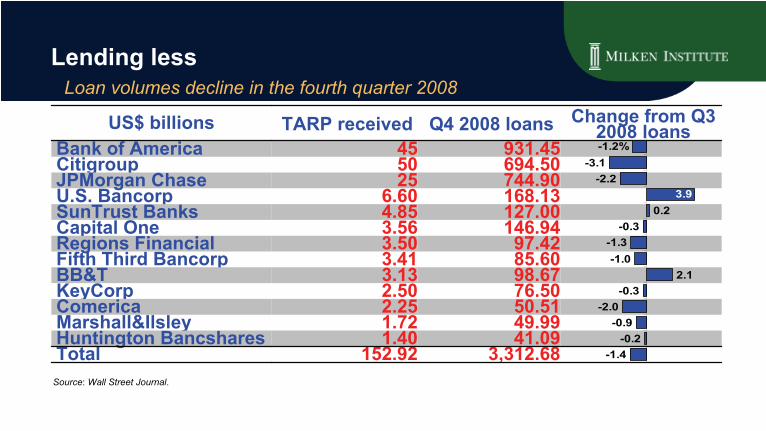

Lending less

Loan volumes decline in the fourth quarter 2008

US$ billions TARP received Q4 2008 loans Change from Q3 2008 loans

Bank of America 45 931.45Citigroup 50 694.50JPMorgan Chase 25 744.90U.S. Bancorp 6.60 168.13SunTrust Banks 4.85 127.00Capital One 3.56 146.94Regions Financial 3.50 97.42Fifth Third Bancorp 3.41 85.60BB&T 3.13 98.67KeyCorp 2.50 76.50Comerica 2.25 50.51Marshall&Ilsley 1.72 49.99Huntington Bancshares 1.40 41.09Total 152.92 3,312.68

Source: Wall Street Journal.

-3.1-2.2

0.2-0.3

-1.3-1.0

2.1-0.3

-2.0-0.9

-0.2-1.4

3.9

-1.2%

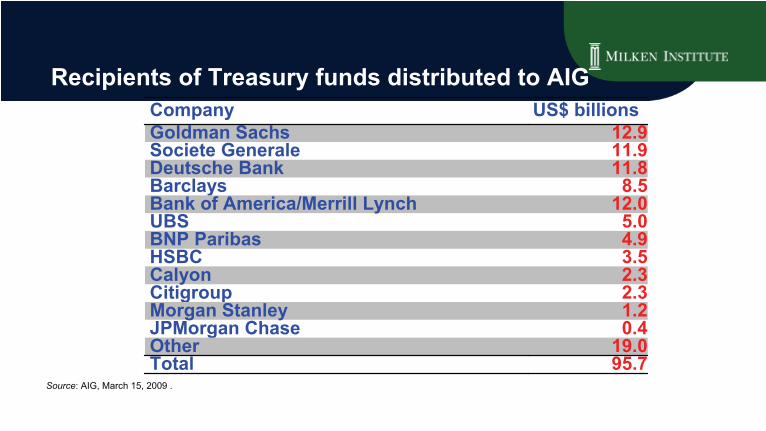

Recipients of Treasury funds distributed to AIGCompany US$ billionsGoldman Sachs 12.9Societe

Generale 11.9Deutsche Bank 11.8Barclays 8.5Bank of America/Merrill Lynch 12.0UBS 5.0BNP Paribas 4.9HSBC 3.5Calyon 2.3Citigroup 2.3Morgan Stanley 1.2JPMorgan Chase 0.4Other 19.0Total 95.7

Source: AIG, March 15, 2009 .

GM and Chrysler to receive TARP funds

Source: http://www.detnews.com

•

The Treasury has injected about $25 billion --

or 3.5 percent --

of the TARP funds, including $1.5 billion to Chrysler Financial, $6 billion to support GMAC.

•

TARP will support up to $1.25 billion on an auto industry warranty program. That would back Chrysler or GM vehicle warranties in the event either company filed for bankruptcy protection.

• A separate $5 billion auto supplier program has also been created.

•

On March 30, the Obama administration gave General Motors Corp.

60 days to come up with a tougher restructuring plan.

U.S. capital injections and write-downs

Will the massive write-downs continue?

Source:

Bloomberg.

0

50

100

150

200

250

300

Priorquarters

Q3 2007 Q4 2007 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009

Losses and write-downs: Total US$ 869.7 billionCapital injections: Total US$ 646 billion

US$ billions, most recently available data, as of March 2009

U.S. financial institutions

Total assets of selected failed or acquired financial institutions

Total assets= $3.0 trillion

Sources: Bloomberg, Milken Institute.

172

310

399

639

668

764

Countrywide,6/30/2008

Washington Mutual,6/30/2008

Bear Stearns,3/31/2008

Lehman Brothers,6/30/2008

Merrill Lynch,12/31/2008

Wachovia,9/30/2008

US$ billions

Purchased by Wells Fargo

Acquired by Bank of America

Filed for bankruptcy

Sold to JPMorgan Chase

Purchased by Bank of America

Sold to JPMorgan Chase

Public-Private Investment Program

US$ 75-100 billion of TARP/FSP capital

Legacy Securities Program

Capital Public-Private

Investment Funds

• Combines private capital with USG capital and potential USG leverage

FinancingLeverage from

Federal Reserve

• Builds on existing TALF framework

Source: U.S. Treasury.

Legacy Loans Program

Capital Public-Private

Investment Funds

• Combines USG and private capital

FinancingFunds will raise FDIC

guaranteed debt

• FDIC will guarantee debt

• Leverage up to 6.1

A question of equity: Stress tests?

U.S. regulatory capital requirements and selected equity ratios

Sources: FDIC, Bloomberg, Milken Institute.

Tier 1leverage

Tier 1 risk-

based

Total risk-

based

Well capitalized >= 5% >= 6% >= 10%

Adequately capitalized >= 4% >= 4% >= 8%

Undercapitalized < 4% < 4% < 8%

Significantly undercapitalized < 3% < 3% < 6%

Critically undercapitalized

Tangible equity capital ratio that is <= 2%

0 5 10 15 20

Citigroup

Wells Fargo

Bank NY Mellon

PNC Financial Services

US Bancorp

Bank of America

JPMorgan Chase

Morgan Stanley

Goldman Sachs

SunTrust Banks

Tier 1 capital ratioTangible common equity ratio

American Recovery and Reinvestment Act of 2009 The US$787 billion stimulus plan is intended to create 3-4 million jobs

Source:

Recovery.gov.

$8 billion

$43 billion

$53 billion

$59 billion

$81 billion

$111 billion

$288 billion

$144 billion

Other

Energy

Education and training

Health care

Protecting the vulnerable

Infrastructure and science

State and local fiscal relief

Tax relief

Administration estimated aggregate effect of the recovery package on GDP and jobs in Q4 2010

Real GDP(US$ billions) Payroll employment

Without Stimulus $11,770 133,876,000

With Stimulus $12,203 137,550,000

Effect of Package Increase GDP by 3.7% Increase jobs by 3,675,000

Source:

Christina Romer

and Jared Bernstein, “The Job Impact of the American Recovery and Reinvestment Plan."

Infrastructure outlays from the American Recovery and Reinvestment Act

U.S.$ billions

Transportation

Energy programs

Broadband,

telemedicine, and distance

learning

Housing

Federal buildings

Clean and drinking water

Source:

Congressional Budget Office.